Revenue Doubles and Market Value Soars: Analyzing the Pandemic-Driven Growth Trajectory of China's IVD Companies

In August, domestic listed companies centrally submitted their interim operating results. The COVID-19 outbreak, which began at the start of the year, rapidly swept across China and subsequently impacted the entire globe. For operators in any industry, the first half of 2020 was undoubtedly exceptional.

The in vitro diagnostics (IVD) industry gained significant prominence during the fight against the pandemic, with the concept of nucleic acid testing rapidly penetrating investor consciousness by leveraging the COVID-19 outbreak. The changes that the pandemic itself brought to this industry have been quite dramatic:

Despite the delayed release of its semi-annual report, Daan Gene shared quite encouraging performance information. This company, which has been listed for 16 years, just recorded its fastest six-month growth in performance, earning in half a year the total profits of the past seven years, finally reversing its long-standing sluggish profitability.

“Model Student” BGI Genomics Delivers Impressive Pandemic Response: It rapidly developed multiple test kits, securing market access in numerous countries, and swiftly boosted testing capacity through its “Fire Eye Laboratory” total solution. In the first half of the year, it achieved a twofold increase in revenue and a sevenfold rise in net profit. Wantai Bioengineering, a “star stock” that nearly reached a RMB 100 billion market capitalization, has sustained momentum with its domestically produced bivalent HPV vaccine. Its semi-annual report disclosed nearly RMB 200 million in revenue from COVID-19 testing products and an almost doubled net profit, serving as a response to widespread skepticism about its fundamentals.

Certainly, some companies that do not specialize in molecular diagnostic technologies have left regrets in their annual reports due to untimely responses or insufficient consideration of the pandemic's impact: Autobio Diagnostics was severely affected in the first quarter by the decline in routine medical services at healthcare institutions, resulting in negative net profit growth and a drop in overall gross margin. Maccura Biotechnology experienced similar challenges. However, Maccura responded quickly in the second quarter by developing nucleic acid and antibody test kits for COVID-19, adopting a low-price strategy to enter centralized procurement programs in multiple provinces, striving to make up for lost time and performance.

In this article, we conduct a concentrated analysis of the semi-annual reports of IVD companies, covering 11 active enterprises that have participated in provincial-level centralized procurement for COVID-19 vaccines. While examining the short-term impact of the sudden COVID-19 pandemic on these companies’ performance, we attempt to identify potential strategic shifts among innovative IVD enterprises committed to domestic substitution in the post-pandemic era.

Crises are always temporary; the impetus for change amidst a crisis may well be the true significance of experiencing it.

In late January, a green channel for approval was established; in early February, the first batch of products received registration certificates; and by mid-May, inter-provincial centralized procurement commenced. The rapid product development journey of COVID-19 diagnostic reagents, from an unknown virus to routine rapid testing, indirectly demonstrates that China’s IVD industry has acquired substantial responsiveness and flexible production capacity. Our analysis begins here.

If the COVID-19 pandemic has brought any systemic changes to China’s healthcare supply side, strengthening the public health prevention and control system is undoubtedly one of them. In late May, the National Development and Reform Commission (NDRC), jointly with the National Health Commission (NHC) and the National Administration of Traditional Chinese Medicine, issued the “Notice on Printing and Distributing the Plan for Enhancing Public Health Prevention, Control, and Treatment Capabilities.” The notice explicitly requires each province to prioritize improving the infrastructure conditions of one county-level hospital (including county-level hospitals of traditional Chinese medicine). It mandates the upgrading and replacement of medical equipment in key departments such as fever clinics, emergency departments, inpatient wards, and medical technology departments. Furthermore, it emphasizes enhancing the configuration of inspection and testing instruments and equipment in infectious disease departments and relatively independent infectious disease wards at county-level hospitals, thereby improving capabilities for rapid detection, diagnosis, and treatment.

By the end of August, centralized procurement bidding for COVID-19-related diagnostic products had been completed in 27 provinces and municipalities across China. Following the initiation of centralized procurement, prices for nucleic acid testing and antibody testing reagents dropped sharply to 10%–20% of their original levels, yet suppliers’ enthusiasm for participation increased. After all, for IVD manufacturers involved in the pandemic response, the competitive arena has shifted from market access to channel deployment.

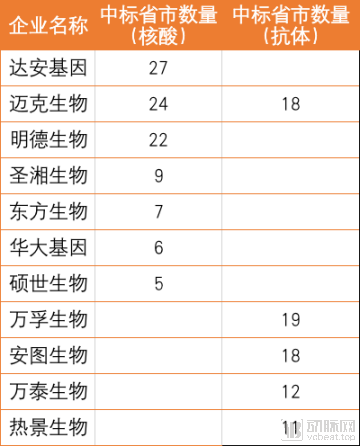

Overview of Companies Winning Bids in the Centralized Procurement of COVID-19 Testing Products

According to statistics from VCBeat, by the end of August, Da An Gene had become a supplier for centralized procurement of COVID-19-related reagents in 27 provinces and municipalities across China, ranking first in terms of the number of regions covered. Maccura Biotechnology was shortlisted in 24 provinces and municipalities, placing second. Notably, Maccura’s COVID-19 antibody detection reagents were also included in the centralized procurement lists of 17 provinces and municipalities, making it the only company among all successful bidders to win bids for both nucleic acid and antibody test kits.

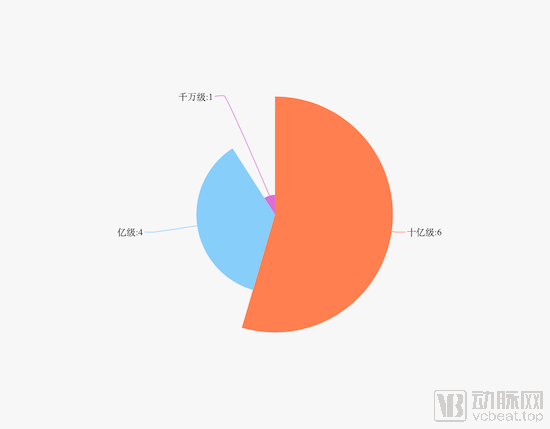

From the consolidated financial report data, we can see that six IVD companies achieved operating revenues exceeding RMB 1 billion in the first half of the year, accounting for more than 55% of the total. Among them, BGI Genomics led the industry by a wide margin, with an operating revenue of RMB 4.108 billion and a net profit of RMB 1.651 billion. Daan Gene, ranking second in operating revenue, and Sansure Biotech, ranking third, had relatively similar revenue levels; however, the latter’s net profit significantly surpassed that of Daan Gene.

Moving down the first-half revenue ranking, Wondfo Biotech, Maccura Biotechnology, Autobio Diagnostics, Wantai BioPharm, and Orient Gene, with revenues in the RMB 1–2 billion range, each reported net profits of approximately RMB 500 million, intuitively forming the third tier of this list. Further segmentation places Shuoshi Biotech, Mingde Biotech, and Hotgen Biotech, with revenues below RMB 1 billion, in the fourth tier.

Overall, the surge in first-half performance was concentrated among companies in the first and second tiers, while weak performance, or even declines, was primarily observed among those in the third and fourth tiers. Of course, there are exceptions to this classification. For instance, Orient Gene and Bioperfectus Technologies, both ranked in the third tier, recorded net profits more than 14 times and 9 times higher, respectively, than those of the same period last year. This performance was closely linked to the sales of COVID-19 testing reagents, a topic we will analyze in detail in the next section.

Brief Summary of Financial Data for 11 IVD Companies in the First Half of 2020

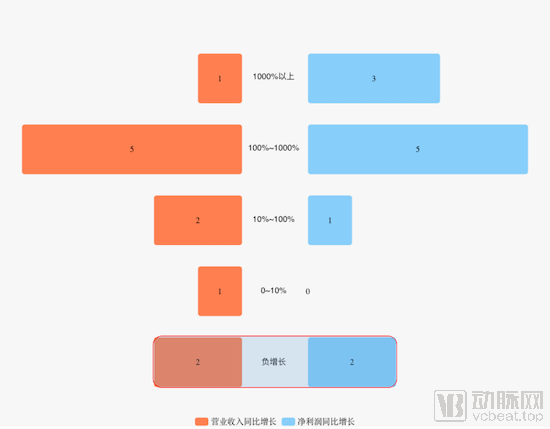

A further analysis of the performance growth data reveals that, for the 11 IVD companies on the list, achieving revenue and net profits several times higher than those in the same period last year has become almost the norm: six companies saw their operating revenues increase by more than 100% year-on-year, with one company recording an operating revenue in the first half of this year that was more than 10 times that of the same period last year; eight companies experienced a year-on-year increase in net profit of over 100%, among which three companies achieved net profits more than 10 times those of the same period last year.

Distribution of Revenue Scale Among 11 IVD Companies in the First Half of 2020

The performance growth revealed in the first half of the year was highlighted by two particularly striking figures: a year-on-year increase of 1,159.39% in operating revenue and a year-on-year surge of 14,700% in net profit, which propelled Sansure Biotech, recently listed, into the spotlight. This Hunan-based company, specializing in viral hepatitis testing, achieved operating revenue 11 times higher and net profit 147 times greater than the same period last year during the turbulent first half of 2020. In addition, BGI Genomics, Da An Gene, Oriental Bio, Shuoshi Biotechnology, and Mingde Biotechnology all doubled their performance. Notably, Da An Gene and Mingde Biotechnology even staged a remarkable turnaround in their financial results driven by the COVID-19 pandemic. We will provide a detailed analysis later in this article.

Distribution of Performance Changes Among 11 IVD Companies in the First Half of 2020

Of course, impressive financial performance is not necessarily the norm for listed in vitro diagnostic (IVD) companies in the first half of the year. Autobio Diagnostics and Maccura Biotechnology, which primarily focus on the production and sales of biochemical and chemiluminescence immunoassay reagents, both suffered setbacks during the COVID-19 pandemic, experiencing negative growth in either revenue or net profit. Hotgen Biotech, which was hit the hardest, had just listed on the STAR Market not long before; with its total net profit originally not being high, it saw a decline of over 80% during the pandemic, with both revenue and net profit registering negative growth.

In fact, as early as late February, shortly after the outbreak of the COVID-19 pandemic, industry experts reached a certain consensus on how the epidemic would impact the healthcare industry: the spread of the virus would exert phased effects on the sector, with different subfields experiencing varying degrees of detriment or benefit at different stages. With the fiscal year half over, these differentiated impacts have gradually been quantified. Through the semi-annual financial reports of the aforementioned companies, we can identify certain characteristics of the pandemic’s impact on the in vitro diagnostics (IVD) industry during the first half of the year.

In Vitro Diagnosis (IVD) refers to products and services that obtain clinical diagnostic information by testing human samples such as blood, body fluids, and tissues outside the human body, thereby assessing diseases or physiological functions. IVD products mainly consist of diagnostic instruments and reagents. Common IVD methods include immunoassay, clinical chemistry, and molecular diagnostics. Regardless of the method used, the technical barriers for IVD reagents are not particularly high.

Thus, in the battle for supply of novel coronavirus (SARS-CoV-2) diagnostic reagents during the first half of the year, early entrants emerged largely as winners. Companies such as Daan Gene, BGI Genomics, Sansure Biotech, Orient Gene, and Shuoshi Biotechnology all initiated reagent development immediately upon the outbreak of the COVID-19 pandemic and, as the epidemic spread, were the first to secure various market access approvals.

First, let us analyze Oriental Biotech and Shuoshi Bio. In the first half of the year, Oriental Biotech achieved operating revenue of RMB 828 million, a year-on-year increase of 388.05%. The net profit attributable to shareholders of the listed company was RMB 524 million, up 1,477.45% year on year. The net profit after deducting non-recurring gains and losses was RMB 517 million, representing a year-on-year increase of 1,647.20%. The net cash flow from operating activities amounted to RMB 367 million, surging by 12,509.96% year on year. Shuoshi Bio recorded operating revenue of RMB 573 million, a year-on-year increase of 368.65%, with net profit attributable to shareholders of the listed company reaching RMB 308 million, up 923.30% year on year.

At the outset of the COVID-19 pandemic, both Oriental Biotech and Shuoshi Biotechnology promptly joined the effort to develop nucleic acid testing kits. Oriental Biotech developed three types of SARS-CoV-2 diagnostic reagents, including antibody detection kits, nucleic acid detection kits, and rapid antigen test strips. These products successively obtained EU CE certification, China’s medical device registration certificates, and Emergency Use Authorization (EUA) from the U.S. FDA. These offerings drove a significant surge in Oriental Biotech’s operating performance over the past six months. Meanwhile, Shuoshi Biotechnology explicitly stated in its semi-annual report that “the substantial increase in revenue during the first half of the year was primarily attributable to the outbreak of the COVID-19 pandemic in the first half of 2020, which led to heightened market demand for COVID-19 testing products and a corresponding rise in the company’s sales volume.”

Let’s turn to Sansure Biotech, known as the “first stock of the anti-epidemic campaign.” On January 28, Sansure Biotech’s novel coronavirus nucleic acid test kit was approved for market launch, making it one of the first six companies to receive such approval. As of June 30, 2020, Sansure Biotech had supplied nearly 38.8513 million tests of its novel coronavirus nucleic acid test kit both domestically and internationally, with more than one-third distributed to overseas markets.

It is reported that Sansure Biotech has established a robust production and sales service network, on the basis of which its products were rapidly deployed to the front lines of epidemic prevention and control in more than 30 provinces, municipalities, and autonomous regions, including Hubei, Hunan, Beijing, and Shanghai. As the pandemic spread globally, Sansure Biotech’s COVID-19 diagnostic kits successively obtained emergency use authorization from the U.S. FDA, CE certification from the European Union, ANVISA certification from Brazil, and over 20 other authoritative international registrations and certifications. In the first half of the year, Sansure Biotech achieved operating revenue of RMB 2.1 billion and net profit of RMB 1.232 billion, representing year-on-year increases of 1,159.39% and 14,687.20%, respectively.

Next are Da An Gene and BGI Genomics.

Da An Gene achieved operating revenue of RMB 2.13 billion and net profit of RMB 778 million, representing year-on-year increases of 313.63% and 1,186.48%, respectively. The company incurred selling expenses of RMB 272 million and maintained a gross profit margin of 67.41%. This marks the most rapid six-month performance growth in its 16 years since going public. Meanwhile, Da An Gene’s stock price has risen by 270% this year, hitting the daily upper limit 14 times year-to-date, and reaching its yearly peak of RMB 45.35 per share on August 4, corresponding to a total market capitalization of RMB 39.779 billion.

BGI Genomics reported operating revenue of RMB 4.108 billion, a year-on-year increase of 218.08%. In the first half of the year (H1), BGI Genomics generated RMB 2.992 billion in revenue from its precision medicine testing business—which includes providing COVID-19 test kits, instruments, and comprehensive sequencing laboratory solutions—representing a more than 12-fold year-on-year growth and contributing 72.83% to total revenue. Additionally, revenue from its infection prevention and control business, related to the research and development of nucleic acid test kits and antibody test kits, reached RMB 184 million, up 429.94% year on year.

According to reports, Daan Gene was one of the first seven companies to enter the National Medical Products Administration’s (NMPA) fast-track approval channel. Its developed novel coronavirus diagnostic reagent received market authorization on January 28, obtained EU CE certification on February 5, and was included in the World Health Organization’s (WHO) Emergency Use Listing on May 14. BGI Genomics has successively completed the research and development of multiple novel coronavirus diagnostic kits, with technologies covering fluorescent PCR, combined probe anchor polymerization sequencing, enzyme-linked immunosorbent assay (ELISA), and colloidal gold methods.

Meanwhile, Da An Gene ramped up production to full capacity, increasing its daily kit output from a standard 50,000 tests to a peak of over 1 million tests per day, with COVID-19 testing-related products shipped to more than 140 countries and regions worldwide. On the other front, BGI Genomics’ COVID-19 nucleic acid test kits (fluorescent PCR method) have gained market access in multiple countries and been included on the WHO Emergency Use Listing. By the end of the reporting period, cumulative overseas shipments had exceeded 35 million tests.

Furthermore, with the research, development, and production of COVID-19 testing kits in place, the demand for biosafety laboratories has grown significantly. BGI Genomics launched the "Fire Eye" Laboratory Integrated Comprehensive Solution, which includes testing instruments and equipment, testing kits, and laboratory design, to rapidly enhance testing capacity. BGI Genomics participated in the design of a new inflatable membrane version of the "Fire Eye" Laboratory that complies with P2 biosafety laboratory standards. Adopting a sealed inflatable membrane architectural model, it offers the advantages of rapid construction and quick deployment.

Although most in vitro diagnostics (IVD) companies responded promptly, the development, production, and sales of COVID-19 testing products required coordination of various internal and external resources. Consequently, the time required for each company to establish a closed-loop system encompassing production, supply, and marketing inevitably varied. As a result, some companies captured the initial wave of the pandemic, as discussed in the previous section, while others emerged as key players in the secondary market phase, such as Wantai Biological, Mingde Biology, and Wondfo Biotech. A notable feature of these companies’ operations in the first half of the year was that, in addition to meeting domestic demand for COVID-19 testing, they leveraged the spread of the epidemic overseas as a significant growth driver.

According to reports, Wantai Bio has successively launched three different types of diagnostic reagents: colloidal gold, chemiluminescence, and nucleic acid tests. It also developed the world’s first approved sandwich-method COVID-19 antibody test kit. Among its products, five COVID-19 testing kits have obtained EU CE certification, one has received Emergency Use Authorization (EUA) from the U.S. FDA, and one has been certified by Australia’s TGA. In the first half of the year, the company’s COVID-19 testing products generated additional operating revenue of RMB 186 million.

In terms of operating data, Wantai Bio achieved an operating revenue of RMB 724 million in the first half of the year, accounting for 85.76% of the company's total revenue. Among this, reagent products generated an operating revenue of RMB 547 million, representing 64.89% of the company's total revenue.

After obtaining the registration certificate for its COVID-19 test kits in China, Mingde Biology’s products were selected in centralized procurement programs for COVID-19 testing reagents across multiple provinces and municipalities nationwide. The company subsequently secured CE marking in the European Union, TGA certification in Australia, and ANVISA approval in Brazil, with its related products exported to more than 50 countries worldwide.

Mingde Biology achieved operating revenue of RMB 361 million and net profit of RMB 200 million, representing year-on-year increases of 253.98% and 397.19%, respectively. A comparison reveals that the net profit realized by Mingde Biology in the first half of the year was nearly five times that of the entire previous year. Notably, the company’s overseas revenue surged more than a hundredfold over the past six months. The semi-annual report shows that revenue from overseas regions amounted to RMB 65.6169 million, accounting for 18.20% of its main business revenue.

As a result, the first six months of 2020 became the most remarkable period in Mingde Biology’s operational history, with the direct effect being greater recognition from the capital market: as of August 24 this year, Mingde Biology’s share price stood at RMB 84 per share, representing a 132.11% increase from RMB 36.19 per share at the beginning of the year.

Wondfo Biotech developed and launched six COVID-19 testing products, generating RMB 841 million in sales revenue and becoming the primary driver of overall revenue growth. Despite a significant decline in outpatient visits at medical institutions during the pandemic, the company’s infectious disease testing business line saw a year-on-year revenue decrease of 22.60% after excluding COVID-19 test kits. Due to the same factors, revenues from chronic disease management testing and eugenics and healthy birth testing fell by 30.50% and 15.21%, respectively. Interestingly, the COVID-19 pandemic created another performance growth point for Wondfo Biotech: its drug testing business in the United States experienced a 53.39% year-on-year increase in sales, driven by heightened demand for drug testing products amid the severe pandemic situation and rising unemployment rates in the country.

In the first half of the year, Maccura Biotechnology, Autobio Diagnostics, and Hotgen Biotech reported unsatisfactory operating performance. When analyzing the reasons, all three companies emphasized the impact of the COVID-19 pandemic. Autobio Diagnostics pointed out that the decline in patient volume for routine diagnosis and treatment at medical institutions led to reduced demand for its core businesses, including chemiluminescence immunoassays and clinical chemistry. Hotgen Biotech stated that although it promptly developed multiple novel coronavirus testing products, it failed to obtain medical device registration certificates in a timely manner due to an underestimation of the severity and progression of the pandemic. As a result, sales of its novel coronavirus testing products were insufficient to offset the decline in sales of its conventional products.

In fact, rather than summarizing successful experiences, we believe that reflection on setbacks is perhaps even more critical. Some long-term plans for industry development are emerging from this very gap. The crises or opportunities brought about by the COVID-19 pandemic will soon pass. In the post-pandemic era, IVD companies must return to their own growth trajectories. During the pandemic, healthcare institutions and public health prevention and control agencies exposed weaknesses in their capacity for precise disease detection to some extent, which may become the entry point for IVD companies to establish incremental competitive advantages.

We have found that most IVD companies have already launched differentiated strategies centered on the aforementioned three points, leveraging their accumulated business capabilities.

For instance, Autobio Diagnostics noted that although reagent sales generally declined, there was a significant increase in instrument and equipment sales, laying the foundation for future volume growth in reagents. Specifically, over 700 new magnetic particle chemiluminescence analyzers were installed, bringing the total installed base to nearly 5,000 units. More than 50 mass spectrometry analyzers were installed in the first half of the year, which is expected to drive subsequent sales of other microbial testing consumables. Furthermore, Autobio Diagnostics stated that it will continue to strengthen R&D investment and refine its comprehensive product portfolio. Horizontally, it aims to expand into product lines such as microbiology and molecular diagnostics; vertically, it is actively developing key raw materials to enhance supply security and stability, thereby building full-spectrum supply capabilities across the IVD (In Vitro Diagnostics) product range.

BGI Genomics is committed to refining its product portfolio across the “Reproduction, Oncology, and Infection” sectors. On one hand, it aims to expand its advantages in birth defect prevention and control while enhancing its oncology prevention and control service system. On the other hand, it seeks to introduce superior resources to drive leapfrog development in its infection prevention and control business. Meanwhile, BGI Genomics is also working to extend the application of domestically produced sequencing platforms across its entire product line.

Maccura Biotechnology leverages its self-developed chemiluminescence immunoassay (CLIA) products as the core driver of its performance, capturing incremental growth in primary care hospitals while replacing existing imported products in high-end hospitals, thereby achieving domestic substitution for CLIA products. Currently, Maccura’s three major product segments—immunodiagnostics, clinical chemistry, and routine laboratory testing—work synergistically to meet over 90% of the testing needs of medical laboratories. The company aims to deepen its presence in multiple niche sectors to build a one-stop IVD service platform. As a more profound impact of the COVID-19 pandemic, Maccura believes that its market channel capabilities have been strengthened, with an increasingly robust distribution network radiating from Southwest China to the rest of the country and gradually expanding globally.

Wondfo Biotech has consistently adhered to a dual-track R&D strategy that combines the expansion of its existing product portfolio with the development and upgrading of new technology platforms. Over the years, this approach has enabled the company to build robust technology platforms and a diverse product lineup. By maintaining high levels of R&D investment and continuously launching new products, Wondfo Biotech has solidified its position as a leader in the POCT industry. The company anticipates that, as a POCT industry leader, it will benefit from strong sales of COVID-19 testing products in the short to medium term, while long-term growth is expected to be driven by new product innovations.

While consolidating its market advantage in the viral hepatitis product series, Sansure Biotech has intensified its efforts to expand its blood screening series, respiratory infection series, reproductive tract infection and genetics series, and automated instruments. With the continuous launch of new products, the proportion of sales revenue from viral hepatitis products has shown a downward trend, yet overall revenue has grown year by year. A diversified product portfolio will help Sansure Biotech further unlock its growth potential.

Furthermore, while continuously consolidating and expanding its in vitro diagnostics business, Wantai BioPharma is vigorously advancing the development of vaccines as its “second core business.” Most changes in key financial indicators are associated with the research and development, production, and sales of the company’s vaccines. In its semi-annual report, Wantai BioPharma stated that it possesses a globally unique Escherichia coli prokaryotic expression virus-like particle (VLP) vaccine technology platform, which is applicable to the development of vaccines against various pathogens. The company has successfully launched the world’s first hepatitis E vaccine, is currently commercializing its HPV vaccine and next-generation HPV vaccine, and is strategically positioning itself for the more promising third-generation HPV vaccine.

As stated at the beginning of this article, the rapid response during the COVID-19 pandemic has validated the growth of China’s in vitro diagnostics (IVD) industry in recent years. Currently, there are more than 30 A-share listed companies whose core business is IVD, alongside a large number of biotechnology firms deeply specialized in specific technologies. Facing an expanding market valued at hundreds of billions of yuan, these companies encounter significant competitive pressure. In the aftermath of the severe disruptions caused by the pandemic, it is imperative for IVD enterprises to identify and establish their own growth trajectories.