Four Emerging Trends in China's Medical Services Industry Post-Pandemic: Insights from 20 Mid-Year Reports

In the first half of 2020, the sudden onset of the COVID-19 epidemic posed significant challenges to the healthcare services industry. Particularly during February and March, healthcare institutions across China (especially hospitals and clinics whose core businesses were not closely related to the epidemic) experienced widespread suspension of services, resulting in severely depressed revenues for some organizations.

According to the data from the "National Medical Service Situation from January to June 2020" released on the official website of the National Health Commission on August 21,In the first half of the year, the total number of visits to medical and health institutions across China reached 3.27 billion, a year-on-year decrease of 21.6%; the number of discharges from medical and health institutions nationwide reached 106.053 million, a year-on-year decrease of 16.6%; the hospital bed occupancy rate was 68.4%, a year-on-year decrease of 17.5 percentage points.。

Lacking a steady stream of business, healthcare service providers are struggling to survive.Taking dental chains as an example, at least ten such groups needed to borrow from banks to weather the crisis in the first half of this year. In March, when the pandemic was not yet fully under control, a questionnaire survey released by Guangzhou Ai Li Bi, a third-party hospital management consulting firm, showed that nearly 60% of private hospitals had less than two months of cash flow runway, casting an atmosphere of anxiety over the entire healthcare services industry.Fortunately, thanks to the collective efforts of the entire Chinese population, the domestic epidemic was basically brought under control from mid-to-late April. Industries have gradually resumed operations, and the medical services sector has also seen a turning point.

After navigating the challenging first half of the year, we cannot help but ask: What impact has the pandemic truly had on the healthcare services industry? What measures have related companies taken? And what does the future hold? To address these questions, VCBeat selected 20 listed companies in the healthcare services sector and analyzed their disclosed interim financial reports for 2020, offering insights into these critical issues.

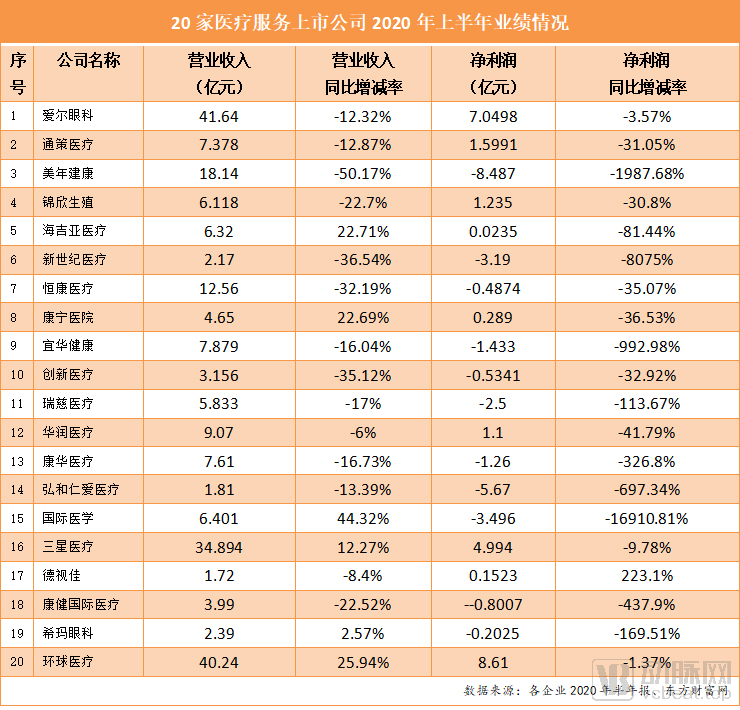

The screening criteria included listed healthcare service companies that had disclosed their semi-annual reports with relatively complete financial data. (United Family Healthcare’s operating entity, New Frontier Health, was excluded from the table due to the lack of comparable data from the same period last year.) For certain companies that reported figures in Hong Kong dollars (HKD) or US dollars (USD), currency conversions were applied to facilitate uniform comparison, using the exchange rates of 1 HKD = RMB 0.905 and 1 USD = RMB 7.016.

Impacted by the COVID-19 pandemic, healthcare companies have generally reported strong performance in the first half of the year. According to data from East Money Choice, as of September 1, a total of 306 healthcare companies listed on China’s A-share market had disclosed their semi-annual reports,Among them, 163 companies achieved year-on-year growth in net profit attributable to shareholders of the parent company, accounting for more than 50%.

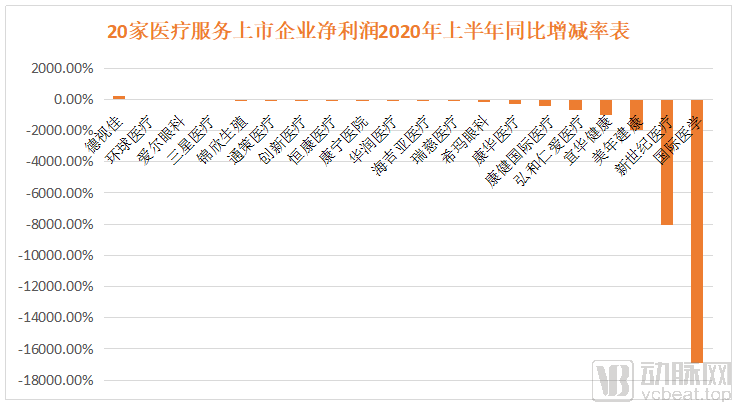

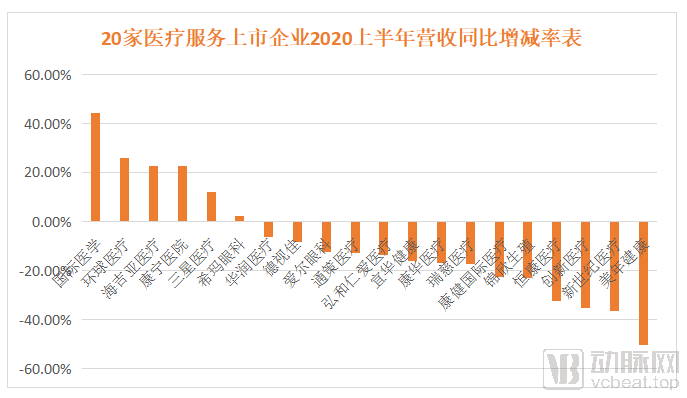

Conversely, looking at the medical service companies within this subsector, among the 20 companies included in this statistical analysis,In terms of the year-on-year growth rate of net profit, only EuroEyes (223.1%) recorded positive growth, accounting for 5% of the companies with positive growth., significantly below the industry average.

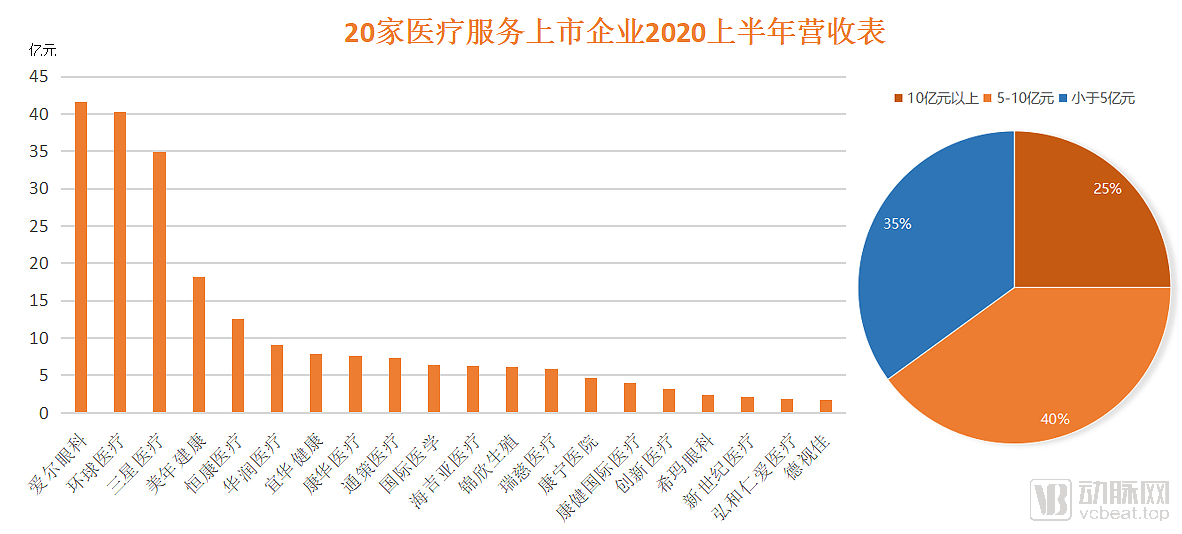

From the perspective of operating revenue,Five companies with annual revenues exceeding RMB 1 billion, including Aier Eye Hospital, Universal Medical, Samsung Medical, Meinian Onehealth, and Hengkang Medical;There are 8 companies with annual revenues between RMB 500 million and RMB 1 billion., including China Resources Medical, Yihua Health, Kanghua Medical, Topchoice Medical, International Medicine, Hygeia Healthcare, Jinxin Fertility, and Ruici Medical;There are 7 companies with revenue of less than RMB 500 million., including Kangning Hospital, Kian Health International Medical, Innovation Medical, C-MER Eye Care, New Century Healthcare, Honghe Renai Medical, and EuroEyes.

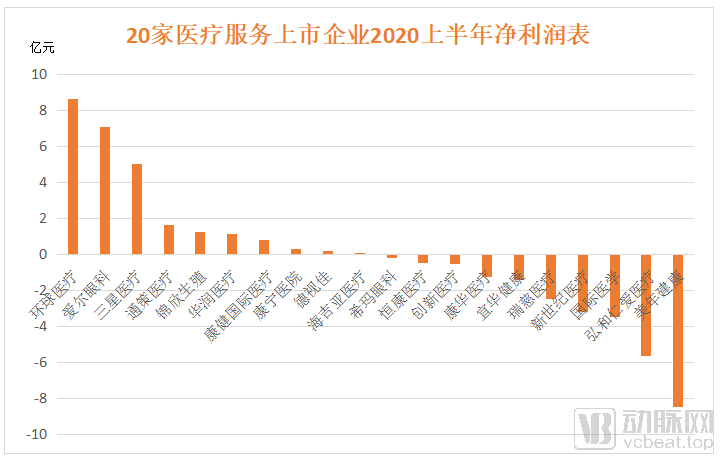

From the perspective of net profit,The number of companies with positive net profit was 10.,Accounting for 50%Among them, there are 6 companies with revenues exceeding RMB 100 million, namely Universal Medical, Aier Eye Hospital, Sanxing Medical, Topchoice Medical, Jinxin Fertility, and China Resources Healthcare; and 4 companies with revenues between RMB 0 and 100 million, namely Health International Medical, Kangning Hospital, EuroEyes, and Hygeia Healthcare.Ten companies reported negative net profits, accounting for 50%., namely C-MER Eye Care, Hengkang Medical, Chuangxin Medical, Kanghua Medical, Yihua Health, Ruici Medical, New Century Healthcare, International Medicine, Honghe Renai Medical, and Meinian Onehealth.

In terms of the year-on-year growth rate of operating revenue,Six enterprises posted positive growth, accounting for 30%., with the top three in terms of growth rate being International Medical Center, Universal Medical, and Hygeia Healthcare;14 companies experienced negative growth, accounting for 70%, with the top three being Meinian Onehealth Healthcare, New Century Healthcare, and Chuangxin Medical.

It is evident that, from the perspectives of year-on-year growth rates in operating revenue and net profit, the healthcare services sector was significantly impacted during the pandemic. However,In terms of the proportion of companies with positive net profits, the medical services industry as a whole maintained relatively stable performance during the pandemic, without widespread losses.。

For healthcare service providers, the impact of the pandemic has varied across different subsectors. The following is a brief analysis of key specialties based on interim reports.

According to Aier Eye Hospital's semi-annual report, during the reporting period, operating revenue was RMB 4.164 billion, a year-on-year decrease of 12.32%; net profit attributable to shareholders of the listed company was RMB 676 million, a year-on-year decrease of 2.72%.

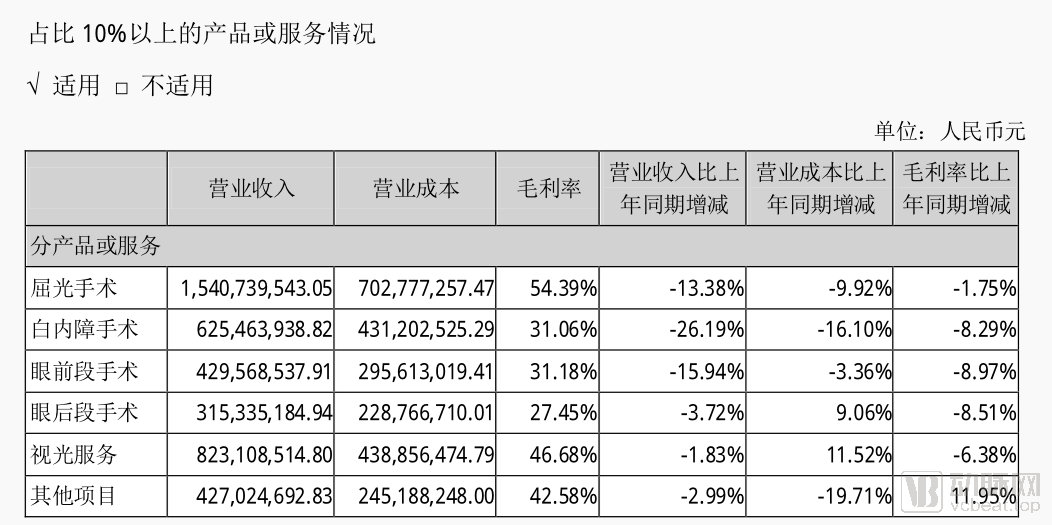

In terms of specific business operations, the causes leading toThe decline in performance was primarily driven by decreases in both outpatient visits and surgical procedures. Outpatient visits totaled 2.6411 million, a year-on-year decrease of 16.53%; surgical procedures amounted to 236,300 cases, a year-on-year decrease of 21.13%.. According to the semi-annual report, revenues from all products or services accounting for more than 10% of Aier Eye Hospital’s total declined. Specifically, refractive surgery revenue decreased by 13.38% year-on-year, cataract surgery by 26.19%, anterior segment surgery by 15.94%, posterior segment surgery by 3.72%, optometry services by 1.83%, and other items by 2.99%.

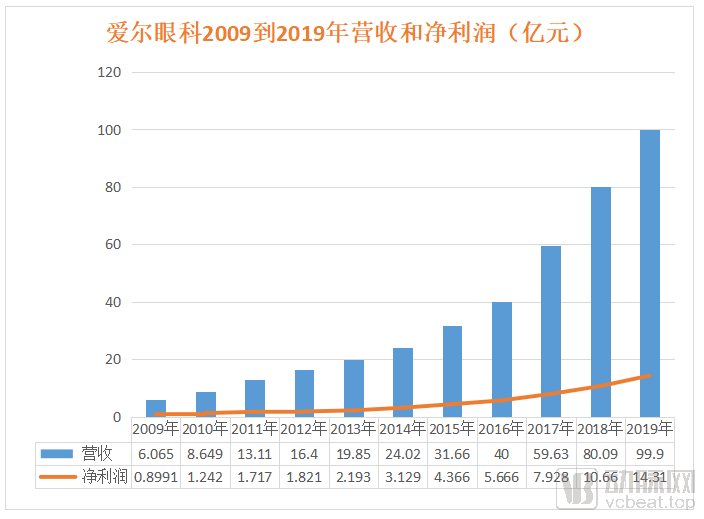

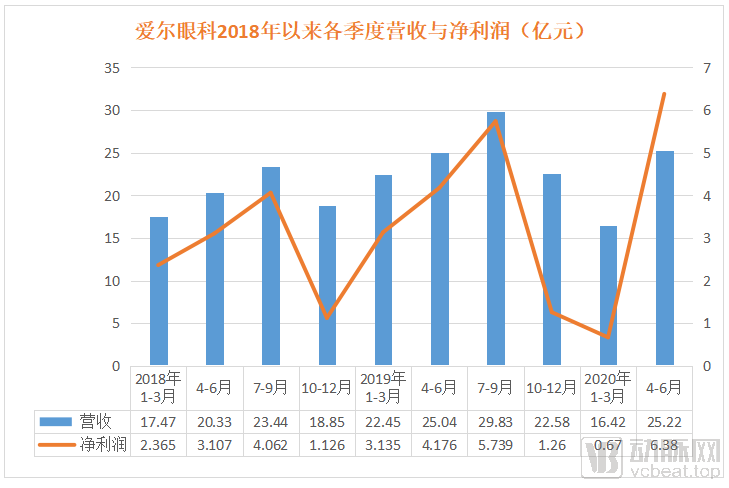

A review of Aier Eye Hospital’s performance over the past decade reveals a consistent trend of steady growth. The company’s revenue rose from RMB 1.31 billion in 2011 to RMB 9.99 billion in 2019, representing a 662.6% increase. Although performance declined in the first half of the year due to the pandemic impact, quarterly data show that Aier Eye Hospital generated RMB 1.642 billion in revenue from January to March and RMB 2.522 billion from April to June. In terms of net profit, the figures were RMB 67 million for January–March and RMB 638 million for April–June.As the company's quarterly revenue growth rate rises, it indicates that it has gradually emerged from the impact of the pandemic.

Interestingly,On the day following the release of its semi-annual report, Aier Eye Hospital’s stock price surged by 7.83%, with its market capitalization breaking through the RMB 200 billion mark., although performance declined in the first half of the year due to the pandemic, it demonstrates that the company’s business continues to gain market recognition.

Behind this, in addition to Aier Eye Hospital’s leading position in the ophthalmic chain sector and market recognition of its management model and other advantages,Also benefited from Aier Eye Hospital's timely response to the pandemic. For instance, during the pandemic, we promptly launched specialized services in response to patient needs, such as opening nighttime optometry clinics, maintaining regular outpatient services on holidays, providing online consultations with specialists, and offering dedicated telephone consultation lines; meanwhile,Accelerate the development of internet hospitals to comprehensively and continuously empower hospital growth.

As of August 26, Aier Eye Hospital had launched a total of 57 online hospitals under its umbrella, significantly enhancing diagnostic and treatment efficiency. During the reporting period, the Company completed mergers and acquisitions, acquiring 30 hospitals. This further refined the Company’s national network strategy, improved profitability and sustainable development capabilities, and laid a solid foundation for the Company’s “second entrepreneurship.”

Like Aier Eye Hospital, EuroEyes also operates in the chain ophthalmology sector. In terms of overall revenue performance, EuroEyes reported interim revenue of RMB 172 million for the first half of the year, a year-on-year decrease of 8.4%. Adjusted net profit after tax for the period amounted to RMB 15.148 million, representing a year-on-year decline of 43.7%. However, in terms of net profit, EuroEyes recorded a net profit of HKD 16.679 million during the reporting period, a year-on-year increase of 211.2%.

The reason for the counter-trend growth in net profit, as shown in EuroEyes' interim report, is that the group's revenue mainly comes from three regions: Germany, Denmark, and China. The group's revenue in Germany during this period was approximately HK$129 million, accounting for 68.5% of total revenue. Despite the impact of the pandemic, EuroEyes still achieved stable performance in Germany.

Public records indicate that EuroEyes, founded in 1993, has established more than 20 ophthalmic clinics and laser eye surgery centers across Germany, Denmark, and China, becoming the largest ophthalmic healthcare chain in Germany and even Europe.It is precisely EuroEyes’ deep-rooted presence in overseas markets that has driven its strong performance in the first half of the year, particularly in the first quarter.

In addition, EuroEyes’ semi-annual report also mentioned that,The company’s related costs during the pandemic were reduced by several government support measures for enterprises and assistance from some lessors in areas such as rent reductions.,Alleviated operational pressures on enterprises. Not only that, during the pandemic, EuroEyes continued to open new clinics to expand its business scope.

Affected by the pandemic, Topchoice Medical’s operating revenue and net profit declined compared with the same period in 2019, but remained above the levels of the same period in 2018, showing a steady recovery. In particular, its single-quarter operating revenue and net profit in the second quarter of 2020 increased by 20.39% and 44.63%, respectively, year on year.

Notably, in the second quarter, Topchoice MedicalThe gross profit margin and net profit margin for the quarter were 50.35% and 34%, respectively, representing year-on-year increases of 5.68 percentage points and 6.18 percentage points.In terms of specific revenue, pediatric medical services increased by 37% year-on-year in the second quarter; comprehensive medical services rose by 24%, orthodontic medical services grew by 22%, and dental implant medical services expanded by 17%.

The reason for such performance isBenefiting from Topchoice Medical’s rational control over operating costs and its continuous enhancement of self-sustaining capabilities through the “Regional General Hospital + Branch Hospitals” model。

Specifically, Topchoice Medical first establishes a central hospital within the region to build its influence, and then opens branch hospitals on the foundation of the central hospital’s maturity, thereby rapidly expanding its brand influence.

According to public information, at the end of 2018, Topchoice Medical and Hangzhou Stomatological Hospital Group launched the “Dandelion Plan,” focusing on dental implantology, orthodontics, and pediatric dentistry, and deeply expanding into major counties and cities in Zhejiang Province to capture a larger market share within the province. As of April 2020, Topchoice Medical had opened 21 dental hospitals in Zhejiang Province, with 15 branch hospitals under construction or preparation—including those in Xiasha and Linping—and an additional nine branches in the planning stage.

During the reporting period, despite the impact of the pandemic,However, Topchoice Medical continues to accelerate the construction of its Dandelion branch clinics and talent reserves. By implementing project objective management and standardizing construction processes, the company strives to compress construction timelines and reduce various costs and expenses, thereby mitigating the impact of the pandemic and ensuring the earliest possible opening of its branch clinics.In addition, Topchoice Medical continues to reduce procurement costs through centralized purchasing, keeps the three major expenses at a relatively low level overall, and further enhances operational capabilities through target management to achieve cost reduction and efficiency improvement.

During the pandemic, Hygeia Healthcare delivered standout performance. According to the interim report, for the six months ended June 30, 2020, the Group’s revenue increased by 22.8% year-on-year to RMB632.3 million; gross profit rose by 39.4% year-on-year to RMB216.3 million; gross profit margin increased from 30.1% in the same period of 2019 to 34.2%; and adjusted net profit surged by 65.4% year-on-year to RMB134 million.

From the perspective of revenue structure, during the reporting period, Hygeia Healthcare’s hospital business revenue reached RMB 555.9 million, an increase of 24.4% year-on-year. Among this, outpatient medical service revenue amounted to RMB 159.6 million, up by 33.3% year-on-year, while inpatient medical service revenue totaled RMB 396.3 million, representing a 21.2% increase from the same period last year.

As of the first half of the year,Hygeia Healthcare recorded 30,382 inpatient visits, a 9.2% year-on-year increase.; outpatient visits remained largely flat year-on-year due to the impact of the pandemic. The report shows that the company’s provision of high-quality, one-stop oncology treatment services has driven continuous growth in revenue per visit. In the first half of 2020, the average charge per inpatient admission was RMB 13,043, an 11.0% increase from the same period last year, while the average charge per outpatient visit was RMB 382, a 34.0% year-on-year increase. As of June 30, 2020, Hygeia Healthcare operated or managed a network of ten hospitals with oncology as their core specialty, located across seven cities in six provinces in China.

Specifically,The increase in revenue was primarily driven by hospitals that have already entered the mature operational stage., the revenue of this segment of hospitals has continued to grow. For example, Chengwu Hygeia Hospital, Suzhou Canglang Hospital, Longyan Bo'ai Hospital, Shanxian Hygeia Hospital, and Anqiu Hygeia Hospital have all achieved steady growth. In addition, newer hospitals such as Chongqing Hygeia Hospital and Heze Hygeia Hospital have also realized rapid revenue growth.

It is not difficult to see that, as a high-barrier specialty oncology healthcare sector, Hygeia Healthcare has maintained robust revenue performance through long-term operations and deep regional penetration, achieving counter-trend growth amid the COVID-19 pandemic.

As a leading enterprise in the health checkup industry, Meinian Onehealth was significantly impacted during the pandemic. In the first quarter of this year,Meinian Health: 56% of Days Affected by Work Suspensions and Patient Flow Restrictions; Q2 Accounted for 30%. As a result, Meinian Onehealth’s net profit attributable to shareholders of the listed company turned from profit to loss in the first half of the year, with a loss of approximately RMB 782 million; the net profit was RMB -848.7 million, representing a year-on-year decrease of 1,987.68%, while operating revenue amounted to approximately RMB 1.814 billion, down 50.17% year on year.

To address the impact, Meinian Onehealth has taken proactive measures. For example,Prepare Talent and Service Systems. For the health checkup industry,Many clients postpone their health checkups from the current quarter to the next quarter or the second half of the year, thereby creating staggered and off-peak consumption.Therefore, Meinian Onehealth focused on strengthening its internal capabilities and managing cash flow during the first and second quarters, when its business was impacted.Laid a solid foundation for the second half of the year, when business is highly likely to see a strong rebound or even an explosive surge.

A comparison of Q1 and Q2 performance shows initial signs of effectiveness. Data indicates that,Meinian Onehealth reported operating revenues of RMB 535 million and RMB 1.279 billion in Q1 and Q2, respectively, representing a quarter-on-quarter growth of 139%. The net profits attributable to shareholders were -RMB 599 million and -RMB 184 million, respectively. It is evident that the net loss narrowed significantly in Q2 compared with Q1, marking a notable quarter-on-quarter improvement.

In addition, last October, Alibaba Group, Ant Financial, and Yunfeng Capital acquired a 16.16% stake in Meinian Onehealth Healthcare for over RMB 7.2 billion. Of this, Alibaba and its affiliates held 10.82%, becoming the second-largest shareholder of Meinian Onehealth. This event, together with this year’s pandemic,Accelerated the Digital Transformation of Meinian Onehealth。

According to public reports, Meinian Onehealth’s Alipay mini-program has been launched, its sales management system is undergoing pilot implementation in Zhejiang Province, and its health examination system and medical quality control management platform have entered the product design and R&D phase. Core entity data has been migrated to the cloud. Alibaba’s empowerment of IT systems may serve as the cornerstone for Meinian Onehealth’s future transition toward refined management, thereby continuously enhancing its long-term competitiveness.

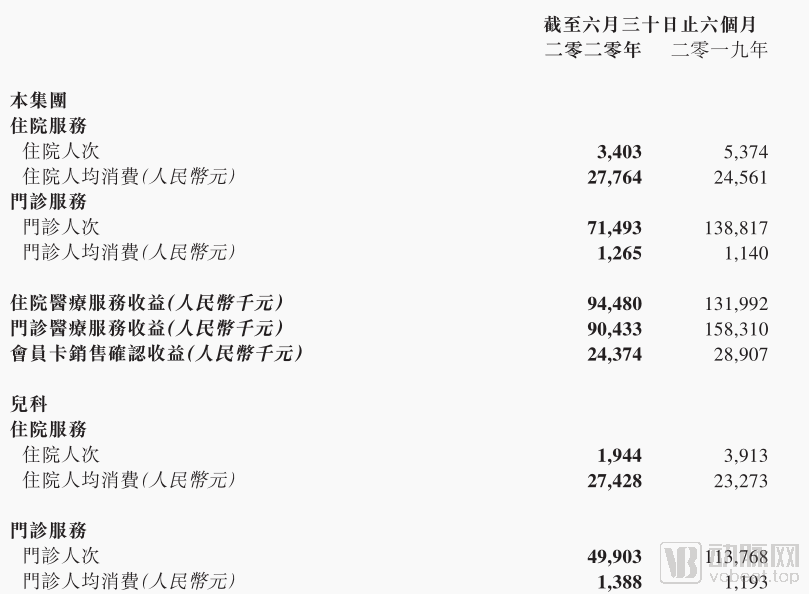

In the pediatric sector, New Century Healthcare reported revenue of RMB 217 million in the first half of the year, a year-on-year decrease of 36.7%; the loss attributable to shareholders amounted to RMB 308 million, representing a year-on-year increase of 3,179.8%. The basic loss per share was RMB 0.63.

Specifically, from a business perspective, the pediatric department generated RMB 146.9 million in revenue, a year-on-year decrease of 42.5%. Revenue from offline pediatric outpatient services amounted to RMB 69.2 million, representing a year-on-year decline of 49%.Outpatient visits: 49,903, a year-on-year decrease of 56.1%Due to an increase in specialist outpatient visits, the average per-capita outpatient expenditure reached RMB 1,388, representing a year-on-year increase of 16.3%. Pediatric inpatient revenue amounted to RMB 53.3 million, a year-on-year decrease of 41.4%, with 1,944 discharges, marking a year-on-year decline of 50.3%. Driven by a rise in specialist inpatient admissions, the average per-capita inpatient expenditure was RMB 27,428, up 17.9% year on year. As of August this year, New Century Healthcare’s pediatric outpatient visits had recovered to 90% of the level recorded in the same month last year, while pediatric discharges had rebounded to 70% of the prior-year figure.

Amid the impact of the pandemic, New Century Healthcare’s medical service revenue recorded its first negative growth since its listing in January 2017. During the period,The Contribution of Online Medical Services to the Company's Business is Gradually Becoming Apparent, with a combined total of 79,510 online and offline visits. Among these, online consultations accounted for 8,017 visits, representing 10.1% of the company’s total consultation volume. The rapid enhancement of online service capabilities ensured that New Century Healthcare could continue to provide routine medical services to customers during the pandemic.During the pandemic, 10% of customers chose to use New Century Healthcare’s online portal for self-service appointment scheduling.

Based on the semi-annual reports released by leading companies in segmented healthcare service sectors, we have found that for healthcare service providers, routine outpatient and inpatient care demands were temporarily suppressed due to government epidemic prevention and control requirements during the initial outbreak of the pandemic. This led to a significant decline in outpatient visits and hospital admissions. However, starting from the second quarter, when the epidemic was effectively brought under control, the situation improved significantly.

Although the year-on-year profits of the vast majority of medical service enterprises have declined, some companies have shown a year-on-year increase in revenue, whichThis growth is primarily driven by the business expansion of hospitals operated by such enterprises that have entered a mature operational phase.Therefore,For some companies, even during the pandemic, hospital expansion remained a strategic choice given their relatively ample capital.。

Furthermore, during the pandemic, healthcare service providers have also been actively pursuing transformation,Both digital transformation and online self-service appointment scheduling have, to some extent, alleviated operational pressures on enterprises.。

When the pandemic struck, the healthcare services industry was significantly impacted. From temporary suspensions to resumed operations, and further to achieving robust revenue growth against the odds, high-quality enterprises in the healthcare services sector have demonstrated strong resilience and vitality.

Based on the response measures adopted by relevant enterprises during the pandemic and their performance in terms of revenue and net profit, we believe that the future development trends of the healthcare services industry will likely focus on the following four aspects.

First, internet healthcare will drive the efficient development of the medical services industry.During this outbreak, offline diagnosis and treatment channels were obstructed and resources were strained, leading to difficulties in accessing medical care. Internet healthcare addressed critical challenges—such as providing free online consultations and follow-up visits, enabling health insurance payments, and facilitating medication delivery—thereby guiding patients to seek medical attention appropriately and meeting the urgent needs of those with chronic diseases. It has thus become a “second front” in epidemic prevention and control.As internet healthcare development deepens in its later stages, internet-based medical models—primarily comprising internet hospitals, telemedicine, medical consortia, internet-based chronic disease management, and family doctor services—will reshape the diagnosis and treatment processes of China’s healthcare services.

Second, the medical services industry will gradually shift its focus from treatment-oriented services to health-oriented services.The sudden onset of the COVID-19 pandemic has heightened public awareness of physical health. Although China’s medical services industry currently focuses primarily on “treatment” rather than “prevention,” the gradual opening of the Chinese medical services market and the rising living standards of the population are driving a transition from “medical services” to “health services.” This shift will spur rapid growth in preventive and rehabilitative health service sectors, including health check-ups, wellness conditioning, health consulting, health management, and aesthetic care.

Third, new medical technologies will bring more possibilities to the healthcare services industry.With the continuous advancement of new medical technologies such as early screening, artificial intelligence, 3D printing, and medical robotics, a disruptive revolution is poised to transform the healthcare services industry. During the pandemic, the da Vinci surgical robot at Zhongda Hospital affiliated with Southeast China University successfully performed surgeries on patients in home isolation, thereby overcoming situational constraints associated with surgical procedures. Undoubtedly,The emergence of new medical technologies will significantly broaden the scenarios for healthcare services and bring about a qualitative improvement in time efficiency.

Fourth, the medical services industry chain will undergo continuous restructuring and integration, resulting in a more diverse industrial ecosystem.China’s healthcare services sector remains relatively traditional overall, with small and fragmented providers operating at a nascent stage of digitalization in their operational and management models. As healthcare institutions deepen reforms in organizational management and informatization, and as the state gradually liberalizes market access, diversified healthcare service providers will flourish. This trend will favor enterprises with superior management efficiency and advanced digital capabilities. In this context, rising industry-wide efficiency and intensifying competition will drive healthcare companies to target more niche market segments and strengthen their competitive moats, thereby enriching the industrial ecosystem.

Looking ahead, China’s healthcare services industry is poised to become a fertile ground brimming with transformation, opportunities, and hope. Driven by the continuous advancement of national policies and the dedication and hard work of every practitioner, the entire healthcare services sector will undergo significant changes.

We firmly believe that after weathering the “storm” of the COVID-19 pandemic, the healthcare services industry is ushering in a new era of clear skies.