New Regulations Unveiled: Unlocking the Trillion-Yuan Opportunity in Health Insurance and Health Management Services

On September 9, the General Office of the China Banking and Insurance Regulatory Commission (CBIRC) issued the “Notice on Regulating Health Management Services Provided by Insurance Companies” (hereinafter referred to as the “Notice”). The new regulations clarify the concept of health management and stipulate that the cost proportion of health management services in insurance products may reach up to 20%.

In recent years, the health insurance industry has experienced rapid growth, with health insurers frequently procuring health management services. Therefore, the “Notice” undoubtedly represents a significant positive development for the health management sector.

Meanwhile, the “Notice” sets forth specific requirements for insurance companies regarding the design of health management services and the initiation of third-party collaborations, thereby directly impacting the health insurance industry.

Nowadays, the integrated development of health insurance and health management has become a major trend. So, what impact will the “Notice” have on the fields of health management and health insurance respectively? And how will it promote their genuine integration? VCBeat promptly interviewed multiple industry experts to conduct a joint analysis.

Following the release of the “Notice,” the China Banking and Insurance Regulatory Commission (CBIRC) provided an overview of its background and underlying rationale. Drawing on the CBIRC’s interpretation and analyses by industry experts, we have identified four key highlights of the “Notice.”

Clarifying the Concept and Classification of Health Management Services

What Is Health Management? There can be myriad answers depending on the implementing entities and application scenarios. Within the scope of health insurance coverage, the Notice defines health management as actions taken to monitor, analyze, and assess customers’ health; intervene against health risk factors; control the onset and progression of diseases; and maintain a state of well-being. It encompasses seven major categories: health examinations, health consultations, health promotion, disease prevention, chronic disease management, medical services, and rehabilitation nursing.

Liu Xuejian, Head of the Insurance Business Department at Zhiyun Health, believes that the aforementioned classification reflects the principle of full-cycle customer management. It forms a complete chain spanning from health check-ups and disease prevention to chronic disease management and post-treatment rehabilitation care, demonstrating that the new regulations impose more systematic requirements on health management.

Emphasizing the Scientific Rigor and Rationality of Health Management Services

At present, health management services included in health insurance products encompass a wide range of sub-items, ranging from appointment registration to tumor radiotherapy programs.

A representative from the relevant department of the China Banking and Insurance Regulatory Commission (CBIRC), while introducing the background behind the formulation of the “Notice,” stated that health management services currently offered by the insurance industry suffer, to some extent, from issues such as low service quality, overly complex service offerings, and unclear service boundaries, with some practices even devolving into mere tools and tactics for customer acquisition.

The “Notice” clarifies that the ultimate goal of health management services is to improve health outcomes and reduce medical costs. Therefore, it requires that the content of health management services adhere to principles such as scientific rigor, reasonableness, safety, effectiveness, and objectivity. Insurance companies shall scientifically and reasonably define the scope of health management services and determine service pricing, based on their own service capabilities, customer needs, and the characteristics of health insurance operations.

“There are two types of health insurance: those that sell well and those that are effective.” Ren Bin, CEO of Insurance Geek, stated that some health insurance products designed to sell well incorporate various services to cater to customer psychology. However, the true value of health insurance should be reflected in its effectiveness, leveraging medical services and health management for risk pooling and transfer, thereby reducing users’ risk of falling ill.

Refine the Operational Rules for Health Management Services

Insurance companies must deliver health management services through a joint effort by their internal teams and third-party providers. The Notice clearly specifies requirements concerning insurers’ organizational management, system development, personnel, talent cultivation, and information systems, as well as the scope of cooperation and qualification criteria for third-party service providers, their selection and assessment, cooperation agreements, service oversight, and quality evaluation.

This also means that the process by which insurance companies procure health management services and engage in third-party collaborations constitutes normal business cooperation, while also requiring them to strictly control supplier quality in accordance with the provisions of the Notice.

Strengthening Supervision and Management of Health Management Services

Furthermore, the Notice clarifies the compliance requirements and internal accountability mechanisms for insurance companies providing health management services, and sets forth requirements for information reporting, emergency response to major incidents, and incident reporting.

In accordance with regulations, insurance companies are required to submit statistical information related to their health management services on a semi-annual basis. The submitted content must be truthful, complete, and verifiable.

Based on the above highlights, the definition and classification of health management services constitute the core of this “Notice,” while the other three key highlights serve to support this core by leveraging various rules to ensure that health management truly delivers value.

“The Notice will incentivize insurance companies to carry out supply-side reforms in health insurance products and drive continuous improvements in health management service standards and quality,” said Gu Shufeng, COO of Miao Health.

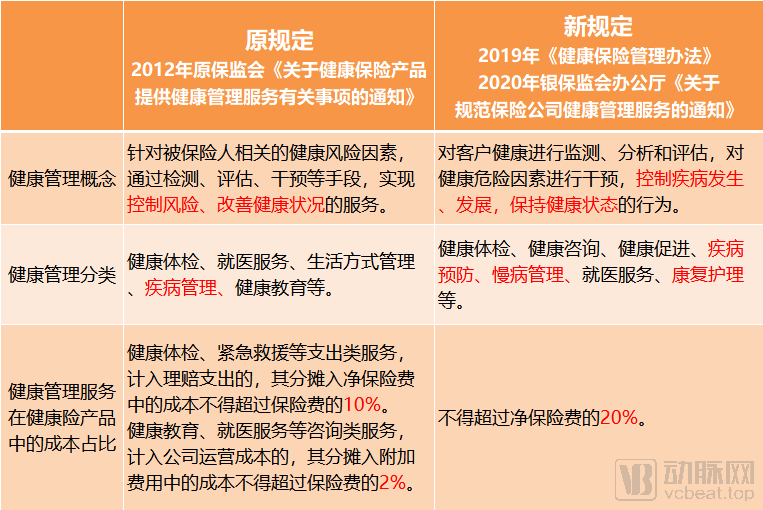

In fact, this is not the first time that regulatory authorities have defined health management services within health insurance products. As early as 2012, the former China Insurance Regulatory Commission (CIRC) issued policies clarifying that insurance companies may provide health management services in health insurance products, and stipulated the concept and classification of health management, as well as its cost proportion in health insurance products.

In 2019, the China Banking and Insurance Regulatory Commission (CBIRC) promulgated the revised Measures for the Administration of Health Insurance, in which Chapter VI, titled “Health Management Services and Cooperation,” comprises eight provisions addressing the integration of health insurance with health management, thereby increasing the allowable proportion of health management costs within health insurance products.

In 2020, the General Office of the China Banking and Insurance Regulatory Commission issued the “Notice on Regulating Health Management Services Provided by Insurance Companies,” which redefined the concept and classification of health management, replacing the 2012 version of the regulations.

A comparison of the above three policies reveals that health management has primarily undergone changes in three aspects: concept, service classification, and cost proportion.

Comparison of Old and New Regulations on Health Management Services in Health Insurance Products; Source: Official Website of the China Banking and Insurance Regulatory Commission (CBIRC); Chart by VCBeat

On the Concept of Health ManagementThe 2012 edition emphasized “improving health status,” whereas the 2020 edition stresses “maintaining a state of health.” Clearly, the latter imposes higher requirements than the former, necessitating more management measures for implementation. Meanwhile, the 2020 edition places greater emphasis on the monitoring, analysis, assessment, and intervention of health status.

“For example, big data platforms for health management can leverage wearable devices to track clients’ health status, thereby shifting the entry point of health management services upstream,” introduced Gu Shufeng. Once a potential health risk is identified during routine monitoring, timely lifestyle interventions or medical referrals can be provided to prevent clients from developing serious diseases. Miao Health has previously integrated standardized health data SDKs and other capabilities for multiple insurers, including PICC Health Insurance and Ping An Health Insurance, while also offering health behavior management services. “Driven by new regulations, collaboration between health management companies and insurance providers will become increasingly extensive and in-depth in the future.”

On Health Management Classification, the 2012 edition included only five items, which increased to seven in the 2020 edition. The most significant changes are twofold: first, chronic disease management is listed as a separate item, offering greater precision compared to the previous disease management category; second, a new item for rehabilitation nursing has been added.

“Listing chronic disease management as a standalone item within health management indicates that the China Banking and Insurance Regulatory Commission (CBIRC) highly recognizes its value,” introduced Liu Xuejian. In the past, few insurance companies marketed chronic disease management as a selling point for their products, for straightforward reasons: First, most customers lacked strong willingness to proactively engage in such management. Second, unlike clearly defined services such as green channels and referral services, chronic disease management is not a single service but a comprehensive package comprising multiple sub-components, making it difficult for insurers to promote in their product marketing. Finally, chronic disease management had no direct reflection in the pricing of insurance products.

However, Liu Xuejian also noted that following the outbreak of the COVID-19 pandemic, people’s willingness to seek medical care at hospitals declined. For patients with chronic diseases, ineffective health management increases the likelihood of disease progression, thereby driving up insurance claim ratios. In this context, online chronic disease management platforms such as Zhiyun Health, integrated with pharmaceutical supply chains, can address issues that previously required hospital visits, thus reducing the risk of disease exacerbation among patients. “Against this backdrop, the value of chronic disease management has become increasingly prominent.”

Liu Xuejian also highlighted the critical role of rehabilitation nursing. “Insurance products may involve multiple claims payouts for patients; if effective rehabilitation and management are implemented during hospitalization, the likelihood of readmission and subsequent claims will decrease.”

On the Proportion of Health Management Service Costs in Health Insurance Products, the 2012 edition stipulated that health education and medical consultation services could not exceed 2%, while health examinations and emergency rescue services were capped at 10%; in contrast, the 2020 edition significantly increased the allowable cost proportion and removed separate caps for specific items.

These changes signify greater potential for value creation in health management, with clearly defined payers. In January 2020, the “Opinions on Promoting the Development of Commercial Insurance in the Social Services Sector,” jointly issued by thirteen ministries and commissions including the China Banking and Insurance Regulatory Commission (CBIRC) and the National Development and Reform Commission (NDRC), set a target to expand the commercial health insurance market to over RMB 2 trillion by 2025. Consequently, within this vast commercial health insurance market, the health management sector enjoys expanded growth prospects.

Health insurance not only boasts a large market size but also exhibits a trend of rapid growth. Data from the China Banking and Insurance Regulatory Commission (CBIRC) shows that from January to July 2020, the original premium income of health insurance reached RMB 530.2 billion, a year-on-year increase of 19.3%; while the total premium income of the insurance industry during the same period was RMB 3,006.2 billion, representing a year-on-year growth of 7%. This indicates that the growth rate of health insurance is significantly higher than the overall growth rate of the industry.

However, alongside the rapid growth in premiums, the health insurance industry faces a stark reality: high claims payouts, widespread product homogenization, and less-than-optimistic profitability. The 2019 annual reports of the six specialized health insurance companies revealed that three of them had yet to turn a profit.

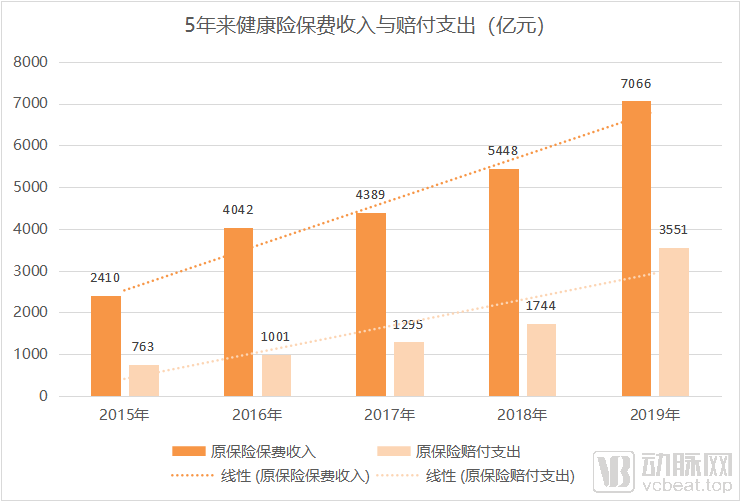

Changes in Gross Written Premiums and Claims Payments of Health Insurance; Source: Website of the China Banking and Insurance Regulatory Commission (CBIRC); Chart by VCBeat

As shown in the chart above, over the past five years, although premium income from original health insurance has maintained rapid growth, claim payouts have exhibited a nearly identical rate of increase.

For the health insurance industry, the Notice appears to be a regulatory measure on the surface, but in reality, it aims to encourage companies to strengthen risk control management and product innovation, thereby promoting the sustained and healthy development of the industry.

“From a health economics perspective, investing 1 yuan in prevention yields the same health outcomes as investing 8 yuan in treatment; commercial insurance institutions urgently need to enhance their risk and cost control capabilities,” said Gu Shufeng. He noted that the current structure of health insurance products is imbalanced and lacks effective supply, necessitating supply-side reforms. In practice, pre-illness prevention, being an uncertain event, is often overlooked by insurers. Cost control and claims risk management in health insurance can be explored through a prevention-oriented approach; therefore, the issuance of the “Notice” has further paved the way for product innovation by insurance companies.

Gu Shufeng explained that during insurance product design, predictions can be made regarding the probability of policyholders developing critical illnesses within a future period, based on their health risk assessment results and the presence of pre-critical illness conditions. Currently, institutions in China have developed risk assessment systems for underwriting by insurance companies, such as Miao Health’s “H-Value” assessment system, which applies differential premium calculations according to the risk levels of policyholders.

From Liu Xuejian’s perspective, single-disease insurance particularly reveals innovative aspects under the new regulations. He noted that in the past, health insurance products, represented by critical illness insurance and million-yuan medical insurance, mostly accepted only healthy individuals for coverage. Single-disease insurance, however, accepts applicants with pre-existing conditions, resulting in high claims risk, expensive pricing, and limited coverage scope, which has prevented sales from achieving scale.

“If chronic disease management is strengthened within single-disease insurance, the claims risk becomes controllable, thereby facilitating the scaled development of such insurance products,” said Liu Xuejian. He noted that competition in the critical illness insurance and million-yuan medical insurance sectors has reached a fever pitch. Given the wide variety of chronic diseases and the large patient population, innovation in single-disease insurance can help differentiate insurance products.

Although health management and health insurance are impacted differently by the new regulations, they are by no means operating in silos; deep integration is the overarching trend.

Ren Bin argues that health management services must not only be scientifically sound and reasonable but also enhance accessibility and user perception. “For instance, the health insurance products we provide to enterprises include standard features such as online consultations and outpatient appointment registration. We establish service access points through customers’ personal accounts, allowing them to select corresponding services upon login. Additionally, we proactively push relevant services to customers via H5 pages,” Ren Bin stated. In short, it is essential to fully inform customers of the availability of these services and leverage various methods to improve convenience of use, rather than focusing solely on the sales phase.

“In the industry, insurtech companies connect insurance carriers, healthcare service providers, corporate clients, and individual customers, leveraging advantages in resources and data,” Ren Bin noted. This necessitates that insurtech companies capitalize on these accumulated strengths to develop truly valuable products and promote the integration of health insurance with health management.

Gu Shufeng suggests standardizing service provider management and service content. For instance, insurance companies or even the entire insurance industry should be encouraged to establish health management service platforms that enable standardized management of providers, including the establishment of admission criteria and exit mechanisms for vendors. Meanwhile, corresponding libraries of health management service systems should be developed for specific population segments or insurance products, thereby creating standardized service offerings.

In Gu Shufeng’s view, the promulgation of the “Notice” formally declares that future competition among health insurance companies or among the health insurance operations of insurers will involve not only coverage scope and premium rates, but also competition in empowering services through health management. “Designing insurance products by integrating health management services from multiple dimensions and at various levels, thereby providing policyholders with more comprehensive and effective health protection, will be an inevitable path for the entire industry.”