Billion-Dollar Smart Hospital Deals Emerge as Next-Gen HIS Reshapes Traditional Market; HIT Industry Poised for a Golden Decade

IDC

International Data Corporation

For most healthcare IT companies, the COVID-19 outbreak at the beginning of the year had a severe negative impact on their business expansion during that period, potentially triggering a major industry reshuffle.

Everything has two sides. A survey conducted by IDC in early 2020 targeting the healthcare industry showed that,In China, 96% of tertiary hospitals have formulated informatization upgrade plans inspired by the pandemic, and 88% of tertiary hospitals have improved or newly built information systems to respond to the pandemic.

During the pandemic, telemedicine and internet-based healthcare supported medical treatment and epidemic prevention in small and medium-sized cities, as well as facilitated consultations and medication access for patients with chronic diseases. Artificial intelligence in medical imaging further assisted in the timely clinical diagnosis of COVID-19 in affected areas. Robotics deployed in hospital wards alleviated the workload of healthcare workers. Big data technology aided epidemiological investigations and regional monitoring... The directions taken by hospitals to improve or establish new facilities all highlight the critical importance of informatization in healthcare. These developments have further prompted doctors and scholars who previously held skeptical or indifferent attitudes toward information technology to gradually recognize its pivotal role in the new public health defense system.

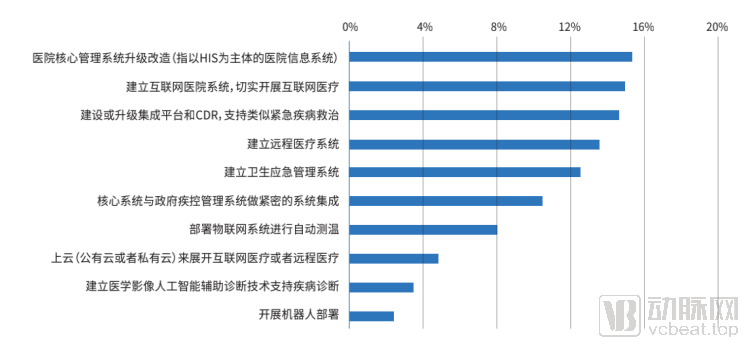

Key Areas of Hospital Information System Upgrades Driven by the COVID-19 Pandemic

(Data source: IDC, Winning Health Technology Group Co.,Ltd. report:

“Building a Medical Digital Transformation Platform with Middle-Platform Thinking to Break Through the Capability Bottlenecks of Hospital Information Systems”

Certainly, the changes in the healthcare IT industry in 2020 were not limited to shifts in hospitals’ awareness and demands. With the release of mid-year reports from various companies, more directions and trends have emerged from these disclosures. To this end, VCBeat analyzed the annual reports of 15 publicly listed healthcare IT companies. Although the healthcare IT market is highly fragmented, these companies collectively accounted for approximately 20% of the IT market share, which is sufficient to outline the general trajectory of healthcare IT development.

Driven by the pandemic, nearly all listed health IT companies saw their stock prices trace a “V”-shaped trajectory over the past six months.

In general,The Impact of the Pandemic on EnterprisesOriginating from two aspects:

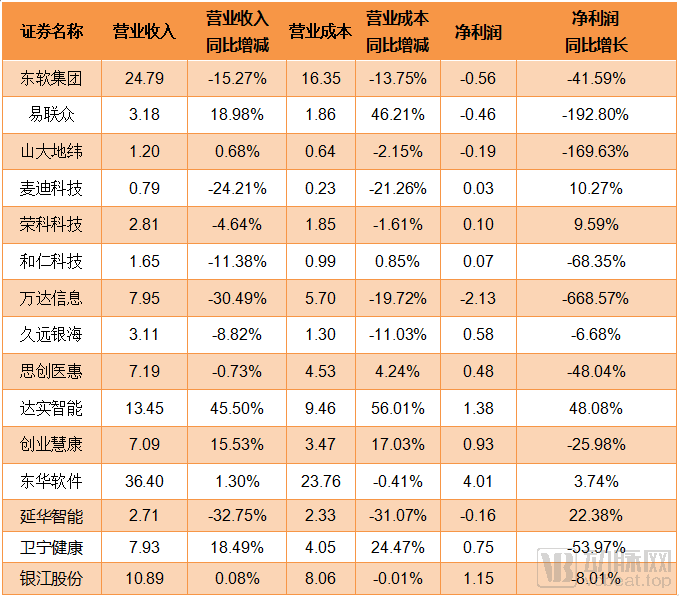

First, restrictions on public transportation and personnel movement, coupled with delays in the resumption of work and project construction across the upstream and downstream sectors of the medical health informatics industry, as well as delays in accounts receivable recognition, have further led to a decline in corporate operating revenues. Among the 15 companies surveyed, only Yilianzhong, Das Intellitech, B-Soft Co., Ltd., and Winning Health Technology Group Co.,Ltd. achieved double-digit growth, while the revenue performance of the remaining companies was unsatisfactory.

Second, the rise in corporate operating costs during the pandemic. The increased figures primarily stem from higher expenditures incurred by large enterprises during the pandemic, such as donating consumable anti-epidemic supplies to medical institutions and providing free support in the form of information technology hardware and software; as well as donating materials, cash, and other resources to healthcare organizations. If this factor were excluded, the intrinsic profit margins of many informatization enterprises might have seen a certain increase.

Brief Overview of Financial Data in the 2020 Interim Report of Information-Based Enterprises (Unit: RMB 100 million)

Brief Overview of Financial Data in the 2020 Interim Report of Information-Based Enterprises (Unit: RMB 100 million)

From the perspective of profit, among the 15 listed healthcare IT companies, 10 experienced varying degrees of profit decline; three saw marginal profit growth; Yanhua Intelligence achieved a 22.38% increase, yet its net profit remained negative; Das Intellitech performed the best, realizing a 48.08% profit growth and a net profit of RMB 138 million despite the pandemic.

Das Intelligents’ strong performance has been bolstered by its smart hospital initiatives, although its revenue streams are not exclusively derived from the healthcare sector. During the reporting period, Das Intelligents won the bid for the Smart Healthcare Project at the New Campus of Suzhou Municipal Hospital in Anhui Province, with a contract value of RMB 234.9 million, accounting for 10.65% of the company’s audited operating revenue for 2019. In addition, the company signed a RMB 325 million contract for the Shenzhen Baohe Big Data Center project and won the bid for the Beijing Expressway ETC R&D and Production Base and Beijing Expressway Data Operations Center project, valued at RMB 175 million. These three major projects together contributed nearly 70% of Das Intelligents’ total revenue.

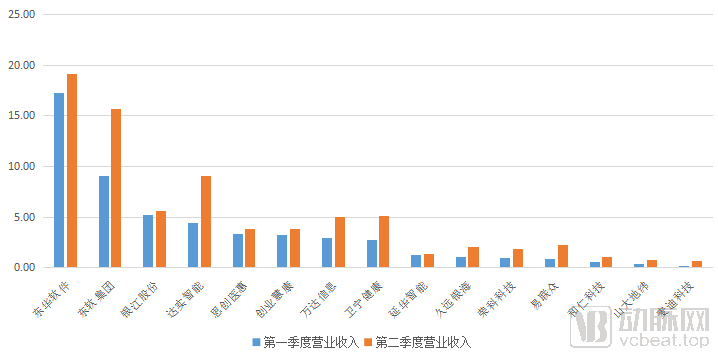

So, for other companies, did performance rebound in the second quarter after the COVID-19 pandemic? The answer is yes.

As shown in the figure below,Changes in Corporate Revenues in Q2: All Companies Reported Higher Q2 Revenues Than Q1, with Many Seeing Increases of Up to 100%; The Impact of the Pandemic Is Being Diluted by the Subsequent Surge in Informatization.

Revenue Fluctuations of Listed Healthcare IT Companies (Unit: RMB 100 Million)

Revenue Fluctuations of Listed Healthcare IT Companies (Unit: RMB 100 Million)

In fact, in the post-pandemic era, hospitals’ enthusiasm for digital transformation has reached an unprecedented high. According to VCBeat’s analysis, the following trends are most likely to shape the direction of the healthcare IT industry this year.

Recently, Huazhong University of Science and Technology and Shenzhen Hospital replaced their existing HIS with a new system from Donghua Software, more than eight years after their last major IT infrastructure upgrade.

“Many hospitals are similar to us in that they may not have upgraded their Hospital Information Systems (HIS) for nearly a decade. However, the pandemic has, to some extent, accelerated the iterative development of our hospital’s informatization. The architecture of the older generation of integration systems is no longer suited to today’s digital technologies and the continuous emergence of new applications,” an IT department physician at a Shenzhen hospital told VCBeat. “Taking 5G infrastructure as an example, traditional HIS platforms typically supported only IPv4, which limited the availability of network address resources within hospitals. In contrast, 5G requires hospitals to support the new IPv6 protocol. Furthermore, the rise of various artificial intelligence applications has compelled us to seek more compatible architectural solutions.”

The pressure of digital transformation in hospitals is not limited to this; it also includes insufficient IT architecture flexibility caused by rigid application architectures and a lack of standardized data management; the significant gap between healthcare big data and the resulting “knowledge” and “medical expertise”; management challenges arising from the surge in diversity of hospital IT operations; and the challenges faced by medical staff regarding the usability of operating systems across multiple platforms.More critically, the requirements for data storage and interoperability in the connectivity rating...Addressing these issues requires healthcare IT to implement fundamental solutions, giving rise to the concept of the “Next-Generation HIS.”

Issues or Deficiencies in the Hospital Core Management System (or Traditional HIS)

(Data sourced from IDC and Winning Health Technology Group Co.,Ltd. report:

“Building a Medical Digital Transformation Platform with Middle-Platform Thinking to Break Through the Capability Bottlenecks of Hospital Information Systems”

However, although the concept of "next-generation HIT" has been widely discussed since last year, there has never been a clear definition. In addition to architectural upgrades to support new technologies and applications, each company releasing a next-generation HIS system has its own unique interpretation of what "next-generation" means.

Neusoft CorporationRecognized as one of the earliest companies to propose a new generation of Hospital Information System (HIS), Baidu invested RMB 1.443 billion in Neusoft Holdings in September 2019. This high-tech investment and management firm is the primary investor in Neusoft Corporation, Neusoft Education Technology, Neusoft Medical Systems, Neusoft Xikang, and Neusoft Wanghai (now renamed Wanghai Kangxin).

The integration of internet companies and healthcare IT enterprises always sparks new innovations; for Baidu, it brings exceptional AI capabilities to Neusoft.

On one hand, the two parties jointly established a “CDSS Special Task Force” to leverage AI in enhancing the quality and efficiency of medical care across various healthcare institutions from a clinical perspective; on the other hand, Baidu Lingyi Zhihui’s AI solutions have been fully integrated into Neusoft’s HIS product suite (referred to by Neusoft as its next-generation HIS).

Based on the current capabilities of Lingyi Zhihui, AI will become the core capability of Neusoft’s next-generation HIS.

Empowered by AI, Neusoft’s Hospital Information System (HIS) offers real-time quality control capabilities for both textual documentation and clinical content—a relatively mature technology. Additionally, AI enables the collection and analysis of workflow data, thereby supporting hospital administrators in decision-making.

Winning HealthWiNex, released this July, shares similarities with Neusoft’s “New-Generation HIS.” This system also incorporates full-process quality control capabilities enabled by an NLP-supported knowledge base. However, at the launch event, Winning Health emphasized not AI, but rather the “middle-platform mindset” aimed at transforming hospital IT architecture.

What is “middle-platform thinking”? The report, “Building a Digital Transformation Platform for Healthcare with Middle-Platform Thinking to Break Through the Capability Bottlenecks of Hospital Information Systems,” describes middle-platform thinking as follows:

“Middle-platform thinking is, first and foremost, an organizational model for technology or business; secondly, from a technical perspective, the middle platform is an architecture that integrates technology, business, and data, emphasizing commonalities and reusability. Distinct from the concept of reuse in traditional application architectures, the middle platform strives to achieve dynamic reusability driven by customer needs, thereby enabling timely responses to frequent business changes.”

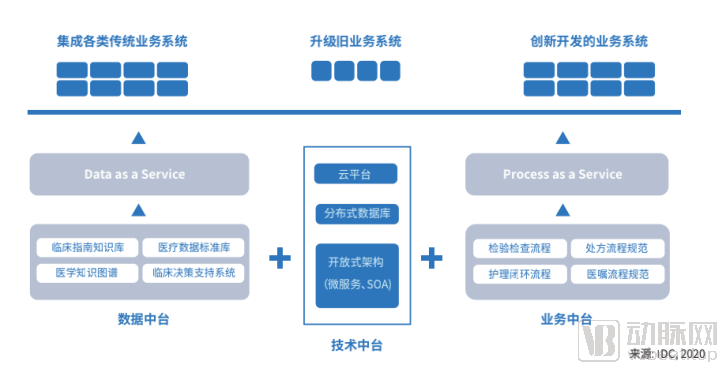

In short,Winning Health Technology Group Co.,Ltd. plans to dismantle its previously redundant integrated information systems, reclassify the complex business-module-based systems into three interconnected platforms—technology middle platform, data middle platform, and business middle platform—to ultimately achieve the optimal solution for business collaboration and data integration.

Winning Health's Ideal Digital Platform Framework (Source: IDC)

Under the new medical IT architecture, Winning Health divides the collaborative workflow of its three middle platforms into four steps, forming a business cycle:

1. Leveraging the process services of the business middle platform as the starting point, import standardized medical business data and integrate it with data from clinical guideline repositories. Utilize business service APIs in conjunction with data service APIs to develop and build various clinical systems, including core hospital information systems, electronic medical records (EMR), and internet healthcare platforms.

2. Source data generated by various clinical systems is stored in the data middle platform for on-demand service access, ensuring real-time data utilization within the platform. Meanwhile, this data is also exported to the Clinical Data Repository (CDR), where it undergoes processing and transformation into knowledge before flowing back into the data middle platform for service invocation. Prior to complete migration to the data middle platform, data from parallel core hospital systems, electronic medical records (EMR), and other healthcare systems, as well as external health data, can be aggregated via an integration platform into the Clinical Data Repository (CDR) and subsequently ingested into the data middle platform.

3. Leverage big data processing and analytics, machine learning, and other technologies to construct new knowledge graphs and knowledge bases within the data middle platform; through review processes, develop innovative medical knowledge services that feed back into the business middle platform. Meanwhile, incorporate newly established standard libraries for medical workflows derived from innovative care models, as well as medical service business rules formulated in accordance with new policies issued by the government during ongoing healthcare reforms, into the business middle platform.

4. The technical middle platform consistently supports the interaction and dynamic cyclical processes between the aforementioned business middle platform and data middle platform.

Through the aforementioned process, the new-generation HIS system developed by Winning Health Technology Group Co., Ltd. not only possesses capabilities for innovative business development but also accommodates the frequent changes mandated by healthcare reforms and meets requirements such as cross-platform deployment. However, it does not address operational convenience for hospitals or the lack of treatment plan support assistance, as indicated in the table.

At CHINC 2020,Hangzhou Century Co.,Ltd.Showcased its next-generation Hospital Information System (HIS). Unlike the two aforementioned companies, Hangzhou Century Co., Ltd.’s new-generation HIS aims to create an “Android” for the healthcare industry. It has developed a technical architecture based on an intelligent open platform, providing a foundational platform infrastructure for delivering continuous healthcare services and driving the transformation of China’s medical informatization development model.

What is refreshing is that Hangzhou Century Co.,Ltd. has further evolved its mature open architecture into a microservices framework system, decomposing legacy integrated systems into independent micro-modules with clear business boundaries. By leveraging the microservices framework to reengineer hospital business systems and functionalize services, it enables rapid deployment, restructuring, and one-stop lifecycle management of hospital operations. This approach supports personalized and specialty-specific applications in healthcare informatization, thereby enhancing user experience.

From this perspective, Hangzhou Century Co.,Ltd. places greater emphasis on the user experience of physicians, focusing on addressing the portability issues of operating systems for medical personnel.

In addition, companies such as Wonders Information, Yanhua Smartech, Heren Technology, and Jiuyuan Yinhai have also developed their own next-generation HIS system products. Traditional non-listed IT firms like Xinxing Technology and Mandala are also assisting hospitals by transforming products such as electronic medical records and outpatient workstations.InterconnectivityModifications will not be detailed here.

To date, it has become increasingly evident that the role of hospital information departments is shifting from the periphery to the center. Having reaped tangible benefits, many hospitals’ informatics initiatives are no longer driven solely by policy. For instance, numerous hospitals had already proactively launched smart hospital construction efforts, staying ahead of accreditation requirements.

On June 16, the Medical Administration and Hospital Management Bureau of the National Health Commission issued the “Letter on Carrying Out the 2020 Graded Assessment of Smart Hospital Services,” stating, “To guide medical institutions in standardizing the development of smart hospitals and continuously enhance patients’ sense of gain in accessing medical care, our Bureau has decided to carry out the 2020 Graded Assessment of Smart Hospital Services.” The notice requires all localities to actively mobilize secondary-level and above hospitals within their jurisdictions to participate.

Building smart hospitals is a major business opportunity, with recently popular concepts such as internet hospitals and clinical decision support systems (CDSS) falling within this category. As hospitals have varying needs for smart hospital development, the scope of tenders exhibits considerable flexibility. Projects across hospitals of different sizes and at different stages of digital maturity show significant variation in winning bid amounts and project timelines.

For example, the smart hospital construction projects won by Hangzhou Century Co., Ltd. this year—including those for Jinan Maternal and Child Health Care Hospital, the Second Affiliated Hospital of Soochow University, and the Affiliated Hospital of Xuzhou Medical University—are all valued at tens of millions of yuan. In May 2020, Wonders Information Co., Ltd. won the bid for the Shanghai Chongming District Smart Hospital Informatics Project, with a contract value of RMB 45 million, and also secured the RMB 57.36 million Digital and Intelligent Medical Consortium Project in Xinchang County, Zhejiang Province. The electromechanical integration project (including smart hospital construction) for the new internal medicine and surgery ward building of Suzhou Municipal Hospital, won by Das Intellitech, reached as high as RMB 235 million.

From a temporal perspective, as smart hospital construction remains in an exploratory phase, the Information Department and enterprise partners must continuously adjust project directions based on actual needs, making it difficult to determine the project timeline. Taking the Jilin University First Hospital Smart Medical Consortium project built by Yilianzhong as an example, the construction period has already exceeded one year, and related requirements are still expanding.

Furthermore, there are significant differences in cost investment among the sub-projects within smart hospital initiatives. Specifically, solutions such as AI-enabled PACS (typically priced at RMB 50,000 per unit), rating-compliant CDSS systems (RMB 500,000–3 million), and hardware upgrades for smart hospitals are relatively mature and easier to implement, resulting in higher gross margins. In contrast, projects such as single-disease CDSS systems and internet hospital platforms suffer from a lack of standardized implementation processes and varying hospital requirements, leading to lower gross margins and longer implementation cycles.

Despite numerous uncertainties, it is clear that tertiary hospitals face mandatory requirements for the graded assessment of smart services. As the electronic medical record (EMR) grading process nears its conclusion, the smart hospital service rating is poised to become the next growth driver for healthcare IT enterprises.

In addition to the two major directions mentioned above, VCBeat has further summarized the development trends of informatization by integrating annual report data, policy trends, and industry trends:

1. Driven by factors such as 5G, AI, and the Internet of Things (IoT), and further accelerated by the COVID-19 pandemic, Hospital Information Systems (HIS) are undergoing a generational upgrade, which may provide IT enterprises with several years of business growth opportunities.

2. The relaunch of the Smart Hospital Service Rating will gradually promote the development of smart hospital construction; however, as current initiatives remain in a pilot phase, IT enterprises will require additional time to accumulate experience and capabilities before benefiting a broader range of hospitals.

3. Although health insurance informatization, electronic medical records (EMR), and laboratory information systems (LIS) are not currently high-profile sectors, they still account for a substantial market size. However, established incumbents in these fields have long since erected high barriers to entry, making it difficult for new entrants to break through.

4. The market potential in the emerging DRG sector remains to be tapped; at this stage, it cannot yet generate significant revenue for health IT enterprises.

5. Imaging AI solutions independently developed by healthcare IT companies can be integrated into PACS at low cost and sold to hospitals at competitive prices, thereby eroding the market share of startups to some extent.

At this juncture, hospitals have not yet fully aligned on the strategic direction for healthcare infrastructure development in the post-pandemic era, and significant uncertainties remain regarding opportunities in health informatization. During this period, enterprises should proactively anticipate future key business directions and strategically position themselves in relevant industries. Once the new landscape takes shape, the healthcare IT sector may undergo transformative changes.