Five Major Shifts in China's Medical AI Landscape in 2020: Insights from Over 40 Industry Stakeholders

“Keep your eyes on the stars and your feet on the ground” is the credo that every innovator and entrepreneur steadfastly upholds.

As a core component of new infrastructure, AI can empower various industries, indicating its immense market potential. Healthcare, being a vital part of the national economy, is inevitably becoming a key arena for AI applications. After years of development, China’s medical AI market reached nearly RMB 30 billion in application scale in 2020, with a compound annual growth rate (CAGR) exceeding 40% over the past five years, classifying it as a high-growth sector. Nevertheless, given the multi-trillion-yuan size of the overall healthcare market, there remains vast untapped potential.

VCBeat Research Institute: Through interviews with 23 entrepreneurs, 10 investors, 5 medical professionals, and 2 device review experts, as well as surveys of 20 companies, we have identified five major changes in medical AI in 2020:

(1) Change 1: Due to the sudden outbreak of the COVID-19 pandemic, AI + public health has become a key focus of new healthcare infrastructure development. AI has played an active role in epidemic monitoring and early warning, imaging-based screening and diagnosis, laboratory testing, vaccine research and development, and the allocation of medical resources.

(2) Change 2: Medical imaging enters a more complex phase, with AI companies achieving breakthroughs by building multi-site, multi-disease screening and diagnostic services or by developing multi-process management solutions centered on single diseases.

(3) Change 3: AI companies empower the development of healthcare systems by providing comprehensive AI-based primary care solutions, comprising AI imaging systems, AI-assisted diagnostic systems, and AI-assisted therapeutic systems.

(4) Change 4: The organizations, systems, and processes for the approval of AI medical devices are undergoing accelerated transformation. Five companies have already obtained Class III medical device certifications, and products from more than ten other companies are currently under certification review. The year 2020 marked the inaugural year of commercialization for medical AI.

(5) Change Five: AI companies are evolving from operating in isolation to providing integrated services. By collaborating with various ecosystem partners—including imaging equipment manufacturers, health IT vendors, third-party medical service providers, and cloud service providers—they leverage complementary resources to deliver integrated solutions to healthcare institutions.

New Infrastructure Builds the Underlying Technical Infrastructure

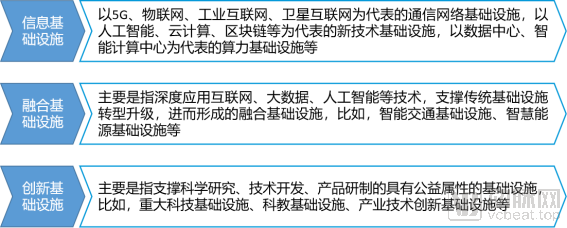

The concept of “New Infrastructure” was proposed at the 2018 Central Economic Work Conference, and since then, the term has frequently appeared in media reports. Traditional infrastructure construction has mainly focused on sectors such as railways, highways, and airports, often referred to as “Tie-Gong-Ji” (an acronym for rail, road, and air). In contrast, “New Infrastructure” is more concentrated on technological innovation fields such as 5G, artificial intelligence, data centers, and the industrial internet, as well as infrastructure supporting upgrades in public consumption related to education, healthcare, and social security.

On April 20, 2020, the National Development and Reform Commission (NDRC) explicitly defined the scope of new infrastructure for the first time. New infrastructure refers to an infrastructure system guided by the new development philosophy, driven by technological innovation, based on information networks, oriented toward the needs of high-quality development, and providing services such as digital transformation, intelligent upgrading, and integrated innovation.

Composition System and Key Content of New Infrastructure; Image Source: VCBeat Research Institute

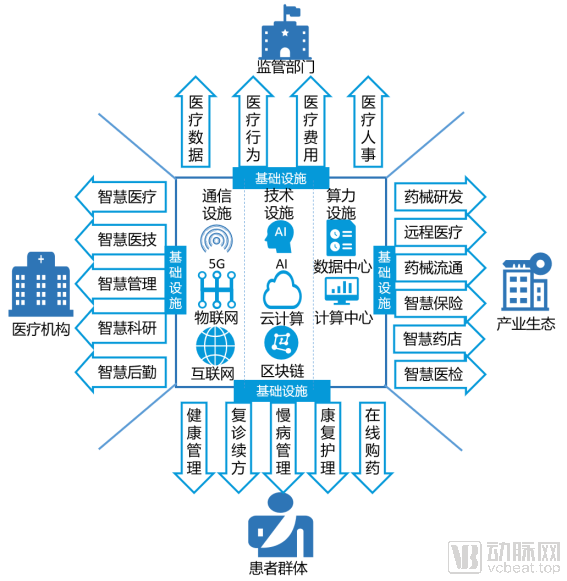

Cross-Facility, Multi-Technology Integration: Empowering the Four Key Stakeholders to Drive New Developments in Healthcare

As a key sector of new infrastructure development, healthcare can fully leverage relevant facilities and technologies to accelerate its own innovative growth. It is evident that AI constitutes a critical component of new infrastructure, necessitating breakthroughs in the healthcare sector across the following three areas:

AI is an integral component of technological infrastructure. Beyond integration with technical infrastructures such as cloud computing and blockchain, it must also converge with communication infrastructures—including 5G, the Internet of Things (IoT), and the internet—as well as computational power infrastructures like data centers and computing centers. For instance, through integration with cloud computing, cloud platforms can collect, store, and analyze electronic medical records, laboratory tests, clinical diagnostics, and other data under authorization, thereby providing substantial high-quality data support for AI model training and fostering superior medical AI products. AI can also integrate with 5G to decentralize diagnostic capabilities to grassroots healthcare facilities with adequate connectivity, thereby enhancing the diagnostic and treatment proficiency of primary care physicians. Furthermore, AI can be integrated with data centers and computing centers, leveraging their robust computational power to develop applications covering all disease types for individual organs.

(1) AI, 5G, and Cloud

From the current perspective, the convergence of 5G, AI, and cloud computing has not yet brought about disruptive changes to the healthcare sector. The advantage of 5G lies in accelerating the volume of data that AI can analyze per unit of time, while the role of cloud computing is to help AI break through the limitations of single devices. By deploying AI on the cloud, it can connect to a broader range of terminals. The integration of cloud computing and AI has already been applied in many medical consortia, particularly for remote CT-assisted diagnosis based on medical consortia during the COVID-19 pandemic. Through this approach, patients no longer need to travel back and forth to large hospitals; they can complete examinations and diagnoses at qualified primary care institutions within the medical consortium. This will effectively triage patients, reduce the workload of tertiary Grade A hospitals, and minimize infection risks associated with patient travel. Patients can receive imaging diagnosis-related information via their mobile phones, which will effectively promote the construction of China’s proactive preventive public health control system.

(2) AI and the Internet of Things

In healthcare, the value of the Internet of Things (IoT) lies in its ability to extend medical data collection from isolated and limited hospital settings to every scenario, including home care, fitness, and travel. While such voluminous and fragmented data hold little value for hospitals, they become highly significant for specialized health management companies once cleaned and processed. These companies can link the data to patients’ health status and leverage it to facilitate disease monitoring. The integration of AI enables these enterprises to adapt their models dynamically based on individual patient conditions, thereby enhancing the analytical capability for multimodal data. This improvement not only boosts the accuracy of related applications but also reduces the service cost per user. Leveraging this efficient data analytics capability, health management companies can establish real-time, high-frequency interactions with users, eventually evolving into engaged communities. Community operators can then seek collaborations with pharmaceutical companies. This model is widely applied in scenarios such as diabetes management and cardiovascular risk management.

AI-enabled healthcare development must provide intelligent services to multiple stakeholders. The construction of smart hospitals for medical institutions involves the intelligent transformation of various domains, including patient care, clinical services (covering outpatient and inpatient care), nursing, medical technology (including pharmaceutical services), management (encompassing administrative and operational aspects), logistics support, teaching and research, and regional coordination. This constitutes a systematic engineering endeavor.

Smart Regulatory Framework for Regulatory Authorities, involving the regulation of medical data, medical practices, healthcare costs, and medical personnel. AI needs to facilitate privacy protection and access control for medical data, ensure the scientific rigor and compliance of medical practices, guarantee the reasonableness and authenticity of healthcare costs, and enhance the flexibility of medical personnel organizations.

Smart Services for the Industrial Ecosystem, providing pharmaceutical companies with clinical research, regulatory submission, and real-world study services; assisting medical device manufacturers in the R&D of AI-powered medical devices; offering internet healthcare providers intelligent consultation, smart prescription renewal, and intelligent patient management services; delivering to insurance companies intelligent distribution, dynamic pricing, and automated claims processing services; supplying pharmacies with smart procurement, prescription fulfillment, and patient management services; and providing third-party medical testing enterprises with imaging and pathology-assisted diagnostic services.

Patient-Oriented Smart Management Development, including health management, online follow-up consultations, chronic disease management, rehabilitation nursing, and online medication purchasing services.

New Infrastructure Fully Supports the Development of the Healthcare Industry,Source: VCBeat

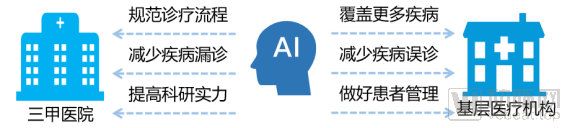

Historically, most AI products have chosen to establish their presence in large tertiary Grade-A hospitals, driven by the abundance of medical data resources, superior physician teams, and stronger payment capabilities. However, given the current distribution of medical resources in China, it is the primary care sector that is in greater need of AI empowerment. Primary care institutions suffer from weak infrastructure, a shortage of medical talent, and suboptimal diagnostic and treatment standards. AI can assist primary care physicians in disease diagnosis, treatment, and patient management, thereby alleviating the imbalance in medical resource distribution. Therefore, while AI empowers large tertiary Grade-A hospitals, it is even more critical to extend this empowerment to the primary care level. The functions of AI should be differentiated across various levels of medical institutions. For large tertiary Grade-A hospitals, the focus is mainly on standardizing diagnostic and treatment processes, reducing missed diagnoses, alleviating physicians’ workloads, and enhancing the hospital’s research capabilities. For primary care institutions, the priority is to improve physicians’ diagnostic accuracy, reduce misdiagnoses, expand coverage for a broader range of diseases, and optimize patient management, thereby encouraging patients to seek care at the primary level.

AI Empowers Tertiary Hospitals and Primary Healthcare Institutions, Image Source: VCBeat

Integrating Peacetime and Wartime Preparedness: Accelerating the Construction of Public Health Prevention and Control Systems

Public health has always been a focal point in the development of China’s healthcare system, encompassing the prevention, surveillance, and treatment of major diseases—particularly infectious diseases such as tuberculosis, HIV/AIDS, SARS, and COVID-19—as well as regulatory oversight of food, pharmaceuticals, and public environmental hygiene, along with related health promotion, health education, and immunization programs.

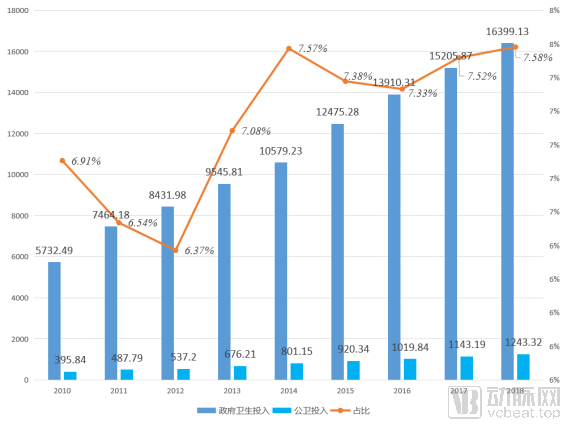

Government Health Expenditure in China, 2010–2018 (in hundred million yuan). Source: China Health Statistics Yearbook.

In 2018, government investment in public health infrastructure reached RMB 124.332 billion, representing a 2.14-fold increase over the preceding decade. Moreover, the proportion of public health infrastructure investment within total health expenditure has shown an upward trend. Nevertheless, given the share of public health investment in total health spending, the development of public health remains a formidable and long-term endeavor.

Public health is a key area covered by the new infrastructure development in healthcare. In particular, the sudden outbreak of the COVID-19 pandemic this year has accelerated public health infrastructure construction. Many provinces have incorporated public health development as a priority project in their three-year plans to address existing weaknesses. Based on the content of public health prevention and control system construction across various provinces and cities, AI can play a significant role in the following five areas:

(1) Monitoring and Early Warning

By leveraging big data on infectious diseases to build surveillance models, it is possible to reconstruct transmission pathways and trace the viral origin; dynamically track affected populations with automated alerts to identify high-risk areas; and simulate and predict future trends, enabling relevant prevention and control authorities to deploy measures proactively.

(2) Screening and Diagnosis

Imaging screening and diagnosis is one of the primary functions of medical AI. Leveraging AI-based image recognition and algorithmic models, it enhances the speed and accuracy of radiologists in interpreting images, facilitates early identification of suspected cases for isolation and treatment, and reduces the risk of disease transmission.

(3) Laboratory Testing

Applications of AI in laboratory testing encompass multiple areas, including digital image-based cell detection, morphometric quantitative analysis, histopathological diagnosis, and prognostic assessment. In the process of computer-based reconstruction of cellular morphology, machine learning is applied directly to compressed waveforms without the need for image reconstruction, thereby enabling efficient image-based, morphology-free cell detection. During histopathological diagnosis, the development of AI analysis modules tailored to different cytopathological orientations can assist in diagnosing various tumor subtypes.

(4) Vaccine R&D

AI algorithms can accelerate virus identification, pharmacological analysis, candidate screening, and clinical trials. For instance, during the development of COVID-19 vaccines, the LinearFold algorithm provided technical support to over 100 research institutions worldwide, reducing the time required for predicting the secondary structure of the SARS-CoV-2 whole genome from 55 minutes to just 27 seconds—a 120-fold increase in speed. This significantly enhanced the prediction speed of the spatial structure of SARS-CoV-2 RNA, thereby shortening the vaccine development cycle.

(5) Regulation and Allocation of Medical Resources

Medical personnel, hospital beds, and supplies must be dynamically allocated during epidemic prevention and control to meet the emergency needs of different regions and medical institutions. AI can provide decision support for the dynamic allocation of medical resources by reflecting in real time the workload of healthcare workers, the number of available beds, and the quantity of diagnostic equipment, while integrating real-time tracking of epidemic trends across various regions.

Medical Imaging Enters Deep Waters: Differentiated Development Seeks Breakthrough

(1) Large Market, High Misdiagnosis Rates, and Abundant Data Drive the Rapid Adoption of AI in Medical Imaging

Medical imaging is the most extensively applied and mature scenario for AI in the healthcare sector. In China, the annual volume of medical imaging examinations exceeds 7.5 billion人次. According to the report "Market Landscape and Industry Development Analysis of Medical Imaging" by Huoshi Chuangzao, the market size of medical imaging in China was projected to reach RMB 600–800 billion in 2020. The substantial examination volume has led to rapid growth in imaging data, with an annual growth rate currently at 30%, whereas the annual growth rate of radiologists during the same period was only 4%, resulting in a significant supply gap. The shortage of radiologists has contributed to a higher misdiagnosis rate. According to misdiagnosis data published by the Chinese Medical Association, the average misdiagnosis rate for malignant tumors is 40%, and that for extrapulmonary tuberculosis exceeds 40%, which is 12 percentage points higher than the overall clinical misdiagnosis rate. Meanwhile, characteristics such as high accessibility, ease of annotation, and relatively high standardization of medical imaging data have substantially lowered the barrier to AI adoption. Consequently, medical imaging has become the primary application market for AI at present.

(2) Severe homogenization, concentrated in pulmonary nodules and fundus imaging

According to the VCBeat database, as of the end of July 2020, there were 89 companies in China specializing in medical imaging and artificial intelligence. In terms of the distribution of imaging-assisted decision-making applications, 72% of these companies focused on pulmonary nodules, and 53% on ophthalmology, making them the two most prevalent application scenarios for imaging examinations.

This is primarily because the resolution of CT images has been continuously improving, while the volume of examinations has been increasing substantially. Similarly, the population undergoing fundus screening is large; the diabetic population alone exceeds 300 million in China. Moreover, fundus cameras are widely available and have become standard equipment in primary healthcare institutions. In addition, both fields feature large data volumes and relatively low annotation difficulty, resulting in low entry barriers for AI companies and facilitating rapid product development. Consequently, numerous enterprises have flocked to develop solutions for pulmonary nodule detection and fundus screening, leading to severe product homogenization. However, fewer than ten companies have successfully entered hospitals and generated revenue.

Distribution of AI Applications for Medical Imaging-Assisted Decision-Making; Data Source: VCBeat Orange Database

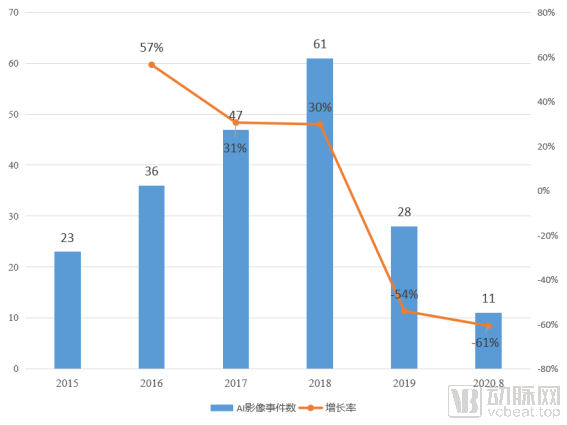

(3) Sharp Decline in Financing Events as Capital Becomes More Rational

VCBeat Research Institute compiled data on the number of financing events in the AI medical imaging sector over the past five years (with 2020 data counted up to September 15). The overall trend in financing activity followed an inverted U-shape. The financing boom in AI medical imaging peaked in 2018, followed by a sharp decline, with year-on-year drops exceeding 50% in both 2019 and 2020. This indicates that the financing frenzy in AI medical imaging has subsided, and investment institutions have become more cautious in selecting innovative enterprises in this field.

AI Imaging Company Financing Trends, 2015–2020; Data Source: Arterial Orange Database

The underlying reasons are as follows:On one hand, the AI medical imaging sector is overcrowded, with severe homogenization of products and services, making it difficult for late entrants to attract interest from investors. On the other hand, investment firms are increasingly favoring companies whose products have already received regulatory approval or are currently under review, as these companies are eligible to participate in hospital tendering and procurement processes, thereby offering more secure investment returns.。

Series A financing serves as a watershed moment in the industry’s development stage. The fact that most companies within the sector are at Series A or later stages of financing indicates that their products or service systems have gained market recognition, established relatively mature business models, and begun to compete with one another in the marketplace. An analysis of AI medical imaging companies that secured funding in 2020 reveals that all were at Series A or later rounds, suggesting that the AI medical imaging industry has entered a growth phase. Consequently, these companies will accelerate product certification applications to gain a competitive edge in the market.

AI Imaging Companies That Secured Financing from January to September 2020, Data Source: VCBeat Orange Database

In the face of a homogenized competitive market, medical imaging companies must break through, move out of the "deep water zone," and pursue a path of differentiated development. Differentiated competitive advantages can be established through the following two directions:First, multi-site and multi-disease screening and diagnosis, such as products covering the screening and diagnosis of multiple sites and organs including the chest, eyes, head, and neck; second, multi-process interventional management centered on a single disease, such as forming a comprehensive management system encompassing screening, diagnosis, treatment, and rehabilitation for cardiovascular diseases.。

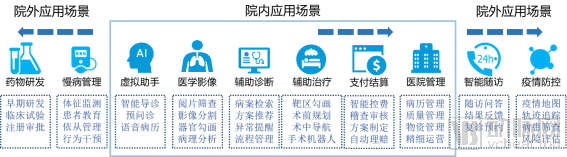

In-Hospital + Out-of-Hospital: Covering More Segments of Healthcare Services

AI applications are primarily concentrated in medical imaging and assisted diagnosis. To better leverage AI’s role in the healthcare sector, it is necessary to expand beyond current application scenarios, including both in-hospital and out-of-hospital settings.

Expansion of AI Application Scenarios Within and Outside Hospitals, Image Source: VCBeat Research Institute

AI application scenarios within hospitals can be extended to assistive therapy, insurance payment, and hospital management.

(1) Adjuvant Therapy

For target volume delineation, AI leverages extensive high-quality, large-scale 3D imaging data, target volume datasets, and expert experience to achieve fully automated organ segmentation. Results are generated in just 2–3 minutes—compared to 2–3 hours for manual delineation by physicians—meeting 90% of clinical needs. Furthermore, the entire delineation process follows model-defined pathways, helping to eliminate inter-physician variability. In preoperative planning, AI algorithms enable rapid segmentation and 3D reconstruction of organs and blood vessels from medical images. This allows physicians to perform personalized, comprehensive quantitative analyses of organs, lesions, and complex internal anatomical structures within a virtual reality environment, thereby enhancing the precision of preoperative planning. During surgery, AI accurately correlates patient imaging data with actual anatomical structures. By leveraging technologies such as VR, MR, and surgical guides, along with 3D digital modeling and algorithm optimization, it enables precise lesion localization. Surgical robots, powered by AI’s robust visual recognition capabilities and combined with 3D stereoscopic vision and multi-degree-of-freedom robotic arms, achieve accurate positioning and flexible movement, assisting physicians in completing surgeries more efficiently and effectively.

(2) Insurance Payment

By learning from extensive data such as clinical guidelines and medical insurance policies, AI constructs a medical expense audit model. This model performs matching analysis on submitted medical expense data, flags unreasonable claims for manual review, and provides support for rational cost control. Meanwhile, leveraging accumulated medical knowledge graphs and algorithms, it comprehensively analyzes the insured’s incidence rates, frequency of examinations and tests, readmission rates, medication usage, and rehabilitation outcomes to determine their risk level. Based on this assessment, insurance companies can launch personalized products and pricing schemes. Furthermore, by integrating big data risk control models with insurance claims rules, the system calculates claim amounts according to the type of risk incurred and the severity of injury, thereby accelerating the claims settlement process.

(3) Hospital Management

In medical record management, the integration of Natural Language Processing (NLP) with knowledge graphs enables the processing of large volumes of complex medical record texts. By learning from medical record management protocols, an intelligent medical record management system can be established to provide timely reminders to physicians who have not entered records by the deadline, flag omitted content in record entries, and issue immediate alerts for inconsistent or non-compliant entries, thereby ensuring the quality of medical record documentation.

AI applications in out-of-hospital settings include drug development, chronic disease management, intelligent follow-up, and epidemic prevention and control.

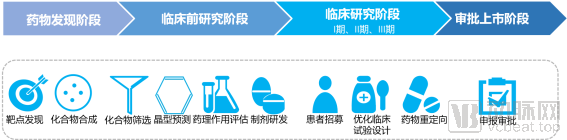

(1) Drug Development

By leveraging its powerful capabilities in relationship discovery and computation, AI can uncover latent associations that are difficult for pharmaceutical experts to detect, thereby constructing deep-level relationships among drugs, diseases, and genes. It enables virtual screening of candidate compounds to rapidly identify those with high potency. Furthermore, AI can extract relevant information from massive volumes of clinical trial data, automatically match trial outcomes with patient profiles to accelerate enrollment, and design optimal clinical trial protocols, thus shortening the overall duration of clinical trials.

Application Scenarios of AI in Drug R&D. Image source: VCBeat.

(2) Chronic Disease Management

AI leverages deep learning to analyze physiological indicators—such as body temperature, blood glucose, blood pressure, blood oxygen saturation, and heart rate—across various value ranges, thereby developing a disease risk identification algorithmic model. By comparing and analyzing data collected from devices against key quantitative metrics, the system identifies potential disease risks. Furthermore, AI utilizes Natural Language Processing (NLP) to analyze and process extensive health education data on chronic diseases, enabling the delivery of customized medical knowledge to patients with different types of chronic conditions to facilitate self-learning. Additionally, AI dynamically monitors and analyzes behaviors related to diet, exercise, sleep, and medication adherence in chronic disease patients, evaluates their health status, and helps them correct unhealthy behaviors, thereby reducing the risk of disease progression.

(3) Intelligent Follow-up

AI can customize follow-up models based on specific requirements, enabling human-computer Q&A through technologies such as voice, visual, and gesture interactions. It can also analyze and process follow-up data to generate results that assist physicians in clinical decision-making. For patients requiring return visits, AI can automatically match them with the appropriate department and recommend optimal appointment times based on their follow-up status.

(4) Epidemic Prevention and Control

AI builds epidemic monitoring models based on big data from the outbreak, dynamically tracking and analyzing data such as the number of deaths, confirmed cases, and suspected cases to generate an epidemic map. Meanwhile, it can reconstruct the movement trajectories of confirmed or suspected patients, identify potential contacts, and facilitate effective isolation. Furthermore, the AI-driven epidemic risk assessment model can evaluate risks based on regional epidemic data and individual temperature readings, thereby identifying high-risk areas and high-risk populations.

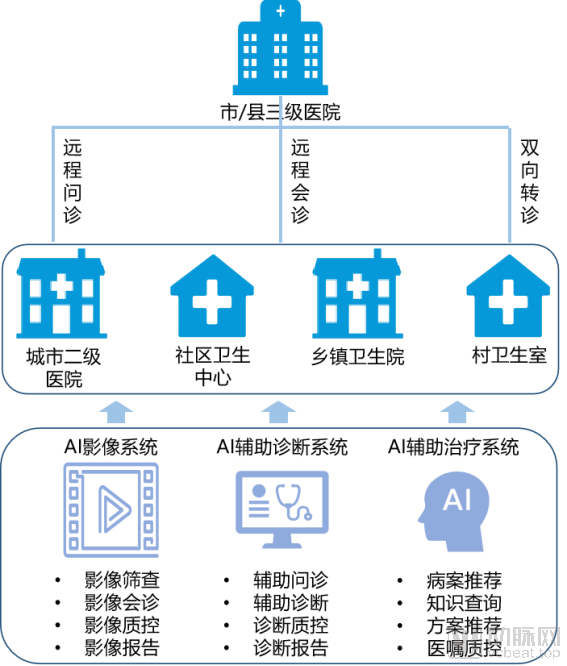

Advancing Tiered Diagnosis and Treatment, Empowering Medical Consortia

The essence of tiered diagnosis and treatment is to integrate the entry points for healthcare service demand. By directing minor illnesses to primary care facilities and major illnesses to hospitals, this model enables medical institutions at all levels to better fulfill their respective roles, thereby improving the overall efficiency of the healthcare system. Medical consortia represent a key initiative in implementing the tiered diagnosis and treatment system.

In August 2016, the National Health and Family Planning Commission (NHFPC), now the National Health Commission (NHC), set specific targets for the development of Medical Alliances in its "Notice on Advancing Pilot Programs for Tiered Diagnosis and Treatment." The goal was to comprehensively promote the establishment of Medical Alliances by 2020, building on pilot experiences, and to form a relatively complete policy framework for such alliances. All secondary public hospitals and government-run primary healthcare institutions were required to participate in Medical Alliances. The development of Medical Alliances has focused primarily on County Medical Communities (CMCs) and Urban Medical Alliances (Urban Medical Groups). To date, China has established 3,346 County Medical Communities and 1,408 Urban Medical Alliances.

County-level medical communities adopt an integrated county-township management model, with county-level hospitals as the lead institutions, township health centers as hubs, and village clinics as the foundation. This model effectively aligns with township-village integration to establish a mechanism for division of labor and collaboration among three-tier healthcare institutions at the county, township, and village levels. Urban medical consortia are led by tertiary hospitals, in partnership with multiple secondary urban hospitals, community health service centers, and other entities, to build “1+X” medical consortia. These consortia vertically integrate medical resources, forming a management model characterized by resource sharing and collaborative division of labor.

The core mission of medical consortia is to enhance the healthcare service capabilities of primary medical institutions, which presents a significant opportunity for the integration of AI with medical consortia.Empower primary healthcare institutions, including urban secondary hospitals, community health centers, township health centers, and village clinics, by building a comprehensive AI-based primary healthcare service solution comprising an AI imaging system, an AI-assisted diagnostic system, and an AI-assisted therapeutic system.。

AI Empowers the Construction of County-Level Medical Consortia and Urban Medical Alliances. Image source: VCBeat.

Multi-party Participation: Parallel Institutional and Organizational Innovation

As previously mentioned, AI plays a critical role in various healthcare scenarios, including imaging screening, disease diagnosis, treatment, payment processing, hospital management, drug R&D, chronic disease management, and epidemic prevention and control. Consequently, there is a clinical demand for AI products that have obtained regulatory approval. These needs are driving policy and regulatory innovation, thereby accelerating the review and approval process for AI products. VCBeat has compiled and systematically organized policies related to the review and approval of AI products.

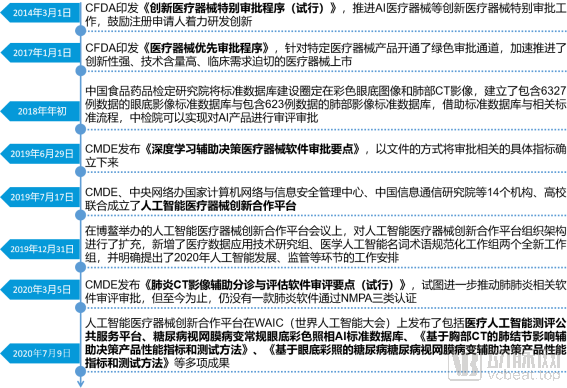

Key Milestones in the Innovative Approval Process for AI Medical Devices, Image Source: Chart by VCBeat

The innovation in the approval of AI medical devices can be traced back to 2014, when the China Food and Drug Administration (CFDA) issued the “Special Approval Procedures for Innovative Medical Devices (Trial)” policy to encourage and accelerate the approval process for AI medical devices.

By early 2018, the National Institutes for Food and Drug Control (NIFDC) of China had established a fundus imaging standard database containing 6,327 cases and a lung imaging standard database containing 623 cases, using three guidelines as the benchmark for database construction: the “Technical Review Guidelines for Medical Device Software Registration,” the “Technical Guidelines for Mobile Medical Device Registration,” and the “Technical Review Guidelines for Cybersecurity in Medical Device Registration.” This standardized approach placed China at the forefront globally. Leveraging these standard databases and related standardized processes, the NIFDC is able to conduct evaluation and approval of AI-based medical products.

However, constrained by the limitations of the era, this database was not sustained for long. The underlying reasons are mainly as follows:First, the data were jointly annotated by hospitals and enterprises. Due to the absence of industry-wide data standards at that time, the data submitted by different companies varied significantly, deviating from real-world conditions. Second, during the evaluation process, enterprises served as both data providers and evaluators, making it difficult to ensure absolute fairness and impartiality in the results. Furthermore, issues such as data volume, data security, and ownership of data benefits have also hindered the subsequent development of this work to some extent.. Consequently, no company has successfully obtained product approval through this database.

The gradual maturation of AI products, coupled with prolonged regulatory approval delays, has placed AI companies in a dilemma. On one hand, AI-powered solutions are indeed becoming an indispensable component of hospital departments in the future; on the other hand, regulatory hurdles have left companies without effective monetization channels, making continuous fundraising an unsustainable long-term strategy.

Since June 2019, the National Medical Products Administration (NMPA) has frequently initiated actions in the formulation of standards for medical AI. On June 29, the NMPA officially released to AI companies the approval-related document “Key Points for the Approval of Medical Device Software Using Deep Learning for Assisted Decision-Making,” thereby establishing specific indicators for approval through this formal documentation.

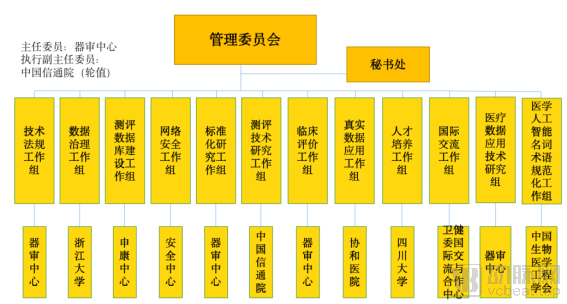

On July 17, 2019, the establishment of the AI Medical Device Innovation Cooperation Platform, along with the subsequent conference held in Boao, expanded the organizational structure of the innovation platform. This provided an authoritative body for the review and approval of AI medical devices, ensuring transparency and fairness in the regulatory process. At this year’s World Artificial Intelligence Conference, the AI Medical Device Innovation Cooperation Platform released several achievements, including the Public Service Platform for Medical AI Evaluation, the Standard AI Database for Color Fundus Photography in Diabetic Retinopathy Screening, “Performance Indicators and Testing Methods for AI-Assisted Decision-Making Products Based on Chest CT for Pulmonary Nodules,” and “Performance Indicators and Testing Methods for AI-Assisted Decision-Making Products Based on Color Fundus Photography for Diabetic Retinopathy.”

Organizational Structure of the AI Medical Device Innovation Cooperation Platform. Image source: CMDE

At the 2020 World Artificial Intelligence Conference (WAIC) held in July, the Innovation Cooperation Platform for AI Medical Devices announced new progress. During the conference, the platform unveiled multiple achievements, including a public service platform for evaluating medical AI, a standard database of conventional color fundus photographs for diabetic retinopathy, “Performance Indicators and Testing Methods for AI-Assisted Decision-Making Products Based on Chest CT for Pulmonary Nodules,” and “Performance Indicators and Testing Methods for AI-Assisted Decision-Making Products Based on Color Fundus Photography for Diabetic Retinopathy.” In brief, this release simultaneously covered three key elements: databases, platforms, and standards. From a structural perspective, third-party evaluation has become feasible, marking a qualitative shift in the momentum driving the regulatory review and approval of AI-based medical devices.

Adapting to the Times: Dynamic Refinement of Review and Approval Key Points

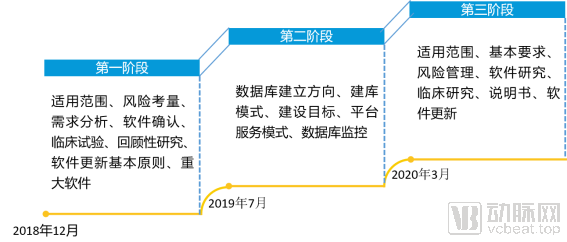

The application process for Class III medical device registration certificates for AI-based medical devices comprises two main stages: preparation of registration submission materials and review and approval, encompassing a total of 11 sections. Medical device registration is an administrative licensing system whereby the National Medical Products Administration (NMPA), in accordance with statutory procedures, systematically evaluates the safety and efficacy studies and their results for the medical device intended for market launch, based on the applicant’s submission, to determine whether to approve the application. In light of the aforementioned innovations in the approval process for AI-based medical devices, changes in key review and approval considerations can be categorized into three phases.

Changes in Key Points for the Review and Approval of AI Medical Devices, Image Source: Chart by VCBeat

(1) Phase I (December 2018–July 2019)

During this phase, the regulatory submission of AI medical devices is based on a classification management system, with specific requirements for registration and filing determined according to the level of risk. In terms of classification management, deep learning-based clinical decision support software for medical devices is subdivided into categories such as medical device data, deep learning, clinical decision support, and medical device software, based on differences in application scope. According to the characteristics of software independence, it is divided into standalone AI software (AI software that constitutes a medical device in itself) and AI software components (AI software embedded within a medical device). Regarding risk considerations, clinical use risk management addresses issues such as false positives and false negatives, and establishes elements, measures, and requirements for risk management.

(2) Phase II (July 2019–March 2020)

The core of this phase lies in an in-depth discussion on database establishment, specifically covering five aspects: direction of database development, database construction models, development objectives, platform service models, and database monitoring. Furthermore, the eight types of test sample databases mentioned at the Artificial Intelligence Medical Device Innovation Cooperation Platform conference include CT lung, CT liver, CT fracture, brain MRI, cardiac MRI, coronary CTA, electrocardiogram (ECG), and ophthalmology. Among these, the AI standard test database for diabetic retinopathy has been established by Peking Union Medical College Hospital.

(3) Phase III (March 2020–)

During this phase, in response to the new demands for AI-assisted diagnostic tools in healthcare driven by the COVID-19 pandemic, the Center for Medical Device Evaluation (CMDE) of the National Medical Products Administration issued the “Key Points for the Review of CT Imaging-Assisted Triage and Assessment Software for Pneumonia (Trial).” The policy clarifies that software for CT imaging-assisted triage and assessment of pneumonia shall be regulated as Class III medical devices. It further requires that such software include at least the following functionalities: abnormality detection, quantitative analysis (e.g., lesion volume proportion, CT value distribution), data comparison (both manual and automated), and report generation. In addition, the policy provides detailed provisions on the volume and sources of training data for AI models, as well as on the overall design of clinical trials.

Three Categories of Scenarios, Five Products Obtain Class III Medical Device Certificates

VCBeat Institute compiled data from the official websites of the National Medical Products Administration (NMPA) and the Center for Medical Device Evaluation (CMDE), identifying five AI-based medical devices that have obtained Class III certification. These products are applied in three clinical areas: cardiovascular diseases, intracranial tumors, and diabetes.

Approval Status of Class III Medical Device AI Products, Data Source: NMPA, CMDE

From the results, it is evident that Keya Medical, Airdoc, and Silicon Intelligence all obtained approval for Class III medical device certificates after passing through the green channel. For companies seeking to accelerate the approval process, the green channel may be a favorable option.

According to policy regulations, VCBeat has outlined three core requirements for companies seeking to access the fast-track channel:

(1) Identify Suitable Application Scenarios

Many existing imaging devices—such as CT, MRI, color Doppler ultrasound, ECG, EEG, and X-ray—have incorporated AI to varying degrees. However, for AI to truly deliver value, companies must avoid the trap of equating “one feature” with “one product.” For instance, when a patient presents with fever and headache, physicians often cannot immediately determine the specific underlying condition. If an MRI-based AI product offers only a single function, such as detecting intracranial hemorrhage, it fails to meet clinical needs. Instead, physicians require AI solutions that provide comprehensive, “all-disease” coverage for at least a specific anatomical region. This represents a key development trend and one viable pathway for designing clinical trials. Current market dynamics indicate that only products capable of diagnosing multiple conditions across multiple body sites can satisfy hospital requirements and proceed through the regulatory approval process.

(2) Select Valid Data

From the perspective of existing algorithmic mechanisms, if AI products are trained using effective data from primary care settings, their performance ceiling will be limited to general applications in primary healthcare, making it impossible to extend their utility to large tertiary hospitals. There is a significant disparity in the diagnostic capabilities for diseases such as breast cancer and brain tumors across hospitals of different tiers. Indiscriminate selection of training data may lead to decreased accuracy with increased training volume. Therefore, for medical AI to be successfully implemented in Grade A tertiary hospitals, it must leverage high-quality data from top-tier institutions and deeply learn the “gold standard” clinical expertise of leading specialists to ensure diagnostic accuracy.

(3) Creating algorithmic barriers to entry

For a long time, the barriers to entry in AI-driven healthcare were not particularly pronounced—companies could catch up and even surpass incumbents simply by securing high-quality data. However, this landscape has now changed. Many AI enterprises have found that as they expand toward comprehensive coverage of all disease types, single-task deep learning algorithms can no longer meet the demand, making multi-task algorithms the prevailing trend. Therefore, beyond continuing to compete for high-quality, effective AI data, medical AI companies must seek breakthroughs at the algorithmic level in the next phase.

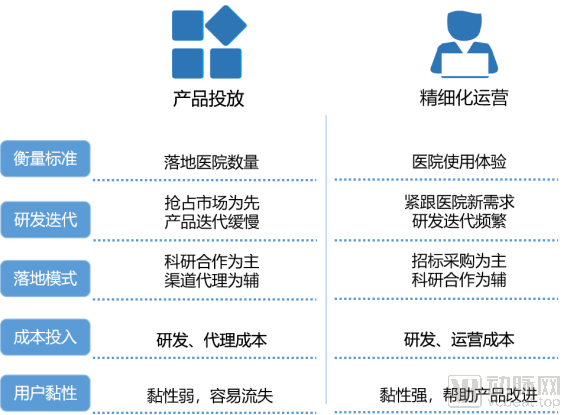

From Wild Expansion to Meticulous Cultivation: Emphasizing Product Operations

The so-called “deployment” of most medical AI products merely involves installing software in a specific hospital department, completing interface integration with device manufacturers, and establishing partnerships with pharmaceutical companies. However, there is still a considerable gap before true commercialization is achieved. Therefore, we refer to this phase as the product launch stage, which also represents the period of wild, unregulated growth for medical AI.

The earliest phase of product deployment can be traced back to IBM’s Watson robot. During this stage, researchers developing medical AI were rarely from medical backgrounds, leading to a misalignment between the designed products and actual clinical needs, leaving substantial room for improvement. Medical AI products entered hospitals primarily to access corresponding clinical data for product testing, thereby identifying directions for subsequent iterations. Consequently, scientific research collaboration became the mainstream business model for commercializing these products, supplemented by channel distribution and hospital relationships. For instance, companies established teams to assist physicians in the Information and Radiology Departments with publishing SCI-indexed papers. The medical imaging auxiliary diagnostic software that emerged in 2015 predominantly adopted this business model: initial products were deployed in hospitals to train AI algorithms using large volumes of physician-annotated imaging data, thereby refining the early-stage products. However, such refined products addressed only specific workflow segments, meaning the resulting AI solutions possessed limited, single-function capabilities and failed to adequately meet physicians’ broader clinical needs.

As collaborations and exchanges with hospitals have increased, enterprises have begun to understand the genuine needs of hospitals and have reformulated their product R&D strategies accordingly. During this phase, a growing number of medical experts have joined AI companies, fostering a true integration of internet-driven AI and clinical medicine. Leveraging years of clinical practice, medical experts possess deep insights into the types of AI products hospitals require. Meanwhile, AI experts, backed by extensive technological accumulation, can design corresponding products through technical means once clear directions are established. This shift ensures that product development is guided by clinical needs, creating a synergistic effect between medical and AI experts.

By 2018, numerous AI products had matured after extensive refinement, and corporate business philosophies had shifted. Building on the earlier strategy of mass product deployment and widespread hospital coverage, companies began to focus on the operational implementation of these solutions.

Numerous factors have triggered this phase. In addition to product maturation, policy advancements have significantly facilitated the transition of medical AI from unchecked expansion to refined, intensive development, marking a shift toward a stage focused on generating revenue through operations. For instance, innovations in approval policies have accelerated the regulatory clearance of AI products. Currently, five products have obtained Class III medical device certificates, with several others undergoing review and approval, poised to receive certification within the year. Furthermore, requirements such as Electronic Medical Record (EMR) grading and Interconnectivity grading mandate that hospitals transform into "Smart Hospitals." This transformation entails achieving hospital-wide information sharing and incorporating medical decision support capabilities, thereby accelerating the deployment of Clinical Decision Support Systems (CDSS). The integration of AI with CDSS enables these systems to better comply with relevant policy requirements. Although traditional CDSS platforms can partially meet grading criteria, AI-enhanced CDSS offers distinct advantages for achieving EMR Grades 4, 5, and 6. By leveraging AI technologies such as deep learning, Natural Language Processing (NLP), and knowledge graphs, these systems provide intelligent medical knowledge retrieval, similar case recommendations, diagnostic test suggestions, and treatment plan recommendations during disease diagnosis and treatment, thereby offering multi-layered support for medical decision-making. Consequently, policies have effectively driven the commercialization of AI+CDSS. Additionally, as local Health Commissions increasingly emphasize tiered diagnosis and treatment, grassroots-level AI+CDSS solutions are opening up a new blue-ocean market for AI enterprises.

At this stage, it is difficult for the vast majority of enterprises to achieve sustainable and stable revenue through simple product placement. They need to shift their business philosophy and focus on refined operations. Enterprises should deploy professional operational teams to hospitals to guide physicians on how to better utilize the products. Additionally, a rapid response mechanism must be established to address issues encountered by physicians during product use and provide timely solutions.

Comparison of AI Product Launch and Refined Operations, Image Source: VCBeat.

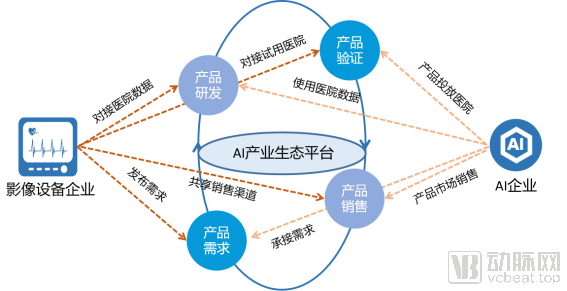

From Solo Efforts to Integrated Services: Achieving Industrial Synergy

In the early stages of medical AI development, industry participants—including AI companies, medical device manufacturers, health IT vendors, and cloud service providers—operated in silos. This fragmented approach resulted in AI enterprises having insufficient industry insight, limited sources and volumes of data acquisition, and narrow sales channels for their products.

After several years of development, the primary arena of competition in the medical AI industry is gradually shifting from “head-to-head rivalry” to “collaborative competition.” Enterprises need to cultivate a mindset of resource integration, complementary advantages, and mutual support; they should transform their perspectives, identify their strategic positioning, and achieve synergistic development through platform-based models; furthermore, they should engage in cross-sector collaboration and joint innovation to reduce the costs and risks associated with innovation.. Various medical AI companies are establishing partnerships with imaging equipment manufacturers, health IT vendors, and healthcare service providers, forming new alliances to compete in the industry.

(1) AI Companies + Imaging Equipment Manufacturers

Imaging equipment manufacturers leverage their advantages in hardware, hospital resources, and market channels to build ecosystem platforms. Medical AI companies participate in selection processes to join these platforms, becoming both developers and users within the ecosystem. A review of AI platform development by imaging equipment manufacturers indicates that the primary players are currently large domestic medical device manufacturers and imaging research institutions.

Product Requirements Phase: Imaging equipment manufacturers distribute customer requirements for AI products, and AI companies claim these requirements from the ecosystem platform for product development based on their product positioning and technical advantages.

Product R&D Phase: By leveraging hospital resources, imaging equipment manufacturers have cultivated deep roots in the healthcare industry for many years and amassed a substantial base of high-quality hospital clients. During AI model training, these manufacturers can facilitate collaborations with hospitals across different regions and of various types, which provide AI enterprises with extensive datasets. Furthermore, these hospitals boast a wealth of expert resources capable of delivering data annotation services, thereby helping AI companies develop AI products with strong generalization capabilities.

Product Validation Phase: Hospital clients of medical imaging equipment manufacturers can serve as the initial beta testers for AI products. Given their large patient populations, these products can be deployed across patients with diverse clinical conditions to validate their accuracy. Finally, hospitals provide feedback on issues encountered during the trial period and the resulting outcomes to AI companies, facilitating more effective upgrades and iterations of prototype products.

Product Sales Phase: Imaging equipment manufacturers have well-established product sales channels, which AI companies can leverage to market their products. This approach not only boosts product sales but also reduces costs associated with channel development and agency partnerships, thereby increasing corporate profits.

By collaborating with medical imaging equipment manufacturers, AI healthcare companies can share resources such as customer bases, partners, and sales channels, thereby establishing a closed-loop service for product requirement analysis, research and development, validation, and commercialization.

Collaboration Models Between AI Companies and Imaging Equipment Manufacturers, Source: Chart by VCBeat

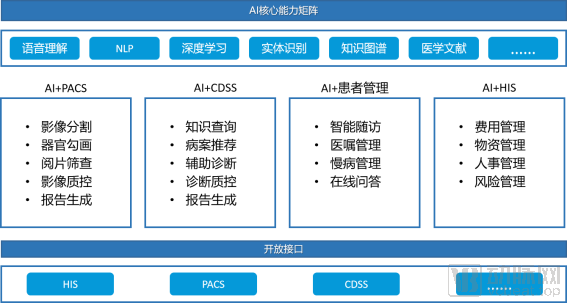

(2) AI Companies + IT Solution Providers

By integrating technologies such as deep learning, image recognition, natural language processing (NLP), and knowledge graphs with the information systems provided by hospital IT vendors, medical AI companies can enhance the data analytics and decision-support capabilities of these systems, thereby significantly improving their operational efficiency.

Collaboration Models Between AI Companies and IT Vendors, Image Source: VCBeat.

By leveraging open interfaces, the AI system integrates with information systems such as PACS, CDSS, and HIS, enabling its core capabilities to be embedded into the daily operations of these systems. Specifically, it can deliver services in the following four areas:

AI+PACS:PACS is an integrated system for the acquisition, display, storage, transmission, and management of medical images. AI can perform tasks such as image segmentation, organ delineation, imaging screening, and image quality control, thereby improving reading efficiency and reducing physicians' workload.

AI+CDSS:A Clinical Decision Support System (CDSS) is a system that leverages available and appropriate computer technologies to improve the efficiency of medical diagnostic decision-making for semi-structured or unstructured medical problems through human-computer interaction. AI can process large volumes of unstructured data to construct knowledge graphs, providing physicians with capabilities such as knowledge querying, recommendation of similar cases, and assisted diagnosis. Furthermore, it can offer standardized reminders throughout the diagnostic workflow, thereby enhancing the standardization and accuracy of diagnoses.

AI+Patient Management: Patient management is also a crucial component of hospital information technology infrastructure, encompassing post-consultation follow-ups, medical order management, chronic disease management, and patient consultations. AI can engage patients through intelligent question-and-answer interactions to address routine inquiries, thereby facilitating better self-management for patients and reducing the time physicians spend on administrative tasks. This allows healthcare providers to devote their primary attention to the diagnosis and treatment of diseases.

AI+HIS: The Hospital Information System (HIS) primarily leverages computers and communication equipment to provide departments within the hospital with capabilities for collecting, storing, processing, retrieving, and exchanging patient diagnosis and treatment information as well as administrative management information, thereby meeting the functional needs of all authorized users. AI can facilitate intelligent verification and fee settlement in pricing and billing processes; furthermore, AI can intelligently monitor diagnostic and therapeutic items and charges in accordance with Diagnosis-Related Groups (DRGs) regulations, thereby reducing the incidence of overtreatment.

(3) AI Companies + Third-Party Medical Service Providers

Third-party medical service providers primarily refer to enterprises that collaborate with AI companies to jointly deliver medical services to healthcare institutions or individuals. These providers mainly offer services such as disease diagnosis and treatment, pharmaceutical services, health check-ups, health management, hospital management, and clinical drug trials. Meanwhile, AI companies primarily empower these medical service providers by leveraging technologies such as speech recognition, image recognition, natural language processing (NLP), and knowledge graphs, thereby enhancing the quality and efficiency of healthcare services.

(4) AI Enterprises + Cloud Service Providers and Telecommunications Operators

While having hospitals serve as the payers is certainly an ideal choice, in practice, it is within primary healthcare settings that AI can truly realize its value. Judging by the current product design philosophy of imaging-based AI solutions, the lowest-level payer capable of affording them extends down to county-level hospitals. Two factors hinder the further penetration of AI into lower-tier facilities: first, there is a limited number of imaging professionals at the grassroots level, with few qualified radiologists willing to remain in these areas. More importantly, primary healthcare institutions lack the financial capacity to pay for enterprise services.

The above is“The Way and Wisdom of Medical AI Innovation: Returning to Needs, Integrating Value”Excerpt from the report, in which we also analyzed Yidu Cloud, Lingyi Zhihui, and Deepwise Medical,OrionStar,Case studies of 10 medical AI companies, including Ruixin Medical, HLT (Happy Life Technology), Keya Medical, Deshang Yunxing, Yizhun Intelligence, and Shukun Technology. The complete framework of the report is as follows; scan the QR code to access the mini-program and read the full report for free:

Report Contents:

I. New Infrastructure Forges a New Landscape for Medical AI

1.1 New Infrastructure Builds the Underlying Technical Foundation

1.2 Cross-Facility, Multi-Technology Integration: Empowering the Four Key Stakeholders to Drive New Developments in Healthcare

(1) Cross-boundary emergence of new capabilities

(2) Multi-stakeholder collaboration to create new scenarios

(3) Multi-tiered Approach to Enhance Coverage

1.3 Integrating Peacetime and Wartime Needs: Accelerating the Construction of Public Health Prevention and Control Systems

II. From Hype to Stealth: Iterative Expansion of Application Scenarios

2.1 Medical Imaging Enters Deep Waters, Seeking Breakthroughs Through Differentiated Development

(1) Large Market, High Misdiagnosis Rates, and Abundant Data Drive the Rapid Application of AI in Medical Imaging

(2) Severe homogenization, concentrated in pulmonary nodules and fundus imaging

(3) Sharp Decline in Financing Events as Capital Becomes More Rational

(4) Seeking Breakthroughs and Differentiated Development

2.2 In-Hospital + Out-of-Hospital: Covering More Segments of Healthcare Services

(1) Expansion of In-Hospital Scenarios: From Screening and Diagnosis to Treatment and Payment

(2) Expansion into Out-of-Hospital Settings: Drug R&D, Chronic Disease Management, and Epidemic Prevention and Control Emerge as New Growth Frontiers

2.3 Advancing Tiered Diagnosis and Treatment to Empower Medical Consortiums

III. Clinical Needs Drive Accelerated Approval, with Five Products Granted Class III Certifications

3.1 Multi-Stakeholder Participation: Parallel Advancement of Institutional and Organizational Innovation

3.2 Adapting to the Times: Dynamic Refinement of Review and Approval Key Points

3.3 Three Types of Scenarios, Five Products Obtain Class III Certificates

IV. Advancing the Business Model to Forge a New Competitive Ecosystem

4.1 From Wild Growth to Meticulous Cultivation: Emphasizing Product Operations

4.2 From Solo Efforts to Integrated Services: Achieving Industrial Synergy

(1) AI Companies + Imaging Equipment Manufacturers

(2) AI Companies + IT Solution Providers

(3) AI Companies + Third-Party Medical Service Providers

(4) AI Companies + Cloud Service Providers and Telecommunications Operators

V. Looking Ahead: Where Is Medical AI Headed?

Special thanks to the following industry professionals for their strong support of this report (listed in no particular order):

Yan Jun, Chief AI Scientist at Yidu Cloud

General Manager, Baidu Smart HealthcareHuang Yan

Qiao Xin, Co-founder and CEO of Deepwise AI

Zheng Lingxiao, Founder and CEO of Ruixin Medical

Peng Tao, Chief Data Scientist at Happy Life Technology

Cao Kunlin, President of R&D at Keya Medical

Yan Yeen, Executive President of Deshang Yunxing

Lv Chenchong, Founder and CEO of Yizhun Intelligent

Liu Dan, Executive Director of CDH Investments

Le Belin, Investment Director at Gaorong Capital

Cheng Miaoqi, Partner at Qingsong Fund