Beyond Regulatory Approval: The Next Frontier for Medical Imaging AI

Recently, the “2nd China Medical Imaging AI Conference” was successfully held in Shanghai as scheduled. This is the first conference themed around medical imaging this year; by the time it took place, autumn had already arrived.

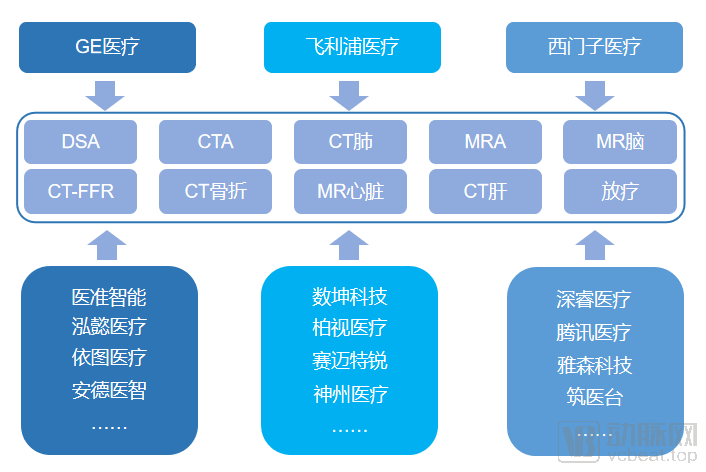

The conference was not large in scale, yet it bore some resemblance to the current state of AI in medical imaging. In the exhibition area, GE Healthcare, Philips, Siemens, and United Imaging occupied the largest and most central spaces. Startups focusing on AI, such as Neusoft Medical, Shukun Technology, Keya Medical, Ande Yizhi, Huiyi Huiying, Yitu Healthcare, Deepwise, Infervision, and Yizhun Smart, also participated actively, alongside other companies involved in medical imaging, including Bayer, Fujifilm, Shimadzu, and Canon. The AI commercialization pathway centered on device manufacturers is showing a trend toward becoming mainstream.

However, from a product perspective, even after a year, the products showcased by various companies can hardly be considered new. Having weathered the pandemic, medical imaging AI appears to have indeed encountered certain challenges.

Looking Ahead: What Development Trends Will Medical Imaging Face After the Capital Tide Recedes?

Regulatory review and approval have been the major events in the AI medical imaging sector this year. Since January 2020, companies such as Keya Medical, Ande Yizhi, and Airdoc have successively obtained Class III medical device certifications. However, due to factors including the impact of the pandemic and unclear business models, the “winter” in the AI imaging industry has not abated despite the progress in regulatory approvals.

From the perspective of capital market preference, there were a total of 19 investment events related to global imaging AI in 2020, with 10 overseas and 9 in China, totaling 1.56 billion yuan (VCBeat Orange Database). Among these 9 cases, Shukun Technology and Keya Medical each secured financing twice. In particular, Shukun Technology raised a total of 400 million yuan across two rounds, accounting for more than one-quarter of the global financing amount. The head aggregation effect in this market is very pronounced.

So, what role has regulatory approval actually played in the development of AI medical imaging?

He Weigang, Director of Department II at the Center for Medical Device Evaluation of the National Medical Products Administration (NMPA), stated in his conference speech: “A medical product undergoes a complete lifecycle from development, through input/output processes, verification, and validation, to final market launch. Even after a product receives approval and enters the market, it has not cleared all hurdles, as post-market surveillance remains a critical regulatory phase. For instance, among medical AI products approved by the U.S. Food and Drug Administration (FDA), many have been subject to recalls due to issues identified during post-market use.”

Therefore, the significance of regulatory approval lies in facilitating quality control for AI products. If an AI product is indeed free of quality issues, the approval process will not hinder the clinical implementation of medical AI. However, if one must address the negative impacts caused by prolonged delays in obtaining approval,This refers to the issue that products lacking Class III medical device certification cannot be included in hospitals’ fee schedules.Dr. Cao Kunlin, President of R&D at Keya Medical, told VCBeat that companies may need six months or even longer to negotiate inclusion in the reimbursement catalogs across various provinces and municipalities. However, given that several years have already passed, do AI enterprises really lack this additional half-year?

Therefore, in the words of Minister He Weigang: “Medical AI is not stuck at the approval stage.”

So, where is medical AI stuck?

Generally, product design philosophy should follow users' core needs, but the starting point for medical imaging AI has not fully aligned with this logic. The abundance of publicly available imaging data for pneumonia has become a significant reason why many companies have developed products for pulmonary nodules.

However, although the pneumonia product has long reached maturity and is widely used in hospitals—making it a truly implemented solution for radiology departments—it has not generated substantial profits for the company due to factors such as intense competition, the lack of Class III medical device certification, and a free-to-use market entry strategy.

In fact, to achieve effective commercialization, one must either accurately identify healthcare needs or precisely pinpoint the needs of partners. Many AI companies have become stuck at this very stage.

The demand for medical applications is reflected in the approval process; the regulatory pathway for AI products inherently includes an assessment by the approving authorities of the product’s clinical utility.

Liang Weimin, Chairman of Ande Medical Intelligence, once described the validity of clinical trials as follows: “In evaluating the efficacy of clinical trials, non-inferiority trials are designed to determine whether one drug is not inferior to another. Such trials are commonly used in clinical studies with objective efficacy endpoints, such as clinical outcomes for antimicrobial agents, adverse events in cardiovascular therapy, and death or disease progression in oncology treatment. In contrast, superiority trials are designed to determine whether one drug is superior to another and are generally employed in trials using placebo as the control.”

“In the approval process for medical artificial intelligence devices, while the definitions of non-inferiority and superiority differ in form, they are similar in essence. To demonstrate either superiority or non-inferiority, an AI product must prove that it has clinical application value or offers advantages over existing products.”

Therefore, to gain approval, existing products must demonstrate clear superiority over current offerings or address unmet needs that existing products fail to resolve.

One of the key factors enabling Keya Medical to become the first company to obtain a Class III medical device certification for an AI product was its ability to address critical clinical needs while achieving superior efficacy through innovation. Cao Kunlin stated that prior to the integration of AI technology, performing a CT-FFR analysis in hospitals took 3–8 hours. In contrast, Keya Medical’s “DeepVessel FFR” reduces this time to under 10 minutes, representing a qualitative improvement in medical efficiency.

Shukun Technology’s CTA product, which passed the special review for innovative medical devices in 2019, follows a similar logic. In traditional imaging examination and diagnosis, such as cardiac CTA, physicians require at least 30 minutes to one hour to complete the workflow of “scanning–post-processing–diagnosis–initial report writing–report review,” while patients need to wait 1–3 days to receive the report. Empowered by AI, Shukun Technology can shorten this timeframe to just a few minutes, integrating the examination and diagnostic processes to make the entire workflow automated and intelligent.

Identifying such market needs is no easy task. Both companies entered the field of cardiovascular AI at the dawn of the AI boom, gradually refining their data collection processes and spending years to develop mature products. Similarly, Ande Medical Intelligence secured the first Class III medical device certificate for AI-assisted diagnosis by leveraging its years of accumulated expertise in brain science. This demonstrates that developing AI solutions requires deep integration into clinical workflows.

Companies like Keya Medical entering hospitals through fee schedules is indeed a viable commercialization model, but is it the best one? For different AI products, the answer is not unique.

“In all likelihood, the future deployment of artificial intelligence will depend on medical device companies.” At the conference, a medical device industry practitioner stated that he believed the model of enterprises entering hospitals one by one through their own sales capabilities might not be viable, given that imaging AI companies still need to face long-term maintenance costs after implementation in hospitals.

The market is indeed moving in this direction. It is no longer novel for medical device giants to establish medical imaging AI divisions in pursuit of comprehensive intelligent transformation. To date, GPS and United Imaging have both been building their own AI ecosystems, and this trend continues to advance.Medical AI needs to accurately identify the needs of its partners.

Philips incorporated big data and AI-driven adaptive intelligence into its corporate strategy as early as seven years ago, with 60% of related investments allocated to software development. Currently, 25% of Philips’ scientists are engaged in more than 250 research projects related to AI and big data, making the company one of the top patent holders in the field of AI-enabled healthcare. Nevertheless, the achievements of this health technology giant remain only a drop in the bucket within the broader medical landscape.

Dr. Zhou Zhenyu, Clinical and Technical Lead of the Integrated Solutions Center for Greater China at Philips, told VCBeat: “Philips currently has over 100 productized modules, but these still cannot cover the diverse needs of physicians. Therefore, we also hope to identify AI companies operating within specific clinical scenarios and collaborate with them through the establishment of the ISAI ecosystem to enhance our product portfolio.”

“To date, we have evaluated more than 1,100 AI companies, fewer than 300 of which are closely associated with medical imaging equipment. We categorized these companies into radiology, radiation therapy, interventional procedures, and other segments. Ultimately, the number of qualifying companies was very limited, as we require that their AI solutions be deployable in specific clinical scenarios that effectively address current pain points in clinical practice and medical technology.”

Consequently, only a select few companies have become Philips partners, with Shukun Technology, mentioned above, being one of them. Philips has stated that Shukun can reduce the time required for CT coronary angiography—from image acquisition and post-processing to the generation of structured reports—by up to 80%. This significant efficiency gain will effectively bolster Philips’ “hardware-software integration” strategy, enabling an end-to-end solution for coronary artery examinations. Furthermore, by leveraging Philips’ equipment ecosystem, Shukun Technology will be able to accelerate its commercial deployment.

United Imaging Intelligence’s strategy differs from that of traditional equipment manufacturers (such as GPS) and AI startups. Zhou Xiang, Co-CEO of United Imaging Intelligence, stated, “On one hand, leveraging the comprehensive ecosystem of United Imaging Group, we can empower devices at the hardware level; on the other hand, we will independently explore the medical imaging AI market. The ‘integration of software and hardware’ enables optimization at the source of image acquisition, more thoroughly helping physicians address challenges encountered in clinical practice. This means that our ‘software-hardware integration’ will be more sustainable and closely coupled.”

Collaborating with imaging equipment manufacturers is an effective go-to-market strategy for startups. However, for medical device companies—whether the “GPS” giants (GE Healthcare, Philips, and Siemens Healthineers) or United Imaging Healthcare—the vision of a comprehensive AI ecosystem will be difficult to realize if there is no sustained talent pipeline in AI-driven healthcare.

In addition to the two development pathways mentioned above, AI startups are also exploring personalized growth models, with research platforms emerging as a highly effective win-win approach.

In an interview, Professor Shen Dinggang, Co-CEO of United Imaging Intelligence, stated: “AI-driven research on disease types exhibits a long-tail distribution. Conditions with large data volumes, such as pulmonary nodules and fundus diseases, occupy the head of the curve; these are easier to develop products for, have high demand, and attract numerous companies. In contrast, the vast majority of other conditions lie in the tail, characterized by a lack of standardized data, limited hospital demand, and very few companies engaged in this space.”

“In such cases, companies are reluctant to engage with these disease areas, but physicians have research needs to standardize data for these conditions and build deep learning models, so we provide them with supportive tools,” said Shen Dinggang. “Meanwhile, through collaboration with physicians, we may also identify new application scenarios from their research.”

To date, research platforms have matured significantly, with both medical device manufacturers and AI companies offering corresponding products. However, developing a high-quality platform is no simple task; only by understanding physicians’ research workflows and habits for specific disease areas can companies create truly sticky products. From this perspective, there is still much work to be done.

Based on clinical application scenarios, reverse-engineering R&D positioning has made identifying suitable partners a promising approach. Taking cerebrovascular disease as an example, stroke remains the leading cause of death in China, creating substantial demand for AI-enabled clinical applications. Recently, GE Healthcare has been collaborating with AI companies both domestically and internationally to comprehensively enhance the treatment capabilities for this critical condition.

During the conference, GE HealthCare announced a collaboration with Hongyi Medical to integrate the RapidAI intelligent stroke imaging analysis platform, distributed by Hongyi Medical in China, into the Edison digital health ecosystem. This integration aims to enhance rapid quantitative analysis capabilities for multimodal stroke imaging based on precision imaging. The combined strengths of both parties yield a comprehensive stroke solution that assists physicians in efficient patient screening, expands the population of beneficiaries, improves the quality of care for patients presenting beyond the standard time window, and enhances prognostic outcomes.

In recent years, precise patient selection and the formulation of individualized treatment plans using multimodal imaging technologies have become a breakthrough in the diagnosis and treatment of stroke. The DAWN and DEFUSE 3 international clinical trials, supported by RapidAI in 2018, confirmed that patient selection via multimodal imaging could extend the time window for endovascular therapy from the original 6 hours to 24 hours. Accordingly, both international and domestic guidelines for the diagnosis and treatment of acute ischemic stroke have been updated: for patients with acute ischemic stroke presenting 6–24 hours after onset, if there is a large vessel occlusion in the anterior circulation and the enrollment criteria of the DAWN or DEFUSE 3 studies are met, mechanical thrombectomy is recommended, thereby ushering in a new era in the management of stroke patients beyond the traditional time window.

Beyond the competition among enterprises, the conference has allowed us to witness the significant contributions of physicians to the AI industry itself. At the event, ten radiology experts from hospitals participated in the launch ceremony for the construction of a radiological imaging database.

Yang Aiping, Director of the Center for Capacity Building and Continuing Education under the National Health Commission, stated at the launch ceremony that the Center had initiated work on its overall business system architecture in 2015, known as the “One Database, Two Platforms” framework.

The “Two Platforms” refer to: the National Distance Continuing Medical Education Platform for healthcare professionals, and the National Distance Modern Hospital Management Capacity Building Platform for hospital administrators of all types; the “One Database” refers to a medical image database that supports the content of the two distance education platforms.

Taking the ultrasound specialty as an example, the database has collected data on five organs, 59 diseases, and thousands of cases. Building on this foundation, the center has expanded its efforts to establish databases for hepatobiliary tumors, radiological imaging, and ophthalmology. Throughout the database development process, the center has consistently adhered to the following characteristics:

First, the clinical reasoning characteristics of data: based on the collection, processing, and storage of data across the entire process, all stages, and the full chain of disease diagnosis and treatment, directly reflecting the most authentic clinical application needs;

Second, dynamic data collection involves continuously gathering the most up-to-date clinical data to ensure that disease categories and modalities within the database remain current.

Third, precise data annotation tailored to the needs of deep learning in computing, providing accurately annotated scientific data;

Fourth, validation of data applications: leveraging data resources to enhance medical care and diagnosis, thereby unlocking the value of data.

Following the launch of this radiology image repository initiative, the Center will further collaborate with CAIERA to strengthen multi-organ and multi-task annotation capabilities and establish additional subspecialty working groups.

Following the ceremony, the Alliance engaged with numerous artificial intelligence enterprises to discuss the requirements and challenges associated with database construction, aiming to ensure that these companies derive tangible benefits from the development of third-party databases.

Overall, despite certain challenges, medical imaging AI continues to advance in a positive direction. Liu Shiyuan, who serves as the Conference Chair, Chairman of the China Medical Imaging AI Industry-Academia-Research-Application Innovation Alliance, and Director of the Department of Radiology at Shanghai Changzheng Hospital, summarized the development of AI in his speech. He believes that,As regulatory approvals advance, capital becomes more rational, and corporate research deepens, medical imaging AI is progressing in a positive direction. In the future, trends in AI development will include multi-disease applications, end-to-end workflow integration, platform-based solutions, hardware-software integration, and online-offline convergence.

Therefore, the medical imaging AI market, bolstered by rational capital support, the participation of numerous chief physicians, and national policy backing, may maintain the status quo in the short term. However, in the long run, the seeds sown in recent years have gradually taken root and begun to sprout; with a little patience, we may yet see abundant fruits.