Ringing the Bell on the HKEX: Zai Lab Re-enters the Capital Markets with a Dual Listing

Zai Lab

Innovative Global Biopharmaceutical Company

Three years after its listing on the Nasdaq in the United States, Zai Lab pursued a secondary listing in Hong Kong. Interestingly, it also took three years from the company’s founding to its IPO on the U.S. stock market. With this Hong Kong listing, Zai Lab has once again embarked on a new three-year journey. On the 28th, as part of a global issuance of 10.6 million new shares, Zai Lab celebrated its first trading day on the Hong Kong Stock Exchange. The opening price was HK$613.5, representing a 9.16% increase over the offer price of HK$562. As of press time, the real-time share price of Zai Lab-SB (09688) stood at HK$607.5, up 8.1%. In the grey-market trading on September 25, the closing prices for Zai Lab’s shares across various grey-market platforms were slightly higher than the public offer price by approximately 1%.

Zai Lab-SB Real-Time Quotes (Data Source: Futu NiuNiu)

Zai Lab, founded by Dr. Ying Du, who holds a Ph.D. in Biochemistry from the University of Cincinnati, is an innovative, research-driven commercial-stage biopharmaceutical company focused on discovering, licensing, developing, and commercializing therapies in the fields of oncology, infectious diseases, and autoimmune disorders. Currently, Zai Lab has a pipeline of 16 investigational assets, seven of which have entered pivotal clinical trials, and two of which have received approval for specific indications and been launched in the markets of Hong Kong, China, and mainland China.

After graduating in 1994, Dr. Du Ying joined Pfizer Inc. in the United States, where she engaged in innovative drug research and development as well as project mergers and acquisitions. In 2002, she founded Hutchison MediPharma, successfully advancing five Class 1.1 novel drugs into clinical trials. A decade later, Dr. Du joined Sequoia Capital China, becoming an investor in star projects such as BGI Genomics, Beta Pharma, and Xikang Biopharma.

According to the VCBeat database, Zai Lab secured $30 million in Series A financing from institutions including Sequoia Capital, Qiming Venture Partners, and Tofu Capital at its inception. Two years later, these three earliest institutional investors increased their holdings during Zai Lab’s $106.2 million Series B round, which also saw the entry of Shangcheng Capital. In 2017, Zai Lab raised Series C funding from OrbiMed, Vivo Capital, and Rock Springs Capital, and listed on the U.S. stock market that September, raising $150 million in public offerings under the ticker symbol ZLAB. As of July 1, 2020, Qiming Venture Partners held a 12.25% stake in Zai Lab, making it the largest institutional shareholder, while Dr. Du Ying held a 4% stake.

To implement its commercialization strategy, Zai Lab has recruited and built a commercial team of nearly 400 professionals with extensive experience in innovative drug expansion, helping the company meet every milestone on the planned timeline for new drug commercialization. To date, Zai Lab has successfully launched ZEJULA and Optune in mainland China, Hong Kong, and Macau. Notably, it took less than three years from FDA approval to the commercial launch of ZEJULA in China. Meanwhile, Optune was commercially launched in Hong Kong within less than three months of securing exclusive licensing rights, and achieved commercialization in mainland China within 20 months, bypassing clinical trials.

Zejula is indicated for the maintenance treatment of adult patients with platinum-sensitive recurrent epithelial ovarian cancer, fallopian tube cancer, or primary peritoneal cancer who have achieved a complete or partial response to platinum-based chemotherapy. The originator was TESARO (acquired by GSK), which received U.S. approval in 2017 and European approval in November of the same year. Zai Lab obtained authorization from GSK to commercialize Zejula in Greater China and facilitated its regulatory approval and market launch in Hong Kong, Macau, and mainland China in 2018, 2019, and 2020, respectively. In September 2020, Zejula received approval from the National Medical Products Administration (NMPA) for the maintenance treatment of adult patients with advanced epithelial ovarian cancer, fallopian tube cancer, or primary peritoneal cancer who had responded completely or partially to first-line platinum-based chemotherapy, representing an additional indication.

In China, Zejula’s competitor is AstraZeneca’s olaparib, which was approved for marketing in August 2018 and included in the National Reimbursement Drug List (NRDL) in November 2019 following a 60% price reduction. Even so, within six months of its launch in mainland China, Zejula gained coverage in approximately 800 hospitals; one year after its launch in Hong Kong, it captured around 80% of the PARP inhibitor market share there. It is reported that Zai Lab has made the necessary preparations for Zejula’s inclusion in the NRDL.

Optune is a portable device for tumor treating fields therapy. It has been launched in the United States, Europe, Japan, and Hong Kong, China. Zai Lab holds the commercialization rights for Optune in Greater China. In May 2020, Optune received marketing approval from the National Medical Products Administration for use in combination with temozolomide for the treatment of patients with newly diagnosed glioblastoma, and as a monotherapy for patients with recurrent glioblastoma.

In the first half of this year, Zejula generated $13.8 million in sales revenue, while Optune generated $5.4 million. Constrained by Optune’s recent commercial launch in mainland China at the end of June and its unique licensing sales model (under which the originator manufacturer receives a 10%–15% share of net sales), Zejula became the primary driver of Zai Lab’s revenue growth in mainland China during the first half of 2020.

Prior to their formal inclusion in the National Reimbursement Drug List (NRDL), Zai Lab actively explored innovative healthcare payment solutions, helping Zejula and Optune bridge the “last mile” to patient access. As of the report’s release, Zejula had been included in regional reimbursement programs covering one province and six cities in China, as well as 17 commercial health insurance plans and 12 city-specific inclusive supplementary medical insurance schemes; Optune had been included in four city-specific inclusive supplementary medical insurance schemes.

Furthermore, Zai Lab stated that it has established manufacturing capacity sufficient for the clinical and commercial production of its drug candidates. Its small-molecule manufacturing facility has an annual capacity of up to 50 million units, with current capacity utilization below 10% of total capacity. The large-molecule manufacturing facility supports the clinical production of ZL-1201, with an annual capacity of 12 to 200-L or 1,000-L clinical batches, and current capacity utilization is approximately 40%.

The aforementioned commercialization team, launched products, payment solutions, and production facilities represent the outcomes of Zai Lab’s asset allocation over the past six years, as well as the primary structural support for future cash flow generation. In addition to long-term external funding support, Zai Lab’s own execution capabilities in the commercialization of innovative drugs are also evident.

On September 11, the Hong Kong Stock Exchange disclosed that Zai Lab had passed the listing hearing, prompting a 1.58% rise in ZLAB’s share price. Unlike most pre-profit biotech companies listed in Hong Kong, Zai Lab is also listed on the U.S. stock market, providing domestic and international investors with greater access to corporate and product information necessary for decision-making, thereby reducing issuance difficulties. However, in a relatively efficient capital market like the Hong Kong Stock Exchange, the likelihood of dramatic stock price fluctuations surrounding a secondary listing is minimal. Consequently, Zai Lab’s Hong Kong IPO is unlikely to be a sensational story; instead, it warrants a focus on the intrinsic value of the IPO itself.

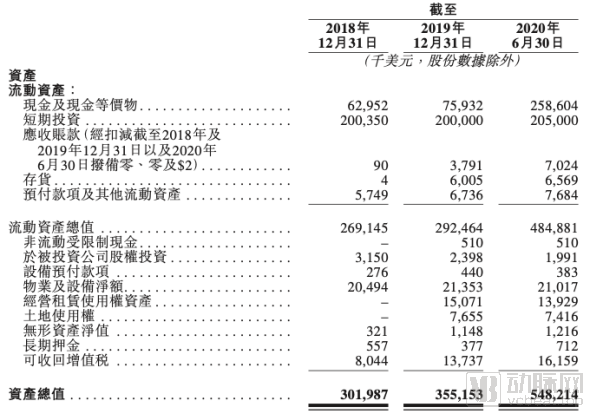

Following the completion of its IPO on the Hong Kong Stock Exchange, Zai Lab will secure approximately HK$6 billion in external funding. Prior to this, the company had already raised around US$300 million from capital markets. A review of static financial data reveals that, after six years of operation, Zai Lab has accumulated assets totaling US$548 million, including US$484 million in current assets. Notably, its cash and cash equivalents alone amount to US$258 million.

Asset Status as of June 30, 2020 (Source: Zai Lab Prospectus)

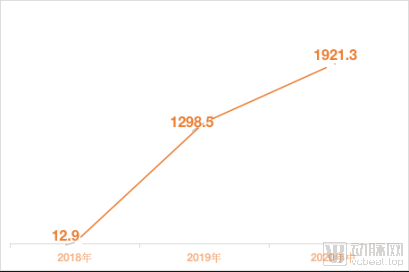

However, an analysis of operating data reveals that Zai Lab’s cash flow is already under considerable strain, a phenomenon common among innovative pharmaceutical companies. In 2018, 2019, and the first half of 2020 alone, Zai Lab incurred cumulative operating losses of $474 million. Furthermore, given that sales-related expenses and R&D expenditures during these three periods showed a year-on-year increasing trend, the financial pressure facing Zai Lab is undoubtedly substantial.

Net Loss and R&D Expenses from December 31, 2018 to June 30, 2020 (Unit: USD 100 million) (Source: Zai Lab Prospectus)

Meanwhile, the seven investigational products that have entered clinical trials require continuous and substantial financial support. The sales revenue generated by the two already-launched products is still in a slow ramp-up phase. According to the prospectus, Zai Lab recorded cumulative operating revenues of $32.327 million from 2018 to the first half of 2020, which was merely a drop in the bucket in addressing its funding gap.

Revenue from December 31, 2018 to June 30, 2020 (Unit: USD 10,000) (Source: Zai Lab Prospectus)

Nevertheless, Zai Lab’s operational performance has been gradually improving. From 2018 to 2019, its gross profit margin rose from 66.7% to 71.1%. With the launch of Zejula in mainland China in the first half of 2020, reduced cost of sales driven by localized production helped further lift Zai Lab’s gross profit margin to 74.1%.

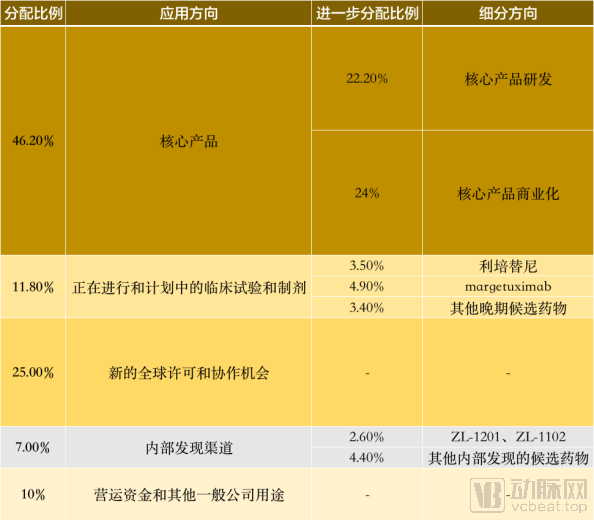

According to Zai Lab’s IPO proceeds utilization plan disclosed for its Hong Kong listing, 90% of the funds raised will be allocated to product development, further development, and commercialization. A closer examination and comparison of this capital allocation plan allow us to assess Zai Lab’s current strategic emphasis among in-licensing and development, independent R&D, and commercialization, as well as its operational style over the next five years at minimum.

Use of Proceeds (Source: Zai Lab Prospectus)

Specifically, Zai Lab has allocated 46.2% of the funds raised to its core products for research and development (R&D) and commercialization. Among these, Zejula will receive approximately HK$2.1 billion, accounting for 32% of the total amount. Half of this sum will be used to hire R&D personnel and further develop the product, while the other half will be directed toward expanding sales and marketing teams to strengthen commercialization capabilities. In the first half of 2020, Zejula contributed over 70% of the company’s revenue, which exceeded US$13 million. From an input-output perspective, it is reasonable that Zejula, as a potential “cash cow,” receives the largest share of funding support.

The remaining 14.2% of funds under the core assets are planned to be used for expanding oncology treatment indications and recruiting key talent for these indications, in order to strengthen commercialization capabilities in the field of oncology. The specific targets for the use of this portion of funds are not clearly stated in the prospectus, but we speculate that they will mainly be used for Optune. This allocation of funds, to some extent, reflects Zai Lab's reliance on Zejula and Optune, two marketed products, to generate cash flow, as well as the challenges associated with the commercialization of innovative drugs.

Allocating 25% of its capital to new global licensing and collaboration opportunities, the second-largest use of funds, demonstrates Zai Lab’s commitment to continuing to expand its R&D pipeline. Zai Lab stated that, as of the reporting date, the company had entered into six licensing or collaboration agreements with global biopharmaceutical companies and would continue to seek potential global licensing and partnership opportunities worldwide that are clinically validated, synergistic with its current pipeline, and aligned with its existing expertise.

Following the capital allocation plan, liprotinib and margetuximab, for which new drug marketing applications have already been submitted in mainland China, received approximately HK$231.5 million and HK$324.1 million, respectively. These two investigational products ranked second only to Zejula and Aipudun in terms of funding allocation in this round, undoubtedly holding the promise of becoming Zai Lab’s third commercialized product. In addition, ZL1201, a self-developed CD47-targeting therapy for multiple tumor types, and ZL1102, an IL-17-targeting drug for psoriasis, both still in the preclinical stage, were allocated 2.6% (approximately HK$172 million) of the R&D budget. Another 4.4% of the funds were reserved for other internally discovered candidate drugs.

From a global R&D perspective, multiple CD47-targeted oncology drugs have entered clinical trials, including investigational products from domestic pharmaceutical companies such as Hengrui Medicine and Hansoh Pharmaceutical. IL-17-targeted therapies for psoriasis have already been launched and have entered the Chinese market. Liang Yi, Chief Commercial Officer of Zai Lab, stated in a media interview that although its core products are in-licensed, Zai Lab has been engaged in independent research and development since its inception and will continue to increase its investment in this area in the future.

As stated in the prospectus, to date, Zai Lab has 12 active in-licensed clinical candidates available for development in Mainland China, Hong Kong SAR, Macau SAR, Taiwan Region, Australia, New Zealand, and other countries in the Asia-Pacific region, through collaborations with GSK, BMS, Paratek, Five Prime, Entasis, Novocure, MacroGenics, Deciphera, Incyte, Regeneron, and Turning Point. Among these, the outcomes of the collaborations with GSK and Novocure are Zejula (Niraparib) and Optune (Tumor Treating Fields), respectively. This section provides a brief summary of Zai Lab’s other in-licensed projects.

Phase III/Pivotal Clinical Trial

In November 2018, it obtained authorization from MacroGenics for the regional development and commercialization of margetuximab, tebotelimab (Phase II), and an undisclosed clinical-stage multispecific TRIDENT molecule in Mainland China, Hong Kong SAR, Macau SAR, and Taiwan Region.

In June 2019, it obtained authorization from Deciphera to conduct clinical studies, sublicense, sell, offer for sale, and import ripretinib in Mainland China, Hong Kong SAR, Macao SAR, and Taiwan Region of China;

In July 2019, obtained authorization from Incyte to conduct clinical studies, sublicense, sell, offer for sale, and import retifanlimab (PD-1) in mainland China, Hong Kong SAR, Macao SAR, and Taiwan region of China;

In April 2020, obtained authorization from Regeneron to develop and exclusively commercialize odronextamab in mainland China, Hong Kong SAR, Macau SAR, and Taiwan;

In July 2020, obtained exclusive license from Turning Point to develop and commercialize products including repotrectinib in Mainland China, Hong Kong SAR, Macau SAR, and Taiwan Region of China.

Phase II Clinical Trial

In December 2017, obtained authorization from Five Prime to develop and commercialize bemarituzumab (FPA144) in mainland China, Hong Kong, Macao, and Taiwan.

Other Stages

In March 2015, obtained authorization from BMS to develop, manufacture, use, sell, import, and commercialize brivanib in mainland China, Hong Kong, China, and Macao, China;

In April 2017, obtained authorization from Paratek to develop, manufacture, use, sell, import, and commercialize omadacycline (ZL-2401) in Mainland China, Hong Kong SAR, Macau SAR, and Taiwan Region;

In April 2018, obtained authorization from Entasis to develop and commercialize durlobactam in Mainland China, Hong Kong (China), Macao (China), Taiwan (China), South Korea, Vietnam, Thailand, Cambodia, Laos, Malaysia, Indonesia, the Philippines, Singapore, Australia, New Zealand, and Japan.

It is evident that in-licensing has been and will continue to be a key commercialization strategy for Zai Lab. Mature in-licensed products can be rapidly launched, quickly entering the revenue-generation phase. For instance, Zejula began sales within two years of being in-licensed, swiftly becoming a leading product in its niche market and a major source of cash flow.

However, the disadvantages of the in-licensing model are also quite apparent. For instance, although Zejula was launched and marketed within two years of being licensed, it was not the only project Zai Lab in-licensed during that period. If survivorship bias is excluded, the new drug development timeline under this model may actually be longer. Secondly, in-licensed projects require continuous investment even after market launch; for example, Zai Lab allocated approximately HK$2.1 billion from its Hong Kong IPO proceeds to Zejula alone. This means that the availability of stable and reliable cash flow has, to some extent, become a constraining factor for the progress of the R&D pipeline. Furthermore, a more severe challenge is that licensing agreements typically include termination clauses. Once triggered, the company can no longer continue the research, development, or commercialization of the candidate drug, which significantly impacts revenue, ongoing operations, and market valuation.

In recent years, as a leading enterprise in China’s innovative drug sector, Zai Lab has accelerated the pace and improved the quality of its strategic layout to mitigate potential R&D risks. Meanwhile, it has strengthened its commercialization capabilities and self-sustaining financial strength, while placing significant emphasis on enhancing its independent development capabilities. Rather than rigidly labeling Zai Lab with any specific new drug development model, we prefer to regard it as a pioneer in biomedical innovation within China. Its practices represent an exploratory approach akin to “crossing the river by feeling the stones.” We are confident that, backed by the team’s strong comprehensive strengths and first-mover advantages, Zai Lab will embark on this new journey with even greater determination.