Cardiac Electrophysiology Firm Set for STAR Market Debut Amid a Booming $4.5B Industry

On September 8, 2020, Huitai Medical, a company specializing in electrophysiology and vascular interventional medical devices, successfully passed the listing review on the STAR Market. This marks Huitai Medical as the second cardiovascular interventional company to go public this year, following Peijia Medical. Unlike Peijia Medical, which operates in the high-profile TAVR sector, Huitai Medical’s core business lies in the cardiac electrophysiology segment, which has received relatively limited attention in China.

Although cardiac electrophysiology has not garnered significant attention in China, this does not diminish the importance of the cardiac electrophysiology market. In fact, cardiac electrophysiology has consistently remained one of the most critical business segments for multinational cardiovascular giants such as Medtronic, Abbott, and Boston Scientific.

In China, cardiac electrophysiology has not received sufficient attention, which may be related to the low level of domestic production in this field. Many sub-sectors of cardiac electrophysiology remain under complete monopoly by foreign companies. Taking three-dimensional (3D) electrophysiology systems and their associated consumables as an example, Johnson & Johnson currently dominates the Chinese 3D electrophysiology market and its primary application area—atrial fibrillation ablation procedures—leveraging its mature technology.

How Are Domestic Companies Strategizing in the Underappreciated Field of Cardiac Electrophysiology? VCBeat (WeChat ID: vcbeat) Analyzes Key Products, Market Landscape, and Chinese Enterprises in the Cardiac Electrophysiology Market.

In the field of cardiology, electrophysiological techniques play a crucial role, primarily in the diagnosis and treatment of arrhythmias. Irregular heartbeats or abnormal cardiac rhythms are referred to as arrhythmias. During each cardiac cycle, the heart undergoes sequential excitation of the pacemaker, atria, and ventricles, accompanied by changes in bioelectric activity. Cardiac electrophysiology involves recording this intracardiac electrical activity, analyzing its manifestations and characteristics to draw inferences, make comprehensive assessments, and guide appropriate therapeutic interventions.

Arrhythmia is a common disease, and atrial fibrillation is a clinically common type of arrhythmia. According to the "Atrial Fibrillation: Current Understanding and Treatment Recommendations - 2018" published by the Electrophysiology and Pacing Branch of the Chinese Medical Association,Currently, the number of patients with atrial fibrillation in China is increasing year by year, and the prevalence rate among people over 35 years old is 0.77%.Based on this calculation, the number of atrial fibrillation (AF) patients in China increased from 4.8 million in 2014 to 5.1 million in 2018. Furthermore, driven by population aging, the number of AF patients is projected to reach 5.3 million by 2023.

Treatment options for arrhythmias include pharmacological and non-pharmacological therapies. Pharmacological treatments can be classified, based on their mechanisms of action, into sodium channel blockers, beta-blockers, agents that prolong the action potential duration, and calcium channel blockers. Although pharmacotherapy is generally the first-line treatment, it can only control heart rhythm to a limited extent, requires long-term administration, and is associated with side effects.

For patients with arrhythmias that cannot be controlled by medication, non-pharmacological interventions such as catheter ablation and pacemaker implantation can help control heart rhythm and alleviate symptoms. In particular, numerous clinical studies in recent years have consistently demonstrated that catheter ablation is superior to antiarrhythmic drug therapy in maintaining sinus rhythm and improving quality of life.

Products for treating arrhythmias are often categorized into two major fields: cardiac rhythm management (CRM) and cardiac electrophysiology (EP). The distinction lies in their primary indications: CRM primarily treats bradycardia (abnormally slow heart rate), whereas EP addresses tachycardia (abnormally fast heart rate). Representative products in CRM are pacemakers, while those in EP are cardiac ablation systems.

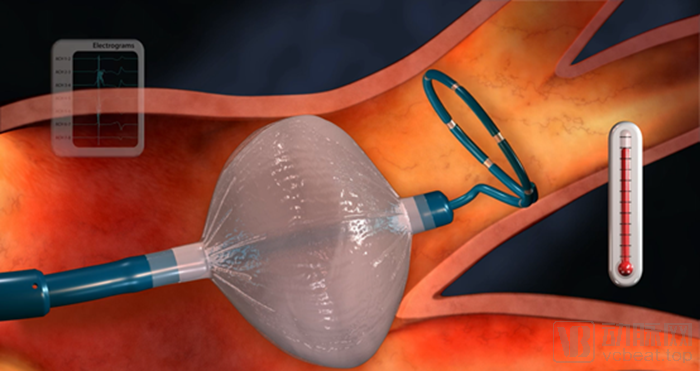

Ablation catheters are devices used in electrophysiological therapy for cardiac arrhythmias. During the ablation procedure, high-frequency electrical energy is delivered through a microcatheter to a small area of intracardiac tissue, thereby eliminating irregular signals generated by abnormal tissue and restoring normal cardiac rhythm.

Schematic Diagram of Medtronic Cryoballoon Ablation Products

Although cardiac electrophysiology is not a hot sector in terms of financing enthusiasm, it boasts substantial commercial prospects.

First, let us examine the considerable market size of cardiac electrophysiology.

According to relevant research reports by Frost & Sullivan, the market size of electrophysiology devices in China was RMB 3.3 billion in 2018. Statistics show that China’s cardiac stent market has a scale exceeding RMB 10 billion; in 2018, the domestic TAVR (Transcatheter Aortic Valve Replacement) market was approximately RMB 280 million. This comparison clearly demonstrates the significance of the cardiac electrophysiology sector within the broader cardiovascular device industry in China.

Meanwhile, China’s cardiac electrophysiology market continues to maintain a remarkably high growth rate. The market size for domestic electrophysiology devices grew from RMB 1.13 billion in 2014 to RMB 3.33 billion in 2018, representing a compound annual growth rate (CAGR) of 30.9%. This growth is driven by factors such as an aging population, a rising number of patients with arrhythmias, the increasing adoption of ablation procedures, and the upgrading of consumable products used in ablation surgeries.The market size of electrophysiology devices in China is expected to reach RMB 12.32 billion by 2023, with a compound annual growth rate (CAGR) of 29.9%.

From a corporate perspective, cardiac electrophysiology products also serve as a critical business pillar. Cardiac electrophysiology has long been a core business segment for international cardiovascular giants such as Abbott, Medtronic, and Boston Scientific.

Cardiac Rhythm and Heart Failure (CRHF) is Medtronic’s largest cardiovascular business segment, accounting for approximately 50% of its cardiovascular revenue, with revenues reaching $2.807 billion in the first half of 2020. Another industry giant, Abbott Laboratories, also derives significant revenue from its cardiac electrophysiology division. In the first half of 2020, Abbott’s cardiac electrophysiology business generated $687 million in revenue, its cardiac rhythm management business generated $875 million, and its heart failure business generated $361 million.

For domestic medical device companies still in their growth phase, the cardiac electrophysiology market is also too significant to overlook. Within the revenue structure of MicroPort Scientific Corporation, a leading Chinese cardiovascular device manufacturer, cardiac rhythm management ranks as the third-largest business segment (following cardiovascular interventional devices and orthopedic medical devices), generating USD 8.269 million in revenue during the first half of 2020.

The cardiac electrophysiology market has become a “cash cow” for major medical device manufacturers, primarily due to the large patient population affected by cardiac arrhythmias. The growing prevalence of these conditions has also driven rapid growth in cardiac electrophysiology procedures.

According to data from the latest Cardiovascular Report 2019, radiofrequency catheter ablation (RFCA) has been widely adopted in more than 600 hospitals across China. Data from the National Health Commission’s online registration system show that the volume of RFCA procedures has continued to grow rapidly since 2010, with an annual growth rate of 13.2%–17.5%. In 2018, the number of RFCA procedures reached 151,600.

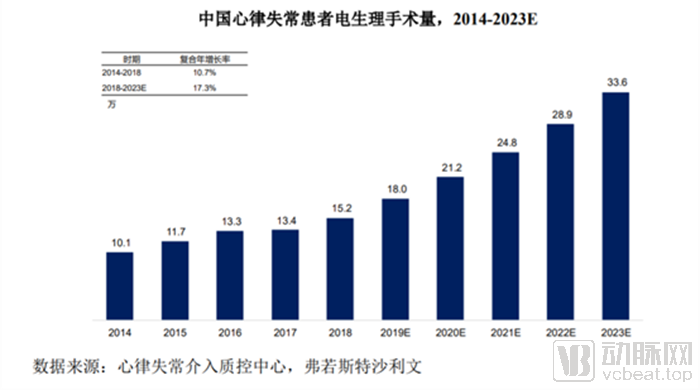

According to data from the National Health Commission’s Quality Control Center for Interventional Treatment of Arrhythmias and Frost & Sullivan, the number of catheter ablation procedures performed among patients with arrhythmia in mainland China has continued to grow in recent years, rising from 101,000 cases in 2014 to 152,000 cases in 2018, representing a compound annual growth rate (CAGR) of 10.7%. The volume of electrophysiology procedures is projected to reach 336,000 cases by 2023, at a CAGR of 17.3%.

Data source: Huitai Medical's prospectus

An investor told VCBeat that there are three major reasons why he is optimistic about the cardiac electrophysiology sector. First, from the perspective of the existing market, the market capacity for minimally invasive interventional treatment of atrial fibrillation is large. It is one of the three major sub-sectors in cardiovascular disease, and the incidence rate of arrhythmia is very high in China.Cardiovascular disease is often referred to as a “silent epidemic” due to its slow-onset symptoms; while heart problems may seem minor, the treatment of cardiovascular disease has consistently been among the most costly healthcare burdens.

Second, in terms of incremental market potential, the advent of 3D mapping systems in the electrophysiology field has enabled more atrial fibrillation (AF) patients to receive precise surgical treatment. It has also facilitated the transition from 2D to 3D procedural approaches for non-AF patients. Consequently, the proportion of arrhythmia cases treated with 3D-guided procedures is expected to rise further in the future.

Third, radiofrequency ablation technology has matured over more than 30 years of development and gained widespread recognition among physicians. Subsequently, cryoablation technology emerged, offering advantages such as a broad range of applications, shorter procedure times, and ease of operation. In addition, other techniques, including laser ablation and ultrasound ablation, are currently under clinical development. Looking ahead, with increasing investment in technological innovation and R&D by domestic and international manufacturers, along with evolving clinical needs, China’s electrophysiology and vascular interventional technologies will continue to undergo iterative upgrades.

In the future, with population aging and the application of wearable devices, the demand for equipment to treat arrhythmias will continue to grow. For example, photoplethysmography (PPG) technology can be used in wearable devices such as health bands and ECG monitoring watches to enhance the detection and screening of atrial fibrillation (AFib). For instance, the Apple Watch can check for irregular heartbeats caused by AFib, a capability that was confirmed in the APPLE HEART study at the 2019 American College of Cardiology (ACC) conference.

From a market perspective, the field of cardiac electrophysiology features both substantial unmet needs and sustained growth potential. Currently, the cardiac electrophysiology market remains dominated by imported products; however, supported by policies promoting import substitution, domestically produced products are poised to break this import monopoly.

From a product perspective, cardiac electrophysiology products also possess sufficiently high technical barriers, combining the attributes of high-end equipment and high-value consumables, which facilitates rapid sales breakthroughs.

While the future holds promise, domestic products currently hold no advantage in the field of cardiac electrophysiology. China’s electrophysiology sector started relatively late, and its medical device market was initially established by large international manufacturers. Although Chinese companies such as MicroPort, Lepu Medical, and Lifetech Scientific are now present in the cardiac electrophysiology market, the sector remains dominated by foreign companies including Johnson & Johnson, Medtronic, Abbott, and Boston Scientific.

In China’s current electrophysiology market, foreign brands represented by Johnson & Johnson, Abbott, and Medtronic account for more than 85% of the market share. According to relevant research reports by Frost & Sullivan, based on sales revenue, the top three players in China’s electrophysiology device market in 2018 were all foreign manufacturers, with Johnson & Johnson dominating the market at approximately 56.7%, ranking first.. Huitai Medical ranks first among domestic manufacturers and fourth in the overall market, with a market share of approximately 3.4%. In 2019, Huitai Medical’s revenue from electrophysiology products reached RMB 170 million.

In the cardiac electrophysiology market, a key advantage enabling imported products to maintain their strong position is the establishment of a comprehensive product portfolio. In terms of horizontal coverage, these products span multiple therapeutic areas, including cardiovascular intervention, heart failure, cardiac rhythm management, and cardiac electrophysiology. In terms of vertical depth within each specific field, they also offer integrated solutions.

In the cardiac electrophysiology market, major products can be categorized into diagnostic equipment, diagnostic consumables, therapeutic consumables, and access consumables. Products in the electrophysiology field primarily include mapping systems, mapping catheters, ablation catheters, electrode catheters, and radiofrequency ablation assistance systems.

Diagnostic equipment mainly includes multi-channel electrophysiology systems. Clinically, these devices are used in cardiology departments and electrophysiology laboratories for intracardiac electrophysiological studies, as well as for monitoring electrocardiographic information and pressure parameters during cardiac interventional procedures.

Diagnostic consumables primarily include electrophysiological electrode catheters, which are used in conjunction with multi-channel electrophysiological recorders to record intracardiac electrophysiological signals for the evaluation of arrhythmias.

Therapeutic consumables primarily include ablation electrode catheters. Types of ablation electrode catheters encompass radiofrequency (RF) ablation electrode catheters, irrigated RF ablation catheters with cooled saline, and cryoablation balloons. Ablation electrode catheters are mainly used for cardiac electrophysiological mapping, stimulation, and recording. When used in conjunction with an RF generator, they enable intracardiac ablation procedures for the treatment of tachycardia.

Currently, catheter ablation procedures can be classified into two-dimensional (2D) ablation and three-dimensional (3D) ablation based on the equipment used.

Two-dimensional ablation refers to catheter ablation procedures that rely on traditional X-ray fluoroscopy for localization prior to delivering ablation therapy. Three-dimensional (3D) ablation represents a significant advancement over conventional radiofrequency ablation, utilizing magnetic or electric field-based localization to construct a 3D model of the cardiac chambers, thereby providing a more precise visualization of the pathological sites. In the treatment of complex arrhythmias and electrophysiology procedures requiring higher precision, operators typically employ 3D electrophysiology systems in conjunction with compatible 3D electrophysiology consumables to achieve accurate detection and treatment of lesions. These 3D electrophysiology consumables generally include pressure-sensing ablation catheters, magnetically localized radiofrequency ablation catheters, and magnetically localized mapping catheters.

Cryoablation is a novel technique for the treatment of arrhythmias, following radiofrequency ablation. Its principle involves the endothermic evaporation of liquid refrigerants to remove heat from tissues, thereby lowering the temperature at the target ablation site. This process destroys cellular tissues with abnormal electrophysiological properties, thus reducing the risk of arrhythmias. Extensive clinical data demonstrate that, compared with traditional radiofrequency ablation, cryoablation is easier for physicians to perform, shortens procedural time, offers high therapeutic efficacy, reduces severe complications such as thrombosis, and alleviates patient pain.

Access consumables mainly include transseptal puncture systems and hemostasis valve-equipped catheter sheaths.

An analysis of the product portfolios of major players in the domestic market reveals that, within the cardiac rhythm and heart failure markets,MedtronicIts product portfolio covers the entire process of diagnosis, treatment, and management for cardiac rhythm disorders and heart failure. This includes cardiac pacemakers and implantable cardioverter-defibrillators (ICDs). Its atrial fibrillation ablation products include the Arctic Front Cardiac CryoAblation Catheter System, specifically designed for pulmonary vein isolation in patients with drug-refractory paroxysmal atrial fibrillation.

Boston ScientificIn the field of cardiac electrophysiology, we possess a high-precision 3D mapping system, which includes the high-precision 3D mapping system itself, 3D mapping catheters, and magnetically localized micro-electrode irrigated ablation catheters. The cardiac 3D mapping system enables real-time visualization of intracardiac catheters and displays various types of cardiac maps, recording and presenting them on the system monitor. It is used for the diagnosis, precise localization, and ablation guidance of various arrhythmias, particularly complex arrhythmias. Currently, Boston Scientific’s cryoablation product, Cryterion, has not yet been registered in the Chinese market.

Johnson & JohnsonIn the electrophysiology field, main products include the CARTO 3D System, the Pentaray multipolar mapping catheter with dual magnetic and electrical localization, mapping catheters, radiofrequency ablation catheters, and surface reference electrodes.

AbbottThe primary move was the acquisition of St. Jude Medical to enter the cardiac electrophysiology sector. In the field of electrophysiology, Abbott’s main products include the EnSite 3D mapping system, the Advisor™ HD Grid Mapping Catheter (magnetic and electrical localization), mapping catheters, and radiofrequency ablation catheters. Global sales revenue in 2018 amounted to $30.58 billion, with electrophysiology business revenue reaching $760 million.

MicroPort EPThe product portfolio primarily includes the Columbus 3D system, circular pulmonary vein mapping catheters, mapping catheters, radiofrequency ablation catheters, and puncture consumables. In 2018, sales revenue reached $670 million, of which electrophysiology product revenue amounted to $12.69 million.

Xinnuopu:Xinonuo Medical was founded in Minnesota, USA, in 2005. In 2007, the company established its production and R&D center in Beijing. Xinonuo Medical is a company specializing in the field of cardiac electrophysiology. Its main products include mapping catheters, radiofrequency ablation catheters, and puncture consumables.

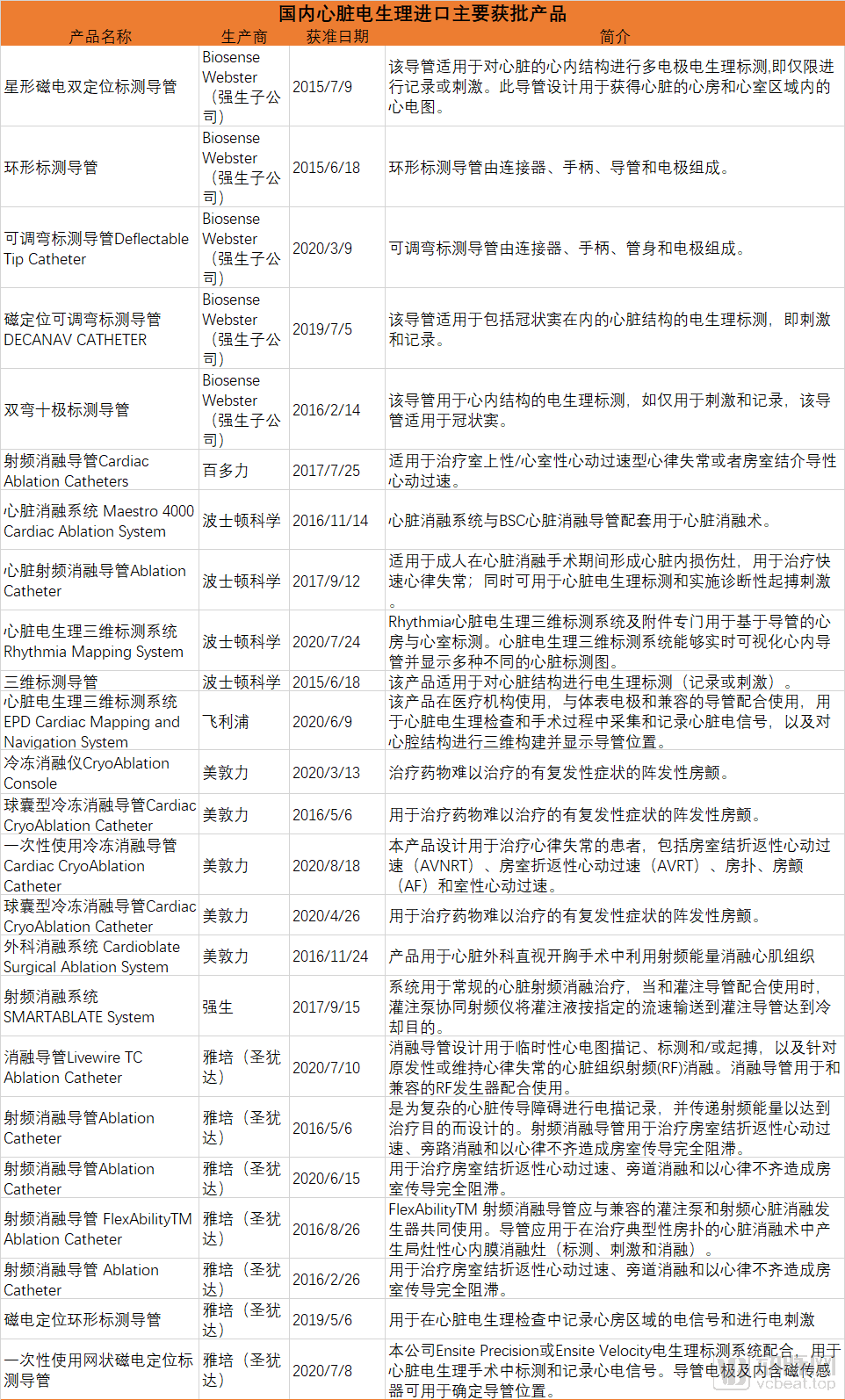

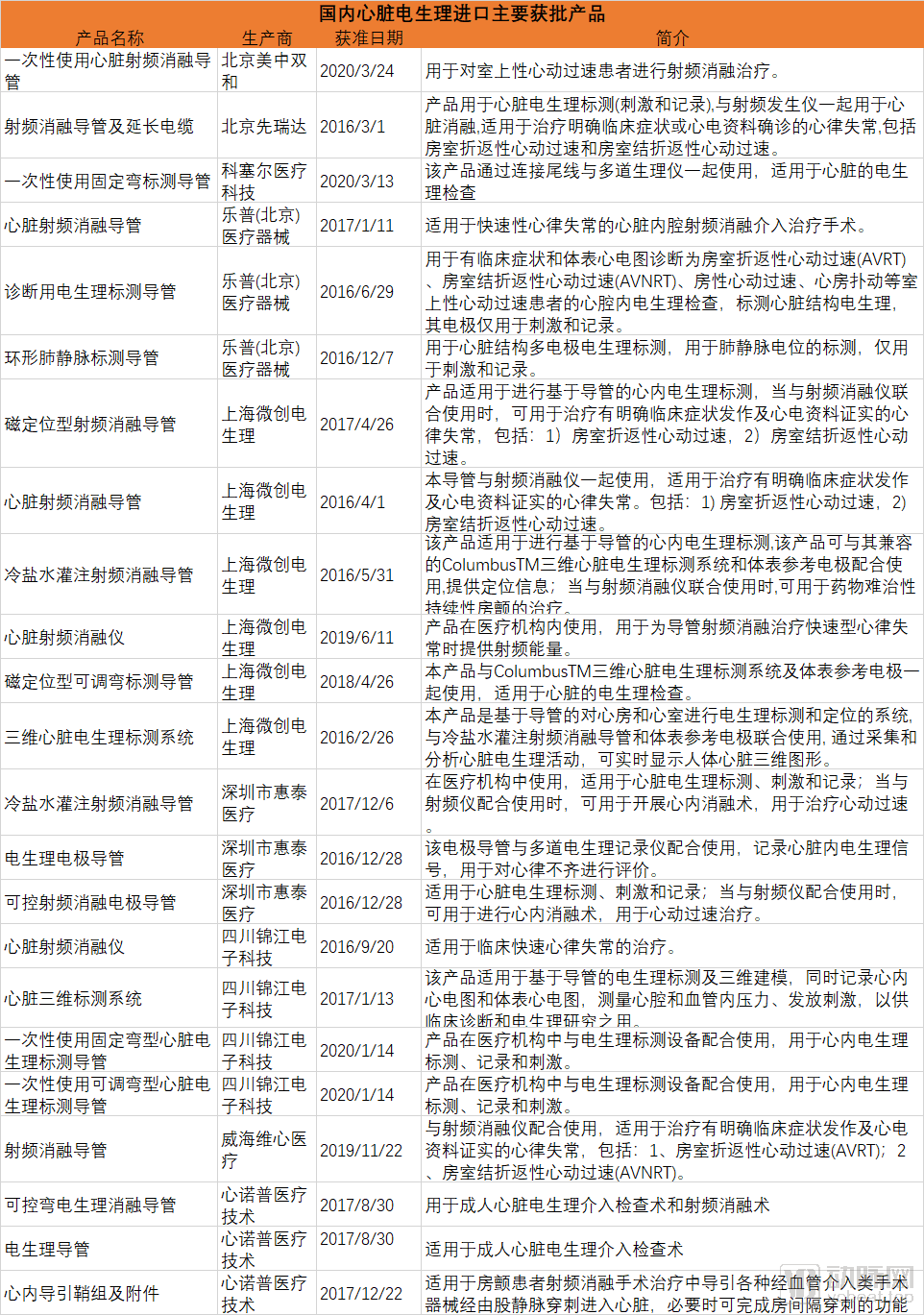

VCBeat has compiled the approval status of major cardiac electrophysiology products based on the database of the National Medical Products Administration. From the perspective of product registration, apart from radiofrequency ablation catheters, there is still a significant gap between domestically produced cardiac electrophysiology products in China and foreign brands in terms of registration volume and product portfolio. This disparity is particularly evident in cryoablation products, where both the number and variety of registered domestic products fall far short of imported ones.

The gap with foreign brands also demonstrates that there is still significant room for domestic substitution. However, due to the technical barriers in the field of cardiac electrophysiology, import substitution in this area remains challenging.

First, the technological and process barriers in the field of electrophysiology.

Electrophysiology devices entail high R&D difficulty and significant entry barriers, involving multidisciplinary intersections across medicine, materials science, biology, mechanical manufacturing, and physicochemistry. In the industrialization phase, processes such as catheter braiding, shape-memory alloy processing, guidewire machining and welding, and balloon catheter manufacturing all fall under precision or even ultra-precision machining categories. Continuous process exploration, refinement, and breakthroughs are required to ensure high yield rates.

Secondly, in the field of high-end medical devices, domestically produced products rely almost entirely on imported raw materials. High-end medical devices have stringent requirements for raw material quality; for instance, the materials required for guidewires and catheters mostly consist of high-value-added tubing, polymers, and precious metals, which must exhibit excellent strength, plasticity, biocompatibility, and corrosion resistance. Huitai Medical pointed out in its prospectus that raw material suppliers are primarily located overseas, and there are currently no qualified domestic alternative suppliers for these imported raw materials.

From the perspective of product iteration, domestic products have limited opportunities to overtake competitors through upgrades. In the electrophysiology product market, the primary obstacle to import substitution is the relatively backward technology of domestically produced 3D electrophysiology systems; currently listed domestic 3D electrophysiology systems lag nearly one generation behind imported products in terms of technical level. As clinical demand for precision therapy continues to rise, the utilization frequency of 3D electrophysiology systems will further increase, and the electrophysiology consumables used in conjunction with these systems are also undergoing upgrades and replacements. Domestic electrophysiology manufacturers need to accelerate their R&D processes and achieve full product line coverage of both 2D and 3D electrophysiology systems and consumables as soon as possible, so as to catch up with and gradually replace foreign manufacturers.

We can also anticipate that the process of domestic substitution will not happen overnight. The position of imported manufacturers in the field of cardiac electrophysiology is not easily shaken. Giants have well-established marketing networks and widespread recognition. Hospitals and operators are usually more cautious when choosing new medical device varieties, preferring imported products.

In high-risk procedures such as electrophysiology, physicians typically need to continuously use these devices for a series of complex diagnostic and therapeutic interventions, imposing extremely high requirements on product maneuverability, quality stability, and safety performance. Through prolonged use of products from a specific brand, physicians gradually develop usage habits and preferences.

Huitai Medical also pointed out in its prospectus that medical device products typically need to go through regional bidding procedures before they can be used clinically in hospitals. Bidding processes and policies vary across different regions in China. For instance, some areas implementing centralized procurement require historical sales data as a necessary condition for shortlisting. However, emerging high-quality domestic manufacturers often find themselves at a disadvantage compared to foreign companies due to their limited historical sales records, further increasing the difficulty of competing with imported products on an equal footing.

Due to the historical monopoly of foreign manufacturers in China’s vascular intervention and electrophysiology medical device markets, coupled with the fact that the evaluation of such devices is a comprehensive process encompassing surgeons’ perceptions, immediate procedural success rates, and tactile handling characteristics, Chinese-made products require more specialized promotion and product education by domestic manufacturers to further achieve import substitution. The subsequent large-scale adoption will also undergo a process of continuous improvement and gradual market acceptance, necessitating a certain period of time.

After decades of development, domestically produced medical devices in China have progressed through several stages: reliance on imports, imitation of imported products, improvement upon imported designs, and finally, independent innovation. In recent years, some outstanding domestic manufacturers have emerged as significant forces. Due to the high barriers to substitution, the domestic cardiac electrophysiology sector has not yet experienced the same boom seen in other areas of cardiovascular medicine. Nevertheless, we believe that with the continuous enhancement of R&D capabilities among Chinese enterprises, the ongoing improvement of the market environment, and the successive introduction of favorable policies, the market share of domestically produced electrophysiology devices will continue to rise.

Reference: HT Medical's Prospectus