Race for a Trillion-Dollar Market: Who Will Lead—Multi-Cancer or Single-Cancer Early Detection?

In recent years, with the leapfrog development of liquid biopsy technology, a wide variety of early cancer screening products have continuously emerged. However, most current screening methods are limited to specific types of cancer. Pan-cancer early screening technology is an important component of health management, enabling the simultaneous detection of multiple cancers. In the face of the still severe challenges in tumor prevention and control, pan-cancer early screening has become a powerful tool for reducing cancer incidence and mortality rates. Therefore, pan-cancer early screening is also regarded as the breakthrough point for next-generation early cancer screening technologies.

In September 2020, industry leader Grail filed for an IPO and announced its plan to launch Galleri, a multi-cancer early detection product, via the Laboratory Developed Tests (LDT) pathway in 2021. Capable of detecting more than 50 types of cancer, Galleri is intended for cancer screening in asymptomatic individuals aged 50 and older, drawing unprecedented attention to multi-cancer early detection.

As pan-cancer early screening products gradually mature, the industry has evolved into a duopoly featuring both single-cancer and pan-cancer early screening. What is the current state of pan-cancer early screening development? What adverse factors exist? In this trillion-yuan blue-ocean market, will single-cancer or pan-cancer early screening become the mainstream? VCBeat has compiled a list of companies involved in pan-cancer screening and conducted interviews with Yi Xin, CEO of Genetron Health, and Yuan Shuo, Investment Director at Qingtong Capital.

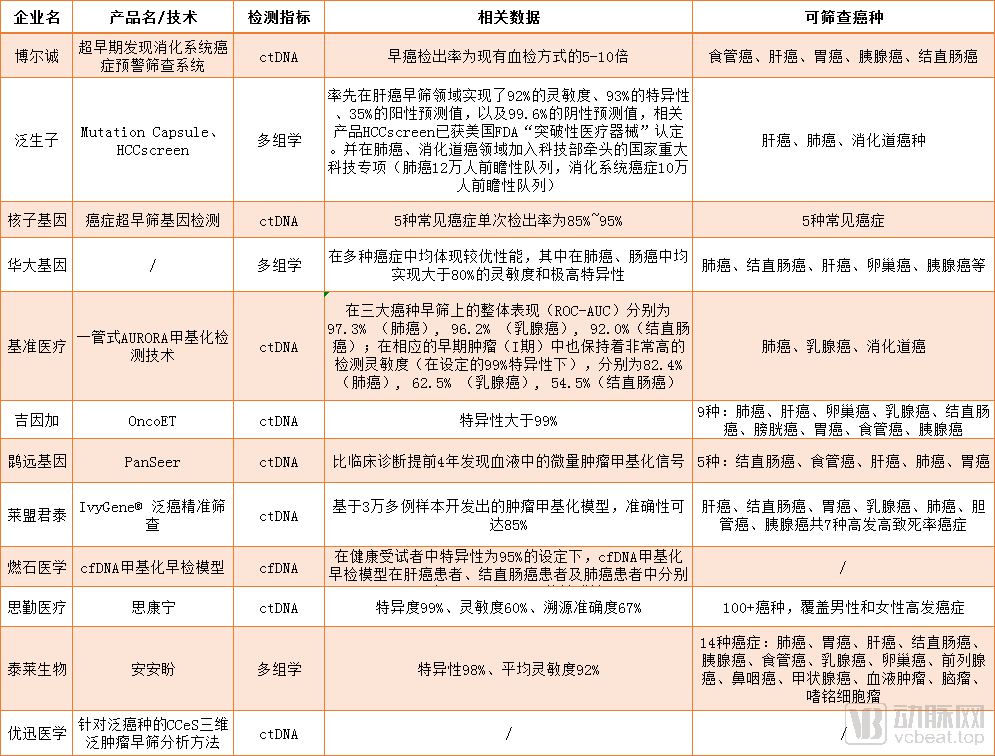

As shown in the table, the number of cancer types that can be screened by various companies ranges from a few or more than ten to over one hundred. For example, Siqin Medical can screen for more than 100 types of cancer, covering high-incidence cancers in both men and women. Many people believe that the more cancer types that can be screened, the better, aiming to capture all possible cancer types. Is this really the case?

Yi Xin, CEO of Genetron Health, believes that screening for a greater number of cancer types is not necessarily better. Many cancers have extremely low incidence rates, making screening of limited value for the general healthy population. Blindly pursuing a higher number of screened cancers will only lead to over-screening, causing unnecessary anxiety and psychological stress for those being tested. Yuan Shuo, Investment Director at Qingtong Capital, similarly stated, “A broader range of cancer types requires larger-scale databases and analytical capabilities. Promoting multi-cancer screening without such accumulated expertise is of little practical significance.”

Yi Xin stated that in terms of cancer type selection, tumors with high incidence rates and significant harm should be prioritized. Currently, the Pan-cancer Screening Study in the Chinese Population (PREDICT, NCT04405557), led by Genetron Health in collaboration with Professor Zeng Qiang’s team at the PLA General Hospital (301 Hospital), has selected six major cancer types characterized by high incidence and high mortality rates as its research focus. As shown in the table, all companies have included cancers with high prevalence in the Chinese population—such as lung cancer, colorectal cancer, liver cancer, and gastric cancer—as essential components of their pan-cancer early screening products.

Meanwhile, personalized and customized pan-cancer early screening protocols represent the future trend. Yi Xin remarked, “Previously, we aimed to cover all cancer types with a single technological approach; however, given the substantial heterogeneity of cancers, varying degrees of indolence, and differing individual benefits among examinees, this strategy has limitations.” A more precise solution for pan-cancer early screening involves assessing individual cancer risk based on personal characteristics, tailoring an appropriate screening panel, and integrating multiple modalities such as liquid biopsy, medical imaging, and endoscopy.

Currently, most pan-cancer early screening companies use ctDNA as the detection marker.

ctDNA methylation is a form of chemical modification of genes that can alter genetic expression without changing the gene sequence. It can induce changes in chromatin structure, DNA conformation, DNA stability, and the manner in which DNA interacts with proteins, thereby regulating gene expression. Gene methylation occurs prior to the onset of cancer and is a critical mechanism in carcinogenesis. In other words, early detection of methylation abnormalities or expression profiles associated with cancer can facilitate the early diagnosis of cancer.

In theory, ctDNA, CTCs, and exosomes can all be used for cancer screening. However, in terms of technological maturity, the advent of next-generation sequencing (NGS) has propelled ctDNA to a more advanced stage, making it the mainstream application direction in liquid biopsy today. Regarding their respective advantages and focuses, ctDNA emphasizes genomic-level analysis to obtain mutation information, rendering it more suitable for early-stage screening.

It is also evident from the table that a small number of companies, such as Tellgen and BGI Genomics, are employing multi-omics technologies for pan-cancer early screening. Amidst intense competition among numerous biotechnology firms, multi-omics technology has become a key tool for companies to secure a competitive advantage in the cancer early screening market.

Multi-omics, known as the “next-generation liquid biopsy,” is a novel biological analysis approach that provides tailored screening solutions with optimal efficacy, based on the distinct developmental stages of various cancers and the specific characteristics of different patient populations.

The fundamental methodology of multi-omics is based on extensive biological data at the molecular level, spanning multiple stages and dimensions of life—including the genome, transcriptome, epigenome, proteome, metabolome, and microbiome. By leveraging techniques such as bioinformatic statistical analysis, computational biology, and machine learning, this approach enables high-level analysis and interpretation of complex biological phenomena involving numerous influencing factors, such as life processes and diseases.

Meta-Pan™, developed by Tellgen Corporation, is a relatively mature multi-omics-based pan-cancer early screening product in China. It covers more than 14 types of tumors with the highest incidence and mortality rates in the country. With a specificity exceeding 98%, the detection sensitivity for most cancers surpasses 92%. Currently, Meta-Pan™ has obtained full Laboratory Developed Tests (LDT) qualifications and reaches end users through channels such as third-party medical laboratories, health examination centers, and commercial insurance plans, making it Tellgen Corporation’s flagship product.

From the perspective of corporate typology, enterprises engaged in the field of pan-cancer early screening include those specializing in this area. For instance, Siqin Medical has launched Sikangning, a pan-cancer early screening product that enables comprehensive screening for high-incidence cancers in both men and women from a single blood sample. This approach identifies early cancer signals while avoiding radiation exposure from imaging, as well as invasive damage from endoscopy and needle biopsies. Kunyuan Genomics has leveraged its proprietary ctDNA methylation-based multi-cancer screening technology, the PanSeer method, to detect trace tumor methylation signals in blood samples four years earlier than clinical diagnosis. This achievement was demonstrated in blood samples from the Taizhou cohort, which comprised nearly 200,000 community residents.

Pan-cancer early screening represents the evolutionary direction of single-cancer early screening; therefore, it is imperative for companies to strategically position themselves in pan-cancer early screening while prioritizing breakthroughs in single-cancer early screening.

Companies specializing in tumor-guided medication, such as Genetron Health and Huirui Gene, are also positioning themselves in the pan-cancer early screening market. VCBeat believes that companies in the field of tumor companion diagnostics have chosen pan-cancer early screening as a new business direction for several reasons.

First, the market size is sufficiently large. Yuan Shuo stated that pan-cancer early screening no longer corresponds to the traditional clinical market, but rather to the much larger health check-up market, which far exceeds the market size for tumor companion diagnostics.

Secondly, compared with the crowded field of personalized tumor treatment, the pan-cancer early screening market remains a blue ocean. Yi Xin stated, "From medication guidance to full-process monitoring and then to early screening, this represents a major development trend in the application of liquid biopsy for tumors. As competition in tumor-guided medication becomes increasingly intense, full-process monitoring and early cancer screening have become breakthrough points for companies specializing in tumor liquid biopsy."

Meanwhile, pan-cancer early screening products boast high repurchase rates (with an average repurchase cycle of 2–3 years), and theoretically, everyone can be a target customer, leading to substantial sales volume once the market matures. Additionally, early screening targets may be correlated with tumor treatment regimens, enabling their application in the development of therapeutic drugs and technologies, thereby creating business synergies that achieve twice the results with half the effort.

Moreover, given the differences in high-incidence cancers across regions and countries, early screening targets for the Chinese population also differ slightly from those for European and American populations, meaning that mature foreign products may not be suitable for the Chinese market. Therefore, domestic companies can hold certain advantages.

Although the market prospects for pan-cancer early screening are promising, driven by factors such as capital investment, favorable policies, and persistently high incidence and mortality rates, it cannot be overlooked that this field is still in its nascent stage and faces numerous challenges that urgently need to be addressed.

Insufficient data accumulation.Compared with single-cancer early screening, pan-cancer early screening products require larger data volumes and greater commercial investment, necessitating long-term accumulation by enterprises.

Data accumulation is key, with multiple companies continuously collecting data through large-cohort clinical studies to refine their products. Abroad, Guardant Health has launched the “Guardant 1 Million” initiative, aiming to complete liquid biopsy genomic sequencing for one million cancer patients within five years. The company hopes to leverage this sequencing data to advance cancer treatment and accelerate the development of the blood-based early cancer screening and detection industry.

Industry pioneer Grail has conducted multiple prospective clinical studies, notably launching the Circulating Cell-free Genome Atlas (CCGA) program in 2016. The program comprises three components: identification of detectable targets directly associated with cancer (CCGA-1); expansion of sample cohorts and algorithm training (CCGA-2); and clinical validation of the product (CCGA-3). To date, the first two phases have been largely completed, involving testing in a total of 6,700 patients, and have established methylation as the target for early-screening products. Based on these findings, the multi-cancer early detection liquid biopsy test has received the FDA’s Breakthrough Device Designation.

Large-scale prospective studies on pan-cancer early screening are also being conducted in China.

Leveraging its proprietary Mutation Capsule technology, Genetron Health has partnered with the National Cancer Center/Cancer Hospital of the Chinese Academy of Medical Sciences to join the National Major Science and Technology Special Projects led by the Ministry of Science and Technology in the fields of liver cancer, lung cancer, and gastrointestinal cancers. Specifically for lung cancer, the company plans to conduct a multicenter prospective cohort study for lung cancer screening among 120,000 high-risk individuals across communities in 20 provinces nationwide. For digestive system cancers, it plans to carry out prospective cohort studies within existing early diagnosis and treatment project cohorts comprising over 100,000 individuals in urban areas and the Huai River Basin.

Genetron Health’s liquid biopsy product for early hepatocellular carcinoma (HCC) screening, HCCscreen, has completed testing on 2,000 patients within a prospective cohort of 4,500 hepatitis B surface antigen (HBsAg)-positive individuals. Preliminary data from 297 patients at one center demonstrated that the product achieved a sensitivity of 92%, specificity of 93%, positive predictive value (PPV) of 35%, and negative predictive value (NPV) of 99.6%. Owing to its superior performance, HCCscreen recently became the first to receive the U.S. FDA’s “Breakthrough Device” designation, and its subsequent Premarket Approval (PMA) application will be eligible for priority review. The achievements and experience accumulated in this single cancer type will provide robust technical and data support for Genetron Health’s research and development of pan-cancer early screening.

Burning Rock Biotech also officially launched China’s first prospective pan-cancer early detection study, “PREDICT,” in May 2020, aiming to establish a methylation profile database for Chinese cancer patients, individuals with corresponding benign lesions, and healthy populations. The study is expected to enroll more than 14,000 participants.

The price is on the high side.Yi Xin believes that a price range of RMB 100–300 for single-cancer early screening and RMB 1,000–2,000 for pan-cancer early screening is appropriate. However, the current prices of liquid biopsy-based early screening products are significantly higher than this range, hindering the widespread adoption of early cancer screening technologies.

Providing cost-effective pan-cancer early screening products has long been a key focus for Chinese companies. Siqin Medical believes that the core to reducing costs lies in eliminating amplification during sequencing and employing more optimized algorithms. According to news reports, Siqin Medical plans to keep the price of its SiKangNing product below RMB 1,000 within three to five years, thereby facilitating the large-scale adoption of early cancer screening.

Approval difficulties.No pan-cancer early screening products have been approved in China. Yuan Shuo stated, “The levels of biomarkers for early-stage cancer in the blood are too low, resulting in weak detection signals. Moreover, early-stage cancers cannot be detected by traditional clinical methods such as CT scans, and there are currently no clinical means to manage them. Consequently, their clinical acceptance remains problematic. The regulatory approval landscape for such products is also somewhat ambiguous, lacking comprehensive policy guidelines.”

Clinical Significance.Yuan Shuo stated, “Current standards for early cancer screening primarily rely on traditional technical methods such as imaging, and the clinical community remains conservative in its attitude toward liquid biopsy. If pan-cancer early screening cannot be aligned with clinical significance, it will serve merely as an alert even if early-stage cancers are detected. Furthermore, consumer willingness to purchase such early screening products in the B2C market is a significant concern.”

Promotion costs are high.Many companies have told VCBeat that the promotion costs for cancer early screening products are high, especially when marketing to consumers via internet channels. VCBeat believes that as a new technology, pan-cancer early screening is not currently an essential service. Companies should initially focus their promotional efforts on health checkup centers, rapidly replacing traditional technologies in these settings. Once market education has matured, they can then expand into internet channels, which could help reduce promotional expenses to some extent.

Returning to the question we raised at the beginning: which will become mainstream, single-cancer early screening or pan-cancer early screening?

Both Yuan Shuo and Yi Xin believe that single-cancer early screening and pan-cancer early screening are not mutually exclusive, but rather complementary.

Yuan Shuo stated that single-cancer early screening and pan-cancer early screening target different populations. The detection of early-stage tumors demands high sensitivity from screening technologies. Although pan-cancer early screening can simultaneously detect multiple types of tumors, it may not necessarily identify the specific tumor type. It is recommended that individuals with a significant family history of cancer and those at high risk opt for single-cancer early screening. Individuals without clear high-risk factors for cancer are better suited for pan-cancer early screening.

Yi Xin believes that single-cancer early screening and pan-cancer early screening should have a relationship of refined screening and initial screening. Initial screening should be conducted through pan-cancer early screening first, followed by refined screening through single-cancer early screening.

VCBeat believes that the choice between single-cancer early screening and pan-cancer early screening depends more on the actual circumstances and preferences of the individuals being screened. We have compared them across three dimensions: price, patient compliance, and the range of screenable cancers.

There is a wide array of single-cancer early screening technologies. Before making comparisons, it is helpful to provide a brief classification of these technologies. Single-cancer early screening can be divided into liquid biopsy-based single-cancer screening techniques and more traditional single-cancer early screening methods (such as colonoscopy, gastroscopy, and low-dose spiral CT, which are currently the mainstream screening modalities in the market).

Price:Pan-cancer early screening > Liquid biopsy-based single-cancer early screening > Traditional single-cancer early screening

Screenable Cancer Types:Pan-cancer early screening > liquid biopsy-based single-cancer early screening = traditional single-cancer early screening

Comfort and Convenience:Pan-cancer early screening = Liquid biopsy-based single-cancer early screening > Traditional single-cancer early screening

From a pricing perspective, pan-cancer early screening requires the detection of numerous loci, resulting in higher costs. In contrast, traditional single-cancer early screening technologies are mature and low-cost. In terms of screenable cancer types, pan-cancer early screening can detect multiple cancers, offering significant advantages. Regarding comfort and convenience, liquid biopsy-based screening technologies are generally more convenient than traditional single-cancer screening methods; notably, some liquid biopsy techniques enable home-based screening, which can substantially improve user compliance. Overall, the three cancer screening approaches each have their own strengths and weaknesses and serve as complementary options. For product development, companies should strategize based on factors such as target populations and comparisons between new and existing technologies.