Four Models of Internet Healthcare + Commercial Insurance Integration: Commercial Insurance Reimbursements Projected to Account for 10% of Online Medical Payments

Since the onset of the pandemic this year, internet healthcare has achieved a major breakthrough in terms of payers. Medical insurance has been opened up to internet healthcare services. In particular, large public hospitals in cities such as Beijing and Shanghai have integrated medical insurance payment almost simultaneously with the launch of their online consultation services. Furthermore, internet hospitals operated by several leading internet healthcare companies have also been included in the medical insurance network, which facilitates the migration of patients to online platforms.

However, amid tightening cost-containment measures and significant regional policy disparities, the comprehensive rollout of online services under basic medical insurance will take time. Consequently, commercial health insurance has naturally emerged as a potential payer, particularly for internet healthcare enterprises. What are the current models integrating internet healthcare with commercial insurance? What challenges remain? What is the long-term value of this connection? By analyzing product and service information from ten companies and interviewing multiple industry insiders, we seek answers to these questions.

As a payer in the internet healthcare sector, commercial insurance most directly provides reimbursement for online medical services and pharmaceutical expenses. VCBeat’s research has found that some internet healthcare companies have partnered with insurers to launch related products.

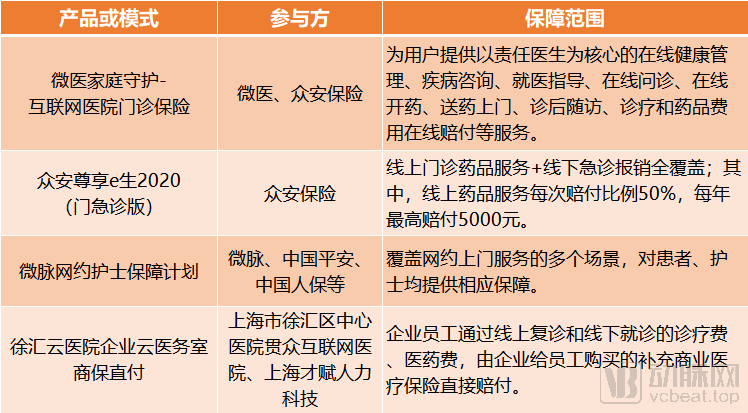

Models of Direct Compensation by Commercial Insurance to Internet Healthcare Patients (Incomplete Statistics) | Source: Public Information, Interviews; Graphic by VCBeat

As early as 2017, WeDoctor and ZhongAn Insurance jointly launched China’s first internet medical health insurance product, introducing the “WeDoctor Family Guardian – Internet Hospital Outpatient Insurance” plan for family users, which provides reimbursement for patients’ online consultation and medication costs.

In 2020, ZhongAn Insurance launched an outpatient and emergency insurance product covering online services through its affiliated internet hospital, offering free consultations and reimbursement for medication costs incurred from online medical care.

Furthermore, Weimai’s on-demand nurse service plan also provides coverage for patients. Xuhui Cloud Hospital, leveraging its corporate cloud clinics and partner enterprise group insurance plans, has introduced a direct billing commercial insurance service for employee online consultations.

Zhu Xuesong, head of WeDoctor Health under WeDoctor Group, believes that the combination of basic medical insurance and commercial health insurance will become the fundamental payment model for internet-based medical consultations in the future. The primary payer for medical services is basic medical insurance, which helps cover the cost of essential diagnostic and treatment services for the public; the secondary payer is commercial health insurance, which can more comprehensively meet the diverse and personalized healthcare needs of individuals.

Although there are currently few products with direct-to-patient reimbursement, their numbers have been gradually increasing from 2017 to 2020. VCBeat has learned that some companies will soon launch similar products.

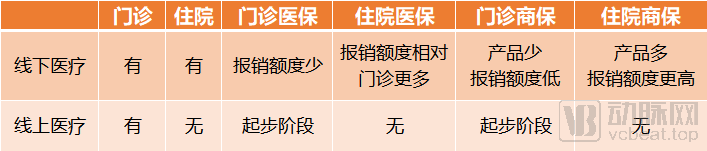

Characteristics of Online and Offline Healthcare and Reimbursement, Source: Public Information, Interviews, Chart by VCBeat

From another perspective, considering characteristics such as online healthcare scenarios and the structure of medical payments:

"In offline settings, medical scenarios include outpatient and inpatient care. 'Most commercial health insurance products are million-yuan medical insurance and critical illness insurance, which provide payment or compensation for inpatient scenarios,' said Liu Xuejian, head of the insurance business department at Zhiyun Health."

Data from the official website of the China Banking and Insurance Regulatory Commission (CBIRC) shows that among registered personal insurance products, only 109 policies include “outpatient and emergency” in their names, while as many as 1,661 policies include “hospitalization.”

The same applies to medical insurance, where reimbursement for inpatient care is significantly higher than for outpatient services.

Online, internet-based healthcare can only be positioned for outpatient services and cannot directly assume the function of inpatient treatment. Although there is currently no precise market data to substantiate this, the above comparison indicates that even with widespread adoption of online medical insurance payments and broad coverage by commercial insurance products, patient reimbursements will still fall short of the overall payment volume seen in offline settings.

This determines that online outpatient insurance based on patient claims reimbursement will become part of the internet healthcare payment system, and the industry’s sustained development requires more payment channels for consolidation.

Although internet-based healthcare cannot provide inpatient services, resulting in a gap in coverage for such claims, its unique attributes help alleviate issues such as the scarcity of high-quality medical resources, inefficiencies in traditional healthcare access, and information asymmetry among patients, providers, and insurers. Consequently, internet-based healthcare stands to benefit from these advantages. We have identified three B2B models linking internet-based healthcare with commercial insurance payment systems.

Internet Healthcare as a Service Provider for Commercial Insurance

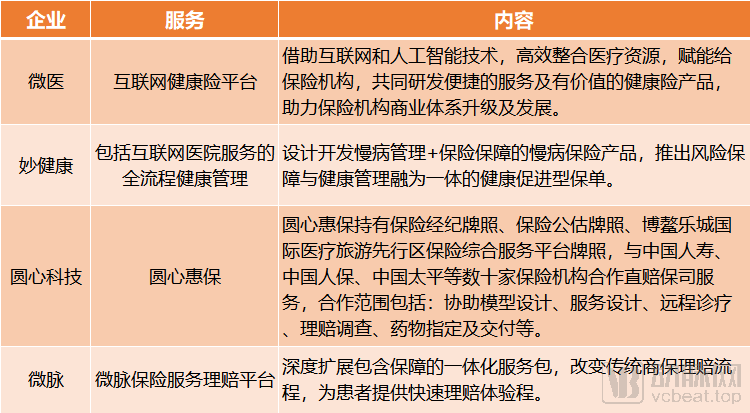

This model primarily involves internet healthcare companies providing a suite of online medical and health services to insurance companies, which then integrate these services into their products for customers.

A relevant executive at Ping An Health Insurance Technology introduced that the "product + service" model simply adds online medical services to traditional commercial insurance—for example, incorporating services such as online consultations into million-yuan medical insurance products—to enhance the competitiveness of insurance offerings.

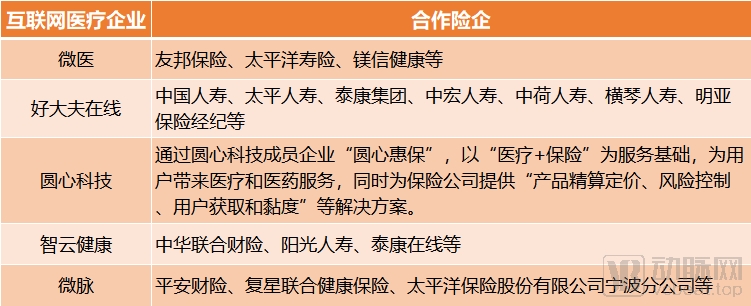

Internet Healthcare as a Cooperation Model for Insurance Companies’ Service Providers. Source: Public Information, Interviews; Chart by VCBeat

A significant number of internet healthcare companies and insurance providers have adopted this model, with Ping An Good Doctor being a typical example. In its 2020 semi-annual report, Ping An Good Doctor disclosed that it was continuously working to integrate with the national basic medical insurance system while simultaneously strengthening collaborations with commercial insurers. Revenue from commercial insurance partnerships and membership-based products remained the primary income source for its core online healthcare segment.

WeDoctor has partnered with AIA Insurance and Magnesium Health to jointly launch “Guardian Beauty Medical Insurance,” a single-disease insurance product specifically for breast cancer. By integrating their respective resources, the three parties have connected the core components of healthcare—medical services, pharmaceuticals, and insurance—to provide customers with a comprehensive, closed-loop service covering the entire breast cancer care journey, from prevention and medical consultation to medication and rehabilitation. Additionally, WeDoctor has established a long-term strategic partnership with AIA Insurance. AIA customers are granted priority access to a range of WeDoctor’s medical and health services, including appointment scheduling, online consultations, and offline clinic visits.

In addition, Haodf Online, Weimai, and Zhiyun Health have also launched collaborations with insurance companies.

The 2019 edition of the Administrative Measures for Health Insurance stipulates that the cost proportion of health management services in insurance products can reach up to 20%; the 2020 Notice on Regulating Health Management Services of Insurance Companies defines the scope of health management services, including: health examinations, health consultations, health promotion, disease prevention, chronic disease management, medical consultation services, and rehabilitation nursing. The scope of internet medical services highly aligns with the health management content outlined in the new regulations; therefore, this model still has further room for development.

“Internet-based healthcare provides a closed-loop online health management service for health insurance, enabling the transition from medical claims processing to health management. This offers new tools for cost-containment models in health insurance,” said a representative of Ping An Health Insurance Technology.

Internet Healthcare as a Product Design Support Provider for Insurance Companies

Precisely because internet-based healthcare can deliver efficient services and accumulate vast amounts of health, medical, and behavioral data, this advantage can be leveraged to serve as a partner for insurance companies in product design and risk control management, providing references for product development and premium rate setting.

Internet Healthcare as a Product Design Support Partner for Insurance Companies | Source: Public Information, Interviews | Chart by VCBeat

Zhu Xuesong stated that through digital health platforms, the roles of internet healthcare as a tool for efficiency enhancement and a lever for payment will gradually converge, forming an HMO system characterized by collaborative efforts to fully safeguard the health of policyholders.

Taking WeDoctor as an example, its digital health platform comprehensively integrates technological capabilities, medical expertise, and pharmaceutical resources. On one hand, it provides commercial insurance companies with healthcare service support, including targeted big data analytics, medical artificial intelligence technologies, and health insurance settlement assistance. On the other hand, leveraging the big data advantages of the digital health platform, it collaborates with commercial insurers to build users’ digital health models. These models serve as the actuarial basis required by insurance companies, enabling product innovation and the customization of insurance solutions for the demand side. Ultimately, this approach delivers a full-process, closed-loop service covering prevention, medical consultation, medication, payment, and rehabilitation.

A representative from Ping An Health Insurance Technology stated that chronic disease management can enable risk control for specialized insurance products. For instance, scientific management of diabetes can mitigate the risk of complications, thereby making diabetes-specific insurance viable.

In this regard, Zhiyun Health is collaborating with insurance companies, leveraging historical consultation data to jointly develop customized products for specific diseases. Liu Xuejian revealed that over a long period, Zhiyun Health has accumulated a vast amount of data, enabling in-depth mining. This data is utilized not only to enhance the efficiency of chronic disease diagnosis, treatment, and management but also to support the design of commercial insurance products.

Through Zhiyun Health’s chronic disease management plus insurance model, policyholders gain medical coverage while enjoying professional digital health management services; for insurers, this approach helps ensure customer health and reduce overall claim ratios in the short term, while enhancing underwriting capabilities in the long term through more granular data and assessments.

Miao Health leverages its extensive experience in the digitalization of health management to collaborate with insurance companies in exploring solutions for controlling premium costs and managing risks, thereby designing and developing chronic disease insurance products that integrate chronic disease management with insurance coverage.

According to Wang Yanhua, General Manager of the Miao Bao Business Division at Miao Health, leveraging its core capabilities in AI, IoT, and big data, Miao Health has established three major platforms: the Miao+ IoT Health Big Data Platform, the H-Health Risk Stratification Management Platform, and the M-AI Health Intervention Platform. These platforms quantify users’ health status through scoring indices, analyze potential health risks, and provide timely interventions, covering the entire lifecycle to reduce the risk of disease.

Currently, Miao Health is also collaborating with reinsurers and insurance companies to advance health-promotion insurance policies that integrate risk coverage with health management. By leveraging multi-point interactions involving insurance agents and health managers, the company aims to harness the integrative payment capabilities of commercial insurance to achieve a comprehensive upgrade of health protection in insurance products.

Under the aforementioned collaboration model, it becomes feasible to develop more single-disease insurance products based on internet healthcare. Meanwhile, once the HMO system is established, patients, insurance companies, and internet healthcare firms can all benefit.

Internet Healthcare as a Product Channel for Insurance Companies

Finally, internet healthcare can also serve as a channel for insurance companies by establishing platforms for the display, sales, and consultation of insurance products.

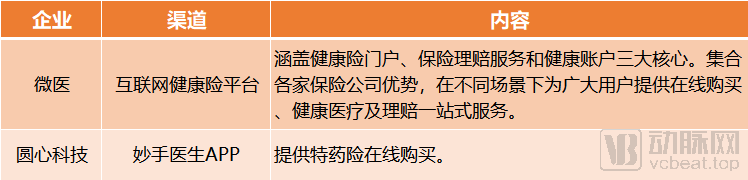

Internet Healthcare as a Product Channel for Insurance Companies: Source: Public Information, Interviews; Chart by VCBeat

WeDoctor’s internet health insurance platform encompasses three core components: a health insurance portal, insurance claims services, and health accounts. By integrating the strengths of various insurance companies, it provides users with online purchase options, healthcare services, and claims assistance. The Miaoshou Doctor app offers an online channel for purchasing specialty drug insurance.

Furthermore, Liu Xuejian revealed that Zhiyun Health has recently acquired an online sales license and plans to design sales scenarios for both online and offline customers to facilitate the conversion of insurance products.

This model is relatively more direct and straightforward, whereby internet healthcare companies leverage their traffic advantages to create sales scenarios for commercial health insurance and expand customer acquisition channels.

Internet healthcare lacks scaled payers, and commercial health insurance products and services are in urgent need of upgrading. During the exploration of the aforementioned four models, the two sectors have begun to connect based on their respective needs, but they still face certain challenges.

First is the challenge of data interoperability and sharing. In Wang Yanhua’s view, the fragmentation between in-hospital medical data and out-of-hospital health data poses a significant barrier to achieving precise cost control.

We have observed that the lack of interoperable data interfaces among medical institutions, healthcare security administrations, pharmaceutical companies, and retail pharmacies across various regions hinders the deeper integration of digital technologies—such as medical big data and artificial intelligence—with the traditional healthcare sector. Meanwhile, patient-centric models and regulatory frameworks for health data sharing remain to be improved.

Next is the challenge of user scale and conversion. Internet healthcare is positioned for consultation and follow-up visits, affecting a limited range of diseases and populations; thus, its overall scale still cannot rival that of traditional healthcare. Even though some platforms have amassed a large user base, driving users to make payments remains a long-term and arduous task.

In addition to enterprises needing to enhance product quality, service quality, and operational capabilities, addressing the aforementioned challenges also requires government efforts to promote the establishment and interoperability of medical and health data.

However, industry insiders interviewed in this article remain generally optimistic about the trend of integrating the two.

From the perspective of open policies regarding medical insurance, relevant executives at Ping An Medical Insurance Technology believe that enabling internet healthcare services to settle claims through basic medical insurance will accelerate their integration with commercial health insurance.

From the perspective of actual demand in commercial insurance, Wang Yanhua stated that the current loss ratio for health insurance in China is basically around 30%-40%, and was even as low as 10%-20% in previous years, representing a very small proportion. In contrast, the loss ratio for leading U.S. health insurers is approximately 80%-85%, indicating that there is still room for an increase in the domestic loss ratio. The underlying reason is that a significant portion of health insurance expenditures is allocated to customer acquisition, with marketing and channel costs accounting for a large share. Consequently, the funds actually applied to claims payments and medical services are relatively limited, suggesting that cost control and risk management capabilities need to be improved.

Following these reasons, the intersection between the two has become clearer. “The most explicit demands that commercial health insurance currently places on internet healthcare include whether it can play a key role in customer acquisition, cost containment, and improving customer satisfaction,” said Liu Xuejian.

So, how can internet healthcare help commercial insurance companies acquire customers, control costs, and improve customer satisfaction? There are two main directions:

For patients, we provide a comprehensive suite of services spanning the pre-hospital, in-hospital, and post-hospital phases. The pre-hospital phase focuses on establishing a tiered diagnosis and treatment system to precisely match medical resources, starting with online consultations and resorting to hospital visits only when necessary, thereby reducing costs. The in-hospital phase primarily involves integrating internet-based healthcare into hospital operations to enhance physicians’ diagnostic and treatment efficiency, shorten hospital stays, and consequently lower medical expenses. The post-hospital phase centers on providing follow-up management to facilitate rapid patient recovery and prevent mild conditions from progressing to severe ones.

For healthy individuals, internet-based healthcare can provide professional health monitoring and guidance, fulfilling the role of “preventive care” by enhancing overall health management awareness among residents and meeting their daily wellness needs. Leveraging advanced AI and big data capabilities, it delivers precise solutions for health and chronic disease management, directing insurance premiums toward prevention to reduce disease risk and thereby lower treatment costs.

Furthermore, Wang Yanhua noted that the direction of medical insurance reform can serve as a reference. For instance, costs can be controlled through centralized procurement of medical resources, while digitalization integrates hospitals, physicians, and pharmaceuticals to create a seamless connection between products and services via volume-based procurement or membership models. Meanwhile, insurance premiums should be allocated more heavily toward prevention to reduce expenditures on disease treatment.

Looking further ahead, what position might commercial health insurance payments occupy within the internet healthcare payment system? In this regard, Zhu Xuesong believes that, based on digital platforms, the gradual maturation and scaling of internet healthcare will also serve as a critical tipping point for promoting the true large-scale development of health insurance. In 2018, the market size of China’s health insurance (based on gross written premiums) was RMB 544.8 billion; it is projected that by 2025, the health insurance market size will exceed RMB 2 trillion. In 2018, health insurance claims accounted for 3% of total healthcare expenditures. Conservatively estimated, by 2025, health insurance claims will account for 10% of total healthcare expenditures.

“With the development of the digital economy, internet healthcare and internet insurance have entered a fast track. Based on the aforementioned growth rate of 3% to 10%, it is projected that commercial insurance will account for no less than 10% of payments in the future online medical payment system.”

Acknowledgments:

Zhu Xuesong, Head of WeDoctor Health at WeDoctor Group

Liu Xuejian, Head of the Insurance Business Department at Zhiyun Health

Wang Yanhua, General Manager of the Miao Bao Business Unit at Miao Health

Relevant Person in Charge at Ping An Health Insurance Technology