National High-Value Medical Consumables Centralized Procurement Launches, Reshaping the Multi-Billion Coronary Stent Market

On October 16, the Joint Procurement Office for National Organization of High-Value Medical Consumables released the "National Centralized Volume-Based Procurement Document for Coronary Stents," with the Tianjin Pharmaceutical Procurement Center undertaking the daily operations of the Joint Procurement Office and issuing negotiation invitations to relevant enterprises.

The release of the document signifies that the national centralized procurement of high-value medical consumables has begun to be implemented, with the nationwide volume-based procurement of such items rolling out faster than anticipated.

Previously, the implementation of volume-based procurement (VBP) for pharmaceuticals was preceded by years of policy signaling and preparation, including the introduction of a series of measures such as the consistency evaluation. Only then did the VBP policy for drugs finally take effect. Based on this, some industry insiders believed that VBP for high-value medical consumables would also require preliminary preparations, such as the standardization of coding for medical consumables, and that national-level VBP for high-value medical consumables would not be implemented in the short term. However, the policy rollout was swift. Between 2019 and 2020, centralized procurement of high-value medical consumables advanced rapidly across various regions, becoming a widespread trend. Moreover, it took only one year to transition from local pilot programs to nationwide centralized procurement.

China’s national volume-based procurement (VBP) initiative targeted coronary stents, with domestically produced products accounting for 80% of the market. The total intended procurement volume in the first year was 1,074,722 units, with a reference price of RMB 2,850, driving down the price of cardiac stents from the ten-thousand-yuan range to the thousand-yuan range. What precedent does this national VBP scheme set for centralized procurement of high-value medical consumables across China, and how will it impact the high-value medical consumables industry? VCBeat (WeChat ID: vcbeat) has compiled and analyzed these developments.

The public announcement of the national volume-based procurement plan has addressed many questions regarding how the national volume-based procurement operates.

First is the question of “what to include” in volume-based procurement (VBP) of high-value medical consumables, namely, the selection of product categories for VBP. Unlike pharmaceuticals, high-value medical consumables, while broadly similar, often feature innovations manifested as subtle improvements. This results in a highly fragmented landscape of product variants, posing significant challenges for nationwide volume-based procurement.

Products subject to volume-based procurement require a comprehensive assessment of factors such as physician preferences, product risks, degree of product differentiation, and market supply risks. Given the substantial procurement volumes involved in national centralized bulk procurement of high-value medical consumables, consideration of these factors becomes even more critical.

The coronary stents included in this volume-based procurement program can be broadly categorized into bare-metal stents and drug-eluting stents. However, there are significant differences among various stents in terms of drug loading dose, drug release kinetics, and manufacturing processes, which in turn determine their radial strength, fractional flow reserve (FFR), and complication rates. Taking MicroPort Medical as an example, its coronary stent portfolio comprises three major product series: Firebird (Firebird Sirolimus-Eluting Coronary Stent System), Firehawk (Firehawk Targeted Elution Sirolimus-Eluting Coronary Stent System), and Firesorb (Firesorb Bioresorbable Sirolimus-Eluting Targeted Coronary Stent System).

The coronary stents selected this time. In terms of domestic production, the share of Chinese-made products has reached 80%. The technical barriers for coronary stents are relatively lower, but the industry scale is large. At present, second- and third-generation coronary stents account for as high as 99% of the market. In the field of coronary stents, there are four main domestic suppliers: MicroPort Medical, Lepu Medical, Jiwei Medical, and Sino Medical. The competitive landscape is tending to stabilize, and market concentration continues to increase, providing a basis for trading volume for price.

How to define the competitive landscape for numerous high-value consumables, providing patients and physicians with a degree of choice while allowing companies room for competition, and how to determine the appropriate level of granularity in consumable categorization—these questions are addressed in the current announcement.

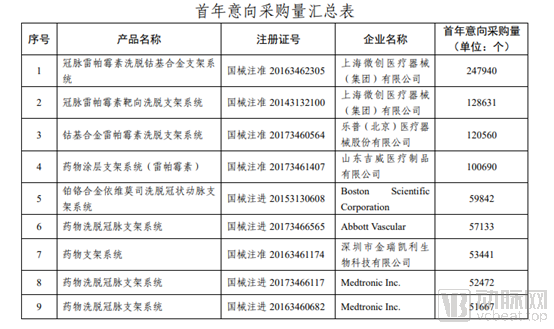

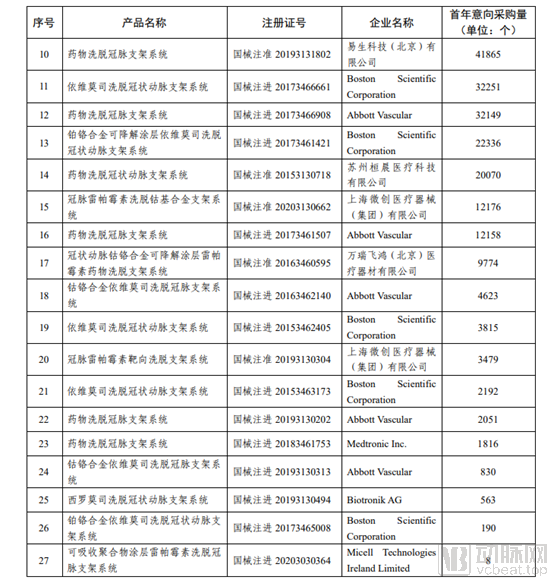

The products selected for this national centralized procurement are coronary drug-eluting stent systems, categorized by material into cobalt-chromium alloys or platinum-chromium alloys, with rapamycin and its derivatives as the loaded drugs. This grouping is not complex, primarily classified based on material and drug type. The initial year’s intended procurement volume table also reveals that the highest demand is for conventional products, while demand for functionally innovative stents is limited. For instance, the intended procurement volume for bioresorbable stents in the first year is only eight units.

Next, regarding the selection and standards for “volume,” previously, under local volume-based procurement models, there were three approaches to determining the procurement volume: one based on market share; another based on enterprises’ historical usage volumes and proportions; and the third based on actual market usage.

The national volume-based procurement adopts a method that allocates market share by specifying the percentage of annual usage within the region. The confirmed procurement volume is determined based on the total procurement demand reported by medical institutions in the alliance regions, with the intended procurement volume serving as the basis. Specifically, the total intended procurement volume for the first year is 1,074,722 units, calculated as the sum of 80% of the total procurement demand reported by each medical institution in the alliance regions.

Based on the intended procurement volumes in the first year of China’s national centralized volume-based procurement (VBP) for high-value medical consumables, MicroPort had the largest intended procurement volume, with cumulative demand for its four product categories totaling approximately 390,000 units, accounting for about 36% of the total. Lepu Medical ranked second, with cumulative demand for one product category reaching 120,560 units, representing approximately 11% of the total. Other domestic companies shortlisted include Shandong Jiwei, Jinrui Kaili, Yisheng Technology, Suzhou Huanchen, and Wanrui Feihong.

Among foreign-funded enterprises, Boston Scientific has a demand of approximately 120,000 units across six product varieties; Abbott has a demand of approximately 110,000 units across six product varieties; and Medtronic has a demand of approximately 110,000 units across three product varieties.

From the perspective of evaluation criteria, industry experts previously believed that national volume-based procurement (VBP) for high-value medical consumables would draw on the models used in VBP for pharmaceuticals and local VBP for consumables, incorporating negotiation, competitive bidding, and expert assessment to maintain established clinical practices.

However, an analysis of the newly released scheme reveals the absence of bidding combined with expert evaluation and negotiation; only a pure bidding mechanism is employed. This implies that the dramatic “soul-searching price cuts” characteristic of drug price negotiations will not occur. Instead, volume-based procurement for high-value medical consumables will adhere to a “lowest bidder wins” principle, favoring products with the most substantial price reductions.

In the event of identical pricing, the centralized procurement plan explicitly stipulates that ranking shall be determined based on two criteria: first, priority is given to products with higher sales volumes in 2019 (based on historical procurement data submitted by each province); second, priority is given to manufacturers whose initial registration certificates were issued earlier by the National Medical Products Administration (based on the initial approval date granted by the National Medical Products Administration).

The former primarily considers physician acceptance and market share of the product, while the latter mainly evaluates the product’s innovativeness. With regard to price, market acceptance, and innovativeness, the core evaluation criterion for China’s national centralized procurement of high-value medical consumables is price.

So, what is the preferred “price” for high-value medical consumables nationwide? How is it determined? It can be observed that the price of RMB 2,580 set in this national centralized procurement is the lowest negotiated price for drug-eluting coronary stents in Jiangsu Province’s volume-based procurement program, and it now serves as the reference price for the national volume-based procurement of coronary stents. Compared with the prices submitted by various manufacturers in Jiangsu Province’s volume-based procurement of coronary stents, this represents a significant price reduction.

Taking MicroPort, the leading domestic manufacturer, as an example, it had the highest procurement volume in this volume-based procurement (VBP) program, with a cumulative demand of 390,000 units. In Jiangsu Province’s VBP, MicroPort quoted RMB 7,500 for its standard Huoniao stent, while the negotiated price was RMB 3,400. This price still leaves room for further reduction relative to the reference price of RMB 2,850.

For imported manufacturers, the reference price of RMB 2,850 implies a price reduction of 80% or even higher. This price range also demonstrates the determination of China’s national centralized procurement to eliminate inflated margins and bring down the artificially high prices of high-value medical consumables.

Previously, in the coronary stent market, domestically produced stents were priced at approximately RMB 9,000–11,000, while imported stents ranged from RMB 15,000 to 19,000. The national centralized procurement of high-value medical consumables may directly usher in an era where coronary stents are priced in the thousands of yuan.

Volume-based procurement of pharmaceuticals has reshaped the landscape of the pharmaceutical industry. In the field of cardiac stents, what impact does the national centralized procurement of high-value medical consumables have on the high-value medical consumables industry?

First, from the perspective of the coronary stent market, nationwide volume-based procurement will reshape the entire landscape of the coronary stent market.

Coronary stents are a segment of the cardiac device market. A coronary stent is a medical device commonly used in percutaneous coronary intervention (PCI), whereby the stent is implanted into the narrowed section of a blood vessel using a conventional balloon dilation catheter, thereby restoring patency to the arterial vessel. Due to its minimally invasive nature and favorable outcomes, PCI has become one of the primary approaches for treating cardiovascular stenosis.

Coronary stents represent a market valued at over RMB 10 billion. In 2018, the market size for PCI cardiac stents in China was approximately RMB 14.294 billion, with a growth rate of 10.49%.

Data on percutaneous coronary intervention (PCI) for coronary heart disease in mainland China in 2018 showed that the total number of PCI procedures performed throughout the year was 915,256, with an average of 1.46 stents implanted per patient. This indicates that the demand for PCI in China is rapidly expanding.

The companies selected in this volume-based procurement are primarily the leaders in the coronary stent field. Among them, MicroPort’s intended volume for the first year far exceeded that of other companies, accounting for approximately 36% of the total procurement volume. Prior to the implementation of volume-based procurement, MicroPort had consistently been the market leader in coronary stents, holding the largest market share. In 2018, the market shares of the four domestic coronary stent suppliers were as follows: MicroPort held 23.52%; Lepu Medical held 21.02%; Jiwei Medical accounted for 15.65%; and Sino Medical accounted for 11.23%.

In this volume-based procurement, all of Sino Medical’s products are made of stainless steel and thus fail to meet the procurement criteria; in contrast, the flagship products of the other three companies all satisfy the requirements and are eligible to participate in the centralized procurement.

Although the results of the current volume-based procurement have not yet been finalized, it is foreseeable that this round will benefit leading domestic manufacturers. The market share of these industry leaders will further expand, and industry concentration will continue to rise.

From the perspective of the entire high-value cardiovascular interventional consumables industry, the volume-based procurement (VBP) of coronary stents has also had a profound impact. VBP will affect the entire industrial chain of high-value medical consumables, and the industry may undergo a significant reshuffle.

In the medical device industry chain, distribution relies more heavily on distributors compared to pharmaceuticals, and the market landscape in the medical device distribution sector is relatively fragmented. The implementation of volume-based procurement (VBP) will compress channel profits and promote industrial upgrading and development. In the long run, VBP will increase the market share of domestically produced high-value consumables. Leading Chinese manufacturers with independent innovation capabilities, diversified business layouts, or single products featuring high technological content and added value—thus holding clear advantages in differentiated competition—are expected to benefit from the increasing industry concentration.

An industry insider told VCBeat, “In the traditional model, distributors held more bargaining power than manufacturers across the entire industry chain. Frankly speaking, gross margins were higher at the distribution stage. The long-term implementation of volume-based procurement (VBP) policies will shift more of the profit chain toward the manufacturing end. Of course, this transition will take some time.”

Regarding whether volume-based procurement will affect the overall valuation of the industry, some medical device investors have stated that although volume-based procurement has lowered prices in the terminal market, it also leaves room for innovation. Although the prices of end products are declining, the market share of domestically produced products can increase significantly, capturing a larger market from imported products. Essentially, as long as products possess sufficient innovation, companies still retain a certain degree of bargaining power; exchanging volume for price is also a business strategy.

A major difference between the national centralized procurement of high-value medical consumables and that of pharmaceuticals is that the latter covers a wide variety of products, whereas the former currently involves only a single product category. In the future, the normalized model for high-value medical consumables may differ from the established volume-based procurement model for pharmaceuticals.

Prior to the implementation of national centralized volume-based procurement for high-value medical consumables, many regions had already conducted volume-based procurement at the alliance, provincial, and municipal levels. Participating provinces and municipalities included Jiangsu, Anhui, Shandong, Chongqing, Shanxi, Liaoning, Gansu, Hunan, Yunnan, and Hainan. In terms of product categories, provincial-level initiatives primarily focused on high-value medical consumables, whereas municipal-level efforts mainly targeted low-value medical consumables.

How Do National and Local Volume-Based Procurement Programs Coordinate?

Previously, Industrial Securities predicted that regarding the coordination between local and central authorities in the volume-based procurement (VBP) of high-value medical consumables, the respective responsibilities and powers of the central and local governments are gradually becoming clearer. The majority of centralized procurement for medical consumables will continue to be led by local authorities, while central departments will be responsible for the centralized procurement of special categories. This prediction aligns well with the current national model of volume-based procurement.

In the future, national volume-based procurement (VBP) may expand to cover more product categories. Based on the current high-value medical consumables procured by provincial and municipal alliances, products already included in centralized procurement include ophthalmic intraocular lenses, vascular interventional high-value consumables, and orthopedic consumables. The expansion of national centralized procurement for medical consumables is highly likely to start with these categories. For intraocular lenses, vascular interventional devices, and orthopedic high-value consumables, certain subcategories have a high degree of localization and limited product differentiation, laying the foundation for volume-based procurement.

Over the past decade, China’s medical device industry has maintained robust growth. This expansion has been driven by rising living standards, increasing demand for healthcare services, and advancements in medical device technology, while also benefiting significantly from regulatory standardization and policy support. After decades of development, the industry is now in a phase of evolutionary transformation. Regulatory frameworks are continuously being refined. From the perspective of healthcare payment, the implementation of volume-based procurement (VBP) is reshaping the supply chain and market landscape of the medical device sector, stimulating innovation, facilitating the commercialization of R&D achievements, and optimizing the allocation of industry resources. In the future, as VBP becomes routine, the high-value consumables sector is expected to undergo further positive transformations, a trend that VCBeat will continue to monitor closely.