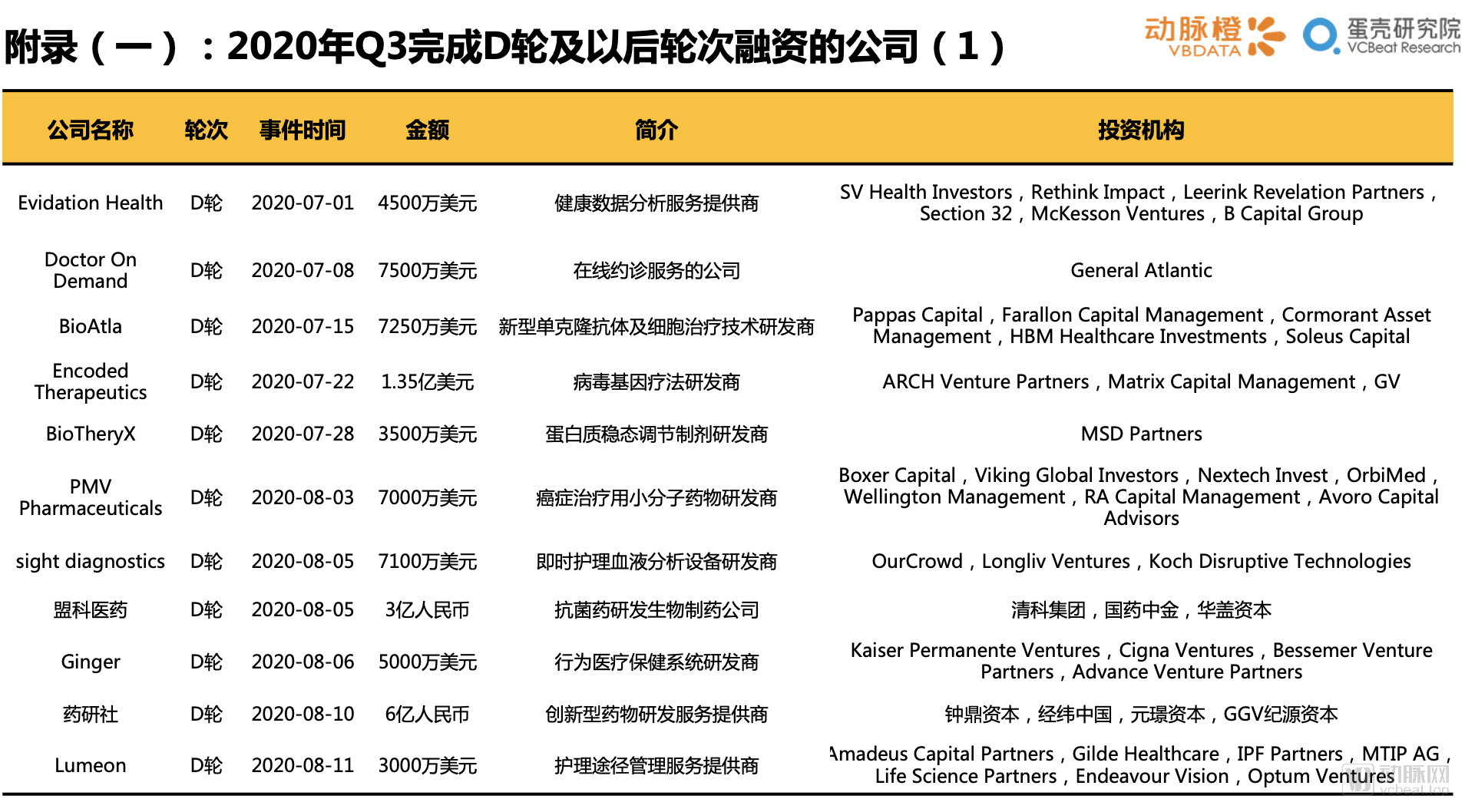

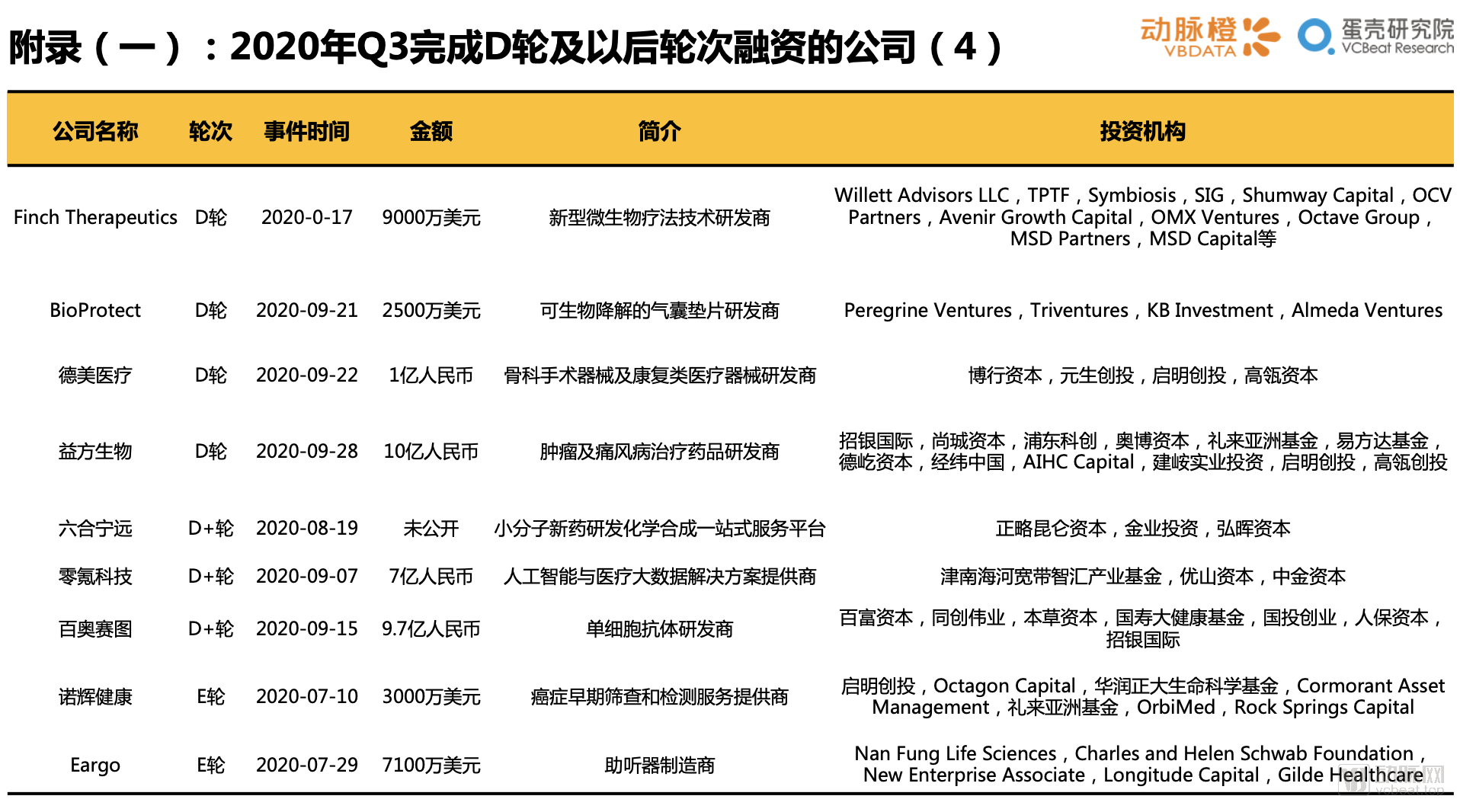

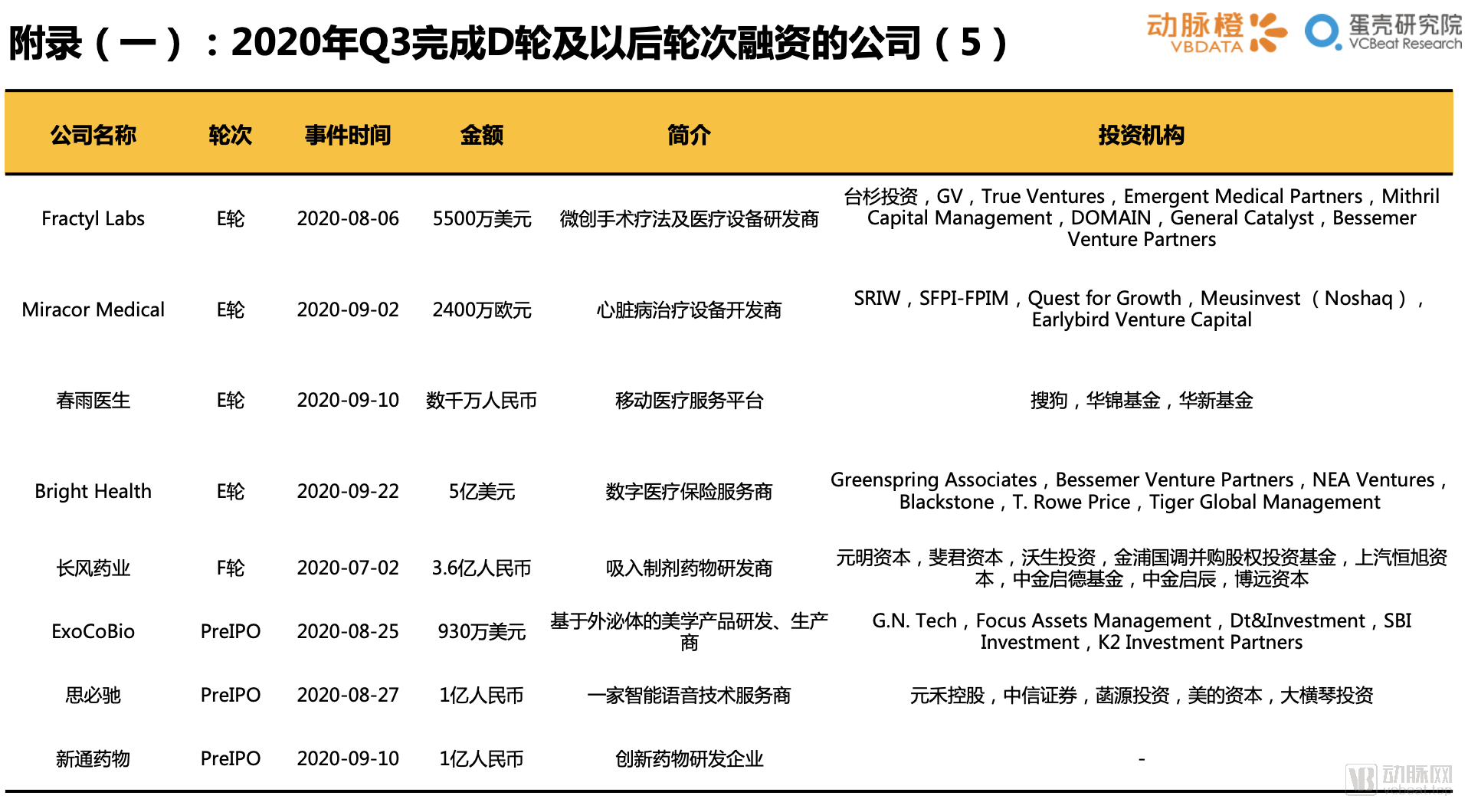

Global Healthcare Industry Capital Report Q3 2020

I. Global healthcare sector saw particularly active financing in Q3, with China standing out: Total global financing in Q3 2020 hit a record high for any third quarter on record; the number of financing deals in China rebounded in Q3, rising by approximately 50%, suggesting a potential turning point and a likely easing of the relatively tight funding environment for domestic startups since 2018.

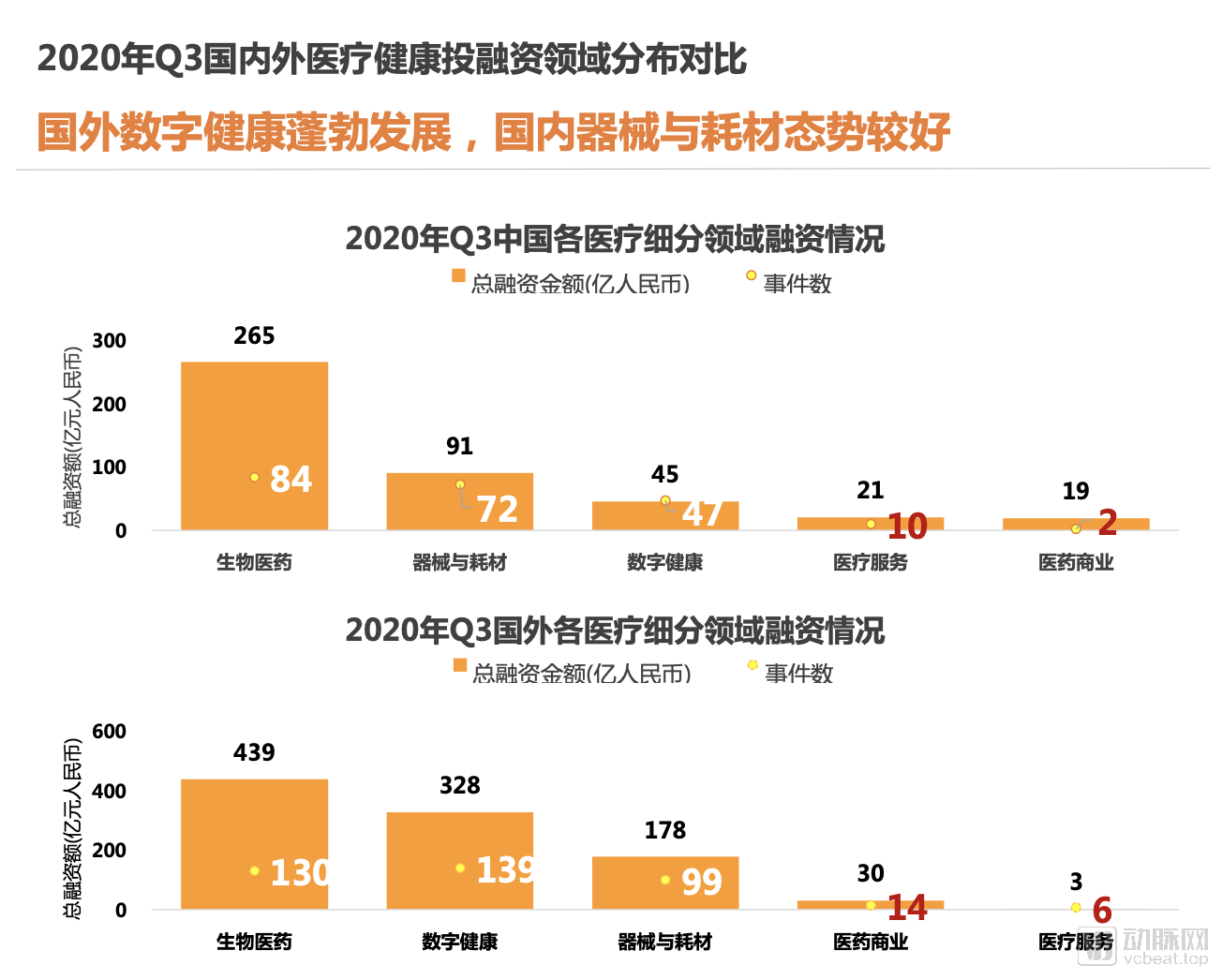

II. The biomedical sector continues to hold an absolute lead both domestically and internationally in terms of the number and volume of financing deals. Digital health is flourishing abroad, while the domestic medical device and consumables sectors are showing strong momentum.

III. Growth in Niche Segments: Overseas digital health companies are maturing, with as many as 15 financing rounds exceeding $100 million; a financing boom is sweeping through China’s medical robotics sector, where the domestic substitution of surgical robots holds promising prospects.

IV. In terms of capital inflow, leading institutions have poured capital into the healthcare industry with unprecedented intensity. OrbiMed and Hillhouse Capital (including its venture capital arm) each invested in more than 20 healthcare companies in a single quarter—a historic first—while 11 firms each made over 10 investments within a single quarter.

V. Strong Performance of Healthcare IPOs in Q3 2020: A total of 65 IPOs were launched across the A-share, U.S., and Hong Kong stock markets, raising over RMB 100 billion; 39 companies went public on the U.S. market, marking a robust comeback.VI. Over 200 financing deals occurred in a single quarter in China and the U.S.; the geographical distribution of healthcare financing in China has initially shifted: Shanghai’s explosive growth in total financing volume has driven the development of the Yangtze River Delta region, surpassing Beijing by a wide margin.

7. Bright Health’s $500 Million Financing Round Tops Global Q3 2020 Funding Rankings; Three Chinese Companies Make the List.

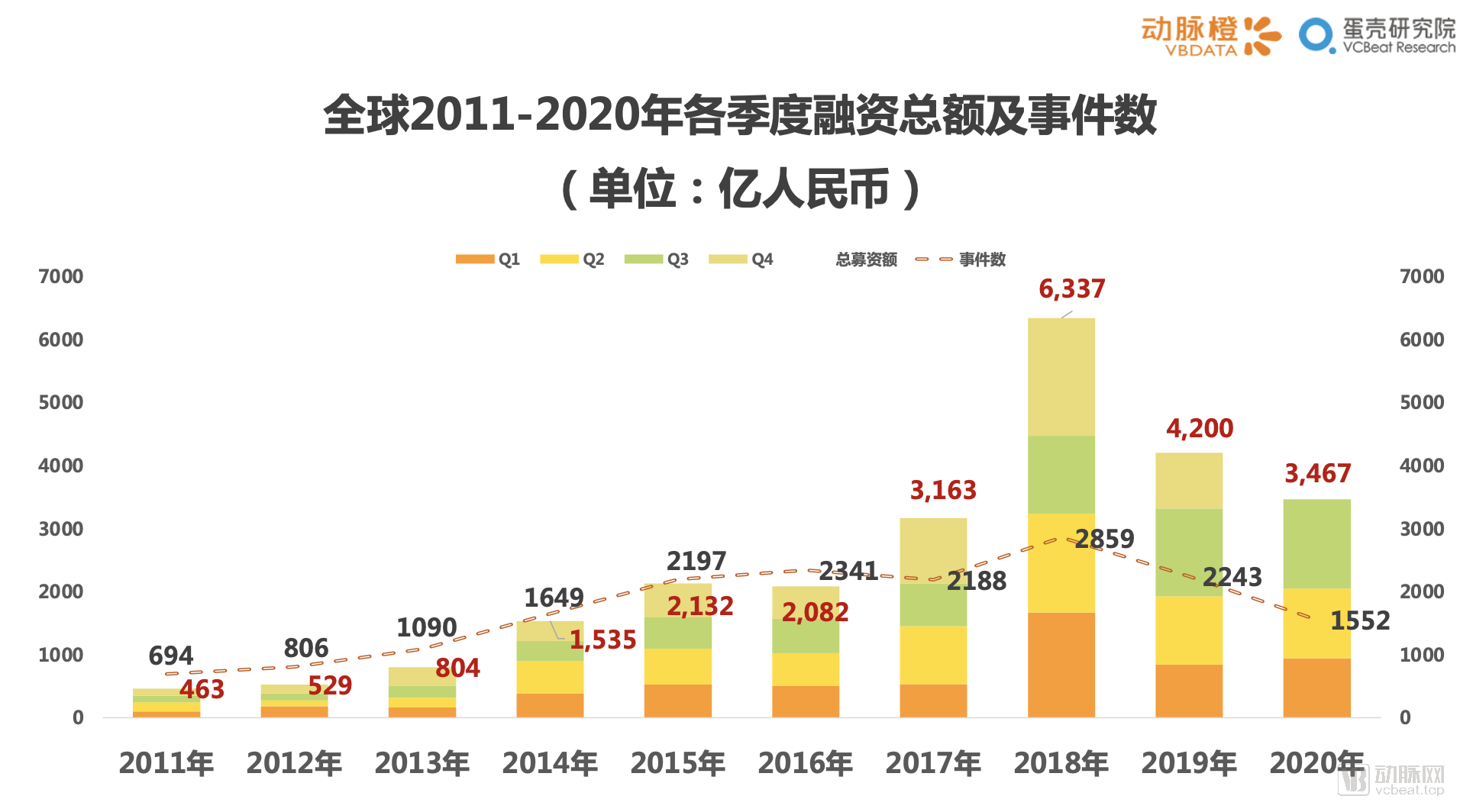

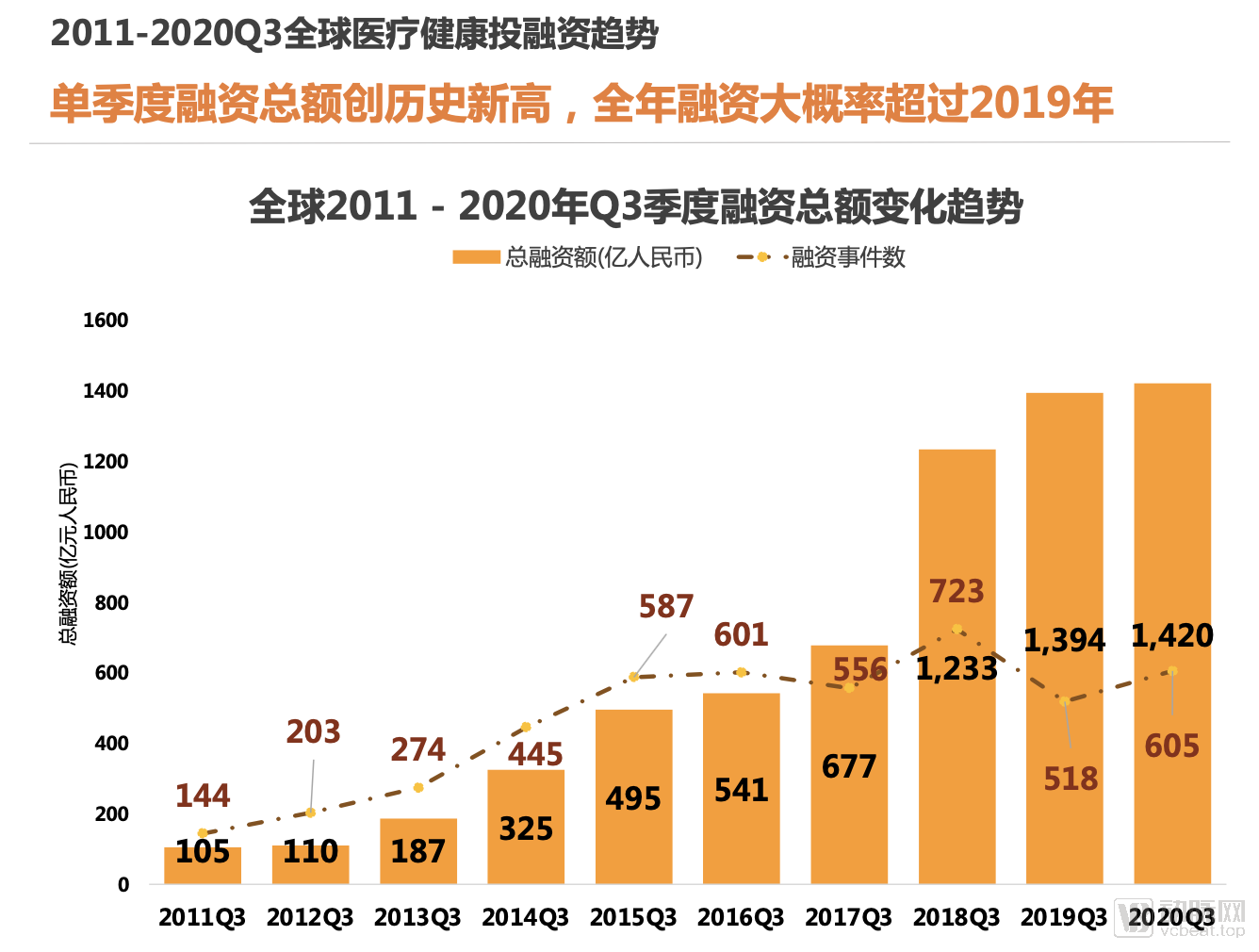

1.1 Global single-quarter financing hits a record high for Q3 across all years; full-year financing is highly likely to surpass last year’s total

In the first half of 2020, there were a total of 605 financing events in the global healthcare industry (including 37 events with undisclosed amounts), with the total financing amount reaching $20.3 billion (approximately RMB 142 billion), setting a new historical high for Q3.

Meanwhile, global healthcare financing reached RMB 346.7 billion by Q3 2020. Based on this trend, the total financing for the full year is projected to significantly exceed the 2019 level (RMB 420 billion). Taking multiple factors into account, we assess that the stimulative effect of the COVID-19 pandemic on capital investment in healthcare far outweighs its negative impact.

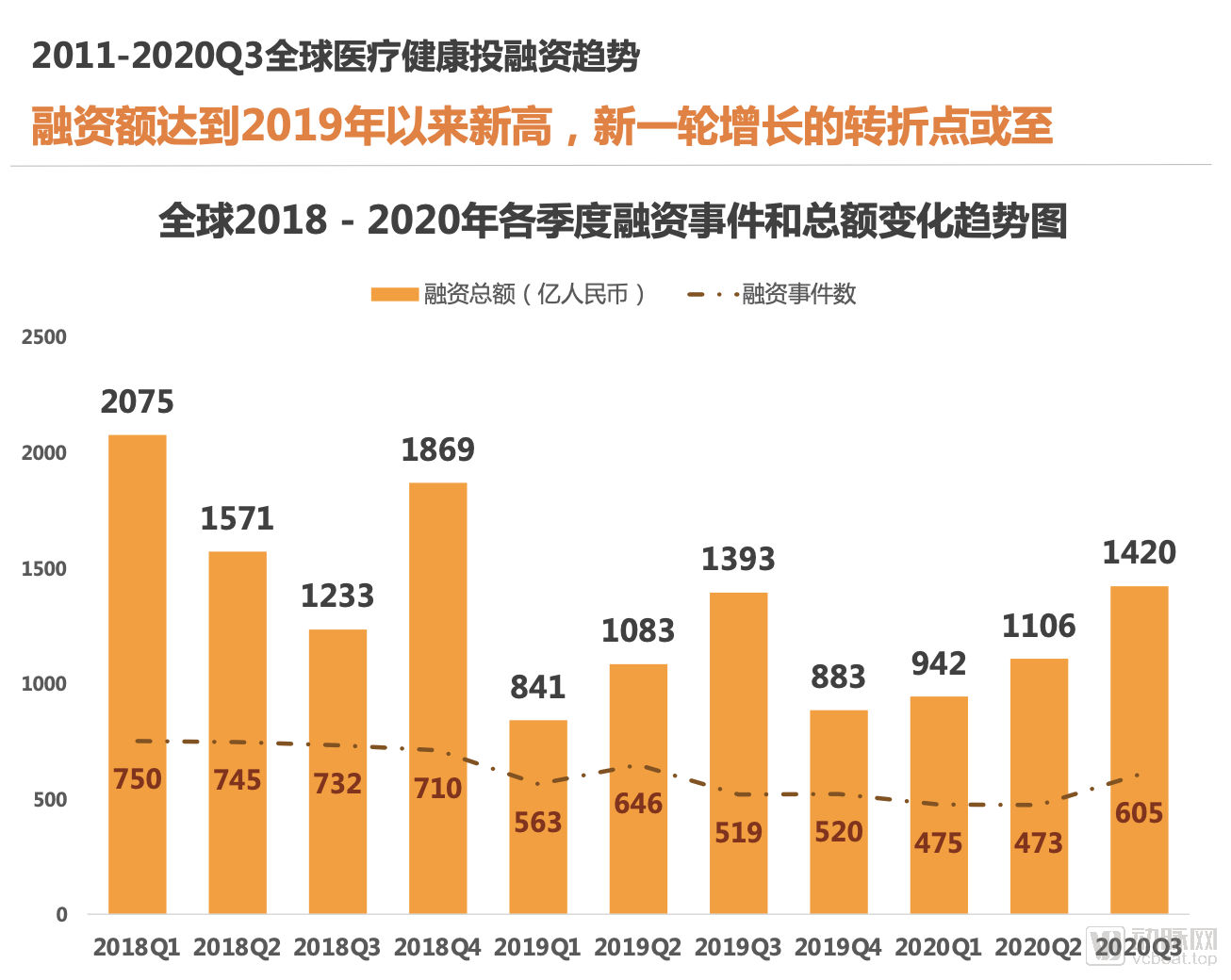

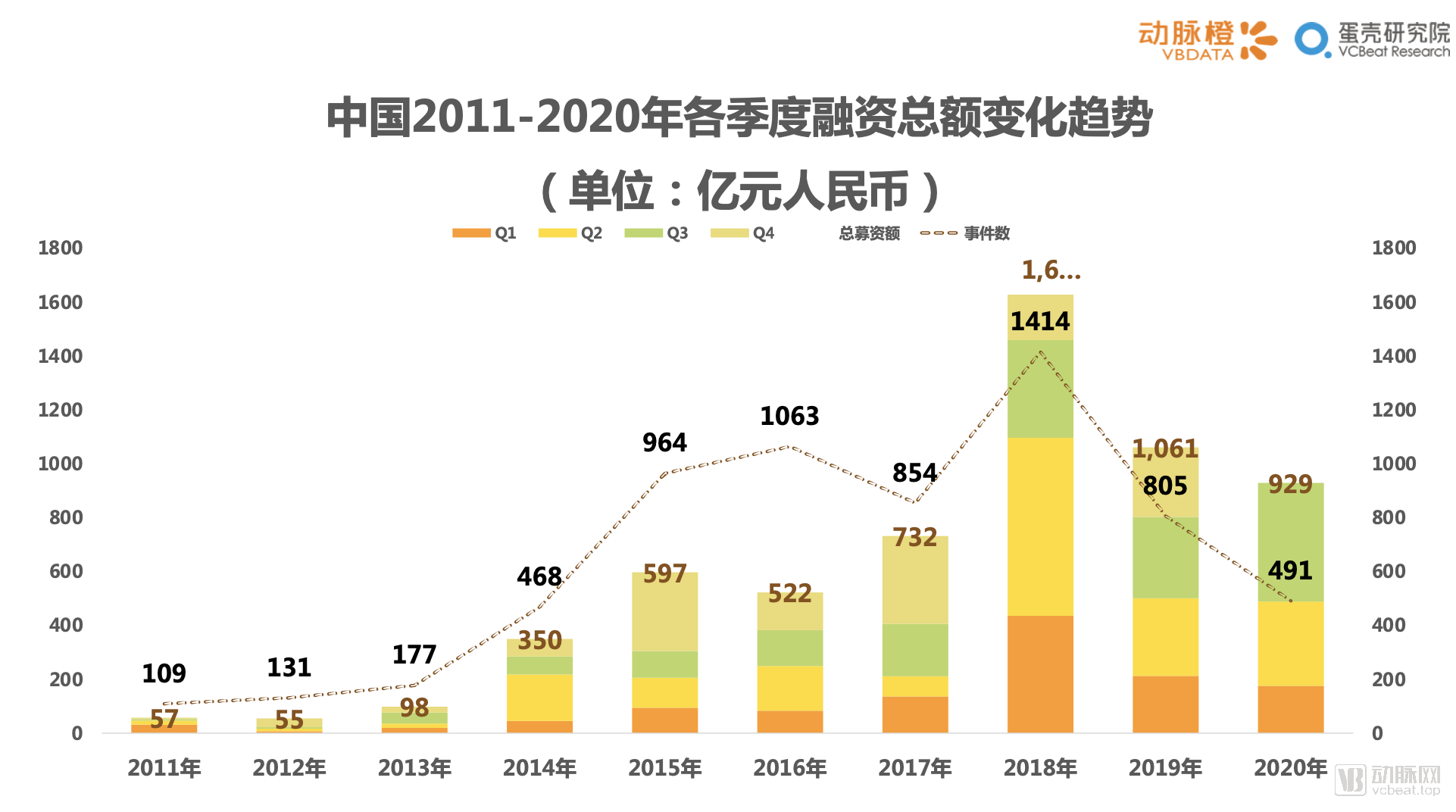

Based on the trend of financing transactions across quarters over the past two years, the total financing amount in Q3 2020 reached a new high for seven consecutive quarters since 2019. Although there is still a gap compared to 2018, the most active year for healthcare investment and financing, a turning point has emerged amidst the overall downward trend. We anticipate that a new wave of investment and financing will arrive as expected.

In addition, the number of financing events increased by 28% month-on-month. A new surge in funded projects has alleviated the significant decline in the number of financing deals observed in the first half of this year. Based on this trend, the financing environment for global healthcare startups is expected to improve in the near future.

1.2 Sustained Development of the Overseas Healthcare Industry: Number of Financing Projects Hits Record High for Q3

In Q3 2020, the overseas healthcare and medical industry continued to thrive, with total financing reaching $14 billion (approximately RMB 97.8 billion); the number of financing deals stood at 388, surpassing the previous peak recorded in Q3 2018.

As can be seen, although the COVID-19 pandemic continues to rage abroad in recurring waves, its impact on global healthcare venture capital investment has unfolded as we anticipated: after a brief period of negative effects, it has provided a more sustainable stimulus to the development of the healthcare industry, particularly in sub-sectors such as vaccines, in vitro diagnostics (IVD), and telemedicine. The response from the capital market serves as compelling evidence.

Observing the quarterly trends in investment and financing within the overseas healthcare industry over the past two years, the third quarter is typically the most active period for fundraising annually. Overseas, the quarterly fluctuation in the number of financing events has generally been modest; however, the 388 transactions recorded this quarter reached the highest level since Q2 2019, indicating an increase in trading activity.

Affected by the Christmas holiday season abroad, financing in the fourth quarter is theoretically expected to decline to some extent. Based on this trend, it is estimated that the total financing amount in foreign countries for the full year of 2020 will remain flat compared to the previous year.

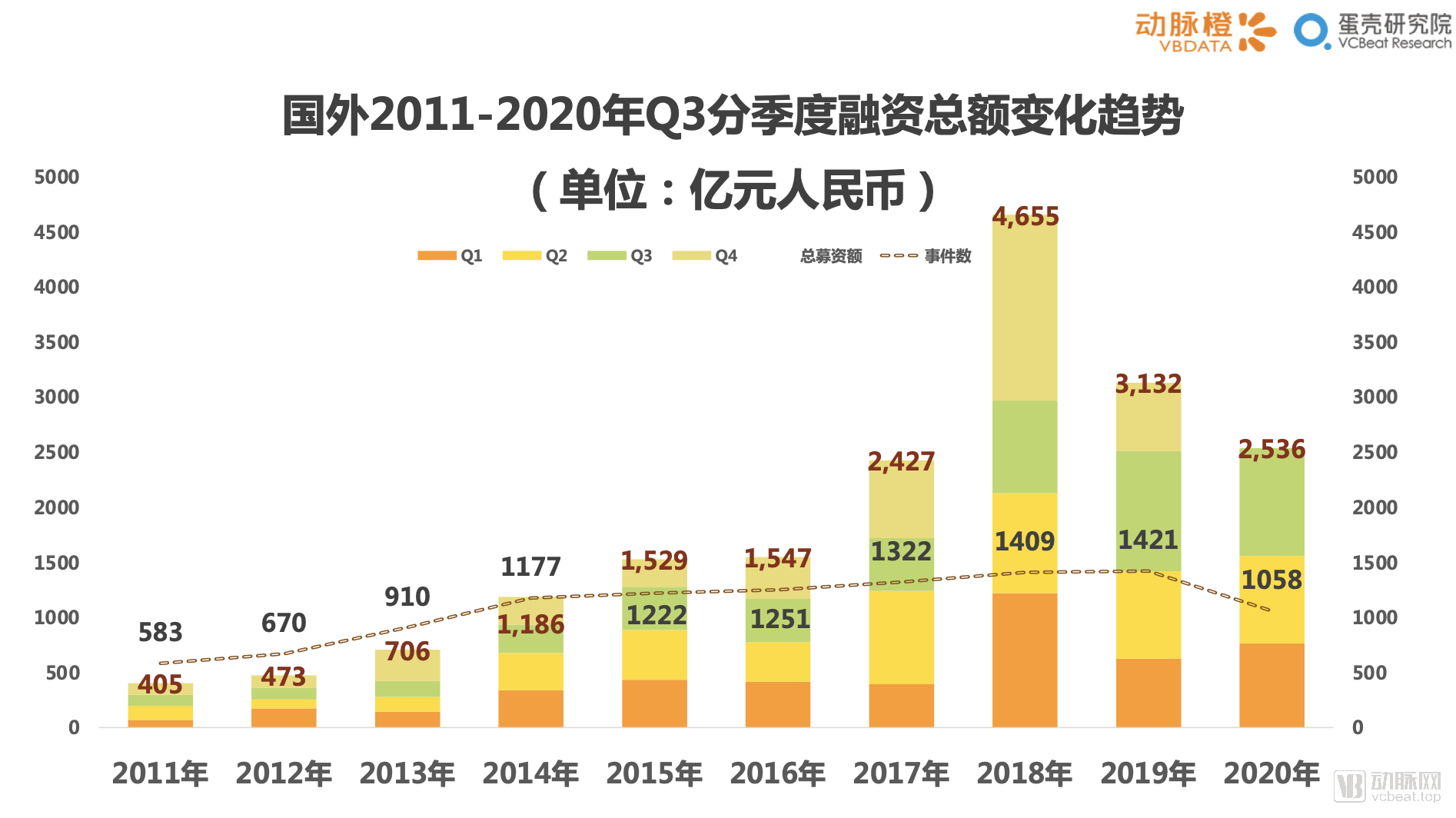

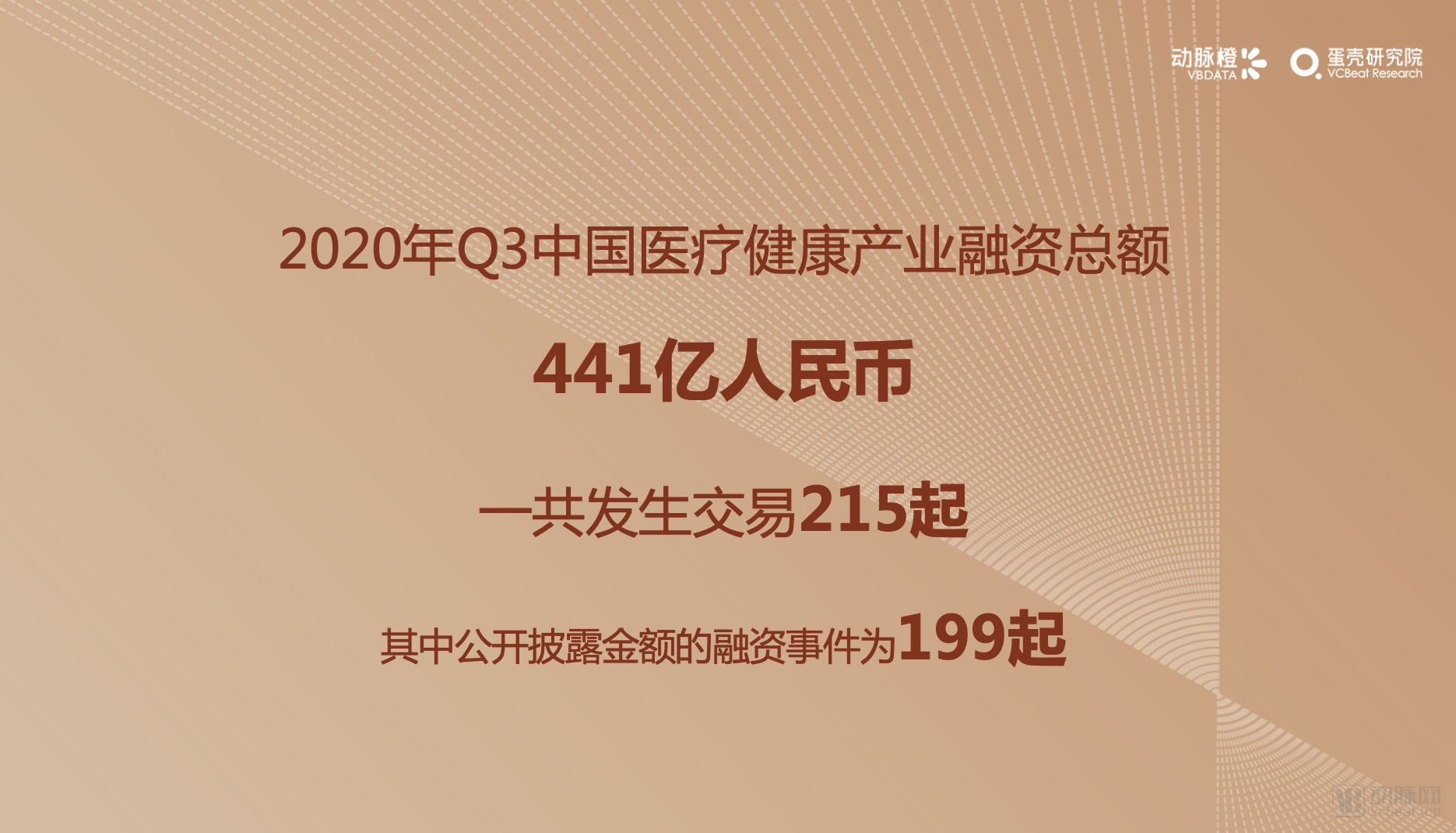

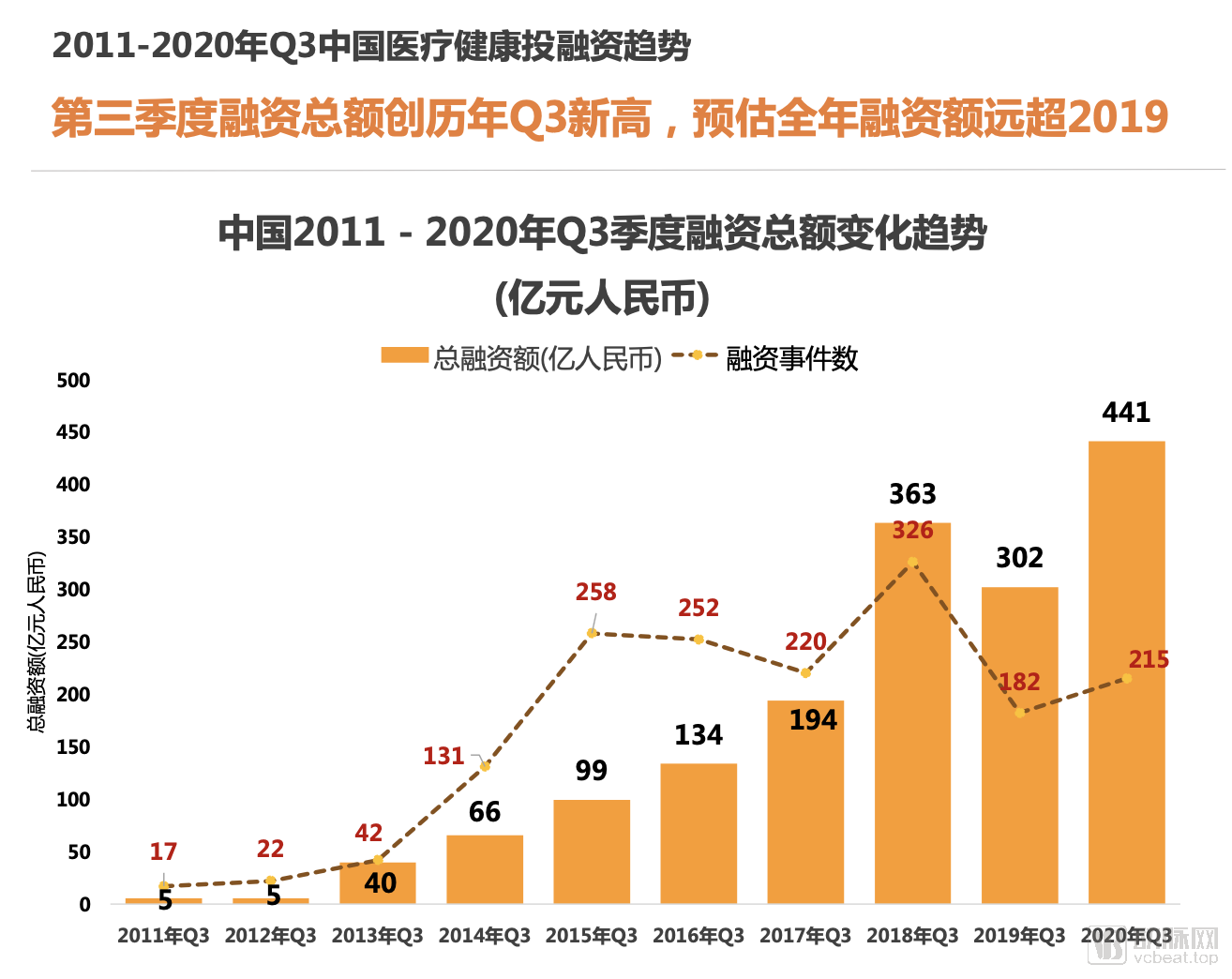

1.3 Domestic Financing Events Rebound in Q3, Rising by Approximately 50%, with Total Financing Amount Hitting a Record High for Q3 Across All Years

In the first half of 2020, China’s healthcare industry recorded 215 financing deals, an 18% year-on-year increase; total funding amounted to RMB 44.1 billion, up 46% year on year, while also setting a historical high for Q3 financing volume.

Meanwhile, as of Q3 2020, there had been 491 financing deals in China’s healthcare industry, totaling RMB 92.9 billion—just RMB 10 billion shy of the full-year total for the previous year. Based on this trend, the total financing amount for 2020 is projected to significantly surpass that of 2019.

Encouragingly, after a sharp decline in healthcare financing deals during the first half of the year, the venture capital market saw a rebound in funded projects this quarter. Following 135 deals in Q1 and 142 in Q2, the number of financing rounds in Q3 increased by over 50%.

Since 2018, the number of financing events per quarter has shown a continuous downward trend. However, the sharp surge in transactions this quarter may signal a new development: the increasingly stringent financing environment that has persisted since 2018 is expected to ease, paving the way for a new phase of sustained growth.

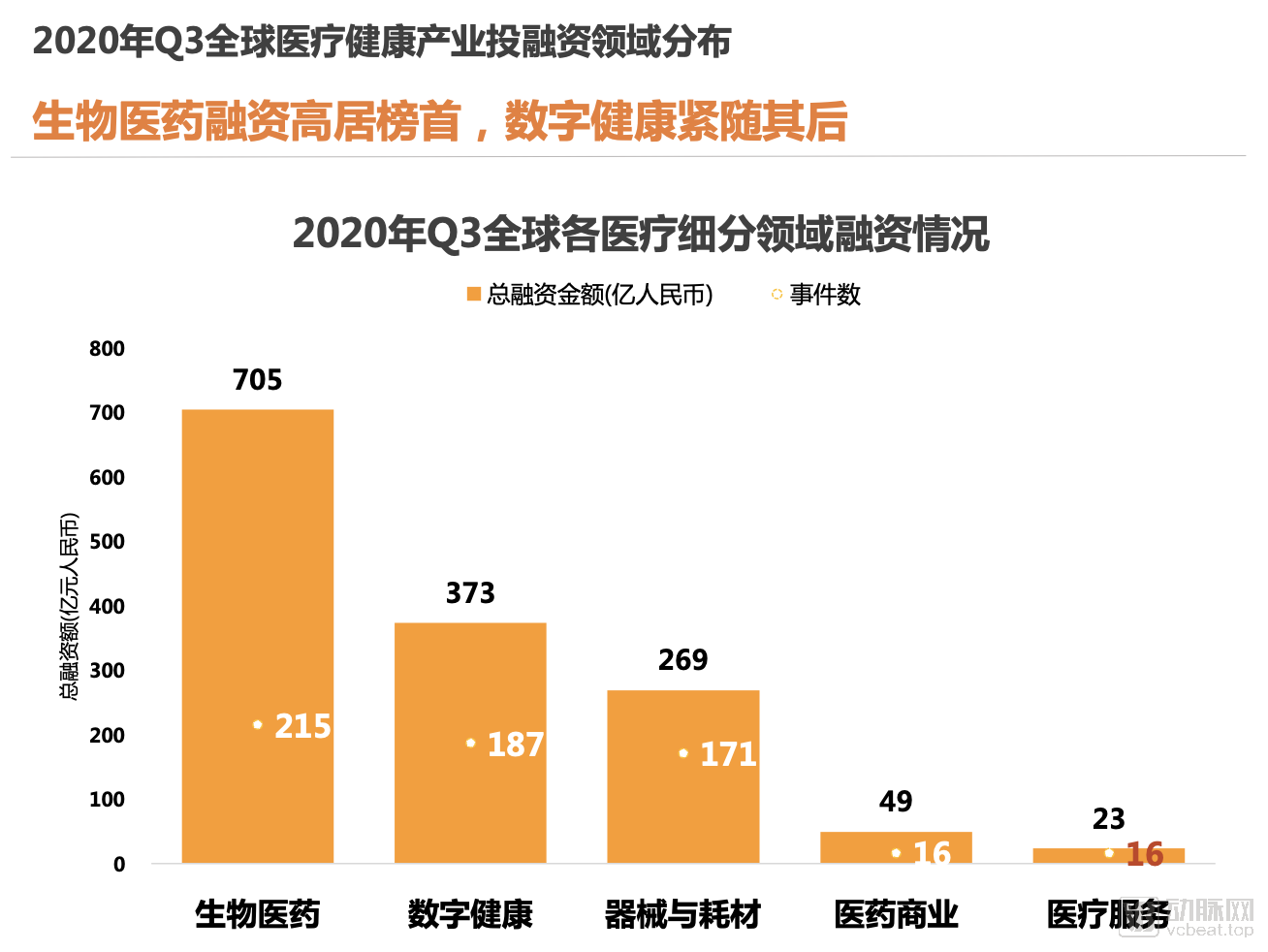

2.1 Global Distribution of Financing by Sector: Biopharmaceuticals Lead, Followed Closely by Digital Health

In the third quarter of 2020, the global biopharmaceutical sector once again topped all sub-sectors with 215 deals and a total financing amount of RMB 70.5 billion. In addition to the perennially hot biopharmaceutical field, companies in the digital health sector also maintained high activity levels. This indicates that digital health remained a key area of focus and preference for major investment institutions during this period, continuously driving the development and innovation of digital health.

2.2 Digital Health Thrives Abroad, While Domestic Medical Devices and Consumables Show Strong Momentum

A comparison of financing distribution across various healthcare sectors in China and abroad during the third quarter of 2020 reveals that biopharmaceuticals remained the most heavily favored sector both domestically and internationally. However, the focus of financing in other sectors differed.

Abroad, digital health is flourishing, with the $500 million Series E financing round completed by digital health insurance provider Bright Health being particularly noteworthy. In contrast, China is focusing more on the medical device sector. Among the 72 financing deals for medical device companies in China, 23 involved in vitro diagnostics (IVD) firms.

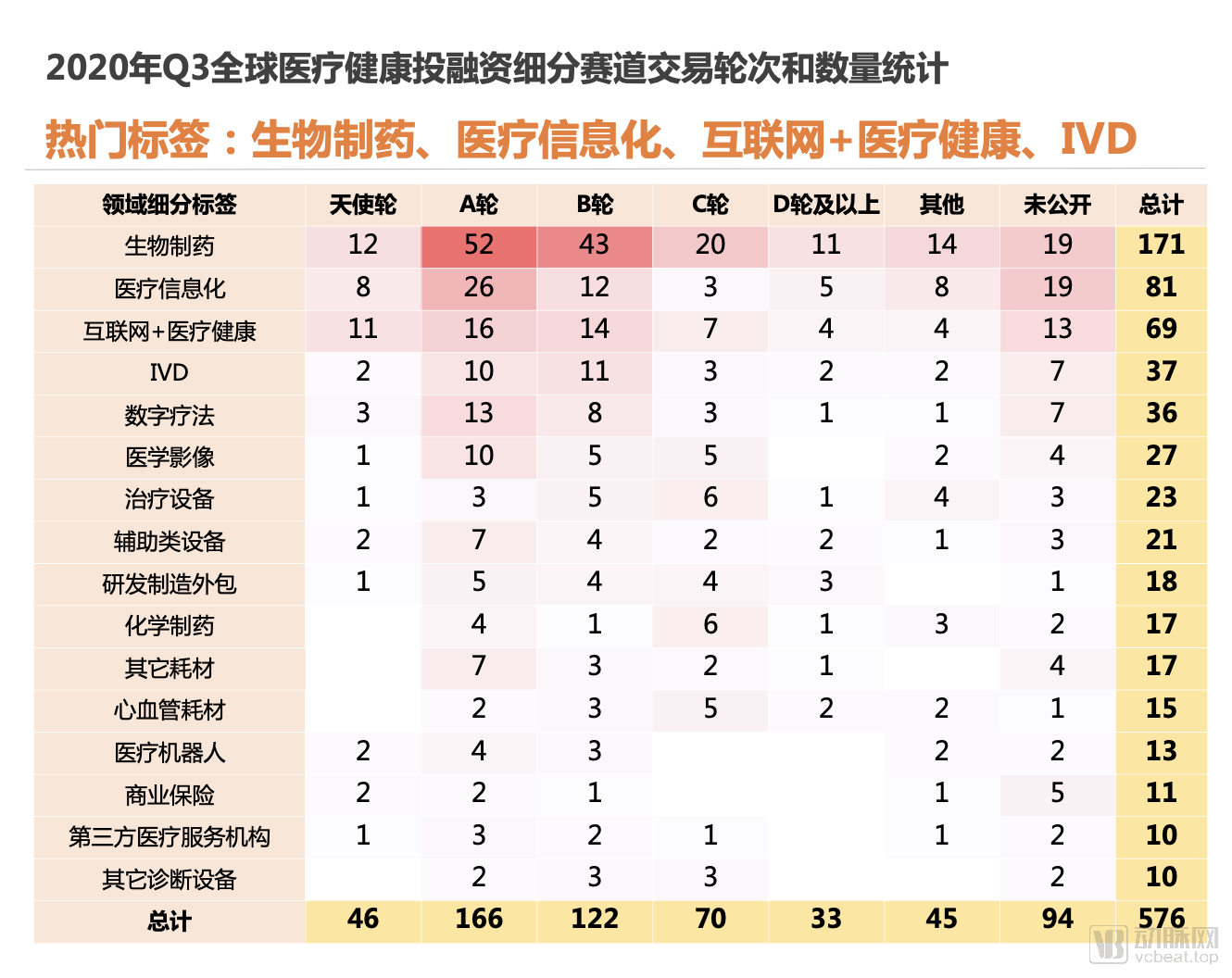

2.3 Global Hot Investment Themes: Biopharmaceuticals, Healthcare Informatics, Internet+Healthcare, IVD

In the third quarter of 2020, tags such as biopharmaceuticals, healthcare informatics, “Internet+” healthcare, and in vitro diagnostics (IVD) garnered significant attention. Beyond the perennially popular biopharmaceutical sector, the digital health field also maintained high activity, particularly among healthcare informatics companies.

In terms of round distribution, among the financing events involving popular tags in Q3 2020, Series A rounds occurred most frequently, totaling 166. Although the number of Series C rounds surpassed that of angel rounds—reflecting growing investor confidence in companies with relatively mature business models—the majority of enterprises remained concentrated at Series B and earlier stages.

2.4 Growth in Overseas Niche Segments: Digital Health Companies Reach Maturity, with 15 Financing Rounds Exceeding $100 Million

The COVID-19 pandemic has undoubtedly spurred another surge in digital health this year. The H1 report previously highlighted the capital gains of telemedicine-related companies, while a new feature this quarter is the frequent occurrence of high-value financing rounds, with funding stages shifting significantly later.

The surge in the digital health sector this year is reminiscent of the boom in 2018, when 12 financing rounds exceeding $100 million throughout the entire year were already considered a frenzy in the digital health capital market. In contrast, there have been as many as 15 such transactions in just the third quarter this year. As the policy environment for digital health improves and user acceptance grows, the business models of more companies are being validated and gaining trust.

From the scope of their business operations, companies in fitness, internet-based insurance, mental health, and digital pharmacies have blossomed across their respective niche segments and are now making a push toward broader markets.

2.5 Growth in China’s Niche Sectors: Chinese Medical Robots Spark a Financing Boom, with Domestic Substitution of Surgical Robots Showing Promise

In the third quarter of 2020, financing activities for Chinese startups in the medical robotics sector were significant. A total of 11 medical robotics companies (two specializing in rehabilitation robots and nine in surgical robots) secured funding during this quarter.

Among them, Tinavi Medical Technologies, the first medical robotics company listed on the STAR Market, and MicroPort MedBot, which secured RMB 3 billion in strategic financing, represent the first tier with more mature commercialization. Close behind are nearly ten startups still at Series B or earlier stages. Most of these companies were founded around 2017 and have gradually completed their financing rounds after three years of development.

Encouragingly, previous financing activities for medical robots in China were predominantly focused on rehabilitation and service robots, while surgical robots—long monopolized by developed countries—require more profound and sustained technological accumulation. The surge in surgical robot financing deals this quarter marks another breakthrough in the intelligence and precision of China’s medical device industry, promising a bright future for domestic substitution.

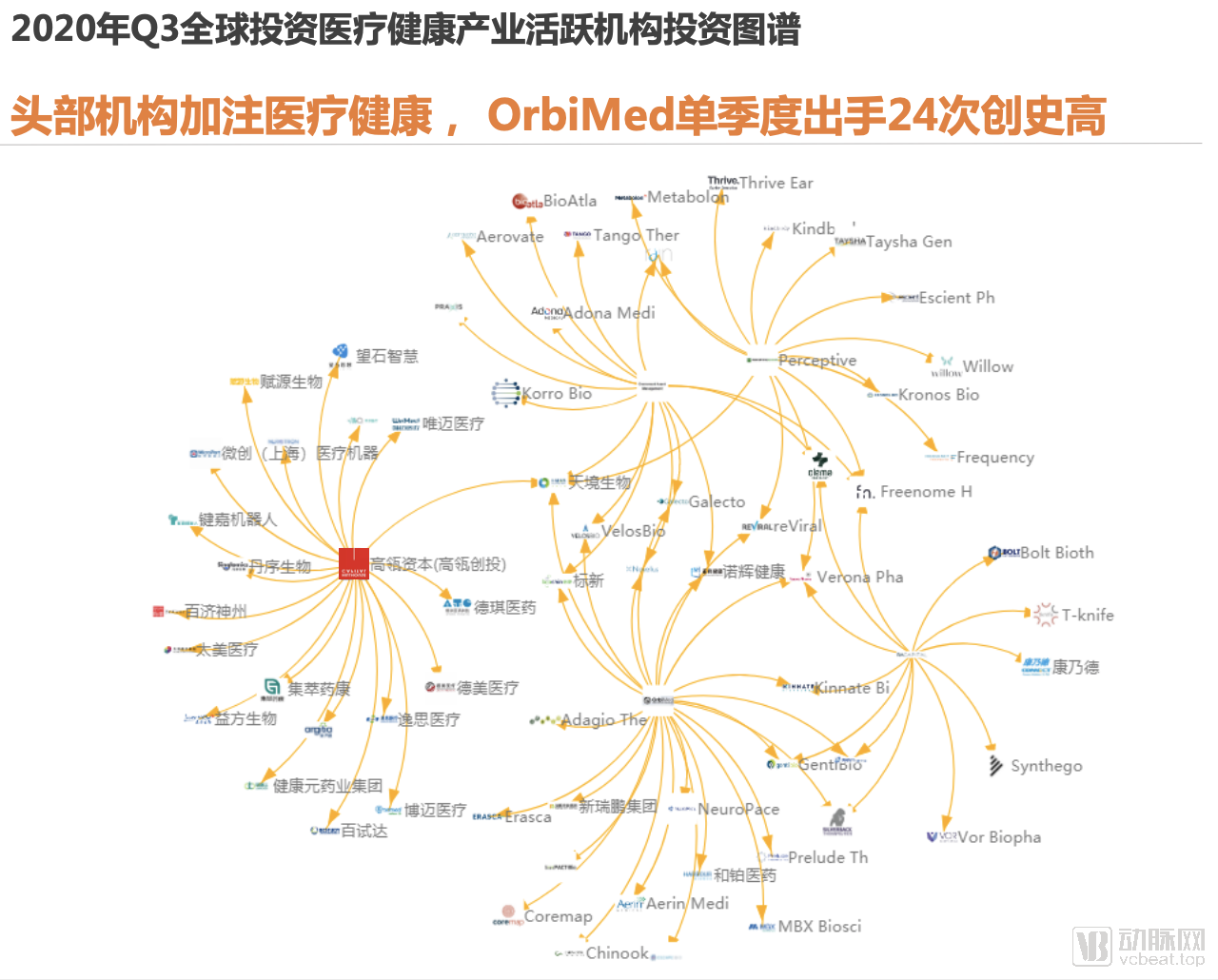

3.1 Top Firms Double Down on Healthcare; OrbiMed Sets Record with 24 Deals in a Single Quarter

In Q3 2020, OrbiMed was the most active global investor in healthcare, with its 24 investments marking the highest number of deals by any single institution in a quarter as recorded by VCBeat Orange. In comparison, GV, which ranked first in investment activity during the first half of 2020 (2020 H1), made only 12 investments.

In addition, Hillhouse Capital and its venture capital arm, GL Ventures, each recorded an astonishing 20 investments in a single quarter, underscoring the pronounced preference shown by top-tier investment firms for healthcare startups since Q3 of this year.

3.2 Eleven Institutions Made Over 10 Investments in a Single Quarter, with Project Resources Increasingly Concentrated Among Active Investors

In Q3 2020, a total of 11 institutions made 10 or more investments. Compared with previous periods, the investment activity level of active institutions reached an unprecedented high in this quarter.

In terms of sectors, active investors favor biopharmaceuticals and medical devices and consumables. Regarding investment stages, a notable characteristic of active investors in Q3 2020 was the increased investment in later-stage rounds, such as Series C and beyond.

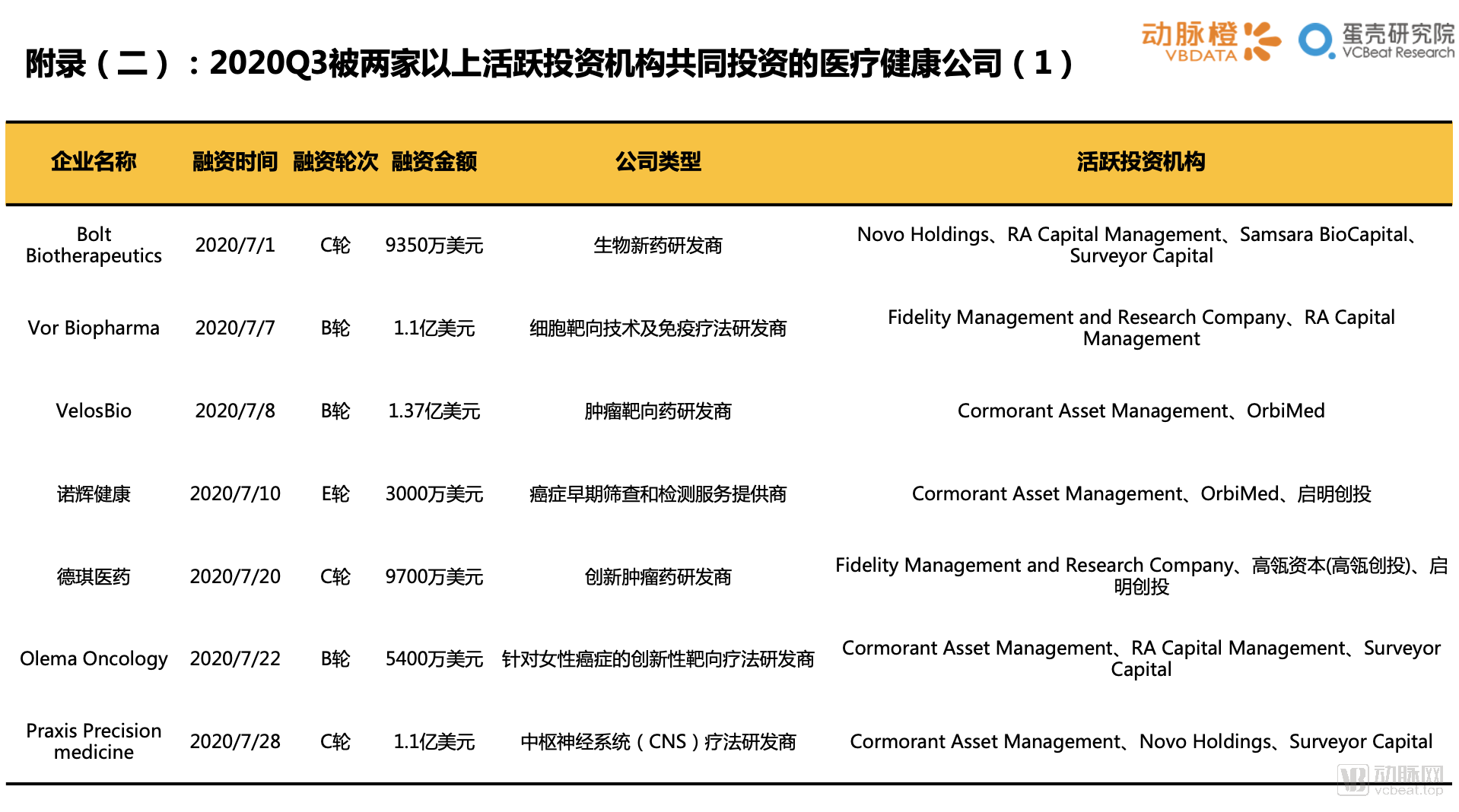

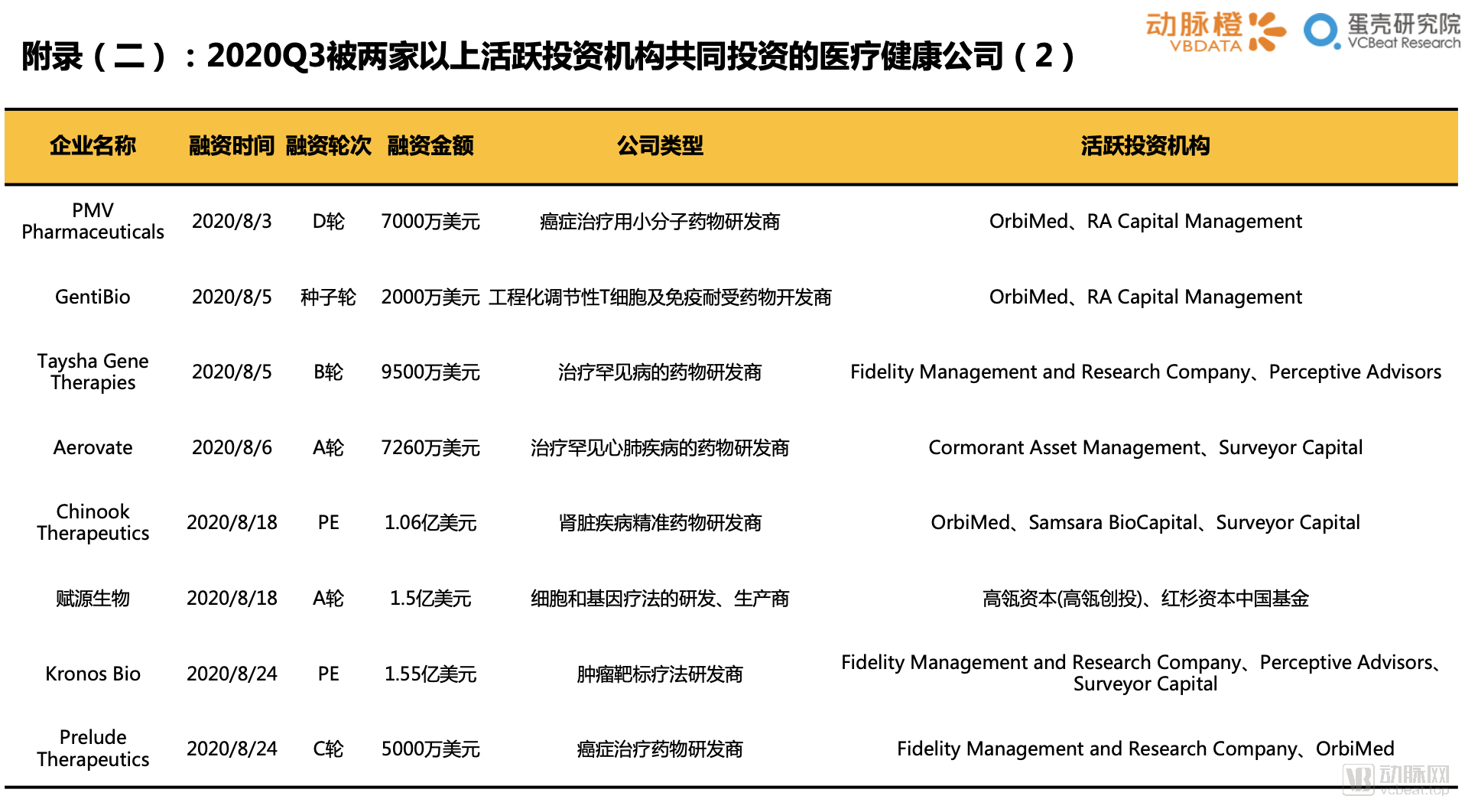

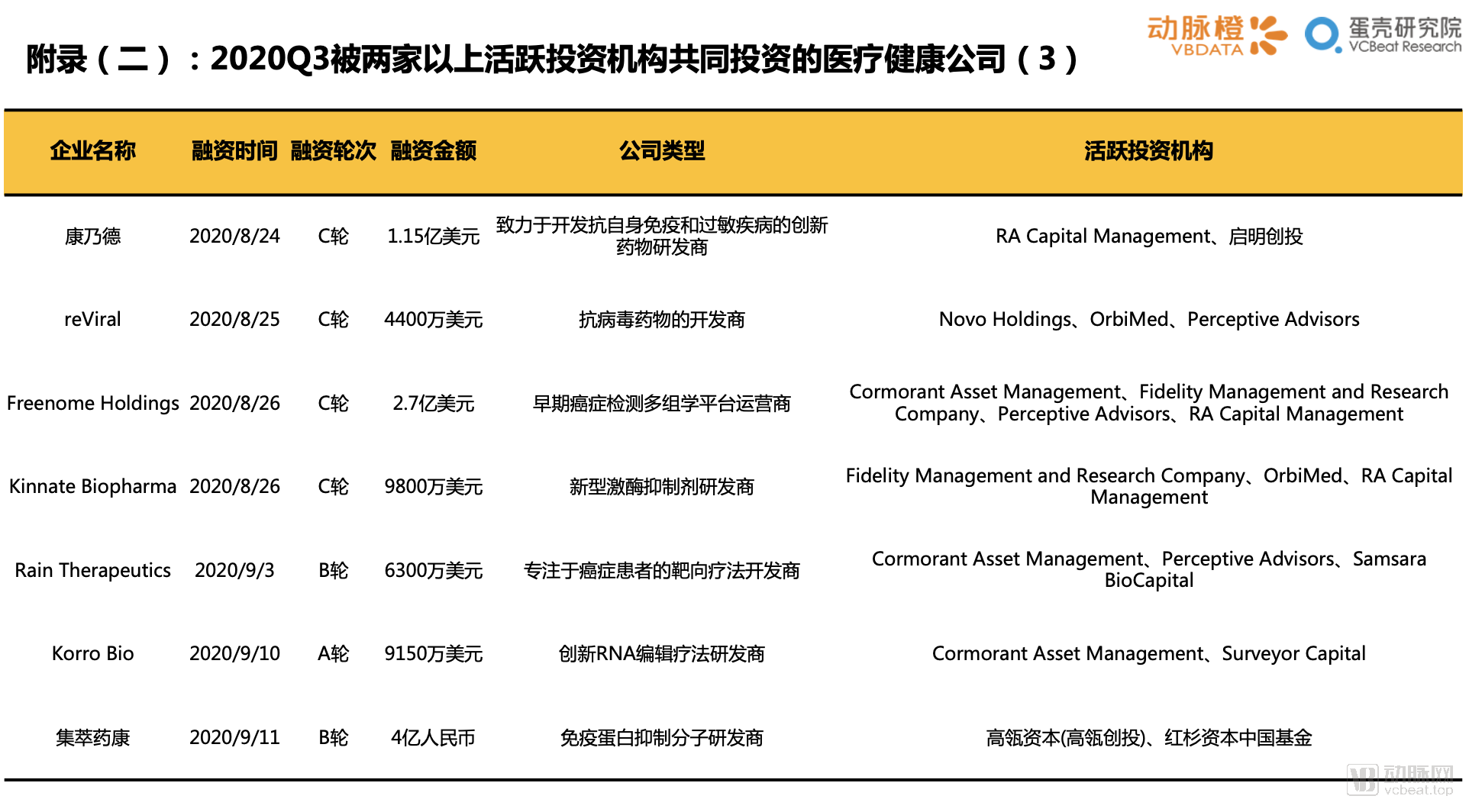

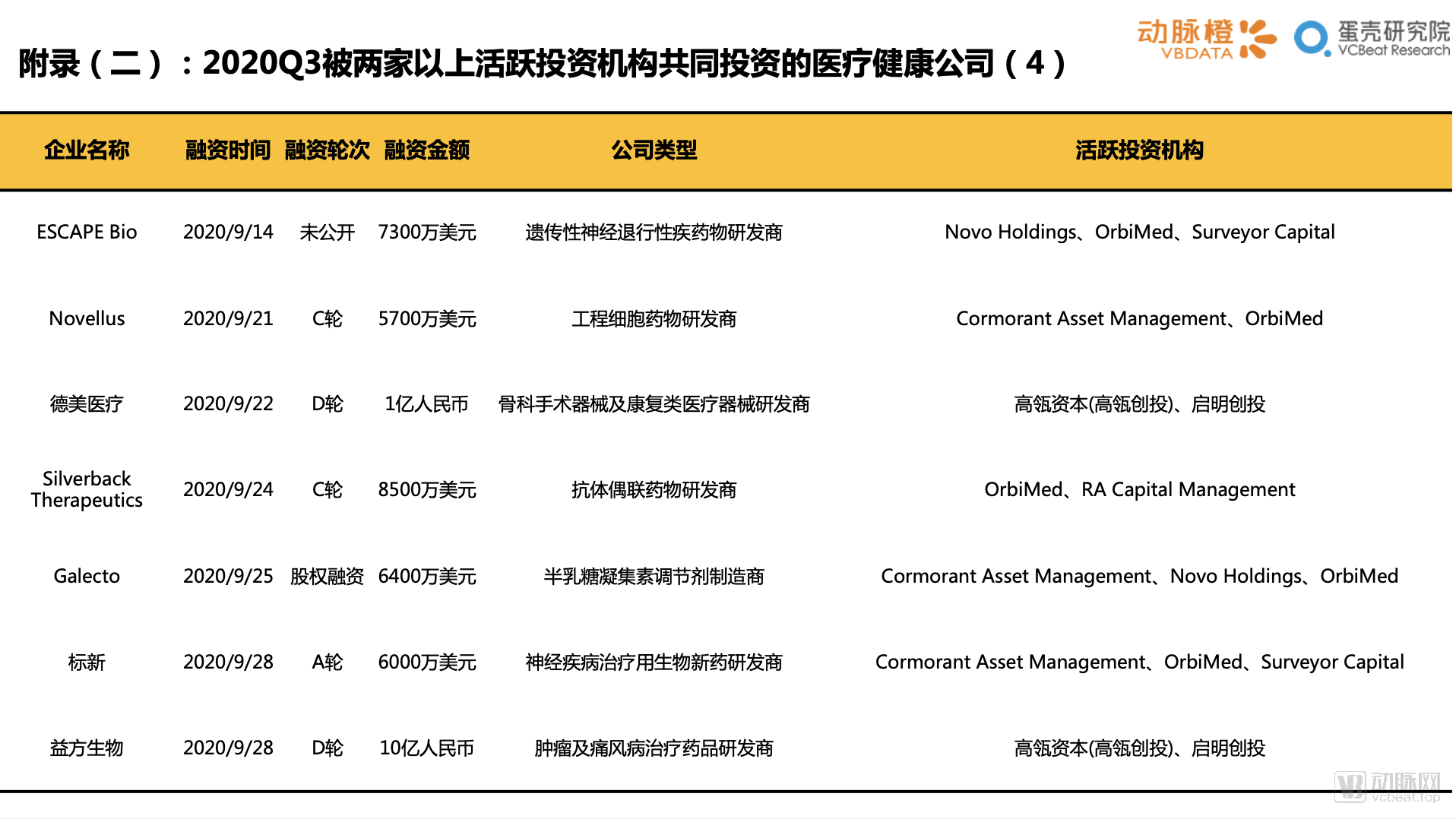

From the perspective of typical portfolio companies, some have secured investments from multiple active firms. For instance, Freenome received backing from four active investors, which to some extent reflects a shared preference among top-tier institutions for certain sectors or high-quality companies, indicating the emergence of the Matthew effect in the capital market.

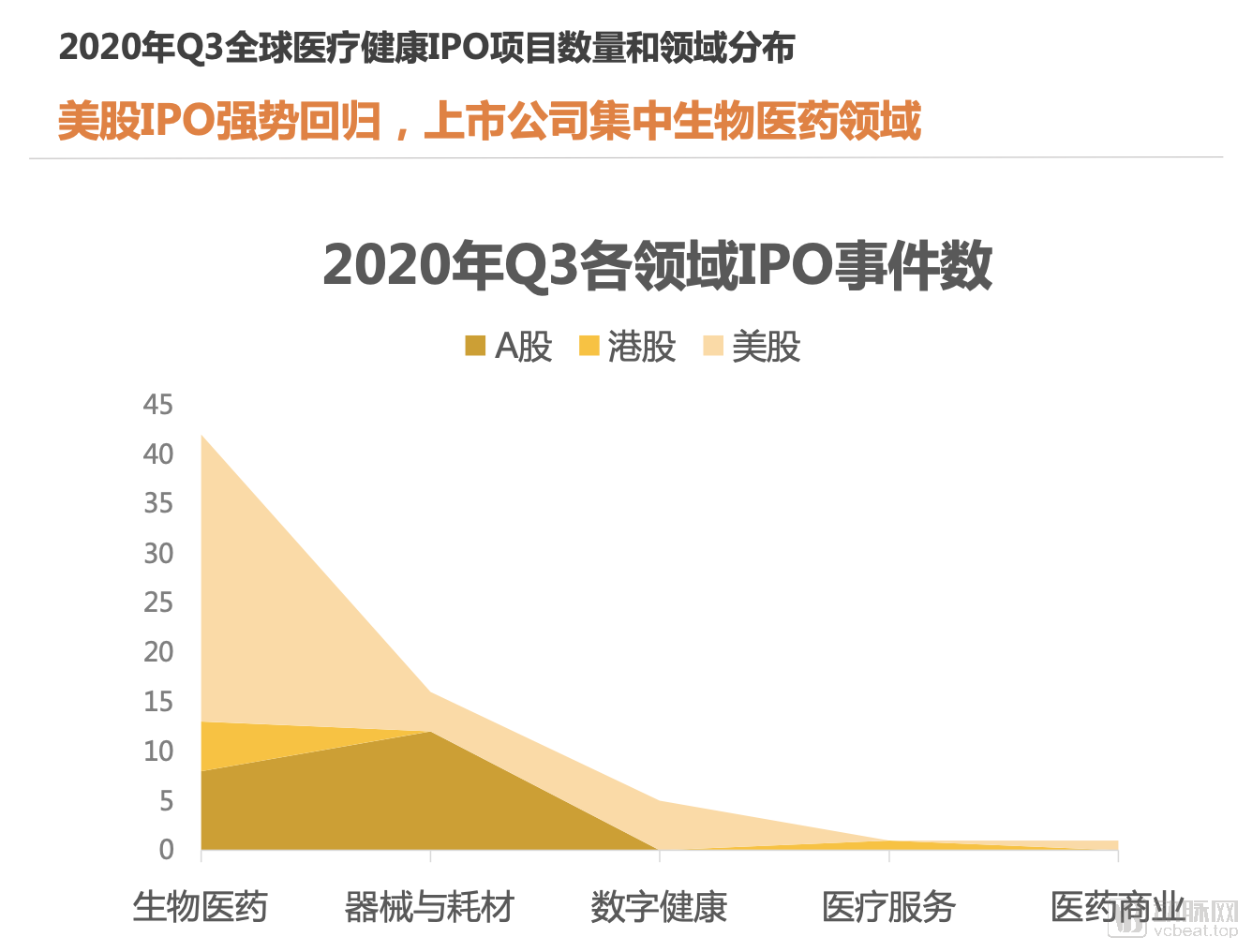

4.1 Strong Return of U.S. IPOs, with Listed Companies Concentrated in the Biopharmaceutical Sector

In Q3 2020, 65 healthcare companies went public across the U.S., A-share, and Hong Kong stock markets. • Among them, 20 companies listed on the A-share market, 6 on the Hong Kong stock market, and 39 on the U.S. stock market. Furthermore, the IPOs in Q3 were primarily concentrated in the biopharmaceutical sector, with 42 related companies going public.

Compared with 20 listings in Q1 and 47 in Q2 of this year, the number of newly listed companies saw a significant increase in Q3. The surge was primarily driven by the pandemic, which indeed slowed down the IPO pace for some companies in the first half of the year. As the secondary market returned to normal operations in the third quarter, companies that had previously planned their IPOs finally made their debuts, albeit later than expected.

4.2 A-Shares/US Stocks/HK Stocks Welcome 65 IPO Projects, Raising Over RMB 100 Billion

Twenty companies were listed on China’s A-share market, including eight biopharmaceutical firms and twelve medical device manufacturers. In contrast, listings on the Hong Kong Stock Exchange and U.S. stock markets were concentrated primarily in the biopharmaceutical sector, with five and twenty-nine companies, respectively. Evidently, in terms of company type, the vast majority are biopharmaceutical companies. The total capital raised by the 26 domestically listed companies amounted to nearly RMB 60 billion. Compared with the total funds raised from 39 IPOs abroad, Chinese enterprises generally secured higher financing amounts than their overseas counterparts.

4.3 26 Chinese Companies Went Public, with 14 Listing on the STAR Market of the A-Shares

In Q3 2020, among the companies listed domestically in China, 14 were listed on the STAR Market, while 4 and 2 were listed on the ChiNext Board and the Main Board, respectively; additionally, 6 companies were listed in Hong Kong. The total capital raised by these 26 domestically listed companies in Q3 reached RMB 60 billion.

It is worth noting that Tigermed, a clinical CRO company, listed on the Hong Kong Stock Exchange in August this year, becoming another CRO enterprise to be dual-listed on both mainland Chinese stock exchanges and the Hong Kong Stock Exchange, following WuXi AppTec and Pharmaron.

5.1 Global: The United States Leads the World, with Over 200 Financing Events in a Single Quarter in Both China and the US

In Q3 2020, the five countries with the highest number of global healthcare financing deals were the United States, China, Israel, Canada, and the Netherlands. In Q3 2020, the United States led the world with 257 financing deals totaling $11.25 billion (RMB 78.63 billion), followed closely by China. Together, the U.S. and China accounted for 85% of the total financing amount and 77% of the total number of financing deals globally.

5.2 United States: California Dominates, with Massachusetts and New York Emerging as Secondary Hubs

In Q3 2020, California recorded a cumulative total of 92 healthcare financing and investment deals, raising $5.63 billion (approximately RMB 38.78 billion), making it the region with the highest frequency of global healthcare venture capital activities. The three major U.S. hubs for healthcare investment and financing exhibit distinct corporate cluster characteristics. California has attracted a large number of healthcare enterprises by leveraging its advantages in capital, technology, and talent. Massachusetts is renowned for its prominent biotechnology industry cluster and abundant medical resources, while New York continues to demonstrate a vibrant atmosphere for digital health innovation.

5.3 China: Shanghai’s Total Financing Amount Sees Explosive Growth, Leading Beijing by an Absolute Margin

In the first half of 2020, the five regions in China with the highest concentration of healthcare investment and financing activities were, in order, Shanghai, Beijing, Guangdong, Jiangsu, and Zhejiang.

Shanghai recorded 57 financing deals this quarter, raising a total of RMB 18.69 billion. This figure not only surpasses Beijing, the second-ranked city, by nearly RMB 10 billion, but also exceeds the RMB 11.4 billion raised in Shanghai during the first half of 2020. Prior to 2020, Beijing had been the leading region for healthcare and medical financing in China for ten consecutive years. However, it has been overtaken by Shanghai for three consecutive quarters this year. The widening gap between the two cities indicates that the shift in the geographic distribution of healthcare and medical investment and financing in China has been initially completed.

6.1 Global Top 10: Bright Health Secures $500 Million in Funding, Ranking First; Three Chinese Companies Make the List

Among the top 10 companies by financing amount in Q3 2020, seven were U.S.-based and three were Chinese, with each securing over RMB 1 billion. The list was dominated by medical device and biopharmaceutical companies; however, Bright Health, a digital health insurance service provider, and Zwift, an interactive fitness and entertainment platform, both ranked highly. As digital health companies, their strong performance indicates that digital health firms broke through the competition this quarter, demonstrating enhanced capital-raising capabilities.

Three Chinese companies—MicroPort (Shanghai) Medical Robot, XtalPi, and Shuidi Inc.—made the list. As a holding subsidiary of MicroPort, MicroPort (Shanghai) Medical Robot was valued at RMB 22.5 billion following its September financing round. The company focuses on the research, development, and industrialization breakthroughs of surgical robots, with its business spanning five “golden tracks”: laparoscopy, orthopedics, vascular intervention, natural orifice surgery, and percutaneous puncture.

6.2 China’s Top 10: MicroPort MedBot Takes the Lead, Biopharmaceutical Companies Claim Seven Spots

In Q3 2020, biopharmaceutical companies continued to dominate among the top 10 Chinese firms by financing amount.

MicroPort MedBot, a subsidiary of MicroPort Scientific Corporation, secured RMB 3 billion in financing in September, marking the second-largest funding deal in China in 2020 after MGI Tech’s $1 billion raise.

Furthermore, with each changing quarter, digital health companies appear to consistently secure a spot on the top funding rankings, which are typically dominated by biopharmaceutical firms. In this period, Shuidi Inc. and Taimei Medical Technology both entered the Top 10.