Seizing Breakthrough Opportunities in Pharmaceutical Distribution Amid the New Retail Era

Introduction: In recent years, with the introduction of new policies such as the “Two-Invoice System” and the “4+7” centralized procurement program, the pharmaceutical distribution industry has been not only implementing healthcare reform requirements but also promoting the flattening of pharmaceutical distribution channels. Particularly in 2020, driven by circumstantial pressures, pharmaceutical distribution companies have been compelled to explore new channels and accelerate the transformation and upgrading of their supply chain services. Taking Dingdang Kuaiyao, which announced the completion of a new round of financing yesterday, as an example, its pioneering online-offline integrated pharmaceutical new retail model—“online ordering with store delivery” and “online ordering with store pickup”—has become one of the industry benchmarks.

However, across the entire pharmaceutical distribution industry, pain points persist alongside opportunities. How can companies leverage new retail to break through bottlenecks and seize new opportunities for industry takeoff? As a long-term capital market partner and companion to China’s new economy enterprises, the Industrial Internet team at China Renaissance has provided its own answers by deconstructing the following sections, based on its in-depth industry research and precise forecasts, hoping to inspire you:

1. Current Status and Pain Points of the Traditional Pharmaceutical Distribution Industry?

2. How Are New Policies in the Current Landscape Accelerating the Separation of Prescribing and Dispensing, and What New Opportunities Do They Bring to the Industry?

3. What are the future trends for each channel in the pharmaceutical distribution industry chain?

4. Where Lies the Breakthrough Point for the Future Blue Ocean of Pharmaceutical E-commerce?

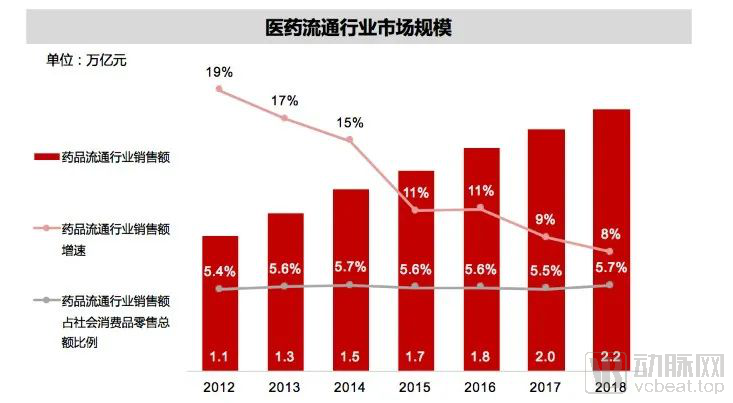

In recent years, population aging in China has intensified. The proportion of the population aged 65 and above increased from 9.1% in 2011 to 11.9% in 2018, accompanied by a rapid rise in healthcare demand. Coupled with the steady growth in residents’ disposable income and consumer spending, the pharmaceutical distribution industry is continuously expanding on a market scale worth hundreds of billions of yuan. In 2018, the market size of the pharmaceutical distribution industry exceeded RMB 2.2 trillion, doubling compared with 2012.

Data Sources: Ministry of Commerce, National Bureau of Statistics, Wind, Huaxing Analysis

As of 2018, there were 20,000 manufacturers in the traditional pharmaceutical distribution channel; the number of wholesalers reached 14,000, including four companies with sales exceeding RMB 100 billion—Sinopharm, Shanghai Pharmaceuticals, China Resources Pharmaceutical, and Jointown Pharmaceutical—as well as more than 20 companies with sales exceeding RMB 10 billion. In terms of retail endpoints, there were 31,000 hospitals at or above graded levels, 489,000 retail pharmacies, and 950,000 primary healthcare institutions.

Although the overall outlook is optimistic, critical pain points remain to be addressed in key segments of traditional pharmaceutical distribution channels:

Pharmaceutical Manufacturing:

1. Weak R&D capabilities—generic drugs account for over 95% of the product portfolio, resulting in severe product homogenization;

2. Extremely low industry concentration—among generic drug manufacturers, the CR8 accounts for only 18.8%;

3. Fragmented market—reliance on pharmaceutical sales representatives for hospital promotion;

4. Greater reliance on sales channels than on product capabilities.

Pharmaceutical Wholesale: Industry Concentration Continues to Rise, While Small and Medium-Sized Enterprises Face Development Constraints

In recent years, the growth rate of the pharmaceutical wholesale market has gradually slowed. In 2017, the sales revenue of pharmaceutical wholesale enterprises across China reached RMB 722.7 billion, a year-on-year decrease of 4%. The number of pharmaceutical wholesale enterprises also declined. During the peak in 2012, there were 16,300 drug distribution companies. Following industry consolidation in 2015, the number dropped to 13,000, before experiencing a slight rebound thereafter. As of 2018, there were a total of 13,598 pharmaceutical wholesale enterprises nationwide.

In this context, large pharmaceutical distribution enterprises have gained a distinct advantage. First, the implementation of the "Two-Invoice System" in recent years has shortened the industry supply chain, giving large distributors with upstream and downstream resource advantages a higher probability of securing business, while encroaching on the development space of small and medium-sized distributors. Second, the rollout of policies such as volume-based procurement has led to continuous declines in drug prices and distribution fees; leveraging their economies of scale, large distributors enjoy relatively lower distribution costs. Furthermore, a significant number of newly launched innovative drugs are biologics with stringent transportation and storage requirements. Large enterprises, equipped with more comprehensive hardware and software infrastructure, are therefore better positioned to secure these contracts. Consequently, between 2011 and 2018, the CR10 (concentration ratio of the top ten companies) in the pharmaceutical distribution industry rose from 34% to 43%, indicating a sustained increase in industry concentration.

Furthermore, to achieve faster coverage of end consumers and enable timely strategic adjustments, the comprehensive implementation of the “Two-Invoice System” has driven major pharmaceutical wholesalers to shift from the traditional allocation model to a pure sales model (direct sales model), with its proportion increasing from 56.9% in 2013 to 65.2% in 2018. Meanwhile, accompanied by the trend of prescription outflow, the four major pharmaceutical wholesalers have strengthened their presence in primary healthcare institutions and retail chain pharmacies, resulting in significant growth in non-hospital sales revenue.

Retail: Chain Pharmacies Highlight Value, Cross-Regional Expansion Becomes a Challenge

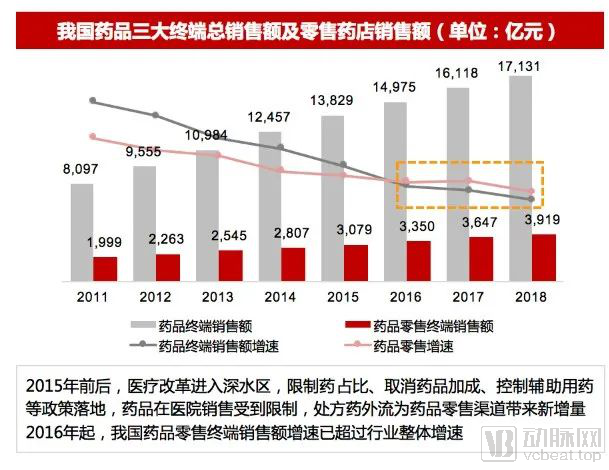

Around 2015, influenced by healthcare reforms, restrictions were imposed on drug sales in hospitals, leading to an outflow of prescription drugs that drove new growth in the pharmaceutical retail channel. Since 2016, the growth rate of sales at China’s pharmaceutical retail terminals has exceeded the overall industry growth rate. In 2018, the pharmaceutical retail channel achieved sales of RMB 391.9 billion, accounting for 22.9% of the total. Of this, brick-and-mortar pharmacies generated RMB 382.0 billion in sales (22%), while online pharmacies recorded RMB 9.9 billion in sales (1%).

Data sources: SFDA’s 2017 Annual Statistical Report on Food and Drug Supervision, Ministry of Commerce, National Bureau of Statistics, Wind, Huaxing Analysis

From the perspective of the terminal retail landscape, public hospitals still dominate. However, over the past three years, the compound annual growth rate (CAGR) of retail pharmacies has reached 9.6%, surpassing the 7% recorded by public hospitals. In this process, the terminal value of chain pharmacies is gradually becoming more prominent. Leveraging four key advantages—cost advantage, brand effect, high operational and management efficiency, and strong professional service capabilities—the chain affiliation rate of pharmacies increased from 38% in 2012 to 52% in 2018. The driving forces behind this trend are mainly two:

First, the competitive landscape has improved, with survival space for players continuously expanding. Following the implementation of the new Good Supply Practice (GSP) in 2013, the number of independent pharmacies declined rapidly. Furthermore, policies introduced in 2018 regarding compliant operations and tiered classification further purified the industry’s competitive environment. Large pharmacy chains have leveraged economies of scale to reduce procurement costs, thereby steadily squeezing the survival space of independent pharmacies.

Secondly, amid the transformation of the pharmaceutical industry, chain pharmacies are increasingly favored. Under policies such as volume-based procurement and medical insurance cost containment, the profits that pharmaceutical manufacturers can secure from the hospital sector are being gradually squeezed. As the secondary terminal directly serving patients, chain pharmacies operate with more market-oriented mechanisms and will become an increasingly important sales channel for pharmaceutical manufacturers in the future.

However, further cross-regional expansion has become a significant challenge for chain pharmacies. Customer acquisition for offline pharmacies relies on dense store networks, but due to varying Good Supply Practice (GSP) compliance policies across regions, it is difficult for cross-regional self-operated stores to establish effective communication with local authorities in the short term. Constrained by these factors, leading chain pharmacy companies exhibit pronounced regionalization in their nationwide layout, making it difficult to form a truly national network.

Faced with expansion challenges, some pharmacy chains have adopted mergers and acquisitions (M&A) to accelerate growth and increase their chain affiliation rate. In 2017, the four major listed pharmacy chains initiated 23 M&A transactions involving 724 pharmacies. However, pharmacy acquisitions require substantial asset investment, and the significant capital needed for frequent M&A activities can severely dilute equity.

Therefore, expanding e-commerce operations has become a channel for some pharmacy brands to explore new growth opportunities and accelerate their strategic deployment. Represented by Dingdang Kuaiyao, pharmaceutical new retail enterprises have successfully established a nationwide pharmaceutical new retail network through the following practices:

1. Achieved coverage of more than 10 first-tier cities across China through just 213 pharmacies;

2. Most stores are forward warehouse stores, with rents significantly lower than those of traditional pharmacies; 90% of revenue comes from online channels;

3. The pharmacy covers a radius of 3-5 kilometers, with sales per square meter and labor productivity 10 to 15 times higher than those of traditional pharmacies, significantly improving efficiency.

Data source: Dingdang Kuaiyao

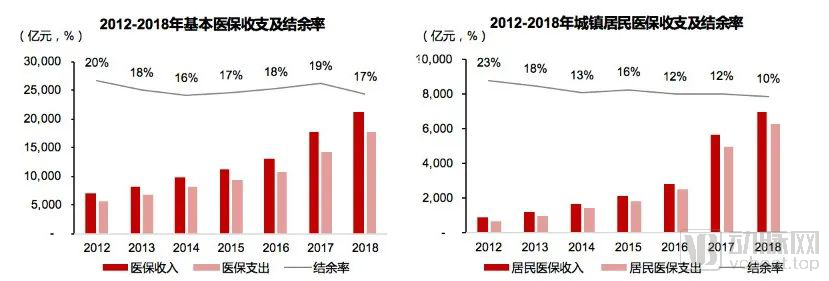

Pressing Times: Narrowing Gap in Medical Insurance Revenue and Expenditure Calls for Urgent Reform, While Multiple Factors Drive the Growth of the Online Pharmaceutical Market

In 2018, the surplus rate of China’s basic medical insurance decreased from 20% in 2012 to 17%, while the surplus rate for urban resident basic medical insurance saw a more significant decline, dropping from 23% to 10%. Furthermore, data from the National Healthcare Security Administration and other sources indicate that in 2018, social medical insurance accounted for 56% of total healthcare expenditures in China. Although the population is basically covered, premium revenues are insufficient to cover expenditures, highlighting an urgent need for further cost-containment reforms.

Meanwhile, with the widespread adoption of mobile internet, pharmaceutical supply chain services have been continuously improved. Due to the impact of the pandemic, the advantages of online medication purchases have become increasingly prominent. Coupled with the economic and social factors mentioned above, the development of pharmaceutical e-commerce has gradually become an industry trend.

Frequent New Policies: Accelerating the Separation of Prescribing and Dispensing

Relevant Policies:

1. National Healthcare Security Administration — DRG (Diagnosis-Related Groups) Payment Reform: Bundled payment by disease group to achieve refined cost control in healthcare insurance;

2. Ministry of Human Resources and Social Security—Unified Online and Offline Medical Insurance: A unified online medical insurance settlement interface to support applications such as online medication purchases.

Impact:

1. Guide the reform of the hospital's revenue system;

2. Promote the integrated development of online and offline channels in the out-of-hospital pharmaceutical market to facilitate channel consolidation.

Relevant Policies:

1. National Healthcare Security Administration — “4+7” Volume-Based Procurement: Lowering drug procurement prices and including select retail pharmacies;

2. National Healthcare Security Administration—Second Batch of Volume-Based Procurement: Expansion in the Number of Drug Categories and Pilot Cities;

3. NDRC — Zero Mark-up on Drugs: Abolishing the practice of "subsidizing healthcare with drug profits."

Impact:

1. Reshaping the drug pricing system to promote the separation of prescribing and dispensing;

2. Enhance the capacity of retail pharmacies to handle prescriptions diverted from hospitals;

3. Manufacturers that lost the bid partner with large retail chains.

Relevant Policies:

State Council – Electronic Prescriptions: Allowing Internet Healthcare Platforms to Issue Electronic Prescriptions

Pilot Programs in Multiple Regions: 17 provinces and municipalities, including Sichuan, Guangdong, and Guangxi, have launched or announced plans to launch pilot programs for electronic prescriptions

Impact:

1. Accelerate the pace of electronic prescription pilot programs;

2. Multiple regions are promoting the outflow of prescriptions.

Relevant Policies:

1. The State Council and the China Food and Drug Administration (CFDA) changed the approval system to a filing system: the approval of internet drug transaction service enterprises by provincial food and drug regulatory authorities was abolished (License B: B2B, License C: B2C); obtaining drug operation qualifications is sufficient;

2. State Council – Promoting Online Drug Distribution: Encouraging Models Such as “Online Ordering and In-Store Delivery.”

Impact:

1. Streamline the approval process for online drug sales;

2. Promote the digitalization of the out-of-hospital market.

In recent years, thanks to the implementation of policies across medical insurance, distribution, prescription, and sales sectors, the process of separating drug prescribing from dispensing has accelerated, with public hospitals’ drug revenue share dropping significantly from 38% in 2014 to 28.7% in 2020.

Prediction: The market size for out-of-hospital pharmaceuticals, where internet-based business models are expected to penetrate, is estimated to exceed RMB 500 billion.

Based on calculations from the hospital and channel sides, the total size of China's prescription outflow market is nearly RMB 300 billion, with an annual outflow of RMB 40–70 billion. The outflow primarily shifts from in-hospital settings to out-of-hospital terminals, either online or offline.

Based on the market share of prescription drug segments, chemical drugs and proprietary Chinese medicines suitable for out-of-hospital prescription treatment account for a combined total of approximately 56%, corresponding to a total prescription drug market size of around RMB 630 billion in 2018. Excluding prescription drugs requiring interventional therapy and cold-chain transportation, which account for approximately 50%, the market size of prescription drug segments suitable for the internet hospital model is about RMB 315 billion. When combined with the over-the-counter (OTC) drug market that allows for concurrent medication, the total out-of-hospital medication market potentially penetrable by the internet hospital model is estimated at approximately RMB 500 billion.

Based on the above observations and analysis, we believe that the pharmaceutical distribution industry exhibits the following development trends across its various channels:

Pharmaceutical R&D and Manufacturing Enterprises: Gradually Moving Toward Polarization

On the one hand, innovative pharmaceutical companies are continually emerging.From 2016 to 2019, the National Reimbursement Drug List (NRDL) in China underwent multiple adjustments, incorporating dozens of oncology drugs. Following these adjustments, it has become an industry consensus that innovative drugs gain access through centralized negotiations. In the future, a dynamic negotiation-based access mechanism for innovative drugs under the national medical insurance scheme is highly likely to be implemented, which is expected to further accelerate the approval process for innovative drugs. As the structure of medical insurance payments evolves, societal support for covering innovative drugs has strengthened, enhancing patients’ affordability. Consequently, large pharmaceutical companies that separately disclose their sales figures in China have reported revenue growth rates significantly higher than their global sales growth rates.

On the other hand, intensified competition in the generic drug market has further consolidated the dominance of large-scale pharmaceutical companies.Under the policies of consistency evaluation and volume-based procurement, capacity contraction and declining drug prices will lead to a Matthew effect in the industry, accelerating the development of leading generic pharmaceutical companies with strong R&D capabilities, manufacturing prowess, and robust product portfolios.

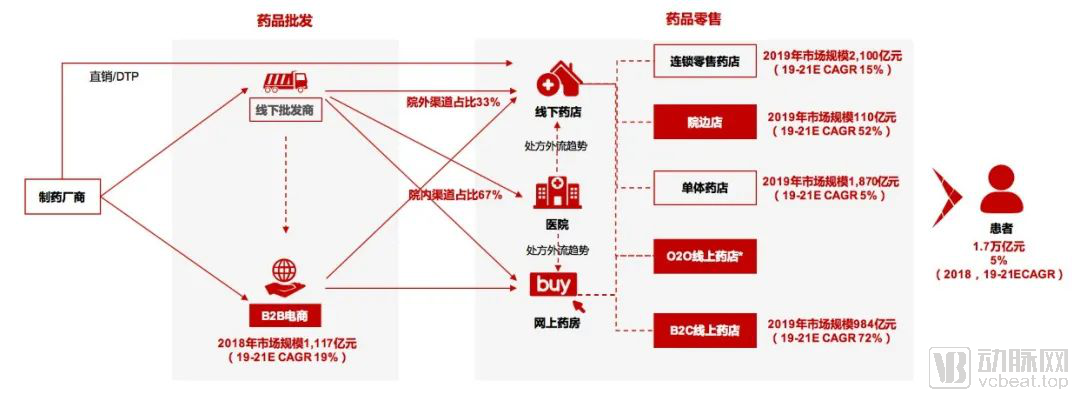

Pharmaceutical Distribution Industry Chain: Focusing on Future Industrial Drivers

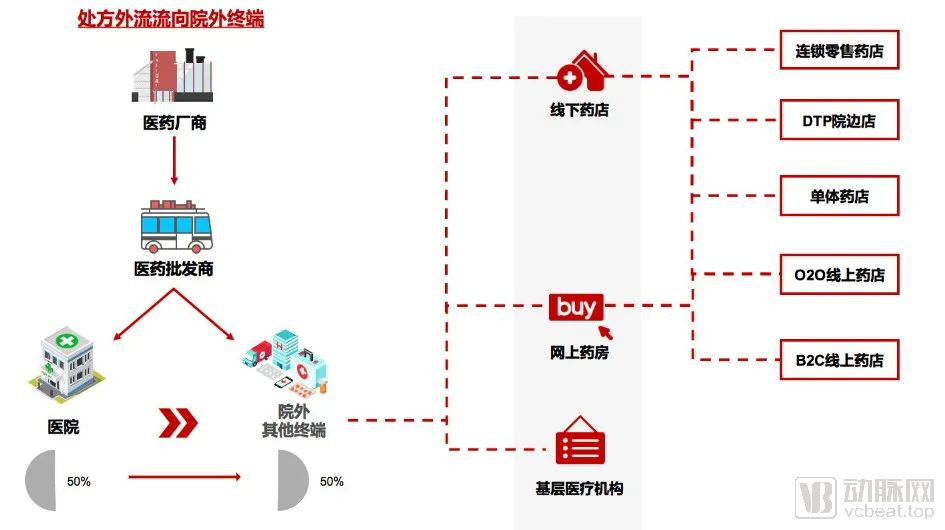

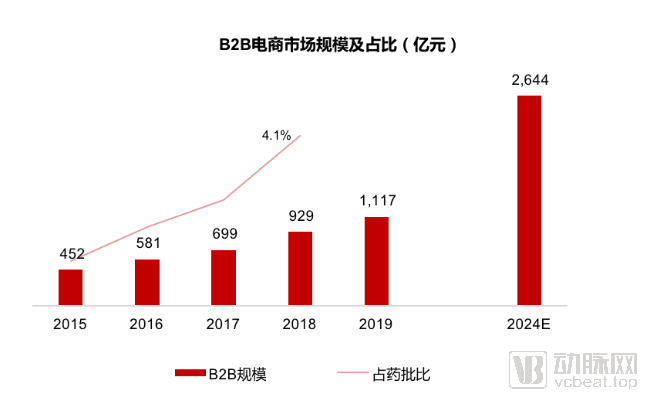

To address the cumbersome nature of the pharmaceutical distribution supply chain, which traditionally involves multiple tiers from wholesalers to retailers and finally to patients, the Two-Invoice System streamlines distribution channels by reducing the number of intermediaries between manufacturers and end-users to just two or even one tier.In the distribution segment, hospital-adjacent pharmacies, B2B e-commerce, O2O, and B2C e-commerce are experiencing rapid growth, indicating that these business models will become key drivers in the future of pharmaceutical distribution.

Source: Statistical Analysis Report on Pharmaceutical Circulation Operations, iiMedia Research, Menet, Huaxing Research; Note: Sales from O2O online pharmacies are included in offline or B2C e-commerce sales figures.

Pharmaceutical Wholesale Industry: Rising Concentration, Technology Enablement, and Integration of Wholesale and Retail

First, the concentration of the pharmaceutical wholesale industry will further increase. Under the Two-Invoice System and Good Supply Practice (GSP) regulations, profit margins in the pharmaceutical distribution chain will narrow, leading to the exit of small-scale distributors.Leading pharmaceutical wholesalers will expand their distribution networks, driving horizontal consolidation within the industry. Compared with the U.S. market, the concentration of China’s pharmaceutical wholesale sector is expected to rise, with the CR10 reaching 90%.

Secondly, traditional wholesalers and B2B e-commerce platforms will actively expand into out-of-hospital channels.As offline wholesalers enhance their supply chain capabilities, volume-based procurement has reduced distribution costs, making the cost advantages of large enterprises through intensive operations increasingly prominent. Meanwhile, these companies are expanding into out-of-hospital channels by establishing store business units and setting up DTP (Direct-to-Patient) stores near hospitals downstream. Furthermore, offline wholesalers have improved their informatization capabilities by building drug traceability systems that enable information collection across the entire process of production, circulation, and consumption.

B2B e-commerce platforms empower the distribution process through technology, establish a pharmacy supply chain stewardship system, and achieve cost reduction and efficiency improvement across the industry chain. Leveraging the advantages of centralized procurement and transparency in B2B models, economies of scale can be realized.

Source: Public information, Statistical Analysis Report on Pharmaceutical Distribution Operations

In the "Outline of the Development Plan for China's Pharmaceutical Distribution Industry" issued by the Ministry of Commerce in 2011, explicit encouragement was given to major traditional wholesalers such as Sinopharm Group and China Resources Pharmaceutical, as well as leading B2B pharmaceutical e-commerce platforms like Yaoshibang, to establish integrated wholesale and retail operations through proprietary or collaborative models. Benchmarking against leading enterprises in the U.S. hospital wholesale sector, China’s pharmaceutical wholesale industry is expected to achieve downstream integration of wholesale and retail operations in the future, thereby enhancing brand equity, service quality, and profitability.

Pharmacies: Strengthened Chain-Based Services

From a long-term perspective, the development direction of pharmacies is to meet customers' comprehensive health needs through enhanced product categories and services. The future trend is the formation of integrated online-offline comprehensive health management groups. Benchmarking against CVS Health in the United States, pharmacies will establish a nationwide pharmaceutical retail network integrating online and offline channels, providing one-stop health management services that include primary care consultations, health counseling, Pharmacy Benefit Management (PBM), Direct-to-Patient (DTP) pharmacies, and multi-tiered pharmacy outlets.

This process is further divided into two developmental stages:

The first stage is the chain development phase, primarily involving cross-regional and cross-category integration.During this period, the industry will actively pursue cross-regional M&A and regional consolidation to secure substantial customer traffic. Driven by capital investment, the chain affiliation rate of pharmacies will continue to rise. Meanwhile, pharmacy product portfolios will expand to cover a full range of categories, leveraging high-frequency daily necessities to drive sales of low-frequency pharmaceuticals, thereby enhancing overall sales per square meter and profitability.

The second phase is the service expansion stage, which will primarily focus on developing health management services.Pharmacies will integrate with the internet by adopting an O2O (Online-to-Offline) model featuring “online consultation and ordering, plus prompt offline medication delivery.” They will also provide pharmacist services to offer medication information and personalized guidance on drug use. Furthermore, comprehensive health management services, including online consultations, disease monitoring, and rehabilitation care, will be incorporated into their business scope.

E-Commerce in Pharmaceuticals: The Strong Get Stronger; Focus on Blue Ocean Markets

In summary, and by comparing with the development trajectory of the U.S. pharmaceutical distribution industry, we believe that China’s pharmaceutical distribution industry will gradually increase its concentration, retail share, and degree of marketization. These trends will empower new-retail pharmaceutical enterprises and pave the way for the development of pharmaceutical e-commerce.

Overall, the pharmaceutical distribution industry, empowered by the internet, will see increasing integration of its online and offline channels. This will not only consolidate pharmaceutical resources but also foster the formation of a nationwide, integrated online-to-offline (O2O) new retail network for pharmaceuticals. Furthermore, it will enable regional coverage and cross-regional expansion with fewer physical stores through models such as virtual franchising. As previously mentioned with Dingdang Kuaiyao, the company has become an industry leader by building an integrated O2O pharmaceutical retail system through its “Dingdang Kuaiyao App + offline self-operated smart pharmacies” development model.

Furthermore, to accelerate coverage of end consumers and facilitate timely strategic adjustments, major pharmaceutical wholesalers have shifted from the traditional allocation model to a pure sales model (direct sales model), with its proportion rising from 56.9% in 2013 to 65.2% in 2018. Meanwhile, driven by the trend of prescription outflow, the four leading pharmaceutical wholesalers have strengthened their presence in primary healthcare institutions and retail chain pharmacies, resulting in significant growth in non-hospital sales revenue.

We believe that the pharmaceutical e-commerce sector will see the strong grow stronger, yet blue-ocean opportunities remain. First, leading players will continue to expand, driving ongoing industry consolidation. Second, there is room for growth in vertical disease-specific segments, giving rise to e-commerce platforms dedicated to medications for specific conditions, such as chronic disease management platforms for diabetes and liver diseases. Third, given the low penetration of pharmaceutical e-commerce in rural markets, companies will focus on these areas to address the shortage of medical resources and medications in rural regions, while capturing the dividends of untapped markets.

From an industry perspective, pharmaceutical e-commerce has become the prevailing trend as a new channel for pharmaceutical distribution. In the future, it will lead new retail in continuously seeking growth points and empower China’s pharmaceutical retail terminals.