Major Investors Enter Pet Healthcare: Hillhouse, Tencent, and Country Garden Back New Rui Peng Ahead of IPO

In the pet healthcare sector, where Hillhouse Capital has held significant stakes for nearly five years, Tencent and Country Garden have joined forces to enter the market.

At the end of last month, New Ruipeng Pet Healthcare Group (“New Ruipeng”), China’s largest pet healthcare enterprise with the most branch hospitals, announced the completion of a strategic financing round amounting to hundreds of millions of U.S. dollars. Investors in this round included Tencent, Country Garden Venture Capital, Boehringer Ingelheim, and other leading domestic and international institutions. Notably,During the financing process, New Ruipeng raised significantly more funds than originally planned., with a valuation of approximately RMB 30 billion. Shortly thereafter, Bloomberg reported that New Ruipeng was planning to initiate an overseas initial public offering (IPO).

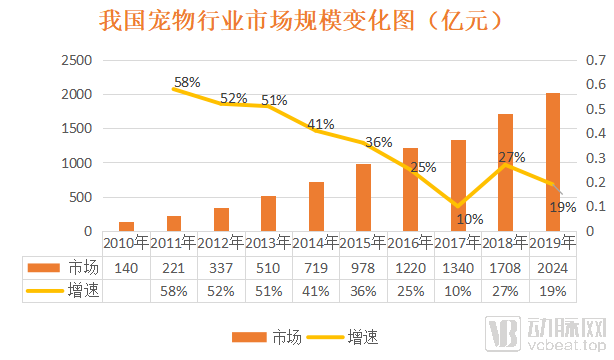

As is well known, the pet economy has been a star sector attracting significant attention in recent years.Amid the prevailing trend among contemporary young people of “petting dogs and cuddling cats,” the pet market has witnessed explosive growth.According to data from the “2020–2026 Research Report on the Current Market Status and Investment Opportunity Forecast for China’s Pet Industry” published by Zhiyan Consulting, China’s pet market size was approximately RMB 202.4 billion in 2019, and the market growth rate is projected to stabilize at around 13% by 2023.

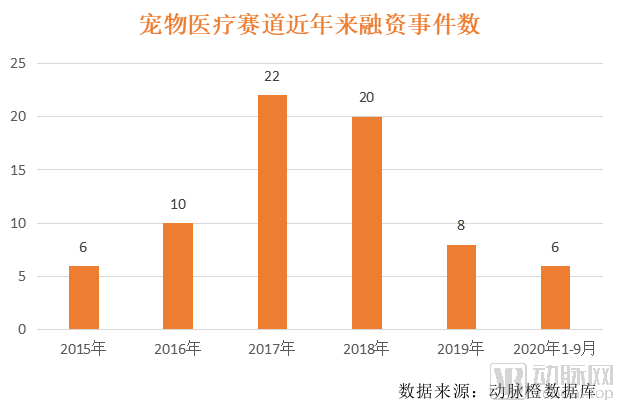

Behind the booming market lies the influx of countless entrepreneurs and investment institutions into this sector, driving attempts and breakthroughs to reshape the pet industry landscape from technological, business model, and capital perspectives.According to statistics from the VCBeat Orange Database, a total of 72 financing events occurred in China's pet healthcare sector from 2015 to September 30 this year.

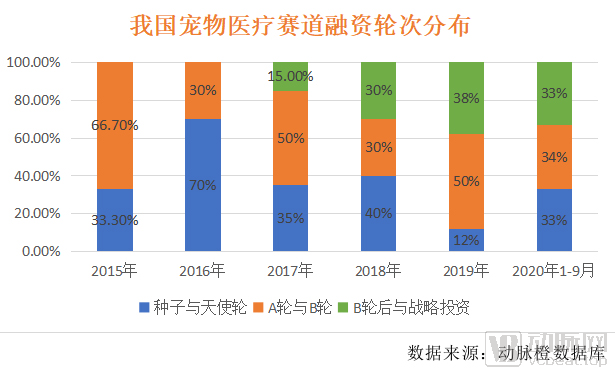

Although the number of financing events in the pet healthcare sector has shown a year-on-year decline since 2018,From the perspective of the proportion of financing rounds, early-stage projects are gradually decreasing, with project stages continuously shifting toward later phases.. In other words,As leading players in the sector, such as New Ruipeng Group, approach their IPOs, the pet healthcare industry is maturing, and its competitive landscape appears poised to solidify.

Of course, it is important not to overlook that,China’s pet healthcare sector currently faces challenges such as a shortage of specialized professionals and a lack of standardized management, while market regulation remains inadequate.. On the other hand, compared with developed countries such as the United States,China's pet healthcare market still has significant room for growth, with abundant market opportunities remaining.

Amid heavy capital investment and the entry of industry giants, what story has China’s pet healthcare sector told under the overarching theme of opportunities and challenges? And how will its subsequent chapters unfold?

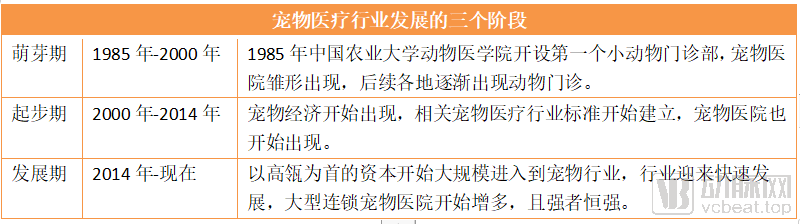

When discussing the inflection point at which the pet market began to undergo significant changes, one cannot overlook the year 2014.

Prior to this, China’s pet healthcare market remained in a relatively “wild” state: atMidstream veterinary hospitals are characterized by their “singular,” “small,” and “fragmented” nature, lacking brand recognition and exhibiting extremely low levels of digitalization. Moreover, upstream medical device R&D and downstream payment models remain in their nascent stages.

Capital’s entry has prematurely altered this landscape.At that time (2014), the online dividends generated by the rapid development of mobile internet were far from exhausted, and the venture capital community was engaged in fierce “battles” around e-commerce, O2O, and community group buying. Meanwhile, Hillhouse Capital, armed with substantial capital, took a different path by conducting in-depth research into the overlooked pet market, followed by significant investment:Hillhouse has progressively invested in various segments of the pet care industry, including veterinary hospitals, pet stores, industry-specific SaaS systems, and supply chain finance., it can be said to be pervasive.

Among them, in the field of veterinary medicine, Hillhouse adopted an “incubation + integration” approach, expanding its store network at a rate of 300 outlets per year throughOver three years, integrated more than 10 pet hospital brands across major cities in China。

“Hillhouse’s entry has directly propelled the pet healthcare industry into a phase of rapid growth,” an investor close to Hillhouse told VCBeat. “Benefiting from substantial capital and Hillhouse’s strong control over the industry, the landscape of the pet healthcare market is being redefined.”

In response to this trend, a significant amount of capital has begun to enter the market.In 2017 and 2018, investment and M&A activity in the veterinary healthcare industry reached its peak, with 42 financing deals occurring solely in the primary market, accounting for 58% of all financing events since 2015.

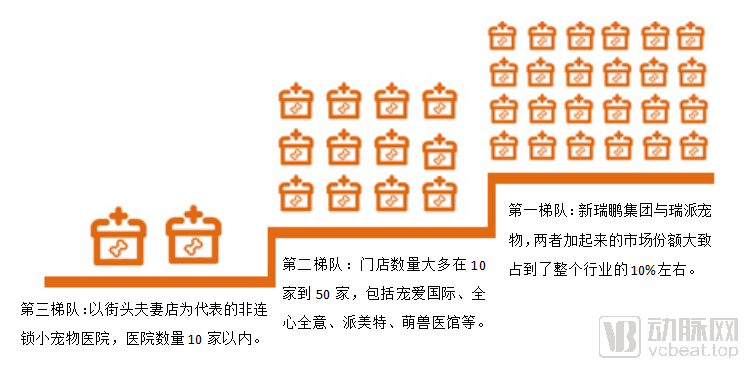

The data demonstrate the change.According to statistics from Chongyejia, there were over 17,000 veterinary hospitals in China in 2018. Among them, Hillhouse Capital, Ruipeng Pet Healthcare, and Ruipai Pet Healthcare (founded in 2012 and rapidly expanded through mergers and acquisitions) ranked as the top three in market share, operating more than 700, 400, and 300 veterinary hospitals, respectively.The increasing prevalence of large chain pet hospitals is becoming a trend.

Another visible trend is that the strong get stronger.With the support of capital,In January 2019, New Ruipeng Group (the integration of Ruipeng and pet hospitals invested by Hillhouse) completed its consolidation, marking the emergence of China’s largest and most well-capitalized pet healthcare platform.As of now, New Ruipeng operates a total of over 1,400 referral centers, central hospitals, specialized hospitals, and community hospitals.Together with Ruipai Pet, they are positioned in the industry’s first tier, with their combined market share accounting for approximately 10% of the entire sector.

Most other veterinary hospital brands operate between 10 and 50 clinics., including Chongai International, Quanxin Quanyi, Paimeite, and Meng Veterinary Clinic. Unlike New Ruipeng and Ruipai Pet, which have adopted a nationwide chain model,These brands exhibit significant differentiation in their market positioning.. For example, Chongai International positions itself in the mid-to-high-end pet healthcare market, while Petmate focuses on regional markets such as the three northeastern provinces of China.

In addition to these chain brands,The rest are non-chain small animal hospitals, typically represented by street-level mom-and-pop clinics., according to data from the "2019 Report on the Development of Pet Hospitals in China," among the 10,000 to 15,000 pet hospitals nationwide,Single-location or small-chain (fewer than 10 locations) veterinary hospitals account for approximately 80%–90% of the market share.

Additionally,In terms of geographic distribution, nearly 80% of pet hospitals are concentrated in first- and second-tier cities., which is attributable to the region's high economic development, large pet-owning population, and pet owners' strong awareness of veterinary healthcare spending.

“Following New Ruipeng’s latest round of financing, its initial public offering is expected to take place within the next one to two years. Thus, the lineup of leading players in the pet healthcare industry has been largely established.”For players in the second tier, adopting a strategy of deepening penetration in various provinces and cities and establishing a foothold through regional operations has also become a preferred business model.“the above-mentioned investors stated.

From Hillhouse Capital’s entry into the pet healthcare sector to the impending IPO of New Ruipeng, in which it has invested, the new landscape of the pet healthcare industry is now largely set.

Behind the sustained rapid growth of the market,Profit Growth for Pet Healthcare-Related Institutions Remains Unpromising。

Taking Ruipeng Pet Healthcare Group before its consolidation as an example, as the first publicly listed pet hospital company, its net profits from 2014 to 2017 were RMB 6.2264 million, RMB 20.2793 million, RMB 21.0541 million, and RMB 22.9606 million, respectively, indicating sluggish growth.

If industry leaders are struggling, smaller and more fragmented pet healthcare providers face even greater challenges.According to a report by Yiming.com, there were more than 23,000 pet hospitals in China as of July 2019, among whichMore than half are hovering on the brink of profitability and loss, or have already fallen into deficit.

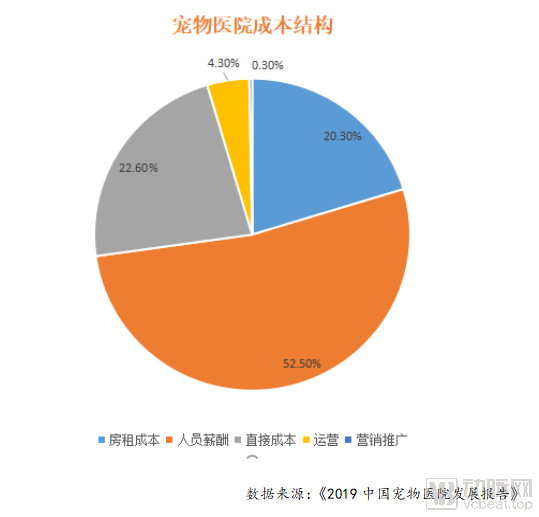

Why Is There Such a Stark Contrast Between Prospects and Profitability?First, let's examine the costs of veterinary hospitals.. According to data from the “2019 Report on the Development of Pet Hospitals,”Rent accounts for approximately 20% of the total costs of a veterinary hospital,Other expenses are primarily allocated to labor costs, medical devices and pharmaceuticals, and daily operational and maintenance expenditures.According to estimates by Danjie Chuangye, the annual rent for a 200-square-meter space in Beijing exceeds RMB 200,000, and the total annual cost for a clinic is at least RMB 1 million.

It is worth noting that,The Largest Cost Component—Labor Costs—Are Continuously Rising.This isDue toThe rapid increase in the number of pet hospitals has led to a shortage of professional veterinary talent.. Given the inherently small pool of individuals willing to pursue veterinary medicine, coupled with the lengthy training period, the growth in the supply of qualified professionals remains slow.

Additionally,The sharp increase in the number of hospitals has intensified competition, driven up customer acquisition costs, and triggered fierce price wars among institutions.Moreover, the costs of medical equipment and pharmaceuticals required for veterinary care are also gradually increasing, therebyPet hospitals are trapped in a vicious cycle of profit squeeze, making survival increasingly difficult.

Costs are gradually rising, but what is the revenue situation? The "2019 Pet Hospital Development Report" shows that 58.9% of pet hospitals have an average daily patient volume of less than 10, 85.2% of pet hospitals have annual revenues below 3 million yuan, and 39.1% of pet hospitals have annual turnovers of less than 1 million yuan.After deducting costs, the profitability of these pet hospitals hovers around the break-even point. Burdened by high costs and suboptimal revenue performance, most pet hospitals have fallen into a state of “promising prospects, but poor financial returns.”

As capital and industry giants enter the market, and leading companies list on secondary markets, the pet healthcare sector will accelerate toward greater consolidation and standardization. Consequently, enhancing the sector’s profitability has become a key focus for industry players in the next phase.

As the industry matures, high-return investment opportunities become increasingly scarce. Therefore, by re-examining the upstream and downstream segments of the industrial chain and observing emerging micro-trends in various niche sectors, one may identify opportunities for the next five to ten years.

First, let’s examine the distribution of the industry chain.In the pet healthcare sector, the upstream consists of pharmaceutical and medical device suppliers, the midstream comprises service providers, and the downstream includes payers.

At the upstream end, R&D of relevant pet drugs in China remains relatively weak, with a low market share., according to data from the "2019 China Pet Medical Industry Research Report," imported manufacturers account for nearly 70% of the domestic pet pharmaceutical market.In terms of medical devices and consumables, imports still dominate the market., but with domestic companies such as Mindray and United Imaging exerting efforts in this field,The pace of domestic substitution is accelerating.

In the midstream sector, veterinary hospitals are the core providers of medical services and currently the area attracting the most capital attention.. However, on the other hand, veterinary hospitals often compete with third-party testing markets in terms of equipment configuration, makingThe third-party testing market has not formed a differentiated and complementary relationship with veterinary hospitals, severely limiting its development.In addition to offline service systems, the number of internet-based pet healthcare service platforms and companies providing digitalization solutions for pet healthcare providers has been gradually increasing in recent years.

At the downstream end, in addition to pet owners as the payers, pet finance (including installment plans for veterinary care and pet health insurance) has also emerged as a minor trend in recent years.Of course, compared with traditional financial services, the pet finance market remains a niche sector, resulting in limited insurance products and a restricted network of partner hospitals.

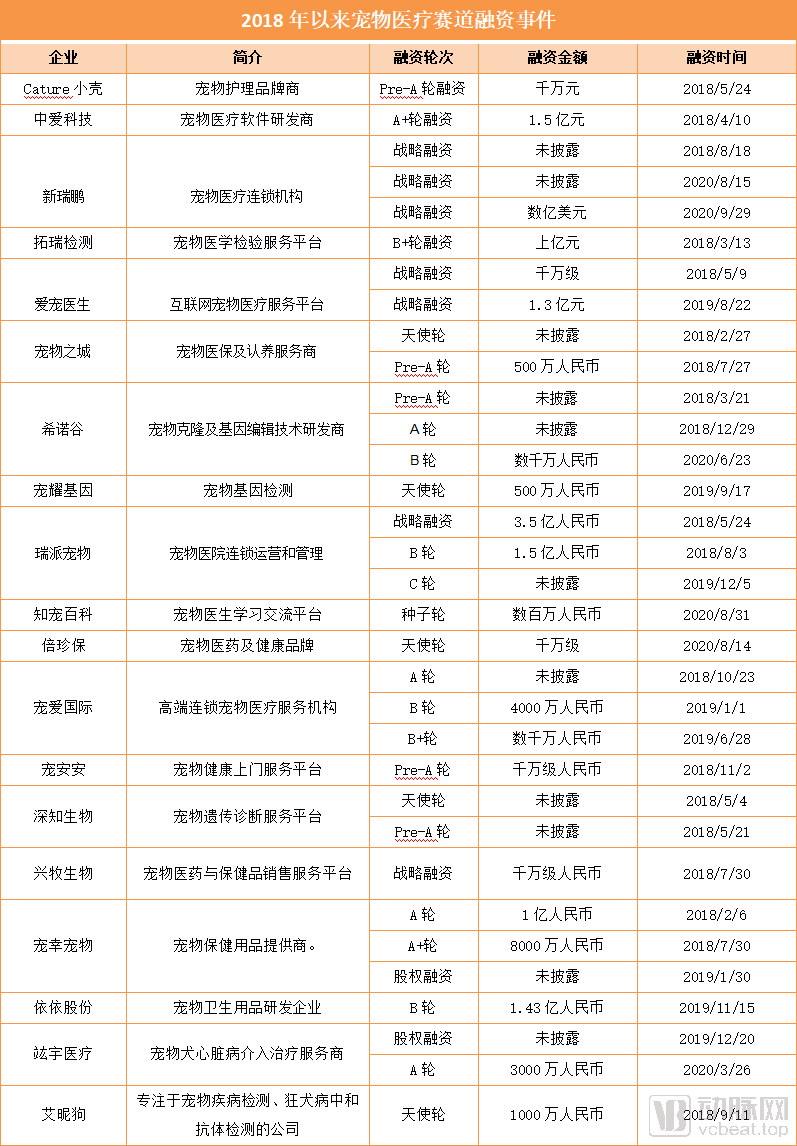

From this perspective, there are still many opportunities in the pet healthcare sector; however,Given the current level of market maturity, various opportunities still require market education and the test of time.Certainly, capital investors with a keen sense of smell have already taken action. To this end, VCBeat has compiled statistics on financing in the pet healthcare sector since 2018.

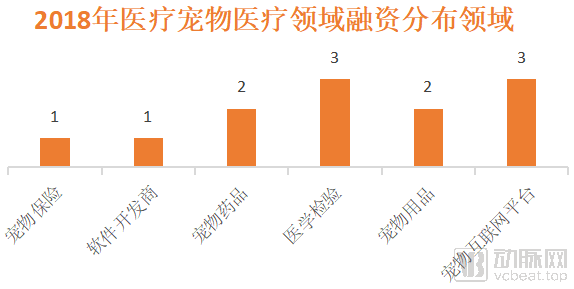

Over the past three years, a total of 19 pet healthcare-related companies have secured financing.Among them, there is one pet insurance company, one software developer, two pet pharmaceutical R&D enterprises, two pet supplies R&D enterprises, three pet medical testing companies, and two pet internet platforms.

Although the financing amounts in the aforementioned sub-sectors are modest in scale, it is evident that investors have already begun to position themselves to seize the next opportunity and gauge the market’s depth. Once conditions mature, a substantial influx of capital will follow naturally.

Next, we will examine the current progress in niche pet sectors by focusing on two aspects: pet insurance and pet pharmaceuticals.

Pet Insurance: Breakthroughs in Pet Identification Technology Signal Imminent Rapid Growth

Pet insurance is not a new concept. As early as 2004, Huatai Insurance launched the first third-party liability insurance for pets. In 2014, PICC and Ping An Insurance sequentially introduced pet medical insurance, leading to an expansion in the variety of pet insurance products. However,At that time, pet insurance did not generate stable profits for insurers; it primarily served as a customer acquisition tool.

Underlying this is the difficulty in standardizing pet products, coupled with issues such as information opacity and low levels of digitalization in the pet healthcare market, which make insurance companies prone to oversights in product design.According to a report by China Securities Journal, based on calculations that take into account factors such as insurance coverage, sum insured, payout limits, and reimbursement ratios, the actual cost savings for users of pet insurance amount to less than 50%, which has also resulted in relatively low acceptance of such products among pet owners.

The situation is changing.For pet insurance companies, the biggest pain point is the difficulty in pet identification.. Some pet owners, after purchasing insurance for their pets, commit fraud by submitting claims for a different sick animal that resembles the insured pet, causing significant losses to insurance companies.Based on this, electronic identification technology has been applied to the field of pet insurance.

For example, in late July this year, Alipay’s insurance platform announced the opening of its pet nose-print recognition technology and, in partnership with China Continent Insurance and ZhongAn Insurance, applied this technology to pet insurance for the first time. This pet insurance product covers two major categories of pets: cats and dogs. At the time of enrollment, Alipay’s insurance platform creates a unique electronic profile for each pet based on its nose-print information. During claims processing, policyholders can complete the claim with a single click by verifying the pet’s identity through nose-print scanning. Reportedly, the recognition success rate of the pet nose-print recognition technology exceeds 99%.

Beyond the technological front, business models are also undergoing transformation.At the end of September this year, Ping An Property & Casualty Insurance announced its entry into the pet market and launched the “Ping An Pet Care Medical Insurance Plan.” This product is China’s first pet insurance plan that integrates zero deductible, direct billing at selected hospital counters, and age-unrestricted renewal. Unlike the mainstream “receipt-based reimbursement” model prevalent in the market, the “Ping An Pet Care Medical Insurance Plan” offers a “direct counter billing” claims settlement method. After receiving veterinary care, pet owners need only pay their out-of-pocket portion at the partner hospital’s counter before leaving, while Ping An Property & Casualty Insurance settles the insured amount directly with the hospital.

Pet Pharmaceuticals: New Preventive Medications, Such as Regular Deworming Treatments, Will Become the Trend

Pet pharmaceuticals account for half of the pet healthcare market.According to statistical data from the Huajing Industry Research Institute in 2019, the pet pharmaceutical market accounted for 52% of the total pet healthcare market. However, research and development of pet drugs in China remains in its early stages, primarily manifested in two aspects.

First, in the field of prescription pharmaceuticals, China has few companies with independent R&D capabilities in pet pharmaceuticals, and those that exist are small in scale. Moreover, the few companies that hold patents for pet drugs mostly rely on expired patents to produce generic medications. Additionally, regarding medication standards, the Ministry of Agriculture currently stipulates only 183 drugs approved for use in pet treatment, which is insufficient to meet the daily diagnostic and therapeutic needs of pets.

Second, in the field of functional products, the development of functional pet consumer products in China remains relatively disordered, with some products lacking support from reliable scientific research teams. In contrast, in developed countries such as those in Europe and the United States, where preventive nutrition is widely adopted, veterinarians commonly recommend that pet owners use functional nutritional supplements or products for daily healthcare and disease prevention in pets.

Additionally,Compared with the more specialized and standardized pet medications abroad, those in China are often used interchangeably for humans and pets, which is one of the reasons for the inflated prices of pet drugs.

The shortage of professionals in pet healthcare is currently a barrier to the development of China’s pet pharmaceutical industry.. In general,It takes at least 10 years to train a senior researcher in veterinary medicine., but the rapid growth of the pet industry in recent years has led to a shortage of talent in veterinary pharmaceuticals.The mismatch between supply and demand has created opportunities for the rise of innovative enterprises, and securing core R&D talent will provide companies with a first-mover advantage.

For example, Beizhenbao, a Chinese pet pharmaceutical and health brand that secured financing this August, has built its R&D team in collaboration with the College of Animal Science and Veterinary Medicine at Huazhong Agricultural University, a leading institution in veterinary medicine in China. It provides traceable, comprehensive solutions based on pets’ health conditions. The company has currently launched five functional health products, including Yanweile Nutritional Granules, Miaoningkang Anti-Stress Soothing Granules, and Youchongqin Oral Care Granules.

Beyond collaborating with academic institutions that possess specialized talent, how should domestic pet pharmaceutical companies further exert their efforts? Let us examine the market structure.Immunization and deworming currently account for the largest share of the pet pharmaceutical market; however, the vast majority of this market in China is dominated by multinational industry leaders, resulting in a strong demand for domestically produced alternatives.In addition, the U.S. pet pharmaceutical industry, which benefits from a more developed pet economy, serves as a reference point. American pharmaceutical companies have developed numerous new drugs for routine use in pets, such as medications for dogs to prevent motion sickness, treat depression, and prevent diseases, all of which have received positive market feedback.

It is not difficult to see that,As the pet economy matures and pet owners’ purchasing power strengthens, demand for new preventive pet medications—such as regular deworming agents—is poised for rapid growth. Meanwhile, pet pharmaceuticals addressing niche indications, including motion sickness and depression, will also enjoy substantial market potential.

As a niche segment within the broader healthcare industry, the veterinary care sector remains relatively specialized. However, drawing on the mature development experience of the U.S. pet healthcare market,In the future, the pet healthcare sector will inevitably see industry leaders emerge with market capitalizations reaching tens of billions, or even hundreds of billions, particularly in the areas of pharmaceutical and medical device R&D, medical services, and payment solutions.

Although the competitive landscape within the niche segment of pet medical services is gradually taking shape, significant uncertainties remain for the future. For leading pet hospital groups, it remains difficult to predict how they will expand and to what extent they can achieve integration. Looking at other sectors such as pet pharmaceuticals and pet insurance, new entrants will continue to emerge and more capital will flow in. However, whether these developments can fundamentally address critical challenges—such as the scarcity of specialized professionals and the need for market education—will test the wisdom of all stakeholders involved.

Certainly, to capitalize on the "cute pet" dividend, pioneers navigating the waves in the field of veterinary medicine require not only capital and talent but also sufficient perseverance and patience. Only in this way will the veterinary medicine sector continue to broaden its horizons.