Learning from CVS's Business Evolution: Strategic Layout Recommendations for China's Internet Healthcare Enterprises

CVS Health

Pharmaceutical Retailers

Author: Zhao Lekang, Analyst at a Securities Firm

Recently, the Hong Kong Stock Exchange disclosed JD Health’s prospectus, which contained a wealth of information. It not only revealed JD Health’s business scale exceeding RMB 10 billion but also provided a detailed description of its ongoing efforts to build a comprehensive online healthcare service ecosystem and its future development direction. This inevitably prompts us to consider the U.S. pharmaceutical and healthcare giants, whose market capitalizations exceed $100 billion: how significant is the gap between such American industry leaders and domestic internet pioneers like JD Health? What are the similarities and differences in the development strategies of Chinese and U.S. pharmaceutical and healthcare enterprises? This article will primarily explore the similarities and differences between the layout strategies of China’s internet giants in the pharmaceutical and healthcare sector and those of U.S. retail pharmacy giants, focusing on their respective development paths and directions.

The development paths of the two largest pharmacy chain giants in the United States, CVS Health (hereinafter referred to as “CVS”) and Walgreens Boots Alliance, have been markedly different. CVS is an exemplary model of vertical integration along the industry chain. In contrast, leveraging its dominant position and resource advantages in the pharmaceutical retail sector, Walgreens Boots Alliance has pursued a horizontal expansion strategy through internationalization to enlarge its market scale. This approach enables the company to replicate its existing portfolio of private-label products, supply chain resources, and operational capabilities in international markets, while fostering synergistic integration to reduce overall group costs and maximize efficiency.

Walgreens Boots Alliance’s core business is relatively focused on pharmaceutical distribution, encompassing both retail and wholesale operations. As of fiscal year 2019, its nearly 14,000 stores were distributed across 11 countries, with approximately 9,200 located in the United States. Revenue from its U.S. retail segment accounted for three-quarters of total revenue, while international operations contributed less than 10%. Wholesale revenue represented nearly 17% of the total.

Domestic internet giants, including Alibaba Health and JD Health, possess inherent digital DNA that dictates their greatest resources and advantages lie in massive online traffic and advanced technological capabilities in internet services, big data, cloud computing, and artificial intelligence. However, they remain relatively weak in offline store channels and pharmaceutical retail supply chains. This reality precludes them from pursuing a horizontal expansion path akin to that of established pharmaceutical retail giants such as Walgreens Boots Alliance.

As expected, Alibaba Health and JD Health have both chosen to follow the vertical industry chain model exemplified by CVS Health, entering the healthcare and pharmaceutical sectors. Therefore, this article focuses on analyzing the strategic development path of CVS Health’s vertical industry chain.

Innovation is the soul of CVS’s development strategy. Over the past decade, CVS has rapidly entered the healthcare and payment sectors across the upstream and downstream segments of the industry chain through strategic acquisitions of leading companies. It has continuously innovated to develop medical and health services covering the entire lifecycle, striving to build a complete, closed-loop ecosystem for its industry chain. Within this closed loop, various business units collaborate efficiently, sharing resources such as customer traffic and data. This approach not only effectively enhances CVS’s profitability but also improves customer experience and brand loyalty.

Prior to 2005, CVS’s primary strategic focus was on aggressive expansion within the traditional retail pharmacy sector, targeting small and medium-sized pharmacy chains for acquisition. Driven by a dual strategy of organic store openings and mergers and acquisitions, the company significantly scaled its store network. The number of stores grew rapidly from approximately 1,000 in 1994 to around 5,500 in 2005, surpassing Walgreens Boots Alliance to become the largest retail pharmacy chain in the United States by store count.

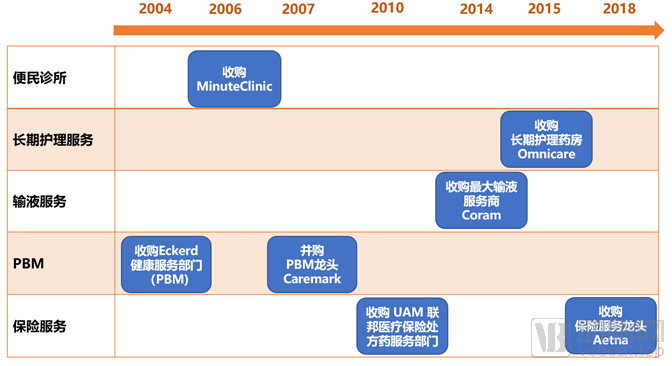

After becoming the largest pharmacy chain in the United States, CVS began to make groundbreaking strides toward vertical integration of its industry chain after 2005. A key milestone was the 2006 acquisition of MinuteClinic, which marked CVS’s entry into the upstream healthcare services sector. Over the following decade, CVS relentlessly pursued mergers and acquisitions, acquiring Caremark (a leading PBM company, noting that CVS had already entered the PBM field with the establishment of Pharmacare in 1994), the federal Medicare prescription drug services division of UAM, Coram Specialty Infusion Services, Omnicare (a long-term care pharmacy), and more than 1,600 pharmacies and clinics from the retail chain Target. This culminated in the 2018 acquisition of the major insurer Aetna. With these moves, CVS largely completed its vertical industry chain layout, successfully expanding into upstream healthcare services and downstream payment services (including PBM and insurance services) by acquiring outstanding companies, including industry leaders, across the supply chain.

CVS Expands Its Upstream and Downstream Supply Chain Through Mergers and Acquisitions. Source: Financial Reports, Company Website, Public Information

In fiscal year 2019, CVS Health’s revenue reached $256.8 billion, with pharmacy retail accounting for only 30% of total income. Nearly 50% of revenue was derived from PBM and other service-based businesses, while the remaining 23% came from its insurance operations.

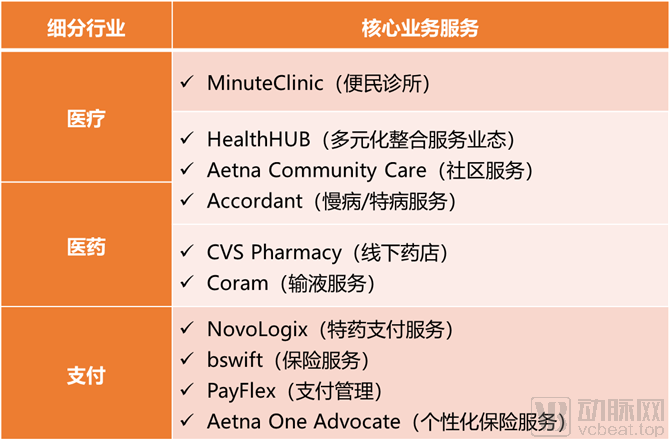

CVS Health offers a highly diversified service portfolio encompassing medical services, pharmaceuticals and health management, pharmacy benefit management (PBM) services, and insurance payment services. In effect, it has established an initial framework for whole-lifecycle health management catering to diverse population groups.

CVS Full Lifecycle Service Portfolio, Source: Financial Reports, Company Website

Notably, CVS’s service offerings are predominantly anchored in physical locations. Leveraging its origins as a retail pharmacy chain, CVS has built a network of nearly 10,000 stores across the United States, providing nationwide coverage. According to its annual report, 70% of Americans live within five kilometers of at least one CVS pharmacy. In particular, its strategic placement of community-based stores provides the physical infrastructure for various community services, home-based care, and convenient clinics. This approach also enhances profitability by reducing costs through effective synergy among its diverse business segments.

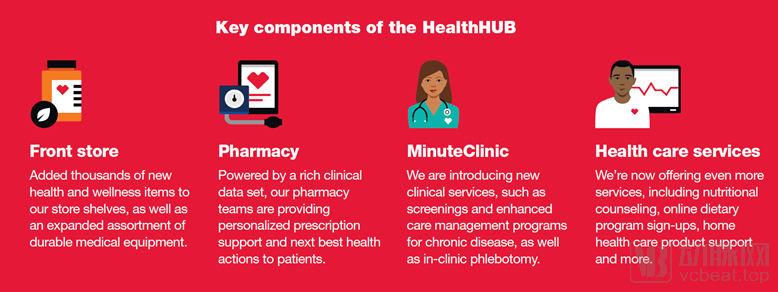

Here, we would like to highlight CVS’s innovative business model: the HealthHUB. This serves as an excellent example of how CVS efficiently integrates and synergizes its acquired capabilities to provide one-stop services and product sales spanning the healthcare, pharmaceutical, and payment sectors of the industry chain.

HealthHUB is an innovative business format that CVS began piloting in 2019. The essence of this model is to integrate CVS’s existing business formats and service capabilities, establishing diversified brick-and-mortar stores that combine convenient medical care, chronic disease management, health management, and the sale and services of traditional pharmacy products. It is somewhat analogous to a shopping mall in the retail industry. By leveraging synergies across various business units and sharing CVS’s physical store resources—particularly its community-based locations—the model provides customers with optimized one-stop services while significantly reducing CVS’s operational costs.

HealthHUB’s Main Business Activities, Source: Financial Report

Currently, the initial scope of HealthHUB’s business includes the following:

1. MinuteClinic’s convenient healthcare services, including various laboratory and diagnostic tests, chronic disease management services (with enhanced monitoring of physiological indicators for patients with chronic conditions), and minor surgical procedures performed at the clinic.

2. Health Services: Each store is staffed with licensed pharmacists who provide nutritional counseling, other health and wellness services, and product recommendations, enabling customers to manage their health at home. Customers may also enroll in online dietary wellness programs offered by the stores.

3. The store’s product assortment includes thousands more health, wellness, and related medical device items than typical stores.

4. Leverage CVS Health’s extensive data resources from healthcare institutions to provide customers with personalized prescription services and corresponding health services.

In fiscal year 2019, CVS piloted the conversion of 50 traditional stores into HealthHUB locations in select U.S. regions. The number of HealthHUB stores was projected to reach 600–650 by 2020, with plans to expand to 1,500 locations in 2021.

Through continuous pilot programs, CVS is exploring which medical services, pharmaceutical care, health services, and products are most in demand, allowing for ongoing optimization and adjustments. Once the model matures, this diversified health service format can be rapidly scaled to other stores, driving innovative upgrades for traditional pharmacy locations. Meanwhile, innovative services and products across various formats can be quickly rolled out nationwide.

Both Alibaba Health and JD Health originated from e-commerce businesses, backed by China’s two major internet giants, Alibaba and Tencent. Consequently, their development strategies and pathways in the pharmaceutical industry are remarkably similar. Here, we focus on how JD Health has vertically integrated its industrial chain following the CVS model to compete for a share of the pharmaceutical market.

According to the prospectus recently released by JD Health, its mission is to become the premier health steward for the nation. It is committed to building a complete and comprehensive “Internet + Healthcare” industry ecosystem, providing users with holistic health and medical services to meet their diverse needs across all aspects of health products and services. The company aims to establish a digital-driven health management platform that covers the entire user lifecycle and all scenarios, with the supply of pharmaceuticals and health products at its core and medical services as the key lever.

This clearly outlines JD Health’s strategic development intent: rather than resting solely on its current RMB 10.8 billion in revenue from pharmaceutical retail, the company aims to actively expand upstream into the broader healthcare sector. Following the CVS Health model, it seeks to build an integrated ecosystem of “healthcare + pharmaceutical” value-added services, offering a one-stop, full-lifecycle health management portfolio that includes medical services, chronic and special disease management, and general wellness services. In the future, JD Health may even follow CVS Health’s lead by venturing downstream into the payment sector, developing a suite of payment-related services such as Pharmacy Benefit Management (PBM) and commercial insurance.

Let’s examine the value-added service products that JD Health has currently developed in the healthcare services sector. A comparison with CVS Health reveals that JD Health is gradually exploring, establishing, and enriching its value-added service offerings across various specialized segments. Although its current service portfolio is far less comprehensive than that of CVS Health, and revenue from services remains only a small fraction of revenue from pharmaceutical retail sales, the strategic blueprint has been laid out, and the path forward is clear.

CVS and JD Health’s Service Business Layout, Source: Prospectus, Company Website, Financial Reports

It is worth noting that CVS Health’s service offerings are primarily delivered through offline channels, whereas JD Health’s services are mainly conducted online, gradually rolled out via the JD Health App and the JD Internet Hospital platform. This distinction aligns precisely with their respective corporate DNA: CVS Health as a traditional brick-and-mortar retail pharmacy giant, and JD Health as an online internet conglomerate.

JD Internet Hospital Platform Offers a Variety of Medical Services, Source: Official Website

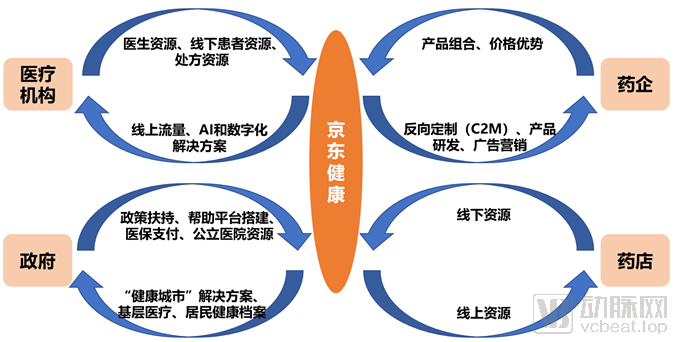

Beyond its comprehensive layout in medical, pharmaceutical, and health services, JD Health aims to achieve what CVS Health cannot accomplish online: leveraging its core competencies in traffic and technology as an internet giant to drive digital transformation across the industry chain and empower B-side participants throughout the entire value chain.

For healthcare institutions and physicians, JD Health can leverage the traffic resources of its 72.5 million annual active users by building a tiered diagnosis and treatment service system comprising general practitioners and specialists. This approach moves the management of mild and chronic conditions, follow-up visits, and health management online, while directing patients with critical illnesses and major medical needs to offline healthcare institutions, thereby optimizing the allocation of medical resources. Meanwhile, JD Health creates a platform for physicians to practice at multiple sites, enabling them to reach more patients online, utilize fragmented time to provide services anytime and anywhere, build their personal brands, and increase exposure to various complex and rare cases, thus enhancing their professional expertise.

Meanwhile, leveraging digital technologies such as artificial intelligence, cloud computing, and big data, JD Health is developing applications including AI-assisted consultation, AI-assisted prescription review, and intelligent health management devices. By integrating these applications with cloud-based infrastructure, JD Health provides healthcare institutions with comprehensive digital solutions covering a wide range of services. Additionally, it helps healthcare systems establish digital operating systems to optimize operational processes.

Furthermore, leveraging its big data capabilities, JD Health can provide reverse customization for pharmaceutical companies and health product suppliers, supporting their product research and development. It can also offer “Healthy City” solutions to local governments, covering areas such as primary healthcare, resident health records, and medical insurance payments.

Correspondingly, by collaborating with various stakeholders across the industry chain, JD Health can secure policy support, access to physician and patient resources, prescription resources, supply chain product offerings, and price concessions from its partners. This facilitates the construction of its comprehensive industry-chain ecosystem platform, thereby enhancing the product and service experience for end consumers and fostering a virtuous cycle.

As an online internet giant, JD Health’s relationship with leading offline retail pharmacy chains remains unclear. Each party possesses unique online and offline resource advantages that the other cannot replicate. Whether their future interactions will lean more toward competition or cooperation remains to be seen.