How Alibaba, Tencent, and Pinduoduo Are Tackling Vaccine Appointment Challenges Through 'Internet + Vaccines'

Authors: Yang Xue, Zhou Tianyi. Jointly published by VCBeat (WeChat ID: vcbeat) and Easy Clinic Setup (WeChat ID: dxykzs).

In recent years, China’s healthcare industry has undergone a significant digital transformation: digitization has reshaped hospital service models and operational formats, bringing many aspects of medical services online. However, the entire healthcare sector resembles an iceberg; the currently digitalized scenarios—such as appointment scheduling, consultations, and follow-up visits—represent only the tip above the water, while numerous underlying scenarios beneath the surface remain largely untouched.

Are there any sectors that urgently require digital transformation but still have low digital penetration? Yes, vaccine services are one such sector.

Especially this year, under the impact of the COVID-19 pandemic, public attention to and demand for vaccines have risen significantly, suddenly amplifying the supply-demand imbalance in the vaccine market.

In reality, the mismatch between vaccine supply and demand has long been a persistent and challenging issue. Taking the 9-valent HPV vaccine as an example, it has remained extremely difficult to secure appointments since its market launch. The high demand for the 9-valent HPV vaccine once sparked a surge in people traveling to Hong Kong for vaccination, and it remains scarce to this day. This shortage pattern recurred with the release of this year’s influenza vaccines. Although the batch release volume of influenza vaccines from July to September this year already exceeded the total for the entire previous year, stocks were depleted by the National Day holiday.

As the imbalance between vaccine supply and demand has become the new normal, if we assume the worst-case scenario—a confluence of this year’s influenza transmission and the ongoing COVID-19 pandemic—society will likely require a large number of temporary vaccination sites. The batch release volume of influenza vaccines is on the order of 30 million doses, while that of COVID-19 vaccines will far exceed this figure. Consequently, the existing vaccine delivery system will face significant pressure in meeting vaccination demands.

However, the challenge lies not only in the sudden surge in demand but also in determining through which channels to meet this vaccination demand.

VCBeat (WeChat ID: vcbeat) has found through statistics that in the niche field of digital vaccine services, internet companies such as Alibaba Health, Tencent Health, Baidu Health, Pinduoduo, and DXY have already made their moves. At this stage, the "Internet + Vaccines" model is mainly focused on vaccine e-commerce, addressing the issue of information asymmetry.

In the future, within the vaccine market—characterized by prominent supply-demand imbalances and low digital penetration—the involvement of internet companies may present an opportunity to integrate the non-EPI (Expanded Program on Immunization) vaccine market from two angles: optimizing demand and expanding supply, thereby boosting vaccination rates that have long remained at low levels.

Open the vaccine appointment channels on your mobile phone, and you will find that it is difficult to secure appointments for many non-EPI (Expanded Program on Immunization) vaccines. The difficulty in booking appointments is not limited to well-known categories such as HPV and influenza vaccines; it also extends to other non-EPI vaccines, including those for herpes zoster and rabies.

The widespread difficulty in securing appointments for various vaccines primarily reflects a surge in vaccine demand. The sharp increase in demand for non-EPI (Expanded Program on Immunization) vaccines is expected to become the new normal for the vaccine industry. Previously, China had low vaccination rates for non-EPI vaccines; the current surge in demand is, to some extent, making up for historical deficits.

China’s vaccination rate for vaccines included in the National Immunization Program remains above 90%. However, coverage rates for non-program vaccines are generally low. Compared with developed countries, China’s vaccine market has substantial room for expansion. In terms of per capita vaccine expenditure among major global markets, China’s figure stands at only $3.71, whereas those in the United States and Japan are $47.27 and $20.44, respectively.

Taking influenza vaccines as an example, the penetration rate in China is only 2.2%. Compared with the over 50% penetration rate in the United States, there is substantial room for growth in influenza vaccine coverage in China.

As new blockbuster vaccines continue to emerge in the non-immunization program category and public awareness of vaccines deepens in China, vaccination willingness is rising, driving sustained growth in demand for non-immunization program vaccines.

The most evident response has been a substantial increase in public willingness to receive influenza vaccination, driven by expert education and outreach following the COVID-19 pandemic in the first half of the year, which has led to surging demand for flu vaccines. From July to September this year, the National Institutes for Food and Drug Control (NIFDC) approved and released 33.3596 million doses of influenza vaccine, already surpassing the full-year total of 30.7842 million doses in 2019.

Spurred by the COVID-19 pandemic, China’s vaccine market is reaching an inflection point for industry growth, with its market size set to expand rapidly, particularly in the segment of non-immunization program vaccines.

According to the third-quarter report for 2020 released by Zhifei Biological Products, a domestic vaccine manufacturer, the company’s revenue for the first three quarters of 2020 reached RMB 11.049 billion, a year-on-year increase of 44.14%, despite the impact of the COVID-19 pandemic in the first half of the year. Net profit attributable to shareholders of the listed company amounted to RMB 2.479 billion, up 40.59% year on year. In the third quarter alone, revenue totaled RMB 4.056 billion, a year-on-year increase of 54.37%, while net profit attributable to shareholders reached RMB 974 million, up 58.13% year on year.

Under the impact of the COVID-19 pandemic, the robustness of the vaccine industry is evident. Non-immunization program vaccines account for over 90% of China’s vaccine market.

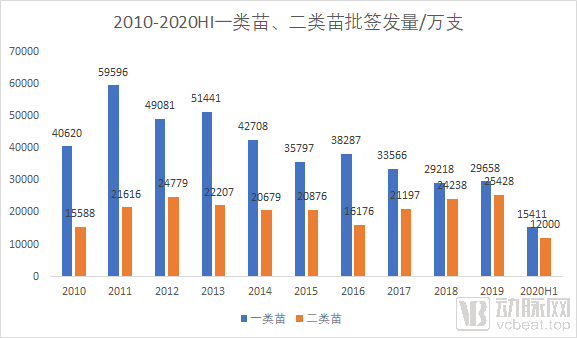

China’s vaccine batch release volume has remained stable at approximately 550 million doses. Of this total, vaccines under the National Immunization Program (NIP) and those outside the program account for roughly a 30:70 split. The share of non-NIP vaccines is gradually increasing, leading to continuous market expansion. In 2010, NIP vaccines accounted for about 46% of the total number of batches released; by 2019, this proportion had declined to 31%. This indicates a clear downward trend in the share of NIP vaccine batch releases, alongside a rapid rise in the volume of non-NIP vaccine batch releases.

In terms of market size, according to Frost & Sullivan data, China’s vaccine market generated RMB 33.17 billion in revenue in 2018. The National Immunization Program (NIP) vaccine market reached RMB 3.08 billion in revenue in 2018, while the non-NIP vaccine market achieved RMB 30.09 billion in revenue in the same year. China’s overall vaccine market is projected to grow to RMB 97.36 billion by 2023, representing a compound annual growth rate (CAGR) of 26.5% from 2018 to 2023.

Among these, non-EPI vaccines account for over 90.7% of the market size. It is foreseeable that the share of non-EPI vaccines will continue to rise as more varieties become available in the future.

The vaccine industry, having weathered the darkest “black swan” events, is now regaining its strength, yet an unexpected industry shift has arrived. Clearly, existing supply and service capabilities are not yet prepared for this change.

On the supply side, there is currently no communication platform between the regulatory authorities responsible for vaccine approval, oversight, and utilization, and influenza vaccine manufacturers. For these enterprises, accurately forecasting demand is challenging, and vaccine production is constrained by specific costs and lead times. Consequently, they generally adopt a relatively conservative strategy and are reluctant to scale up production.

In terms of service capacity at vaccination sites, China has approximately 30,000 to 40,000 public vaccination sites, while the number of non-public vaccination sites ranges from 300 to 400.An industry insider stated, “The vaccination capacity of the primary-level community health centers and township health clinics we have contacted is nearly saturated, resulting in significant pressure on offline vaccination services.””

On one side, there is rapidly growing demand; on the other, lagging supply and service capacity. To alleviate the mismatch between supply and demand, where can China’s vaccine supply generate incremental growth?

In the United States, family physicians can administer vaccinations during home visits, and pharmacies also offer influenza vaccination services. When U.S. residents seek flu shots, pharmacies typically post notices; after consumers register, the pharmacy’s data is immediately uploaded to the Centers for Disease Control and Prevention (CDC) website, eliminating multi-tiered reporting procedures. Authorized entities can directly access the website to view specific county-level vaccination statistics within each state, ensuring a high degree of transparency.

We believe that following the implementation of the Vaccine Administration Law of the People's Republic of China, private clinics and hospitals will have the opportunity to become a new source of growth in vaccine administration.

A former employee of the Shanghai CDC stated that public vaccination sites are already stretched to their limits in administering vaccines under the National Immunization Program. If they were to further cope with a surge in demand for non-program vaccines, most public sites would be largely unable to bear the burden. This portion of the workload could instead be shouldered by non-public vaccination sites.

In China, Article 44 of the Vaccine Administration Law of the People's Republic of China stipulates that vaccination entities must meet three conditions: (1) hold a Medical Institution Practice License; (2) have physicians, nurses, or village doctors who have undergone professional training in preventive vaccination organized by the health administrative department of the county-level people's government and passed the assessment; and (3) possess refrigeration facilities and equipment that comply with vaccine storage and transportation management standards, as well as cold-chain custody systems.

It is also explicitly stated that medical institutions meeting the specified conditions may undertake non-immunization program vaccination services, as determined by the health administrative departments of local people's governments at or above the county level, and shall report to the health administrative department that issued their Medical Institution Practice License for record-filing.

It can be seen from these three regulations that the model of vaccine administration in pharmacies is not replicable in China, whereas non-public medical institutions can meet the required conditions.

An industry insider stated, “Last year, we witnessed a small wave of emergence of private vaccination sites, primarily driven by the Vaccine Administration Law of the People’s Republic of China, which was passed in June 2019 and changed the application process for medical institutions providing vaccination services from a registration system to a filing system.”

According to statistical data from local Centers for Disease Control and Prevention (CDC), private medical institutions in 19 provinces (municipalities) across China, including Beijing, Shanghai, Guangdong, Hunan, Hubei, Jiangsu, Shandong, and Sichuan, have obtained qualifications for vaccine administration, with clinics and outpatient departments well represented among them.

For non-public medical institutions, offering vaccination services can drive patient traffic to clinics and attract individuals with high health needs, most of whom possess strong purchasing power. There are vaccine categories with significant appeal for both adults and children, such as HPV vaccines and influenza vaccines; for children, these include multi-antigen and multivalent vaccines that can serve as alternatives to Category I vaccines.

However, at this stage, the number of non-public vaccination sites remains small. According to statistics from VCBeat, there are 416 clinics in Beijing offering self-paid influenza vaccination services. More than 90% of these clinics are public community health service centers and township health centers. A small proportion are non-public medical institutions. Among private hospitals providing vaccination services, most specialize in women’s and children’s healthcare, such as Beijing Changyang Women and Children’s Outpatient Department (a clinic under Amcare Windmill Medical), Beijing United Family Hospital Clinic, New Century Ronghe Outpatient Department, and Beijing Jiahui Women and Children’s Hospital.

Why Have Not Many Non-Public Institutions Entered the Vaccine Vaccination Market After Policy Liberalization?

First, although the regulatory framework has shifted from a registration-based system to a filing-based system, the stringent review mechanisms for vaccination sites remain unchanged. This is one of the reasons why there has not been a rapid increase in vaccination sites operated by non-public medical institutions following the policy liberalization. Meanwhile, policy implementation involves a certain time cycle and process. Although Article 44 of the Vaccine Administration Law of the People's Republic of China explicitly stipulates the filing-based system, the specific detailed rules are delegated to provincial and municipal governments for formulation. Currently, only Jiangsu and Zhejiang provinces have issued such detailed rules nationwide.

Meanwhile, the service and management capabilities required for vaccination pose significant challenges for most clinics. The vaccine supply chain differs entirely from that of pharmaceuticals, and administering vaccines demands substantial professional expertise, such as assessing eligibility for special populations. Therefore, vaccination services must be implemented through specialized vaccination sites with professional support. Currently, in addition to community health service centers, some private clinics and hospitals with high-quality medical care and services have obtained the relevant qualifications.

How to Enable a Large Number of Private Clinics and Hospitals to Possess Comprehensive Vaccination Service Capabilities: VCBeat Has Learned That DXY, Which Boasts Extensive Clinic Resources Within the Industry, Is Attempting to Establish a Comprehensive Service Platform,and collaborate with vaccine manufacturers,Establish a seamless pathway from vaccine supply to vaccination sites, providing comprehensive support to clinics while delivering practical, end-to-end vaccination services to the market.

Earlier this year, reports emerged that DXY was actively expanding into this sector. Insiders revealed that DXY Doctor’s vaccine appointment service currently covers more than 10 cities and partners with approximately 80 clinics, with rapid expansion still underway.

We can expect that an increasing number of private hospitals and clinics will begin to participate in the vaccine market, helping to expand its overall size.

In the vaccine market, both demand and supply are undergoing transformation, yet another critical element cannot be overlooked: the digital platforms that bridge the two.

The 2019 “Changsheng Bio-technology Vaccine Incident” served as a wake-up call for vaccine distribution management, accelerating the implementation of end-to-end online traceability for vaccines. Through Alibaba Health’s “Code-based Traceability” system, coverage of vaccine manufacturers has reached 100%. However, in another core aspect of digitalizing vaccine services—appointment scheduling—the public still cannot access real-time information on local vaccine inventory online, particularly for non-EPI (Expanded Program on Immunization) vaccines.

Digitalization of vaccines is by no means a novel endeavor. Currently, digital solutions for vaccines can be categorized into two types. The first type comprises digital platforms designed for government regulatory purposes, enabling end-to-end digital management of vaccine distribution and immunization records. The second type consists of digital solutions tailored to individual vaccination providers, primarily focusing on internal information systems that digitize traditional processes such as registration, queue management, health education, and statistical reporting.

We can regard internet platform enterprises as a third category of businesses, as they are exploring user-centric digital vaccine services.

Yin Jie, head of the Immunization Program Center at AliHealth, pointed out: “Vaccination services must achieve a certain coverage rate to make a greater contribution to public health. Therefore, the operation of ‘Internet + Vaccine’ platforms needs to reach a certain scale. In the field of vaccination, there is an information asymmetry between doctors and patients; many users require service guidance, which may take the form of educational content or physician consultation services. This requires ‘Internet + Vaccine’ platforms to continuously iterate their products, optimize services, and increase penetration rates based on public needs. Internet platforms have accumulated certain advantages in comprehensive operations.”

To increase the vaccination rates of non-immunization program vaccines, it is necessary to build a complete service chain that integrates content, consultation, and fulfillment channels. Vaccines are intended for the entire healthy population, which can be categorized into three groups. The first group consists of individuals with virtually no knowledge about vaccines; for example, many elderly people are unaware that they can receive free pneumococcal vaccinations during the winter. The second group has some basic knowledge but seeks more comprehensive and professional information and assistance, thus requiring consultation services. The third group comprises those who have already decided to get vaccinated and need convenient fulfillment channels. Therefore, enhancing awareness, reducing attrition during the intermediate stages, and lowering the barriers to fulfillment are key to improving the uptake of non-immunization program vaccines. This can only be achieved on the foundation of digitalization.

Internet companies hold certain advantages in building platforms that integrate content, consultation, and services. In terms of content support, enterprises such as Ali Health and Tencent Health operate their own science popularization platforms; regarding user reach, they command massive user bases; and within the service ecosystem, they can link upstream vaccine manufacturers.

Leveraging these advantages, the “Internet companies + vaccines” model promises not only to break down appointment barriers but also, more importantly, to drive further market integration by Internet enterprises.

Although numerous players have entered the vaccine appointment market, limited coverage of public vaccination sites remains a major shortcoming across all channels.

Let’s start with public vaccination sites. Why is it more difficult for public vaccination institutions to digitize their services? First, the vast scale of the public vaccination system means that digital transformation involves longer processes and takes more time compared to non-public vaccination sites. In China, there are only 300–400 non-public vaccination sites, with approximately 200 actual operating entities behind them. These entities operate with greater flexibility, incur lower communication costs, and achieve online integration more rapidly.

However, the vast number of public vaccination sites makes it challenging to standardize and migrate services to online platforms. Taking Zhejiang Province as an example, there are more than 1,700 vaccination sites excluding Ningbo City. The digital transformation of public vaccination sites requires unified planning, and their digitization process will be slower than that of non-public institutions.

How to Overcome the Challenge of Online Appointment Booking at Public Vaccination Sites: China Is Actively Exploring an Internet-Based Appointment System for Immunization Program Vaccines, with Notable Success Already Achieved in Provinces and Municipalities Such as Shanghai, Zhejiang, and Guangdong.

Private vaccination sites hold immense potential. Although few institutions currently possess vaccination qualifications, the opening of policy creates significant opportunities. The key issue lies in the absence of platform enterprises to assist and guide clinics and other relevant medical institutions in obtaining these qualifications.

As the “gatekeeper,” the CDC grants vaccine administration qualifications only to high-quality medical institutions with stable operations and standardized medical practices. In this regard, the DXY Clinic Development Alliance has been committed to connecting premium clinic institutions and assisting the clinic industry in building organizations that adhere to standardized medical practices and deliver high-quality services. By activating and connecting more private vaccination sites, vaccine appointment platforms like DXY would possess distinct advantages in this area.

Whether it is the shortage of HPV vaccines or influenza vaccines, the core contradiction reflected behind them is the supply-demand imbalance. To resolve this supply-demand imbalance, internet platforms must adopt a phased approach when implementing optimization solutions.

At this stage, we can see that the solutions of most Internet platforms are to alleviate contradictions by eliminating information asymmetry and expanding supply.

In terms of business model, existing internet platforms all adopt the vaccine e-commerce model. Although the scale of vaccine e-commerce is currently limited, it is a rapidly growing market and an important scenario in health consumption, leading many companies to enter the vaccine services sector.

Internet companies have all entered the vaccine e-commerce service sector. Among them, Ali Health offers a wide variety of vaccine appointment options, covering non-immunization program vaccines such as HPV vaccine, influenza vaccine, pneumococcal vaccine, herpes zoster vaccine, hepatitis B vaccine, and rabies vaccine. Other companies mainly cover HPV vaccine and influenza vaccine.

Alibaba Health’s vaccine service platform includes services such as the “Ma Shang Fang Xin” traceability platform, time-slot appointment tools, online consultation channels, and intelligent vaccination scheduling tools. Among these, city-level appointment services have been implemented at selected vaccination sites in Zhejiang Province, Guangzhou, Jinan, Harbin, Hefei, Haikou, and other regions, with plans for gradual expansion. For popular vaccines such as HPV, influenza, and pneumococcal vaccines, once vaccination sites enable the service, users can complete the process of “demand registration – receiving vaccination reminders – making online appointments” through the Yilu app or the Alipay Health channel.

According to Alibaba Health’s annual report, vaccine services are included in the consumer healthcare segment. This segment encompasses consumer-oriented medical services such as medical aesthetics, health check-ups, and dental care offered through its online platform and self-operated stores, as well as integrated marketing services provided to upstream platforms. In 2019, Alibaba Health’s consumer healthcare revenue reached RMB 21.4287 million, representing a year-on-year increase of 67.1%.

In June 2020, Tencent Health partnered with Gaoji Medical to launch an HPV vaccine appointment service on the “Tencent Health” WeChat mini program, enabling residents in 38 cities across China, including Beijing, Shanghai, and Guangzhou, to book appointments online for quadrivalent and nonavalent HPV vaccinations at nearby inoculation centers.

Baidu Health has also launched an HPV vaccine appointment service, with its HPV vaccine scheduling and public education initiatives serving over 150 million users.

Pinduoduo has also launched an online appointment and vaccination service for influenza vaccines. This service covers more than 30 cities across China, including Beijing, Shanghai, Guangzhou, Shenzhen, Changsha, Nanjing, and Xi’an. Users can freely choose their vaccination location and vaccine type, with group-buying prices for pediatric influenza vaccines as low as RMB 159.

In the second phase, internet platforms combined with vaccines can also play a role in integrating the vaccine industry chain and achieving precise matching of supply and demand.. Taking Alibaba Health as an example, it is leveraging its vaccine service platform to attempt digitalized supply-demand matching, thereby providing reverse feedback to production and supply.

Taking influenza vaccines as an example, due to the inherent lead time in supply chains and the specific production cycles required for these vaccines, manufacturers find it difficult to rapidly adjust output in response to fluctuating demand. Consequently, many vaccine enterprises adopt a relatively conservative approach to production planning.

For manufacturers, there is a need for a platform that can provide insights into the needs of the vaccination population. Internet platforms can achieve precise matching between supply and demand by conducting accurate research and forecasting of user needs.

Whether through online appointment scheduling or digital supply-demand matching, both stages are essentially optimizations of the existing market. In expanding the incremental market, internet platforms can connect with upstream vaccine manufacturers to cultivate market awareness for non-immunization program vaccines that currently have low market recognition, thereby establishing new entry points.

Without the catalyst of the COVID-19 pandemic, it would likely have taken much longer for the Chinese public to deepen their understanding of vaccines. The pandemic also exposed certain weaknesses in China’s vaccine industry. With COVID-19 vaccines on the verge of approval, existing service capacities are insufficient to meet the surge in vaccination demand. It is therefore urgent to establish a more comprehensive and robust system for vaccine development, production, and administration in China.