Did JW Therapeutics’ IPO Day Dip Signal a Turning Point for Immune Cell Therapy Investments in the Primary Market?

JW Therapeutics

Developer of Cellular Immunotherapy Products

On November 3, 2020, JW Therapeutics was listed on the Hong Kong Stock Exchange at an issue price of HK$23.8 per share, issuing a total of 9.77 million shares and raising over HK$2.3 billion.

Image from Tiger Brokers

JW Therapeutics opened at HK$24.35 today, but performed poorly after the opening, with its share price declining. The stock ultimately closed at HK$22 on its first day of listing, slightly below the offering price.

Following Fosun Kite and JW Therapeutics, which successively submitted their products for New Drug Application (NDA) and entered priority review, and Legend Biotech’s successful listing in the United States, JW Therapeutics has now successfully listed on the Hong Kong Stock Exchange. VCBeat has noted on multiple occasions this year that 2026 marks the rise of immunocyte therapy in China.

Leading companies are advancing their pipelines rapidly, backed by strong resources, and have now raised substantial capital through secondary market listings, virtually cementing their leading positions in this niche sector. However, behind them lie numerous startups struggling through arduous R&D efforts. Has JW Therapeutics demonstrated the potential to become a major player? And how can startups in the primary market continue to establish their foothold in this sector?

In April 2016, WuXi AppTec and Juno Therapeutics (hereinafter referred to as “JUNO”) announced a partnership to establish JW Therapeutics, aiming to combine Juno’s chimeric antigen receptor (CAR-T) and T-cell receptor (TCR) technologies with WuXi AppTec’s R&D and manufacturing platform and its extensive experience in the local Chinese market, thereby jointly building a leading cell therapy company in China.

At the time, JUNO was still one of the strongest contenders for the first CAR-T product. However, in July 2016, the Phase II clinical trial of JUNO’s lead candidate, JCAR015, resulted in the deaths of two leukemia patients due to neurotoxicity, leading the FDA to halt the trial. Although JUNO subsequently presented its latest clinical trial progress at various academic conferences, it did not file for product approval.

Kite Pharma (hereinafter referred to as “KITE”), which initially kept pace with JUNO, ultimately overtook it; its CAR-T product successfully received approval from the U.S. Food and Drug Administration (FDA) in late 2017, becoming the second CAR-T therapy to be marketed globally.

Gilead, with its forward-looking strategy, acquired KITE for $11.9 billion before KITE’s products received regulatory approval. Meanwhile, in early 2018, Celgene spent $8 billion to acquire JUNO Therapeutics. Subsequently, in 2019, Bristol Myers Squibb (BMS) acquired Celgene for the hefty sum of $74 billion, making JUNO a wholly-owned subsidiary of BMS. The competition between JUNO and KITE has thus evolved into a strategic rivalry between two pharmaceutical giants, Gilead and BMS.

Following its acquisition by Gilead, KITE has experienced increasingly rapid growth, with its first product successively entering the European and Japanese markets, and its second product already approved for marketing by the U.S. FDA. In contrast, JUNO’s performance has been somewhat less impressive.

Interestingly, the strategic choices made by KITE and JUNO in the Chinese market appear to extend their fierce competition from the international arena. Both companies established joint ventures in China—Fosun Kite and JW Therapeutics, respectively—to introduce their products into the Chinese market through licensing agreements. Both products received Investigational New Drug (IND) approval in 2018 and submitted New Drug Applications (NDA) in 2020. Currently, both are under priority review. Although JUNO has fallen significantly behind KITE in the global market, it may yet regain some ground through the performance of JW Therapeutics in the domestic market.

“An immune cell therapy company established as a joint venture between JUNO and WuXi AppTec”—with this label alone, JW Therapeutics was sufficient to attract the world’s top-tier investment institutions.

In its early development stage, backed by two industry giants, JUNO Therapeutics and WuXi AppTec, JW Therapeutics did not have a strong demand for capital; it only initiated its Series A financing round in 2018 when it filed its Investigational New Drug (IND) application.

As soon as the news broke, major investment institutions flocked in. In this round of financing, WuXi AppTec and JUNO Therapeutics continued to inject capital, while Sequoia Capital China Fund, Temasek, Yuanming Capital, and Yuanhe Origin also joined strongly. The total amount raised reached $90 million, ranking second among cell therapy company financings that year, only behind Shanghai Cell Therapy Group’s Series C funding.

Subsequently, JW Therapeutics did not rush to continue raising capital in the primary market. It was not until June 2020 that the company launched its $100 million Series B financing round. Existing shareholders, including JUNO Therapeutics, WuXi AppTec, Temasek, and Sequoia Capital China, continued to increase their investments, while a new cohort of institutional investors, such as ARCH Venture Partners, Loyal Valley Capital, and Mirae Asset, were introduced. Although this round was positioned as Series B, its timing made it akin to a Pre-IPO financing.

Recently announced cornerstone investors for the public offering include more prominent institutions demonstrating their interest in the company. Rock Springs Capital, Hillhouse Capital, Taiping Asset Management, and others have participated. Excluding any over-allotment option, ten cornerstone investors collectively subscribed for 59.5% of the total shares offered, subject to a six-month lock-up period.

With such a cohort of investors endorsing JW Therapeutics, the company is poised to continue wielding significant influence in the secondary market.

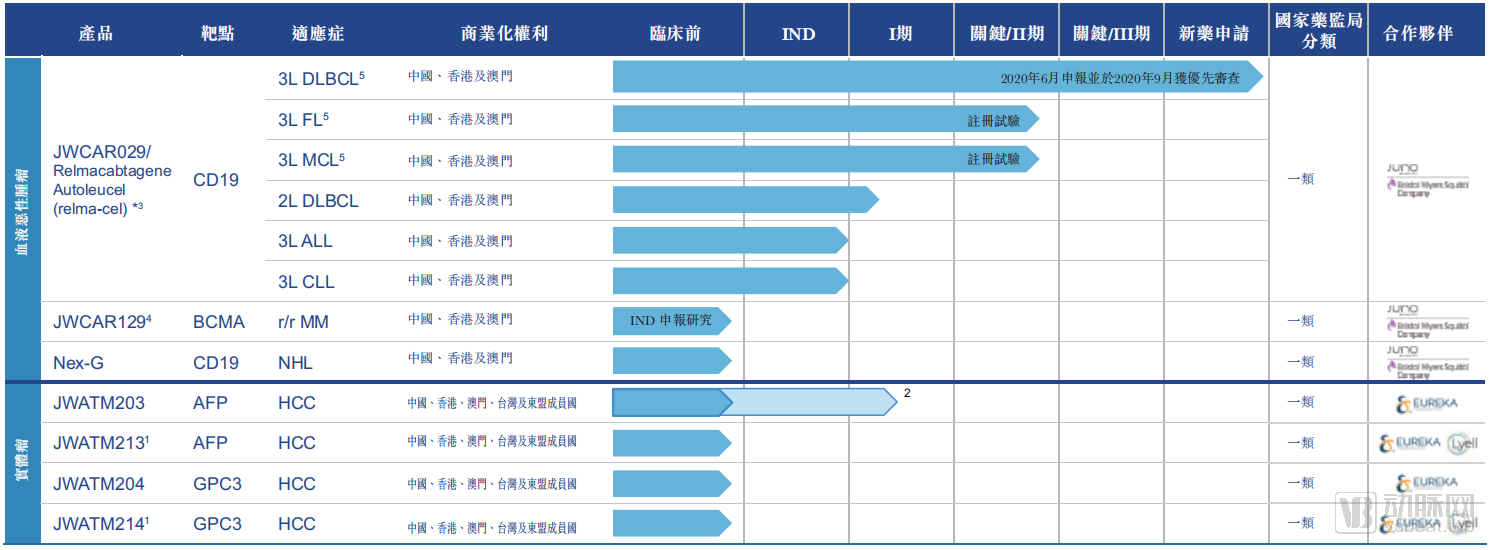

JW Therapeutics' Pipeline List

JW Therapeutics’ current pipeline consists entirely of licensed-in assets, which can be categorized into two main segments based on indications: hematologic malignancies and solid tumors. The hematologic oncology products are sourced from JUNO Therapeutics, targeting CD19 and BCMA, respectively. The solid tumor products are derived from the startup Eureka Therapeutics, targeting AFP and GPC3, respectively.

Relma-cel (JWCAR029), the company’s flagship product, is a CD19-targeted CAR-T therapy known as JCAR017 in JUNO Therapeutics’ pipeline. Although JUNO completed a relatively comprehensive development program for this product abroad, it never received regulatory approval for marketing outside China. JW Therapeutics has carried out corresponding localization adaptations and advanced multiple clinical trials of the product in China.

Currently, this product has filed for a New Drug Application (NDA) in China and has successfully entered the priority review process. The indication sought for marketing approval is third-line treatment of diffuse large B-cell lymphoma (DLBCL). In the completed Phase I and II clinical trials, Relma-cel successfully met the predefined primary endpoints, with an overall response rate (ORR) of 58.6% at three months. In terms of best overall response, the ORR and complete response (CR) rates reached 75.9% and 48.3%, respectively.

Relma-cel’s two additional indications, follicular lymphoma and mantle cell lymphoma, have also entered Phase II clinical trials. Although no domestic data have been released yet, the clinical results from JUNO’s earlier overseas trials suggest that its clinical value is comparable to that of the two already marketed CAR-T products.

The remaining pipeline assets are mostly in the preclinical or IND-enabling stages, still relatively far from market launch. Additionally, JW Therapeutics continues to closely monitor advancements in other cell therapy products. In January 2020, the company entered into an exclusive priority rights agreement with Acepodia, potentially bringing two of Acepodia’s pipeline candidates into its portfolio.

To date, JW Therapeutics has not invested a significant amount of capital compared to other innovative drug R&D enterprises.

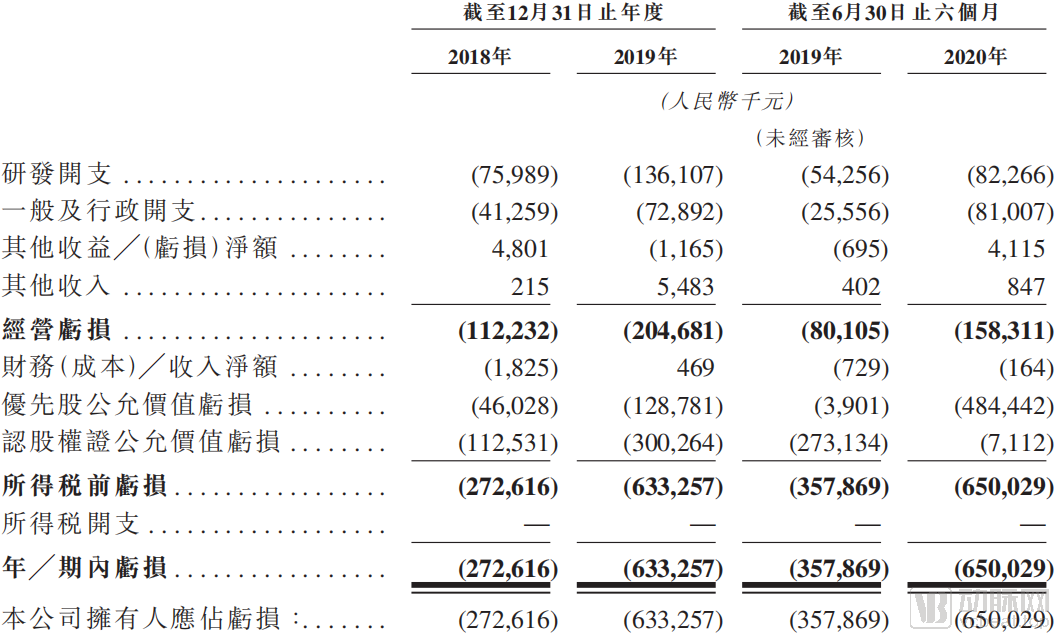

Selected Financial Data of JW Therapeutics

In 2018 and 2019, JW Therapeutics reported operating losses of only RMB 112 million and RMB 205 million, respectively, with the cash burn over these two years remaining below the amount raised in its Series A financing round in 2018. Although the operating loss appeared to surge in the first half of 2020, it actually included more than RMB 57 million in share-based compensation expenses. Excluding this component, the operating loss for the first half of 2020 showed little actual change compared to 2019.

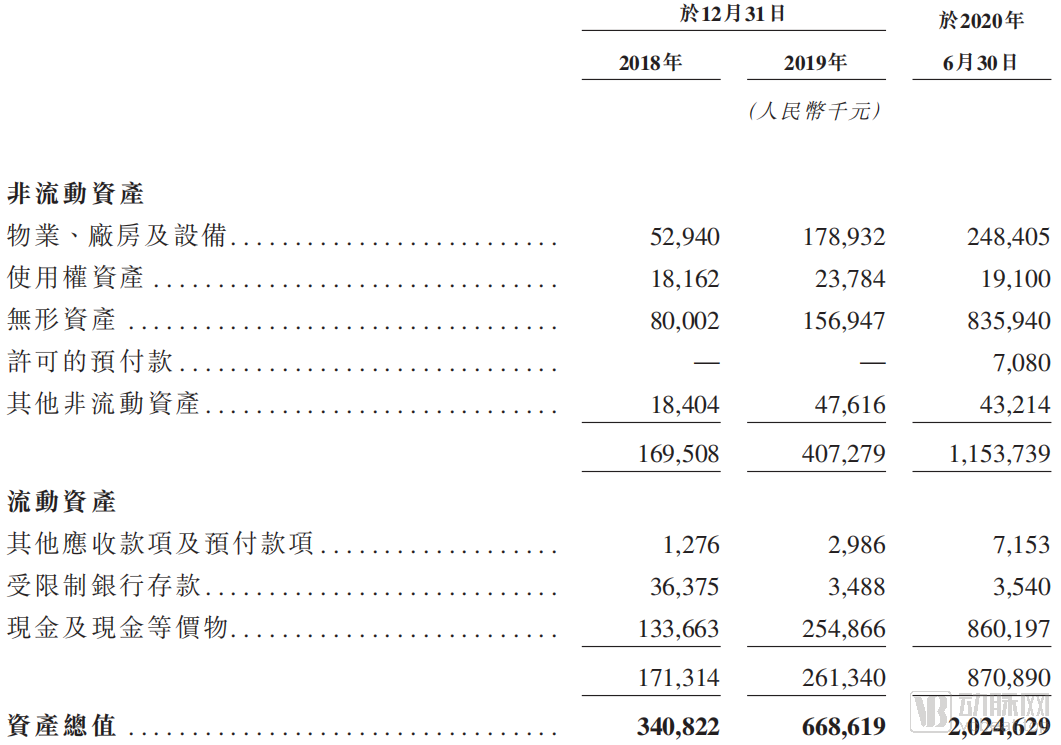

Selected Financial Data of JW Therapeutics

In terms of assets, JW Therapeutics appears to be in a more comfortable position. After completing its Series B financing round, JW Therapeutics’ current assets reached RMB 870 million. Furthermore, this IPO is expected to raise approximately RMB 2 billion for the company. Therefore, funding issues are unlikely to pose any obstacle to JW Therapeutics’ future development.

On the other hand, JW Therapeutics’ intangible assets exceeded RMB 800 million in the first half of 2020, primarily due to its acquisition of Syracuse Biopharma for $105 million. Syracuse Biopharma was established in 2017 by Eureka Therapeutics (JW Therapeutics’ partner in the solid tumor pipeline) and is dedicated to developing and commercializing clinical projects based on Eureka’s proprietary antibody screening technology platform in China and ASEAN countries. Following the completion of this acquisition, JW Therapeutics obtained the license from Eureka Therapeutics for its proprietary ARTEMIS antibody TCR technology targeting solid tumors in China and Southeast Asian countries.

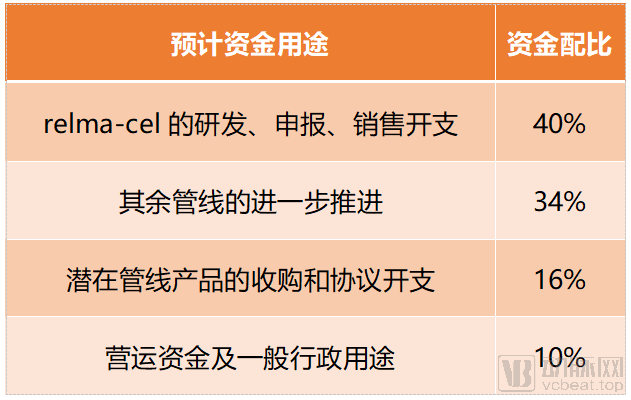

JW Therapeutics' Estimated Use of Proceeds from Financing

Based on JW Therapeutics’ current pipeline layout, its first product, Relma-cel, is expected to receive approval shortly, followed by rapid advancement of the remaining two indications under investigation. As JW Therapeutics’ other pipeline assets, aside from Relma-cel, are still in earlier stages of development, it is unlikely that a second product will reach the market within the next few years after the launch of its inaugural therapy.

Therefore, JW Therapeutics’ profitability in the coming years will rely primarily on revenue generated by Relma-cel, with its major capital investments also centered around this product. The remaining pipeline candidates will be advanced sequentially, gradually enriching JW Therapeutics’ product portfolio.

Many investors, drawing parallels from the market performances of two domestic immune cell therapy companies—Yongtai Biopharma and Legend Biotech—that listed on secondary markets in 2020, anticipated that JW Therapeutics would also experience a high opening followed by a decline. However, JW Therapeutics’ shares fell below the IPO price on its first day of trading, dropping before ever having the chance to “open high,” which seemed to confirm the secondary market’s lukewarm reception toward the immune cell therapy sector. But is this really the case?

Legend Biotech (left, in USD) and Yatai Bio (right, in HKD): Post-IPO Price Trends

Legend Biotech and Yatai Bio both exemplify the typical pattern of opening high and closing low. On their first day of listing, Legend Biotech’s stock surged by over 60%, while Yatai Bio’s rose by more than 40%. However, in the following months, both companies experienced sustained declines in their share prices. To date, Legend Biotech’s stock price remains above its initial public offering (IPO) price, whereas Yatai Bio’s has fallen below its IPO price.

From this perspective, the secondary market appears skeptical of immune cell therapy, and JW Therapeutics seems unable to escape the fate of “peaking at IPO.” However, a closer examination of Legend Biotech and Yatai Bio reveals that the situation is not so straightforward.

Legend Biotech’s weak performance after a strong opening was largely influenced by its controlling parent company, GenScript. On the evening of September 21, 2020, GenScript announced that on September 17, 2020, Chinese customs anti-smuggling authorities had inspected its corporate offices in Nanjing and Zhenjiang, China. GenScript stated that “the inspection pertained to alleged violations of Chinese laws and regulations governing imports and exports,” while industry observers speculated that the matter was related to the ongoing nationwide special inspection of human genetic resources.

This news directly impacted the stock prices of GenScript and Legend Biotech. Although GenScript’s executives increased their shareholdings at the earliest opportunity to boost market confidence, GenScript’s stock continued its downward trajectory. As a controlling subsidiary of GenScript, Legend Biotech was naturally affected by this spillover effect, with its stock price moving in tandem with that of GenScript. Therefore, the decline in Legend Biotech’s stock price was primarily driven by external factors rather than issues with its core business operations.

Yongtai Biopharma’s situation is relatively unique, as its CAR-T pipeline remains in the preclinical stage. In terms of clinical trials, only its core product, EAL, is currently under development. This product primarily involves isolating, culturing, and reinfusing patients’ CD8+ T cells. Its technological approach and indicated indications differ from those of CAR-T products, and it does not essentially belong to what is commonly referred to as the immune cell therapy industry. Therefore, it is not suitable for direct comparison with JW Therapeutics.

Therefore, the pattern of opening high and closing low observed in Legend Biotech and Yongtai Biologics does not reflect the secondary market’s sentiment toward the immune cell therapy industry. Whether JW Therapeutics can stage a turnaround hinges primarily on whether its products can successfully obtain regulatory approval for market launch.

Crowded Tracks, Saturated Pipelines

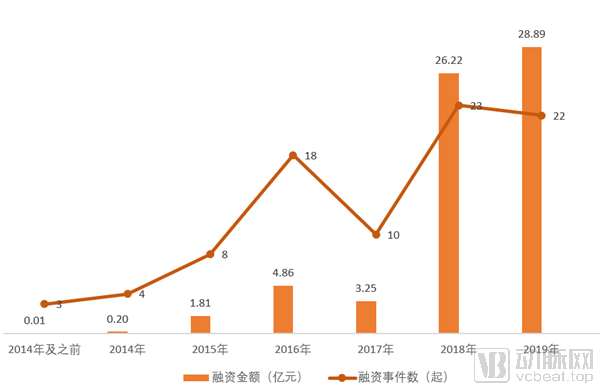

Annual Investment and Financing Statistics for Immune Cell Therapy Source: Artery Orange Database

According to statistics from VCBeat on the immune cell therapy industry, the domestic sector entered a phase of rapid development after two CAR-T products were approved for market launch abroad in 2017. For the pharmaceutical industry, regulatory approval for market launch signifies the validation of a business model. Consequently, following the trajectory of these two launched products, investors in the primary market widely regarded the immune cell therapy sector as having immense growth potential. In 2018 and 2019, the number of financing events exceeded 20 for two consecutive years, with average funding amounts surpassing RMB 100 million each year—a significant increase compared to 2017. This surge also gave rise to star enterprises such as JW Therapeutics.

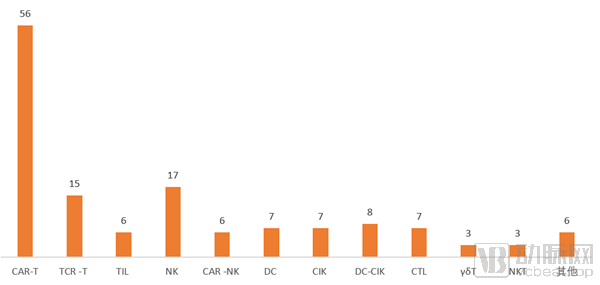

Number of Companies in the Immune Cell Therapy Subsector (by Cell Type)

Attracted by capital, this already niche industry has entered its most crowded phase. A large number of companies have flocked to the immune cell therapy sector, riding the wave of market enthusiasm. In particular, in the CAR-T arena, nearly every company has established at least one CAR-T product pipeline to bolster investor confidence. As a result, we now see as many as 56 companies competing in this therapeutic area with inherently limited indications, strongly reminiscent of the PD-1 landscape in 2019.

In a statistical analysis conducted in May 2019, there were already 19 PD-1 pipelines developed by Chinese companies that had reached the clinical trial stage, along with a large number of product pipelines still in the preclinical research phase. Following the successive approvals and market launches of four domestically produced products, competition in the domestic PD-1 market has become increasingly fierce. With six PD-1 monoclonal antibodies joining forces with two PD-L1 monoclonal antibodies approved in 2020, intense competition was inevitable. In this context, Hengrui Medicine, leveraging its extensive market foundation, took the initiative by announcing a major fourth-quarter promotional campaign offering an annual medication cost of RMB 39,600, thereby kicking off the price war for PD-1 monoclonal antibodies.

If the PD-1 market, touted as a hundred-billion-yuan opportunity, is facing such challenges, how large could the CAR-T market possibly be? Let us estimate this based on data from JW Therapeutics’ prospectus. According to Frost & Sullivan, the target patient populations for relma-cel’s three indications—third-line diffuse large B-cell lymphoma (DLBCL), third-line follicular lymphoma (FL), and third-line mantle cell lymphoma (MCL)—are estimated at approximately 28,700, 5,200, and 3,400 patients, respectively, totaling 37,300 patients. Assuming a product price of RMB 500,000 and a 10% penetration rate, the market size for relma-cel is projected to reach RMB 1.865 billion. While this market size might accommodate one or two companies, it would be extremely difficult to sustain six or seven, let alone more than ten, competitors.

Consequently, the CAR-T field today faces a predicament nearly identical to that of PD-1 monoclonal antibodies in their early days. A large number of companies have flooded into this sector, with products targeting similar antigens and indications. JW Therapeutics, whose product has already entered the New Drug Application (NDA) stage, has virtually secured its position among the first batch of market entrants. As leading products approach commercial launch, the pressure on trailing companies will intensify. First-to-market products will rapidly capture market share; for latecomers offering minimally differentiated products, securing greater support from physicians and patients may leave them with few options beyond aggressive promotional efforts and price reductions. Given the inherently high costs and substantial R&D investments associated with immune cell therapies, engaging in price-cutting promotions will likely condemn these companies to a slow decline characterized by razor-thin profit margins—a scenario akin to “boiling a frog in lukewarm water.”

Fortunately, immune cell therapy differs significantly from PD-1 monoclonal antibodies. In the development of monoclonal antibody or small-molecule drugs, a mid-course strategic pivot would necessitate restarting all work from scratch. In contrast, for immune cell therapies, many completed research findings can be leveraged in the development of new pipelines when shifting direction, such as techniques for cell purification, culture, and preparation, as well as genetic editing processes for immune cells. Therefore, for companies whose CAR-T pipelines are still in the early stages, a timely strategic shift may represent a favorable option.

Differentiated Competition or Cost Reduction

Immune Cell Therapy Industry Landscape

If a shift in strategic direction is desired, there are essentially two options: pursue differentiated competition against leading products by selecting novel targets and indications, or further reduce product costs. These two approaches have given rise to two major new scenarios in the immune cell therapy industry: solid tumor CAR-T and universal (off-the-shelf) CAR-T. However, both directions face similar challenges:

1. No successful examples.Although numerous companies worldwide are developing related products, and successful patient treatment cases have been frequently disclosed, no product has yet completed large-scale clinical trials or initiated a New Drug Application (NDA) filing. Consequently, every company engaged in such research is essentially groping in the dark with a candle, seeking opportunities within this vast market.

2. The effective mechanism is unclear.For CAR-T therapies targeting solid tumors, the most critical factor is target selection; for universal CAR-T therapies, it is determining which genes to knock out to address immune rejection. Basic research on these targets remains insufficiently in-depth. Therefore, although there are currently some typical high-profile targets, such as GPC3 in hepatocellular carcinoma or Claudin18.2 in gastrointestinal tumors, more robust evidence is still lacking to support their use.

3. How to Circumvent Technical Barriers.A significant number of patents related to CAR-T cell therapy are held by leading companies such as Novartis, KITE, and JUNO. How startups can navigate around these companies’ patents is also a topic worthy of discussion.

4. In addition to selecting the right direction, it is also essential to offer something distinctive.As previously mentioned, dozens of companies are currently developing CAR-T therapies. Many have long anticipated the industry’s overcrowding and are simultaneously advancing solid tumor CAR-T or universal (off-the-shelf) CAR-T approaches. For instance, JW Therapeutics has already established a presence in the solid tumor CAR-T space. Under these circumstances, these two adjusted sectors may also rapidly become saturated. Whether for the sake of future corporate growth or to craft a more compelling narrative for investors, companies should carefully reassess their core strengths and resources, adopt a more focused strategic direction, and further differentiate themselves from competitors.

JW Therapeutics is not the first immuno-cell therapy company to go public, and it certainly will not be the last. As a representative enterprise in the first tier, JW Therapeutics’ listing on the Hong Kong Stock Exchange signifies that this sector has truly reached a stage where new giants are emerging, while also serving as a wake-up call for other companies to carefully seize the right timing for their own development.

Efficient pipeline advancement, strictly controlled R&D expenditures, ample cash reserves, and decisive action in acquisitions—JW Therapeutics has already taken on the shape of a pharmaceutical giant. We look forward to the next update from JW Therapeutics being good news that relma-cel has entered the market, bringing benefits to patients.