National Healthcare Security Administration Releases Detailed Guidelines for Internet Medical Services to Be Included in Health Insurance Reimbursement

Yesterday, the National Healthcare Security Administration released the “Guiding Opinions on Actively Promoting Medical Insurance Payment for ‘Internet+’ Medical Services” (hereinafter referred to as the “Opinions”). As the document outlines specific measures concerning medical insurance agreement applications, reimbursement coverage, and settlement recipients, among other areas, it is more comprehensive and detailed than previous guiding opinions. Consequently, many industry insiders have circulated it with the label “major policy announcement.”

So, what are the specific advancements in this new policy? How can internet hospitals be included in medical insurance payment schemes? How does “Internet+” medical insurance reimbursement work? How will medical insurance funds be regulated? What industry opportunities does the new policy create? VCBeat has promptly summarized the key policy points and interviewed relevant executives from digital health companies to explore answers to these critical questions.

Incorporating internet-based healthcare services into medical insurance payment is not an entirely new policy. Since August 2019, the National Healthcare Security Administration has issued relevant documents on three occasions. In July 2020, the General Office of the State Council released the Implementation Opinions on Further Optimizing the Business Environment to Better Serve Market Entities. In October, fourteen departments, including the National Development and Reform Commission and the Ministry of Industry and Information Technology, jointly issued the Work Plan for Expanding Domestic Demand and Promoting Consumption in the Near Term. Both documents proposed including eligible internet-based follow-up consultation services within the scope of medical insurance reimbursement.

Judging from the main content of the document, the “launch” of medical insurance coverage is accelerating from framework planning to practical implementation.

National Healthcare Security Administration’s Relevant Documents on Payment for Internet-Based Medical Services. Source: Official Website of the National Healthcare Security Administration; Graphic by VCBeat

On August 30, 2019, the National Healthcare Security Administration issued the “Guiding Opinions on Improving Pricing and Medical Insurance Reimbursement Policies for ‘Internet+’ Medical Services,” establishing principles for price item management and price formation mechanisms for “Internet+” medical services. As the document primarily outlines broad principles without specifying detailed implementation rules or timelines, it had limited impact on advancing the practical implementation of medical insurance reimbursement for internet-based healthcare services.

Following the outbreak of the pandemic in 2020, internet-based healthcare played a pivotal role in epidemic prevention and control. To encourage “contactless” medication purchasing services, medical insurance coverage was urgently extended to provide reimbursement for online follow-up consultations and prescription purchases. During this period, the National Healthcare Security Administration (NHSA) and the National Health Commission (NHC) jointly issued the *Guiding Opinions on Promoting “Internet+” Medical Insurance Services During the Prevention and Control of the COVID-19 Pandemic*, which specified the implementation details for delivering “Internet+” medical insurance services during the outbreak. This initiative prompted cities such as Beijing, Shanghai, and Tianjin to rapidly incorporate internet-based diagnosis and treatment services into their medical insurance schemes, with some hospitals even enabling direct online settlement.

The new policy introduced yesterday builds upon previous measures by establishing more detailed provisions regarding designated medical insurance providers, settlement procedures, and fund supervision. For instance, it clarifies the scope of agreement-based management and the application criteria for “Internet+” medical services, thereby addressing how such services can be included in medical insurance reimbursement. It also specifies the coverage and eligible parties for insurance payments, resolving the issue of how reimbursements are to be processed. Furthermore, by strengthening regulatory measures for “Internet+” medical services, the policy sets forth specific requirements for the supervision of medical insurance funds.

“The new policy is highly comprehensive, covering the key components of medical insurance agreement management, including clinical practices, follow-up consultations and medication purchases, as well as extended prescriptions,” said Ma Guanglei, Deputy Secretary-General of the China Pharmaceutical Commerce Association and General Manager of Yi Fuzhen. This signifies that the inclusion of internet-based healthcare services in medical insurance reimbursement has moved into the stage of practical implementation.

To date, internet hospitals have been categorized into three types based on the sponsoring entity: internet hospitals led by physical hospitals, internet hospitals jointly established by physical hospitals and enterprises, and internet hospitals established by enterprises relying on physical medical institutions.

Since the onset of the pandemic, internet hospitals primarily operated by physical hospitals have rapidly integrated medical insurance payment systems, whereas only a few enterprise-led internet hospitals have achieved such connectivity. So, under the new policy, which internet hospitals are eligible to apply for medical insurance coverage?

The “Opinions” stipulate that, within the regulatory framework established by provincial-level or higher health commissions and traditional Chinese medicine administrations, medical institutions providing “Internet+” healthcare services may, through their affiliated brick-and-mortar medical institutions, voluntarily apply to the local healthcare security administration in their pooling area to sign a supplementary agreement for the inclusion of “Internet+” healthcare services under the basic medical insurance scheme. These constitute the basic qualification requirements for medical institutions.

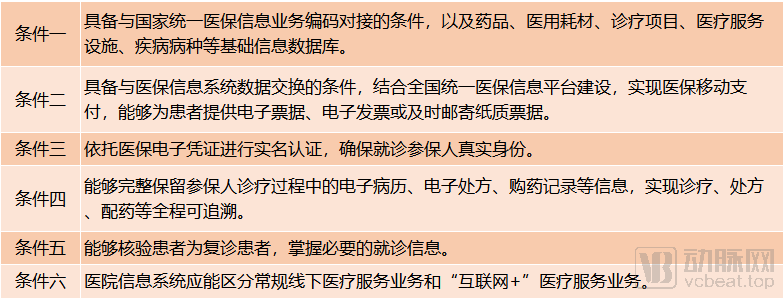

The "Opinions" also stipulate six basic conditions for applying for designated medical insurance provider status:

Six Basic Conditions for Applying for Medical Insurance Agreement, Source: National Healthcare Security Administration, Graphic by VCBeat

These six conditions focus on clarifying the standards for system construction, primarily to ensure the authenticity of patients and the medical consultation process, facilitate the exchange of medical and health insurance information, and enable effective supervision of health insurance funds.

The “Measures for the Administration of Internet Hospitals (Trial)” explicitly stipulates that internet hospitals established by enterprises must rely on physical medical institutions, while the other two types already have physical medical institutions. In other words, regardless of the type, every internet hospital has an associated offline physical entity, thereby meeting the condition in the “Opinions” that allows application for medical insurance agreements “through the physical medical institution on which it relies.”

“Theoretically, medical institutions are not distinguished by whether they are enterprise-led or non-enterprise-led,” Ma Guanglei believes. As long as the business scope of a medical institution includes internet medical services, it is eligible to apply.

It is reported that some internet healthcare companies have explored medical insurance payment in the past few years, such as WeDoctor's Wuzhen Internet Hospital and Sichuan WeDoctor Internet Hospital.

During the pandemic, WeDoctor launched electronic medical insurance certificates in Wuhan, Hubei Province, and facilitated the inclusion of online follow-up consultations and medication purchases for patients with severe chronic diseases under medical insurance coverage. In Huanggang, Hubei Province, WeDoctor entered into a strategic cooperation agreement with the local Medical Insurance Service Center. On February 27, the Huanggang Municipal Medical Insurance Bureau designated Huanggang WeDoctor Internet Hospital as a contracted medical institution under the municipal medical insurance scheme. In Tai’an, Shandong Province, after implementing chronic disease management services and achieving notable results, WeDoctor saw the Tai’an Municipal Medical Insurance Bureau sign an agreement on June 9 to designate WeDoctor Taishan Internet Hospital as a contracted provider, thereby exploring “Internet+” medical insurance services.

“In the model of co-building and operating internet hospitals in partnership with physical medical institutions, Weimai serves as an example. The vast majority of its partner physical medical institutions are designated providers under China’s basic medical insurance scheme. Under the new policy, internet hospitals that meet the specified criteria are eligible to apply for supplementary agreements to include their services in medical insurance coverage,” said Zheng Haihua, General Manager of Weimai’s Internet Hospital Center. He added that applications can be submitted once system-level integration is completed and six basic conditions are satisfied.

Thus, it can be seen that among the internet hospitals currently enabled for medical insurance reimbursement, although those led by brick-and-mortar hospitals—particularly public hospitals—dominate, the new policy does not impose restrictions on the entities applying for or operating internet hospitals. Therefore, for digital healthcare companies, there are greater possibilities for integration with medical insurance payment systems.

Follow-up consultations for common and chronic diseases constitute the foundational services of internet healthcare. Currently, many internet hospitals center their operations on these services, expanding pre- and post-consultation offerings, integrating pharmaceutical and insurance resources, bridging online and offline care, and launching services such as chronic disease management.

The "Opinions" state that the scope of medical insurance reimbursement includes consultation fees and medication costs incurred from online follow-up visits and prescription issuance. Among these, follow-up visit services are charged and reimbursed according to the pricing standards for general outpatient consultation items at public hospitals, while medication costs are reimbursed in accordance with the payment standards and policies applicable to offline medical insurance. Fees for drug delivery services are not covered by medical insurance.

It is worth noting that, on the basis of clarifying which items are reimbursable and which are not, the "Opinions" also propose prioritizing coverage for follow-up visits and prescription renewals for outpatient chronic and special diseases. Localities may start with outpatient chronic and special diseases and gradually expand the scope of medical insurance payment for "Internet+" medical services for common and chronic diseases.

A representative from WeDoctor stated that the “Opinions” reflect the National Healthcare Security Administration’s strong recognition and enhanced support for internet-based medical services. Given the convenience of “Internet Plus Healthcare,” internet hospitals clearly hold significant advantages in managing chronic diseases and providing follow-up care. This will facilitate the effective division of labor between internet hospitals and physical hospitals, thereby better achieving the integration and seamless coordination of online and offline medical services.

Given the internet’s ability to transcend geographical barriers, there are now multiple combinations for medical consultations and medication purchases, which differ significantly from the traditional healthcare model where both diagnosis and dispensing occur within hospitals. In this regard, the Guidelines support the circulation of electronic prescriptions and explore the interconnectivity of information on out-of-hospital prescriptions from designated medical institutions with designated retail pharmacies. In regions with adequate conditions, reliance on the national unified medical insurance information platform should be leveraged to accelerate the deployment of functional modules related to out-of-hospital prescription circulation, thereby facilitating the transfer of follow-up visit prescriptions in “Internet+” medical services.

In response to the scenario where medical services and pharmaceuticals are billed separately following the circulation of prescriptions, the "Opinions" have established corresponding settlement methods: consultation fees and medication costs incurred at medical institutions (the portion covered by the basic medical insurance fund) shall be settled directly between the medical insurance handling agencies and the medical institutions; medication costs incurred at designated retail pharmacies (the portion covered by the basic medical insurance fund) shall be settled between the medical insurance handling agencies and the designated retail pharmacies.

In other words, after receiving internet-based medical services, patients only need to pay the out-of-pocket portion, regardless of whether they purchase medications within or outside the hospital. Prescription circulation has also become a hot topic in recent years; with the support of medical insurance payments, the market for prescription drugs dispensed outside hospitals is poised to achieve genuine growth.

It has been several years since individual medical institutions and enterprises began exploring the integration of internet healthcare with health insurance payment systems. The fundamental reason for the consistently cautious approach adopted by policymakers during this process is to ensure the secure supervision of health insurance funds.

All three policy documents issued by the National Healthcare Security Administration have imposed stringent requirements on fund supervision. The current "Opinions" propose that healthcare security agencies should comprehensively leverage technologies such as big data and the internet, and utilize the intelligent audit and monitoring system for healthcare security to conduct real-time supervision of information including settlement details of "Internet+" medical services, pharmaceuticals, medical consumables, medical service items, and outpatient medical records. Fraudulent activities aimed at defrauding healthcare security funds in "Internet+" medical services shall be severely cracked down upon.

“The National Healthcare Security Administration (NHSA) primarily exercises oversight over designated institutions through contractual management. If a designated institution violates regulations, the NHSA will impose financial penalties or decline to renew the contract. Therefore, the new policy repeatedly emphasizes the importance of contractual management,” said Ma Guanglei. He noted that the “Guiding Opinions” explicitly require the retention of electronic medical records, e-prescriptions, and medication purchase records generated during insured patients’ diagnosis and treatment processes, thereby enabling end-to-end traceability across diagnosis, prescription, and dispensing. This requirement will prompt the NHSA, medical institutions, prescription circulation platforms, and pharmacies to jointly sign circulation agreements. In practice, each party will fulfill its respective responsibilities, achieving collaborative supervision across three dimensions: authenticity management, rationality management, and cost-effectiveness management.

Ma Guanglei also believes that multi-party joint regulation first requires achieving interconnectivity and real-time sharing of information. Taking the Yifuzhen third-party prescription circulation service platform as an example, it has broken down the information silos among healthcare providers, pharmaceutical companies, and medical insurance agencies, establishing a “three-medical linkage” regulatory mechanism. This ensures both patient medication safety and the secure use of medical insurance funds.

With stricter health insurance regulatory measures in place, previously prevalent industry practices such as the approval of fraudulent prescriptions and the issuance of medications before prescription documentation can be further controlled. This will help standardize internet-based medical services, which is a fundamental condition for promoting the industry’s sustainable development.

It takes time for policies to move from top-level design to implementation, and local healthcare security administrations need to formulate and implement detailed rules based on local medical standards and the status of healthcare security funds. Previously, provinces such as Shandong, Beijing, and Sichuan had already included certain internet-based medical services in healthcare security coverage, but these were primarily focused on fees for online follow-up consultations and remote medical services. Traditional medical care involves a complete process encompassing both diagnosis/treatment and medication. Clearly, the current "Opinions" better align with this typical healthcare scenario.

Wang Shirui, Founder and CEO of Medlinker, stated that the "Guidelines" clearly specify requirements for institutions providing “Internet+” medical services eligible for health insurance reimbursement, including institutional qualifications, sources of health insurance quotas, the scope of internet-based consultations and medication costs, and reimbursement ratios. This will further accelerate the rollout of local online health insurance payment policies, improve the efficiency of health insurance fund utilization, and enable the public to access more convenient, affordable, and effective medical services.

The implementation of medical insurance reimbursement for internet-based healthcare across various regions will also drive a series of positive developments within the industry.

The most direct approach is informatization services. Zheng Haihua, General Manager of Weimai’s Internet Hospital Center, believes that deploying internet hospital platforms for physical hospitals by building SaaS cloud services for internet hospitals is part of the service offerings of digital healthcare enterprises. Influenced by new policies, a large number of medical institutions in China will intensify their efforts to build internet hospitals, while also promoting the integration of regional electronic medical insurance accounts, which presents new opportunities for these enterprises.

Services such as chronic disease management and health management, which have evolved from online follow-up consultations via the internet, have gained new growth momentum. Zheng Haihua noted that public hospitals are constrained by institutional and systemic factors and suffer from a shortage of operational talent. Internet healthcare companies can help bridge this operational gap by providing patients with comprehensive online whole-course health management services covering pre-hospital, in-hospital, and post-hospital stages. Once medical and pharmaceutical expenses become reimbursable, patients will be more motivated to choose online services. Internet healthcare enterprises can effectively integrate online and offline patient flows, thereby achieving a closed-loop service model for the entire course of treatment.

In summary, the journey of integrating internet healthcare into medical insurance payment systems has evolved from eager anticipation in previous years, to initial progress a year ago, and now to rapid breakthroughs. While the path has been tortuous, the future is undoubtedly bright.