Hyaluronic Acid: The 'Moutai of Aesthetic Medicine,' a Billion-Dollar Beauty Business

As the 2020 “Double 11” shopping festival had just begun, stockpiling medical aesthetic products became a necessity. The pursuit of physical appearance by millions has driven higher penetration rates in the medical aesthetics industry, supporting the multi-billion-yuan market capitalizations of listed hyaluronic acid companies. This has also turned hyaluronic acid—a product with a raw material cost of no more than RMB 30 per unit—into a wealth-creation myth in the capital markets. Two female billionaires have emerged from the medical aesthetic hyaluronic acid industry: Zhao Yan, Chairwoman of Bloomage Biotechnology, and Jian Jun, Chairwoman of Imeik.

Haohai Biological Technology, Bloomage Biotechnology, and Imeik have successively gone public over the past two years, keeping hyaluronic acid-related stocks in the market spotlight and driving their valuations to new highs.

Since its listing two months ago, Imeik’s stock price has climbed steadily. At the midday close on November 3, it stood at RMB 551.90 per share, representing a 366.64% surge from its issue price of RMB 118.27 per share. Its market capitalization has exceeded RMB 65 billion, while Bloomage Biotech’s market cap has surpassed RMB 70 billion. The combined market value of the two companies now exceeds RMB 100 billion.

Currently, in the medical field, it is difficult to find another niche sector as prosperous in the capital market as hyaluronic acid. With gross profit margins for medical aesthetic hyaluronic acid injection products reaching as high as 90%, hyaluronic acid has been dubbed the “Moutai” of the medical aesthetics industry.

VCBeat (WeChat ID: vcbeat) compiled statistics on the registration certificates for hyaluronic acid products in China, revealing that a total of 26 companies have obtained such certifications. In the hyaluronic acid industry, which is characterized by high technical and regulatory barriers, Bloomage Biotechnology and Imeik are neither the first domestic companies to obtain certification nor the ones with the largest number of certified products. How, then, have they become favorites in the capital market and emerged as leaders in the hyaluronic acid sector? VCBeat has conducted a comprehensive review of this industry.

For most people who are not concerned with medical aesthetics, the term "hyaluronic acid" may still be somewhat unfamiliar. However, hyaluronic acid, also known as hyaluronan, is naturally present in everyone's body. Hyaluronic acid is inherently found within the skin, where it helps draw moisture from both the body's interior and the skin's surface, while also enhancing the skin's long-term water-retention capacity. Although the human body contains only about 15 grams of hyaluronic acid, life would not be possible without it. Hyaluronic acid is a high-molecular-weight polysaccharide that is transparent and viscous in texture, and it is currently recognized as the most effective humectant discovered in nature.

Based on differences in application fields and technical requirements, sodium hyaluronate raw materials are classified into pharmaceutical grade (including ophthalmic solution grade and injectable grade), cosmetic grade, and food grade.

In the mid-1990s, products primarily based on sodium hyaluronate began to enter fields such as orthopedics, ophthalmology, and plastic surgery worldwide. Hyaluronic acid, characterized by its non-immunogenicity and biodegradability/absorbability, has been widely used in the aesthetic medicine sector.

Currently, the hyaluronic acid industry is in its spotlight. Bloomage Biotech, Imeik, and Haohai Biological Technology all listed on the capital market between 2019 and 2020, with strong performances.

Hyaluronic acid has become a trending sector. Although the hyaluronic acid industry appears to have surged in popularity overnight, it has actually been preparing for this moment for over 30 years.

As early as 2003, China was already capable of producing medical-grade sodium hyaluronate gel. At that time, hyaluronic acid was still referred to as hyaluronic acid (HA) and had little association with medical aesthetics or plastic surgery. Medical-grade hyaluronic acid was primarily used for preventing postoperative adhesions, as a viscoelastic agent in ophthalmic surgeries, and as an intra-articular injection in orthopedics. In the Hong Kong and Taiwan regions of China, hyaluronic acid was known as “bolusuan” (hyaluronic acid), and its use as an injectable cosmetic filler began to emerge.

With the rise of domestic medical aesthetics consumption, the hyaluronic acid industry for medical aesthetics has begun to develop. There was a period when Chinese brands were virtually absent from the market for hyaluronic acid used in medical aesthetics. Today, three major domestic leaders have emerged: Imeik, Bloomage Biotechnology, and Haohai Biological Technology.

From Scratch to Mainstay: The Domestic Medical Aesthetic Hyaluronic Acid Industry in China Has Evolved Over 20 Years. Over the past two decades, the development of China’s hyaluronic acid industry can be divided into three stages.

The first phase, from 2003 to 2008, marked the commencement of industrialized production of hyaluronic acid in China. During this period, although China had overcome the technical barriers to large-scale manufacturing, the applications of industrially produced hyaluronic acid remained relatively limited.

Although sodium hyaluronate gel does not appear to be a product with high technical barriers today, there were very few manufacturers capable of producing it at that time. Major domestic manufacturers included Shandong Zhengda Freda Pharmaceutical and Changzhou Institute of Materia Medica, among others, which were able to produce sodium hyaluronate gel. In the National Medical Products Administration’s medical device database, the first registration certificates for sodium hyaluronate gel were issued to Shandong Zhengda Freda Pharmaceutical (Shandong Bausch & Lomb Freda Pharmaceutical) and Changzhou Institute of Materia Medica.

The key to the industrialization of hyaluronic acid lies in reducing the cost of its extraction. Previously, hyaluronic acid was extracted from rooster combs and was once referred to as "white gold." Pharmaceutical-grade, high-purity hyaluronic acid commanded a unit price of 1,000 yuan per gram. Today, hyaluronic acid companies purchase raw materials by the ton, with the raw material cost for a single syringe of hyaluronic acid amounting to only around tens of yuan.

The significant reduction in the production cost of hyaluronic acid is primarily attributed to the technology of extracting hyaluronic acid via bio-fermentation.

Dr. Guo Xueping, Chief Scientist at Bloomage Biotech, pioneered microbial fermentation technology in China, driving the large-scale application of hyaluronic acid in the pharmaceutical field. The invention of this technology significantly reduced the price of hyaluronic acid, which was once as expensive as gold, while creating widespread lucrative opportunities for the hyaluronic acid industry.

Many of China’s current leading hyaluronic acid companies also emerged during this period, including Shandong Freda Bioengineering Co., Ltd. (now acquired by Lushang Group) and the predecessor of Bloomage Biotech, Shandong Freda Biopharmaceutical Co., Ltd.

In 1998, Ling Peixue, Dean of the Shandong Institute of Biopharmaceuticals, founded Shandong Freda Bioengineering Co., Ltd. (now known as Freda Beauty), engaging in the research and development, production, and sales of hyaluronic acid-based cosmetics. Meanwhile, Ling Peixue established Shandong Freda Biochemical Co., Ltd. for raw material production (later renamed Shandong Freda Biopharmaceutical Co., Ltd.).

In 2000, Zhao Yan, Chairman of Bloomage Group, accidentally met Guo Xueping, Deputy Director of the Shandong Institute of Biopharmaceuticals, and a team of scientists. After learning that hyaluronic acid content and metabolism are directly linked to skin maturation and aging, Bloomage International Investment Group formally injected capital into Shandong Freda Biopharmaceutical Co., Ltd., formerly known as Shandong Freda Biochem Co., Ltd., which had been engaged in raw material production. In 2017, through multiple share acquisitions, Bloomage Freda became a wholly-owned subsidiary of Bloomage. In 2019, Bloomage Freda was officially renamed Bloomage Biotechnology Corporation Limited, marking the end of any equity relationship between Bloomage Biotechnology and Freda. The historical ties between Bloomage Biotechnology and the Freda group once led to a public verbal dispute between the two companies.

The hyaluronic acid companies that emerged in the first phase have now grown into leading upstream raw material suppliers for the entire hyaluronic acid industry, and China is currently the world’s largest producer and exporter of hyaluronic acid raw materials.

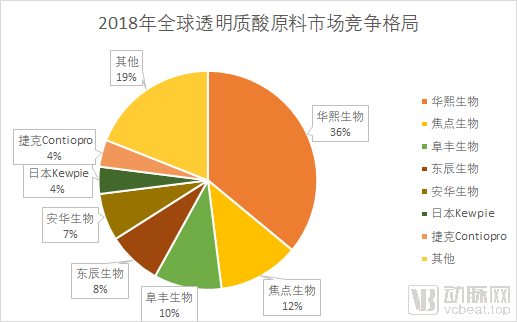

According to Frost & Sullivan, Bloomage Biotechnology holds the largest share in the global hyaluronic acid raw material market, accounting for 36% of the market. The company's hyaluronic acid production reached nearly 180 metric tons in 2018.

Focus Biotech, the world’s second-largest supplier of hyaluronic acid raw materials and a former subsidiary of Freda, currently has an annual production capacity of 120 metric tons for cosmetic-grade and food-grade hyaluronic acid, with approximately 60% exported. In February 2020, Lushang Group acquired a 60.11% equity stake in Focus Biotech for RMB 259 million. Additionally, Lushang Group had previously acquired Freda in 2018.

If 2003 was a pivotal milestone in the development of China’s hyaluronic acid industry, then 2008 marked the second major turning point. The companies that emerged during the first phase dominated the upstream market for hyaluronic acid raw materials; however, this did not mean that the market landscape was set in stone. After 2008, the medical aesthetics hyaluronic acid market began to rise, ushering in an era of diverse proliferation and vibrant growth for hyaluronic acid products.

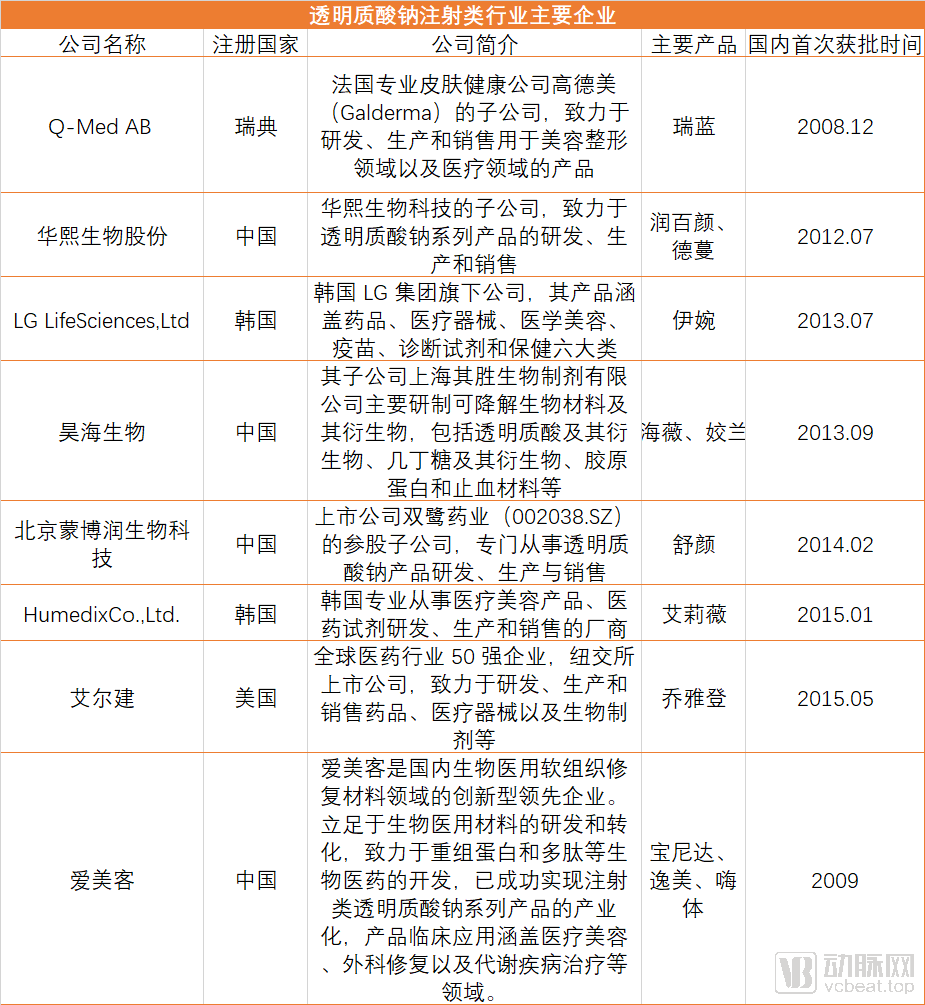

In 2008, Restylane, a hyaluronic acid injection product from the Swedish company Q-Med AB, entered the Chinese market, while the first domestic product was Yimei (2009), under Imeik.

In medical aesthetic injections, hyaluronic acid is primarily used for mid-to-deep dermal filler injections to correct moderate to severe facial wrinkles, including nasolabial folds, forehead lines, and neck lines.

Compared to the applications of sodium hyaluronate gel in ophthalmology and orthopedics, the combination of hyaluronic acid with medical aesthetics is akin to a destined encounter of gold wind and jade dew, surpassing countless mundane pairings.

As indicated by the market size, the integration of hyaluronic acid with medical aesthetics has directly expanded its market capacity to more than twice its original volume.

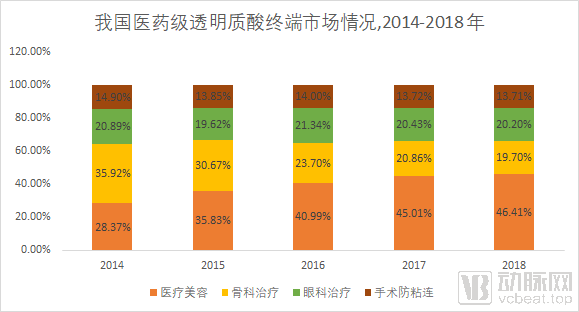

According to an analysis by Frost & Sullivan, the market size of injectable drugs for osteoarthritis in China was approximately RMB 9.8 billion in 2018, among which the market size of pharmaceutical-grade hyaluronic acid orthopedic end-use products was about RMB 1.57 billion. In 2018, the market size of pharmaceutical-grade hyaluronic acid ophthalmic end-use products in China was approximately RMB 1.61 billion. Meanwhile, in 2018, the domestic market size of hyaluronic acid for medical aesthetics reached RMB 6.399 billion. (Data source: Zhongyan Puhua Research Report)

Hyaluronic acid has shone brightly in the medical aesthetics market, not only due to the inherent properties of hyaluronic acid itself but also because injectable treatments are categorized as minimally invasive aesthetic procedures.

In medical aesthetics, procedures such as injectable fillers and laser treatments are classified as non-surgical medical aesthetic services. Compared to invasive surgical procedures that require scalpels, non-surgical options are more widely accepted by the public due to their relatively lower technical complexity, shorter recovery time, reduced risks, and lower unit costs. Consequently, medical aesthetic institutions benefit from lower promotion and customer acquisition costs. Many clinics use hyaluronic acid treatments as loss leaders to attract clients, and the convergence of these driving factors has fueled rapid growth in the hyaluronic acid market within the medical aesthetics industry.

According to data from the 2019 Health Statistics Yearbook, in 2018, the number of outpatient visits at plastic surgery hospitals and cosmetic hospitals in China were 843,500 and 6.549 million, respectively; in 2017, these figures were 717,900 and 4.6263 million, respectively. This indicates that the growth rate of non-surgical medical aesthetics far exceeds that of surgical medical aesthetics.

Faced with this vast market, domestic companies have also strategically entered the medical aesthetics hyaluronic acid market, launching hyaluronic acid injection products. In 2012, Bloomage Biotech launched Runbaiyan, a sodium hyaluronate injection. The “Runbaiyan” injectable modified sodium hyaluronate gel, developed by Bloomage Biotech, was the first domestically produced cross-linked hyaluronic acid soft tissue filler to receive approval in China. Haohai Biological Technology launched Haiwei in 2013. Imported products have also successively entered the Chinese market.

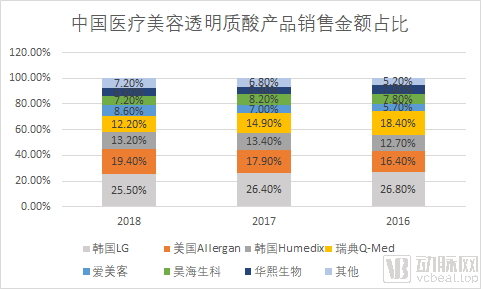

In terms of market share in the medical aesthetic hyaluronic acid sector, Allergan, Imeik, Q-Med AB, LG Life Sciences, Ltd., Bloomage Biotechnology, and Haohai Biological Technology hold the majority of the market. Among domestically produced brands, Imeik has the highest market share for medical aesthetic hyaluronic acid products.

Share of Sales Revenue of Medical Aesthetic Hyaluronic Acid Products in China, Data Source::Frost & Sullivan

During the initial phase of development for hyaluronic acid enterprises, the decisive technologies were industrialization and fermentation techniques; whereas in medical aesthetic injectable hyaluronic acid, the core technical barrier lies in how to modify the structure of hyaluronic acid.

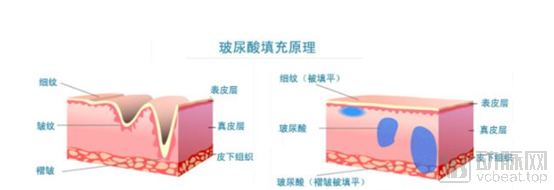

The half-life of native hyaluronic acid in tissues is only 1–2 days. For hyaluronic acid products used as dermal fillers, structural modification of hyaluronic acid is required to enhance molecular stability, thereby slowing its degradation rate in vivo and prolonging its duration of action. This modification also transforms hyaluronic acid into a gel with appropriate viscoelastic properties, providing superior support and contouring capabilities, thus achieving more ideal clinical outcomes in medical aesthetics.

Currently, structural modification of hyaluronic acid is primarily achieved through cross-linking. Cross-linking refers to a reaction in which two or more molecules are covalently bonded to form a more stable molecular network structure.

During this period, another major leader in the medical aesthetics market emerged: Imeik.

Founded in 2004, Imeik was established by its Chairman, Jian Jun, who recognized the potential of hyaluronic acid-based medical aesthetics after learning about “lunchtime beauty” hyaluronic acid injections during his long-term work abroad.

Imeik was not the first entrant in the hyaluronic acid industry; how did it break through the fierce competition between imported and domestic brands?

The answer is to take the road less traveled and innovate.

Unlike early hyaluronic acid companies, which were all R&D-driven, Imeik did not disclose its early R&D personnel and capabilities; the R&D management staff disclosed in its prospectus all joined the company after 2007.

In 2009, Imeik seized the market opportunity by launching “Yimei,” a sodium hyaluronate injection product, and subsequently introduced a range of products targeting facial and neck wrinkle correction. These include Bonita, China’s first injectable material containing PVA microspheres; Ai Fu Lai, China’s first injectable material containing lidocaine; Hi-Ti, China’s first injectable material approved for neck wrinkle correction; and Yimei Plus One, a novel composite injectable material.

While many hyaluronic acid manufacturers continue to crowd into the niche of treating facial nasolabial folds, Imeik took a different path in 2016 by launching “Hearty,” creatively pioneering the market for neck wrinkle reduction and achieving rapid revenue growth thanks to this forward-looking strategy.

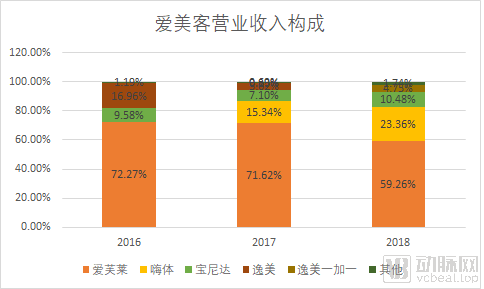

In 2019, Imeik's main business revenue reached RMB 320 million, representing a year-on-year growth of 44.28%. Among its product portfolio, HiTi and Ifresh are the flagship products. In 2019, HiTi accounted for 43.50% of the revenue, Ifresh contributed 39.27%, and Bonita made up 12.10%.

“Hearty” has now become a viral product in the market. In the first half of 2020, despite the impact of the pandemic, Imeik achieved revenue of RMB 242 million, representing a year-on-year increase of 0.72%. However, Hearty generated revenue of RMB 144 million, up 58.24% year on year, accounting for 59.47% of the company’s total revenue.

“HiTi” rapidly gained widespread market popularity and achieved high-speed growth because neck wrinkles, unlike facial wrinkles, are deeper and difficult to improve or conceal with skincare and cosmetic products. Moreover, they tend to reveal one’s age more easily. Hyaluronic acid fillers can provide rapid volumization, delivering significant visible results in a short period.

Meanwhile, hyaluronic acid injections are used for wrinkle reduction in neck lines. “Hearty” remains an exclusive product in China, allowing it to capture the entire market share. With “Hearty,” Imeik has pioneered a new application scenario for hyaluronic acid in medical aesthetics.

Carving out a niche in China’s hyaluronic acid industry, which is dominated by several major players, Imeik has been hailed as the “medical aesthetics prodigy” for its innovations in hyaluronic acid-based medical aesthetic treatments.

The listing of Imeik has revealed to the market that hyaluronic acid injection products in the medical aesthetics industry boast gross profit margins as high as 90%, earning them the moniker “the Moutai of medical aesthetics.” The substantial disparity between factory-gate prices and end-user prices has also drawn criticism, labeling the hyaluronic acid industry as one characterized by exorbitant profits.

Comparing hyaluronic acid to Moutai in the medical aesthetics industry is partly reasonable, but also a misinterpretation.

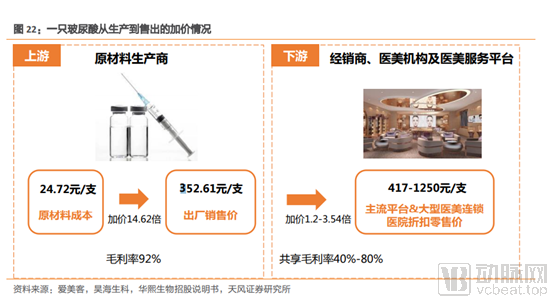

Indeed, data from a report by Tianfeng Securities Research Institute shows that at the upstream level, the raw material cost for one syringe of hyaluronic acid is approximately RMB 24.72, with an ex-factory price of RMB 352.61 per syringe, yielding a gross profit margin of 92%. Downstream distributors and medical aesthetic institutions sell it at prices ranging from RMB 417 to RMB 1,250 per syringe, sharing a gross profit margin of 40%–80%.

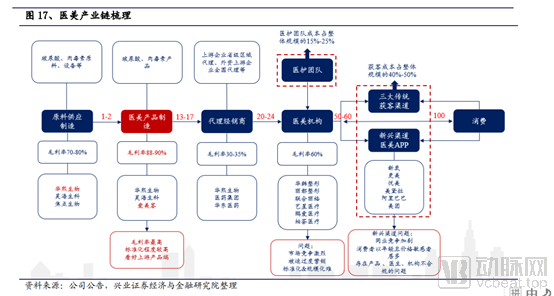

Indeed, within the entire medical aesthetics industry chain, upstream raw material manufacturing and product manufacturing represent segments with higher gross profit margins. According to research reports from Industrial Securities, the overall gross profit margin for medical aesthetics product manufacturing reaches 88%–90%, significantly exceeding that of other segments. Compared to downstream medical aesthetics institutions, upstream product manufacturing features a higher degree of product standardization, greater market concentration, and lower risk.

On the other hand, the high gross profit margins are largely attributable to the R&D-driven nature of the pharmaceutical industry. The medical device sector as a whole features substantial R&D investment and extended development cycles. In an interview, Jian Jun, Chairman of Imeik, also noted that, based on financial disclosures by listed companies, medical device and pharmaceutical firms with strong R&D capabilities and technological advantages generally exhibit higher product gross profit margins. This is primarily due to the industry’s characteristic traits of high R&D expenditure and long development timelines.

Hyaluronic acid, as a star sector, has garnered widespread attention not only for its high gross margin but also because it is favored due to a combination of multiple investment logics.

From a fundamental perspective, hyaluronic acid operates within the “beauty economy,” a high-growth sector characterized by rapid market expansion. As an upstream segment of the medical aesthetics industry, it enjoys relatively high gross profit margins. Furthermore, regarding the overall industry structure, while companies in the hyaluronic acid space have overlapping business activities, they each pursue distinct strategic focuses. This has led to multiple growth drivers emerging, rather than intense cutthroat competition within a single homogeneous track.

Bloomage Biotech positions itself as a comprehensive enterprise covering medical endpoints, consumer skincare, and upstream raw materials. As the world’s largest producer and distributor of hyaluronic acid, Bloomage Biotech is not content with limiting the application of hyaluronic acid to the medical field alone.

In the consumer skincare sector, Bloomage Biotech owns multiple brand series, including “BIOHYALUX,” “BIO-MESO,” “CYTOCARE,” “MEDREPAIR,” “PLUMOON,” “QUADHA,” and “DermaRun.” Its product portfolio encompasses single-use ampoules, various creams, lotions, toners, facial masks, hand masks, facial mists, and more. Bloomage Biotech strives to build its skincare brands into “shining examples of domestic products,” achieving repeated breakthroughs in mainstream visibility through collaborations with the Forbidden City and live-streaming e-commerce by key opinion leaders.

In the field of medical products, Bloomage Biotech offers injectable hyaluronic acid products, orthopedic injections, medical skin protectants, ophthalmic viscoelastic agents, and other related products.

Imeik, meanwhile, is focused on the medical aesthetics sector, with ambitions that extend far beyond hyaluronic acid dermal fillers.In addition to hyaluronic acid products, Imeik is also applying for registration of Type A botulinum toxin products and recombinant human glucagon-like peptide-1 (GLP-1) analogs. Botulinum toxin offers facial wrinkle-reducing effects, and Imeik’s product has entered the clinical trial application stage. GLP-1 can be used for the treatment of type 2 diabetes and obesity. In the future, Imeik’s development trajectory appears increasingly aligned with becoming China’s Allergan.

Haohai Biotech’s core business spans the full spectrum of ophthalmology (including intraocular lenses, orthokeratology lenses, and artificial vitreous bodies), orthopedic products, anti-adhesion and hemostatic products, as well as medical aesthetics and wound care. Hyaluronic acid is utilized across multiple business lines; however, from a revenue composition perspective, Haohai Biotech’s hyaluronic acid business constitutes a “secondary venture.” To draw a loose analogy, Haohai Biotech has the potential to become China’s Alcon in the future (Alcon being the world’s largest specialized company in ophthalmic pharmaceuticals and medical devices).

Overall, although all three companies are involved in the hyaluronic acid sector, they follow distinct development logics, making the industry more compelling to watch. Thus, it can be argued that China’s hyaluronic acid industry has entered its third stage of development, with companies now listed on capital markets and having established differentiated, in-depth strategic approaches.

Leveraging the prestige of medical aesthetics, we can examine the industrial chain and development logic of the hyaluronic acid industry. In fact, this is far from a short-lifecycle sector; it holds substantial potential market opportunities in the future. China’s medical aesthetics industry is entering a period of rapid growth. According to Frost & Sullivan, China was projected to become the world’s largest market for medical aesthetic services in 2021, with an estimated market size exceeding RMB 900 billion. Looking ahead, there are many more promising areas within the broader medical aesthetics market worth anticipating.