More Than 20 Biopharma Companies Listed on HKEX: Breaking the IPO Underperformance Cycle

Recently, the domestic biopharmaceutical company BeiGene announced that it will seek a listing on the STAR Market of China’s A-shares, with completion expected in the first half of 2021. Previously, BeiGene was listed on the U.S. stock market in 2016 and on the Hong Kong stock market in 2018. Upon successful listing on the STAR Market, BeiGene may become the first pharmaceutical company to be triple-listed across these three markets.

As of press time, BeiGene’s Hong Kong-listed market capitalization has surpassed HK$200 billion, while its U.S.-listed market cap reached $25.761 billion. It may be hard to imagine that this biopharmaceutical company, which has been operating for a decade and remains unprofitable with cumulative losses exceeding RMB 19 billion, has now become a pharmaceutical enterprise with a market valuation on par with Hengrui Medicine.

Unfortunately, in the entire biopharmaceutical sector, there are not many companies that have gained recognition from the capital market like BeiGene. The Biotech model has not yet been fully validated in China.

Just prior to this, Simcere Pharmaceutical and JW Therapeutics, two biopharmaceutical companies backed by Hillhouse Capital, both saw their Hong Kong IPOs break issue price upon listing. Meanwhile, other biopharmaceutical firms listed in Hong Kong—such as Ascletis Pharma, Kintor Pharmaceutical, and EverMed—have continued their downward trends, with several companies trading significantly below their offering prices.

Some argue that one of the Hong Kong Stock Exchange’s advantages lies in its dominance by institutional investors, which enables more accurate price discovery of company value compared to mainland China. However, the underperformance of biopharmaceutical stocks on the Hong Kong market has led some to question whether the sector is experiencing a wave of IPOs breaking their issue prices, signaling the bursting of the biopharmaceutical bubble.

On the other hand, among biopharmaceutical companies listed on the Hong Kong Stock Exchange, there are also top performers. RemeGen, which went public around the same time as Simcere Pharmaceutical and JW Therapeutics, also had Hillhouse Capital as one of its cornerstone investors. On its first day of trading in Hong Kong, RemeGen’s closing price was HK$69.8, a 33.97% increase over the offering price, pushing its market capitalization above RMB 30 billion.

It is difficult to determine whether the biopharmaceutical industry is overheating at present; moreover, the presence of certain bubbles is not necessarily a bad thing for the sector.

In any case, the recent short-term stock price volatility in the biopharmaceutical sector has provided us with an opportunity to re-examine the industry. In this diverse and rapidly evolving biopharmaceutical landscape, what types of companies hold long-term investment value? What dimensions should constitute the investment value of biopharmaceutical enterprises?

In fact, this is not the first time that Hong Kong-listed biopharmaceutical stocks have experienced a wave of break-issue prices.

In 2018, the Hong Kong Stock Exchange (HKEX) implemented sweeping reforms to allow pre-revenue biotechnology companies to list. This policy attracted a large number of biopharmaceutical firms that had been preparing for IPOs on the NASDAQ in the United States to turn instead to the HKEX. However, the first wave of pioneers did not reap the benefits; Ascletis Pharma, the first company to list under this new framework, and subsequently BeiGene, both saw their share prices fall below their IPO prices.

However, for China’s biopharmaceutical industry, which is in a period of rapid growth, stock price volatility does not necessarily indicate a lack of corporate value. The wave of IPOs breaking their issue prices in 2018 coincided with a downturn in the Hong Kong stock market, where cumulative share prices fell by 24% from their peak. Healthcare stocks such as Ascletis, BeiGene, and Ping An Good Doctor all traded below their IPO prices, while non-healthcare companies like Dreamsky Technology and Meituan Dianping were not spared either.

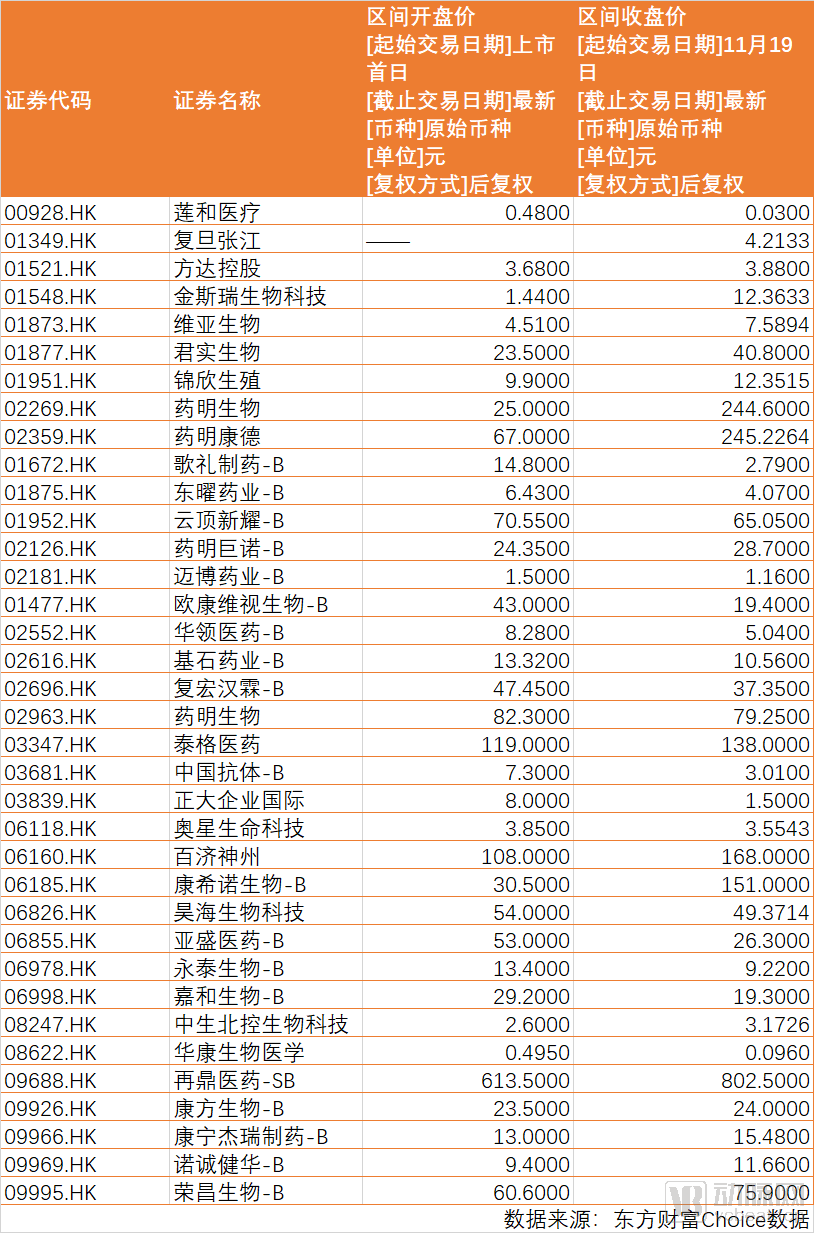

Now, the policy allowing unprofitable biopharmaceutical companies to list on the Hong Kong stock market has been in effect for two years, with more than 20 unprofitable biotech firms having gone public on the Hong Kong exchange. By examining their stock price movements, we may gain some insight into the secondary market’s preferences for biopharmaceutical enterprises.

Based on the data, from 2018 to November 2020, there were 36 biotechnology companies listed on the Hong Kong Stock Exchange, with a total market capitalization not exceeding RMB 800 billion. Among them, 20 were unprofitable biotechnology companies. Overall, unprofitable biotechnology companies performed modestly on the Hong Kong Stock Exchange. Moreover, several companies, including Jiayue Biologics, Yongtai Biopharma, Kintor Pharmaceutical, CStone Pharmaceuticals, and Hua Medicine, have fallen below their initial public offering (IPO) prices.

Of course, short-term stock price fluctuations are also influenced by many external factors, such as market conditions, and cannot be directly equated with the company's value.

However, a summary reveals that companies with underwhelming performance in the Hong Kong stock market can be broadly categorized into two groups: one concentrated in hot sectors such as PD-1/L1 inhibitors and cell therapy, and the other primarily adopting a license-in model at this stage.

The recent wave of biopharmaceutical stocks breaking their IPO issue prices is, to some extent, linked to market disappointment and skepticism regarding the overcrowding in the biopharma sector and the value of the license-in model.

In the secondary market, the performance of biopharmaceutical stocks has not dampened investment enthusiasm for the biopharma sector in the primary market. Biopharmaceutical financing continues to lead the broader healthcare investment landscape in both deal volume and total amount, with valuations in the industry repeatedly doubling.

According to data from the VCBeat database, there were more than 200 financing rounds in the biopharmaceutical sector from January to November 11, 2020, with several companies securing funding at the billion-yuan level.

The continuous influx of capital into the industry has provided essential support to this high-risk, high-investment sector, helping scientists achieve breakthroughs from zero to one. However, it has also raised concerns. Against the backdrop of the Hong Kong Stock Exchange allowing pre-profit biotech companies to list and the Shanghai STAR Market adopting a registration-based IPO system, some short-term capital, driven by profit-seeking motives, may engage in short-term arbitrage at the expense of the biopharmaceutical industry’s long-term development. This could ultimately lead to stagnation in innovation and undermine China’s already fragile ecosystem for innovative drug development.

However, the biopharmaceutical industry differs from the internet sector, where capital infusion can accelerate industrial progress. As a hard-tech field, biopharma demands long-term R&D and the perseverance to endure prolonged periods of obscurity. Short-term capital enthusiasm cannot sustain the decades-long R&D cycles characteristic of this industry.

As the saying goes, "One fears he won't come, yet also fears he will act recklessly."

Biotech innovators are seeing lackluster performance on the Hong Kong Stock Exchange, while biopharmaceutical investments remain hot in the primary market. Does this contrast signal an impending burst of the biopharma bubble? Are the PD-1/L1 market and the license-in model being disproven?

PD-1/L1: From the pre-launch dream of a trillion-yuan market to continuous price cuts after launch, it is often regarded as a manifestation of the bursting of the biopharmaceutical bubble.

PD-1/PD-L1 immune checkpoint inhibitors are novel anticancer therapies that have emerged in recent years, offering a new lifeline to many cancer patients. Since the approval of the first PD-1 monoclonal antibody, Opdivo, in China in June 2018, major pharmaceutical companies and national regulatory authorities have accelerated their efforts. To date, a total of eight PD-1/PD-L1 monoclonal antibodies have been approved for marketing in China.

Some have questioned whether the crowded PD-1/PD-L1 landscape and the resulting homogenized competition among innovative drugs could lead to overcapacity. Is this a continuation of weak innovation and excessive duplication?

At least from the perspective of patient accessibility, the clustering of PD-1/PD-L1 inhibitors has brought down the once-exorbitant prices of these “miracle drugs,” which is not a bad thing. According to the currently announced domestic prices for Opdivo and Keytruda, although they are the lowest globally, patients still need to pay RMB 300,000–600,000 per year. For most Chinese families, this price remains a significant financial burden.

In 2019, Junshi Biosciences officially announced the pricing for its PD-1 monoclonal antibody, shocking the industry with an annual treatment cost of only RMB 187,200—less than one-third the price of imported drugs. Recently, Hengrui Medicine’s PD-1 inhibitor, Airuika (camrelizumab), launched a major fourth-quarter promotional campaign offering an annual medication cost of RMB 39,600. Hengrui Medicine’s short-term promotion has pushed the PD-1 price war into the tens-of-thousands-of-yuan range.

As immunotherapies continue to hit the market, price competition among these drugs has intensified. With multiple domestic companies catching up rapidly, foreign pharmaceutical firms are also facing significant pressure. The biggest beneficiaries are, of course, patients and their families, who are gradually gaining access to these new medications at lower prices.

For patients, the clustering of PD-1/L1 inhibitors is not necessarily a bad thing. However, will low-priced innovative drugs ultimately backfire on the entire innovative pharmaceutical industry? Has the PD-1/L1 segment already become a red ocean, leaving companies that enter this market now destined to become mere casualties?

Let us first examine the current market rankings. Within the PD-1 inhibitor sector, Merck’s Keytruda dominates the high-end market, leveraging its advantages in clinical efficacy and the number of approved indications. Hengrui Medicine’s camrelizumab has caught up and surpassed competitors, driven by its robust sales capabilities. According to IQVIA data, camrelizumab generated over RMB 2 billion in sales during the first half of 2020. During the same period, Innovent Biologics’ Tyvyt achieved sales of RMB 921 million. In the third quarter alone, Innovent’s PD-1 product recorded sales exceeding RMB 600 million, bringing its total sales for the first three quarters to RMB 1.521 billion. Junshi Biosciences’ Tuoyi and BeiGene’s Baizean reported first-half sales of RMB 426 million and USD 49.943 million (approximately RMB 343 million), respectively.

In the highly competitive PD-1/L1 market, some companies are still attempting to carve out a niche by pursuing differentiation through two pathways: developing unique clinical indications and implementing combination drug therapies.

Taking Genor Biopharma as an example, the primary strategy for its PD-1 monoclonal antibody GB226 (geptanolimab) is to focus on differentiated indications in the Chinese market. Peripheral T-cell lymphoma (PTCL), a subtype of non-Hodgkin lymphoma (NHL), is relatively rare in Europe and the United States, accounting for only about 6%-10% of all NHL cases. The FDA has not yet approved PD-1 monoclonal antibodies for the treatment of PTCL. However, this lymphoma subtype is more prevalent in Asian countries, representing approximately 21.4% of all NHL cases.

Furthermore, players in the PD-1/PD-L1 space are also striving to achieve further differentiation through combination therapies. For the same indication, companies can extend the product lifecycle of PD-1 inhibitors by employing different combination regimens.

BeiGene has not ranked among the top performers in domestic PD-1 sales. Currently, BeiGene’s PD-1 inhibitor, tislelizumab injection, is being developed as a monotherapy and in combination regimens for a range of indications in the treatment of solid tumors and hematologic malignancies. There are currently 15 registrational clinical trials underway in China and globally, including 11 Phase 3 trials and four pivotal Phase 2 trials.

It is worth noting that while launching first during the peak sales period certainly offers advantages, pharmaceutical companies with strong commercial capabilities can still succeed by entering the market later. This holds significant implications for domestic pharmaceutical companies: even those not primarily known for R&D can potentially overtake competitors if they do not fall significantly behind in innovative drug development and ensure their me-too or similar products reach the market within 2 to 8 years. By doing so, they may catch up during the latter half of the peak sales window. Hengrui Medicine’s ability to rise from a late-mover position in PD-1/L1 sales precisely demonstrates the power of robust commercial execution.

At different stages of industry development, entrepreneurs with a visionary perspective should anticipate which resources are non-scalable and which possess exclusivity or scarcity when market competition stabilizes, and then devise strategies to overcome these barriers in pursuit of greater growth opportunities.

Looking back at the development of innovative drugs in China, fast-follow companies emerged as early as the post-2000 era, with Betta Pharmaceuticals and Chipscreen Biosciences being notable examples. After 2010, the PD-1 single target ignited the entire industry and paved the way for the success of the second wave of companies, including BeiGene, Innovent Biologics, and Junshi Biosciences.

Although China’s biopharmaceutical industry has experienced several waves of enthusiasm, it has remained in a catch-up position.

An investor who has invested in dozens of biopharmaceutical companies in China stated, “China’s pharmaceutical industry is large but not strong, with significant variations in drug quality. Not only are innovative drugs scarce, but generic drugs also struggle to reach the level of ‘high-quality generics.’ There remains a gap between patients’ demand for high-quality generic drugs and the current accessibility and affordability of medicines.”

Currently, the majority of innovative drugs entering clinical trials in China are follow-on innovations based on known foreign targets and lead compounds. This situation stems from two main factors: on one hand, China has a relatively weak foundation in basic research for new drug discovery, with insufficient investment in applied basic research, resulting in a scarcity of foundational achievements such as novel targets, mechanisms, and methodologies; on the other hand, there is a lack of integrated basic and applied basic research oriented toward delivering new drug outcomes.

For a long time, three factors have severely constrained the development of China's biopharmaceutical industry: insufficient and inconsistent investment in funding and talent, neglect of basic research, and a lack of forward-thinking mindset and strategic vision.

How to Improve? The aforementioned investors believe that the biopharmaceutical industry differs from the equally booming semiconductor chip sector; it requires strengthened collaboration and a flourishing, diverse ecosystem. Through international cooperation, pharmaceutical companies should be guided to actively respond to and participate in global competition, learn advanced technologies and management expertise from abroad, and continuously enhance the capabilities and standards of domestic enterprises in novel drug discovery and development.

He added, “One of the primary forms of international cooperation is license-in. However, this model presupposes that the licensee possesses clinical development capabilities and top-tier clinical talent commensurate with those of leading global pharmaceutical companies, thereby enabling the application of first-in-class or best-in-class drugs to Chinese patients.”

The license-in model was once a viable business strategy for the development of domestic biopharmaceutical companies; however, with inflated licensing fees, it has now become a relatively costly approach.

License-in and follow-on innovation, while not the most glamorous narratives, represent a “shortcut” for innovation in China’s biopharmaceutical industry.

It is difficult for innovative drugs in China to replicate the growth model of U.S. biotech companies, but there is an opportunity to reenact the rapid development path experienced by Japan’s pharmaceutical industry over the past two decades.

Most Japanese pharmaceutical companies seized the once-in-a-lifetime opportunity presented by the breakthroughs in innovative drugs during the 1980s. By adopting a follow-on innovation strategy, they built their foundations and narrowed the gap with the world’s leading pharmaceutical firms.

Japanese pharmaceutical companies started with generic drugs in the 1970s. Due to their weak R&D foundation at that time, it was difficult for them to achieve First-in-class breakthroughs, so most pharmaceutical companies adopted a follow-on innovation strategy.

The rapid growth and overtaking of Japanese pharmaceutical companies cannot be separated from the explosion of innovative drug research and development that began globally in the 1970s. Japan benefited from over a decade of foundational theoretical advancements made in Europe and America between the 1950s and 1970s, saving time and economic costs. After major innovative drugs were launched in Europe and America, Japanese pharmaceutical companies often brought follow-on innovative drugs targeting the same mechanisms to market within a few years. With the accumulation of their own technological capabilities, innovative drugs such as lansoprazole and candesartan cilexetil, launched after the 1990s, demonstrated relative advantages over original branded drugs in terms of side effects, completing the transition from "me-too" to "me-better" drugs.

Take a Long-Term View: The Complete R&D Cycle for Innovative Drugs Can Span 40–50 Years, Divided into Phases of Technological Accumulation, R&D Breakthroughs, Peak Sales, and Decline. Chinese pharmaceutical companies that seize the R&D breakthrough phase have the potential to become leading innovators in the industry.

We are in a period of R&D breakthroughs in the new cycle of innovative drugs. To seize this investment opportunity, we should replicate Japan’s follow-on innovation model of the 1980s and 1990s.

The aforementioned investors stated that great Chinese innovative drug companies do not necessarily follow a single growth model or path. In-house R&D capability is the foundation for sustained innovation, robust business development (BD) capability serves as a critical moat, and localized commercialization capability is key to future cash flows. While all these factors are crucial, the domestic innovative drug industry is still in its early stages, making it difficult to find companies that excel in every area. From a long-term perspective, enterprises that control core resources throughout the industry’s development trajectory possess certain investment value.