New Winners Emerge Amid IPO Boom: Challenges Remain for Chinese Biotech Firms Going Public Overseas

“Listing within four years of establishment,” “Three listings within six years of establishment,” “The first Chinese concept stock listed in three markets”... Few could have imagined that the spotlight moment for domestic biotech companies in the capital markets would arrive so swiftly. Since the implementation of the new regulations by the Hong Kong Stock Exchange (HKEX) in April 2018, 22 mainland Chinese biotech companies have gone public on the HKEX, with their stock names marked with a “-B” suffix (the HKEX designation for pre-revenue or unprofitable biotech firms). These companies were generally founded around 2012, with no more than ten years elapsing between their establishment and their initial public offerings (IPOs). Meanwhile, the number of mainland Chinese biotech companies that have already filed applications and are awaiting IPO approval on the HKEX has reached 11.

In response to the impact of the pandemic, countries and regions around the world have introduced accommodative economic policies, sparking an IPO boom that has swept through the biotechnology industry. This trend has also reversed the fortunes of biotech in the private equity market. Practitioners who were still trapped in a nearly two-year “capital winter” at the end of 2019 found themselves fielding visit requests from various investment institutions as soon as work resumed in 2020. The pace of investment due diligence and decision-making has become increasingly rapid, while the asset valuations acceptable to investors have continued to rise. One investor jokingly remarked on social media, “These days, if you’re not raising hundreds of millions, you can hardly claim to be in the biopharmaceutical business.”

Another group of relatively less noticeable winners in this wave of enthusiasm are securities firms and investment banks that serve as a bridge between primary market companies and capital markets, with a deep focus on overseas business. Futu’s latest unaudited Q3 financial report shows that, benefiting from a surge in user numbers and active trading,Futu Achieves Operating Revenue Nearly Three Times the Industry Average, with Net Profit Surging 18-Fold (GAAP Basis)). As a leading internet brokerage platform, Futu’s primary business involves providing securities brokerage and margin trading and short-selling services for U.S. and Hong Kong stocks to individual investors.

Selected Financial Data from Futu’s Unaudited Q3 Financial ReportData Source: Excerpted from the relevant financial report

Since 2017, Futu has ventured into B-end services by acting as a joint bookrunner and joint lead manager, providing IPO distribution services to companies such as Yixin Group, ZhongAn Insurance, and China Literature. In March 2019, Futu listed on the NASDAQ in the United States. Having experienced the entire U.S. listing process firsthand, the B-end services team gained practical insights and experience in distributing IPOs to individual investors in the U.S. market, leading to more mature business processes and models. In May of the same year, Futu Anxin was established as a brand, offering corporate clients solutions for U.S. and Hong Kong stock IPO distribution, investor relations and PR, as well as one-stop ESOP option management.

According to the latest quarterly report, Futu AnYi has cumulatively signed 81 clients for its IPO distribution and investor relations (IR) services, and 126 clients for its ESOP solutions. New clients added in Q3 include well-known companies such as Beike Zhaofang, XPeng Motors, and MINISO.

For biotechnology companies making their initial foray into overseas capital markets, Futu Anyi offers a comprehensive suite of IPO distribution products and operational systems.

“Our goal is to help companies reach tens of millions of investors with a single click,” a product lead at Futu AnYi told VCBeat. “Specifically, we have optimized our operational mechanisms, such as the planning of push resources like splash screen pop-ups, and iterated on operational tools including corporate community accounts and live streaming.”

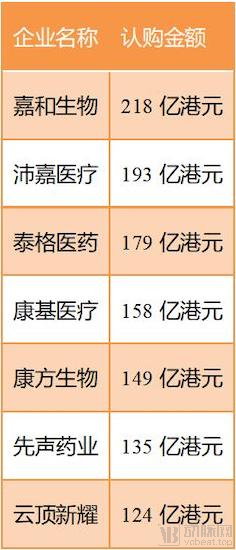

After establishing a systematic IPO distribution framework, Futu Anyi quickly facilitated Futu’s first subscription case exceeding HK$10 billion, namely the Jiumaojiu IPO, which has become a phenomenal event in Hong Kong stock IPO subscriptions. As of press time, there have been 19 cases on the U.S. and Hong Kong stock markets where Futu’s subscription volume surpassed HK$10 billion, with nearly half of them being biopharmaceutical companies.

Selected Cases of Futu AnYi with Subscriptions Exceeding RMB 10 Billion: Data Source: Provided by Interviewees

IR services serve as a bridge connecting companies with investors. The substantial user base accumulated on the Futu platform has given Futu AnYi a first-mover advantage in launching B-side business operations. Li Hua, founder of Futu, was an early core developer of Tencent QQ and the R&D head of Tencent Video, demonstrating strong proficiency in applying internet-centric thinking. It is therefore unsurprising that the internet brokerage platform he designed and operated has experienced exponential user growth and high levels of user engagement. “Our platform’s daily active users (DAU) have exceeded 600,000, peaking at 1.4 million, with a customer retention rate of 98.1%,” stated the aforementioned Futu AnYi executive.

Selected User Data from Futu’s Unaudited Q3 Financial Report; Source: Excerpted from the relevant financial report

In the IPO cases facilitated by Futu’s AnYi service, the most notable feature is the large number of investors, with subscription records frequently being broken. For many companies, Futu has become a key partner for listings on the Hong Kong and U.S. stock exchanges.

Futu served as an underwriter for XPeng Motors’ IPO, where subscription amounts on its platform reached $2.21 billion and the number of subscribers exceeded 46,000, setting a new record for online brokerages;

When Futu served as the distributor for MINISO, the subscription amount on Futu reached $1.48 billion, with the number of subscribers exceeding 34,000.

During Nongfu Spring’s IPO in Hong Kong, Futu recorded subscription amounts of HK$35.1 billion, with over 116,000 subscribers accounting for 16% of the total market subscriptions. This set a new record in the history of the Hong Kong stock market, marking the first time that a single channel attracted more than 100,000 subscribers for a new stock listing. By comparison, Alibaba and Xiaomi, which were also listed on the Hong Kong stock exchange, had global subscriber totals of just over 200,000 and 110,000, respectively.

Another topic as hot as the IPO frenzy is the frequent first-day trading below issue price seen in Hong Kong stocks. VCBeat’s analysis reveals that among the 125 stocks listed on the Hong Kong Stock Exchange from early 2020 to present, 36% broke their issue price on the first day of trading. In comparison, the corresponding figure for the first half of 2019 was a 38.1% rate of first-day declines. Notably, biotech companies listed with the “-B” suffix had a lower-than-average rate of first-day breaks. However, as even biotech firms—long regarded as high-potential investment targets—experience first-day declines, concerns are mounting that liquid assets may be insufficient to support the growing number of new listings in the capital markets.

In fact, as capital markets expand, the scale of global liquid assets is also growing. On one hand, amid the global spread of the COVID-19 pandemic, central banks around the world have adopted accommodative monetary policies to address the economic crisis, leaving institutional investors with ample cash reserves. On the other hand, with the rise of online brokerages, the barrier to entry for retail investors has been lowered, leading more individual investors to include equities in their asset allocation. According to Futu’s unaudited financial report for the third quarter, the platform’s cumulative registered users reached 10.4 million, a year-on-year increase of 52%; the number of new accounts opened stood at 1.173 million, up 80% year on year; and the number of clients with assets under management reached 418,000, a year-on-year surge of 137%. At the end of the third quarter, client assets totaled $25.9 billion, while total trading volume reached $130.9 billion, representing a year-on-year growth of 381%.

However, among the approximately 2,500 companies listed on the Main Board of the Hong Kong Stock Exchange (HKEX), the 320 firms included in the Stock Connect program account for over 90% of the total market capitalization and trading volume. Most HKEX-listed companies experience their peak valuation at the time of listing, followed by extremely poor liquidity. This may well be an unavoidable factor contributing to the frequent post-IPO price breaks seen in the Hong Kong market.

“It is not objective to claim that IPOs trading below their offering price have become the new normal for biotech companies,” Wu Biwei, Senior Partner and President of Financial and Corporate Services at Futu, told VCBeat. “Currently, the performance of the biomedical sector is highly divergent. Leading companies enjoy strong market capitalization and liquidity, with the market granting them high valuations and considerable tolerance, while some other companies face the opposite situation.” For companies encountering less favorable conditions in the capital markets, there are still strategies to cope. In addition to strengthening core competencies such as strategy, technology, and products, companies should also pay close attention to liquidity indicators.

“Stocks with low liquidity are not only prone to price volatility, but also pose significant entry barriers for institutional investors, which directly impairs a company’s subsequent financing capabilities,” emphasized Wu Biwei. Liquidity in public capital markets is typically much higher than in private markets, largely due to regular information disclosure mechanisms. This necessitates that companies at different stages and of different types formulate tailored communication strategies to effectively convey their value to investors and enhance investor recognition.

Wu Biwei explained that most companies lacking IPO experience are prone to delays or even failure in their listing efforts due to inadequate preparation for the listing process and key considerations. Such setbacks often stem from regulatory constraints related to listing readiness, current policies, and quiet periods, as well as improper investor communications and tax planning. “This scenario is relatively common in overseas capital markets such as the U.S. and Hong Kong stock exchanges.”

In addition to the investor communications mentioned earlier, employee incentives and management represent another critical yet relatively challenging issue that must be properly addressed during a company’s initial public offering (IPO) process.

The first one to two years after a company’s IPO constitute a critical period of talent turbulence. During this time, employees can directly observe the value and fluctuations of their stock options. Effectively managing employee expectations and properly addressing talent incentive issues can help companies navigate this phase smoothly. This is particularly crucial in the biotechnology sector, where competition for talent represents the core competitive dynamic.

Futu Anyi has also made strategic arrangements in employee incentives and management. Its Employee Stock Ownership Plan (ESOP) solution includes services such as equity incentive plan design, tax planning, trust establishment, exercise implementation, and foreign exchange reporting, providing enterprises with a one-stop service. It is reported that Futu Anyi has become a trusted partner for hundreds of companies, including Tencent, China Gas, Genor Biopharma, Jiumaojiu, Beike, XPeng Motors, So-Young, Zhihu, and Himalaya.

During the Q&A session of Futu’s Q3 earnings call webcast, Futu Anyi stated that the company will continue to explore the characteristic needs of new and potential new listings in the Hong Kong and U.S. stock markets, with a focus on strengthening its B-side service capabilities as a key element of its future development strategy. On one hand, the company will leverage investor relations (IR) services to drive growth in the number of corporate accounts, enabling individual investors to access rich, first-hand information through Futu, thereby facilitating better assessment of corporate value and fostering a win-win ecosystem. On the other hand, it will enhance collaboration with primary market partners, such as private equity firms and investment banks, to further expand its competitive advantage and brand influence.