Three Emerging Trends in Digital Diabetes Management: A Stakeholder-Driven Perspective

Diabetes has become a global health issue. To advocate for prevention and control worldwide, the World Health Organization (WHO) and the International Diabetes Federation (IDF) jointly established United Nations World Diabetes Day, which has featured a different theme each year for the past 14 years. This year’s theme is “Nurses and Diabetes,” aiming to underscore the critical role of nursing professionals in diabetes health management and to enhance the self-management capabilities of patients with diabetes.

Self-management is an effective approach to controlling diabetes; however, as it primarily takes place outside clinical settings, patients often lack sufficient motivation for adherence. This results in poor compliance with critical aspects such as blood glucose monitoring and medication administration, thereby compromising glycemic control.

In recent years, with the widespread application of digital technologies in the healthcare sector, digital management of diabetes has emerged as a prominent field. This domain has expanded the conceptual boundaries of “caregivers,” imbuing the term with digital connotations and providing patients with more efficient and diverse care options.

However, industry practices in recent years have shown that digital diabetes management still faces challenges such as insignificant improvements in patient adherence, weak willingness to pay, and unclear business models for enterprises. We attempt to re-examine the logic of the digital diabetes management industry by starting from the key stakeholders involved in diabetes care.

In April this year, a Chinese research team published an article on the latest epidemiological survey of diabetes in China in BMJ Online. The survey results showed that, according to the diagnostic criteria of the American Diabetes Association (ADA), the overall prevalence of diabetes among adults in China was 12.8%.

Behind the vast population of people with diabetes lies a stark reality: the rates of awareness, treatment, and control among patients are all below 50%. In three large-scale epidemiological surveys conducted over the past decade, these figures were even lower.

In other words, not all patients are aware of their diagnosis, and even among those who have initiated treatment, ideal disease control is not always achieved.

If intensified self-management is the core of diabetes control, then improving management adherence is the core within that core. Low patient adherence will lead to a series of impacts ranging from the individual to the societal level.

First and foremost, diabetes poses a significant threat to individual health and life. It can cause damage to the retina, kidneys, nervous system, and cardiovascular and cerebrovascular systems, making it a leading cause of blindness, kidney failure, cardiovascular and cerebrovascular events, and amputation in China. Poor adherence further increases the risk of complications.

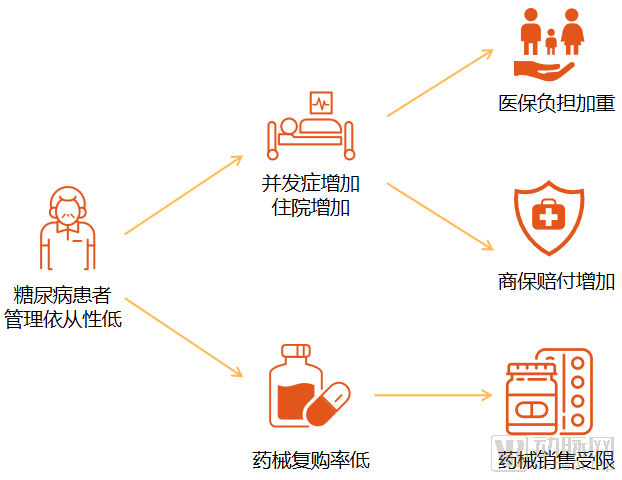

The Ripple Effects of Low Management Adherence Among Diabetic Patients, Chart by VCBeat

As shown in the figure above, from societal and industrial perspectives, the rising incidence of diabetes complications leads to increased hospitalizations and medical expenditures, thereby intensifying the burden on public health insurance and correspondingly raising commercial insurance claims. Meanwhile, pharmaceutical and medical device manufacturers also experience adverse impacts on sales volumes due to patients’ non-adherence to prescribed medications and failure to perform recommended blood glucose monitoring.

From the aforementioned value chain, we can analyze the stakeholders’ motivation to change the status quo based on the degree to which they are affected, which may reveal the payers for digital diabetes management.

First, not all patients are motivated. Diabetes has a long disease course from diagnosis to the onset of complications, with nonspecific symptoms, leading to weak self-management awareness among patients; health issues that do not directly threaten life tend to be overlooked. Even if patients have the willingness to engage in self-management, they are often unwilling to pay for someone to “manage” them.

Secondly, while there is strong momentum for health insurance to change the status quo, its positioning is limited to meeting basic medical needs and does not cover non-therapeutic aspects. Even within therapeutic care, its cost-containment strategies primarily focus on DRG payment reform and centralized drug procurement, which are unrelated to adherence interventions.

Finally, from an industry perspective, since patient adherence is closely linked to product sales for pharmaceutical and medical device companies as well as the operating costs of commercial insurance providers, we believe that these stakeholders have sufficient incentive to change the status quo and are willing to pay for services that improve patient adherence.

In the United States, digital chronic disease management companies such as Livongo and Welldoc primarily rely on commercial insurance providers as their payers. In the U.S., employers purchase commercial health insurance for their employees. For insured individuals with chronic conditions, insurers are responsible not only for covering routine treatment costs but also for the expenses associated with treating complications if these patients fail to manage their conditions effectively. Consequently, insurers have a strong incentive to support effective self-management among these patients. Companies like Livongo and Welldoc address this need precisely; their business model can be simply understood as “delivering high-quality services to end-users (C-side) while helping payers and employers (B-side) reduce costs.”

However, the current coverage rate of commercial health insurance in China is relatively low. According to a 2018 survey by the Insurance Association of China, the penetration rate of commercial health insurance in China is less than 10%, and many products do not allow individuals with pre-existing conditions to enroll. This indicates that the payment volume from commercial insurance companies for management services remains limited. Therefore, at this stage, domestic enterprises should prioritize improving patient adherence and enhancing glycemic control outcomes as their core orientation, thereby delivering value propositions to multiple stakeholders—including commercial insurers, pharmaceutical companies, and medical device manufacturers—and exploring diversified payer sources.

The expenditure structure of patients with diabetes is approximately 74% for medications, 18% for medical services, and 8% for blood glucose monitoring. Domestic diabetes management companies are not only exploring and developing consumer-facing (C-end) payment models but also gradually extending into business-to-business (B-end) payment models. For example, Tang Hushi (Sugar Nurse), established in the early stages of the digital diabetes management industry, has built a model that equally emphasizes both B2C and B2B segments. On the consumer side, Tang Hushi acquires users from public domains and directs them to its private-domain app through the sale of smart monitoring devices. Its free, personalized digital management services enhance patient adherence while generating data, which in turn drives long-tail consumption in areas such as medical supplies, pharmaceuticals, commercial insurance, and clinical trial recruitment.

On the B2B front, Tang Hushi collaborates with pharmaceutical and medical device companies as well as pharmacies to enhance patient adherence while boosting drug repurchase rates.

In 2016, Tang Hushi launched the Insulink automatic insulin injection dose recorder, which enables real-time tracking of patients’ insulin administration. The system intervenes when patients miss their insulin doses. Trial results demonstrated that Tang Hushi’s effective management reduced the attrition rate among insulin users by 23%, enabling pharmaceutical companies to engage patients more frequently and extend the duration of therapy (DOT).

During its research, VCBeat found that major pharmaceutical companies such as Sanofi and Novo Nordisk have partnered with Tang Hushi (Sugar Nurse) to provide patients with corresponding hardware and software devices. Additionally, Tang Hushi has developed the “Tang Hu Wan Jia” chronic disease membership system for pharmacies, helping them attract customers, enhance member stickiness through chronic disease management services, and increase medication repurchase rates.

Regarding commercial insurance companies, Tang Hushi has partnered with major insurers such as Ping An Insurance and Taikang Life to reduce claims payouts through diabetes management services.

Under the existing business model, U.S.-based digital chronic disease management companies are increasingly demonstrating their effectiveness. Livongo’s financial reports show that its revenue has climbed steadily in recent years. The company generated $170 million in full-year 2019 revenue and achieved $161 million in revenue in the first half of 2020 alone. In August 2020, Livongo merged with Teladoc, a leading giant in the U.S. digital health sector, forming a powerful alliance.

How will domestic companies grow, supported by a diversified payer landscape? It is worth watching.

While clarifying the payers for digital diabetes management, it is essential to consider the specific pathways to enhance patient adherence. A review of mainstream industry practices reveals that success hinges on effectively executing two key initiatives.

First, data collection through smart devices.

In the past, low adherence to diabetes management was largely attributed to the lack of efficient data collection and management tools. Multidimensional data serves as a fundamental prerequisite for patient behavior analysis and personalized management. With the emergence of smart monitoring devices integrated with mobile applications, patients now have access to efficient tools for data collection and management.

Companies such as Livongo, One Drop, and Dario each offer their own smart blood glucose monitoring devices as part of comprehensive diabetes management solutions, provided to patients alongside companion mobile applications. Companies without proprietary blood glucose monitoring hardware achieve data acquisition through strategic partnerships; for instance, Welldoc partnered with Dexcom to integrate the latter’s continuous glucose monitoring (CGM) devices. Similarly, in developing its “artificial pancreas,” Bigfoot collaborated with Dexcom for dynamic glucose monitoring while also acquiring Patients Pending, a company specializing in insulin injection logging technology, thereby integrating its TimeSulin insulin injection recorder into Bigfoot’s closed-loop system.

In summary, smart devices and data are two indispensable elements for companies implementing digital diabetes management.

Domestic companies are also involved in these two areas to varying degrees: some focus on devices, others on data, while companies like Tang Hushi cover both.

It is understood that Tang Hushi provides data monitoring and management for patients through smart hardware and a mobile app, and has already developed multiple models of smart blood glucose meters. In terms of key technologies, the Tang Hushi R&D team possesses extensive IoT experience, while the biochemical technology expertise of its strategic shareholder, Sinocare Inc., helps ensure monitoring accuracy.

Public information shows that the Sugar Nurse blood glucose meter and Sugar Nurse APP obtained CFDA registration as early as 2014; the insulin injection dose monitor has been registered with the FDA and CE, and has obtained 12 patents.

Second, intelligence-led, multi-level intervention.

Certainly, human inertia is universal; the availability of efficient tools does not guarantee their adoption. It is also impractical for healthcare professionals or other stakeholders to constantly remind patients to use these tools at all times. Therefore, it is essential to establish a multi-layered intervention mechanism that prioritizes intelligent decision-making, supplemented by human assistance, and incorporates incentives for habit formation.

Intelligence plays a dominant role in this intervention mechanism. In this regard, Welldoc’s expert analysis system and Livongo’s intelligent decision support system are both characterized by their intelligent capabilities; they analyze patient data and then provide real-time, personalized guidance, occupying a core position within the overall management solution.

In China, Tang Hushi has also implemented an intelligent decision support system. This system comprehensively analyzes patients' baseline data, medication records, blood glucose levels, and other metrics to provide personalized feedback. By leveraging over 6,000 scenario-based interactions and employing rich, patient-friendly language, the app has achieved a 52% increase in user retention.

Human intervention primarily serves a supportive role. For instance, while Welldoc requires very frequent daily blood glucose monitoring, the customer service center will only step in with necessary interventions if a patient fails to monitor on schedule for a certain period.

Furthermore, incentivizing patients through interactive entertainment to foster habit formation is also a common practice. For instance, abroad, mySugr uses cartoon-style interfaces and gamified design to improve adherence among adolescents with type 1 diabetes, while Mango Health motivates patients to take their medications on time by allowing them to redeem accumulated points for physical gifts. In China, Sugar Nurse (Tang Hushi) employs gamified designs and operations, such as “Guess the Blood Glucose Level” and “Challenge the Myth,” to organically integrate disease education with blood glucose monitoring, thereby promoting habit formation among diabetic patients.

Undoubtedly, given the current overall level of digital technology adoption in healthcare and patients’ awareness of self-management, the diabetes digital management industry remains in its nascent stage. Based on the above analysis, we can identify three key development trends in the industry.

The Rapid Development of Health Insurance Brings Greater Opportunities

The collaboration models between digital diabetes management platforms and pharmaceutical/medical device companies or pharmacies are well-defined, with tangible results achievable in the short term. In contrast, while health insurance currently has a low penetration rate within the commercial insurance sector, this field is experiencing rapid growth, offering significant potential for further exploration of digital diabetes management solutions.

Data from the China Banking and Insurance Regulatory Commission (CBIRC) show that from January to October 2020, gross written premiums for health insurance reached RMB 716.2 billion, a year-on-year increase of 16.6%. In contrast, total gross written premiums for the entire insurance industry during the same period amounted to RMB 3.96 trillion, representing a year-on-year growth of 6.9%. This indicates that the growth rate of health insurance significantly outpaced the overall industry average. In January 2020, thirteen ministries and commissions, including the CBIRC and the National Development and Reform Commission (NDRC), issued the “Opinions on Promoting the Development of Commercial Insurance in the Social Services Sector,” which set a target to expand the commercial health insurance market to over RMB 2 trillion by 2025.

Specifically, the collaboration between digital diabetes management and health insurance can follow two major directions.

First, health management delivers greater value within health insurance products. The new regulations on health insurance clearly define seven categories of health management services, including chronic disease management and disease prevention. Meanwhile, the cost allocation for health management can account for up to 20% of net premiums, a significant increase from the previous caps of 2% and 10%.

Of the RMB 2 trillion market for future health insurance, 20% amounts to RMB 400 billion. As diabetes is one of the major chronic diseases, it is poised to capture a significant share of this market.

Insurance companies can either build their own health management services or collaborate with third-party providers. While developing in-house health management capabilities offers greater control, it also entails higher construction and operational costs. By opting for third-party partnerships, insurers can delegate specialized tasks to professional teams, thereby reducing their own resource investment.

Digital diabetes management companies can seize opportunities by leveraging their strengths to provide high-quality, stable management services to insurance companies, thereby improving patient care and reducing claims payouts. However, it is worth noting that these companies should demonstrate the effectiveness of their management through more objective and detailed data, ensuring authenticity to enhance insurers’ willingness to pay.

In its early years, Welldoc conducted three clinical trials to compare the performance of its product in terms of glycated hemoglobin (HbA1c) control, frequency of hospitalizations and emergency department visits, and medical costs. After these results were published in academic journals, insurance companies began purchasing Welldoc’s products and services for their insured members. Subsequently, Welldoc invested in multiple additional clinical trials to further demonstrate the real-world effectiveness of its product.

Second, it assists insurance companies in designing differentiated products and promotes insurance sales. Since effective patient management can enhance insurers’ risk control capabilities, it becomes feasible to develop more insurance products tailored for patients with diabetes. Particularly amid the current homogeneous competition in million-yuan medical insurance policies, digital diabetes management companies can leverage their data advantages to help insurers design more competitive products.

Meanwhile, as diabetes digital management platforms aggregate a highly targeted patient population, the platform itself constitutes a high-quality scenario for insurance sales, serving as a precise distribution channel for insurance products. The Analysis Report on the Operation of the Online Life Insurance Market in 2019, released by the Insurance Association of China, shows that from 2016 to 2019, the compound annual growth rate (CAGR) of premiums for commercial health insurance via online channels reached 95%. With its characteristics of high efficiency and low cost, the internet has become an inevitable trend in distribution channels.

Potential User Growth

As previously stated, the awareness, treatment, and control rates among patients with diabetes remain suboptimal and require improvement. This analysis primarily focuses on enhancing the control rate and is therefore limited to a specific subset of patients. It is foreseeable that as national public health standards improve, the awareness and treatment rates for diabetes will rise, leading to an increase in the number of patients entering the control and management phase.

Meanwhile, older adults currently exhibit low reliance on mobile internet, resulting in limited penetration of digital diabetes management among patients. However, the National Guidelines for the Prevention and Management of Diabetes at the Primary Care Level (2018) point out that the diabetic population is trending younger. Over time, the proportion of future diabetes patients who are highly dependent on the internet will increase, making them more receptive to digital management tools.

The convergence of the above factors will drive growth in the potential user base for digital diabetes management.

Enhanced Influence of Domestic Enterprises

Industry development is a process of mutual learning. In the field of digital health, the business models of foreign companies have provided significant inspiration to their Chinese counterparts. While deeply cultivating the domestic market, Chinese enterprises are also expanding into overseas markets.

We have observed that, over the past two years, Chinese companies have increasingly appeared at the forefront of global digital health rankings, with some actively expanding into overseas markets. Specifically, in the realm of digital diabetes management, Tanghushi (Sugar Nurse), a domestic enterprise, has obtained CE marking and FDA registration for certain products. Its overseas sales have expanded to 15 countries across Asia, Africa, and Latin America. Recently, it has also partnered with WeHealth, an initiative by the French pharmaceutical company Servier, to explore digital chronic disease management in the European market.

As Chinese companies enhance their technical capabilities and deepen their business model exploration, their global influence is expected to grow, with a rising presence of Chinese enterprises anticipated in overseas markets.