MGI Tech IPO Prospectus Analysis: Pandemic-Driven Business Restructuring and the Challenge of Reducing Dependence on BGI

MGI

Gene Sequencing Instruments and Related Reagent & Consumables R&D Manufacturer

The gene sequencer industry may not be the most profitable, but it holds significant strategic importance and industrial value. Its strategic status is reflected in the security of human genetic resources, while its industrial value corresponds to the rapid development of the genetic testing industry.

Recently, the listing application information for MGI was posted on the STAR Market website of the Shanghai Stock Exchange. Although news that MGI had begun receiving pre-listing tutoring was disclosed several months ago, the release of this prospectus is still highly exciting, as it offers the first close-up look at the market development of China’s domestically produced sequencer industry.

MGI’s achievements in recent years have been widely recognized. As the first domestically produced sequencer manufacturer to go public, the information disclosed in MGI’s prospectus holds significant reference value for the development of China’s gene sequencing sector. Accordingly, we have reviewed the prospectus and summarized key insights below:

1. The company's revenue has continued to grow, and it successfully achieved profitability in 2018 and in the first three quarters of 2020;

2. Sequencer shipments grew steadily from 2017 to 2019, and the market is still in a promotion phase primarily driven by equipment sales;

3. The COVID-19 pandemic in 2020 had a significant impact on MGI’s business, with a notable decline in revenue from the sequencer segment, while the laboratory automation business saw substantial growth. Overall performance was strong; however, whether the laboratory automation business, which benefited from the pandemic, can sustain this momentum in the long term remains to be seen.

4. BGI-affiliated companies remained MGI’s largest customer, accounting for nearly 70% of its revenue in 2019;

5. Active expansion in overseas markets, accounting for 9.35% of revenue in 2019.

BGI’s strategic positioning in the sequencer market dates back a decade, when BGI Genomics had not yet gone public, the NIPT industry had not yet emerged, and Illumina did not yet dominate the sequencer landscape, with Thermo Fisher and Roche still remaining competitive. In 2010, BGI Genomics purchased 128 Illumina sequencers in one go, becoming the world’s largest gene sequencing service provider; at its peak, it even accounted for 40% of Illumina’s total business volume.

However, this also planted a ticking time bomb for BGI’s development. Due to its long-term reliance on Illumina’s instruments and reagents, BGI lacked sufficient bargaining power against upstream suppliers and was forced to accept Illumina’s annual price increases for reagents. Recognizing the critical nature of this issue, BGI swiftly decided to expand upstream. In 2013, it acquired the U.S.-based Complete Genomics (CG) for $117.6 million, leveraging CG’s technology to develop gene sequencers with independent intellectual property rights.

The project was initially incubated within BGI Group for the first few years, untilMGI Tech Co., Ltd. was established in April 2016Wang Jian, Chairman of BGI Genomics, assumed the role of Chairman, while Mu Feng, Rotating CEO of BGI Group, was appointed as the company’s CEO. With these two senior executives jointly taking the helm, BGI has demonstrated its unwavering determination to succeed in the domestic DNA sequencer market.

During the first two years after its establishment, MGI maintained a cautious and low-profile stance. Even landmark events such as the successful approval of the BGISEQ-50 for medical device registration in 2017 (whereas the earlier BGISEQ-500 product had been registered by BGI Genomics) did not receive extensive public exposure. It was not until MGI’s $200 million Series A financing round in 2019 that people realized the company, which had been quietly biding its time, had already taken the lead in China’s sequencer industry. The subsequent $1 billion Series B financing round in 2020 further propelled MGI into the spotlight, and together with several other financing deals, reignited interest in the domestically produced sequencer sector.

Despite undergoing two successive rounds of substantial financing, Wang Jian has firmly retained actual control over MGI.Through Smart Manufacturing Holdings and Huazhan Venture Capital, Wang Jian indirectly holds 52.3% of the shares in MGI. Following this issuance, he will continue to serve as the company’s actual controller, ensuring that MGI stays on its original course.

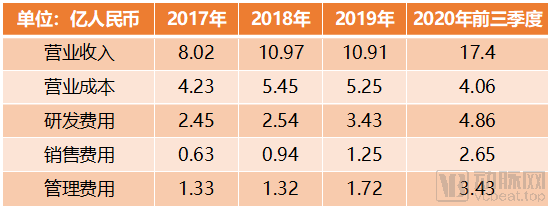

MGI: Selected Financial Data

The data disclosed in MGI’s financial report for its initial public offering dates back to 2017, providing a largely comprehensive reconstruction of the company’s development trajectory since its inception.In 2017, MGI achieved revenue exceeding RMB 800 million and recorded profits in the first three quarters of both 2018 and 2020.Although it cannot yet be said that MGI has entered a stage of stable profitability, it has at least basically met the initial conditions for profitability.

Let’s first examine the relevant data from 2017 to 2019. As MGI is still in its market expansion phase, with sequencers being the primary products sold, its gross profit margin remains relatively low, hovering around 50% during 2017–2019. However, as the installed base grows and reagent revenue becomes the dominant contributor, there is significant potential for a substantial increase in gross profit margin.

Regarding other cost aspects,MGI has consistently maintained high R&D investment., R&D expenditure in the first three quarters of 2020 reached RMB 486 million, accounting for approximately 28% of revenue. The substantial R&D investment is a key reason why MGI has not yet achieved stable profitability; however, this is essential for MGI, which is still in its early development stage. Selling and administrative expenses have been kept at relatively low levels over the past few years, rising steadily in line with the expansion of business scale.

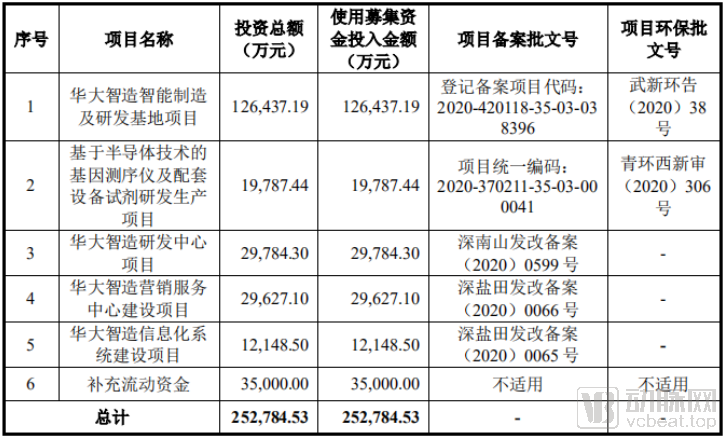

MGI: Expected Use of Funds Raised

For this IPO fundraising, MGI’s primary objective is to raise capital for the future construction of a series of R&D facilities., including its R&D base in Wuhan, sequencer-related production projects, and R&D centers. The remaining funds are also allocated to the construction of marketing centers and the company’s information technology systems. Therefore, MGI’s expenditures on R&D and marketing are expected to continue growing in the coming years.

On the surface, MGI’s revenue scale in the first three quarters of 2020 appeared to have reached a new high, increasing by nearly 60% compared to the previous year. Although sales and administrative expenses rose significantly, the company achieved overall profitability. To uncover the underlying truth, we need to start with an analysis of MGI’s business structure.

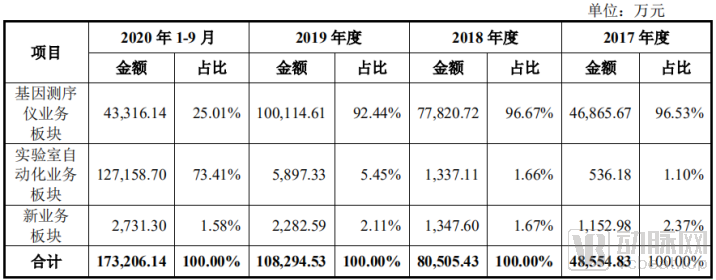

MGI’s business is primarily distributed across three major segments: the gene sequencer segment, the laboratory automation segment, and the new business segment.

MGI's Main Business Segments

In 2020, affected by the COVID-19 pandemic, MGI’s revenue structure underwent significant changes. The gene sequencer business, which originally accounted for more than 95% of revenue, experienced a sharp decline due to the pandemic, while the laboratory automation business benefited from the pandemic-driven demand and rose to become the largest revenue contributor.

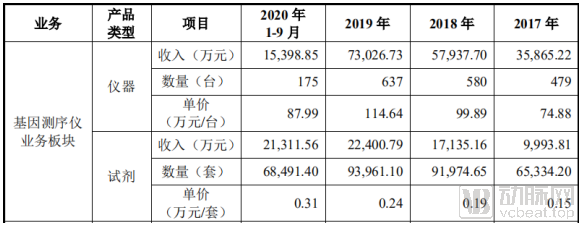

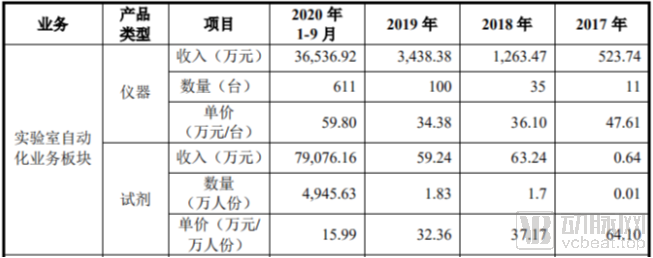

Partial Data on the Gene Sequencer Business Segment

The sequencer segment remains in its early stages of development, with a primary focus on rapid market expansion.According to the data disclosed in the financial reports, MGI’s sequencer sales maintained steady growth from 2017 to 2019, reaching RMB 732 million in 2019 with a shipment volume of 637 units. The average unit price of sequencers continued to rise during these three years, exceeding RMB 1 million. The unit price of supporting reagents also increased year after year, with the average price from January to September 2020 more than doubling that of 2017.

In 2020, global sales of sequencers were mediocre due to the impact of the COVID-19 pandemic. Illumina, the NGS sequencer giant, also revealed in its latest Q3 2020 financial report that sequencer sales in the first three quarters of 2020 amounted to only $276 million, a 26.6% decline from $376 million in the same period of 2019. During the same period, MGI was more severely affected, with sequencer sales in the first three quarters of 2020 reaching only RMB 198 million.

The good news is that sales of sequencing reagents have remained unaffected, with total sales for the first three quarters reaching RMB 226 million, nearly matching the full-year figure for 2019. This also indirectly reflects the high loyalty of MGI’s sequencing instrument user base, accumulated over the past few years, as customers continue to choose MGI’s products.

As the global pandemic gradually stabilizes, MGI’s future sequencer sales are expected to return to normal. With the expanding global coverage of sequencers, reagent sales will increasingly become a key pillar of MGI’s future revenue.

Partial Data on the Laboratory Automation Business Segment

Laboratory automation has not actually been a core business of MGI in the past few years.Annual sales in 2019 totaled less than RMB 35 million, which is incomparable to the sequencer business.

In 2020, due to the COVID-19 pandemic, sales of laboratory automation equipment and reagents experienced significant growth, rapidly becoming MGI’s primary source of revenue.Instrument revenue reached RMB 365 million, while sales of supporting reagents amounted to RMB 791 million. Calculated by number of tests, considering that previous reagent sales were only at the scale of tens of thousands of tests, MGI supported nucleic acid testing for nearly 50 million people during the pandemic. Moreover, these products were primarily sold overseas; in the first three quarters of 2020, MGI’s overseas revenue share increased to 68.81%, with the majority coming from its laboratory automation business.

Due to changes in business structure brought about by the COVID-19 pandemic, MGI significantly increased its sales force to strengthen sales efforts, which led to a substantial rise in selling and administrative expenses in 2020.

The unit selling price of its reagents underwent significant adjustments amid rising sales volume. In the first three quarters of 2020, the unit selling price of reagents was only RMB 15.99 per test, representing a decline of over 50% compared with RMB 32.36 per test in 2019. Nevertheless, due to the extremely low cost of reagents, the gross profit margin of the laboratory automation business still reached 80.63%.

MGI did not disclose its specific quarterly revenue figures for 2020 in its prospectus, making it unclear whether its laboratory automation business segment can maintain such a revenue scale in an environment where pandemic control has become normalized. However, from a long-term perspective, the windfall gains brought by the pandemic are unlikely to be sustainable. The laboratory automation business may leverage this opportunity to build its reputation in the market, but it could also prove to be short-lived. How the business will develop in the future remains to be seen pending MGI’s next information disclosure.

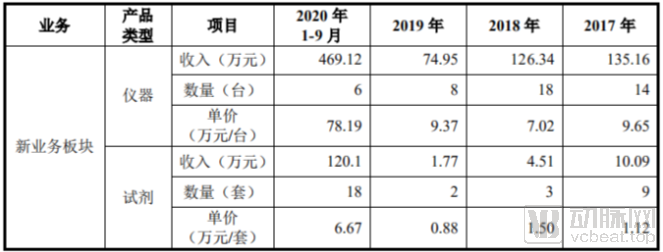

Partial Data on the New Business Segment

The positioning of the new business segment is more marginal; neither its sales revenue nor its sales volume can compare with those of the two leading “big brothers.”Several products are indeed highly forward-looking, but based on sales performance, they are unlikely to become one of MGI’s revenue pillars in the short term.

The products covered by the new business segment—cellomics solutions (related to single-cell library preparation) and BIT products (related to end-to-end management of gene sequencing)—share certain synergies with its core business. However, the continuous expansion in sequencer sales has failed to drive widespread adoption of these two product lines. The remote ultrasound robot, on the other hand, appears to have no relevance to its core business. Although this product was deployed at Leishenshan Hospital, Jiang’an Fangcang Hospital, and Huangpi Fangcang Hospital during the pandemic, its sales performance in the first three quarters of 2020 remained lackluster.

Therefore, based on MGI’s current product positioning, although its product portfolio is already highly diversified and spans multiple related fields with sequencers at the core, its primary revenue source in the coming years will likely still depend on the expansion of sequencer installation base. Whether the growth in laboratory automation business driven by the pandemic can be sustained remains to be seen.

Returning to another issue of concern: how much market share has MGI actually captured from Illumina?

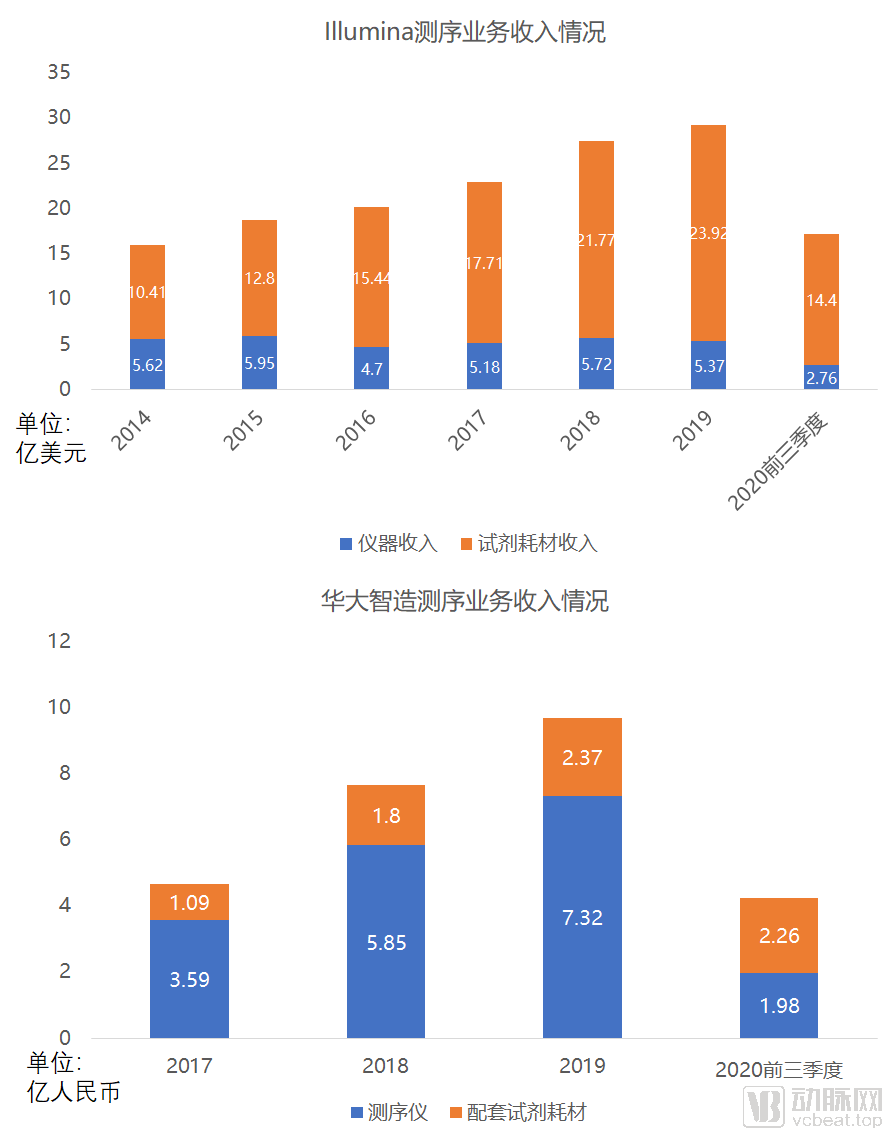

Comparison of Sequencer Businesses Between MGI and Illumina

Judging solely by sequencer sales, MGI appears to be rapidly catching up with Illumina. In 2019, Illumina’s sequencer sales amounted to $537 million (approximately RMB 3.5 billion), while MGI’s sequencer sales had already reached RMB 732 million. Achieving roughly 20% of Illumina’s sales volume within just a few years, MGI seems to have secured victory in its first phase.

However, the issue is that sequencer sales are not the true profit driver in this sector. For established sequencing companies represented by Illumina, the instrument market is nearing saturation; revenue from reagents and consumables, driven by a large installed base, is the actual source of revenue growth.

For instance, in 2019, Illumina’s reagent revenue reached $2.392 billion, approximately 4.5 times its sequencer revenue. In contrast, MGI’s sequencing reagent revenue in 2019 was only RMB 237 million, accounting for just 32% of its sequencer revenue.

Moreover, MGI is facing another issue: based on sales figures to date, after four years of development, its largest customer remains BGI.

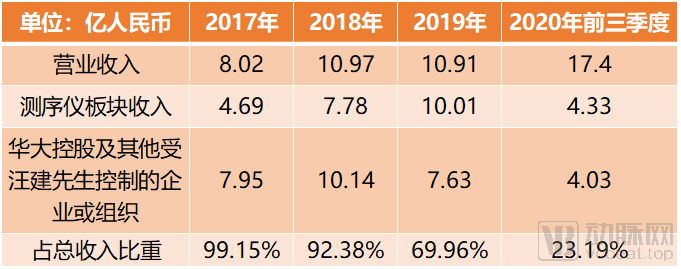

Data Related to MGI's Largest Customer

In 2017 and 2018, BGI Holdings and other enterprises or organizations controlled by Mr. Wang Jian (hereinafter referred to as “BGI-related entities”) accounted for more than 90% of MGI’s revenue. In 2019, this proportion decreased to approximately 70%, which, despite the decline, remained at a high level.

In the first three quarters of 2020, although the proportion of revenue from MGI-related enterprises in MGI’s manufacturing segment appeared to decline significantly, it is worth noting that four of its top five customers were new entrants. Coupled with a sharp rise in laboratory automation business, the products purchased by these customers were likely unrelated to sequencers. Furthermore, based on a comparison between the procurement scale of MGI-related enterprises and the revenue of the sequencer segment, it is speculated that MGI-related enterprises still contributed the majority of the revenue related to sequencers.

From the perspective of the relationship between BGI and MGI, their collaboration is a win-win partnership. BGI has reduced its dependence on upstream suppliers by extensively applying MGI’s products, while MGI has secured financial support for its early-stage development through this cooperation.

However, from a long-term perspective, even though BGI Genomics is the world’s largest gene sequencing service provider, its procurement scale remains quite limited. Particularly in terms of sequencer purchases, the procurement demand of BGI-affiliated companies will gradually approach its upper limit, after which only annual recurring revenue from reagents will remain. Therefore, for MGI to achieve further growth in revenue scale in the future, it needs to more broadly expand its customer base.

MGI is certainly well aware of this, and has long sought to broaden its market channels through a series of strategic initiatives. Its suite of operational strategies offers valuable lessons for other companies in the genetic testing industry.

As we analyzed in our previous in-depth article, among the three major application scenarios—hospitals, research institutes, and third-party clinical laboratories—third-party clinical testing remains the most significant. For domestically produced sequencers to achieve rapid development, industrial collaboration is indispensable.

Collaborating with NGS companies to sell domestically produced sequencers is one of the options for industrial cooperation. Currently, many domestic gene sequencing devices are located in third-party medical testing laboratories, especially in "specialized testing" laboratories that specifically provide genetic testing services. Our statistical data shows that many of these enterprises produce their own gene sequencing equipment through acquisitions, collaborations, and other means. The layout in gene sequencing equipment not only ensures the company's own sequencing capabilities but also significantly enhances the completeness of its end-to-end solutions.

For instance, MGI has chosen to collaborate with Panasonics and Genetron Health, selling its products through OEM arrangements to broaden its sales channels. In addition to procuring and using their own equipment, genetic testing companies also prioritize partnering products when co-establishing laboratories with hospitals. Both approaches effectively enhance the adoption rate of domestically produced sequencers.

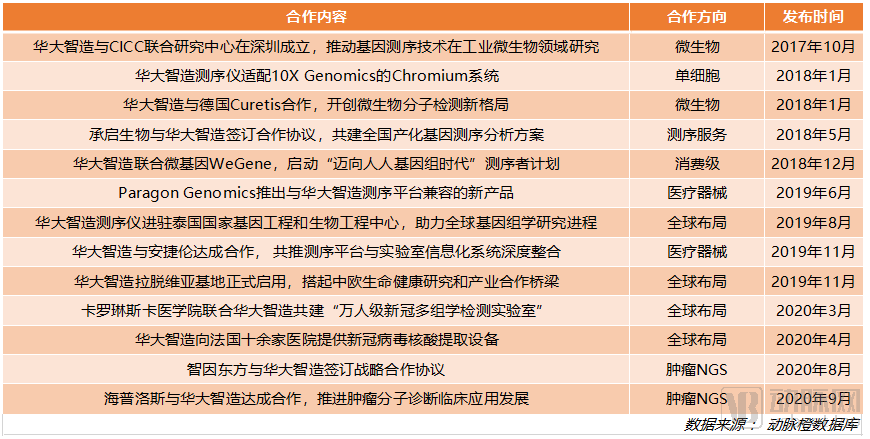

MGI External Collaboration News

Beyond the simple collaborative sales of sequencers, domestically produced sequencers can also engage in extensive strategic cooperation in specific application scenarios of sequencing technology, such as tumor NGS, pathogen detection, and single-cell sequencing. Many of these application scenarios are seeking more cost-effective sequencing solutions, where the price advantage of domestic sequencing systems can be prominently demonstrated.

MGI has long recognized this fact. Since late 2017, it has been actively seeking industrial collaboration opportunities and has made strategic arrangements across various development directions. For instance, while the single-cell sequencing market is largely monopolized by 10X Genomics, MGI Sequencing adapted to the 10X Genomics Chromium system as early as 2018, thereby entering the single-cell sequencing field.

Cooperation in overseas markets is also one of MGI’s key strategic focuses, with multiple projects advanced to enhance its influence abroad. These initiatives have yielded significant results, with overseas markets accounting for 9.35% of the company’s business in 2019. Notably, sales in the Asia-Pacific region excluding China reached approximately RMB 76 million in 2019.

MGI’s series of strategic moves corroborate our assessment. While the genetic testing industry has entered a phase of comprehensive marketization, the upstream sector remains dominated by foreign enterprises for an extended period, which could pose a significant obstacle to future industrial development. In contrast to the temporary lag in China’s domestically produced sequencer industry, the domestic genetic testing sector has developed relatively rapidly, with the tumor next-generation sequencing (NGS) field already achieving large-scale industrialization.

Although domestically produced sequencers and China’s genetic testing industry are not in a relationship of mutual dependence where the loss of one spells the doom of the other, it is ultimately beneficial and harmless for the genetic testing sector to control upstream equipment and reagent costs. On the path to breaking foreign monopolies, MGI’s initial charge still requires greater support from downstream industries.