Medical Devices Year-End Review 2020: Over ¥5 Billion Invested, Industry Racing Toward IPOs

In 2020, the entire medical device industry chain experienced significant volatility; at the same time, it was a year of rapid growth for the Chinese medical device market.

In the primary market, both the number of financing events and the total amount raised in the medical device sector saw a significant increase in 2020.

In the medical financing trends of the past few years, the medical device sector has maintained stable performance, unlike innovative drugs, which have seen a sudden surge in recent years. This year, financing in the medical device sector has generally remained stable, with a small peak emerging.

Many attribute the emergence of this minor peak to heightened industry attention driven by the pandemic. However, Hu Minjie, Executive Director at Capital Healthcare (Yi Kai Capital), stated that while the pandemic did lead to significant performance gains in specific medical device segments—such as ICU equipment, in vitro diagnostics, and disinfection products—it was not the primary driver of growth across the entire medical device industry.

The primary reasons are twofold: First, the total capital inflow into the industry this year has been substantial. Investment firms adopted a relatively conservative stance in 2019, and investment activities were further constrained during the first half of the year due to the impact of the COVID-19 pandemic. Consequently, these firms needed to deploy the capital that had accumulated over the previous one to two years in the second half of 2020. This has driven overall growth in the healthcare sector, and as medical devices constitute a key segment of healthcare, significant capital has also begun flowing into the device sector.

On the other hand, the introduction of a series of policies, such as the registration-based IPO system on the STAR Market and the ChiNext Board, has lowered listing thresholds. The gap between the primary and secondary markets has narrowed, with many projects entering the pre-IPO stage.

Compared with innovative drugs, the medical device sector is more resilient, carries relatively lower risk, and features lower valuations. With a limited number of listed companies, the industry remains in a growth phase, making the medical device track one of the preferred choices for capital allocation.

When there is abundant capital in the market and exit channels are highly accessible, everyone rushes in frenetically.

The direction of the tides will ultimately reshape the course of the riverbed. In 2020, against the backdrop of a massive influx of capital, changes in exit pathways for IPOs, and the implementation of volume-based procurement policies for medical devices, the medical device industry underwent significant transformations, with certain rigid frameworks being reconstructed.

Currently, VCBeat (WeChat ID: vcbeat) has identified several major trends:

In the primary market, cardiovascular interventional therapy leads in financing, with multiple sub-sectors such as structural heart disease and neurointervention seeing broad-based growth; surgical robotics remains an evergreen sector, attracting new entrants that continue to expand its boundaries.

In the secondary market, policies such as the establishment of the STAR Market and the implementation of the registration-based IPO system have significantly shortened the time required for companies to go public. The boundary between primary and secondary market investments is becoming increasingly blurred, and listed companies will face a "20/80" divergence in the future.

In terms of policy impact, the volume-based procurement (VBP) policy will compel industry innovation. To cope with the pressure from centralized procurement, mergers and acquisitions (M&A) integration and expanding into overseas markets will become key to development.

Next, VCBeat will analyze this year’s hot investment sectors, major publicly listed companies in the secondary market, and medical device policies, to present and elucidate the changes that occurred in the medical device industry in 2020.

“This year, there were many investment opportunities in the medical device sector that we wanted to pursue, but valuations were so high that we ended up making no investments,” an investor from a well-known private equity (PE) fund told VCBeat. His fund invested RMB 3 billion in the healthcare sector this year. While it has historically focused more on innovative drugs, it has been paying attention to the medical device industry for the past two to three years. This year, he has felt increasing pressure from rising valuations.

As a well-capitalized fund, the surge in valuations within the medical device sector this year has not triggered panic; instead, it has fostered greater composure. “Many companies are crowding into currently popular niches. We prefer not to cast a wide net. Although valuations are elevated at present, we are willing to wait for the emergence of true industry leaders.”

The experience of this fund may indirectly reflect the current state of the primary market in the medical device sector: true industry leaders have yet to emerge, projects are still in their growth phase with substantial room for expansion, yet enthusiasm for investment and financing remains undiminished. Market sentiment is relatively optimistic, with hot sectors and prominent companies being highly sought after.

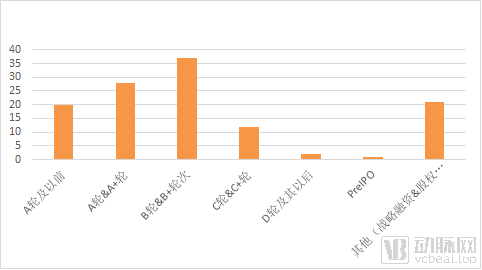

According to statistics from the VCBeat database, as of November 30, 2020, there were a total of 231 medical device financing deals in China, with over 92 projects securing funding amounts exceeding RMB 100 million.

From the perspective of financing rounds, most medical device financings are concentrated in Series A and Series B.

As the institution that has invested the most in the medical device sector this year, Hillhouse stated that in the six months since the launch of Hillhouse Ventures, the number of early-stage investments in the biopharmaceutical and medical device sectors has nearly tripled compared to the same period last year, with many of these being Series A and Series B projects.

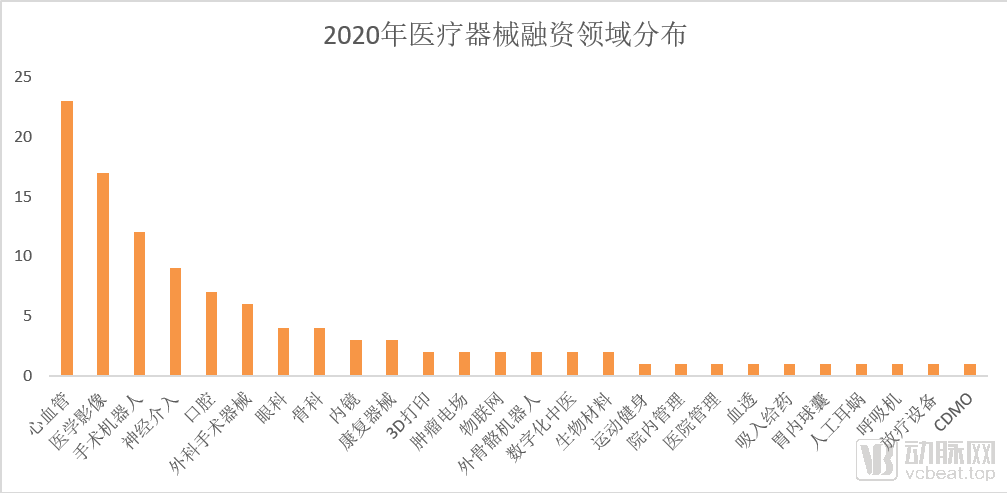

Data on financing and investment in the primary market also reveals that large-scale funding rounds are predominantly concentrated in hot sectors such as cardiovascular care, surgical robots, neurointerventional devices, surgical instruments, and medical imaging.

What is the allure of these hot sectors? Will their future development remain robust, or will they peak and then decline? VCBeat will next provide an analysis of different niche segments.

Vascular Intervention: Entering the Second Half of the Game

Not an exhaustive list; some companies have overlapping areas of involvement.

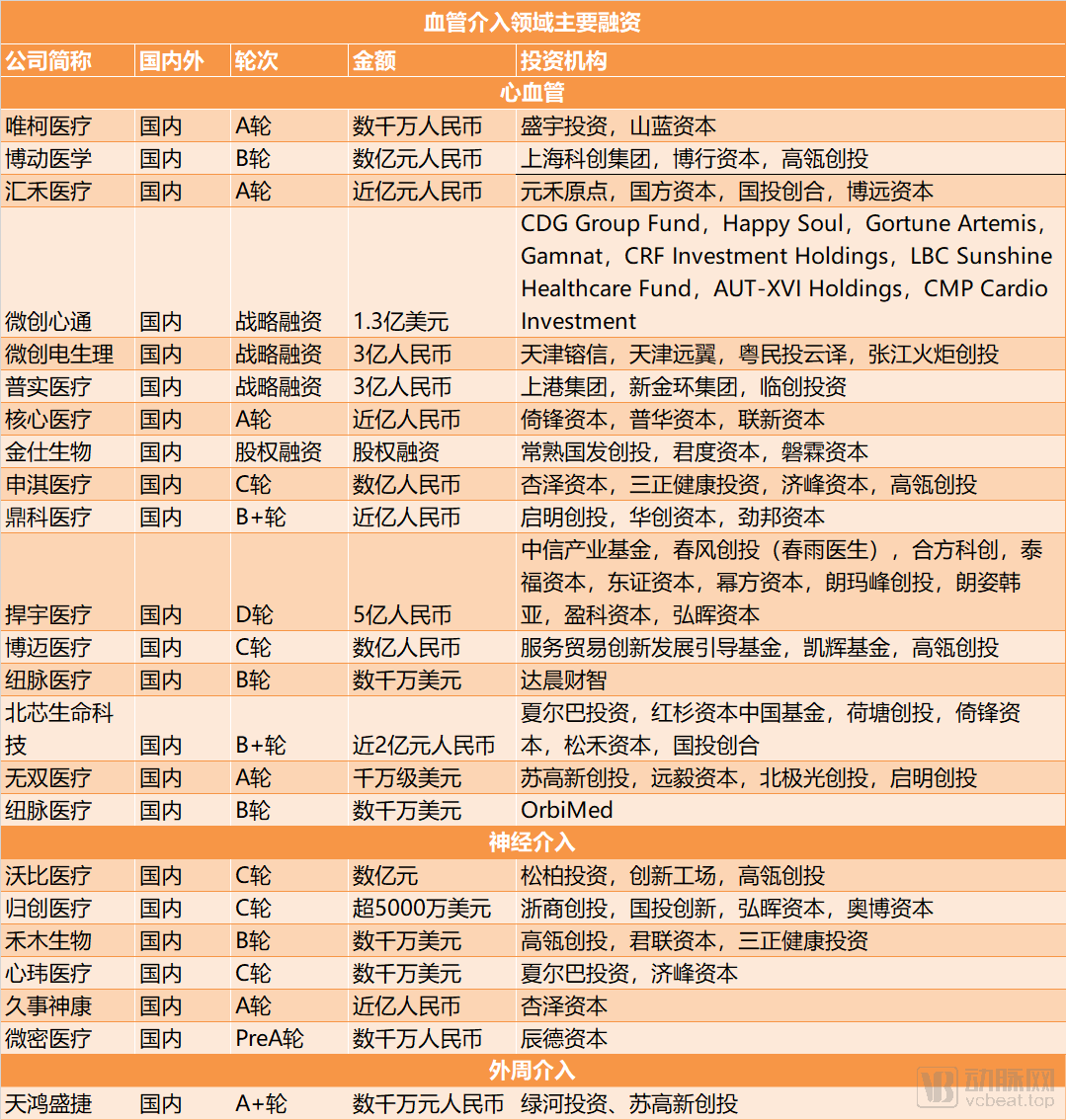

Vascular intervention can be described as a sector that attracted both significant capital and attention in 2020. Within cardiovascular intervention, more specialized sub-sectors—including structural heart disease, cardiac rhythm management, basic consumables such as guidewires, artificial hearts, and cardiac electrophysiology—have all secured financing, marking a comprehensive boom across the entire field.

How hot is the financing in the field of vascular intervention this year? With valuations on the rise, many popular companies have reached a point where even those with capital cannot secure a stake.

The surge in popularity of vascular interventions this year can be described as capitalizing on favorable trends and timing.

First and foremost, it is worth emphasizing that the fundamental logic underpinning valuations in the cardiovascular sector remains the immense market potential driven by a large patient population, with minimally invasive intervention regarded as an unstoppable trend.

Cardiovascular and cerebrovascular diseases have long been the leading cause of death in China. A breakdown of financing in the field of vascular intervention reveals that sectors such as neurointervention, structural heart disease, cardiac electrophysiology, and artificial hearts correspond to stroke, valvular heart disease, arrhythmias, and heart failure, respectively—conditions with large patient populations. The fundamental driver behind the heightened activity in these areas remains the substantial unmet clinical needs.

Why has vascular intervention exploded specifically this year? Behind this trend lie the driving force of publicly listed companies in the secondary market and the impact of volume-based procurement policies.

In the cardiovascular field this year, Venus Medtech and Peijia Medical have successively listed on the Hong Kong Stock Exchange., listed companies in the secondary market have significantly driven the valuation of innovative enterprises.Meanwhile, the smooth operation of exit channels in the secondary market,This has made pre-IPO projects in the cardiovascular sector highly sought-after, and coupled with the scarcity of leading companies in the vascular intervention track, valuations in the vascular intervention field have risen rapidly.

Take the neurointerventional field as an example. With the listing of Peijia Medical, the dual-track model of cardiovascular intervention plus neurointervention quickly heated up the neurointerventional sector, especially as clinical demand in this area is experiencing rapid growth. Neurointervention has suddenly become a hot spot, with companies intensively securing large-scale financing rounds.

In the second half of this year, the volume-based procurement (VBP) of coronary stents has also spurred market attention to other niche segments within the cardiovascular field.

From the perspective of future trends, we believe that with leading companies completing their financing rounds, and with Peijia Medical and Venus Medtech already listed while MicroPort CardioFlow is poised to list on the Hong Kong Stock Exchange, the cardiovascular sector has arguably entered its second half.

For a mature sector such as TAVR,Multiple companies have already obtained certification, and leading firms have completed their IPOs; the fierce commercial competition has only just begun.

For the neurointerventional sector, which is still in the clinical approval phase, companies currently offer relatively limited and homogeneous product portfolios. These products have not yet entered large-scale clinical validation. Although numerous players have emerged with no significant differentiation at present, the gap between them is expected to widen in future development.

In the second half of the vascular intervention game, the test lies in how to grow from a single tree into the top tier of the forest; how to commercialize pillar products and capture market share; how to expand across disease areas and broaden the product portfolio; and how to both strengthen local R&D capabilities and establish the ability to mobilize global resources.

Surgical Instruments: Overseas Expansion Capabilities Will Become More Critical

Another sector worth watching in 2020 is surgical instruments, a field that previously received limited attention but has emerged as a dark horse.

The primary products in minimally invasive surgical instruments are staplers and ultrasonic scalpels. In surgical practice, staplers are colloquially referred to as “guns,” and ultrasonic scalpels as “knives.” Based on the size and length of the instruments, they are further categorized into long guns, short guns, large knives, and small knives.

This year, Hillhouse Capital invested in two minimally invasive surgical instrument companies: Yisi Medical, which specializes in surgical staplers, and Houkai Medical, which focuses on ultrasonic scalpels.

The surgical instruments sector, much like the cardiovascular field, is a hot spot in both the primary and secondary markets.

In the secondary market, Kangji Medical, a domestic platform for minimally invasive surgical instruments and accessories (MISIA), listed on the Hong Kong Stock Exchange in June, while Tianchen Medical, which specializes in staplers, listed on the STAR Market in September.

In the primary market, multiple companies—including Houkai Medical, Fangrun Medical, Esis Medical, Biomere Medical, Intuitive Medical, and Leisheng Medical—completed financing rounds, with participation from several well-known domestic investment firms such as Hillhouse Venture Capital, Qiming Venture Partners, Yusheng Venture Capital, and China Renaissance.

Surgical instruments are poised to become a major market trend this year, following a logic similar to that of vascular interventions. This is primarily driven by the continuously growing volume of surgical procedures and the substantial market size. In 2019, the market size for minimally invasive surgical instruments and accessories (MISIA) in China reached RMB 18.5 billion.

Furthermore, China’s high-end surgical instrument market is predominantly dominated by imports, presenting substantial opportunities for domestic substitution. Taking the stapler market as an example, its size in China reached RMB 9.479 billion in 2019, with multinational medical device giants such as Johnson & Johnson and Medtronic holding a combined market share of over 60%. In particular, laparoscopic staplers, which entail higher technical requirements and significant patent barriers, are essentially monopolized by foreign manufacturers represented by Johnson & Johnson and Medtronic, making them the product category with the lowest rate of import substitution.

Turning to ultrasonic surgical devices, Johnson & Johnson holds an absolute monopoly with approximately 80% of the market share. When other imported brands are included, domestic manufacturers account for less than 10% of the market.

The second major reason for the heightened attention on surgical instruments is that this industry exhibits relatively inelastic demand; consequently, obtaining regulatory approvals and pursuing mergers and acquisitions will be comparatively easier in the future, making the sector more susceptible to rapid maturation driven by capital investment.

Looking at future trends, surgical staplers will be subject to volume-based procurement nationwide, leading to market consolidation and increased concentration.

China’s surgical stapler market is characterized by a large number of manufacturers and significant product homogenization, with surgical staplers now included in volume-based procurement (VBP) programs. Previously, surgical staplers were already listed in VBP initiatives across multiple provinces, with price reductions approaching those seen for coronary stents. In Jiangsu Province’s medical consumable price negotiations, the price of linear staplers originally costing over RMB 2,000 dropped to just over RMB 100, while hemorrhoid staplers initially priced at RMB 4,000–5,000 fell to RMB 200–300. The average price reduction for surgical staplers reached 83.93%, with the highest reduction hitting 96.29%.

Competition driven by product homogenization and pressure from volume-based procurement may determine that M&A capabilities and overseas market expansion will become critical competencies in the surgical instrument market.

Surgical Robots: More Players, More Tracks

In addition to the sectors of vascular interventional and surgical instruments, surgical robotics has also emerged as a hot field this year. Due to high technical barriers and lengthy R&D cycles, the development of domestically produced surgical robots in China has remained in its early stages.

This year, Tinavi Medical Technologies Co., Ltd., a company specializing in orthopedic surgical robots, listed on the STAR Market, boosting market confidence in the surgical robotics industry.

The market landscape for surgical robots has long been dominated by Intuitive Surgical, with numerous companies continually challenging its position.In 2020, the surgical robotics sector exhibited new characteristics: an increase in market participants and a broadening of the competitive landscape.

The widening of the track refers to the expansion of disease indications and surgical procedures addressed by surgical robots. In the past, the segment dominated by emerging startups was primarily focused on laparoscopic surgical robots. Currently, however, companies are increasingly entering fields such as orthopedics, pulmonology, vascular intervention, and neurosurgery.

The growing number of players indicates that, in addition to startups, medical device giants are also significantly increasing their investments in the surgical robotics sector. Leveraging their strong resources and financial advantages as industry leaders, they have rapidly expanded across multiple segments of the surgical robotics market.

This year, MicroPort Scientific Corporation has made a high-profile entry into the surgical robotics sector, announcing that its subsidiary, MicroPort Surgical Robot Co., Ltd., has completed RMB 3 billion in financing. Its surgical robot product portfolio covers multiple categories, including laparoscopic surgical robots, orthopedic surgical robots, and lung biopsy robots. Internationally, medical device giants such as Medtronic, Smith & Nephew, and Stryker have also largely secured their positions in key segments of the surgical robotics market.

The remaining sectors, including rehabilitation, dentistry, and medical imaging, are evergreen fields.

The rehabilitation equipment sector stands to benefit from the broader context of healthcare cost containment. With the implementation of DRG (Diagnosis-Related Groups) policies, the rehabilitation industry is expected to usher in new development opportunities. Drawing on historical experience in the United States, after the adoption of a prospective payment system based on DRGs, total treatment costs for acute-phase rehabilitation were capped, and treatment cycles were shortened. This measure spurred a surge in demand for post-acute rehabilitation services, driving rapid growth in specialized rehabilitation hospitals. It is anticipated that rehabilitation equipment companies capable of providing empowerment and solutions to primary-care hospitals in China—which currently face a shortage of rehabilitation professionals—will be favored by the market.

As the dental sector falls under consumer healthcare and is not subject to medical insurance cost-containment measures, dental services with consumer-oriented attributes are expected to attract attention.

In reviewing the medical device sector in 2020, in addition to focusing on the primary market, developments in the secondary market were equally noteworthy.

During its interviews and research, VCBeat asked an industry insider to summarize the past year in a single word; he immediately replied, “IPO.”

With the opening of the STAR Market and the implementation of the registration-based IPO system, this year has also seen a surge in initial public offerings (IPOs) in the medical device sector. According to statistics from VCBeat, more than 15 companies in the medical device field went public this year, covering multiple segments such as high-value cardiovascular consumables, rehabilitation equipment, surgical robots, ophthalmic intraocular lenses, and minimally invasive surgical instruments.

In terms of listing venues, the STAR Market has the highest number of listed medical device companies, followed by the Hong Kong Stock Exchange. The market capitalization of these listed companies is generally around RMB 10 billion to RMB 20 billion. Only two companies, Contec Medical Systems and Winner Medical, have a market capitalization exceeding RMB 50 billion. Based on this trend, it is predicted that more mid-tier enterprises in the medical device sector will go public in the future.

Looking at future trends, we believe that IPO listings will exhibit the following major trends.

First, the distinction between primary and secondary market investments will become increasingly blurred. Meanwhile, in the future, going public will merely mark the beginning, with post-IPO companies likely experiencing a Pareto distribution where the top 20% outperform the remaining 80%.

The primary driver behind the integration of the primary and secondary markets is the introduction of policies such as the Hong Kong Stock Exchange’s biotech listing chapter, the STAR Market, and the registration-based IPO system on the ChiNext Board, which have streamlined exit channels.

This means the gap between the primary and secondary markets has narrowed significantly. Previously, it typically took institutional investors 3–4 years after a primary-market investment for a company to go public; now, this timeline is measured in months. The overall time to listing has been shortened, while overall valuation expectations have risen, necessitating larger capital raises in the primary market.

In the medical device sector, large-scale clinical adoption is no longer a prerequisite for market launch; companies can go public even before completing commercialization. Previously, a company’s listing and initial public offering (IPO) were often regarded as hallmarks of a mature market segment, signaling that the sector had entered its next stage of development. Today, however, going public can be viewed as merely another round of financing.Going public signals that the sector is beginning to mature, yet the impact of IPOs on widening competitive gaps and solidifying tiered market structures may not be immediately apparent. As no clear market leader emerged during the pre-IPO phase, some funds have opted for a broad investment strategy.

This has also led to a situation in the primary market where well-capitalized private equity (PE) funds have adopted venture capital (VC) investment strategies, casting a wide net during the pre-IPO stage and thereby overturning some traditional PE investment philosophies.

This also means that for medical device companies, going public may merely mark the beginning, as they will still face a Pareto distribution (80/20 rule) post-listing.

Hillhouse Capital stated: While the ability to go from 0 to 1 is key to success in the innovative drug sector, it is the comprehensive, end-to-end capability that determines the future trajectory in the medical device industry. Although R&D and innovation capabilities are vital for medical devices, strong manufacturing, operational, and commercialization capabilities are equally critical for device companies. Therefore, identifying entrepreneurial teams with a grand vision and discovering robust business models constitute one of the core investment logics in the medical device sector.

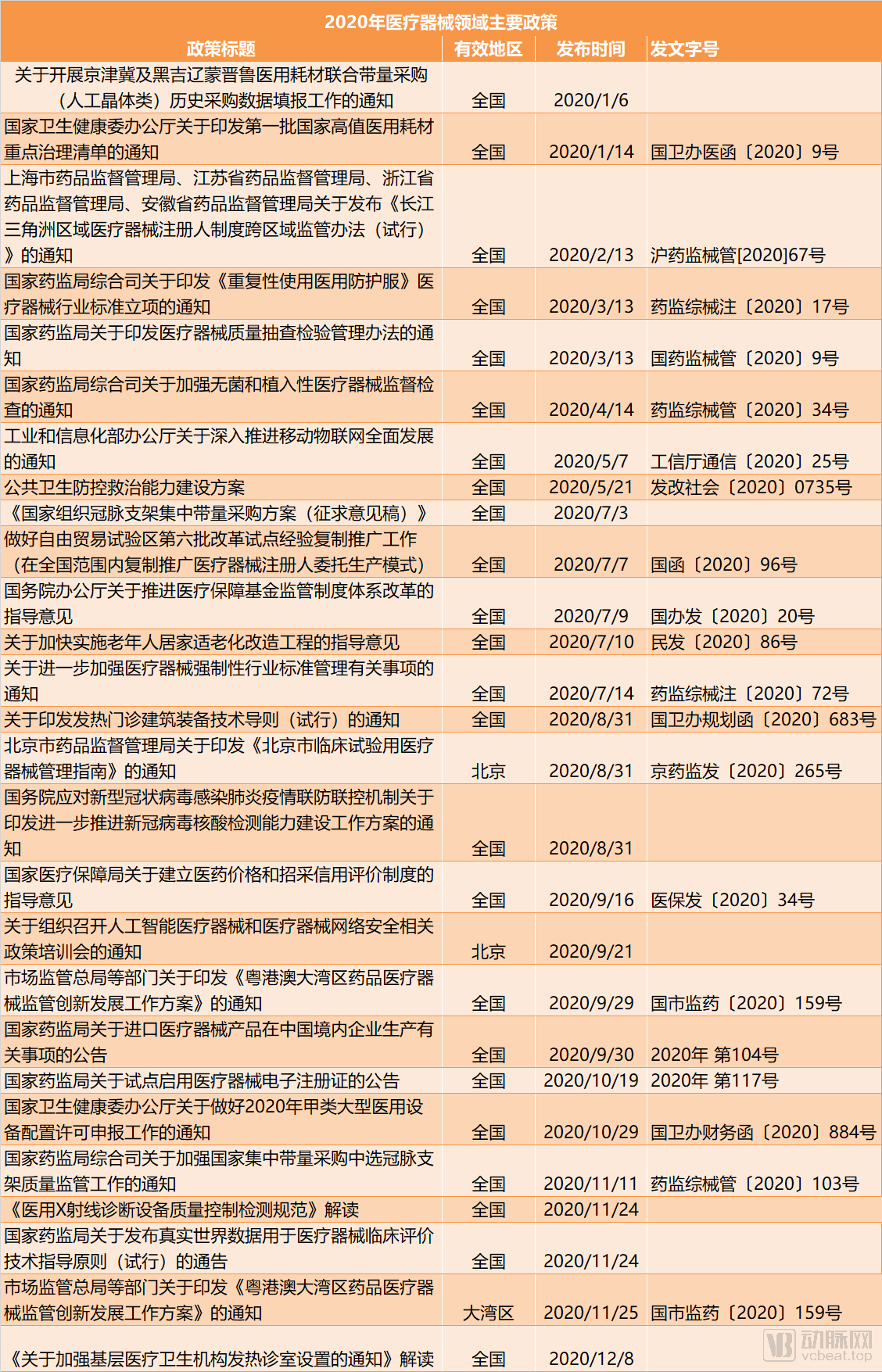

In 2020, several major policies were introduced in the medical device sector. VCBeat broadly categorizes these policies into four groups:The first category pertains to review and approval.The use of real-world data in the clinical evaluation of medical devices, the nationwide rollout of the marketing authorization holder (MAH) system for medical devices, and the introduction of policies allowing medical institutions in mainland cities of the Guangdong-Hong Kong-Macao Greater Bay Area to use drugs and medical devices approved in Hong Kong and Macao by 2022 have further streamlined the approval pathway for innovative medical devices.

VCBeat believes that the most important factor is the Medical Device Registrant System, which decouples medical device registration from production, thereby lowering the entry barrier for the medical device industry.Capital, entrepreneurs, and social resources can enter the medical device industry more easily under the Medical Device Registrant System. This not only expands the market size of the medical device industry but also enhances resource utilization efficiency.

Next is the use of real-world data for the clinical evaluation of medical devices. In March 2020, the first medical device product in China to be approved for market entry using real-world data from the Boao Lecheng International Medical Tourism Pilot Zone was Allergan’s “Glaucoma Drainage Device.”

On November 24, the National Medical Products Administration (NMPA) released the “Technical Guidelines for the Use of Real-World Data in Clinical Evaluation of Medical Devices (Trial),” which clarifies that real-world evidence derived from real-world data collected in countries or regions where the medical device is already marketed may serve as a supplement to existing clinical evidence to support registration applications in China.

In addition to supporting product registration and supplementing existing evidence, common scenarios in which real-world evidence may be considered for the clinical evaluation of medical devices include: providing clinical evidence within the pathway for clinical evaluation of equivalent devices;

Real-world data generated from the special domestic use of urgently needed imported medical devices can be used to support product registration as a supplement to existing evidence; serve as an external control for single-arm trials; provide clinical data for establishing single-arm target values; support modifications to the scope of application, indications, and contraindications; support revisions to the clinical value of the product in the package insert; support post-marketing studies for conditionally approved products; facilitate full-lifecycle clinical evaluation of medical devices used to treat rare diseases, thereby accelerating their market entry to meet patient needs; and support post-marketing surveillance.

Real-world evidence refers to clinical evidence regarding the use, risks, and benefits of medical devices, generated by analyzing real-world data, which may serve as valid scientific evidence for regulatory decision-making. Due to the diverse sources of real-world data, data quality may vary significantly; therefore, not all real-world data can yield valid real-world evidence.

Real-world data requiresRepresentativeness(The population covered by the data encompasses the study's target population),Completeness, accuracy, authenticity, consistency, and reproducibility.

The second category is new infrastructure., including new requirements for age-friendly renovations, the enhancement of primary healthcare service capabilities, and the strengthening of public health prevention and control capacities, have injected new growth momentum into the medical device industry.

The third category is regulatory-related policies., from electronic registration certificates, interpretation of various product standards and specifications, to strengthened sampling inspections and regulatory oversight, the medical device regulatory system is evolving toward greater stringency, comprehensiveness, and digitalization.

The fourth category comprises healthcare insurance-related policies, with the national volume-based procurement policy and subsequent regulatory oversight emerging as the most significant policies introduced this year.

The most impactful policy on the medical device sector this year has been the implementation of volume-based procurement, which has sent shockwaves through the entire medical device market.

In fact, volume-based procurement is not an isolated policy; it represents the National Healthcare Security Administration's determination to control costs.

Hu Minjie, Executive Director of China Merit Capital, stated, “The volume-based procurement policy is, in essence, implemented in synergy with a series of other measures, including DRG payment reforms and the acceleration of regulatory review and approval processes. Its implementation signifies that the healthcare market has entered an era of cost containment.” This shift will impact all aspects of the medical device industry, including business models, product R&D, and marketing and sales.

It is anticipated that the products subject to volume-based procurement will be those with abundant supply options and marginal sales, thereby enhancing healthcare accessibility without increasing the financial burden on the medical insurance system.

From an impact perspective, we believe that volume-based procurement will first compel companies to expand their product portfolios and innovate through iterative product development, while the future profit margins for single, homogeneous products will be significantly compressed.

It is foreseeable that, in the future, accelerating R&D innovation and building differentiated advantages will become the norm for the survival of medical device companies amidst fierce competition.

Hillhouse told VCBeat, “With the implementation of volume-based procurement for medical devices, industry turbulence is inevitable. In the short term, the impact on the sector is significant; however, in the long run, centralized procurement encourages medical device companies to focus more on genuine innovation. Driven by innovation, cost control, and quality competition, this approach better promotes the development of the pharmaceutical and healthcare industry, enabling innovative companies with true clinical value to capture larger market shares.”The following three dimensions may offer greater opportunities: first, enterprises with strong innovation capabilities that can provide multi-dimensional support; second, products that continuously meet the substantial demands of the population; and third, manufacturing upgrades driven by the engineer dividend.”

In addition to spurring innovation, under the pressure of volume-based procurement, offsetting domestic VBP impacts with overseas sales will become a trend.

Take surgical staplers, a product category on the verge of nationwide volume-based procurement (VBP), as an example. China has numerous surgical stapler manufacturers, predominantly concentrated in the mid-to-low-end market segment. Prior to the implementation of the VBP policy, Chinese surgical stapler manufacturers had already begun expanding into overseas markets, with Brazil, the United Kingdom, and Italy ranking as the top three export destinations for Chinese surgical staplers. In this product category, the top three Chinese brands by export volume in 2019 were Pert, Tianchen, and Rich.

It is anticipated that the normalization of the volume-based procurement (VBP) policy will accelerate the expansion of domestic medical device enterprises into overseas markets. Products that are simple to operate, ready-to-use, and have a short learning curve for physicians hold a competitive advantage in global market entry.

2020 was a tumultuous year, presenting numerous challenges to the medical device industry, from the pandemic in the first half of the year to volume-based procurement in the second half. However, overcoming these challenges is merely a small step forward on the path to advancing the medical device sector.

Currently, the overall penetration rate of medical devices in China is relatively low, their utilization relative to pharmaceuticals is insufficient, and the product portfolio remains skewed toward the low end, indicating substantial room for development and improvement.

Finally, according to the Blue Book of Medical Devices: Report on the Development of China’s Medical Device Industry (2019), more than 90% of medical device manufacturers in China are small and medium-sized enterprises, with an average annual main business revenue of RMB 30–40 million. This figure reveals a substantial gap compared to the average annual main business revenue of RMB 300–400 million for enterprises in China’s pharmaceutical industry.

Flowing water does not compete to be first; it strives for ceaseless continuity. In an era where industry rules are constantly being redefined, maintaining rationality is key. Only through innovation can one protect oneself from being eliminated by new rules and emerge as a survivor after the great sift of these changing standards.