Cancer Early Screening Industry Enters Harvest Phase with 11 Financing Rounds Exceeding 100 Million RMB in 2020

In 2020, the cancer early screening market experienced leapfrog development. Several companies, including New Horizon Health, ClearMed Biotech, and Genetron Health, secured individual financing rounds exceeding RMB 100 million. Fanta Genetics and Burning Rock Biotech, both heavily invested in the cancer early screening sector, successfully listed on the NASDAQ. Illumina acquired Grail for $8 billion, and China’s first Class III medical device certification for a genetic testing-based cancer early screening product was issued. These significant events, clustered in 2020, signaled that cancer early screening had become an industry hotspot, transitioning from the R&D phase to commercialization, with companies entering a harvest period.

VCBeat has compiled and summarized the changes in core elements of the cancer early screening market in 2020, including investment and financing data, products, technologies, and business models, yielding the following insights:

1. A surge of capital is flooding into the cancer early screening sector, with 10 financing rounds exceeding RMB 100 million; investment will increasingly concentrate on leading enterprises.

2. Leading companies enter the IPO phase, with two precision oncology firms moving toward public listing; New Horizon Health has filed its prospectus on the Hong Kong Stock Exchange, poised to become the first publicly listed genetic testing company whose core revenue stream is derived from early cancer screening.

3. The First Gene Testing-Based Cancer Early Screening Registration Certificate Is Issued; Compliance Will Become the Market Mainstream, and Companies Must Prioritize Product Registration Efforts;

4. An increase in large-scale prospective studies, with further maturation of the industry;

5. ctDNA is a prominent biomarker for early cancer screening at present, and multi-omics will play a significant role in the context of early cancer detection;

6. Health examination centers are a critical sales channel for early cancer screening products at this stage, and the influence of key opinion leaders should be prioritized.

Cancer early screening products are used for the early detection and warning of cancer in its initial stages or precancerous lesions. Early screening, along with early diagnosis and treatment, remains the most effective method to reduce mortality rates.

In a broad sense, early cancer screening spans multiple disciplines, including radiology and pathology, with diverse examination methods such as cytological testing, imaging studies, endoscopy, tissue biopsy, and liquid biopsy. This article focuses solely on early cancer screening based on genetic testing and liquid biopsy technologies.

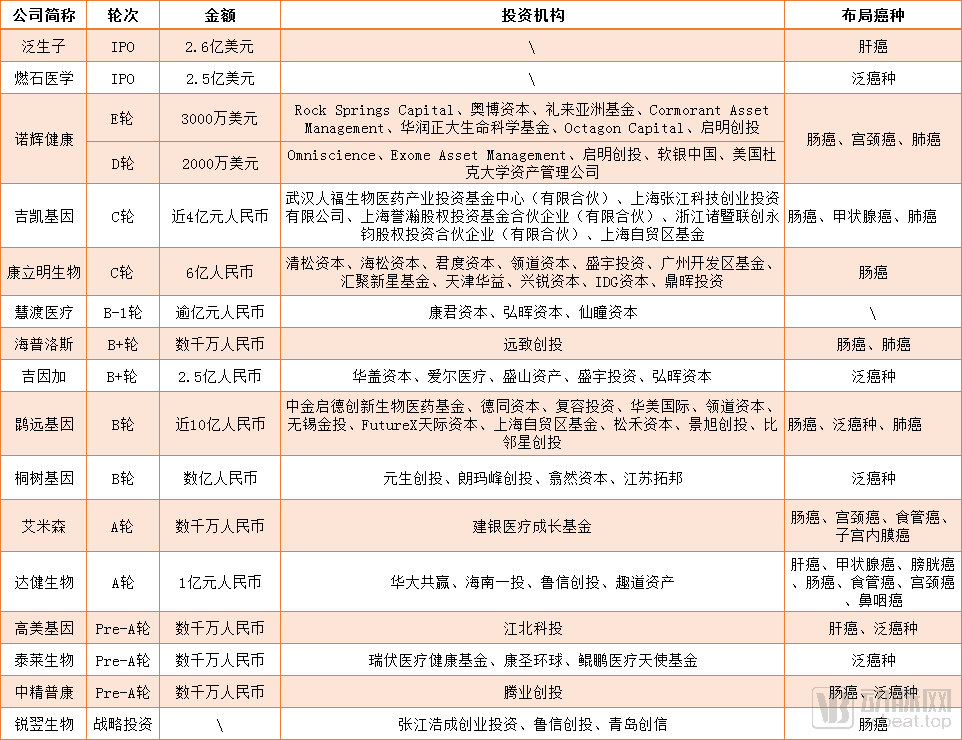

VCBeat compiled statistics on investment and financing in the cancer early screening market from January 2020 to December 2020. A total of 16 companies with clear business layouts in early screening completed 17 financing rounds, with a cumulative amount of approximately RMB 6.3 billion (calculation rules: exchange rate conversion based on USD 1 = RMB 6.57; amounts described as “tens of millions” are calculated as RMB 10 million; amounts described as “hundreds of millions” or “over one hundred million” are calculated as RMB 100 million).

List of Financing Data in the 2020 Cancer Early Screening Market (Source: VCBeat)

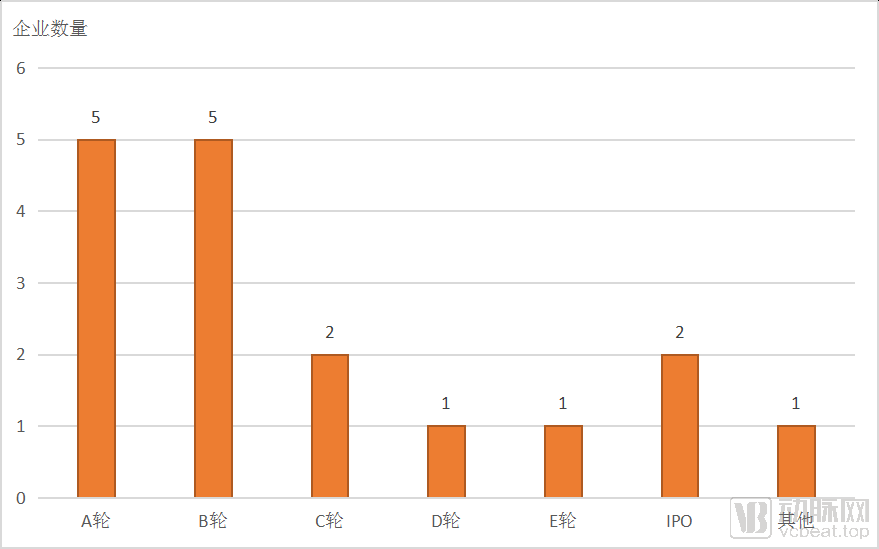

This year, a significant influx of capital has poured into the cancer early screening sector. Among the 16 companies that secured financing, 10 raised over RMB 100 million in single rounds, with some achieving this milestone as early as their Series A or B rounds, underscoring the strong investor confidence in this field. Notably, New Horizon Health completed two financing rounds exceeding RMB 100 million each within a single year, earning it the title of “Financing King” in the cancer early screening niche for 2020. Going forward, capital is expected to increasingly concentrate on leading enterprises. Five other companies raised funds in the range of tens of millions of RMB, all at early-stage financing rounds.

From the perspective of funding rounds, the cancer early screening sector was dominated by Series A and Series B financings in 2020, indicating that the industry still has substantial room for growth.

Listed companies include Burning Rock Biotech and Genetron Health, both of which are precision oncology firms with business lines covering early cancer screening and diagnosis, treatment, and full-cycle care. However, early cancer screening has not yet become a core revenue source for either company. Recently, both companies released their Q3 2020 quarterly reports.

In the third quarter of 2020, Burning Rock Biotech achieved sales revenue of RMB 124 million, representing year-on-year and quarter-on-quarter growth of 19.4% and 15.8%, respectively. The central laboratory model (sample collection model) remained the primary source of revenue for Burning Rock, accounting for 73% of total income, with both year-on-year and quarter-on-quarter growth rates exceeding 20%.

Genetron Health’s sales revenue in the third quarter of 2020 increased by 37.6% year-over-year and 10.1% quarter-over-quarter, reaching RMB 110 million. The company’s business is divided into three segments: IVD, LDT, and research services, which accounted for 26.9%, 63.8%, and 9.3% of revenue, respectively. Among these, the IVD segment achieved the fastest year-over-year growth in Q3, with year-over-year and quarter-over-quarter increases of 217.3% and 65.9%, respectively, primarily driven by sales growth of the GenetronS5 sequencer and the Lung 8 Assay.

Meanwhile, both Burning Rock Biotech and Genetron Health place significant emphasis on advancing their cancer early screening programs.

In November, Burning Rock Biotech announced the latest data on its DNA methylation-based early cancer screening technology, ELSA-seq. In a study involving early-stage samples for six types of cancer (lung cancer, colorectal cancer, liver cancer, ovarian cancer, pancreatic cancer, and esophageal cancer), ELSA-seq achieved approximately 98% specificity and 81% sensitivity. Additionally, Burning Rock plans to launch a pan-cancer early screening product in the future that covers nine cancer types (adding gastric cancer, hepatobiliary cancer, and head and neck cancer).

Genetron Health has strategically focused on early screening for liver cancer. In September, its liquid biopsy product for early detection of hepatocellular carcinoma, HCCscreen™, which is based on next-generation sequencing (NGS) technology, was granted “Breakthrough Device” designation by the U.S. Food and Drug Administration (FDA). Data show that HCCscreen maintains a sensitivity of over 93% while achieving a specificity of 98%.

It is also worth noting that in November, New Horizon Health filed a listing application with the Hong Kong Stock Exchange, paving the way for China’s first publicly listed genetic testing company whose core revenue stream is derived from early cancer screening.

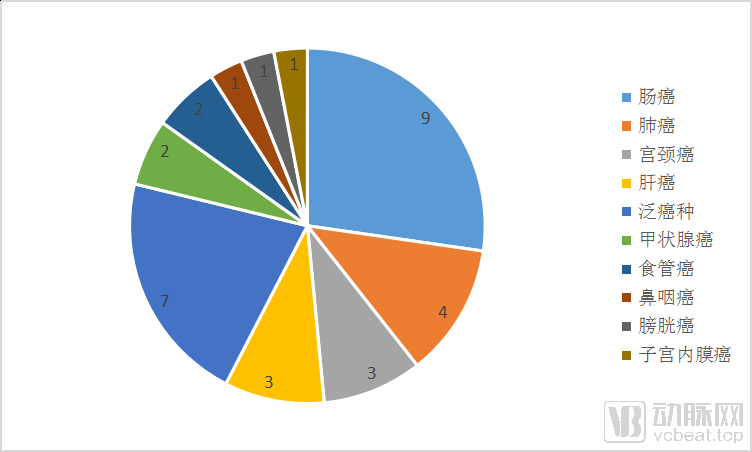

From the perspective of cancer types targeted by 16 companies, early screening for colorectal cancer remains a hot investment track, with nine companies focusing on colorectal cancer early screening securing financing. New Horizon Health, ClearMed Biotech, and Genetron Health, all long-established players in the colorectal cancer early screening market, secured substantial funding this year. In addition, GeneChem, which officially announced its entry into the cancer early screening market in September, also chose colorectal cancer as its entry point. Similarly, GeneChem has attracted significant capital interest, completing a Series C financing round of nearly RMB 400 million.

Cervical cancer, liver cancer, and lung cancer also attract significant attention. Colorectal, cervical, liver, and lung cancers all share three characteristics: high incidence rates, high early-stage cure rates, and certain limitations in existing screening methods. Consequently, companies that focus on cancer types with substantial demand, potential for clinical intervention, and the ability to develop products superior to current solutions are more favored by capital markets and can quickly secure a competitive advantage.

Furthermore, pan-cancer screening has emerged as a focal point for capital investment, with seven companies specializing in pan-cancer early screening securing funding this year. Unlike single-cancer screening, which primarily targets high-risk populations, pan-cancer early screening is mainly directed at healthy individuals and enables the simultaneous detection of multiple cancer types. In the face of the still severe challenges in cancer prevention and control, pan-cancer early screening complements single-cancer early screening, serving as a powerful tool to reduce both cancer incidence and mortality rates.

In 2020, early cancer screening products achieved a major breakthrough with the issuance of China’s first registration certificate for genetic testing-based early cancer screening. In November, Colotect Plus, the colorectal cancer early screening product developed by New Horizon Health, officially received an Innovative Class III Medical Device Registration Certificate from the National Medical Products Administration (NMPA), marking the “first certificate” in the field of genetic testing for early cancer screening.

Previously, all industry-approved products were cleared for “auxiliary diagnosis” only; they could not be used independently or serve as the basis for early diagnosis or definitive diagnosis of cancer. Instead, they provided supportive evidence to assist clinicians in evaluating patients with suspected colorectal cancer symptoms, thereby aiding differential diagnosis. In contrast, Changweiqing is intended for screening high-risk individuals aged 40–74 years, including those at elevated risk for colorectal cancer but without clinical symptoms, to distinguish healthy individuals from those who may have colorectal cancer or advanced adenomas, thereby identifying occult cases.

Cancer Early Screening Products Approved in China (Data Source: Official Website of the National Medical Products Administration)

According to VCBeat statistics, as of 2020, a total of seven early cancer screening and diagnostic products in China had obtained Class III medical device registration certificates. These products were developed by five companies: Bo’ercheng, ClearMed Biotech, New Horizon Health, Jinbaihui Biotechnology, Weizhen Biotechnology, and Perseus LifeScience. Among the approved products, the vast majority remain colorectal cancer screening assays. It is anticipated that a wider variety of early cancer screening products will receive approval in the future.

Notably, Borui Cheng’s colorectal cancer early screening product, Si Bo Ding, was approved in 2015, making it the first cancer auxiliary diagnostic product to receive approval in China. In April this year, its gastric cancer early detection product, Si Bo Wei, also obtained approval from the National Medical Products Administration (NMPA). Reportedly, Si Bo Wei demonstrates a sensitivity of 61.76% and a specificity of 85.07% for gastric cancer detection, with an early-stage gastric cancer detection rate 5–10 times higher than that of traditional tumor markers.

Furthermore, numerous companies have also achieved breakthroughs in their cancer early screening products this year.

In August, Herui Gene launched its first early liver cancer screening product based on the PreCar study, named Laisining. Designed and developed to fully meet clinical needs, this product can not only detect subtle molecular biological differences between patients with cirrhosis and those with liver cancer 6 to 12 months earlier than the traditional gold standard, but also monitor liver cancer recurrence, providing precise postoperative dynamic monitoring for patients and effectively extending their survival time.

It is also worth noting that, in recent years, cancer early screening companies have placed significant emphasis on conducting large-scale prospective studies.

In July, Genetron Health published large-scale clinical data on pan-cancer early screening in the prestigious international journal Nature Communications, demonstrating that the PanSeer® assay can detect trace ctDNA methylation signals for five types of cancer up to four years earlier than clinical diagnosis.

In September, New Horizon Health announced key results from its Clear-C trial, a large-scale, prospective, multicenter, registrational clinical study for early cancer screening. The data demonstrated that Changweiqing® achieved a sensitivity of 95.5% for detecting colorectal cancer, compared with 69.8% for the fecal immunochemical test (FIT). Changweiqing® helps alert clinicians to patients’ risk of colorectal cancer and improves patient adherence to follow-up colonoscopy for confirmation.

In November, ClearMed Biotech announced the launch of the “Early Screening Project for Colorectal Cancer in China’s Health Checkup Population—A Multicenter Study on the Application of SDC2 Gene Methylation Technology for Colorectal Cancer Screening.” This signals that ClearMed Biotech is poised to proceed with its application for regulatory approval of its colorectal cancer early screening test.

Genetron Health initiated a prospective, multicenter study in 2019 on its early liver cancer screening product, targeting 4,500 HBsAg-positive individuals. To date, over 2,000 participants have been tested. Preliminary results from 297 subjects demonstrated sensitivity, specificity, positive predictive value (PPV), and negative predictive value (NPV) of 92%, 93%, 35%, and 99.6%, respectively. The company plans to launch the second cohort of 2,500 participants for HCCscreen screening in the first half of 2021, which will serve as the registration study for future approval in China.

Prospective, multicenter studies for early cancer screening products involve large cohort sizes, long follow-up periods, and high costs, placing substantial demands on the cash reserves and financing capabilities of early cancer screening companies. Taking Grail as an example, its research initiatives have enrolled at least several thousand patients, with the STRIVE study reaching a scale of hundreds of thousands of participants. These studies require long-term follow-up of enrolled patients. According to published reports, conducting such large-scale clinical trials requires approximately $1 billion in funding, reflecting their prohibitively high costs.

However, prospective, large-scale clinical studies are an indispensable prerequisite for cancer early screening products to obtain regulatory approval. It is anticipated that an increasing number of enterprises will conduct prospective clinical trials for their cancer early screening products. This trend also indicates that compliance will undoubtedly become the mainstream standard for cancer early screening products, and companies must prioritize the regulatory registration process.

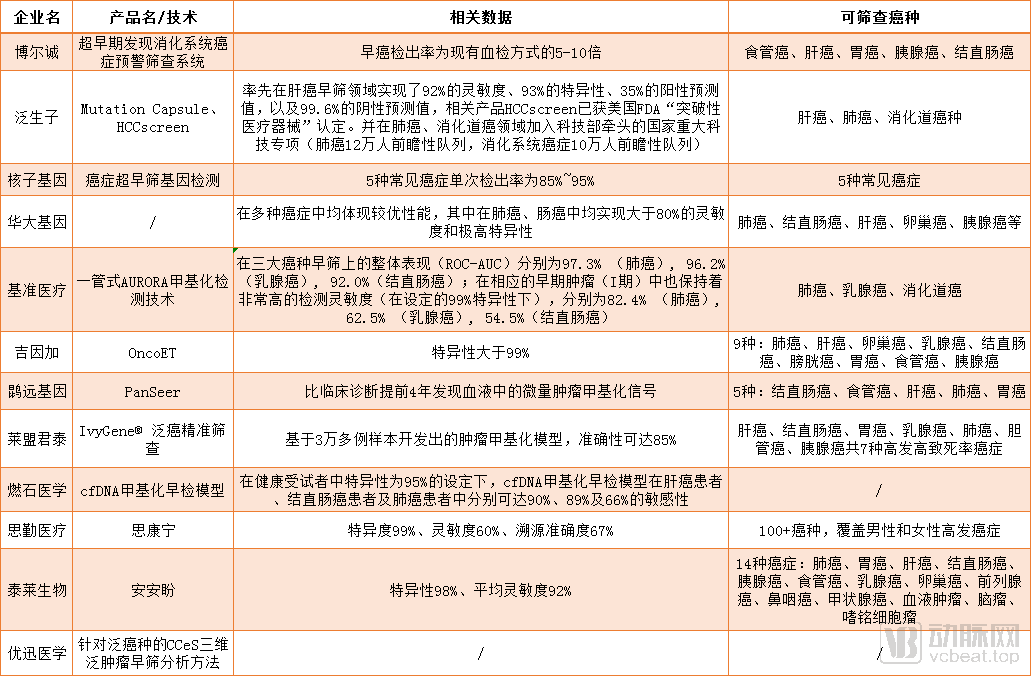

In 2020, Chinese companies also achieved significant results in pan-cancer early screening products.

Early cancer screening was a business highlight for Huirui Gene in 2020. In addition to the early screening for liver cancer mentioned above, Huirui Gene is also deploying pan-cancer early screening. At the 2020 CSCO Annual Meeting, Huirui Gene unveiled its roadmap for multi-cancer early screening and diagnosis for the first time: within three to five years, the company aims to deliver research findings on early screening and diagnosis for 5 to 8 types of high-risk, high-incidence cancers in China, and to achieve their industrial commercialization.

Domestic Companies Deploying Pan-Cancer Early Screening (Source: Artery Orange)

Compared with using a single blood sample to screen for multiple types of cancer, the advantages of using a single blood sample to screen for a single type of cancer are no longer significant. Pan-cancer screening is inevitably the future trend of blood tests. However, screening for multiple types of cancer requires companies to have large-scale databases and analytical capabilities. In addition, early screening for a single type of cancer generally adopts the fluorescent PCR method. This technical route has low costs, and the PCR method is sufficient for detecting several or dozens of sites. However, early screening for multiple types of cancer requires a wide range of gene detection, requiring large-panel testing of multiple genes and multiple sites, thus resulting in higher costs.

Moreover, the relationship between cancer and genes is highly complex. Multi-cancer detection requires resolving the issue of tumor origin; if the primary site of the cancer cannot be determined, a positive detection result is clinically insignificant, as individualized diagnostic workups would still be necessary.

Therefore, although there is significant attention on pan-cancer early screening, its development pace is slower than that of single-cancer early screening products due to limitations in technical complexity, analytical capabilities, databases, and costs. Currently, no pan-cancer early screening products have been approved in China, and few have entered the market as Laboratory Developed Tests (LDTs); thus, further time is required for maturation.

Tumor markers are a class of biochemical substances synthesized and secreted by tumor tissue cells, indicating the presence and progression of tumors in the body and reflecting certain biological characteristics. Recently, research on liquid biopsy markers commonly used for early cancer screening—such as circulating tumor DNA (ctDNA), circulating tumor cells (CTCs), microRNA (miRNA), and exosomes—has advanced rapidly. These markers enable the early detection of subtle signs of cancer and have become a key direction in the development of novel tumor markers.

ctDNA refers to DNA fragments released into the bloodstream through tumor cell necrosis, apoptosis, or normal secretion. Carrying cancer-associated genetic variant information, ctDNA can be detected when molecular alterations occur in tumors, thereby enabling early cancer detection. Consequently, ctDNA has become a focal point of research in the field of early cancer screening, with relatively mature technological development. Industry giant Grail achieves multi-cancer early screening by detecting ctDNA levels in the blood.

However, ctDNA degrades rapidly and is present in low abundance; in particular, patients with brain cancer, kidney cancer, and other malignancies exhibit even lower circulating tumor DNA levels in their blood compared to those with other cancer types. Consequently, high-sensitivity detection is required, and the technology continues to require ongoing advancement and refinement.

miRNA is an emerging star in the field of early cancer screening. As regulatory molecules involved in gene expression and protein translation, miRNAs play a pivotal role in the initiation and progression of tumors, enabling early diagnosis of cancers, cardiovascular diseases, and other conditions. This year, Zhanxing Biotechnology launched its independently developed ultra-early miRNA tumor screening kit. This product can be used for early screening of various cancers, providing an accurate and highly sensitive detection method for early cancer screening.

Circulating tumor cells (CTCs) are cancer cells that detach from the primary tumor, either spontaneously or due to diagnostic and therapeutic procedures, and invade the peripheral blood circulation. Theoretically, CTCs offer high specificity and can be used for early cancer screening. However, their concentration in the blood of patients with early-stage cancer is extremely low, resulting in lower sensitivity compared to circulating tumor DNA (ctDNA). Furthermore, in the sequence of cancer progression, ctDNA is typically detected before CTCs. Therefore, CTCs do not present a significant advantage for early screening; at present, they are primarily used to guide clinical treatment and assess prognosis.

Whether CTCs can become a powerful tool for early cancer screening remains to be validated over time, and researchers are currently conducting related studies. In February this year, Canadian biotechnology company Cellular Analytics released its latest research findings, demonstrating that liquid biopsy-based CTC detection can more effectively identify early-stage mesothelioma.

Multi-omics is also gaining attention. In January this year, Tellgen, a company specializing in multi-omics-based pan-cancer early screening, completed a Pre-A financing round worth tens of millions of yuan; in April, Zhongjing Pukang, a multi-omics cancer early screening company, also secured tens of millions of yuan in Pre-A funding; in September, Geneseeq announced its entry into the cancer early screening market, having independently developed MERCURY, a multi-omics-based tumor early screening model. This model integrates liquid biopsy, CNV analysis, methylation analysis, and the company’s proprietary NOAH algorithm, delivering significantly improved performance compared to traditional early screening technologies. Data show that in early screening for liver, colorectal, and lung cancers, the MERCURY model achieves a sensitivity of 80%–95% at a specificity of 98%.

Multi-omics is a novel biological analytical approach that enables the targeted provision of screening products with optimal efficacy, tailored to the distinct developmental stages of various cancers and specific population characteristics. Its fundamental methodology leverages extensive multi-dimensional molecular data across diverse biological processes—including genomics, transcriptomics, epigenomics, proteomics, metabolomics, and microbiomics. By employing bioinformatics, statistical analysis, computational biology, and machine learning, this approach facilitates high-level analysis and interpretation of complex biological phenomena influenced by numerous factors, such as life processes and disease mechanisms.

Multi-omics testing comprehensively considers the impact of factors such as genetic mutations, gut microbiota, and diet on the onset and progression of cancer. By integrating multi-dimensional, massive datasets, it provides more suitable and precise solutions for early cancer screening. As the era of multi-omics is just beginning, it is poised to play a pivotal role in scenarios such as early cancer detection and medication guidance in the future.

For cancer early screening companies, channel capability is indispensable. Sales channels for cancer early screening products include health checkup centers, hospitals, insurance companies, and e-commerce platforms.

Commercial Health Checkup Providers: As a critical component of health management, cancer early screening products are well-suited for health checkup scenarios. Health checkup centers serve as important sales channels for New Horizon Health, which has partnered with multiple providers, including iKang Guobin, to incorporate its products into checkup packages. On iKang Guobin’s Tmall flagship store, a promotion is currently offered: “Receive a complimentary Changweiqing test for actual payments exceeding RMB 1,500.”

Hospitals: At the current stage, market education for cancer early screening remains limited, with most consumers still associating cancer testing primarily with hospital settings. Expanding product coverage across hospitals, strengthening physician education, and enhancing clinical recognition play a crucial role in promoting the adoption of cancer early screening products.

Insurance Companies: Early screening can significantly reduce medical costs. By partnering with insurance companies to provide cancer early-screening products for their policyholders, insurers can monitor the health status of the insured while promoting cancer screening, thereby achieving substantial synergies.

E-commerce Platforms: A key characteristic of cancer early screening products is their high degree of internet integration; cancer early screening products from ConliMed and New Horizon Health are both available for purchase on e-commerce platforms.

This year, early cancer screening products have also jumped on the bandwagon of e-commerce live streaming, attempting to promote their offerings through collaborations with key opinion leaders (KOLs) and celebrities. In November, Kangliming Biology partnered with Wang Feng to promote its product, Chang’anxin, in a live-streaming session.

Currently, due to the lack of a systematically established awareness of early cancer screening and low levels of market education, early cancer screening products remain primarily concentrated in health checkup centers and hospitals.

In summary, early cancer screening is widely recognized as a blue-ocean market. PwC predicts that the next five years will mark a critical period of rapid growth and industry consolidation in this field, giving rise to numerous standout companies and commercial opportunities. Going forward, industry concentration is expected to gradually increase, and with advancing technological maturity and a growing number of commercialized products, early cancer screening will continue to experience robust development for some time.