Market Growth Halved and Regulatory Pressure Intensifying: Where Is the Aesthetic Medicine Industry Headed? | 2020 Year-End Review

Compared with the capital frenzy triggered by the wave of IPOs among numerous star medical aesthetics companies in 2019, the medical aesthetics industry in 2020 appeared significantly more subdued and fraught with challenges.

First,Due to the sudden outbreak of COVID-19, the market growth rate of the medical aesthetics industry has slowed down significantly this year.According to data on China’s medical aesthetics services market released by the renowned research firm Frost & Sullivan, the overall growth rate of China’s medical aesthetics services industry in 2020 is projected to narrow significantly to 5.7% due to the impact of the pandemic, a figure far below the 18% industry growth rate recorded in 2019.

Furthermore,Stringent Regulation of the Medical Aesthetics Industry Arrives in Succession This YearIn April, eight national ministries and commissions jointly issued the “Notice on Further Strengthening Comprehensive Supervision and Law Enforcement in Medical Aesthetics,” clarifying that medical aesthetics advertisements fall under the category of medical advertisements, and non-medical institutions are prohibited from publishing medical advertisements. In July, the State Administration for Market Regulation released the “Guidance on Strengthening Supervision of Online Live-Streaming Marketing Activities (Draft for Comments),” explicitly stipulating that advertisements for medical services, pharmaceuticals, and medical devices shall not be disseminated through online live-streaming platforms…

Affected by the above factors,This year, many medical aesthetics institutions have fallen into difficulties or even gone out of business.. Behind this, apart from the sharp decline in customer traffic caused by the pandemic as an incidental event,The deeper reason lies in the long-standing operational and management problems plaguing the medical aesthetics industry.. According to the "2020 White Paper on Insights into China's Medical Aesthetics Industry," there are approximately 13,000 institutions in China qualified to provide medical aesthetic services, while the number of illegally operated medical aesthetic establishments exceeds 80,000.Legitimate medical aesthetic institutions account for only 14% of the industry.. Moreover, even among licensed medical aesthetic institutions, 15% still engage in out-of-scope operations.

Crisis and opportunity always go hand in hand.. In the later stages of the pandemic, medical aesthetics-related technologies and service scenarios began to undergo iteration,The Online Transformation of Medical Aesthetic Institutions Is Accelerating. As policies and regulations are gradually improved,The medical aesthetics industry is also moving toward standardization and healthy competition.. In this process, numerous medical aesthetic companies within the industry have actively sought transformation and explored new business ventures, while internet giants from outside the sector are also accelerating their entry, aiming to capture a share of the market.

From the perspective of the entire medical aesthetics industry chain, inUpstream, this year, China's leading hyaluronic acid company, Imeik, successfully went public, and Huadong Medicine acquired a 20% stake in a Swiss hyaluronic acid company; inMidstream, Aier Eye Hospital Group, a leading player in the medical aesthetics industry, acquired a 51% equity stake in Guangdong Hanfei; SoYoung’s internet hospital practice license was approved, marking its transition from medical aesthetics to broader healthcare services; and Lianli Ge Group entered into strategic partnerships with JD Health and Mei Daifu.Downstream, Alibaba has established China’s first “Medical Aesthetics Live Streaming Industry Demonstration Center” in Chengdu...

Changes are underway, and this isFor the medical aesthetics industry, which is still in its growth phase, the competitive landscape remains highly uncertain.Moving forward, medical aesthetics practitioners must urgently address several critical challenges: how to supply a greater volume of higher-quality medical aesthetic products and devices, how to ensure compliance in both medical quality and marketing practices, how to resolve issues of consumer trust, and how to meet the demands of the primary consumer demographics—those born in the 1990s and 2000s.

Looking back at 2020, we may find answers to these questions in the trends of the medical aesthetics industry.

Next, you will learn about:

1. The medical aesthetics industry, impacted by the pandemic and regulatory policies, is undergoing a major reshuffle, with an intensifying trend toward market concentration among leading players;

2. The upstream market demonstrates robust growth and strong profitability, with product differentiation and channel coverage emerging as core competitive factors;

3. Leading midstream medical aesthetic institutions are the first to recover, accelerating the industry's online transition;

4. Downstream traffic giants continue to deepen their strategic presence, leading to more diversified customer acquisition methods in the medical aesthetics industry.

The medical aesthetics industry has long been in a state of “ice and fire.”

On the one hand, the market continues to expand.. According to Guohai Securities’ in-depth report on the medical aesthetics industry, “A Trillion-Yuan Market, Crafting Beauty,” the compound annual growth rate (CAGR) of the market size in the medical aesthetics industry reached 28.97% from 2012 to 2019, and compared with the United States and South Korea,China's per capita spending on medical aesthetics and the penetration rate of treatments per 1,000 people still have at least fourfold growth potential.

On the other hand, net profits for mid- and downstream enterprises in the medical aesthetics industry have remained persistently sluggish.For example, Pengai Medical’s third-quarter report for fiscal year 2020 showed a net profit attributable to shareholders of the parent company of RMB -158 million, representing a significant year-on-year decline of 180.92%. Moreover,Illegal Aesthetic Medicine Is Continuously Eroding the Legitimate Medical Aesthetics Market: The “White Paper on Insights into China’s Medical Aesthetics Industry (2020)” shows that an average of approximately 100,000 people suffer injuries or disabilities each year due to illegal medical aesthetic practices, with most consumers facing difficulties in safeguarding their rights, which severely undermines consumer confidence in the industry.

In summary, the medical aesthetics industry offers substantial room for rapid market growth, thereby presenting more entrepreneurial opportunities while also entailing fiercer market competition. Against this backdrop, customer acquisition costs in the medical aesthetics sector continue to rise, a situation further exacerbated by irregular industry practices, making it persistently difficult to improve the low net profit margins of mid- and downstream enterprises. This, in turn, has madeHigh-quality investment targets in the medical aesthetics industry are relatively scarce.

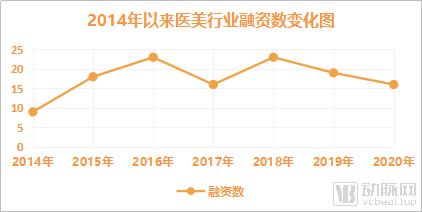

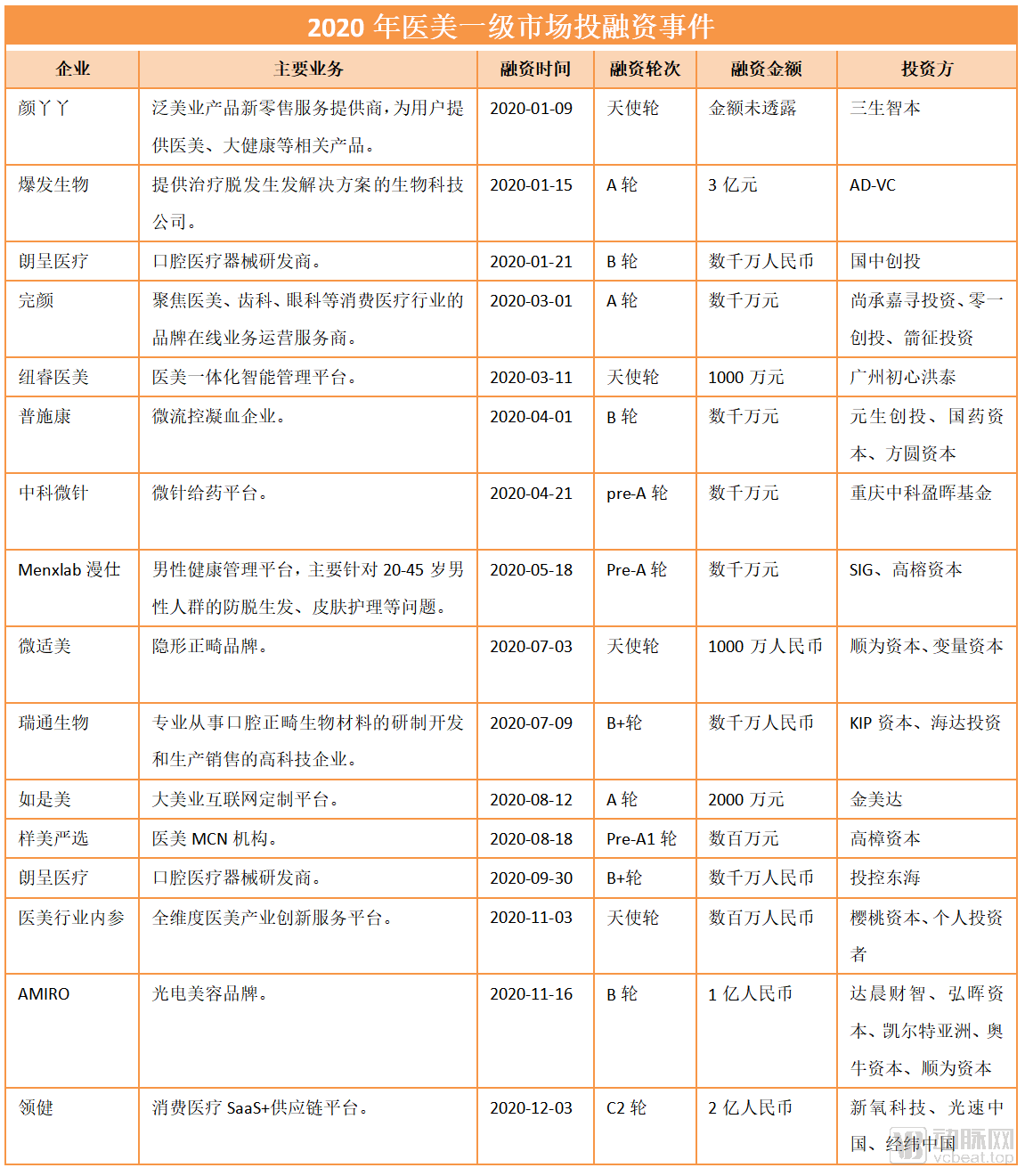

A closer look at the investment and financing performance in the primary market this year. Data from the Artery Orange database shows that as of December 14, there were 16 financing events in the medical aesthetics industry in 2020, compared with 19 in 2019 and 23 in 2018,The amount of financing has shown a downward trend year by year.. In terms of total financing amount,The total financing in the medical aesthetics industry has declined from a peak of approximately RMB 1.6 billion in 2016 to around RMB 800 million this year.

Notably,This year’s large-scale financing, similar to last year, is primarily concentrated in leading enterprises within the medical aesthetics sector that demonstrate significant high-growth potential or have already validated their business models, with a trend toward increased investment.In other words, the concentration effect among top players in the medical aesthetics industry is intensifying, and high-quality targets are not lacking in capital attention. The steady rise in the stock price of Aimeike (300896.SZ), a hyaluronic acid company, since its listing in September serves as clear evidence.

(Data source: VCBeat Orange Database; as of December 19, 2020)

Not only that,In the secondary market, mergers and acquisitions (M&A) and integration events also occur from time to time.For instance, Huadong Medicine, which has been active in the medical aesthetics sector for many years, acquired a 20% stake in the Swiss hyaluronic acid company Kylane this October; Pengai Medical Aesthetics International acquired seven clinics this year, including Guangdong Hanfei Group, Shanghai Mingyue Medical Aesthetic Clinic Co., Ltd., and Kunming Liangyan Medical Aesthetic Clinic Co., Ltd.

Large institutions continue to expand, while high-quality innovative companies in niche sectors keep securing financing.The Trend of “The Strong Get Stronger” Emerges. Meanwhile, small and medium-sized institutions were ultimately eliminated due to broken capital chains, driven by factors such as low profitability and an inability to secure financing.The Medical Aesthetics Industry Enters a Major Reshuffle“The COVID-19 pandemic this year, coupled with the frequent introduction of national regulatory policies, has accelerated this trend,” said Yang Jing from Sinopharm Capital. Institutions that collapsed amid the pandemic had long suffered from poor management; this industry consolidation will undoubtedly foster healthier development within the sector.

As a professional private equity investment firm focused on the healthcare sector, Sinopharm Capital invested in Yanshu Medical Aesthetics in 2017, co-invested in Singapore’s Vistar Medical Technology in 2019, and invested in Pushikang in 2020, demonstrating its continued optimism about the entire medical aesthetics industry. In Yang Jing’s view,The medical aesthetics industry may see new breakthroughs in the following areas。

First, leading companies are accelerating mergers and acquisitions to identify high-quality targets and expand their industrial ecosystems.With core businesses remaining stable, both vertical mergers and acquisitions to enhance supply chain synergy and horizontal mergers and acquisitions to expand market share will become key drivers for leading enterprises to continuously scale up and strengthen their core competitiveness in the future.

Second, small and medium-sized enterprises (SMEs) must identify differentiated competitive advantages amidst the industry trend where the strong grow stronger., striving to rank among the top three in the niche sector.As industry consolidation accelerates, small and medium-sized enterprises (SMEs) must carve out new paths amidst homogeneous competition, establish differentiation, and strive to become leaders in their respective sectors. This positioning will pave the way for favorable outcomes, whether through sustained financing leading to an initial public offering (IPO) or becoming attractive targets for mergers and acquisitions by larger corporations.

Third, the marketing segment will be a key focus, and companies with precise customer acquisition capabilities are likely to emerge as leaders.Customer acquisition costs in medical aesthetics marketing remain persistently high, creating an urgent market demand for enterprises capable of delivering precise customer acquisition.

In a nutshell,During the upcoming industry consolidation, the medical aesthetics sector will undergo continuous survival-of-the-fittest selection, with truly valuable enterprises gradually emerging to the forefront.In this process, enterprises of different types need to identify their respective core strengths and value propositions, achieving steady growth by securing breakthroughs in specific areas and continuously expanding their core business footprints.

This year, the upstream sector of China's medical aesthetics industry has undoubtedly been highly active.

From an industrial perspective, first, foreign products are being actively “introduced.”“This October, HUGEL’s botulinum toxin type A product, ‘Letybo,’ received approval from China’s National Medical Products Administration (NMPA), making HUGEL the fourth upstream aesthetic medicine pharmaceutical company to gain market access in China, following Allergan, Lanzhou Biological Products Institute, and France’s Ipsen. HUGEL is also partnering with Sihuan Pharmaceutical to accelerate its expansion into the domestic market. Additionally, we understand that several other European upstream brands will sequentially complete clinical trials and obtain regulatory approval in China. These developments indicate that overseas botulinum toxin brands are actively vying for market share in China, offering a glimpse into the broader growth trajectory of the upstream aesthetic medicine sector,” Mingfeng Capital told VCBeat.

Second, upstream domestic medical aesthetics companies and industrial groups are also actively “going global.”Such companies primarily establish connections with advanced technologies from overseas, particularly in Europe, to indirectly access more sophisticated R&D support abroad, thereby enriching and upgrading their proprietary product pipelines. For example, Huadong Medicine has entered into strategic collaborations with South Korea’s Jetema and Switzerland’s Kylane.

“From a capital perspective, the upstream medical aesthetics sector exhibited markedly high activity in 2020,” stated Mingfeng Capital.The listing of Imeik on the ChiNext board in September was undoubtedly one of the landmark events of this year.As of now, Imeik’s market capitalization has surpassed RMB 72 billion, with a P/E ratio of 170x. Meanwhile, Bloomage Biotech’s stock price has risen by 72.54% year-to-date, reaching a market cap of RMB 68.9 billion; Haohai Biological Technology has seen a 4.67% increase this year, with a market cap of RMB 14.3 billion. Roughly calculated,The combined market capitalization of the "big three" hyaluronic acid players in the medical aesthetics industry has approached RMB 150 billion.This largely demonstrates the capital market’s strong willingness to “pay up” for China’s upstream medical aesthetics sector.

(Stock Price Trend of Imeik After Listing Source: East Money)

“Upstream of the Medical Aesthetics IndustryUnlike sectors currently heavily impacted by centralized procurement and medical insurance policies, it itselfIt is a niche segment with weak policy correlation, featuring a favorable competitive landscape and rapidly increasing activity.. “We are actively making forward-looking strategic investments for the next 3–5 years by fully leveraging our strengths,” stated Mingfeng Capital. The upstream segment of the medical aesthetics industry has unique characteristics, which require investment firms to have an in-depth understanding of the sector. Specifically, this is mainly reflected in the following two aspects.

First, medical aesthetics exhibits a certain degree of technological overlap with many other fields; the same technology can be applied in one domain and simultaneously extended to indications within medical aesthetics.This extended technical judgment imposes high professional requirements on investors.

Secondly, in addition to the companies and technologies that have already emerged, a significant proportion of projects in the upstream segment of the medical aesthetics industry are in the mid-to-early stages of industrial commercialization; while the underlying technologies are highly mature, they requireIt will take another 3–5 years to achieve industrial commercialization, which places demands on the industry-specific capabilities of investment institutions and investors.

Of course, the variety of products in China’s regulated medical aesthetics injectables market remains relatively limited.For instance, the National Medical Products Administration (NMPA) of China has approved no more than 50 product specifications of various soft tissue fillers, whereas the Korea Food and Drug Administration (KFDA) had already approved 112 product specifications by 2015. It is important to note that a broader portfolio of pharmaceuticals and medical devices enables more comprehensive combination treatment plans for aesthetic clinics and consumers, thereby driving higher per-capita spending.

Demand is growing rapidly, while the range of available products remains relatively limited, resulting in a significant supply-demand gap across the upstream and downstream segments of the medical aesthetics pharmaceuticals and devices industry, which makesUpstream companies in the medical aesthetics industry will maintain a relatively rapid market growth rate over an extended period.According to data from Guosheng Securities, global medical aesthetics pharmaceutical and device companies have long maintained a compound annual growth rate (CAGR) of over 20%, indicating the industry’s high growth potential.

# Profitability Analysis. According to the financial reports of listed companies, in the first three quarters of 2020, as a representative of upstream enterprises in the medical aesthetics industryBloomage Biotech, Haohai Biological Technology, and Imeik all achieved positive net profit margins of 27.38%, 11.48%, and 61.51%, respectively, placing their profitability levels in the medium-to-high range.. As mentioned earlier, mid- and downstream enterprises have low net profit margins, and their profitability needs improvement.

In this process, what other opportunities for breakthroughs are available to upstream companies in the medical aesthetics industry? Mingfeng Capital has proposed four directions.

1., technically other than the existing filler materialsInnovative filler materials are highly likely to become the next explosive growth point.

Second, from the perspective of the industrial landscape, high-quality overseas technologies with exclusive leading advantages,Projects that have successfully undergone localized industrial transformation will also have opportunities for breakthroughs in the future.

Third, upstream projects with e-commerce attributes may also achieve breakthroughs in the future.The pandemic has significantly boosted e-commerce activity, with the advantages of e-commerce channels garnering increasing attention from investors. “Of the $617 million raised by Perfect Diary, 30% will be allocated to investments and mergers and acquisitions. Upstream projects with e-commerce DNA and attributes are likely to become a key focus for capital and emerge as an important future trend.”

Fourth, large industrial groups will urgently need toFill gaps in the product portfolio, which also harbors promising entrepreneurial opportunities.

In summary, from the perspective of the entire industry chain, upstream pharmaceuticals and medical devices represent the segment with the most stable investment returns in the medical aesthetics industry.For upstream manufacturers, the intensity of competition is relatively lower compared to that in the midstream and downstream sectors. However, barriers related to R&D, technology, regulatory approvals, and brand recognition are significantly higher. Moving forward, in the face of foreign products being “brought in” and domestic enterprises “going global,”China’s upstream medical aesthetics companies will find themselves on an international competitive stage, presenting significant opportunities for pharmaceutical and medical device enterprises to scale up and strengthen their market position, while also posing substantial challenges.

In this process,The core competitive advantages of pharmaceutical and medical device companies lie in product differentiation and channel coverage.Therefore,The integration of technology and capital, coupled with expanded consumer reach through channel coverage capabilities, will be a key trend for upstream medical aesthetics companies in the coming years.Based on this, we anticipate a gradual increase in financing and investment for upstream pharmaceuticals and medical devices in the medical aesthetics sector, cross-border mergers and acquisitions will emerge, and the momentum for collaboration between upstream and downstream segments of the medical aesthetics industry will strengthen.

The sudden outbreak of the novel coronavirus epidemic this year has dealt a significant blow to midstream medical aesthetic institutions. This is manifested by a shrinking incremental market, intensified price wars, a further decline in average revenue per user (ARPU), and the closure of a large number of clinics.

However, as the epidemic came under control,Midstream Companies in the Medical Aesthetics Industry Have Shown a Better-Than-Expected RecoveryPengai Medical Aesthetics International’s third-quarter financial report shows that its total revenue for the quarter reached RMB 281.3 million, representing a year-on-year increase of 18.2% and a quarter-on-quarter growth of 68.7%. Lancy Co., Ltd.’s semi-annual report indicates that its medical aesthetics business achieved operating revenue of approximately RMB 354 million, a year-on-year increase of 28.68%. Huahan Plastic Surgery’s 2020 interim report reveals that its revenue during the reporting period amounted to RMB 393 million, up 9.94% year on year……

The underlying reasons for the recovery of the medical aesthetics industry are, on one hand, due toRevenge Spending by Consumers Driven by the Pandemic, on the other hand, is due toWhile the pandemic impacted offline institutions, it also drove increased demand for online services.. From the current recovery status of the midstream segment of the medical aesthetics industry,Top-tier institutions show the strongest recovery. Behind this, in addition to the advantages that leading institutions possess in terms of technology, resources, and capital, it also includes the results of actively exploring online integration.

In specific online initiatives, each institution adopts a different approach.This August,BTL Medical Group, JD Health, and Mei Dafu, an online aesthetic medicine consultation platform, held a strategic signing ceremony in Beijing.The signing primarily leverages JD Health’s internet medical technology, United Liage’s offline medical aesthetic institution resources, and Mei Daifu’s professional physician resources. The three parties will join hands to create an “Online Plastic Surgery Hospital” and jointly build a closed-loop service ecosystem integrating internet healthcare and medical aesthetic services.

This October,Pengai Group and Meibei Reach Strategic Cooperation. According to the collaboration terms, Meibei will provide Pengai with services including brand promotion, user operations, and reputation management.

Although most institutions have emphasized the importance of digitalization, few have provided detailed discussions on how to effectively implement it. By analyzing the digital strategies of multiple institutions and data outcomes from medical aesthetics internet platforms, we have identified several key directions.

First, it is important to clarify that the midstream segment of the medical aesthetics industry, categorized by hospital ownership, includes public hospitals and private hospitals. Private hospitals dominate in cosmetic surgical procedures, while public hospitals focus more on reconstructive surgery for trauma repair. Among them,Private institutions account for nearly 80% of the total market share., dominating the landscape. Therefore, discussions on the digital transformation of medical aesthetic institutions primarily focus on private entities.

Next, as companies of different sizes possess varying capabilities, the methods they adopt will also differ. BelowThe midstream medical aesthetics sector is broadly categorized into three types of institutions: large, medium, and small. These are respectively referred to as large medical aesthetics institutions, medium-sized medical aesthetics institutions, and small medical aesthetics institutions.

Specifically,Large-scale medical aesthetic institutions are primarily nationally renowned chain hospitals in the medical aesthetics sector.. Such institutions possess a certain degree of brand recognition, strong bargaining power against upstream suppliers, ample capital resources, and a high concentration of talent. However, the issue lies inAs regional coverage and promotional effectiveness reach their peak, achieving subsequent performance growth and user retention will become increasingly difficult.

Medium-sized medical aesthetic institutions are primarily individual hospitals or small chains with a few locations, positioned between large hospital chains and medical aesthetic clinics.Such hospitals typically generate annual revenues of approximately RMB 50 million, with staff sizes ranging from 100 to 300 employees. The advantages of these hospitals lie in their established regional reputation and superior service capabilities compared to clinics. However, the challenge is that such hospitalsDue to the lack of economies of scale, costs in areas such as marketing and promotion have remained persistently high, resulting in insufficient risk resilience.

Small-scale medical aesthetics institutions are primarily medical aesthetics clinics., typically staffed by a small number of physicians and a limited service team, with annual operating revenue of approximately RMB 10 million. The advantage of such clinics lies in their focus on cost-effectiveness, primarily catering to a younger customer base. The issue with these medical aesthetic institutions is thatServices are relatively monolithic, lacking the conditions and capabilities to expand into a broader service portfolio.

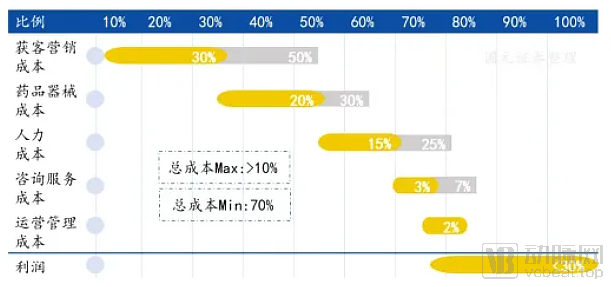

From the above three types of medical aesthetic institutions, it can be seen thatCustomer acquisition and cost control are urgent issues that medical aesthetic institutions need to address.Compared with traditional broad and scattered promotional marketing,The benefits of going online enable medical aesthetic institutions to move toward more refined operations.. This precisely aligns with the core demands of medical aesthetic institutions for customer acquisition and cost control.

(Cost Structure of Traditional Medical Aesthetic Institutions Source: Guoyuan Securities)

What are the methods for online operations? These include leveraging platforms such as Baidu and Toutiao.Search Engines and Content Distributionfor customer acquisition, including through professional internet-based medical aesthetics platforms such as So-Young and Gengmei“Content + Community”Traffic diversion strategies also include building in-house capabilities or collaborating with MCN agencies.Building a Doctor's Personal IP Brandto attract users, and institutions throughShort Videos and Live Streamingand other forms for marketing and promotion.

Search engine and content distribution advertising models still hold a significant position in the current promotional strategies of medical aesthetic institutions, but the cost pressure associated with such marketing promotions is considerable. To this end,Innovative marketing, building physicians’ personal brands, and short-form video and live streaming are gaining increasing traction among aesthetic medicine institutions’ online strategies this year.

Innovative Marketing, including internet-based viral marketing tactics such as appearance tests. This type of marketing and promotional approachThe advantage is that, at a lower cost, users are more willing to forward and share, resulting in broader audience reach.. However, due to increasingly stringent controls by platforms such as WeChat on similar marketing tactics, subsequent viral marketing strategies will gradually shift toward methods such as embedding content within WeChat Official Account posts. Therefore, for medical aesthetic institutions,Selection of such engagement models will increasingly favor institutions with strong content marketing capabilities.

Building a Doctor's Personal Brand, primarily include methods such as real-person IP or cartoon character IP. This type of approachThe advantage is the ability to more quickly and effectively capture users’ mindshare, thereby generating substantial traffic.Compared to the marketing approach of the early era of medical aesthetics, which relied primarily on referrals from acquaintances, professional physician IPs with established personal brands are better equipped to address users’ initial trust issues, enhance user stickiness, and improve long-term user retention.

Short Videos and Live Streaming, it involves public platforms and private-domain traffic platforms.Public platforms are characterized by high traffic volumes, making them suitable for user acquisition. Private-domain traffic platforms feature more precise user targeting, making them ideal for retention.. Therefore, medical aesthetic institutions that are new to short-form video and live streaming should not simply allocate the majority of their budget to public platforms; instead, they should integrate public platforms with private-domain traffic platforms. This approach maximizes the aggregation of targeted traffic into their own user pools, thereby avoiding a return to the previous cycle of acquiring customers only through one-off advertising campaigns. Thus,User operations capability will also become a key consideration for medical aesthetics institutions selecting short-video and live-streaming strategies in the near future.

It should be noted that midstream medical aesthetic institutions represent the most service-intensive segment of the entire industry,User Experience Will Directly Impact the Development of the Medical Aesthetics IndustryTherefore, the overall service quality of midstream medical aesthetic providers must be strictly controlled. Consequently, in recent years, calls for the medical aesthetics industry to “return to its medical essence” have grown increasingly loud. Under these circumstances, the industry is gradually reaching a consensus: only by returning to the essence of medicine can the medical aesthetics industry achieve better development.

This July, over 150 medical aesthetic institutions across China, including United Liger, Mylike, and Yestar, have rallied behind the first public welfare initiative for black-market medical aesthetic repair and relief launched by So-Young. The program provides free corrective aesthetic treatments to victims of illegal medical aesthetics, as well as patients with facial deformities resulting from congenital conditions or accidental injuries. Covered procedures include common reconstructive surgeries for the eyes, nose, breasts, and scars.Joint actions by medical aesthetic institutions indicate that mainstream players in the industry are helping to gradually improve the medical aesthetics ecosystem.

Of course, the “medical” nature of healthcare services also makes it difficult for medical aesthetics companies to achieve exponential market growth in the short term. Therefore, reducing management and marketing costs while expanding the profit growth zone will remain a long-term challenge for midstream players in the medical aesthetics industry.

In the medical aesthetics industry, the downstream sector has currently formed an industrial landscape characterized by a combination of various models, including medical aesthetics e-commerce, marketing, and financial services. However, regardless of whether it involves e-commerce, marketing, or finance, the primary objective remains customer acquisition for medical aesthetics providers.

Unlike in previous years, when the focus was primarily on connecting with users through medical aesthetics marketing, traffic giants have adopted a more in-depth strategic layout this year, demonstrating a stronger willingness to transform the industry.

For instance, in June this year, Meituan launched the “Installment Plans for Beauty: Easier and More Affordable” campaign, marking its entry into the medical aesthetics installment financing sector. During the Double 11 shopping festival, Meituan continued to ramp up its efforts, consistently pushing in-app advertisements for medical aesthetics installment plans that highlighted “interest-free promotions on best-selling items across the board, with discounts as low as 50% off and up to 12 months interest-free.”From traffic acquisition to financial services, internet platforms will provide users with more choices in consumption decisions, shorten the decision-making path, and drive conversions.

On September 22, Alibaba’s first national “Medical Aesthetics Live Streaming Industry Demonstration Center” was established in the “Shezhuang Town” of Wuhou District, Chengdu. Following its establishment, the center will collaborate with medical aesthetics institutions and nursing schools in Chengdu to identify and intensively train live-streaming hosts for the medical aesthetics industry. By delving into specific segments of the medical aesthetics field, deeply optimizing individual aspects—such as talent development and platform construction—will become a trend in the strategic layout of major enterprises within the medical aesthetics industry. The benefits this brings areWhen internet platforms provide comprehensive, in-depth services for a specific segment of the medical aesthetics industry (such as marketing or operations), they are better positioned to identify differentiated pathways and avoid becoming entangled in price wars over traffic.

In October, So-Young Technology officially launched its VR Smart Showroom, built on virtual reality (VR) technology, to provide users with online experiences such as 720° panoramic interaction and surgical observation. Prior to the launch of the VR Smart Showroom, So-Young Technology had already explored the application of 5G technology in the medical aesthetics industry, including video consultations, live streaming, and AI-powered tools.From community content to technological innovation, internet-based medical aesthetics platforms are entering an era of technological revolution and innovative applications.

The Gengmei app has also continued to deepen its industry presence this year, launching advertising campaigns for nearly ten nationally popular TV series and variety shows, including "The Bad Kids" and "Sisters Who Make Waves," thereby expanding market awareness while reaching beauty-conscious users across multiple scenarios. In addition to continuously upgrading its aesthetic tool, Gengmei AI, to provide users with customized professional beauty enhancement plans, offering merchants operational solutions and intelligent tools, hosting the 7th Annual Top Doctors Awards, and curating a selection of meticulous and skilled physicians for users, Gengmei has alsoStrengthen collaboration with various stakeholders in the medical aesthetics industry, including raw material brands.

Judging from the strategic moves of the traffic giants, they are allBreak free from the constraints of traditional internet-based customer acquisition methods, and provide new support for patient acquisition in the medical aesthetics industry through multi-dimensional approaches encompassing technology, talent, and formats.. Yet, as recently as last year, traffic giants were primarily focused on capturing the medical aesthetics sector by leveraging high-frequency services to displace low-frequency ones. Clearly, this year’s stringent regulatory policies and the pandemic have accelerated a shift among these traffic giants toward understanding the medical aesthetics track through an industrial lens.

As traffic giants continue to expand their reach across the breadth and depth of the industry, they will increasingly foster connections along the upstream and downstream segments of the industrial chain and promote the integration of online and offline operations. This trend will drive the transformation and upgrading of the medical aesthetics industry.

However, beyond effectively acquiring customers,Improving the quality of medical services will be a long-term challenge for all enterprises in the medical aesthetics industry.Upstream pharmaceutical and medical device enterprises must deliver higher-quality, more cost-effective products; midstream medical aesthetic institutions must ensure the safety of medical services; and downstream entities, such as e-commerce and marketing agencies, must provide truthful promotions and reviews. Every link in this chain is indispensable.

By reviewing the overall landscape of the medical aesthetics industry in 2020 and observing and summarizing typical events across the upstream, midstream, and downstream sectors, we have gained a glimpse into just the tip of the iceberg. Beneath the surface lie the subtle shifts in supply and demand throughout the entire medical aesthetics industry.

According to the latest data report from Medical Aesthetics Industry Insider,The demographic profile of medical aesthetics consumers—including age, educational background, spending power, and industry awareness—has undergone significant changes in recent years.

FromTarget User GroupFrom a demographic perspective, in addition to young women primarily in first- and second-tier cities, young users in third- and fourth-tier cities, postpartum mothers, the silver-haired population, and male consumers are also joining the ranks of medical aesthetics spending. Secondly, demand for service categories is becoming increasingly diversified, with treatments such as anti-aging, hair care and transplantation, body contouring, and intimate plastic surgery gaining significant popularity. Thirdly, regarding consumer psychology, beyond self-gratification, factors such as career advancement and marriage prospects have become key drivers for many individuals seeking aesthetic procedures.

FromUser StructureFrom a macro perspective,Medical Aesthetics Users Are Becoming Younger and Older at the Same Time, with users aged 20-25 accounting for 37% and those aged 26-30 making up 26%. Notably, men are increasingly participating in medical aesthetics consumption. It is reported that the primary male demographics for medical aesthetics currently include celebrities, white-collar professionals, university students, and successful middle-aged individuals.

It is foreseeable that China’s medical aesthetics industry will continue to have substantial growth potential over the next three to ten years, and early entrants have undoubtedly secured a first-mover advantage. Of course, as consumption patterns evolve, latecomers still have opportunities. However, in this process, those who can address the industry’s most critical pain points with optimal solutions will achieve sustainable success more rapidly.

As 2020 draws to a close, practitioners in the medical aesthetics industry are poised to turn a new page in their journey toward ambitious horizons. Yet, it must not be forgotten that while the calendar can be turned, the original commitment to enhancing people’s beauty should never be cast aside.

Special Acknowledgments:

Sinopharm Capital

Mingfeng Capital

SoYoung Inc.

Gengmei App

(The above list is in no particular order.)