Mental Health Sector Sees Over 50 Funding Rounds in 2020, with Capital Flowing to Tech-Driven Companies Amid Surging Demand and Significant Service Gaps

Text and photos by Xiang Lianhua, Wang Yue, and Li Aijie

Mental Health Industry: Among the many specialized sectors within healthcare, it is not the most prominent; however, under the impact of the COVID-19 pandemic, mental health has once again drawn widespread public attention.

According to Baidu’s “2020 National Guide to Fighting ‘Depression’—Big Data on Searches for Mental Health Day,” the search volume for content related to psychological support reached its highest level in nearly a decade amid the pandemic, and patients with depression are becoming increasingly younger.

Furthermore, data from the White Paper on Mental Health of Urban Residents in China shows that 73.6% of urban residents are currently in a state of suboptimal psychological health, while 16.1% experience varying degrees of psychological issues. With economic development and consumption upgrades, an increasing number of people are beginning to pay attention to their own mental health status.

However, the mental health industry continues to face significant pain points and disorderly practices, such as a shortage of psychiatric resources and uneven quality among psychological counselors. In China’s mental health sector, where no unicorn companies have yet emerged, how many players have entered the market? What challenges have arisen during its development? And what changes might lie ahead?

By analyzing events and data, VCBeat has compiled the “Global Mental Health Value Trends Report 2016–2020” (hereinafter referred to as the “Report”). The Report points out that the global digital mental health sector has seen vigorous development over the past five years, with a number of early-established companies achieving mature business models. Meanwhile, emerging startups and innovative business models continue to proliferate. In China, the digital mental health landscape remains a blue ocean, characterized by relatively limited participation from startups, most of which are still in their early stages of development.

Based on the report, VCBeat reviewed the development of the mental health market in recent years and summarized the mental health sector in 2020 as follows:

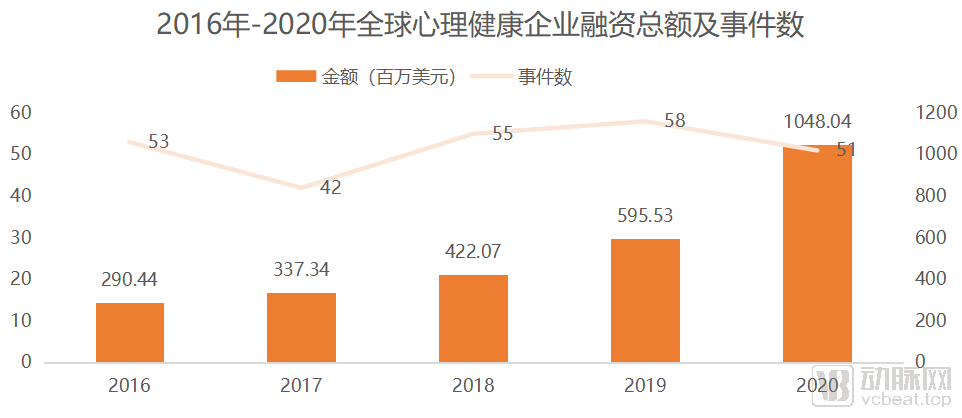

1. In 2020, there were 51 financing deals in the digital mental health sector, with total funding reaching $1.048 billion, a 76% year-on-year increase; the average deal size reached $20.54 million, approximately double that of 2019.

2. The number of financing and investment events in the domestic market has declined somewhat compared to 2019, with capital adopting a more cautious and rational stance;

3. Domestic capital is concentrating in technology-driven enterprises, with psychotherapy services gaining favor;

4. The mental health market continues to grow, with a substantial gap in counseling and therapeutic services;

5. Policies continue to promote the development of mental health systems and platforms, with guidance content becoming increasingly detailed.

Global Digital Mental Health Industry Sees Continued Expansion in Financing Scale

According to a report by VBInsight, the mental health sector witnessed 51 financing events in 2020, with total funding amounting to $1.048 billion, a 76% year-on-year increase; the average single-round financing reached $20.54 million, approximately double that of 2019.

Data Source: VCBeat Orange Database, VCBeat Industry Think Tank Report

It is evident that the mental health market has experienced rapid growth over the past five years, with total corporate financing even doubling in 2020, while the maturity of business models continues to advance.

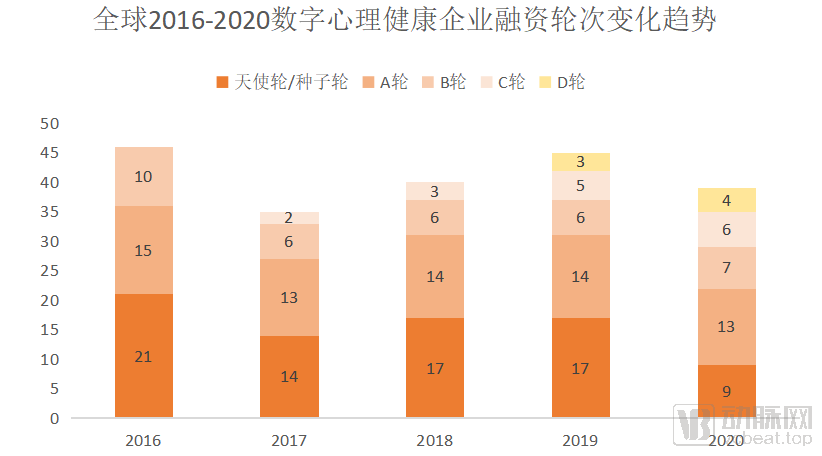

Data Source: VBInsight Orange Database, VBInsight Industry Think Tank Report

In terms of funding rounds, the digital mental health sector remains in its early stages of development: there have been no publicly listed companies in the past five years, over 60% of companies are at the seed to Series A stage, and the most advanced companies have reached only Series D.

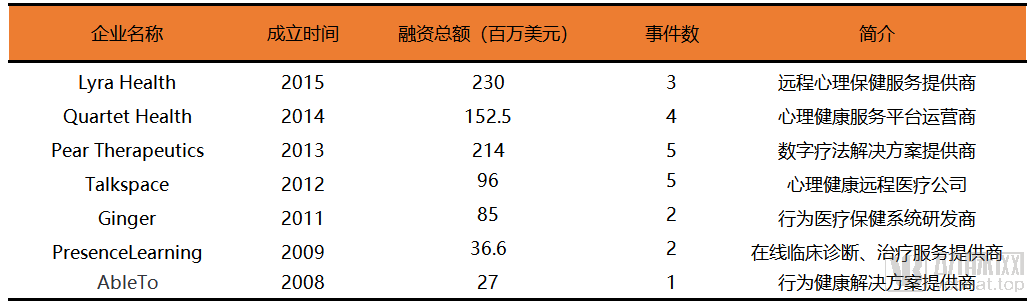

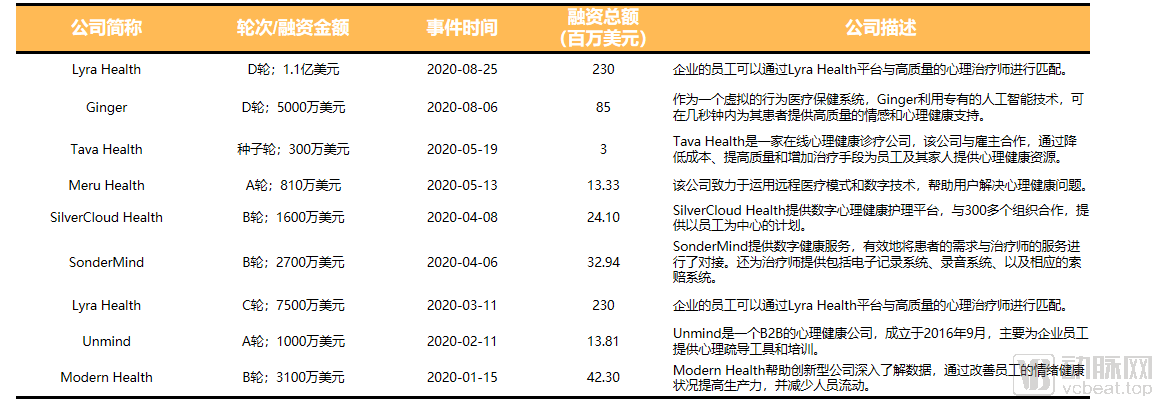

Mental Health Companies That Have Completed Series D Financing (Data Source: VCBeat Orange Database, VCBeat Industry Think Tank Report)

These seven companies all operate in the telemedicine sector, providing online consultation services or building digital platforms and services for mental health. This indicates that current online platforms with mature business models are more favored by capital investors.

In terms of business segmentation, overseas employer-focused enterprises are growing rapidly, while meditation apps remain highly popular.

Financing Events Involving B2B-Focused Enterprises in 2020 (Image Source: VBInsight Industry Think Tank Report)

Enterprise-oriented products are primarily offered as employee benefits, with companies purchasing the services and employees choosing to use them. Quartet and Talkspace have previously completed their Series D financing rounds. The rapid growth of such companies highlights the strength of their business model, which lies in the diversity and stability of their B-end users. Whether in terms of financing rounds or user scale, enterprises that enter the market through employers, health plans, or medical institutions are better positioned to gain a competitive advantage.

However, given the current domestic market in China, the B2B business model with enterprises as service buyers appears difficult to realize in the short term.

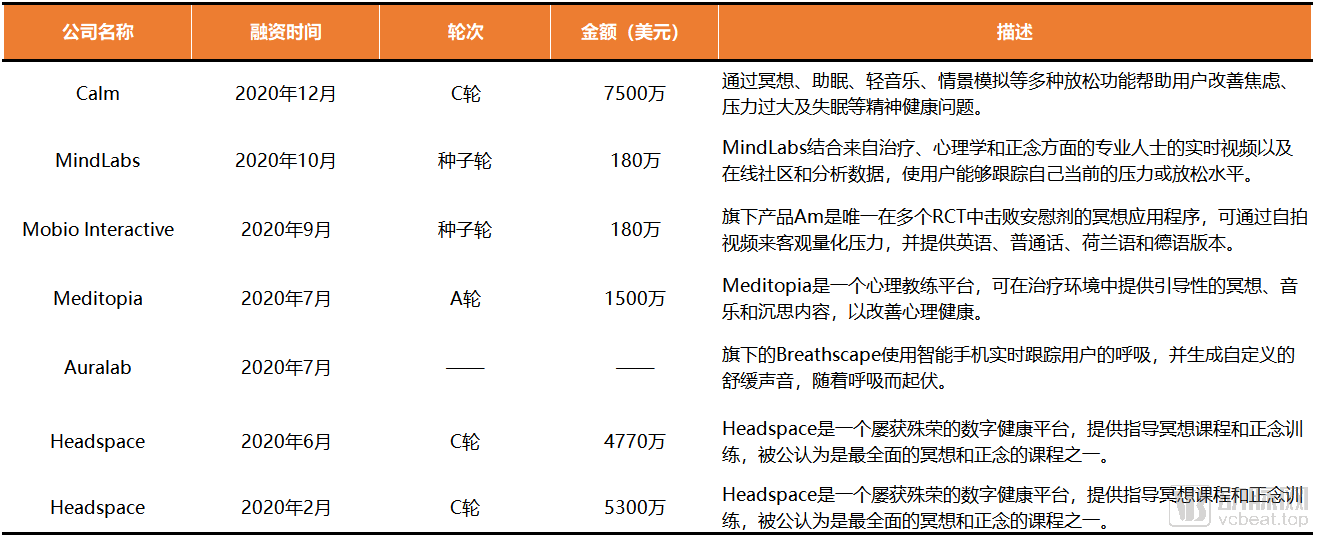

Additionally, the development of meditation services, which have gained significant popularity abroad, has been relatively slow in China; this year, no meditation-related companies in the country have secured financing.

2020 Financing Landscape of the Meditation Market (Data Source: VCBeat Database, VCBeat Industry Think Tank Report))

Currently, companies such as KnowYourself, Tide, and Now are leading the meditation market in China. However, constrained by the domestic meditation culture and public awareness, no unicorn enterprise akin to Calm has yet emerged. By comparison, the Chinese meditation market remains lukewarm.

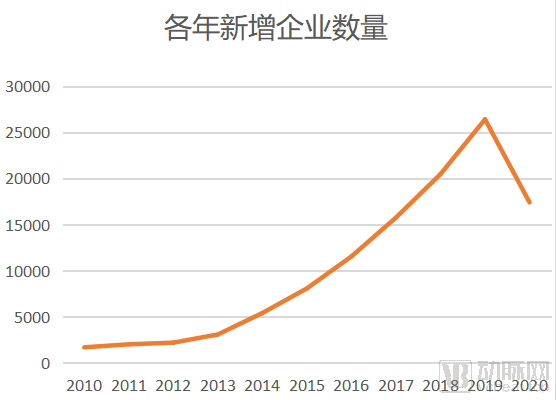

Rapid Growth in the Number of Enterprises in 2013

How many companies in China are involved in the mental health sector?

Providing exact figures may be difficult, but data from Qichacha shows that China currently has more than 90,000 enterprises with “psychological counseling” included in their names or business scopes, representing a sevenfold increase in registrations over the past six years. Affected by the pandemic, the number of companies associated with psychological counseling fell by 24.65% year-on-year in the first quarter of 2020, and the number of newly established enterprises for the full year also declined.

Growth in the Number of Psychological Counseling-Related Enterprises (Data Source: Qichacha)

Prior to 2013, the growth in the number of mental health-related enterprises remained relatively stable. However, after 2013, there was a notable surge in newly established companies. This trend may be attributed to the implementation of the Mental Health Law in 2012. Following the enactment of this legislation, the national government successively issued relevant guidelines and standards, which helped raise public awareness and promote industry development.

This year, the widespread impact of the COVID-19 pandemic across society has drawn significant attention to mental health issues.

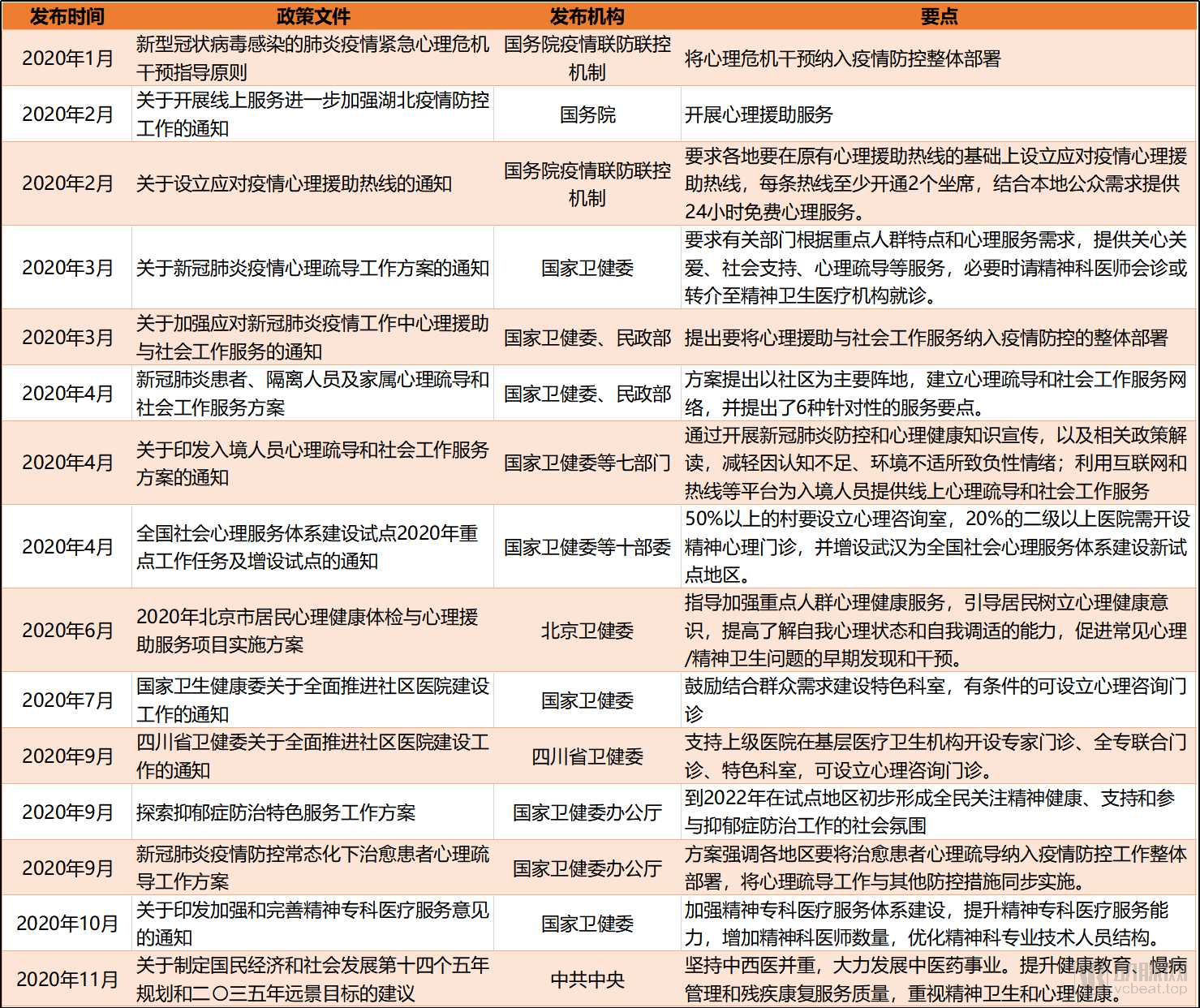

Summary of Mental Health Policies in 2020 (Source: Compiled from Public Information)

Public data show that since January 2020, there have been 15 policies related to mental health, eight of which were associated with the COVID-19 pandemic. This indicates that mental health issues have been regarded as an integral component of overall pandemic prevention and control efforts.

Reviewing the trajectory of policy development, it is evident that China’s approach to mental health is evolving from macro-level emphasis and guidance to the concrete establishment and standardization of mental health platforms and institutions. Measures adopted vary depending on the type and severity of mental health issues.

Furthermore, during the pandemic, the National Health Commission of China held multiple press conferences on psychological health topics to deploy mental health services under the epidemic situation.

On February 3, 2020, at a press conference held by the National Health Commission, experts introduced social psychological services such as online counseling and telephone hotlines implemented during epidemic prevention and control efforts, and provided several recommendations on how the general population can maintain mental health while staying at home for extended periods during the outbreak.

In March 2020, the National Health Commission stated at a press conference held by the State Council’s Joint Prevention and Control Mechanism that frontline healthcare workers would be designated as a priority population for psychological intervention. Dedicated psychological counseling hotlines and online mental health service platforms were established for medical personnel. Furthermore, the National Health Commission deployed 415 mental health professionals to Hubei Province to provide professional psychological counseling and crisis intervention services for both patients and healthcare workers.

At a press conference held by the National Health Commission in May, experts emphasized the need to summarize lessons learned from mental health service delivery during the initial phase of epidemic prevention and control, and to continue strengthening public education on mental health.

During the pandemic, mental health services gradually evolved from providing advisory guidance to concrete implementation, and later to summarizing experiences and continuously promoting mental health initiatives, thereby increasing public awareness of the mental health industry.

Insufficient Number of Practitioners, Huge Gap in Mental Health Services

Although attention to mental health has continued to rise in recent years, it cannot be ignored that China still faces an imbalance in medical resources for psychological counseling and treatment.

Generally, most people refer to all mental health service providers as "psychiatrists," but more accurately, this group can be subdivided into psychological counselors, psychotherapists, and psychiatrists.

According to public information, the Ministry of Human Resources and Social Security has issued over one million Level 3 or Level 2 Psychological Counselor qualification certificates since 2002. However, only 30,000 to 40,000 individuals are engaged in full-time or part-time work in the psychological counseling industry. With the cancellation of the national certification examination for psychological counselors, the shortage of qualified professionals is expected to continue widening.

Compared with psychological counselors, psychotherapists are even scarcer. By the end of 2017, there were only about 6,000 psychotherapists in China. Psychotherapists are similar to psychological counselors in terms of psychological counseling, but the qualification certificate for psychotherapists can only be obtained by individuals with a medical background. Some therapists who hold the Licensed Physician Certificate have prescription rights.

Furthermore, China currently has approximately 40,000 psychiatrists. Although the total number of physicians has continued to grow in recent years, supply remains insufficient, with less than 10% of patients suffering from psychological or mental disorders seeking medical care.

Internet hospitals, offline chains, pan-psychology services, and community-based models—diverse strategies abound

In general, most people experience a state of suboptimal psychological health, characterized by its transient nature, minimal impact on social functioning, and the capacity for self-adjustment; in some cases, professional assistance from a psychologist is required.

When the severity of abnormal psychological activities meets the criteria for medical diagnosis, it is termed a mental disorder. A mental disorder refers to various abnormal psychological processes, abnormal personality traits, and maladaptive behavioral patterns resulting from physiological, psychological, or social factors. It is characterized by an individual’s inability to act in socially acceptable and appropriate ways, leading to consequences that are maladaptive for both the individual and society.

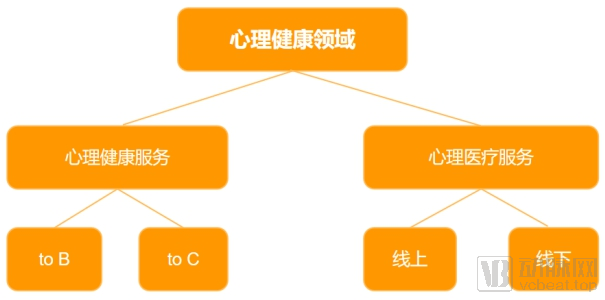

To address different psychological issues, players entering the mental health sector have adopted distinct business models, primarily including a health service model for common psychological problems and a medical service model for psychological disorders.

Mental Health Business Categories

Players in the health service model can be categorized into B2B and B2C types based on their target customers. Given the current state of the domestic market, B2C enterprises clearly constitute the majority. Key innovative companies include Yi Xinli (Simple Psychology), Yu Jian, and Yi Dian Ling, among others. Their primary service model leverages internet platforms to migrate offline psychological counseling services to online channels.

In recent years, a wave of companies focused on broad mental health has emerged in the market, each adopting different market entry strategies. These include Sleepace, Woniu Sleep, and XinChao Technology, which specialize in the sleep sector, as well as The Depression Lab, which has built online communities for individuals with depression. These diverse players are deeply cultivating their respective vertical niches and offering tailored solutions for various population groups.

Players in the medical service model can be categorized into online and offline models based on their service delivery platforms. Online innovative enterprises, such as Haixinqing and Zhaoyang Doctor, have moved psychiatric specialties from traditional public hospitals to online platforms, adopting a business model similar to that of typical internet healthcare companies like Chunyu Doctor and WeDoctor.

Furthermore, with the development of internet hospitals, some players have begun to explore the model of specialized psychiatric and psychological internet hospitals. Examples include Xiaodong Health Internet Hospital, under Xiaodong Health, and Yining Psychological Internet Hospital, under Wenzhou Kangning Hospital Group. Reportedly, Xiaodong Health Internet Hospital is the first platform in China to obtain a license for a specialized psychiatric and psychological internet hospital since the National Health Commission implemented the Administrative Measures for Internet Hospitals.

Offline, numerous enterprises have also begun to explore new business pathways. Previously, when patients sought professional treatment for mental disorders in offline settings, they primarily visited psychiatric specialty hospitals or psychiatric departments within public hospitals; however, this process required consideration of factors such as institutional selection and geographic location. Consequently, market players represented by Ankang Medical and Boen Medical have adopted a chain-based model to establish branded chains of psychiatric and psychological outpatient clinics.

Some mental health service companies focus primarily on the research and development of hardware devices, with representative firms including Huichuang Medical. It is reported that Huichuang Medical’s near-infrared brain imaging product employs the Verbal Fluency Task (VFT) as a standard paradigm, enabling quantitative and precise assessment of conditions such as depression, schizophrenia, and bipolar disorder. Its efficacy has been clinically validated and recognized by the academic community over many years. This September, Huichuang Medical completed its Series A financing round, raising RMB 10 million.

Light Consultations Dominate Online Platforms, with Weak Medical Attributes

Behind the rigid demand in the physical healthcare market for mental health, the emerging market that leverages the internet to deliver mental health and psychiatric counseling, as well as diagnostic and treatment services, has also remained under close scrutiny.

Currently, mental health service platforms leveraging internet technology primarily fall into two categories: one is a health service platform centered on psychological counselors, focusing on psychological counseling and psychoeducation, with content as its core product; the other is a treatment-oriented service platform led by clinical psychiatrists and psychologists. Both are classified as vertical mental health platforms.

Data source: VCBeat Orange Database

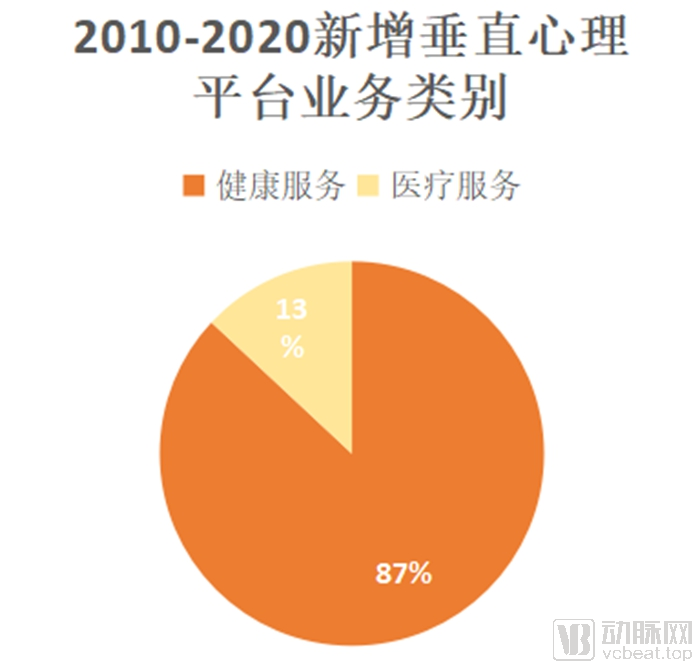

By reviewing the business categories and establishment dates of new vertical mental health platforms over the past decade, it is evident that most entrants have focused their efforts on mental health services targeting general psychological issues.

“The reason why most companies choose to focus on mental health services is, to some extent, because integrating with the internet allows them to offer services that go beyond traditional offline therapy and counseling,” Zou Zou, founder of Xin Chao Technology, told VCBeat. “Whether it’s content-oriented services such as psychological counseling referrals, public education, and course training, or technology-driven areas like hardware development, all can serve as entry points into the industry.”

Internet platforms offering consulting services are less constrained by geographic limitations, not only enabling clients to access needed services more conveniently but also creating greater opportunities for service providers. Moreover, leveraging the internet allows entrepreneurs to enter the market through multiple vertical niches, adopt asset-light operational models, and reduce the burden of platform maintenance.

Multiple Psychotherapy Service Providers Garner Investor Interest

In the mental health sector, the most significant capital market event in China in 2020 was HaoXinqing’s completion of its RMB 125 million Series A financing round, a sum comparable to its 2019 fundraising.

Selected Financing Events in China’s Mental Health Sector in 2020 (Data Source: VCBeat Orange Database)

Haoxinqing, founded in 2016, focuses on the central nervous system (CNS) field. By leveraging intelligent diagnosis and treatment systems along with an internet hospital service network, it provides smart rehabilitation management and online medical services to patients with psychiatric and psychological disorders. Within less than a year of its establishment, Haoxinqing secured RMB 50 million in angel-round funding, led by Nhwa Pharmaceutical. In 2018, the company raised tens of millions of RMB in Pre-A round financing from Neutron Capital and Korea Investment Partners (KIP).

Following the completion of its Series A financing, Haoxinqing will continue to expand its business scale while increasing R&D and investment in its intelligent diagnosis and treatment system.

To better meet patients’ diverse needs, Haoxinqing is actively establishing offline counseling centers. In late 2019, its first psychological counseling clinic was successfully launched in Beijing, aiming to provide users with an integrated online-to-offline healthcare service. It is reported that Haoxinqing will comprehensively expand its offline clinic operations in 2021, with plans to open more than 30 clinics. This initiative will fill the gap in China’s psychological medical clinic sector and significantly enhance users’ experience of face-to-face consultations.

Another company that secured financing this year, Wanling Pangu, has focused its product strategy on AI-based screening and diagnosis. Through its proprietary “Wanling Cloud” system, mental health assessment results can be directly integrated into hospital information systems, while the platform also provides prognostic evaluations, treatment plans, and medication recommendations.

From a financing perspective, the number of funding deals in China’s mental health industry in 2020 declined significantly compared with 2019, with most investments concentrated in companies at relatively early to mid-stages, a pattern similar to that observed in 2019.

The decline in capital market activities this year is largely attributable to the impact of the pandemic. Although the pandemic has heightened public awareness of the importance of mental health, the economic shock it caused has made institutions more rational and cautious in their investment decisions.

Furthermore, during the pandemic, various psychological platforms and institutions, driven by their original intention to help the public, launched free, pro bono psychological hotline services for groups in need. This initiative, to some extent, diverted corporate resources without generating additional economic revenue for these enterprises. However, by exposing more people to mental health knowledge, it facilitated market education and contributed to the future development of the industry.

From the perspective of business operations, among the companies that secured financing this year, Wanling Pangu, Haokxin Qing, Xiaodong Health, and Huichuang Medical all belong to the category of providers of psychological medical services. The first three companies have invariably integrated technologies such as artificial intelligence, while Huichuang Medical focuses primarily on medical device research and development. Meanwhile, Luye Medical Group (Manlang Medical), which acquired Xinlin Medical and Cuixin Psychology, is the second-largest private mental health service provider in Australia.

It is evident that capital has shown greater enthusiasm this year for projects in the specialized diagnosis and treatment of mental disorders. Empowered by technologies such as artificial intelligence, enterprises are able to integrate more segments of the value chain, thereby establishing superior business models.

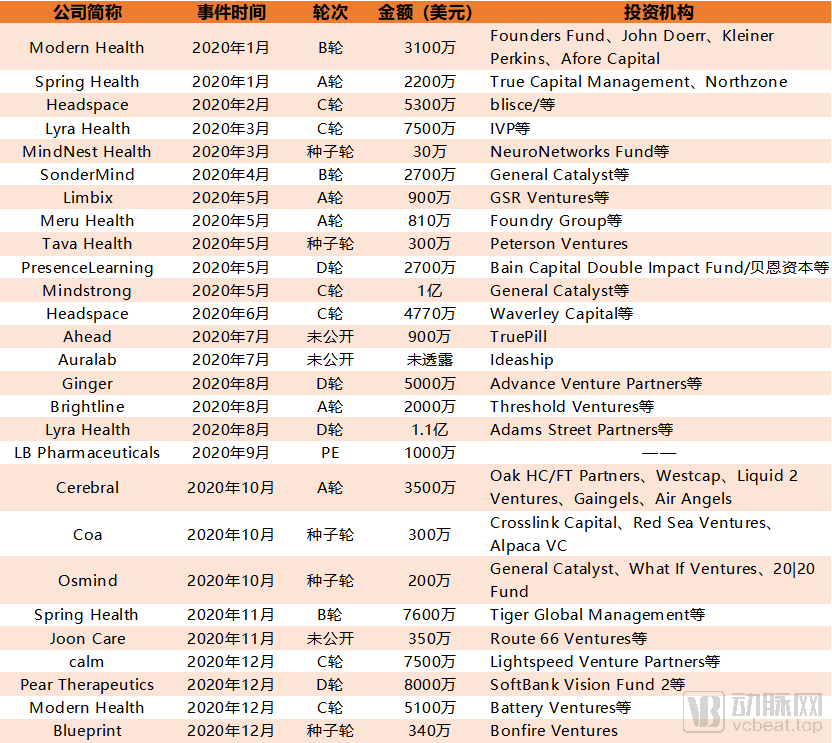

Compared with China, the financing scale in the U.S. mental health sector is significantly larger, with 22 companies securing over $900 million in funding. In terms of financing rounds, companies in the U.S. mental health sector are generally at later stages than their counterparts in China.

Selected Financing Events in the U.S. Mental Health Sector in 2020 (Source: VCBeat Database)

Notably, Calm, a unicorn in the mental health sector, announced the completion of its $75 million Series C financing round at the end of this year, less than two years after closing its Series B round. Following this financing, Calm will pursue greater business growth through mergers and acquisitions.

Although no company in China has gone public via an initial public offering (IPO) this year, publicly available information indicates that Wenzhou Kangning Hospital Co., Ltd. (hereinafter referred to as “Kangning Hospital”), a private specialized psychiatric hospital listed on the Hong Kong Stock Exchange and known as the “first psychiatric stock,” has once again initiated its push for an A-share IPO.

On September 30, 2020, the official website of the Zhejiang Securities Regulatory Bureau updated the basic information on companies under listing tutelage. The information indicated that Kangning Hospital and its securities firm had signed the filing documents for listing tutelage on September 18, thereby accepting Guotai Junan’s guidance for its initial public offering.

Kangning Hospital was established in February 1996, primarily providing specialized medical services to patients with mental and psychological disorders. In November 2015, Kangning Hospital successfully listed on the Main Board of the Hong Kong Stock Exchange, becoming the first company from Wenzhou to be listed in Hong Kong.

In March and July 2017, Kangning Hospital suspended its IPO twice, and the application was rejected in early 2018. As Kangning Hospital resumes its A-share IPO plans, this move, regardless of the outcome, will in a sense help raise public awareness of psychological and mental health.

The Feasibility of Digital Therapeutics in Curing Mental Health Conditions

With the development of innovative “Internet+ Psychology” service models, emerging digital therapeutics have, in recent years, leveraged remote physician support to implement digital solutions that modify patients’ behaviors and lifestyles, thereby treating psychological diseases and mental disorders. Digital therapeutics have demonstrated significant advantages in the personalized treatment of patients with mental disorders.

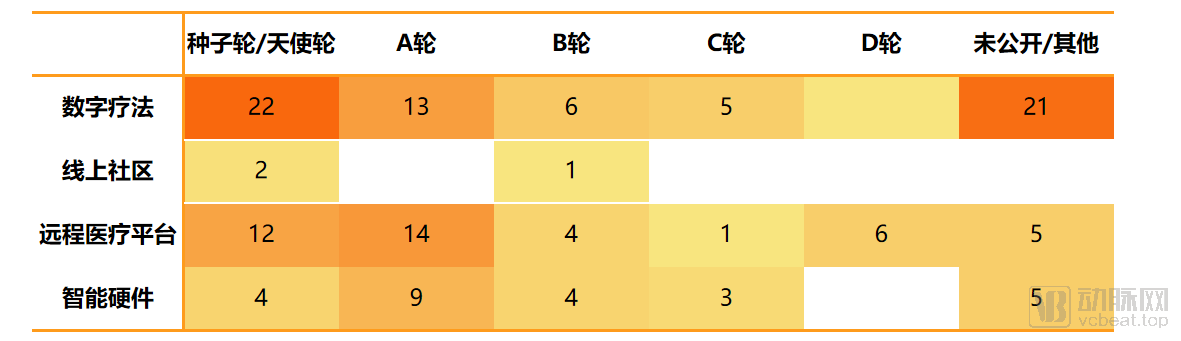

Global Mental Health Corporate Investment and Financing Sub-sector Transaction Rounds, 2016–2020 (Image source: VBInsight Industry Think Tank Report)

For digital therapeutics, mental health represents the second key frontier—after diabetes—where pharmacological interventions have limited efficacy and digital solutions can most readily gain traction. Digital therapeutics have already demonstrated tangible success in the mental health sector; for instance, Pear Therapeutics’ digital therapeutic Somryst has received FDA 510(k) clearance for treating insomnia symptoms through algorithm-driven cognitive behavioral therapy for insomnia (CBT-I).

While some domestic companies have combined digital therapeutics with psychological services, none have obtained certification for digital therapeutics in the strict sense of the definition.

However, this November, ShuKang APP, China’s first digital therapeutic, received marketing approval from the National Medical Products Administration (NMPA). It can be prescribed directly by physicians to patients and is primarily indicated for the rehabilitation of chronic diseases and chronic pain, such as hypertension, diabetes, and post-operative recovery in oncology patients.

Although ShuKang is not indicated for psychological disorders, its approval signifies domestic recognition of digital therapeutics and fills a gap in China’s digital medicine market.

Exploration Beyond the Field

During the pandemic, most mental health enterprises—including YiXinLi, HaoXinqing, and Zhaoyang Psychology—established free psychological counseling assistance hotlines. Beyond this sector, numerous other companies also participated in the deployment of online mental health services, collaborating with relevant resource providers to offer psychological counseling services and technical support. These participants included tech giants such as Alibaba, Tencent, JD.com, and Ping An Group, as well as internet healthcare companies like WeDoctor, Haodafu, and Chunyu Yisheng.

Due to differences in their respective business focuses, these companies offer slightly different types of services. Tencent Medical Classic provides authoritative and trustworthy information by assembling a team of science communication experts, and also offers content related to psychological counseling.

Alibaba Health launched the “Buy Medicines Without Leaving Home” service on the Taobao app, enabling patients to safely purchase required medications from home through online consultations, e-prescriptions, and home delivery.

Miaoshou Doctors, in collaboration with the Psychosomatic Medicine Committee of the Chinese Medical Doctor Association, has officially launched its “Free Psychological Counseling Clinic.”

WeDoctor Group, in collaboration with the China Disaster Prevention Association, the China Health Management Association, and the Chinese Mental Health Association, launched the “Wei Xin Zhan Yi” public welfare initiative. A dedicated psychological support section was established on the WeDoctor Internet General Hospital platform to provide mental health care to the general public, healthcare workers, and police officers across China.

"In the near future, WeDoctor will continue to deepen its collaboration with experts and strengthen the development of key disciplines, including psychological counseling and traditional Chinese medicine, thereby establishing specialized departments and distinctive service capabilities."

Technology Drives Development and a More Segmented Mental Health Market

Currently, in addition to supply imbalances, the mental health market in China faces challenges related to users’ willingness to pay. Therefore, continuous market education is essential. Enhancing public awareness of mental health represents not only progress for the industry but also for society as a whole.

In the development of mental health platforms, an analysis of this year’s domestic market conditions reveals that artificial intelligence, big data, and other technological tools have gained significant recognition for their application in assisted diagnosis. Chen Guanwei, CEO of Haoxinqing, has also stated that AI technology can address the shortcomings of light-consultation platforms, enhance diagnostic accuracy, and reduce misdiagnosis.

In terms of service offerings, as public awareness of mental health continues to grow and technology advances, consumer needs are becoming increasingly specific, thereby giving rise to more specialized and vertically focused services.

Regardless of whether they are young, middle-aged, or elderly, individuals have their own psychological needs, which vary across different social strata. In addition to depression, which has gained broader public awareness, issues such as workplace anxiety and postpartum depression are also prevalent. Consequently, we may see the emergence of more products with refined age segmentation and specialized service offerings in the future.

In terms of product form, most mental health services currently rely on mobile apps or websites as their delivery platforms. However, future product development is unlikely to be confined to a single, simple format. It is reported that some software developers have partnered with hardware manufacturers to integrate mental health services into various everyday objects, such as headphones, smart bands, and smart speakers. This approach offers greater convenience for individuals who are less adept at using apps or similar digital products.

The above data is sourced from the VCBeat database. We have launched VBInsight, an industry think tank designed to help track dynamic trends in the digital health sector. It covers various types of data, including company lists, bidding and tendering information, investment and financing details, and updates on leading enterprises, with real-time updates across nine key dimensions. To request a trial, please scan the QR code below.