Fifth Year of China's National Reimbursement Drug Negotiation: Exploration Phase Ends, Imported Drugs Face Bottlenecks

On December 28, 2020, the National Healthcare Security Administration published on its website the notice on issuing the “National Basic Medical Insurance, Work-Related Injury Insurance, and Maternity Insurance Drug Catalog (2020),” thereby revealing the final results of the medical insurance negotiations.

This year’s national medical insurance negotiations carried a stronger sense of rigorous selection. Compared with the preliminary “List of Declared Drugs That Passed Formal Review for the 2020 National Reimbursement Drug List Adjustments,” which included 751 products, the 162 drugs that ultimately entered the negotiation stage were carefully selected. In the end, 119 drugs successfully reached agreements, setting a new record for national medical insurance negotiations.

Since its inception in 2016, the national medical insurance negotiations have become the “year-end final exam” for the pharmaceutical industry. For many products, inclusion in the national reimbursement drug list represents a dividing line between survival and extinction. Now in its fifth year, the negotiation mechanism has gradually revealed its development trends. Furthermore, these policy moves are also impacting related ancillary industries, such as the rapidly growing commercial health insurance sector.

VCBeat has identified key insights from national medical insurance negotiations by compiling relevant data from the past few years:

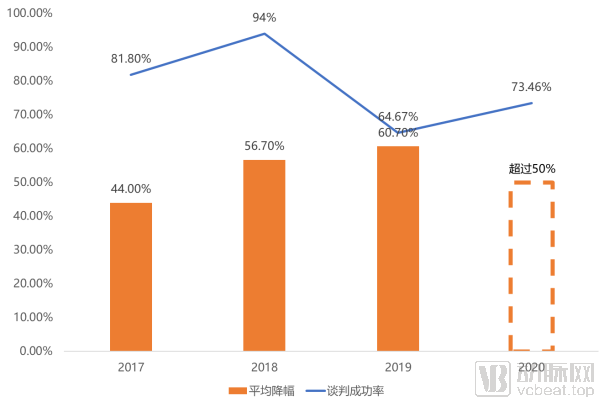

1. The average decline in 2020 narrowed compared to 2019, with the success rate rebounding;

2. Further changes to information disclosure: inclusion of the list of products passing formal review, continued non-disclosure of final prices for certain drugs, and removal of the list of products entering medical insurance negotiations;

3. New negotiations for drugs included in the National Reimbursement Drug List were conducted, with all 14 drugs successfully negotiated; however, none of them appeared on the list of applications that passed the formal review.

4. All four domestically produced PD-1 monoclonal antibodies were included in the National Reimbursement Drug List, while all four imported PD-1/PD-L1 monoclonal antibodies were excluded;

5. Of the products up for renewal in the 2018 national medical insurance negotiations, 13 were successfully renewed, while the remaining 4 did not appear on the list of those that passed the formal review.

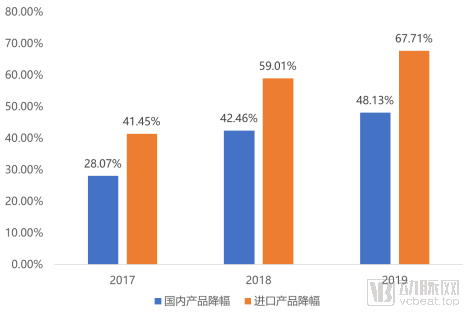

6. The average price reduction for imported products was higher than that for domestically produced products.

What trends might these key points indicate? What implications do they hold for the insurance industry as a whole? We will conduct a relevant analysis in this article.

In recent years, the price reduction magnitude and success rate of China's National Reimbursement Drug List (NRDL) negotiations have tended to stabilize. Over the past four years (excluding the special case of 2016, which involved only three drugs), the success rate of NRDL negotiations hit its lowest point in 2019 at 64.67%, while the average price reduction reached its peak at 60.70%.

The 2020 national medical insurance negotiation results showed an improved success rate compared to 2019. Although the authorities did not disclose the exact average price reduction, the reported figure of “over 50%” suggests that it may not have exceeded the reduction achieved in 2019.

Meanwhile, this year’s national medical insurance negotiations have introduced new changes, incorporating 14 drugs already listed in the National Reimbursement Drug List (NRDL), each accounting for over RMB 1 billion in medical insurance fund expenditures. Official statements indicate that these drugs “have been included in the NRDL for a considerable period, their R&D costs have long been recouped, and thus there is room for price reductions.”

Therefore, the 2020 national reimbursement drug list (NRDL) negotiations can be regarded as both a summary of achievements over the past few years and a new beginning. The fact that the NRDL negotiations did not further drive down price reductions conveys several messages:

1. The National Healthcare Security Administration is highly confident in the future management of its funds:This year, a total of 751 drugs passed the formal review for the National Reimbursement Drug List (NRDL) negotiations. Of these, 162 drugs entered the negotiation phase, and 119 were successfully included, both figures reaching record highs. In previous years, widespread concerns about the NRDL fund deficit have gradually faded from frequent discussion, thanks to dual cost-containment measures implemented through centralized volume-based procurement and NRDL negotiations. The expanded scale of this year’s NRDL negotiations demonstrates the national healthcare security administration’s strong confidence in its ability to further control costs in the future. NRDL negotiations will continue to serve as the primary gateway for new pharmaceutical products, particularly innovative and specialized drugs, to gain rapid access to the national reimbursement list.

2. Stabilization of National Reimbursement Drug List (NRDL) Negotiations:Based on the data disclosed this year, the national medical insurance negotiations did not impose further requirements for price reductions on drugs; instead, the average reduction rate remained largely consistent with the three-year historical average. This moderation in price cuts may also be reflected in the success rate of negotiated drugs. The 2020 national medical insurance negotiations achieved a delicate balance between the “low success rate, high price reduction” pattern seen in 2019 and the “high success rate, low price reduction” trend observed in 2017. This suggests that future medical insurance negotiations are likely to maintain a stable trajectory within the fluctuation range witnessed in recent years.

3. Drugs included in the catalog added to the negotiation queue:This year’s negotiations included 14 drugs already listed in the National Reimbursement Drug List (NRDL), all of which were successfully renegotiated. Notably, these 14 products were not even included in the previously disclosed list of candidates that had passed formal review. This proactive move by the national healthcare security administration aims to drive further price reductions for NRDL-listed drugs. If this approach becomes a regular practice, it could emerge as the third major pathway for cost containment of reimbursed drugs, following volume-based procurement and NRDL access negotiations.

4. Further improvement of the information disclosure system:This year’s disclosure of information regarding the national medical insurance negotiations has added the publication of the list of drugs that passed the formal review, building upon the 2019 framework, thereby providing the public with maximum transparency for oversight purposes. Regarding specific drug information, only the list of successfully negotiated drugs is disclosed, while the list of drugs entering the negotiation process is not made public. In line with the 2019 practice, the disclosure of information on successfully negotiated drugs continues to allow for the non-disclosure of final prices for certain medications. Overall, this approach balances public oversight with a strong commitment to respecting the privacy and interests of all pharmaceutical companies participating in the medical insurance negotiations.

In addition, there are several other key points of concern.

For example, the 17 drugs that were included in the National Reimbursement Drug List (NRDL) through price negotiations in 2018 underwent a new round of negotiations this year. Ultimately, 13 drugs successfully renewed their contracts, while the other four products are no longer listed in the “Negotiated Drugs During the Agreement Period” section recently disclosed by the National Healthcare Security Administration.

VCBeat’s comparison of the 751 drugs that passed the formal review revealed that the four drugs that failed to successfully renew their contracts were not included in the list of those passing the formal review. Given that the formal review is merely a preliminary check on the completeness of submitted materials, and considering that the originator companies for these four products are all top-tier global pharmaceutical firms with extensive experience in national medical insurance negotiations, the likelihood of material-related issues is relatively low. It is more probable that the pharmaceutical companies voluntarily chose to forgo contract renewal for these products.

This scenario mirrors that of 2019. During the 2019 negotiations, four drugs that had successfully secured renewed coverage in the 2017 negotiations failed to reach an agreement, with these products also originating from four major international pharmaceutical companies. In this year’s national medical insurance negotiations, two of these drugs—fulvestrant injection and tolvaptan tablets—passed the formal review but ultimately failed to be included in the National Reimbursement Drug List (NRDL).

In contrast, all 13 drugs that passed the formal review for renewal this year successfully renewed their contracts. Regarding the specific price reduction ranges, although only three drugs disclosed their final negotiated prices, two of them successfully renewed without further price reductions.

This further corroborates our earlier prediction regarding the stabilization of national medical insurance negotiations.Successful negotiations without price reductions may indicate that the National Healthcare Security Administration (NHSA) considers current prices already aligned with the clinical value of the drugs, rendering further price cuts unnecessary. This also demonstrates that healthcare insurance negotiations are not solely “price-driven,” unlike volume-based procurement. The ultimate goal of such negotiations is to align drug prices with their clinical value, thereby enabling the healthcare insurance system to cover a broader patient population on an affordable basis.

During the 2019 national medical insurance negotiations, the core topic of discussion was whether PD-1 monoclonal antibodies could be included in the reimbursement list. Ultimately, among the four products under negotiation, only Innovent Biologics’ sintilimab successfully passed the negotiations.

In 2019, four new contenders joined the ranks of PD-1/PD-L1 monoclonal antibodies vying for inclusion in China’s National Reimbursement Drug List (NRDL) negotiations: camrelizumab from Jiangsu Hengrui Medicine, tislelizumab from BeiGene, durvalumab from AstraZeneca, and atezolizumab from Roche.

Apart from sintilimab, the other seven products were included in the list of drugs that passed the formal review; however, the final outcomes showed a clear polarization. Three domestically produced PD-1 monoclonal antibodies were successfully included in the National Reimbursement Drug List (NRDL), although their final prices were not disclosed, while all four imported PD-1/PD-L1 monoclonal antibodies were excluded.

The importance of inclusion in the National Reimbursement Drug List (NRDL) for domestically produced innovative specialty drugs can be roughly gauged from the market performance trends of several already-launched products.

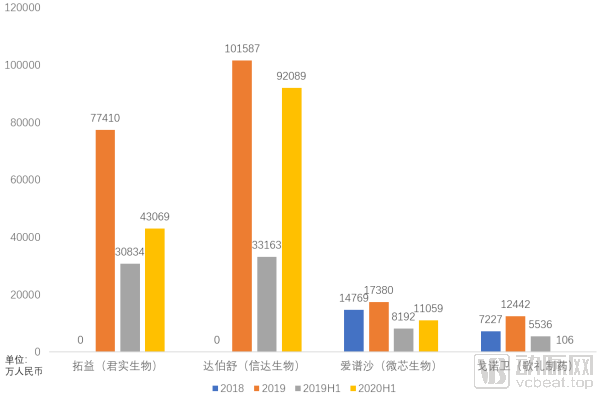

Tuoyi (toripalimab) and Tyvyt (sintilimab), both approved in late 2018, have exhibited divergent sales trajectories during the first year and a half following their market launch.

In late February 2019, the PD-1 monoclonal antibodies from Junshi Biosciences and Innovent Biologics were prescribed for the first time almost simultaneously, marking their official market launch. Although there were certain differences in their approved indications, Tuoyi (Junshi’s product) and Tyvyt (Innovent’s product) achieved nearly identical sales volumes during the first wave of commercialization in the first half of 2019. Following the national medical insurance reimbursement negotiations, Tyvyt’s sales grew rapidly, significantly surpassing those of Junshi; indeed, its sales volume in the first half of 2020 nearly matched its total annual sales for 2019.

Changes in sales volume are naturally influenced by Innovent Biologics’ marketing strategies, but national medical insurance reimbursement has also played an irreplaceable role.

MicroCore Biopharma’s Aipusha was successfully included in the National Reimbursement Drug List (NRDL) during the 2017 reimbursement negotiations and had its contract renewed in 2019. Despite undergoing two rounds of negotiations and corresponding price reductions, Aipusha’s sales have maintained steady growth over the past few years. For a novel drug that has been on the market for five years, clinical usage typically stabilizes; therefore, the continued growth under such circumstances underscores the critical supportive role played by its inclusion in the NRDL.

On the other hand, Ascletis Pharma’s situation was quite the opposite. Its core product, GanoWei (danoprevir sodium tablets), failed to secure inclusion in the National Reimbursement Drug List (NRDL) during the 2019 NRDL negotiations. By the first half of 2020, amid the dual impact of this NRDL setback and the COVID-19 pandemic, coupled with a complex market environment for antiretroviral drugs, sales of GanoWei plummeted. In this year’s NRDL negotiations, Ascletis Pharma suffered consecutive setbacks with two of its products: GanoWei (danoprevir sodium tablets) and XinLiLai (ravidasvir hydrochloride tablets).

Therefore, for domestically produced innovative specialty drugs, most Chinese-made products have only been approved within China and have not yet entered overseas markets. As the most powerful payer in China, inclusion in the National Reimbursement Drug List (NRDL) has effectively become an imperative mandate for these domestic innovators. Consequently, the inclusion of four domestically produced PD-1 monoclonal antibodies in the NRDL this time was largely anticipated.

For the National Healthcare Security Administration, including all products with the same target in the national reimbursement drug list aligns with the national strategic direction of promoting the development of innovative and specialty pharmaceuticals, while also preserving room for future price negotiations on these products.

In terms of imported products, all four imported PD-1/PD-L1 inhibitors were excluded. Combined with the data we analyzed earlier, the eight products that failed to renew their contracts in 2019–2020 were all imported products, and six of them may have voluntarily withdrawn from this year’s national reimbursement drug list (NRDL) negotiations. It appears that imported products are not faring well in the NRDL negotiation process.

(Based on publicly available information; results may be inaccurate)

In this regard, our statistical analysis reveals that among the drugs successfully included in the National Reimbursement Drug List (NRDL) through price negotiations between 2017 and 2019, the average price reduction for imported products was significantly higher than that for domestically produced products. Given the NRDL negotiation process, pharmaceutical companies must ensure their first two bids do not exceed the National Healthcare Security Administration’s (NHSA) target price by more than 15% to qualify for further price discussions. It is highly likely that the NHSA’s expected price reductions for imported products were generally higher than those for domestically produced ones. This may be one of the reasons why imported products face greater challenges in NRDL negotiations.

The National Healthcare Security Administration’s target price is relatively high, which is inextricably linked to the inherently high prices of imported drugs. Most of these imported drugs are novel and specialized pharmaceutical products. Beyond basic tariffs and transportation costs, three main factors contribute to their high pricing:

1. Recoup R&D Costs:New specialty drugs require substantial capital support from early-stage research and development through clinical development. Therefore, after successful market launch, subsequent sales must not only cover production and marketing costs but also recoup the costs incurred during drug development, including expenses associated with failed drug candidates. The optimal sales period for a new specialty drug spans the few years between market launch and patent expiration. To rapidly recover significant costs within this short timeframe, high pricing is virtually the only viable strategy.

2. Low Bargaining Power of Payers:Most novel specialty drugs target therapeutic areas that currently lack high-quality solutions, serving as essential necessities for patients and creating a near-monopolistic landscape. In this environment, patients have virtually no bargaining power over treatment options. Even if pharmaceutical companies set exorbitant prices, patients are compelled to accept them. While pharmaceutical firms do consider the target population’s ability to pay and the net profit margin of drug sales when designing product pricing, the ultimate decision-making authority rests with the manufacturers.

3. Balancing Global Prices:The pharmaceutical market is a globalized one, with the United States being the largest pharmaceutical market worldwide and also having the highest drug prices. Pharmaceutical companies need to balance product pricing across the global market while considering domestic prices. Domestic product pricing can be slightly lower but should not be excessively low. The "Patient Assistance Programs" frequently used for oncology drugs in China are designed with consideration for the affordability of domestic patients, aiming to secure pricing flexibility through drug donations and thereby balance global pricing.

After comprehensive consideration of several factors, although the production costs of new specialty drugs are not particularly high, pharmaceutical companies still need to sell them at high prices due to various reasons. This also means that multinational pharmaceutical companies need to take all aspects into account during the process of participating in medical insurance negotiations, and it is difficult to reach an agreement with the expectations of the National Healthcare Security Administration on the pricing of certain drugs. Moreover, this situation is unlikely to be alleviated in the short term.

Taking PD-1/PD-L1 monoclonal antibodies as an example, while domestically produced PD-1 inhibitors remain available as alternatives, the exclusion of two PD-L1 inhibitors from coverage has significantly impacted treatment options for many patients. Particularly amid the influx of numerous new global drugs into the Chinese market, addressing reimbursement issues for these products is likely to become one of the core considerations for the National Healthcare Security Administration in its next steps.

Among the three primary reasons mentioned above, neither R&D costs nor global pricing can be regulated externally by pharmaceutical companies. Therefore, enhancing the bargaining power of payers is virtually the only way to incentivize pharmaceutical companies to offer price concessions on new specialty drugs.

While individual patients lack bargaining power, insurers covering large patient populations possess significant leverage in negotiations with pharmaceutical companies. The market strategy of exchanging price for market share is once again evident in the collaboration between insurers and pharmaceutical firms.

With coverage extending to over 95% of the population in China, the National Healthcare Security Administration (NHSA) naturally holds the strongest bargaining power. The NHSA reimbursement negotiations are precisely this pricing negotiation process between the state healthcare security system and pharmaceutical companies. As stated in the widely circulated “soulful price slashing” video from late 2019, “It is now our entire country that is negotiating with you.” It is precisely due to its vast coverage that the national healthcare security system possesses the leverage to negotiate with pharmaceutical companies.

In this regard, specialty drug insurance focusing on new and specialized drugs shares a similar logic with national medical insurance reimbursement negotiations. However, specialty drug insurance offers a narrower scope of coverage, targets a more precise patient population, and comes at a relatively lower cost, thereby providing an alternative pathway for patients to afford new and specialized medications.

So, under the current trend of medical insurance negotiations, in which direction will specialty drug insurance move?

The initial advantage of specialized drug insurance lay in leveraging the time lag between the domestic approval of new specialty drugs and their inclusion in the national medical insurance scheme, thereby providing patients with payment coverage for these medications through flexible and dynamic formulary adjustments.

However, under the current landscape of national medical insurance negotiations, this year’s negotiation cycle has been advanced from “products approved in the previous year” to “products approved before August of the current year,” significantly shortening the window period between drug approval and inclusion in the national reimbursement drug list (NRDL). This measure directly impacts the viability of the commercial model for specialized drug insurance. If the national medical insurance continues to incorporate newly approved products with such efficiency, the window of opportunity for specialized drug insurance will become increasingly narrow.

Therefore, after several years of development in specialty drug insurance products, and with the further advancement of the Hainan Boao Lecheng International Medical Tourism Pilot Zone, these products have found a new direction—covering global pharmaceuticals.

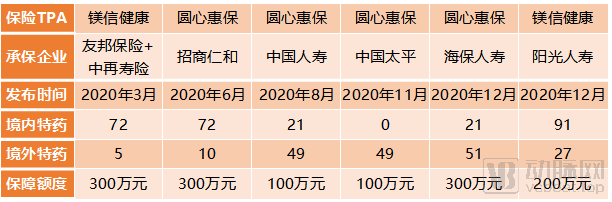

In March 2020, AIA Group, in partnership with China Re Life and Medbanks Health, launched China’s first special drug insurance covering both domestic and overseas medications. This innovative product, named “Guardian Health,” leveraged the open policies of the Boao Lecheng International Medical Tourism Pilot Zone to expand coverage beyond the 72 special drugs already approved in China to include five additional specialty drugs approved only overseas.

On the other hand, Yuanxin Huibao has partnered sequentially with China Merchants Renhe Life Insurance, China Life Insurance, China Taiping Insurance, and Haibao Life Insurance to launch four global specialty drug insurance products. Coupled with the product launched by Medbanks Health in collaboration with Sunshine Life Insurance at the end of the year, there are currently as many as six global specialty drug insurance products available in Hainan.

In terms of product design, due to the special policies of the Medical Tourism Pilot Zone, several products require patients to undergo clinical evaluation before ultimately traveling to Hainan for diagnosis and treatment. The products can be categorized into two main types based on the proportion of domestic versus overseas new drugs. The three products offered by AIA + China Re Life Insurance, China Merchants Renhe Life Insurance, and Sunshine Life Insurance focus more on domestic new drugs; whereas those from China Life Insurance, China Taiping Insurance, and Haibao Life Insurance place greater emphasis on overseas new drugs.

Peng Xuan, CEO of Yuanxin Huibao, which has successively collaborated on four global specialty drug insurance products, stated to VCBeat: “Overall, the national medical insurance negotiations are certainly a positive development. They help draw greater attention to the medical insurance system and enable more people to access medications at lower costs. This aligns with our ongoing efforts. In the specialty drug insurance sector, we remain committed to this path and will continue to expand our coverage, extending from specialty drugs to general pharmaceuticals, as well as into other areas such as chronic disease management.”

Following the opening of the Hainan Boao Lecheng International Medical Tourism Pilot Zone, on November 25, 2020, the National Medical Products Administration (NMPA), in conjunction with eight other ministries and commissions, issued the Work Plan for the Innovative Development of Drug and Medical Device Regulation in the Guangdong-Hong Kong-Macao Greater Bay Area. After the implementation of the Work Plan, the approval authority for the use of clinically urgent drugs already marketed in Hong Kong and Macao by designated medical institutions operating in the nine mainland cities of the Guangdong-Hong Kong-Macao Greater Bay Area was transferred from the NMPA to the People's Government of Guangdong Province, as authorized by the State Council.

Products already marketed in the United States or Europe can enter the Hong Kong market directly. Therefore, following the integration of the Guangdong-Hong Kong-Macao Greater Bay Area, in addition to Hainan, nine cities in Guangdong will also become regions where new global drugs are accessible within China. Of course, this policy is currently in a pilot phase and will require a considerable period before it reaches the level of openness seen in the Hainan Boao Lecheng International Medical Tourism Pilot Zone.

“Hainan remains a relatively favorable choice within the next three years. Currently, policies promoting the integration of the Guangdong-Hong Kong-Macao Greater Bay Area are accelerating adjustments and innovations. The University of Hong Kong-Shenzhen Hospital is in a pilot phase, subject to product catalog controls, and its services are primarily oriented toward clinical applications, which means broad public accessibility may not be achieved quickly. At present, Hainan is expected to maintain its period of policy dividends over the coming three years,” said Peng Xuan.

Regarding the payment for new specialty drugs, in addition to specialty drug insurance and the national basic medical insurance, the “Huimin Bao” (city-specific supplemental medical insurance), which gained significant popularity in 2020, has provided a promising approach to covering patients’ out-of-pocket expenses for these drugs after basic medical insurance reimbursement. Many new specialty drugs still require patients to bear substantial out-of-pocket costs even after coverage by basic medical insurance. This financial burden is particularly pronounced among urban and rural residents enrolled in the basic medical insurance scheme, which typically offers lower reimbursement rates. The emergence of Huimin Bao, characterized by high deductibles and coverage for critical illnesses, serves as a robust supplement to basic medical insurance payments.

Overall, the synergy among the National Basic Medical Insurance, Special Drug Insurance, and City-Specific Supplementary Medical Insurance (Huimin Bao) has established a comprehensive payment and coverage system for new specialty drugs. The National Basic Medical Insurance has incorporated most new specialty drugs already marketed in China through price negotiations. Special Drug Insurance covers new specialty drugs not included in the National Basic Medical Insurance and further extends coverage to global new specialty drugs not yet launched in China. Huimin Bao serves as a supplement to the National Basic Medical Insurance, minimizing patients’ out-of-pocket expenses.

As a critical measure for the inclusion of new and specialized drugs in the national medical insurance scheme, drug price negotiations have finally stabilized after several years of development. With the normalization of these negotiations, Huiminbao (city-specific supplemental commercial health insurance) and specialized drug insurance will also stabilize, ultimately achieving comprehensive and stable development of China’s payment system for new and specialized drugs.