Major Players Like Mindray and Ropion Expand into Pet Healthcare; Newrui Leads Funding Surge as the Sector Enters High-Growth Phase – 2020 Annual Review

As the “loneliness economy” continues to gain momentum, pet-ownership attitudes evolve, and consumption upgrades take hold, China’s pet-owning population is expanding rapidly, making the pet economy a new hotspot.

As a vital component of the pet economy, veterinary care has experienced rapid growth alongside the sector’s overall rise. Compared with the increasingly competitive and saturated pet food industry, veterinary care clearly holds greater potential for development.

In 2020, capital interest in the pet healthcare market remained strong. Although the number of financing events was lower than during the 2018 peak, several large-scale funding rounds emerged. Notably, industry leader New Ruipeng completed a strategic financing round worth hundreds of millions of U.S. dollars, with investors including major corporations such as Tencent, Country Garden, and Boehringer Ingelheim. Meanwhile, reports indicated that New Ruipeng was planning to initiate an initial public offering (IPO).

The financial report of Ringpu Biology, a large veterinary pharmaceutical group, for the first three quarters of 2020 also reflects the booming pet healthcare market. Ringpu Biology’s pet drug revenue grew by 173% in the first three quarters, far outpacing its livestock (up 98%) and poultry (up 43%) business segments.

Next, VCBeat will analyze financing events, newly registered enterprise information, upstream and downstream industry chain dynamics, and major policies in the pet healthcare sector in 2020, highlighting the changes that occurred in the industry during that year.

Capital Tilts Toward Leading Enterprises

Pet Healthcare Emerges as a Hot Sector in 2020

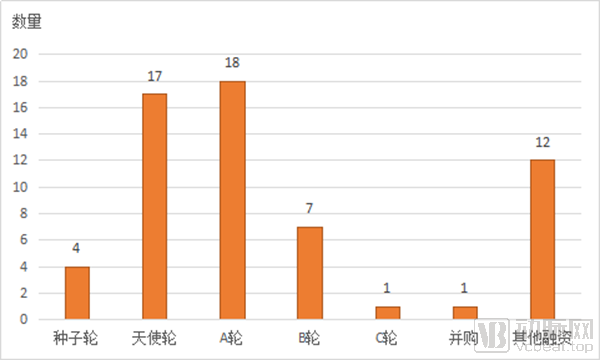

The pet healthcare industry encompasses subsectors such as veterinary pharmaceuticals, medical devices, clinical services, diagnostic testing, and pet insurance. VCBeat has compiled financing data across these subsectors from 2015 to 2020, identifying a total of 61 financing events involving 31 companies.

Distribution of Financing Rounds from 2015 to 2020

In terms of funding rounds, the vast majority of companies are at the angel or Series A stage, indicating that the sector is still in its early development phase. Only one company, Ruipai Pet Healthcare, has reached Series C. With a network of more than 300 chain pet hospitals across China, Ruipai Pet Healthcare attained a valuation of $7 billion after receiving investment from Mars, Incorporated in December 2019.

In 2020, the industry also witnessed an acquisition. In July, Kanghua Biological announced its plan to acquire a 10% equity stake in Yiyao Biological, an animal vaccine R&D enterprise, for RMB 28 million, and obtained the exclusive agency sales rights for Yiyao Biological’s “Rabies Inactivated Vaccine (PV/BHK-21 Strain)” once the product met the conditions for market sale. This acquisition enabled Kanghua Biological to enter the veterinary rabies vaccine sector, and its stock hit the daily upper limit following the announcement.

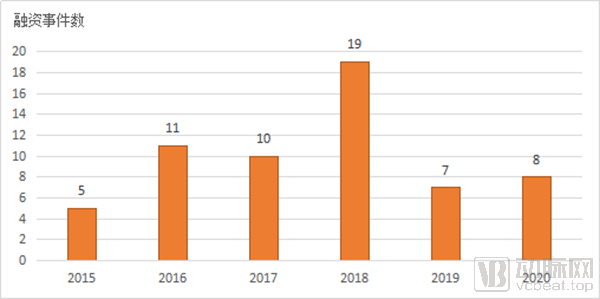

Number of Financing Events from 2015 to 2020

As the foundation of the pet healthcare industry has been further strengthened and pet owners have placed increasing emphasis on their pets’ health, various types of capital began to flow intensively into the sector in 2016. By 2018, the industry’s ability to attract investment had significantly improved, with the number of financing and investment deals reaching a peak. In 2018, Ruipai Pet Healthcare secured two rounds of funding totaling RMB 500 million. Although the number of financing deals declined in 2019 and 2020, investor preference for leading enterprises in the sector remained strong.

In terms of the number of financing events, the pet healthcare industry saw relatively few deals in 2020, with only eight transactions; however, one significant large-scale financing round emerged. In September 2020, New Ruipeng Group completed a strategic financing round worth hundreds of millions of U.S. dollars, backed by Tencent, Country Garden, and Boehringer Ingelheim.

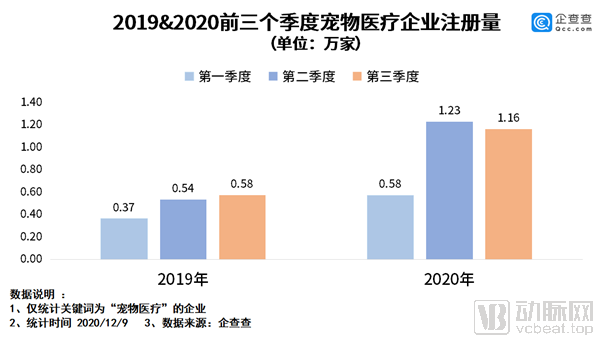

The surge in newly registered enterprises in 2020 also reflects the booming interest in the pet healthcare industry.

According to data from Qichacha, a total of 30,000 new enterprises related to pet healthcare were registered in China during the first three quarters of 2020, representing a year-on-year increase of 50%. Affected by the pandemic, the number of registrations was lowest in the first quarter at 5,800, rose to 12,300 in the second quarter, and stood at 11,600 in the third quarter. As these newly registered companies gradually grow and expand, the industry is poised to experience a peak period of financing.

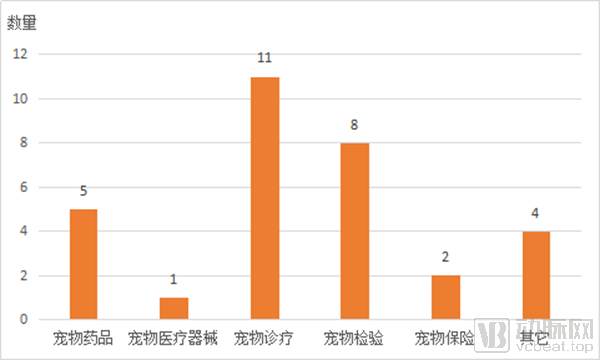

Distribution of Financing Events by Sector, 2015–2020

From the perspective of sub-sectors, the pet diagnosis and treatment sector leads by a wide margin in both the number of financing deals and the total amount raised, with 11 pet diagnosis and treatment companies securing funding. The pet pharmaceuticals and pet diagnostics sectors have also attracted significant capital attention. How did each sub-sector of the pet healthcare industry perform in 2020? VCBeat has analyzed and reviewed the developments within these sub-sectors.

Pet Healthcare: Low Chain Hospital Penetration, Deep Online-Offline Integration

From a financing perspective, the number of funding events in 2020 decreased compared to previous years, with capital concentrating on leading enterprises. Investors showed a stronger preference for companies with clear business models and significant growth potential. Although only New Ruipeng Group completed a strategic financing round worth hundreds of millions of US dollars in this sector in 2020, its funding amount far exceeded that of other companies. It is believed that with the influx of capital, the pet diagnosis and treatment sector still holds substantial room for future growth.

The pet healthcare sector primarily comprises two categories: offline veterinary hospitals and online consultation platforms.

Offline veterinary clinics are the core of pet diagnosis and treatment, mostly operating as single-store entities. The "2020 White Paper on China's Pet Medical Industry" shows that currently, about 75% of pet hospitals in China are non-chain hospitals, with small-scale hospitals still being the main body.

The centralization and specialization of veterinary hospitals are becoming an inevitable trend. In the past two years, high-quality chain hospital groups such as New Ruipeng Group and Ruipai Pet Hospital have experienced rapid expansion. In January 2019, New Ruipeng Group, formed through a partnership between Ruipeng Pet Hospital and Hillhouse Capital, announced the completion of its integration, thereby establishing China’s first pet healthcare group with over 1,000 clinics. Currently, New Ruipeng operates approximately 1,400 veterinary hospitals across more than 90 cities in China, while Ruipai Pet Hospital manages over 300 facilities.

New Ruipeng and Ruipai, the two major chains of pet hospital groups, have already achieved considerable scale and established a competitive advantage within the industry. In other regions, several regional chain hospitals have also emerged, such as Jiawen Pet Hospital in East China, Kangxu Pet Hospital in Henan Province, and Paimet, which is deeply rooted in Northeast China.

The rise of internet technology has given birth to online veterinary consultation platforms. Online consultations can effectively address current challenges in the pet healthcare industry, such as the shortage of veterinarians and the geographical and temporal constraints limiting access to specialist care. By providing more convenient, efficient, and high-quality medical health services for pets, this model has become an emerging trend.

However, online consultations can only address minor health inquiries; the majority of diagnostic and treatment needs still require visits to offline hospitals. Consequently, the deep integration of online and offline services has become a trend. For instance, Mogu Pet Doctor, an online veterinary consultation platform, opened its first physical hospital in November 2020, aiming to establish a model that combines online consultations with offline medical care, thereby creating a closed-loop service ecosystem encompassing online consultations, offline hospital visits, and online medication purchases.

Meanwhile, offline veterinary hospitals are undergoing a period of consolidation and facing intensified competition, necessitating online channels for patient acquisition and service enhancement. Veterinary hospital chains of varying sizes, including New Ruipeng, Ruipai, and Ai Chong Yisheng, are all expanding into the online consultation sector. In August 2020, New Ruipeng entered into a strategic partnership with Meituan to jointly develop features such as “online veterinary consultations” and “online vaccine appointment scheduling.”

As offline hospitals increasingly establish online consultation services and demand for digitalization surges, opportunities have emerged for enterprises providing IT solutions to the pet healthcare sector. AiChong Technology, which initially focused on online veterinary consultation services, has now evolved into a one-stop service platform for the pet industry, offering SaaS-based store management systems to more than 30,000 pet hospitals and supply stores across China.

Furthermore, the pet healthcare industry has high entry barriers, with stringent requirements for veterinarians’ professionalism and technical expertise. Regulatory authorities mandate that only qualified professionals holding a Veterinary Drug Operation License, an Animal Diagnosis and Treatment License, and a licensed veterinarian credential are permitted to provide medical services such as pet vaccination and pharmaceutical sales.

The shortage and structural imbalance of veterinarians have become a major factor constraining industry development. A research report by CICC estimates that the overall talent demand in the pet industry is approximately 368,000, while the current number of licensed veterinarians is only about 77,000. With only around 10,000 individuals passing the licensing examination each year, the talent gap is unlikely to be filled in the short term.

Some companies are already making efforts to address the shortage of veterinarians. For example, in 2020, Ruipai Pet Medical Group launched its “Ten-Hundred-Thousand Talent Development Program,” aiming that same year to cultivate 16 internationally recognized leading experts, 147 mid-career and young elite specialists, and more than 1,000 outstanding veterinary professionals, with tailored, one-on-one development plans designed for individuals based on their specific profiles.

Pet Pharmaceuticals: High Industry Barriers, Lack of Innovative Drugs

Pharmaceuticals are the primary means of treating pets. Against the backdrop of volume-based procurement reshaping the human pharmaceutical and medical device markets, this rapidly growing potential market, valued at hundreds of billions of yuan, is attracting a surge of domestic and international pharmaceutical companies vying for entry and numerous investment institutions flocking to invest.

Companies involved in the pet pharmaceutical industry can be broadly categorized into three groups: human pharmaceutical R&D companies, livestock and poultry pharmaceutical R&D companies, and pure-play pet pharmaceutical R&D companies.

Currently, multinational corporations such as Pfizer, Boehringer Ingelheim, Eli Lilly, and Bayer, which dominate the majority of China’s pet pharmaceutical market, are primarily human pharmaceutical R&D enterprises. Among them, Zoetis, a subsidiary of Pfizer, is a global leader in animal health, serving animal health companies, livestock and poultry producers, and companion animal owners in over 100 countries worldwide. According to reports, Zoetis achieved global revenue of $1.8 billion in the third quarter of 2020, representing a 15% increase, with adjusted net income of $524 million, up 20%. Meanwhile, benefiting from China’s favorable market environment, the expansion of digital marketing, and continuous veterinary education, the company has seen strong growth in its pet product segment in China.

In China, human pharmaceutical companies such as Hisun Pharmaceutical, Tongren Pharmaceutical, and Harbin Pharmaceutical Group have also entered the pet medication market. Hisun Pharmaceutical has broken China’s reliance on imported deworming medications; its product Hai Le Miao is the only domestically approved dewormer for cats, while Hai Le Chong is the only milbemycin oxime-based dewormer for dogs approved for marketing in China. Hanwei Biomedical Technology has developed pet-specific drugs such as Mobixin and Tanbixin. Saifute and Yisaning, pet-specific prescription drugs under Harbin Pharmaceutical Group, have both obtained national regulatory approvals.

Many pharmaceutical R&D companies specializing in economic animals have also turned their attention to the pet medication sector. Ringpu Biology, a leading domestic veterinary drug R&D enterprise, offers comprehensive solutions for animal disease prevention and control. Its portfolio includes the research, development, production, and sales of poultry and livestock vaccines, veterinary drug formulations (such as chemical drugs, functional additives, traditional Chinese medicine veterinary drugs, and pet medications), and veterinary active pharmaceutical ingredients (APIs). It is one of the few veterinary pharmaceutical companies in China whose products cover animal disease prevention, diagnosis, treatment, growth promotion, and immune system regulation.

In recent years, Ringpu Biology has aggressively expanded its presence in the pet pharmaceutical sector. Financial reports indicate that Ringpu Biology’s pet drug revenue grew by 173% in the first three quarters of 2020, significantly outpacing its livestock (98% growth) and poultry (43% growth) business segments. Recombinant Canine Alpha-Interferon (lyophilized) was a key product in Ringpu’s 2020 strategic lineup; it received regulatory approval in March 2020 as China’s first veterinary interferon product expressed via recombinant Escherichia coli. Looking ahead, the company plans to further strengthen its footprint in the pet care market.

Companies such as Oubofang and Beizhenbao specialize in the research and development of veterinary pharmaceuticals. In 2020, Beizhenbao, a company dedicated to R&D in pet medications and health supplements, completed an angel funding round worth tens of millions of RMB. Beizhenbao aims to develop and manufacture functional products, over-the-counter (OTC) drugs, and prescription medications for pets. Currently, the brand has launched five functional health supplement products, including Yanweile Nutritional Granules, Miaoningkang Anti-Stress Soothing Granules, and Youchongqin Oral Care Granules.

It is worth noting that China’s veterinary pharmaceutical industry is dominated by generic drug development, with a low level of innovation. Oubofang is one of the few domestic companies dedicated to the R&D of innovative veterinary drugs, having laid out the development of eight original drugs in the fields of parasiticide, pain management, dermatology, and antibiotics. In 2016, the company obtained a new drug certificate for Vetacoxib Chewable Tablets, a Class 1.1 chemical veterinary drug, marking a breakthrough from zero in China’s original veterinary chemical drugs. This achievement has also positioned China as a holder of a “Best-in-Class” product within the global $1.8 billion veterinary pain management market.

Due to shortages of veterinary pharmaceuticals and the lack of corresponding therapeutic agents for many conditions, the off-label use of human medications in animals remains prevalent in the market. Domestic companies are increasingly strengthening their research and development efforts in pet medicines. In November 2020, Bevean (phenobarbital tablets), the first dedicated prescription drug approved in China for treating epilepsy in pet dogs and cats, received approval from the Ministry of Agriculture, ending the long-standing absence of legally authorized medications for canine and feline epilepsy in the country. It is anticipated that the growing availability of species-specific veterinary drugs will gradually reduce the reliance on off-label use of human medications in animals.

Pet Diagnostics: Huge Growth Potential, Genetic Testing Becomes a Hot Service

The Pet Testing Market Is Poised to Become the Next Growth Engine for the In Vitro Diagnostics Market.

Previously, pet diagnostic testing primarily focused on infectious disease detection, with targets including canine distemper virus, canine parvovirus, canine coronavirus, Toxoplasma gondii antigens/antibodies, and inflammatory markers such as C-reactive protein, procalcitonin, and serum amyloid A. In recent years, the molecular diagnostics market has gained significant momentum, making pet genetic testing a hotspot for startups. In March 2020, Sinogene, a pet genetic testing company, completed a Series B financing round worth tens of millions of RMB.

Pet genetic testing enables intelligent analysis of multidimensional health data, including individual pet genes and gene-environment interactions. This approach effectively uncovers in-depth insights into pet health and disease risks, allowing veterinary hospitals to develop personalized health management plans.

The vast potential of the pet healthcare market has also attracted many companies originally focused on human medicine to expand into the pet diagnostics sector.

In October 2020, Mindray Medical established a new subsidiary focused on animal healthcare technology—Shenzhen Mindray Animal Medical Technology Co., Ltd.—with a registered capital of RMB 200 million. Its business scope covers the research and development, sales, and technical services of veterinary medical devices, consumables, and biological products. Prior to this, Mindray had already launched multiple veterinary diagnostic instruments. With the establishment of this dedicated subsidiary, Mindray is set to increase its investment in the pet diagnostics sector, which is expected to make a significant contribution to the company’s future financial performance.

Furthermore, as a leading domestic POCT enterprise, Wondfo has also made inroads into the pet testing sector. In 2017, it established Wandekang to provide rapid testing products and services for pets, economically important animals, and food safety. In October 2020, Wandekang entered into a strategic partnership with Laso Bio to jointly promote the application of POCT and genetic testing in pet diagnostics.

In November 2020, in vitro diagnostics company Jinrui Biology launched its veterinary brand “Genvet” along with a new series of professional pet diagnostic equipment. The newly released products include the VP10 Biochemistry Analyzer, VH30/20 Three-Part Differential Hematology Analyzer, VH50 Five-Part Differential Hematology Analyzer, VF10 Immunoassay Analyzer, VU10 Urine Analyzer, and the VIMS Pet Management Software.

Pet Medical Devices: Mindray and United Imaging Focus on Strategic Deployment, Accelerating the Localization of Equipment

Veterinary medical devices include magnetic resonance imaging (MRI), computed tomography (CT), veterinary-specific hemodialysis machines, endoscopes, phacoemulsification systems, surgical microscopes with high-definition teaching systems, digital radiography (DR) systems, color Doppler ultrasound diagnostic instruments, and anesthesia ventilators.

As the pet population in China continues to grow, demand for veterinary medical devices is rising rapidly. Most companies manufacturing veterinary imaging equipment adapt technologies based on human medical device principles, creating opportunities for firms such as Mindray Medical, United Imaging Healthcare, and Kaipu Medical.

Mindray Medical has made breakthroughs in the field of veterinary devices, having launched more than four veterinary patient monitoring products and over ten veterinary ultrasound systems.

In November 2020, United Imaging Healthcare’s “China’s First Ultra-High-Field Animal MRI System uMR 9.4T” and the “World’s First Ultra-High-Performance Large-Animal Whole-Body PET-CT uBioEXPLORER” were officially unveiled at the 83rd China Medical Equipment Fair (CMEF).

Kap Medical, a medical imaging equipment manufacturer, has long established a presence in the veterinary medical device sector, launching products such as the Supernova Pet MRI, a magnetic resonance imaging system dedicated to pets, and the RayNova Pet DR, a digital X-ray system designed for animals. As China’s leading provider of digital X-ray detectors, iRay Technology has seen its products widely adopted in the veterinary field. According to iRay Technology’s prospectus, the company’s global market share in medical and veterinary X-ray detectors rose from 8.09% in 2017 to 12.91% in 2019, ranking first in China in 2018.

Pet medical equipment plays a crucial role in disease diagnosis and treatment. Many veterinary hospitals strive to equip themselves with high-end devices, but the high cost of imported equipment imposes a significant financial burden on these facilities. In the future, as more domestic enterprises engage in the research and development of pet medical devices, the localization of such equipment in China is just around the corner.

Pet Insurance: In Its Early Stages, Innovative Technologies Help Boost Coverage Rates

The pet insurance market is poised for rapid growth, with industry experts asserting that the widespread adoption of insurance is indispensable to achieving standardized veterinary care and transparent pricing in the pet industry.

Pet insurance is categorized into pet medical insurance, pet mortality insurance, and pet liability insurance. Key players in this sector include large comprehensive insurers such as Ping An Insurance and China Pacific Insurance, as well as startups specializing in pet insurance, such as Tips and Pet City. Among them, Ping An Insurance launched “Meng Chong Bao” (Cute Pet Insurance). China Pacific Insurance introduced “Tai Chong Ai Pet Social Security and Medical Insurance.” Tips launched its core product under the pet social security model, “Xiao Bao Er Medical Care Allowance.” Tips currently covers 240 cities across China, collaborates with over 1,000 partner hospitals, and has accumulated more than 150,000 paying members. In April 2020, it entered into a strategic partnership with Alipay, becoming the designated service provider for the pet industry on the Alipay mini-program platform.

Additionally, in April 2020, Alipay issued 400,000 pet medical insurance policies.

However, at present, the penetration rate of pet insurance in China remains low, which is closely related to the broader landscape of veterinary care. As the industry is in a phase of rapid development yet lacks standardization and maturity, issues such as overtreatment, insurance fraud, low consumer acceptance, and poor cost-effectiveness of insurance products have emerged, hindering the growth of the pet insurance market.

Relevant companies are exploring the use of new technologies to address challenges in the development of pet insurance. In May 2020, Lufax launched a “Pet Health and Medical Insurance” product, introducing intelligent pet image recognition technology for the first time; in July 2020, Alipay introduced pet nose print recognition technology; Tips has also developed a risk control system covering various stages, including insurance product development, channel selection, and subsequent claims processing.

Policy Frameworks Are Being Gradually Refined

The Pet Healthcare Industry Has a Promising Future

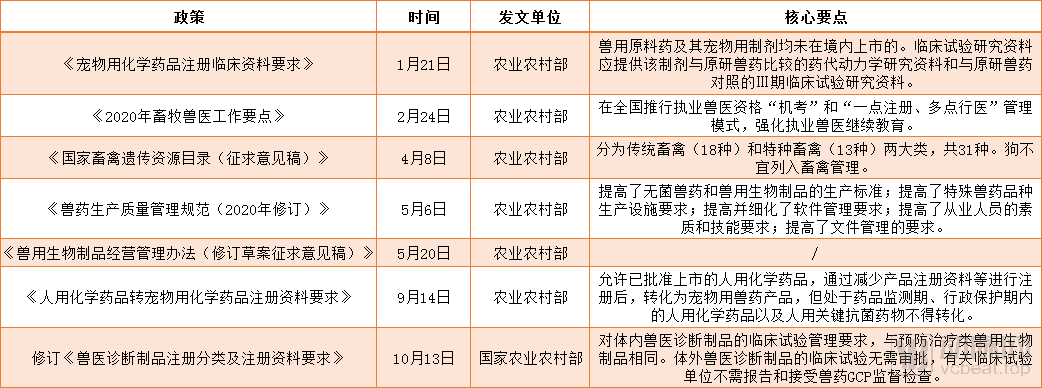

Multiple policies related to pet healthcare were issued in 2020.

In May, the Ministry of Agriculture and Rural Affairs issued the Good Manufacturing Practice for Veterinary Drugs (2020 Revision), which came into effect on June 1, 2020. Compared with the Good Manufacturing Practice for Veterinary Drugs implemented in 2002, the 2020 revision raises production standards for sterile veterinary drugs and veterinary biological products; enhances requirements for production facilities of special veterinary drug categories, while improving and detailing software management requirements; and elevates qualifications and skill requirements for personnel, as well as strengthening documentation management requirements, thereby aligning veterinary drug production management more closely with current practical realities.

In the field of diagnostics, the Ministry of Agriculture and Rural Affairs of China organized the revision of the "Classification and Registration Data Requirements for Veterinary Diagnostic Products," which came into effect on October 15, 2020. The policy stipulates that clinical trials for in vitro veterinary diagnostic products do not require approval, and the institutions conducting such trials are not required to report or undergo supervision and inspection for Good Clinical Practice (GCP) for veterinary drugs. This has further stimulated enthusiasm for the development of veterinary diagnostic products, promoted their commercial production and application, and met the needs for animal disease diagnosis and monitoring.

Previously, China’s laws and regulations concerning animal diagnosis and treatment and veterinary drugs primarily targeted economic animals, with few specialized legal provisions dedicated to pet healthcare. As the pet healthcare industry in China began to take shape, related policies have been gradually improved.

On September 14, the Ministry of Agriculture and Rural Affairs issued and implemented the "Requirements for Registration Materials for the Conversion of Human-Use Chemical Drugs to Pet-Use Chemical Drugs," stating that approved human-use chemical drugs may be converted into veterinary drug products for pets through streamlined registration processes, such as reduced submission of registration materials. However, human-use chemical drugs under monitoring periods or administrative protection, as well as key human-use antimicrobial drugs, are excluded from such conversion.

Previously, even when human pharmaceutical data were sufficient and efficacy was stable, the registration process for repurposing these drugs as veterinary medicines for pets still required the submission of extensive experimental data and literature. This resulted in prolonged trial periods and increased R&D and registration costs. The "Requirements for Registration Materials for Repurposing Human Chemical Drugs as Pet Chemical Drugs" streamlines the registration process for pet medications, accelerating the approval of veterinary drugs for pets. This facilitates the more rational utilization of existing drug resources and encourages more enterprises to actively develop relevant human drugs into veterinary medicines for pets, thereby addressing the significant shortage of clinical medications in pet diagnosis and treatment. In the future, more companies are expected to engage in pet drug R&D, converting a greater number of human drugs into pet medications.

It is evident that current policies primarily focus on diagnosis and treatment, pharmaceuticals, and diagnostic procedures, with insufficient attention paid to the niche sector of pet insurance.

The pet healthcare sector remains a blue-ocean market, characterized by low penetration and significant growth potential. Industry experts believe that China’s pet healthcare industry has not yet entered its explosive growth phase; as a large number of pets subsequently enter the high-incidence period for diseases, medical demand will increase substantially.

In the future, regulatory oversight of pet healthcare policies will intensify, leading to a more standardized industry. Companies will adopt refined management practices, and the sector as a whole holds substantial growth potential. This trend will undoubtedly create more opportunities for practitioners in pet diagnostic and treatment institutions, pharmaceutical manufacturers, medical device and equipment producers, brand owners, and industry investors. Meanwhile, for startups, traditional markets such as conventional clinical services and generic pet drugs have entered a phase of consolidation. It is therefore more crucial to focus on innovative and distinctive projects to seize emerging opportunities in the development of pet healthcare.