Six Policy Pathways and Four Major Trends Shaping China's Medical Reform: A 2020 Review of Medical Consumables and Hospital Policies at the Dawn of the Second Decade

Editor’s Note: This article is contributed by the WeChat official account “Yipu Youcai.” Reproduction without permission is prohibited.

This year marks the beginning of the second decade of China’s new healthcare reform, and it is also the anticipated year when the reform “enters deep waters.”

This year, the financial anxiety of public medical institutions has become particularly pronounced. Major policies such as zero mark-up on drug sales, Diagnosis-Related Groups (DRG), and Big Data Diagnosis-Intervention Packet (DIP) have continued to take effect, while the recurrent waves of the COVID-19 pandemic have sharply increased cost pressures for these institutions. In June 2020, the National Health Commission, together with the National Administration of Traditional Chinese Medicine, issued the Notice on Launching the “Year of Economic Management” Campaign in Public Medical Institutions, explicitly requiring public medical institutions to adopt the mindset of “tightening their belts.”

This year, the National Health Commission has increasingly strengthened its focus on hospital operational management. Just last week, the Commission issued the “Guiding Opinions on Strengthening Operational Management in Public Hospitals,” aiming to further promote high-quality development of public hospitals and enhance the scientific, standardized, refined, and informatized levels of hospital operational management.

This year, the volume-based procurement (VBP) of high-value medical consumables, a topic of public speculation for two years, was finally implemented. Although the National Healthcare Security Administration’s intense “soul-searching” price negotiations remain vivid in memory, the over 94% price reduction for coronary stents still sent shockwaves through the industry.

This year, the National Healthcare Security Administration (NHSA) has increasingly demonstrated its “strong” stance. With intensified unannounced inspections, the continuous advancement of DRG pilots, and efforts to formulate the first national-level medical consumables reimbursement list, no one can predict where the NHSA’s next move in its tightly orchestrated reforms will land.

The only clear trend is that the purchasing power of medical insurance is growing increasingly strong, and certain rigid frameworks are being restructured. The main thread of healthcare reform will continue to revolve around the two major supply-and-demand negotiation markets—medical insurance versus pharmaceuticals and consumables, and medical insurance versus hospitals—gradually advancing toward value-based healthcare.

Just as the direction of tidal currents ultimately reshapes the riverbed, following the main thread of healthcare reform, this 2020 year-end review categorizes policies by stakeholder into two groups—medical consumables and public medical institutions—to comprehensively map out the policy regulatory landscape of 2020, with the aim of drawing insights from the present to inform the future.

To be precise, the curtain on China’s national reform of medical consumables was raised in 2019.

In June of that year, the National Health Commission, in conjunction with the National Administration of Traditional Chinese Medicine, issued the Measures for the Management of Medical Consumables in Medical Institutions (Trial), which has been hailed by the industry as the most detailed set of regulations on consumables management in the past decade. The Measures provide specific regulatory requirements for the entire lifecycle management of medical consumables, including selection, procurement, acceptance, and storage.

One month later, a landmark policy document was officially released. The State Council issued the “Reform Plan for the Governance of High-Value Medical Consumables,” setting the direction for high-value medical consumable reform in areas such as “eliminating markups on consumables, curbing artificially inflated prices, reducing overuse, and exploring volume-based procurement.” With this, the fundamental framework for medical consumable reform was established.

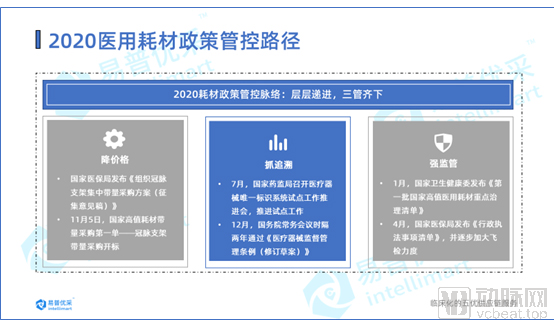

Focusing on 2020, the policy regulation of medical consumables can be summarized into three main lines.

The first initiative targets “price reduction”: With volume-based procurement (VBP) as the core, national and local efforts are advancing in tandem, marking the official entry of China’s high-value medical consumables industry into the VBP era. The second focuses on “traceability”: Continuously advancing pilot programs for Unique Device Identification (UDI) and exploring a full lifecycle management system from source manufacturing to final clinical use. The third strengthens regulatory oversight; for instance, the National Health Commission issued the first batch of key governance lists for high-value medical consumables early this year, while the National Healthcare Security Administration has conducted increasingly stringent and frequent unannounced inspections. These measures leverage administrative tools to gradually standardize procurement and usage practices for medical consumables. Let us examine each in detail.

The Debate Over Volume-Based Procurement of High-Value Medical Consumables Has Long Been a Topic of Public Discussion.

“Lack of Consistency Evaluation for High-Value Medical Consumables Hinders Volume-Based Procurement” “Volume-Based Procurement for High-Value Medical Consumables Is Only a Matter of Time” “Which Category of High-Value Medical Consumables Will Be Targeted First for Volume-Based Procurement?” “Will Prices Plummet as Sharply as Those of Pharmaceuticals?”

All speculation and doubt were dispelled on the third day of July 2020.

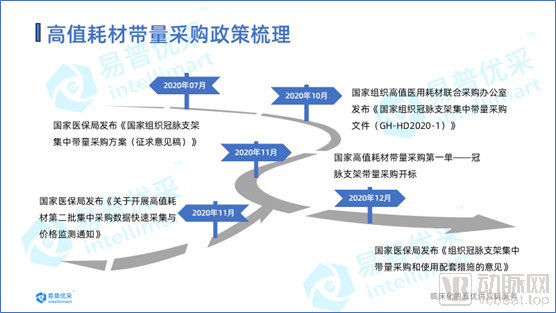

On July 3, the National Healthcare Security Administration released the “National Centralized Volume-Based Procurement Plan for Coronary Stents (Draft for Comments).” Subsequently, on October 16, the Joint Procurement Office for National Centralized Procurement of High-Value Medical Consumables issued the “National Centralized Volume-Based Procurement Document for Coronary Stents.” With this, the long-anticipated volume-based procurement of high-value medical consumables has finally been implemented.

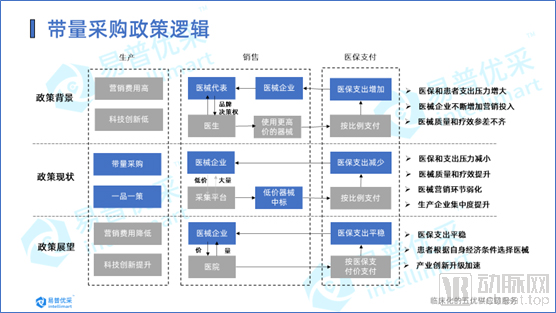

The policy logic behind volume-based procurement (VBP) for high-value medical consumables is similar to that for pharmaceuticals: both aim to lower artificially inflated prices and save medical insurance funds by exchanging volume for price. For the industry, medical device companies can leverage their comprehensive advantages in R&D, production, quality control, and management to win bids with low prices while ensuring quality. With the volume guaranteed by the payer—the medical insurance system—companies can reduce channel and terminal promotion costs. This frees medical device enterprises from disordered distribution channels, enabling them to strengthen innovative R&D, avoid homogeneous competition, and guide the industry toward innovation and upgrading.

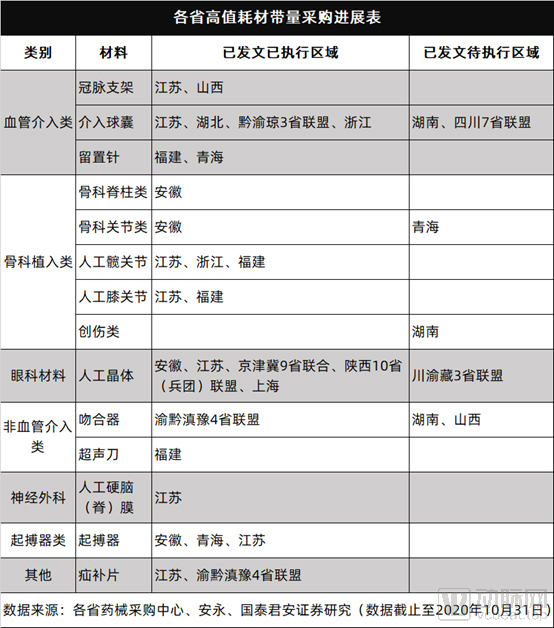

Unlike pharmaceuticals, local explorations of volume-based procurement (VBP) for high-value medical consumables have been no less significant than national-level initiatives. According to research statistics from Guotai Junan Securities, the national VBP for coronary stents was completed on November 5, 2020, with the average terminal price of the 10 selected products dropping by more than 90%. As of November 20, 2020, local VBP initiatives included six completed or ongoing provincial alliance procurements, 11 independent procurements by provinces and municipalities directly under the central government, and over 30 prefecture-level (including alliance) procurements. These efforts were primarily concentrated in three major fields: cardiovascular intervention, orthopedics, and ophthalmology, achieving an average terminal price reduction of approximately 60%. China’s high-value medical consumables industry has officially entered the era of volume-based procurement.

Regarding future plans for volume-based procurement, Zhong Dongbo, Director of the Department of Pharmaceutical Prices and Tendering and Procurement under the National Healthcare Security Administration, explicitly stated in an interview that, given the difficulty in establishing bioequivalence evaluations for medical consumables, centralized procurement of high-value medical consumables will adhere to a “one product, one strategy” approach, with procurement schemes meticulously tailored to each item. He emphasized that national-level volume-based procurement would continue to advance, targeting high-value medical consumables characterized by large volumes, high prices, and ease of data collection, with the goal of achieving basic coverage by 2022.

Regarding the impact on enterprises, Zhong Dongbo stated that although procurement volumes have seen a significant decline, the reduced prices are not substantially different from the actual ex-factory prices of enterprises. With market expansion, there remains objective revenue, allowing enterprises to maintain normal operations.

From the “4+7” pilot program for pharmaceuticals to its nationwide rollout, and further to coronary stents, volume-based procurement has undoubtedly been the most prominent “trump card” initiative undertaken by the National Healthcare Security Administration in the two years since its establishment. However, subsequent issues warrant further reflection and discussion: Will the market share of stainless steel stents be squeezed out by cobalt-based stents? Will doctors’ extensive use of low-priced bid-winning products restrict the promotion of innovative products? Will public hospitals gradually withdraw from their leading position in academic innovation?

How Important Is UDI Implementation for Medical Consumables?

As the “electronic ID card” for medical devices, the Unique Device Identification (UDI) system serves as the foundation for the unique and precise identification of medical devices. It spans all stages of the entire supply chain, including production, distribution, and use. UDI has become a focal point and hot topic in international medical device regulation, and it is also a key instrument for China to advance scientific regulation of medical devices and better achieve full lifecycle management.

Meanwhile, drawbacks such as “complex product classification, diverse categories, and the absence of both local and national standards” have long been the most criticized aspects of the medical consumables industry. Therefore, the implementation of the Unique Device Identification (UDI) system is of breakthrough significance for medical consumables.

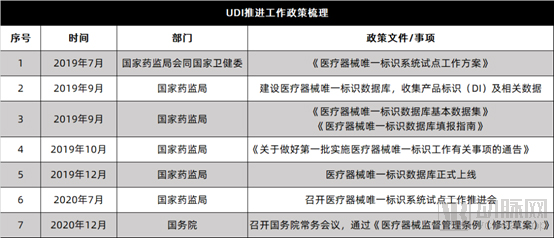

In July 2020, the National Medical Products Administration (NMPA) convened a meeting to advance the pilot program for the Unique Device Identification (UDI) system, further promoting UDI exploration efforts among pilot entities. In December, the State Council Executive Meeting reviewed and approved the "Regulations on the Supervision and Administration of Medical Devices (Revised Draft)," emphasizing the need to strengthen regulatory measures by introducing additional oversight mechanisms such as product unique identification traceability and extended inspections.

Mainstream opinion holds that the implementation of the Unique Device Identification (UDI) system will significantly influence lean hospital management and the upgrading of the medical device industry. On one hand, standardized coding provides a foundational guarantee for the procurement of medical consumables, facilitating price tracking and transparency. On the other hand, it enables data traceability throughout the entire lifecycle of medical consumables, which is of great significance for collaborative management, clinical application, lean hospital administration, and the scientific optimization of consumable quality.

More importantly, this future is not far off.

Dr. Zhang Liang, Chief Consulting Advisor at Wanghai Kangxin Supply Chain, believes that the Unique Device Identification (UDI) system, as a hallmark of the Internet of Everything, connects the entire upstream and downstream supply chain for end-to-end traceability. A comprehensive UDI solution comprises two layers. The first is the system layer, which leverages secondary nodes of the Industrial Internet and national standards to facilitate code integration between hospitals and manufacturers, thereby achieving full-process traceability of medical devices from initial production to final clinical use by patients. The substantial data accumulated through this process provides hospitals with a broader perspective for observing and analyzing consumables, enabling multi-dimensional data analysis of clinical usage, consumption ratios, and physicians’ usage patterns, thus progressively promoting scientific and rational utilization of medical consumables.

Another dimension relies on the currently highly popular “Industrial Internet.” In the hospital supply chain, managers often focus their attention on managing the flow from “manufacturers → distributors → hospitals → patients,” while neglecting the reverse transmission of information. How upstream manufacturers can collaborate more closely with clinical departments and hospitals, and how they can better optimize and improve the quality of medical consumables, actually depend on the efficient and precise feedback of data related to clinical usage.

In July 2019, the National Medical Products Administration announced the first batch of 108 pilot units for the Unique Device Identification (UDI) system. As the effectiveness of the pilot program gradually becomes evident, the nationwide rollout of UDI implementation is poised to be launched soon.

On December 22, the State Council executive meeting approved the “Regulations on the Supervision and Administration of Medical Devices (Revised Draft)” for the first time in two years.

On the same day, the Yangtze River Delta Branch of the Center for Drug Evaluation and Inspection and the Yangtze River Delta Branch of the Center for Medical Device Technical Evaluation and Inspection, both under the National Medical Products Administration (NMPA), were officially unveiled in Shanghai. Shortly thereafter, on December 23, the Greater Bay Area Branch of the NMPA’s Center for Drug Evaluation and Inspection and the Greater Bay Area Branch of the Center for Medical Device Technical Evaluation and Inspection were formally established in Shenzhen.

Amid the tightening regulatory landscape for the overall pharmaceutical and medical device industry, two consecutive days of “major actions” appear to signal to the entire sector that the medical device industry has entered the era of the strictest regulation in its history.

The naming of the “Sub-center for Technical Review and Inspection of Medical Devices” is particularly revealing. The inclusion of the word “Inspection” appears to assign distinct responsibilities to these regional sub-centers, suggesting that they will focus on medical device inspections. This signals that the National Medical Products Administration (NMPA) is tightening its regulatory oversight of medical devices, with increasingly stringent supervision across the entire product lifecycle and in matters of compliance.

From a longer-term perspective, the state had already set a strict regulatory tone for high-value medical consumables as early as the beginning of the year. On January 9, Han Zheng, Member of the Standing Committee of the Political Bureau of the CPC Central Committee and Vice Premier of the State Council, together with Ma Xiaowei, Director of the National Health Commission, conducted research visits at the National Healthcare Security Administration.

This is not Vice Premier Han Zheng’s first visit to the National Healthcare Security Administration (NHSA). In fact, he conducted inspections at the NHSA in 2018 and 2019. Each set of instructions issued during these visits has implicitly outlined the NHSA’s key priorities for the subsequent period. This time, the focus centers on “cracking down on insurance fraud and improving unannounced inspection methodologies.”

Meanwhile, the National Health Commission has also stepped up regulatory oversight. In January, it released the First Batch of the National Key Governance List for High-Value Medical Consumables, which prominently includes high-volume, high-cost items such as orthopedic implants and stents.

In April, the National Healthcare Security Administration released the List of Administrative Law Enforcement Matters (2020 Edition). The 16 items listed cover three major areas: supervision of healthcare security funds, regulation of medical service practices, and oversight of pharmaceuticals and medical consumables. Among these, the supervision of pharmaceuticals and medical consumables primarily focuses on compliance inspections of centralized procurement activities.

Whether it is the increasingly frequent unannounced inspections conducted throughout the year or the successive regulatory measures introduced by various ministries and commissions, the state has long accelerated its oversight of medical consumables. The passage of the amended Regulations on the Supervision and Administration of Medical Devices at the end of 2020, a document akin to the industry’s “constitution,” seemed to signal a fresh start for the regulation of the entire medical device industry in 2021.

Public hospitals, which once rode the waves with ease, are having a truly “difficult” year.

From a macro perspective, after 11 years of healthcare reform, under the main theme of coordinated development among medical services, health insurance, and pharmaceuticals, drug and consumable procurement has advanced aggressively, payment reforms have steadily deepened, while broader healthcare system reforms have progressed relatively slowly. As the combined effects of pharmaceutical and health insurance policies continue to intensify, public hospitals, situated at the “eye of the storm” of these reforms, can no longer remain insulated from change. Moreover, in recent years, the pace of public hospital reform has been sluggish, with certain institutional and mechanistic bottlenecks proving difficult to overcome. Shortcomings in internal management within public hospitals have become increasingly prominent, making comprehensive reform imperative.

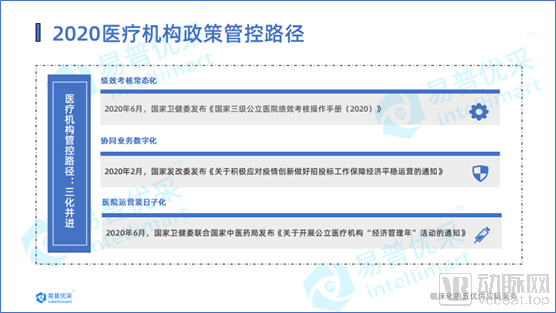

Overall, state oversight of public medical institutions is primarily focused on three areas. First, performance evaluation has become routine. Second, driven by the impact of the COVID-19 pandemic, public hospitals have seen a surge in demand for online interactions, with collaborative operations and even broader management practices gradually transitioning toward digitalization. Third, amid sharply rising cost pressures, the state has explicitly required public medical institutions to firmly embrace the principle of “tightening their belts” and ensuring that every penny is spent wisely.

Similarly, 2020 was also a critical milestone for the performance appraisal of public hospitals.

In January 2019, the General Office of the State Council issued the “Guiding Opinions on Strengthening Performance Appraisal of Tertiary Public Hospitals,” explicitly requiring that a relatively comprehensive performance appraisal system for tertiary public hospitals be basically established by 2020. In December of the same year, the National Health Commission released the “Notice on Strengthening Performance Appraisal of Secondary Public Hospitals,” requiring the nationwide launch of performance appraisal for secondary public hospitals in 2020.

At the beginning and end of 2019, two notices were issued, both concerning the arrangement of performance appraisal work for the year 2020. In particular, the inclusion of secondary public hospitals in the scope of performance appraisal signals that public hospitals are entering a new phase of normalized performance appraisal.

Upon reviewing the "Operational Manual for Performance Assessment of National Tertiary Public Hospitals (2020)" issued by the National Health Commission in June 2020, it is evident from the document and data reporting requirements that the 2020 version of the performance assessment primarily covers four aspects: medical quality, operational efficiency, sustainable development, and satisfaction evaluation. One new tertiary indicator was added, namely the proportion of revenue from key monitored high-value medical consumables. The total score is 1,000 points. The Analytic Hierarchy Process (AHP) is used to calculate the weights of indicators at various levels, with the respective proportions being 4:3:2:1. Operational efficiency ranks second only to medical quality, accounting for 30% of the total weight.

From a holistic design perspective, the state has made substantial efforts to enhance hospital operational efficiency and standardize the rational use of high-value medical consumables. For healthcare institutions, the key to navigating the rigorous performance evaluation lies in establishing an efficient and compliant operational system, and implementing a scientific management model for high-value medical consumables that encompasses pre-event forecasting, in-process monitoring, and post-event assessment.

It is foreseeable that linking the consumption of high-value medical consumables to departmental performance, along with a UDI-based lifecycle traceability management system for such consumables, will become key focal points for future hospital operational management and information technology development.

During the period when healthcare institutions were fully engaged in pandemic control, online procurement met their business interaction needs for online tendering and procurement, bid evaluation, and efficient collaboration with suppliers through a “zero-contact” approach. It is no exaggeration to describe online procurement as the “second front” in hospitals’ fight against the epidemic.

The government also provided immediate support for this second front. In February, the National Development and Reform Commission (NDRC) issued the Notice on Actively Responding to the Epidemic, Innovating Tendering and Bidding Work, and Ensuring Stable Economic Operation, which explicitly stated that “on-site transaction activities for tendering projects shall be suspended in a timely manner, online processing shall be promoted, and on-site participation requirements shall be reduced. All projects subject to mandatory tendering by law shall achieve online bid submission and bid opening within the year.”

Undeniably, the high transmissibility of the COVID-19 pandemic has spurred a surge in demand for online collaboration. Catalyzed by the pandemic, “hospital digitalization,” characterized primarily by efficient collaboration, standardized processes, and data services, has entered its inaugural year.

Digitalization has also been a policy vigorously promoted by the state for many years, in which new infrastructure clearly holds exceptional significance. In March this year, the Standing Committee of the Political Bureau of the CPC Central Committee pointed out that it is necessary to increase investment in public health services and emergency material supply, and accelerate the construction of new infrastructure such as 5G networks and data centers.

Against this backdrop, the industrial internet has stepped into the spotlight. National and provincial governments have intensively rolled out numerous policies, with core components of the industrial internet—such as intelligent manufacturing, supply chain upgrading, and digital services—becoming key areas of policy support. The industry has also begun to recognize the value of the industrial internet, leading to a growing number of rational assessments from various perspectives, although doubts and debates about new models and business formats persist. What is the value of digitalizing hospital supply chains? Does the deep integration between hospitals and upstream enterprises, facilitated by the industrial internet, truly hold practical significance?

Yet, beneath these varied developments lies a broader consensus within the industry on the overarching direction of the industrial internet.

“Year of Economic Management” has clearly become one of the hottest topics in the healthcare industry in 2020.

This initiative, jointly launched by the National Health Commission and the National Administration of Traditional Chinese Medicine, officially kicked off in July with a one-year duration, immediately capturing significant attention across the industry. The tight timeline—just one day between finalization and release—has further sparked considerable reflection.

“Tight deadlines and heavy workloads” appear to be the underlying message of this initiative. According to official documents, the “Public Hospital Economic Management Year” campaign stems from the directive issued at the 2020 National Health and Financial Work Conference, which called for “promoting high-quality development in public hospitals and launching an Economic Management Year.” Unlike hard metrics such as performance assessments, the Economic Management Year aims to leverage cost control and oversight across supply chain management—including procurement of pharmaceuticals and medical consumables, as well as inventory and sales management—by integrating economic management principles into all aspects of medical care, teaching, and research. This requires hospitals not only to “tighten their belts” but also to identify precisely where and how tightly to tighten them.

From a deeper perspective, the “Year of Economic Management” initiative can be interpreted through two key points. First, it compels medical institutions to establish a comprehensive management system for medical consumables, encompassing ex-ante control, in-process monitoring, and post-event evaluation, thereby identifying unreasonable usage patterns and pinpointing areas requiring stringent oversight. Second, the core objectives of the “Year of Economic Management” align closely with those of major performance evaluations. As DRG payment reforms continue to deepen, hospitals face mounting cost pressures. Leveraging economic management to alleviate these pressures has proven an effective strategy for public medical institutions to break through current challenges. Consequently, the “Year of Economic Management” initiative may gradually become institutionalized in the future.

Four years ago, a new patient-centered, value-oriented healthcare paradigm was introduced in China, closely aligning with the strategic policy direction of the “Healthy China 2030” national strategy and rapidly catalyzing a transformation in the healthcare industry.

Four years on, following extensive research and in-depth exploration, the National Healthcare Security Administration and relevant ministries have intensively rolled out a series of value-based regulatory policies. By targeting pain points and tackling difficult issues, these policies are driving reforms in management mechanisms across multiple dimensions—including innovation, payment, clinical practice, and procurement. The heightened focus on healthcare costs and quality is gradually forming the core framework and fundamental character of the Healthcare Reform 2.0 era.

Amid the ongoing rationalization of the pharmaceutical landscape and the deepening reform of medical insurance payment systems, we have identified several major trends in 2021:

1. Continuous Deepening of Lean Operations in Public Hospitals. With changes in compensation channels for public hospitals, the advancement of the tiered diagnosis and treatment system, strengthened supervision of medical insurance funds, insufficient fiscal investment, and the impact of public health emergencies, public hospitals have faced significant operational pressure in recent years. Meanwhile, as the "Year of Economic Management" initiatives and rigorous performance evaluations further intensify next year, internal demand for business-finance integration and refined management within hospitals will reach its peak, inevitably driving the continuous deepening of lean operations in public hospitals.

Just last week, the National Health Commission issued the “Guiding Opinions on Strengthening Operational Management in Public Hospitals,” providing the first-ever definition of hospital operational management and clearly outlining the pathways for establishing an operational management organizational system, as well as the key tasks and content of operational management. All these measures are laying the groundwork for the deepening of lean operations in healthcare institutions next year.

Establishing a whole-process lean management system encompassing “Optimal Selection, Optimal Procurement, Optimal Supply, Optimal Management, and Optimal Evaluation” may become the most effective approach to alleviating operational pressures on hospitals, ultimately achieving scientific and compliant procurement sourcing, efficient collaboration between supply and procurement, full traceability of medical consumables, evaluable and controllable end-to-end management, as well as cost reduction and efficiency improvement in hospital operations.

2. Medical consumables are entering an era of innovative upgrading. The volume-based procurement policy can, to a certain extent, streamline the distribution channels for pharmaceuticals and medical devices, guide established manufacturers of high-value consumables toward innovation, conserve medical insurance funds, and enhance the reimbursement capacity for innovative products, thereby driving industrial innovation and upgrading. However, given the significant differences in industrial characteristics, growth potential, and competitive landscapes across various categories of high-value consumables, it is essential to strictly implement a “one product, one policy” procurement strategy.

Amidst extremely compressed profit margins, where lies the breakthrough for medical device companies? Drawing lessons from the development strategies of Japan and the United States, it is evident that the U.S. prioritizes rapid innovation, while Japan focuses on refining and specializing in established domains, particularly those gradually being deprioritized by Europe and the United States. For Chinese medical device enterprises, the optimal approach may be strategic innovation—identifying and deeply cultivating niche areas where neither the U.S. nor Japan excels. The secondary strategy involves competing through superior service and technology, continuously enhancing product quality to precisely meet clinical needs.

3. Healthcare is entering the era of the industrial internet. Unlike pharmaceuticals, which are highly standardized, medical devices exhibit high levels of personalization and customization due to variations among patients and their conditions. Therefore, from the perspective of the industrial internet, it is crucial to integrate the demand side and supply side of hospital supply chains. By leveraging precise feedback from clinical usage data and patient data, upstream manufacturers can be driven to continuously improve the quality of consumables, more accurately meet patients’ actual needs, and accelerate the rapid upgrading of the medical device industry.

4. Medical Supply Management in the Era of Value-Based Healthcare Enters a Specialty-Specific Phase. Given the wide variety of medical supplies and significant differences in their usage and management, the traditional “one-size-fits-all” approach is no longer sustainable. As hospitals advance their lean management capabilities, medical supply management will inevitably shift toward a specialty- and disease-specific model. This entails implementing differentiated, customized management strategies for supplies used across different diseases and departments, generating comprehensive and scientifically grounded data reports based on system analytics, deeply mining data value, and providing optimization recommendations for supply management from an operational perspective. These efforts aim to offer strategic direction for hospitals to enhance scientific management, improve supply selection, and reduce costs.

No winter lasts forever, and no spring fails to arrive. All the growing pains experienced during the period of transformation in 2020 will serve as a resounding prelude to advancing toward value-based healthcare.