Over $12 Billion Injected into Medical AI, Marking a Strong 'V'-Shaped Recovery: 2020 Annual Review

No one doubts the notion that “artificial intelligence is the core productive force of the future.” Creating human-like computer systems is so compelling that nearly every industry is attempting to leverage AI to facilitate the transition from automation to intelligentization.

The same holds true in the healthcare sector. Although artificial intelligence (AI) is still in its early stages of adoption, the underlying technologies—such as computer vision and natural language processing (NLP)—have undergone multiple iterations, with their corresponding market sizes continuing to expand. According to the 2020 report by VCBeat Research Institute, titled “The Path and Wisdom of Healthcare AI Innovation: Returning to Needs and Integrating Value,” the compound annual growth rate (CAGR) of medical AI over the past five years exceeded 40%, and the application market size approached RMB 30 billion in 2020.

However, emerging technologies often face the dilemma of rapid development coupled with slow commercialization. This is particularly true in “slow” sectors such as healthcare, where regulatory reviews for software safety and the transition between legacy and new technologies severely test the patience of both capital investors and enterprises. Consequently, troughs and stagnation are common phenomena, and medical artificial intelligence is no exception to this challenge.

The turning point emerged in mid-2020. Although the pandemic temporarily slowed the development of most sectors within the healthcare industry, it also propelled hospitals to proactively undertake intelligent transformation. Furthermore, approvals by the National Medical Products Administration (NMPA) helped restore confidence among professionals in the medical imaging AI sector, while the “New Infrastructure” initiative expanded artificial intelligence into a broader market. Driven by these multiple factors, the development of medical artificial intelligence is poised for significant growth.

To understand the current state of medical AI development and provide an outlook for the coming year, VCBeat processed and analyzed data from nearly 100 artificial intelligence companies.

The entire article is divided into three parts:

I. Maturity Assessment of AI Healthcare Scenarios

II. The Return of Capital and the Agglomeration Effect Among AI Leaders

III. Externalization of Potential Tracks and the Future Development of AI

From these three perspectives, VCBeat attempts to clarify the development trajectory of medical artificial intelligence in 2020.

In the healthcare industry, artificial intelligence (AI) applications are primarily concentrated in computer vision and natural language processing. Building on these two foundational technologies, AI has expanded into more than ten application scenarios. After several years of development, disparities among different sub-sectors have become increasingly pronounced. In some niches, companies have already passed regulatory hearings and are preparing for initial public offerings; in others, firms are still exploring viable paths, attempting to reshape technology around actual clinical needs. However, regardless of the chosen niche or stage of development, the pervasive challenge of monetizing AI remains unresolved in healthcare. To date, the vast majority of companies continue to strive for profitability.

Analysis of the Development Stages of Startups

I. Medical Imaging

Medical imaging has served as the entry point for artificial intelligence (AI) into healthcare. Within less than a decade, more than 200 companies have begun developing products by addressing needs in radiology, pathology, and radiotherapy assistance. In 2020, while there were no significant changes in the fields of pathology and radiotherapy assistance, AI in radiology successfully navigated the regulatory review and approval process that had long plagued it, transitioning from “clinical implementation” to “commercialization.”

In January 2020, Keya Medical’s CT-FFR product, “DeepVessel FFR,” broke through regulatory barriers by securing the first Class III medical device certificate for an AI-based medical device in China, shifting its focus from R&D to pricing catalog inclusion and market sales. In February, Lepu Medical’s “AI-ECG Platform” received approval from the National Medical Products Administration (NMPA), marking another milestone for cardiac-related AI. In June, an MR imaging software for auxiliary diagnosis of intracranial tumors, more closely aligned with the definition of “auxiliary diagnosis,” was approved, propelling Ande Yizhi into prominence. July proved fruitful for two AI companies, Airdoc and Silicon Intelligence, as the NMPA issued two registration certificates for “software for auxiliary diagnosis of diabetic retinopathy based on fundus images” in a single month.

The year-end is a harvest month for established medical imaging AI companies. In early November, Shukun Technology’s auxiliary triage software for detecting vascular stenosis in coronary CT angiography images received approval. Infervision and United Imaging Intelligence followed suit, obtaining the first “AI + pulmonary nodule” registration certificate and the first “AI + fracture” registration certificate, respectively, on the same day. A month later, Deepwise Medical also secured its “AI + pulmonary nodule” certificate, bringing medical artificial intelligence’s 2020 to a perfect close.

Status of NMPA Class III Medical Device Approvals for AI in Healthcare in 2020

A closer look at the regulatory approval status of nine AI products reveals that they cover both high-volume scenarios, such as pulmonary nodules, fundus imaging, and electrocardiography (ECG), and specialized niches with substantial market potential, such as CT angiography (CTA), CT-derived fractional flow reserve (CT-FFR), and brain magnetic resonance (MR) imaging. This suggests that as long as product quality is robust, regulatory review and approval can be secured.

However, according to the 2019 planning of the AI Medical Device Innovation Cooperation Platform, it was proposed to establish eight major test sample databases for CT lung, CT liver, CT fracture, brain MRI, cardiac MRI, coronary CTA, ECG, and ophthalmology. With the exception of CT-FFR, all products approved in 2020 fall within these categories. In other words, the next approval scenario is highly likely to emerge from among CT liver or cardiac MRI applications.

It is also worth noting that the National Medical Products Administration (NMPA) exercises extreme caution in describing the functionalities of AI products within its Class III medical device certifications. These certifications merely outline the basic functions of the product and explicitly emphasize that “diagnoses must not be made solely based on the product’s output.” While limiting the scope of use for imaging AI may not necessarily hinder product sales, the question of how to ensure the safety of subsequently added features remains critical as more functionalities are integrated. Given that the current review and approval process for AI imaging solutions typically takes over a year, determining how to regulate the approval of updates to artificial intelligence software will be the next major challenge requiring discussion among all stakeholders.

II. CDSS, Big Data Management, and Voice Input

Clinical Decision Support Systems (CDSS), big data management (including data mining, data governance, etc.), and voice entry have all achieved disruptive breakthroughs due to the integration of AI. Specifically, the development of Natural Language Processing (NLP) has provided researchers with effective tools to manage massive and multi-dimensional medical data, while also offering more efficient solutions for intelligent doctor-patient interactions and data monitoring. In 2020 alone, the CDSS sector saw policy-driven advancement, while leading companies in the big data management and voice entry sectors began pursuing initial public offerings.

As a key driver in the performance evaluation of public hospitals, healthcare informatization imposes specific requirements on institutions through rating systems for electronic medical records (EMR), interoperability, and smart hospital services. In the analysis of performance assessments for tertiary public hospitals, key indicators include the efficiency and quality of medical services, rational drug use, and the graded level of EMR systems. Therefore, the implementation of Clinical Decision Support Systems (CDSS) can effectively enhance the efficiency and quality of medical services, promote rational drug use, and improve the maturity level of EMR systems.

In mid-2020, market expansion for Clinical Decision Support Systems (CDSS) remained largely driven by evaluations related to Electronic Medical Records (EMR), interoperability, and smart hospital services, although new policies also provided support. On July 30, the Bureau of Medical Administration and Hospital Management issued the "Notice on Further Strengthening Quality Management and Control of Single Diseases," which emphasized the requirement to report data on the first batch of 36 diseases/surgical procedures. Hospitals at Level II and above were required to complete the supplementary submission of relevant case information by December 31, 2020. This policy created new market opportunities for specialized CDSS product and service providers such as Huimei Technology and Senyi Intelligence.

In contrast, the development of big data management has benefited from the pandemic. By integrating and analyzing information such as patients’ electronic medical records (EMRs) and electronic health codes, Centers for Disease Control and Prevention (CDCs) can visually track suspected cases and their close contacts. In early 2020, Beijing Dashu Yida developed a disease surveillance and early warning system for the Nanjing CDC, which directly connected to local hospitals’ EMRs, thereby enabling big data-driven disease control.

This disease control surveillance and early warning system leverages big data and artificial intelligence technologies to model medical knowledge graphs and directly extract electronic medical records (EMRs) for semantic structuring. AI algorithms then match the structured data against a knowledge base to determine whether the EMRs contain keywords associated with infectious diseases such as COVID-19. Cases identified as suspected or highly suspected by the AI are automatically reported to disease control authorities, thereby preventing omissions or delayed reporting by hospitals. In addition to the 40 statutorily notifiable infectious diseases, the system also supports the inclusion of additional locally prevalent infectious diseases as defined by regional health authorities.

Among these three tracks, two AI companies are attempting to transition phases by surpassing the “corporate profitability” stage. Unisound’s medical business, which focuses on medical record quality control and voice entry, submitted its IPO prospectus for the STAR Market on November 3. Yidu Cloud, a company specializing in medical AI and big data, passed the hearing by the Hong Kong Stock Exchange on December 13 and plans to list in Hong Kong on January 15.

III. New Drug Development

New drug development has been advancing at a rapid pace in recent years, and the heightened societal demand for agile pharmaceutical development following the COVID-19 pandemic has further accelerated this progress.

In the early stages of the pandemic, it was clearly unrealistic to develop new drugs specifically targeting the novel coronavirus, while existing “old” drugs—the mainstay of the anti-epidemic effort—failed to demonstrate satisfactory efficacy. This reality created an opportunity for AI-driven new drug development.

However, only the deep integration of AI models with physics-based thinking can simultaneously meet the demands for both speed and precision in drug development. The most direct and effective drug screening strategy in response to the pandemic involves leveraging cloud-based supercomputing to support physicochemical algorithms in constructing viral models, and then, starting from structural insights, using AI to accelerate the identification of FDA-approved marketed drugs with antiviral activity.

Taking XtalPi as an example, the company possesses leading quantum physics-based drug simulation algorithms and an AI-driven drug discovery platform, supported by robust high-performance computing resources across multiple cloud platforms. This infrastructure enables the rapid execution of large-scale, high-precision drug simulation calculations. When data on the novel coronavirus was still scarce, XtalPi leveraged the limited available information to investigate the virus’s key structures and infection mechanisms at the molecular level, thereby identifying effective approaches to block infection and treat pneumonia.

“The greatest advantage of artificial intelligence is its ability to significantly expand the search space for new drugs, using millions of potentially active molecular scaffolds as a starting point for screening,” Dr. Zhang Peiyu, Chief Scientist at XtalPi, told VCBeat. “By combining AI with computational chemistry and scoring candidate molecules based on a comprehensive assessment of multiple key properties, we can progressively approach the most ideal and promising compounds for successful development.”

From the perspective of development stages, companies engaged in new drug R&D are still in a phase of substantial investment, while also achieving certain commercialization results. Due to its purely B2B nature, new drug R&D may become the first sector to successfully navigate all stages of development.

IV. Other Tracks

As a key component of internet healthcare, chronic disease management is one of the few sectors that benefited during the pandemic. With face-to-face consultations with doctors unavailable, more patients enrolled in platform-based programs.

In this field, companies such as Miao Health tend to build AI-powered chronic disease management platforms for doctors and patients, such as health risk stratification management platforms and AI-driven health intervention platforms. Taking its H Platform as an example, the platform’s NLP-based health knowledge graph can intelligently structure and clean raw health and medical data, creating a tag library of over 170,000 user-generated healthcare behaviors. It also constructs professional health and medical profiles for users, enabling applications of health data such as risk prediction for major and chronic diseases, alerts for abnormal indicators, disease-specific warnings, and health risk factor alerts.

In terms of scenario maturity, AI-driven chronic disease management companies are still in the phase of accumulating consumer-end (C-end) users, while their primary payers remain ill-defined. Therefore, it may not be AI itself that limits their scalable growth; rather, these companies need to actively explore viable business models.

Hardware acceleration is one of the few niche yet high-potential segments in medical AI. At RSNA 2020, industry discussions on medical imaging AI advanced beyond previous years. The focus has shifted away from how AI can replace physicians in image interpretation toward “behind-the-scenes” innovations, highlighting new clinical breakthroughs enabled by upstream AI technologies in imaging, such as image acquisition, data reconstruction, and workflow optimization.

Currently, both GPS and a few startups are developing related technologies, which have been fully integrated into clinical applications. For instance, SubtleMR by Subtle Medical leverages artificial intelligence to ensure compatibility with all MRI scanners, enhancing the efficiency of high-quality image acquisition and reducing motion artifacts. Meanwhile, SubtlePET employs deep learning technology to accelerate PET (Positron Emission Tomography) imaging and reduce radiation exposure, enabling hospitals and imaging centers to increase PET scan speeds by fourfold.

In contrast, the integration of certain emerging technologies appears somewhat directionless. For instance, the AI-driven transformation of VR/AR has undergone years of exploration, yet no significant outcomes have emerged to date. Currently, VR-related technologies are primarily applied in fields such as geriatric rehabilitation and psychotherapy, with limited AI integration and still remaining in the stage of exploring market demands.

Psychology and medical aesthetics are more consumer-oriented (B2C). Applications such as simulated plastic surgery and virtual avatars can provide patients with novel experiences. The key characteristics of these two sectors lie in the fact that modeling precision and intelligence levels determine user satisfaction. Current AI technologies still struggle to adequately understand human psychology and aesthetics. While AI-driven skin monitoring to help consumers choose appropriate skincare products is a promising application, many other AI solutions in medical aesthetics remain of limited practical value and await technological breakthroughs.

In 2019, the primary market for medical AI was somewhat sluggish, with only 40 financing rounds and a total funding amount of just RMB 3.89 billion. Amidst commercialization challenges, more companies directed their investments into research and development, as evidenced by the number of Chinese papers accepted at top-tier conferences such as MICCAI, which doubled.

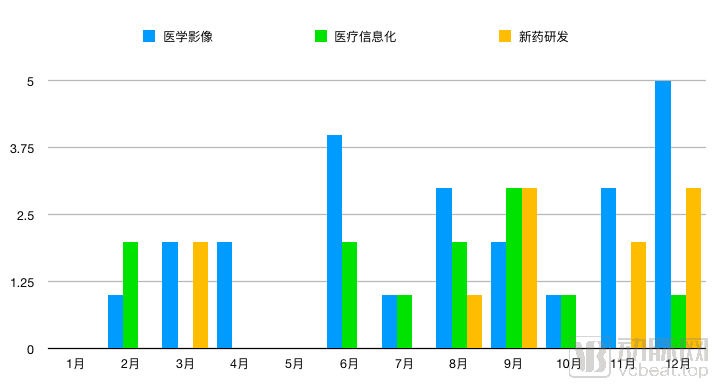

The trend in 2020 was completely different from that in 2019. Affected by the pandemic in the first half of the year, a large number of enterprises significantly cut costs, resulting in declines in both revenue and expenses. In June, mid-year, the medical AI sector began to recover, with AI technologies—largely overlooked in the first half of the year—regaining favor among investors. In 2020, there were a total of 47 financing rounds in the AI healthcare sector, involving approximately RMB 8.48 billion, representing a year-on-year increase of 118.0%. Companies that secured funding began to invest in market operations.

Number of Financing Events by Month in 2020

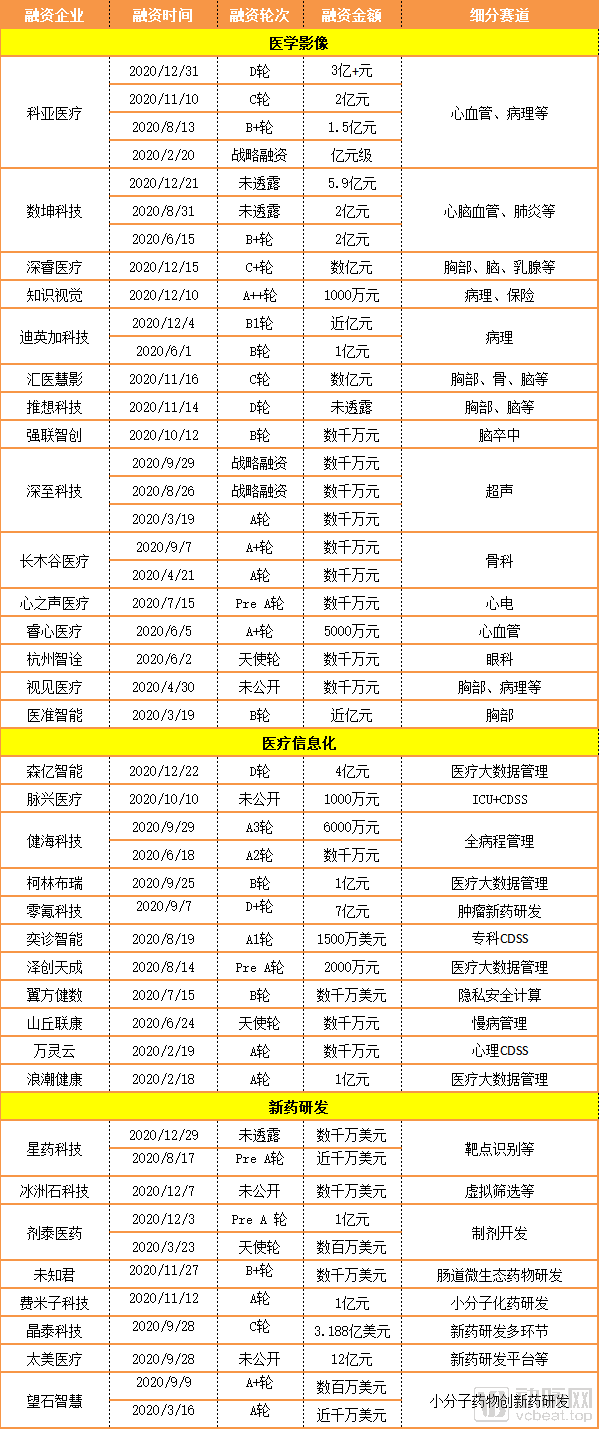

List of Public Financing for Medical AI in 2020 (Data Source: VCBeat Database)

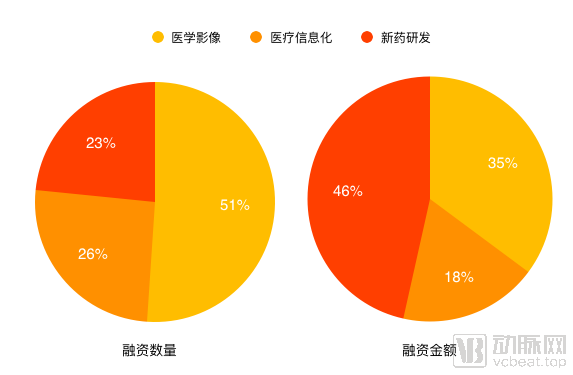

From a longitudinal perspective, it is evident that the majority of companies securing financing have been in operation for no less than three years. A small number of newly established firms, such as Metagenomi (Jitai Medicine), benefit from strategic backing by leading AI-driven drug discovery enterprises like XtalPi (Jingtai Technology). Furthermore, there has been a significant increase in financing events at Series B and beyond, a trend particularly pronounced in the medical imaging sector (with a total of 24 financing rounds, 14 of which were at Series B or later).

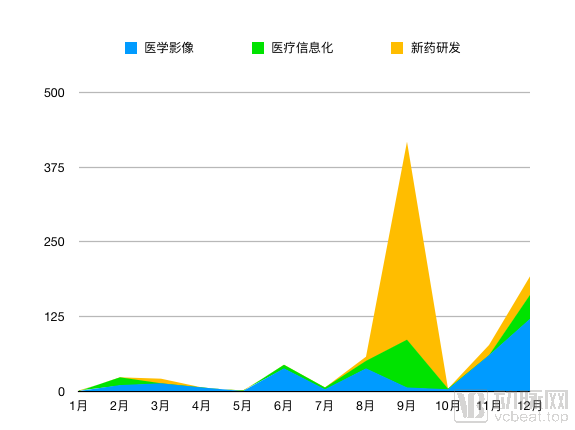

Financing by leading enterprises has a significant impact on funding data within specific industry sectors. In September, LinkDoc Technology’s $700 million RMB D+ round, Taimei Medical Technology’s $1.2 billion RMB financing, and XtalPi’s $318.8 million USD Series C round—three substantial investments in these three leading companies—accounted for half of the total financing in the medical AI sector. In December, Deepwise Healthcare’s multi-hundred-million RMB C+ round, Keya Medical’s $300 million RMB Series D, Senyi Intelligent’s $400 million RMB Series D, and Shukun Technology’s nearly $600 million RMB financing similarly drove the majority of capital inflows into their respective sub-sectors.

Monthly Financing Amounts in 2020

List of Public Medical AI Financing in 2020 (Data sourced from the VCBeat Database)

The aforementioned data indicate a pronounced concentration of market power among top-tier players in the AI healthcare sector. In the field of medical imaging, certified companies such as Shukun Technology and Keya Medical are able to secure multiple rounds of financing within a year, whereas a large number of uncertified and emerging enterprises struggle to obtain capital support. In contrast, the healthcare informatics industry is relatively less concentrated. This disparity can be attributed to the current state of healthcare informatics in China: due to significant regional variations in healthcare quality and informatics infrastructure, leading informatics vendors are unable to extend their reach into every local market. Under these circumstances, local companies with in-depth knowledge of their respective regions are well-positioned to seize opportunities and potentially emerge as standout performers.

However, whether in medical imaging, healthcare informatics, or new drug development, the barriers established are not solely resolvable through algorithms. More importantly, building an AI system for pulmonary nodules, constructing a specialty-specific knowledge graph, or developing a drug discovery platform requires extensive accumulation of medical data. These valuable clinical data do not belong to any single enterprise, thus constituting their most robust barrier.

A common question is: With so many tracks in the medical AI sector, which one will achieve profitability first? Given the current pace of development, no one can provide a definitive answer. However, by observing the behavior of investors, we may be able to uncover some clues.

As shown in the financing list, new drug R&D had the fewest financing deals but raised the largest total amount of capital, with the highest average deal size (RMB 358 million), accounting for over 50% of the total financing volume. Medical imaging had the highest number of financed projects, yet the smallest average deal size (RMB 124 million), slightly lower than that of the healthcare informatics sector (RMB 130 million).

In terms of average transaction value, the pricing models for artificial intelligence (AI) and health informatics are relatively clear. Standalone AI-assisted diagnostic products for pulmonary nodules are generally priced in the range of RMB 500,000 to 1 million, while hospital-wide AI imaging solutions integrated with Picture Archiving and Communication Systems (PACS) can reach nearly RMB 10 million. Specialty Clinical Decision Support Systems (CDSS) are typically priced between RMB 1.5 million and 3 million, and smart hospital construction solutions can amount to tens of millions of yuan, depending on the scale of the hospital. Most companies in these two sectors report annual revenues in the tens to hundreds of millions of yuan, with a few achieving revenues in the billions. In contrast, services across various stages of new drug development vary significantly, making it difficult to specify precise pricing for potential opportunities and returns. However, as upstream suppliers to pharmaceutical companies, their revenues are also relatively substantial.

Based on financing amounts and commercialization outcomes, different medical AI sectors have taken distinctly divergent paths by leveraging different underlying technologies. Therefore, VCBeat has analyzed these three sectors separately, examining their industrial chain dynamics and breakthrough advancements, and providing individual summaries for each.

Medical Imaging

As the number of approved AI-based medical imaging products continues to rise, an increasing number of medical device CRO companies are expanding into medical imaging AI as a key business area and pursuing differentiated strategies.

Taking Aotai Kang as an example, this CRO company boasts 14 years of project experience in the industry. It has completed clinical trial and registration services for over 500 medical devices and pharmaceutical products, secured more than 30 Class III medical device registration certificates in the past five years, and successfully obtained approval for 15 national innovative medical devices. Since 2017, Aotai Kang has identified the potential of the artificial intelligence (AI) sector and rapidly expanded its CRO services in this field. Currently, among the nine AI-powered medical products that have received regulatory approval in China, Aotai Kang provided CRO services for three of them, ranking first in the industry in terms of both case volume and success rate. Looking ahead, Aotai Kang will continue to focus on CRO services for innovative and high-end medical devices, particularly in the six key areas of cardiovascular and cerebrovascular diseases, neurointervention, oncology, orthopedics, medical imaging, and cosmetic surgery.

Rao Yiwei, founder of Aotai Kang, stated to VCBeat: “As of December 2020, Aotai Kang had provided CRO services to the majority of the top 20 medical imaging AI companies, including Keya Medical, Yitu Technology, Infervision, Xingmai Technology, Huiyi Huiying, and Ruixin Medical. Among these, Keya Medical and Infervision have products that received the first regulatory approvals.”

Generally, the approval and registration fees for a single product range from RMB 5 million to 10 million. With the resurgence of AI in medical imaging, the sector is expected to attract more CRO players in 2021.

Medical Informatics

How to better enhance the performance of NLP so that it can better handle heterogeneous data is a problem that AI explorers have been trying to break through. The emergence of the artificial intelligence model GPT-3 has provided new ideas for this—forcing AI to learn with massive amounts of data. However, there are still controversies over the practical results of GPT-3, and its practicality needs further verification by scholars.

Industry Direction: The development of smart hospitals remained a key focus in hospital construction in 2021. Based on the situation in 2020, NLP-powered knowledge bases have been integrated into electronic medical records (EMR) and Hospital Information Systems (HIS). After accumulating substantial clinical data, AI is poised to contribute to the creation of innovative diagnostic and therapeutic approaches for diseases.

New Drug Development

In December, DeepMind’s AlphaFold2 solved the “protein folding prediction” problem, marking the biggest news in the “AI + new drug development” sector. This major challenge, which has plagued the biological community for over 50 years, is now being cracked by AI.

Since most modern drugs target proteins, drug development is almost invariably based on protein structure design. Therefore, if AI can achieve accurate and scalable protein structure prediction, it will replace certain applications of cryo-electron microscopy, nuclear magnetic resonance, or X-ray crystallography in structure determination, significantly enhancing the efficiency of protein discovery and reducing associated costs.

Nevertheless, traditional approaches still hold certain advantages in the study of protein–protein interactions. However, with the advancement of AI, computational methods may achieve breakthroughs in areas not yet explored by machine intelligence. Time will tell.

Overall, artificial intelligence has staged a perfect V-shaped recovery in the post-pandemic era, with each sector empowering healthcare in its own unique way and incrementally transforming every aspect of the industry. In the new year, we hope that every explorer in the medical field will embrace the “deliberate pace of healthcare,” holding fast to their dreams with unwavering consistency.