China's Gene Testing Industry in 2020: 62 Financing Rounds, Over RMB 20 Billion Raised, and a Strategic Shift Toward In-Hospital Adoption

After the turbulent competition in tumor NGS during 2017 and 2018, followed by a sharp decline in overall financing in 2019, the genetic testing industry appeared to flourish in 2020. From gaining an edge over CT imaging in the early debate on nucleic acid testing amid the COVID-19 outbreak, to Burnstone Medicine and Genetron Health listing on the U.S. stock market within a single week mid-year, and then to MGI Tech and New Horizon Health securing large single-round financings before subsequently filing for IPOs, the sector witnessed 62 financing events throughout the year, with cumulative amounts exceeding RMB 20 billion. The fervor for genetic testing burned brightly from the beginning to the end of the year.

The concept of precision medicine has gained widespread acceptance, while the plummeting cost of implementing genetic testing technologies has enabled its clinical applications to span a comprehensive, end-to-end spectrum—including early screening, disease diagnosis, precision medication, refined R&D, and precise follow-up. The current focus is on increasing the penetration rate of genetic testing across these various application scenarios.

In VCBeat’s previous annual review of genetic testing, we attempted to categorize the implementation models of genetic testing into two types: in-hospital and out-of-hospital. Over the past year, products and services adopting these two models have seen shifting dynamics, with their respective characteristics of “product-as-a-service” and “service-as-a-product” becoming increasingly distinct.

In fact, in the preceding years, the keywords associated with genetic testing were scenarios, physicians, patients, high-risk populations, users, or products. In 2020, however, there was only one keyword for genetic testing: hospitals. In 2020, we observed the following characteristics of China’s genetic testing industry:

1. MGI Tech Continues to Lead, with Oncology Remaining the Hottest Segment

2. Domestic Equipment Enters the Market: How Will It Break Through?

3. “Creative” Hospital Admissions: What Are the New Challenges for Tumor NGS?

4. Early Screening Outside Hospitals Becomes Widespread, While Hospital Admission Remains Challenging

5. Financing remains robust as mNGS rapidly moves toward standardization

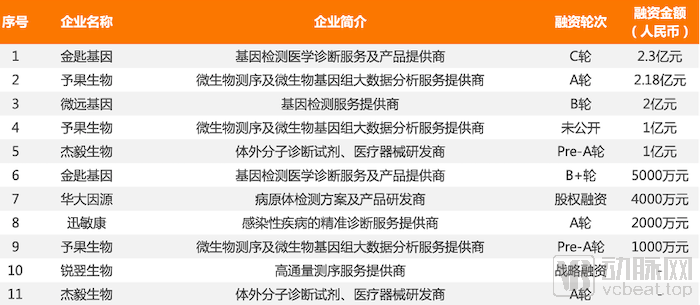

Let’s first examine the financing landscape. As of press time, the Artery Orange database has recorded a total of 62 financing deals in China’s genetic testing sector in 2020, with a combined funding amount of RMB 20.59 billion (including USD 1.64 billion, with all figures converted based on the USD exchange rate on the respective announcement dates). Notably, in October, MGI Tech secured a Series B financing round of USD 1 billion (equivalent to RMB 7.165 billion), setting a new record for the largest single-round financing in China’s gene sequencing sector and retaining its position as the top-funded company in the genetic testing industry for the year.

62 Financing Deals in the Genetic Testing Sector in 2020

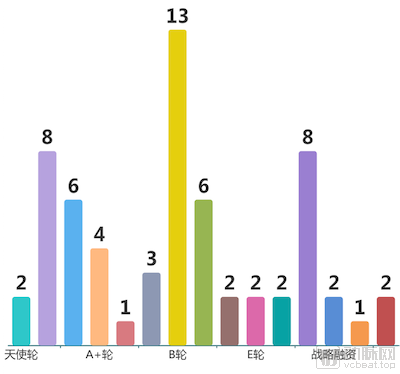

Throughout 2020, financing for domestic genetic testing companies in the primary market entered a transitional phase from early-stage startups to mid-to-late stage development, exhibiting a distribution characterized by a broad middle and narrow ends. The strong grew stronger, while the funding landscape for early-stage projects further contracted, with only two angel-round disease screening projects securing financing.

Funding Stages of the 62 Deals in 2020

In mid-June, Burning Rock Biotech and Genetron Health, two leading domestic companies in the oncology next-generation sequencing (NGS) sector, listed on U.S. stock exchanges within a week of each other, raising $250 million and $260 million respectively through public offerings. This marked the first time that companies whose core business is providing oncology NGS services and products have entered the global capital markets. Since their listings, both stocks have performed relatively steadily, with Burning Rock Biotech’s share price trend slightly outperforming that of Genetron Health, at one point approaching a doubling of its market capitalization.

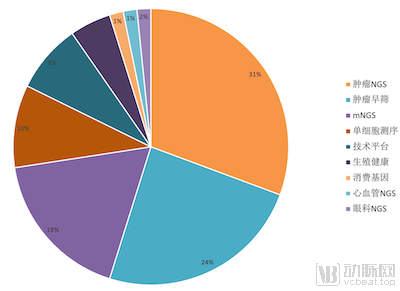

Subsectors of the 62 Financing Rounds in 2020

In 2020, 31% of financing events occurred in the field of tumor NGS, making it the most heavily funded application scenario in genetic testing. This was followed by early cancer screening, which accounted for 24%. Furthermore, single-cell sequencing projects, which ranked fourth in the number of financing events, were also primarily focused on oncology, including new cancer drug development and clinical support. Notably, mNGS ranked third in the number of financing events in 2020, indicating that in-hospital diagnosis of pathogenic infections remains a highly popular application area for genetic testing.

Among the top 10 largest financing deals, nine companies—including MGI Tech, Genetron Health, Burning Rock Biotech, 3D Medicines Diagnostics, and Zhenhe Technology—raised a cumulative total of RMB 16.419 billion (equivalent), accounting for 79.7% of the total. Correspondingly, technological platforms, companion diagnostics, disease screening, and clinical translation emerged as the most prominent application scenarios for genetic testing during the year.

Genetron Health and Burning Rock Biotech, both of which went public in 2020, excel in advancing the clinical application of tumor next-generation sequencing (NGS). According to their respective prospectuses, Burning Rock’s companion diagnostic products for lung cancer medications and Genetron’s corresponding products captured market shares of 26.7% and 16.7%, respectively. In contrast, 3D Medicines, Geneseeq, and Kayou Diagnostics are relatively more adept at productizing tumor NGS services, adopting in vitro diagnostic (IVD) strategies, expanding their product portfolios, and strengthening automation capabilities. Meanwhile, GeneChem and MedPath Translational Medicine possess deep expertise in translational medicine, building robust R&D platforms that bridge basic research with clinical applications. The tumor NGS companies that ranked among the top 10 in financing in 2020 each demonstrate distinct differentiated advantages.

It is estimated that the domestic tumor NGS market in China will grow from $300 million in 2019 to $4.5 billion in 2030. In 2019, the penetration rate of tumor NGS in China was only 6.4%. It is projected that by 2030, guided by clinical practice guidelines, the penetration rate of tumor NGS could reach 45.2%.

As the most critical upstream technology platform for genetic testing, gene sequencers are monopolized by overseas giants, representing a hidden pain point in the growth of China’s genetic testing industry. The lack of bargaining power has severely hindered the healthy development of the sector, creating the greatest predicament of the “printer and ink cartridge” era in genetic testing.

In the early stages, genetic testing was conducted prior to hospital admission, with samples sent to independent clinical laboratories outside hospitals for centralized analysis, gradually giving rise to independent medical testing institutions of considerable scale. Statistics show that nearly 90% of China’s genetic testing market share is held by a dozen large independent medical testing laboratories. Overseas technology platform giants have adopted diversified market strategies toward these independent laboratories, leading to the emergence of joint development models. Since around 2014, companies such as Illumina, Life Technologies, and Thermo Fisher have partnered with domestic firms—including Da An Gene, Berry Genomics, Annoroad, Genetron Health, CapitalBio, and KingMed Diagnostics—to co-develop gene sequencing platforms tailored to specific application scenarios.

Through a “printer and ink cartridge” sales model and joint customized development with midstream manufacturers, overseas gene sequencing instrument vendors have equipped domestic research institutions and medical laboratories with robust genetic testing capabilities within a few years.

In those years, as BGI Genomics’ genetic testing business continued to expand, it was increasingly constrained by spiraling and difficult-to-control costs. Determined to address this challenge, the company embarked on the path of domesticating gene sequencers, starting with the acquisition of key technology patents. After years of internal technology incubation, MGI Tech was established in 2016, taking up the mantle of localizing core components of gene sequencers. With a steady pace of launching one new model each year, it successively introduced high-, medium-, and low-throughput gene sequencers. In December 2020, after becoming the third company globally capable of mass-producing clinical-grade sequencers, MGI Tech applied for an initial public offering on the STAR Market.

According to MGI Tech’s prospectus, from 2017 to September 2020, the company had cumulatively shipped 1,871 gene sequencers and generated cumulative revenue of RMB 1.822 billion. Notably, MGI Tech’s sales revenue from gene sequencers in 2019 was equivalent to 20% of Illumina’s revenue from the same product line in that year.

In addition, teams with the capability to develop sequencing platforms, such as Qitan Technology, Sinano Biology, and Jinshi Technology, also achieved phased results in 2020.

In June, Sena Bio stated upon announcing its Series C financing that its self-developed gene sequencer had passed laboratory prototype testing, with plans to enter external testing the following year and initiate regulatory submission for market approval. By integrating NGS sequencing principles with the concept of “error-correcting codes” from the field of information and communications technology, the device can automatically detect and correct trace sequencing errors occurring during the process, thereby ensuring read length while significantly improving accuracy.

In September, Qitan Technology officially announced the launch of its nanopore gene sequencing platform, QNome-9604, on its official website. This product employs an innovative nanopore sequencing principle based on electrical signals. Although its functionality and stability are still undergoing rapid optimization and iteration, it has already achieved medium-throughput performance, generating 500 Mbp of data within an 8-hour sequencing run. With competitive accuracy and read lengths exceeding 150 kb, the platform is well-suited for rapid and flexible applications such as microbial detection and amplicon sequencing.

In late December, Jinshi Technology, which has maintained a relatively low profile, also held a launch event for the engineering prototype of its protein nanopore gene sequencer. Although no specific data were disclosed, Jinshi Technology presented a product roadmap at the event: launching a nanopore sequencer meeting the needs of scientific research services in early 2022, and introducing a high-end sequencer with a 10M throughput for the clinical market around 2024.

However, as overseas gene sequencer manufacturers have already seized the market for scientific research institutions and medical testing laboratories, domestic gene sequencers face the challenge of breaking through. As the only manufacturer to achieve mass production of gene sequencers, MGI Tech still relies heavily on the internal resources of the BGI Group: in 2017 and 2018, more than 90% of MGI Tech’s revenue came from the BGI Group; by 2019, this proportion had decreased to approximately 70%.

In recent years, overseas gene sequencer manufacturers have increasingly focused on deeply developing ecosystem resources, including exploring new application scenarios based on technology licensing, integrating into hospital workflows, and pursuing cross-industry collaborations. For example, Illumina partnered with funds such as the Bill & Melinda Gates Foundation and Bezos Expeditions to establish Grail for developing early cancer screening products; improved reporting workflows for genetic disease research at Mayo Clinic; and jointly developed clinical information platforms such as IntelliSpace Genomics and Watson for Genomics with Philips and IBM. Currently, according to public news, MGI Tech mainly stimulates incremental market growth through technology licensing, such as collaborating with Genetron Health and Geneseeq to develop gene sequencers, while other domestically produced gene sequencers are still in the stage of optimizing engineering prototypes or have not yet launched formal marketing efforts.

As the range of technical platform options expands, collaborations between genetic testing companies and hospitals to move tumor next-generation sequencing (NGS) from off-site regional central laboratories to in-house hospital settings have become a new mainstream trend in the industry. While this shift involves changes in the competitive landscape of upstream sequencing platforms and subtle adjustments in the relationships between upstream and midstream players, it is driven primarily by the substantial demand for tumor NGS, its time-consuming nature, operational complexity, and the current oversupply in the genetic testing market.

For genetic testing manufacturers, the service scenario is shifting from out-of-hospital to in-hospital settings, and the service offering is evolving from standalone testing services or reagents into comprehensive laboratory solutions, thereby deepening integration with hospital operations. Typically, after hospitals establish customized laboratories, they continue to procure the corresponding reagents and services. This helps alleviate the competitive pressure caused by the commoditization of homogeneous services amid excess genetic testing capacity.

By establishing in-house NGS laboratories, hospitals can also significantly reduce the costs of implementing such projects and shorten turnaround times. Ying Jianming, Director of the Department of Pathology at the Cancer Hospital of the Chinese Academy of Medical Sciences, stated that rapid, accurate, and compliant genetic testing is crucial for hospitals to implement clinical oncology diagnosis and treatment. Zhi Xiuyi, Director of the Lung Cancer Diagnosis and Treatment Center at Capital Medical University and Chief Expert in Thoracic Surgery at Xuanwu Hospital of Capital Medical University, believes that establishing in-house NGS laboratories can provide a new tool for building patient records and help hospitals improve their information systems.

However, establishing an in-house tumor NGS laboratory requires meeting both automated, high-precision technical standards and healthcare institution management regulations. This means that genetic testing companies undertaking this business face substantial upfront investments, including collaborative instrument development with upstream equipment manufacturers, deployment of dedicated on-site teams for close interaction with hospitals, and ongoing operational and maintenance costs.

In-House Implementation of Tumor NGS Testing Workflow

The in-house implementation of NGS involves several key stages, including benchmarking and comprehensive evaluation, laboratory design, equipment procurement, system installation and training, and data generation and interpretation. At each stage, genetic testing companies must deploy dedicated sales and technical teams to work in close collaboration with the hospital. After the in-house NGS laboratory becomes operational, these companies are also required to provide long-term on-site and remote support, such as data analysis assistance.

A Summary of In-Hospital Strategies Adopted by Domestic Companion Diagnostic Manufacturers in 2020, Primarily Categorized into Two Types: Deployment of On-Site Teams and Introduction of Reagents.

The representative of the in-hospital team model is Burning Rock Biotech. In 2016, Burning Rock Biotech became the first company in China to provide turnkey solutions and ongoing support to Chinese hospitals. At the early stage of the domestic tumor NGS industry, Burning Rock Biotech established an in-hospital support team. In 2017, Burning Rock Biotech began collaborating with Agilent Technologies to jointly develop Magnis BR, the first fully automated NGS library preparation system based on capture methodology in China. This system can convert DNA samples into sequencing-ready libraries in approximately 9 hours, helping hospitals streamline testing processes, reduce manual labor, and mitigate risks. By the time of its stock market listing in June 2020, Magnis BR had been deployed in 11 hospitals across 9 provinces in China.

Of Burning Rock Biotech’s RMB 381.7 million in operating revenue in 2019, RMB 87.7 million came from in-hospital business, accounting for 23%, a figure nearly three times the RMB 33.2 million recorded in 2018.

Representatives of reagent manufacturers entering hospitals include Genetron Health and GenePlus, among others.

Since 2017, Genetron Health has progressively advanced the regulatory registration of three major product categories, implementing a three-step strategy to deepen its in-hospital services. The first step involved completing product registration for IDH1 and TERT gene detection kits. These two kits utilize PCR-based methods, requiring no additional training for pathologists upon introduction into hospital pathology departments. Notably, these kits specifically target gliomas, a rare indication, which facilitated rapid market access into hospitals. The second step saw the successive registration of biochip readers, mid-to-high-throughput NGS sequencers, and automated liquid handling systems. In particular, following the launch of the Genetron S5 gene sequencer in late 2019, Genetron Health accelerated its in-hospital deployment. In the third step, after establishing its brand and instruments within hospitals, Genetron Health focused on securing sequential approvals for more in-depth companion diagnostic products, thereby continuously meeting hospitals’ needs for precision medication.

Gene+ completed a RMB 250 million Series B+ financing round in November 2020. A year earlier, Gene+’s gene sequencers, the Gene+Seq-2000 and Gene+Seq-200—developed based on MGI’s core DNBSEQ technology and four-channel optical detection system—along with the corresponding lung cancer genetic testing kits and the supporting Gene+Oncobox software, successively obtained product registration certificates.

With complete certifications for its sequencers, kits, and software, and equipped with the Oncobox fully automated NGS analysis and interpretation system for oncology, Genetron Health has begun to pursue in-house implementation, providing hospitals with an integrated, end-to-end NGS solution. The company has successfully entered prestigious institutions such as Sun Yat-sen University Cancer Center, Henan Cancer Hospital, West China Hospital, and Zhejiang Cancer Hospital.

It is not difficult to see that whether for team-based or reagent-based hospital entry, customization of key equipment—such as library preparation systems and gene sequencers—is indispensable. If genetic testing companies primarily build their competitive advantage through clinical service capabilities during the service or product promotion phase, then in the localization phase, technical collaboration capability becomes an additional critical factor in competitiveness.

Disease screening is a high-priority national initiative and serves as a key lever for the prevention and control of several high-incidence diseases. Programs such as the annual “two-cancer screening” for women in urban and rural areas, and tuberculosis screening among young students, have basically achieved full coverage of eligible populations. Furthermore, in recent years, with the advancement and cost reduction of related technologies such as high-throughput gene sequencing, circulating tumor cell detection, and gene methylation testing, genetic testing has been increasingly widely applied in the precise diagnosis and treatment, as well as early screening and diagnosis, of clinical oncology and other major diseases. According to CIC projections, by 2030, the market size for early cancer screening will reach $28.9 billion, serving a user base of 20.3 million people.

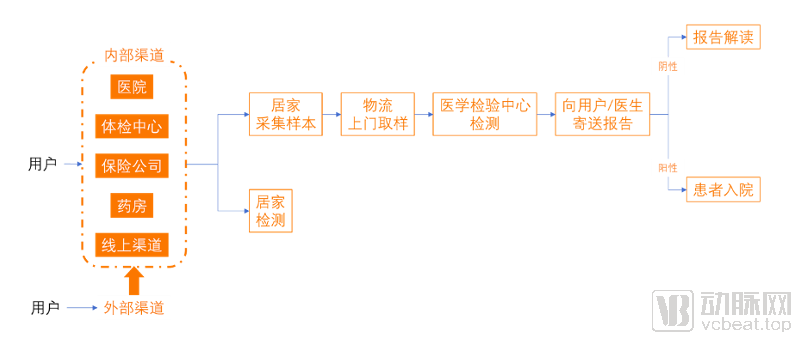

Prior to their widespread inclusion in the service price catalogs of medical institutions, genetic testing for early cancer screening was primarily conducted outside hospitals. The few tests available within hospitals were mainly offered in the form of Laboratory Developed Tests (LDTs). Health checkup centers currently serve as the primary channel for these services, with additional involvement from insurance companies, internet healthcare platforms, and offline pharmacies. VCBeat has observed entry points for genetic testing services focused on early diagnosis and screening on the official websites of both iKang Guobin and Meinian Onehealth, with prices ranging from several hundred to tens of thousands of yuan. Some tests are sold as standalone products, while others are embedded within premium health checkup packages. On the genetic testing channels of JD Health and Ali Health, the number of early diagnosis and screening projects is second only to that of non-invasive prenatal screening for neonatal diseases.

Application Process for Out-of-Hospital Early Diagnosis and Screening Programs

For years, disease screening programs based on out-of-hospital genetic testing have been mired in controversy over their efficacy. A key reason for this is that marketers have blurred the line between consumer-grade genetic testing and clinical-grade liquid biopsy performed in hospital settings. Typically, liquid biopsy refers to the detection of tumor cells in the human body by monitoring biomarkers released into the bloodstream by primary tumors or metastatic lesions. Currently, the major tumor biomarkers validated through extensive research include circulating tumor cells (CTCs), circulating tumor DNA (ctDNA) fragments, and liquid biopsy assays.

Although multiple liquid biopsy products have been approved and launched overseas, the only related product in China to have obtained a Class III medical device registration certificate is New Horizon Health’s ChangWeiqing, which is used for early screening of colorectal cancer. In its marketing efforts, New Horizon Health has positioned ChangWeiqing as a foothold for entering the hospital market.

Developing clinical-grade testing products to meet the needs of hospitals and disease control centers is an essential requirement for tumor screening products to fulfill their role in early diagnosis and early screening.

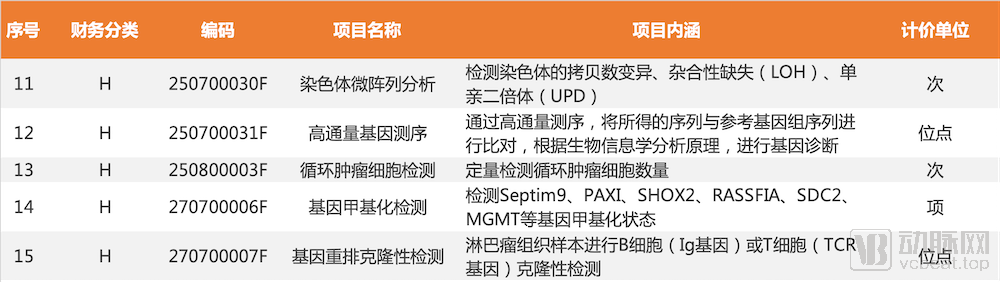

Not long ago, the Guangdong Provincial Healthcare Security Administration included several early screening-related technologies, such as high-throughput gene sequencing, circulating tumor cell (CTC) detection, and gene methylation testing, in the list of medical services with market-regulated pricing. These services are priced and charged per “locus,” per “test,” and per “item,” respectively. Notably, for gene methylation testing, which is widely used in cancer early screening, the detection of methylation status for multiple common loci—including Septin9, PAX1, SHOX2, RASSF1A, SDC2, and MGMT—has been incorporated into the pricing catalog.

List of Medical Service Price Items Subject to Market-Adjusted Pricing (Partial Inclusion)

In August 2020, a special project on liquid biopsy for tumors, supported by the National Key R&D Program, was launched. This initiative aims to break through key technologies in early cancer screening, diagnosis, and early intervention via liquid biopsy; establish a highly sensitive, specific, efficient, and cost-effective system for liquid biopsy of malignant tumors; develop screening/early diagnostic kits with independent intellectual property rights; and validate these tools for lung cancer and gastrointestinal cancers in large-scale, multicenter, prospective cohorts. Genetron Health and GenomiCare both participated in the project, providing critical technical support.

In September, Genetron Health’s HCCscreen™ received the “Breakthrough Device Designation” from the U.S. Food and Drug Administration (FDA). HCCscreen™ can simultaneously detect multiple methylation patterns and gene mutations in cell-free DNA from peripheral blood. In November, Genetron Health partnered with the Wuxi Municipal Government to launch the “Comprehensive Prevention and Control Project for Early Screening of Liver Cancer,” jointly establishing an operational center with invested capital. The project aims to provide screening and comprehensive prevention and control services to 150,000 individuals at high risk for liver cancer in Wuxi over a three-year period using HCCscreen™.

In December, Genetron Health completed a RMB 1 billion Series B financing round. Its early colorectal cancer screening and diagnostic products, ColonES® (Changlesi®) and ColonAiQ™ (Changaikè™), have completed the second round of pre-review for FDA product registration filings. Additionally, its multi-cancer early detection technology, PanSeer®, has achieved phased data results from a large-scale natural population cohort study. Following the completion of the Series B financing, Genetron Health plans to further expand its pipeline of early cancer screening product development and conduct expanded prospective validation for pan-cancer early screening products.

Pharmaceuticals

Furthermore, Burning Rock Biotech’s IPO prospectus explicitly listed investment in the research and development of cancer early screening technologies. Gene+ has also established an early screening platform capable of simultaneously detecting genomic variants and methylation levels. In collaboration with the Health Management Institute of the Chinese PLA General Hospital (301 Hospital), Xiangya Hospital, Henan Provincial People’s Hospital, Shenzhen People’s Hospital, and 17 other public hospital health examination centers—totaling 21 institutions—Gene+ is jointly conducting the PREDICT study (NCT04405557), a pan-cancer screening project for the Chinese population.

Validating the efficacy of early cancer screening products requires large-scale clinical trials, demanding substantial time and financial investment, while also necessitating regulatory innovation during the product registration process. As an increasing number of companies with robust genetic testing capabilities join the ranks of clinical research in early cancer screening, the adoption of these products in hospitals may be just around the corner.

mNGS is regarded as the next most promising application scenario for NGS and gained significant traction in 2019. In 2020, as the COVID-19 pandemic brought this technology to the forefront, an increasing amount of capital was attracted to the field. Star investment firms specializing in the healthcare sector, such as Fortune Capital, Proxima Ventures, Puhua Capital, Chende Capital, Volcanic Stone Capital, Guoke Jiahe, and CDH Investments, have all entered the market. During this period, mNGS financing exhibited two notable characteristics: exceptionally short intervals between funding rounds for invested projects, and a high frequency of financing events.

In terms of disclosure timing, the interval between Jinshi Medicine’s Series B and Series B+ financing rounds was no more than three months; Jieyi Biology completed both its Pre-A and Series A rounds within five months; and Yuguobiology announced its Pre-A and Pre-A+ rounds within a six-month period. Given that companies do not necessarily make public announcements immediately upon closing equity transactions, the actual completion dates of these financings may have been earlier, with even shorter intervals between rounds. In February, Yuguobiology and Ruiyi Biology successively announced their financing news; in August, Jieyi Biology and Weiyuan Biology followed suit. Weiyuan Biology’s Series B round raised as much as RMB 200 million, pushing capital attention in the mNGS sector to an unprecedented peak.

Summary of Financing Events in the mNGS Field in 2020

However, despite the dizzying array of capital-market activities, the internal order of the mNGS industry appears relatively stable. This may be partly because, having experienced the chaotic competition in tumor NGS, professionals in the genetic testing sector aim to establish industry standards and regulations first when entering a new field. On the other hand, pathogen detection and infectious disease diagnosis are inherently critical clinical needs within hospitals, which requires mNGS products and services to demonstrate clinical-grade accuracy from the outset.

Furthermore, regulatory authorities place significant emphasis on the compliant application of mNGS technology in both research and clinical settings, with several leading projects actively participating in the development of technical standards related to mNGS.

Senior industry practitioners told VCBeat that, since 2018, the National Institutes for Food and Drug Control (NIFDC), as a technical support department of the Center for Drug Evaluation (CDE) under the National Medical Products Administration, has organized relevant enterprises to conduct joint research on mNGS reference materials for three consecutive years.

“Regulating new technologies and products inevitably requires innovative rules,” the industry practitioner stated. “Such rules will inevitably become clearer through continuous interaction between enterprises and regulators, hence the high level of participation from all parties.”

In November, the “Expert Consensus on the Clinical Application of Metagenomic Next-Generation Sequencing (mNGS) for Detecting Infectious Pathogens,” the first expert consensus in China’s mNGS industry, was published in the Chinese Journal of Infectious Diseases. The consensus was discussed and drafted by a panel of 22 experts from 18 institutions across China. Professor Zhang Wenhong from Huashan Hospital Affiliated to Fudan University served as the corresponding author. This expert consensus provides guidance and recommendations, supported by evidence, on the clinical application scope, sample collection, analysis and interpretation, and quality control of mNGS.

Furthermore, single-cell sequencing was an indispensable topic in genetic testing in 2020. High-throughput single-cell sequencing technology is poised to gradually replace traditional bulk-sample next-generation sequencing, particularly in clinical practice and drug development. It can supplement or substitute existing molecular, cytological, and histopathological testing methods, or facilitate the development of systemic therapies such as emerging immunotherapies and cell and gene therapies.

In May 2020, Junhui Bio’s automated single-cell image analysis and isolation system was approved by the Hunan Provincial Medical Products Administration and officially obtained a Class II medical device registration certificate, becoming the first such certification in China in this field.

In September, November, and December, Singleron Biotechnologies secured three rounds of financing totaling $70 million, with investors including Tencent, Lilly Asia Ventures, Sherpa Capital, CDH Investments, and SoftBank China. Singleron’s product portfolio includes the Singleron Matrix™ automated single-cell sequencing library preparation instrument, GEXSCOPE® high-throughput single-cell sequencing kits, FocuSeq™ targeted high-throughput single-cell sequencing products, CeleScope™ bioinformatics analysis software, and the SynEcoSys™ single-cell database. The company has served nearly 300 renowned hospitals, pharmaceutical companies, and research institutions.

Another highly watched company in the single-cell sequencing field is Danxu Bio, which was founded in 2020 and completed its RMB 100 million Series A financing round in September. Co-founded by Professor Xie Xiaoliang, an academician of four academies in China and the United States, who also serves as its Chief Scientific Advisor, Danxu Bio primarily leverages its single-cell sequencing technology platform for the research and development of antibody-based therapeutics.

In August 2020, Danxu Bio reached an exclusive licensing agreement with BeiGene for the global development, manufacturing, and commercialization rights (excluding the Greater China region) of its first product, the neutralizing antibodies against SARS-CoV-2 (DXP593 and DXP604).

In reality, looking back from any point in time, genetic testing has always been a work in progress: older products mature, new ones emerge, some business models are disproven, and superior ones take their place. Many strong players will rise during this process, but dominance is not permanent. Embracing change is what enables the strong to become stronger.