Hetai Medical, China's First Domestic Cardiac Electrophysiology Listed Company, Secures Dual Strongholds in Vascular Intervention

On January 7, 2021, the first IPO in the medical sector for the year debuted as Huitai Medical, a company specializing in minimally invasive cardiovascular procedures, listed on the STAR Market. The issue price was RMB 74.46 per share, with an opening price of RMB 221.73, representing a gain of over 200% at the time of reporting.

In 2020, transcatheter heart valves led the medical device market in the field of minimally invasive cardiovascular interventions. The successive IPOs of Venus Medtech and Peijia Medical attracted widespread market attention and also drove a surge in primary market financing for vascular intervention technologies. This year, the vascular intervention sector remains hot, with the spotlight now on cardiac electrophysiology. In addition to Huitai Medical’s IPO, MicroPort EP raised RMB 300 million in August 2020 and may also pursue an IPO in the future.

Founded in 2002, Huitai Medical’s main products include high-value consumables in the field of cardiac interventional medical devices, such as electrophysiology multi-channel recording systems, radiofrequency ablation catheters, and electrode catheters; as well as interventional access and therapeutic products in the cardiovascular and peripheral intervention fields, such as guidewires, guiding catheters, angiographic kits, and microcatheters. Within the broader minimally invasive vascular intervention sector, Huitai Medical holds a strong position in two key segments: cardiac electrophysiology and access-related consumables.

In both major sectors, Huitai Medical is a key player among domestic brands. According to relevant research reports by Frost & Sullivan, Huitai Medical ranked first in market share among Chinese-branded electrophysiology medical device manufacturers and third among Chinese-branded coronary access medical device manufacturers in 2019, based on product sales revenue.

HyTai Medical's Financing History

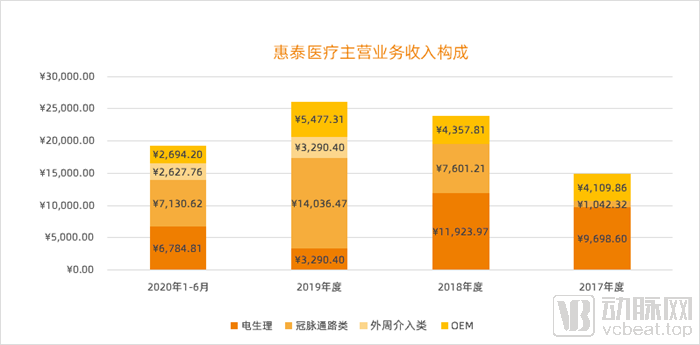

Huitai Medical’s revenue from principal operations recognized from sales of medical device products in 2017, 2018, 2019, and the first half of 2020 were respectivelyRMB 140 million, RMB 240 million, RMB 380 million, and RMB 190 million; the year-on-year sales revenue growth rates for the first two years were 60.82% and 67.85%, respectively,Achieved rapid growth. The net profit was RMB 78.0753 million in 2019, RMB 16.6748 million in 2018, and RMB 27.0814 million in 2017. In the revenue for the first half of 2020, electrophysiology products accounted for 35.27%, and coronary access products accounted for 37.07%.

In Huatai Medical's revenue structure, there are four main businesses: cardiac electrophysiology, coronary access, peripheral intervention, and OEM. Although coronary access products accounted for the largest share of revenue in 2019 and achieved rapid growth.However, we believe that the most noteworthy business segment of Huitai Medical is its cardiac electrophysiology business.。

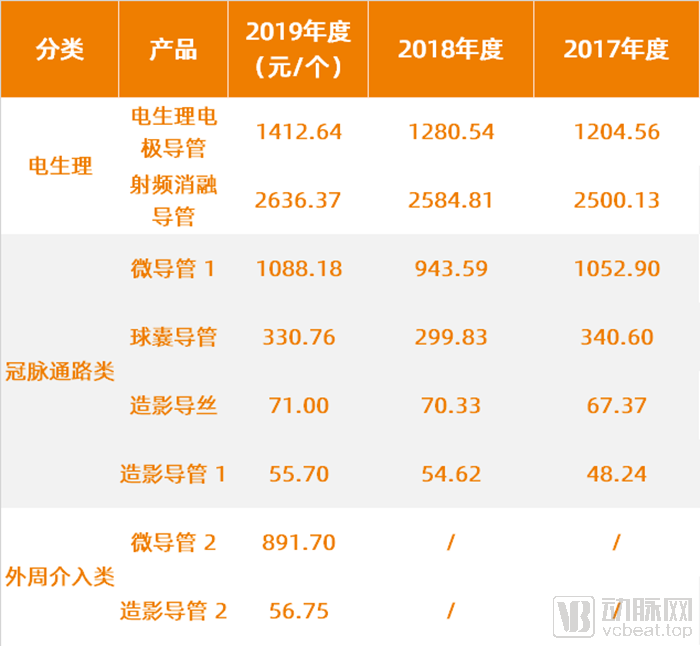

First, fromIn terms of gross profit margin and unit price, the cardiac electrophysiology business has the highest unit price and gross profit margin among the four main businesses. The gross profit margin of cardiac electrophysiology reached 77%.The unit price of the product is significantly higher than that of coronary access products.

Huitai Medical's Gross Profit Margin on Core Business

Unit Price of Huitai Medical's Main Products

In terms of industry influence,Huitai Medical holds the largest market share among domestically produced cardiac electrophysiology devices, establishing itself as the leader in China’s domestic electrophysiology sector and positioning it to become a primary driver of large-scale import substitution in the field.

Huitai is the first Chinese manufacturer to obtain market access for electrophysiology electrode catheters and steerable radiofrequency ablation electrode catheters, enabling their clinical application. This achievement filled the gap for domestic brands in the field of electrophysiology. Additionally, in 2011, Huitai became the first Chinese manufacturer to receive European Union CE certification for both product categories.

In the field of cardiology, electrophysiological techniques play a crucial role, primarily in the diagnosis and treatment of arrhythmias. Arrhythmia refers to any abnormality in the origin of the cardiac rhythm, heart rate and rhythm, or impulse conduction, manifesting as irregular heartbeat (too fast or too slow), with typical symptoms including palpitations and fatigue.

Atrial fibrillation is a common clinical arrhythmia. According to the "Atrial Fibrillation: Current Understanding and Treatment Recommendations-2018" published by the Electrophysiology and Pacing Branch of the Chinese Medical Association, the number of patients with atrial fibrillation in China has been increasing year by year. The prevalence rate among people over 35 years old is 0.77%. Based on this calculation, the number of patients with atrial fibrillation in China increased from 4.8 million in 2014 to 5.1 million in 2018. Furthermore, due to population aging, it is estimated that the number of patients with atrial fibrillation will reach 5.3 million by 2023.

Treatment options for arrhythmias include pharmacological and non-pharmacological therapies. Pharmacological treatments can be classified, based on their mechanisms of action, into sodium channel blockers, beta-blockers, agents that prolong the action potential duration, and calcium channel blockers. Although pharmacological therapy is generally the first-line treatment, it can only control heart rhythm to a certain extent, requires long-term administration, and is associated with side effects.For patients with arrhythmias that cannot be controlled by medication, non-pharmacological interventions such as catheter ablation and pacemaker implantation can help control heart rhythm and improve symptoms.

Electrophysiological treatment of arrhythmias is primarily achieved through catheter ablation. The diagnostic process of catheter ablation involves puncturing the femoral vein, internal jugular vein, or subclavian vein to deliver electrode catheters to specific sites within the cardiac chambers. This procedure first identifies and localizes the abnormal sites responsible for tachycardia, followed by localized radiofrequency ablation at these sites, serving as an interventional diagnostic approach to block abnormal electrical conduction pathways or origins in the heart.

According to data from the National Health Commission’s Quality Control Center for Interventional Management of Arrhythmias, the number of catheter ablation procedures performed for arrhythmia patients in mainland China has continued to grow in recent years, increasing from 101,000 cases in 2014 to 152,000 cases in 2018, with a compound annual growth rate (CAGR) of 10.7%.

China’s cardiac electrophysiology market is maintaining rapid growth. According to a report by Frost & Sullivan, the domestic market size for electrophysiology devices grew from RMB 1.13 billion in 2014 to RMB 3.33 billion in 2018, representing a compound annual growth rate (CAGR) of 30.9%. Driven by factors such as an aging population, an increasing number of patients with arrhythmias, the widespread adoption of ablation procedures, and upgrades to consumables used in these procedures, the market size for electrophysiology devices in China is projected to reach RMB 12.32 billion by 2023, with a CAGR of 29.9%.

The cardiac electrophysiology market is also a key business segment for global medical device giants. In 2019, Abbott’s electrophysiology revenue was $1,721 million; Medtronic’s electrophysiology revenue was $5,849 million; Boston Scientific’s revenue was $329 million; and Johnson & Johnson’s revenue was $2,997 million.

A defining characteristic of the cardiac electrophysiology market is import monopoly, with foreign enterprises accounting for more than 80% of the market. Foreign brands such as Johnson & Johnson, Abbott, Boston Scientific, and Terumo leverage their strong R&D capabilities, comprehensive product portfolios, and first-mover channel advantages to capture over 80% of the domestic market share.。

Currently, the domestic cardiac electrophysiology manufacturers include only a few companies such as Huitai Medical, MicroPort EP, Lepu Medical, Sichuan Jinjiang Electronics, and Xinonop. Among them, Huitai Medical has achieved the largest market share for domestically produced products in China.

However, even as the leader in the domestic electrophysiology sector, Huitai Medical ranks only fourth in China’s overall market, with a mere 3.4% market share, indicating substantial growth potential for Huitai Medical in the cardiac electrophysiology field.

How Can Huitai Medical Maintain Its First-Mover Advantage and Become a Major Force in Domestic Substitution in the Future?We believe the key lies in 3D electroanatomical mapping products for cardiac electrophysiology.

Currently, based on HT Medical’s product portfolio, the company has established a presence in the cardiac electrophysiology field with diagnostic, therapeutic, and access products. It holds nine registration approvals for electrophysiology products, including one multi-channel electrophysiology system and eight electrophysiology consumables, all of which are Class III medical devices. Its main products include the multi-channel electrophysiology system, electrophysiology electrode catheters, steerable radiofrequency ablation electrode catheters, and cooled saline-irrigated radiofrequency ablation catheters.

These 2D mapping products have enabled Huitai Medical to secure a foothold in the electrophysiology field; however, its ability to become a dominant brand will ultimately depend on its 3D mapping products.

From 2000 to 2010, China's cardiac electrophysiology field transitioned from two-dimensional to three-dimensional electroanatomic mapping.Three-dimensional electroanatomical mapping systems can reduce procedural time and fluoroscopy exposure, enhance ablation efficacy, and lower the postoperative recurrence rate of atrial fibrillation. Cardiac 3D electroanatomical mapping systems consist of two main components: equipment and catheter consumables.

Johnson & Johnson, Abbott, and Boston Scientific have all launched three-dimensional electrophysiology devices and consumables, subsequently dominating the market. Johnson & Johnson’s main products include the CARTO 3D system, the PENTARAY star-shaped magnetic-electric dual-location mapping catheter, mapping catheters, radiofrequency ablation catheters, and surface reference electrodes. Abbott’s main products include the EnSite 3D system, the ADVISOR magnetic-electric location circular mapping catheter, mapping catheters, and radiofrequency ablation catheters. Boston Scientific’s Rhythmia cardiac electrophysiology 3D mapping system was launched in China in 2015.

Among domestic players, MicroPort Medical also offers the Columbus 3D mapping system and circumferential pulmonary vein mapping catheters. In 2013, Sichuan Jinjiang Electronics’ 3D mapping system received regulatory approval for market launch; its hybrid magnetic-electric 3D mapping system is currently in clinical trials, while its mapping catheters are already commercially available.

Huitai Medical’s 3D mapping products are expected to be launched this year. Its independently developed dual-mode 3D mapping and navigation system has completed clinical trials and is currently in the stage of addressing supplementary registration requirements, with approval anticipated in the first half of 2021. In terms of catheter consumables, Huitai Medical’s next-generation electrophysiology product, the pressure-sensing ablation catheter, has been recognized as an “NMPA Innovative Product” and entered the special approval pathway. The magnetic location-enabled cold saline irrigated radiofrequency ablation electrode catheter is currently under regulatory review.

As a pioneer in the field of cardiac electrophysiology in China, Huitai Medical has established certain advantages in this sector. If it can maintain its first-mover advantage amidst increasingly intense competition, it may emerge as a more formidable competitor in the domestic electrophysiology market.

Breakthroughs in the field of cardiac electrophysiology represent a major highlight for Huitai Medical, while its other core business focuses on coronary access products. In the peripheral vascular intervention sector, Huitai Medical’s product portfolio is also primarily composed of access devices.

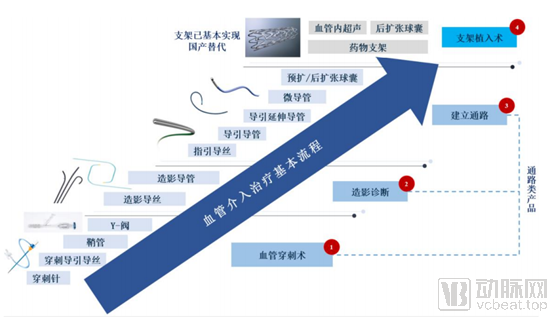

Access products are primarily composed of catheters and guidewires. In percutaneous coronary intervention (PCI) procedures, these access products establish the pathway for stent implantation. In the field of access products, the research, development, and manufacturing of guidewires and catheters demand exceptionally high standards in materials science and processing technology.

According to a report by Frost & Sullivan, the top five companies in China’s coronary access product market by sales are Terumo, Medtronic, Abbott, Merit Medical Systems, and Boston Scientific. Among them, first-tier players Terumo and Medtronic each hold approximately 20% of the market share, while second-tier companies Abbott, Merit Medical Systems, and Boston Scientific each account for around 10%. Together, these top five foreign brands capture roughly 70% of China’s coronary access product market. In contrast, domestic manufacturers hold a relatively small overall market share, with their product portfolios primarily consisting of coronary access support devices that feature lower technological sophistication and added value.

Huitai Medical ranked fourth among domestic manufacturers, with a market share of 1.3% in 2018 and an overall market ranking of 13th.

In the field of access products, since 2015, Huitai Medical has laid out products with relatively low technical barriers, such as angiographic guidewires and angiographic catheters, and gradually established a comprehensive portfolio of coronary products, including coronary guiding catheters, guiding wires, microcatheters, and extension catheters.

Moving forward, Huitai Medical will continue to expand its portfolio of access products in the peripheral vascular intervention and neurointervention fields. According to Huitai Medical’s prospectus, in the field of access products, the company has mastered multiple essential industrialization technologies for access products that were previously monopolized by foreign companies, such as “hydrophilic coating technology,” “wire mesh-reinforced extrusion,” and “dissimilar alloy joining.” It possesses advanced manufacturing capabilities for producing a variety of vascular intervention products, including catheters, balloons, and guidewires.

As Huitai Medical continues to launch its coronary access and peripheral access products and expand its sales channels, the revenue from its access product portfolio has experienced rapid growth, with a compound annual growth rate (CAGR) of 266.97%.

However, the localization rate for access consumables is higher than that in the cardiac electrophysiology field. Affected by the volume-based procurement (VBP) policy for high-value medical consumables, prices of low-end catheter and guidewire products dropped by more than 40% in previous regional VBP programs.

Huatai Medical faces certain challenges in maintaining high-speed growth within its access product business.

In addressing upcoming challenges, Huitai Medical has established a professional team. Its executive leadership includes numerous technical and marketing professionals from Johnson & Johnson, Medtronic, MicroPort, Lifetech Scientific, and Mindray.

Cheng Zhenghui, founder of Huitai Medical, earned his master’s degree from the Institute of Metal Research, Chinese Academy of Sciences. He served as General Manager of Lifetech Medical from July 1999 to April 2001, and in 2002 established Huitai Limited, the predecessor of Huitai Medical. Yuchen Qiu, Vice President responsible for R&D of vascular interventional products, previously worked as a Product Development Engineer at Johnson & Johnson Cordis. Zhang Yong, a core technical leader spearheading the development of next-generation electrophysiology devices, formerly held senior manager positions at MicroPort Medical and Covidien.

In the field of minimally invasive cardiovascular interventions, Huitai Medical has secured two strategic high grounds—cardiac electrophysiology and access consumables—enabling it to provide a multidimensional portfolio of products in the cardiovascular intervention sector.

At the same time, competition in these two fields is intensifying. On one hand, the pressure from medical insurance cost containment is being transmitted upstream along the industrial chain, placing greater strain on cardiovascular intervention companies. Meanwhile, the medical device industry is entering a golden period of development; cardiovascular intervention has become a highly sought-after sector, driving continuous industrial upgrading, and more players are expected to enter the cardiac electrophysiology market.

"As a key investor in Huitai Medical, Hu Xubo, Managing Partner at Qiming Venture Partners, stated, 'We are delighted to have accompanied Huitai Medical throughout its journey and witnessed this historic moment of its listing on the STAR Market. The founding team of Huitai Medical is ambitious and committed to independent R&D and innovation, striving to become a leading global brand in minimally invasive cardiovascular interventional devices. It aims to provide high-performance, high-quality, and more cost-competitive solutions for healthcare systems in China and worldwide. We believe that Huitai Medical will leverage its listing on the STAR Market as an opportunity to embark on a new and even more promising chapter.'"