Intuitive Surgical and Johnson & Johnson Vie for Dominance as Robotic Pulmonary Intervention Emerges as the Next High-Growth Frontier

The acquisition moves of medical device giants can be described as the “schedule” for observing the surgical robotics sector. Amid the complex and crowded R&D landscape for surgical robots, the segments targeted by these industry leaders may hold greater explosive potential in the future.

An analysis of the strategic moves by global giants in the surgical robotics sector in recent years reveals that rigid robotic systems, including orthopedic and laparoscopic surgical robots, have entered a highly competitive stage of commercialization worldwide. Companies such as Medtronic, Zimmer Biomet, Intuitive Surgical, and Stryker have already commercialized products in these fields, while flexible surgical robots are still in their nascent stages of development.

The primary difference between flexible surgical robots and rigid surgical robots is that flexible surgical robots can deform in response to their surrounding environment, making them more suitable for unstructured scenarios.

The flexible surgical robot sector will be a key segment within the broader surgical robot industry. Based on existing product applications, flexible surgical robots have been utilized in the treatment of diseases across several critical areas, including the lungs, gastrointestinal tract, and intracranial regions.

In the field of flexible surgical robots, pulmonary interventional surgical robots are currently the most noteworthy. This sector has frequently attracted favorable attention from industry giants, with mergers and acquisitions far exceeding those in other segments of the surgical robotics market in both frequency and transaction value. Leading companies in this space have also completed financing rounds in the primary market this year.

Just last week, the leader in the medical endoscopy field acquired Veran Medical Technologies (VMT), a company specializing in lung interventional navigation, for $340 million.

Previously, Johnson & Johnson also acquired the respiratory surgical robot company Auris Health for the astronomical sum of $3.4 billion. Both VMT and Auris Health are key players in the field of pulmonary intervention; the former specializes in pulmonary navigation, while the latter excels in surgical robotics.

In addition to Johnson & Johnson and Olympus, other giants with product portfolios in the field of pulmonary intervention include Medtronic and Intuitive Surgical, the parent company of the da Vinci Surgical System.

Why Is the Pulmonary Intervention Field Too Lucrative for Industry Giants to Ignore, Prompting a Wave of M&A and R&D Investment? What Product Forms Currently Exist in Pulmonary Intervention? What Are the Future Development Directions for Pulmonary Intervention Surgical Robots? VCBeat (WeChat ID: vcbeat) has compiled an overview of the key companies and major R&D directions in the pulmonary intervention sector.

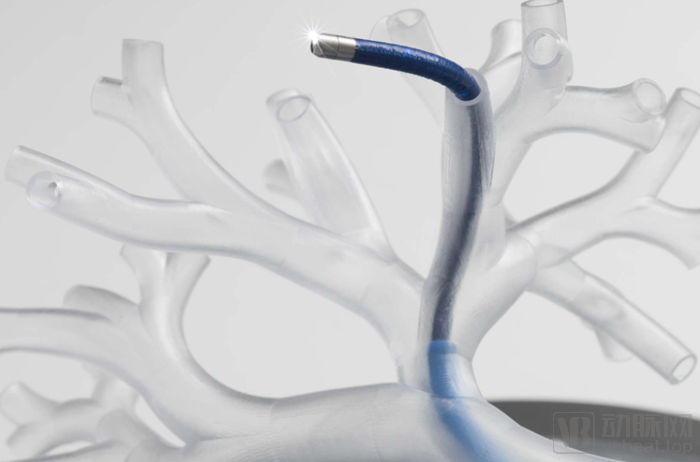

Pulmonary Interventional Surgical Robot. Image source: Auris Health

In fact, modern medicine is rapidly advancing toward endoscopic techniques for the treatment of many human organs, including the stomach, liver, and colon. Taking the digestive tract as an example, gastrointestinal endoscopy has evolved over more than a century from a purely diagnostic tool into one of the key approaches for minimally invasive therapy.

However, performing in-depth endoscopic examinations of the lungs remains challenging. This is primarily due to the extensive branching within the pulmonary system, which makes it difficult to navigate the course of each airway, compounded by the progressive narrowing of the bronchi. Accurately accessing deep lung regions for biopsy and extended interventional therapies has long been a significant challenge.

Meanwhile, there is a significant unmet need in the field of pulmonary diseases, where early diagnosis is critical for the treatment of lung cancer. As the cancer with the highest mortality rate, lung cancer is known as the “silent killer,” and its incidence and mortality rates continue to rise.

In China, reported statistical data show that the total number of newly diagnosed lung cancer cases in 2015 was approximately 787,000 (as data from the National Cancer Registry Center are typically delayed by several years, the latest report presents registration data from 2015).

According to data from the American Lung Association’s (ALA) “State of Lung Cancer 2020” report, 23% of lung cancer cases in the United States are diagnosed at an early stage, when the five-year survival rate is 59%. Another 22% of cases are detected at a locally advanced stage (spread to regional lymph nodes), with a five-year survival rate of 32%; 47% of cases are not identified until the late stage, by which time the survival rate has dropped to just 6%.

In the early diagnosis of lung cancer, CT imaging can detect pulmonary nodules, but only a biopsy can definitively determine whether the lesion is malignant. Methods for lung cancer biopsy include bronchoscopy and percutaneous needle aspiration.

However, even with these two approaches, precise biopsy of peripheral lesions remains a major challenge in biopsy-based diagnosis.

For bronchoscopy, the biopsy diagnostic yield is higher for central lesions located at the pulmonary hilum. In contrast, for peripheral lesions, bronchoscopes have difficulty reaching the target site, resulting in a lower probability of obtaining a pathological diagnosis. According to data from the Auris Health website, approximately 40% of pulmonary nodules are located outside the airways.

Percutaneous needle biopsy involves locating pulmonary lesions via CT or X-ray scanning, inserting a biopsy needle through the chest wall into the lung lesion to obtain tissue samples. This is currently a common method for diagnosing peripheral parenchymal lesions. However, percutaneous needle biopsy is not suitable for tiny nodules. Furthermore, the absence of cancer cells in biopsy specimens does not completely rule out lung cancer, as there is a risk of false-negative results. Additionally, complications such as pneumothorax are prone to occur.

Overcoming the limitations of existing biopsy methods to enable physicians to monitor the trajectory of pulmonary airway branches in real time and achieve whole-lung accessibility during lung biopsies—this constitutes the significance of interventional lung robots in diagnostic applications.

However, the significance of pulmonary interventional robots extends far beyond this. In the future, these robots will evolve into a comprehensive pulmonary interventional platform equipped with various therapeutic tools, thereby unlocking new possibilities for minimally invasive pulmonary interventions.

A platform-based product for pulmonary interventional diagnosis and treatment has been established on flexible surgical robots. In the current industrial landscape, multiple surgical robotics companies have made strategic moves in this area, with products from Medtronic, Johnson & Johnson, and Intuitive Surgical already having entered the commercialization stage.

In terms of objectives, all products aim to achieve access to the entire lung; however, their implementation pathways differ significantly. Product strategies can be categorized into two types: one approach combines endoscopy with navigation software, while the other involves an interventional surgical robot platform integrated with diagnostic or therapeutic devices such as endoscopes, biopsy forceps, and microwave ablation systems.

A representative of the former approach, combining endoscopy with navigation products, is Medtronic’s superDimension™ Navigation System. This system provides navigation assistance to physicians during bronchoscopy procedures.

The pathway enabled by the superDimension™ Navigation System is established through CT scan-based modeling to construct a 3D model of the patient’s lungs. This 3D model serves as a “map” for physicians during biopsy procedures.

After the map is generated, catheter positioning must still be completed. The bronchoscope catheter of the superDimension™ Navigation System is equipped with a sensor at its tip, which emits signals to three magnetic poles and an electromagnetic localization board during the procedure. The position of the bronchoscope can be localized using the electromagnetic board placed beneath the patient.

With the assistance of navigation-guided bronchoscopy, physicians can access deeper regions of the lungs. Upon reaching the lesion, a biopsy brush and forceps are extended through the catheter to obtain tissue samples.

In this process, the CT-based model is not generated in real time but is constructed preoperatively, resulting in a temporal discrepancy. Since respiratory motion may affect the position of pulmonary nodules, compensating for this error is critical.

Representatives of the latter approach to surgical robots include Johnson & Johnson’s Auris Health and Intuitive Surgical’s Ion endoluminal system. Pulmonary interventional surgical robots enable real-time navigation, with robotic arms that can actively advance under the control of the physician’s operating handle.

The primary distinction between surgical robots and electromagnetic navigation products lies in the fact that the catheter of a surgical robot is actively controlled, whereas endoscopy combined with electromagnetic navigation involves passive manipulation.

"Active" means that the doctor controls the robotic arm catheter through a handle, and the robotic arm can automatically advance during operation, exhibiting characteristics of a robot.

Operation via a joystick-like controller enables physicians to achieve full control over the bronchoscope, ensuring precise maneuvers when navigating the small airways of the bronchial tree. In contrast, passive systems involve direct manual control of the endoscopic catheter by the physician. Robotic endoscopic surgery systems can alleviate operator fatigue associated with prolonged procedures and effectively shorten the training curve for endoscope insertion.

Lu Hanjie, an investor in the Life Sciences Group at Huachuang Capital, stated, “Active soft-tissue robots offer higher precision in distal control and can achieve automatic steering. In contrast, catheters for electromagnetic navigation often require pre-shaping before insertion. A robotic system for pulmonary interventional procedures is a comprehensive platform, whereas electromagnetic navigation is more akin to a disposable product.”

In addition to operational differences, lung navigation for robotic endoscopy products is real-time navigation.

In the establishment of lung models, surgical robots are similar to electromagnetic navigation systems, as both are built using CT imaging. In terms of navigation and positioning technology, Auris employs a hybrid positioning approach that integrates three distinct navigation technologies—electromagnetics, optical pattern recognition, and robotic kinematic data—to measure the bronchoscope’s position and provide accurate positional data to physicians performing bronchoscopic procedures.

Why Minimally Invasive Pulmonary Interventions Are Gaining Favor Among Industry GiantsFirst, the lungs still present significant opportunities for exploration. Meanwhile, innovations in flexible endoscopic equipment are meeting the demands of clinical procedures, and the evolution from diagnostic tools to therapeutic platforms represents a key trend in the endoscopy industry. Consequently, endoscope manufacturers such as Olympus and Aohua Endoscopy are paying close attention to this field.

MicroPort MedBot has also previously announced its entry into the field of bronchial surgical robotics and has successfully completed the first robot-assisted bronchoscopic alveolar lavage procedure. MicroPort has further entered into a strategic cooperation agreement with Singapore-based NDR Medical Technology (“NDR”) and established a joint venture in China to handle the distribution, manufacturing, and co-development of NDR’s products in the Greater China region. The percutaneous puncture surgical robot developed by NDR can be applied to percutaneous lung biopsy and percutaneous nephrolithotomy.

Entering the field of pulmonary interventional surgical robots means solving a dual challenge: on one hand, it involves the development of endoscopic systems, and on the other hand, it concerns the development of surgical robot systems.

In the research and development of endoscopic systems, the design and manufacture of endoscopes involve numerous precision structural designs and machining technologies. Endoscope components are characterized by small dimensions, a high prevalence of thin-walled parts, and stringent machining accuracy requirements. Furthermore, compliance with biocompatibility standards significantly limits the selection of applicable materials for these components. In addition to high-precision hardware manufacturing, advanced image processing capabilities—including low-loss image signal transmission, spectral staining technology, and light adjustment algorithms—are essential to deliver images that are low-latency, highly responsive, clear, and bright.

In the development of surgical robots, flexible robots differ significantly from rigid surgical robots. Flexible surgical robots offer a higher degree of operational freedom, but this inevitably results in lower force application, poorer controllability, and a lack of sensing capabilities.

Endoscopic surgical robots rely on motors within a confined volume to achieve high-precision advancement, retraction, rotation, and bending of the endoscope, thereby replacing physicians in the process of endoscope insertion. Therefore, the primary challenge lies in extending the length of the flexible robotic arm while maintaining sufficient rigidity at its distal end. Adequate distal rigidity is essential to ensure the operational precision and stability required for performing surgical procedures. Meanwhile, sufficient length of the flexible robotic arm is necessary to reach distant surgical targets.

While meeting performance specifications, electronically controlled endoscopes must ensure absolute patient safety; therefore, comprehensive safety assurance features need to be designed, involving the use of a series of micro-sensors and risk detection algorithms.

However, it is worth noting that building a therapeutic platform with surgical robots is not as simple as playing with building blocks. The underlying technology and platform must be sufficiently robust to support multiple therapeutic suites.

Lu Hanjie, an investor in the Life Sciences Group at Huachuang Capital, stated, “Taking endobronchial thermal vapor ablation for chronic obstructive pulmonary disease (COPD) as an example, companies both domestically and internationally are currently attempting to develop combination products. However, integrating high-temperature therapeutic devices requires that the robotic arms of surgical robots be heat-resistant. Furthermore, with regard to light sources, it is crucial to configure dimming and spectral staining algorithms to render images familiar to physicians, ensuring clear visualization even in complex scenarios such as active bleeding. Therefore, flexible surgical robots are not merely assembled from disparate components; rather, they necessitate a system designed from the ground up.”

The greatest challenge lies in controlling costs while achieving high-performance R&D, thereby reducing the barriers to clinical commercialization.

The robotic arms of surgical robots have always been expensive, yet in previous surgical applications, some patients were still able to afford them.

However, diagnosis differs from treatment. Across all healthcare systems, the prerequisite for diagnostic products to realize their maximum commercial value is sufficient population coverage. The business model reliant on high-priced, repeatedly consumed disposables may be ill-suited to the diagnostic context.

In diagnostic scenarios, it is also worth considering how to select a business model that fits the local healthcare system.

Currently, Johnson & Johnson’s Auris lung diagnostic robot charges patients over $2,000 per diagnostic procedure, which is not considered affordable for a single biopsy. However, within the U.S. healthcare system, where costs are covered by insurance, commercial insurers demonstrate a strong willingness to pay for technologies capable of early disease detection. Across the broader healthcare ecosystem, early screening and diagnosis translate into extended periods of medication use; consequently, pharmaceutical companies are highly motivated to facilitate the clinical adoption of early diagnostic technologies.

However, there are significant differences between the domestic and international environments. In China, the healthcare system is primarily funded by medical insurance, which faces substantial pressure to control costs. Whether high-priced products like surgical robots can identify a suitable business model to achieve large-scale clinical application remains a major challenge.

From the perspective of existing solutions, bronchoscopic lung biopsy may not constitute a significant market, and its scale is unlikely to support a dedicated industry sector.

Why are giants such as Medtronic, Johnson & Johnson, and Intuitive Surgical willing to dive in? Because diagnosis is only the first step; in the future, pulmonary interventional products have the opportunity to become integrated diagnostic and therapeutic platforms, thereby unlocking the pulmonary intervention market.

Johnson & Johnson’s acquisition of Auris Health, made at a substantial cost years ago, has gradually revealed its product form and strategic layout after two years of development. It turns out that Johnson & Johnson’s initial interest in acquiring Auris Health lay not in the surgical robot as a form factor, nor in establishing a presence in the surgical robotics business per se, but rather in Auris Health’s flexible robotic arms capable of navigating through natural orifices. By integrating Auris Health’s lung intervention robot with the tissue microwave ablation technology from NeuWave Medical—another company acquired by Johnson & Johnson for $300 million in March 2016—the company launched a transbronchial microwave ablation product in 2020. This product was granted Breakthrough Device designation by the U.S. Food and Drug Administration (FDA) in July 2020.

Medtronic has also launched the CoreCath™ 2.7S electrosurgical device in the field of pulmonary intervention, which is combined with flexible bronchoscope products to resect soft tissue obstructions in the upper respiratory tract and tracheobronchial tree, provide electrosurgical hemostasis, and evacuate surgical smoke during such procedures. In addition, Medtronic is exploring the combination of superDimension with the Emprint ablation catheter to perform transbronchial interventional ablation for lung cancer. Currently, this product has only received CE certification.

Broncus Medical, a startup from China, is also developing the InterVapor thermal vapor therapy system for emphysema, which treats chronic obstructive pulmonary disease (COPD) using high-temperature water vapor.

The strategic moves of various companies have already highlighted the product development trend of combining pulmonary navigation with minimally invasive therapy. Developing therapeutic products within the interventional portfolio not only extends the diagnostic capabilities of existing diagnostic products but also enables the formation of a “1+N” product matrix, thereby maximizing product value.

Whether electromagnetic navigation bronchoscopy (ENB) or pulmonary interventional robots, their clinical applications are still in the early stages. More evidence needs to be collected over the next decade to confirm the safety and efficacy of these technologies.

However, a foreseeable trend is that navigational bronchoscopy or other forms of guided bronchoscopy, which can assist physicians in freely exploring the lungs, will receive close attention over the next decade.