Medical IPO Boom in 2020: Sector Reaches Nearly RMB 2 Trillion Market Cap, Harvest Season for Hillhouse, Sequoia, and Qiming

“This is the seventh time I’ve won the lottery this year.”

At the end of 2020, a retail investor posted on their WeChat Moments, “As shown below,” accompanied by a screenshot of an SMS notification confirming an IPO allotment. In 2018, the Hong Kong Stock Exchange revised its listing rules; in 2019, the Shanghai Stock Exchange launched the STAR Market; and in 2020, the Shenzhen Stock Exchange implemented the registration-based IPO system for its ChiNext board. The IPO market was effectively rebooted, with 585 companies going public throughout the year, averaging 1.6 listings per day.

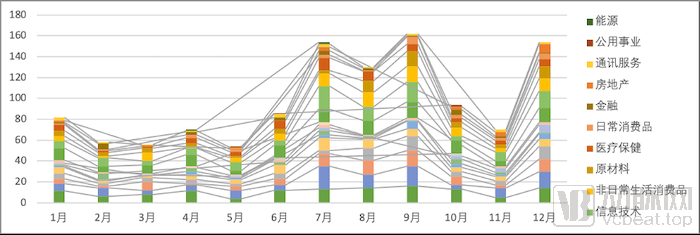

Number of IPOs Across Different Industries in 2020

As internet-based brokerages continue to strengthen their qualifications and capabilities, cross-border and cross-market portfolio investment has become increasingly convenient, truly ushering in the golden age of IPO subscriptions and equity investment. This progress is driven by the innovative practices of financial regulators, corporate executives, venture capitalists, and capital market organizers.

In 2020, regulatory reforms in mainland China’s capital markets, ranging from the registration-based IPO system to the new delisting rules, advanced into deep waters.

On February 14, the rules for refinancing were adjusted, relaxing restrictions on listed companies' refinancing.

On March 1, the Securities Law of the People's Republic of China came into effect, fully implementing the registration-based system.

On March 20, the China Securities Regulatory Commission (CSRC) issued a policy document encouraging hard-tech companies to list on the STAR Market. Subsequently, the Shanghai Stock Exchange adjusted the issuance and listing rules for STAR Market enterprises, refining the industry scope by specifying six major sectors.

On April 17, the Guiding Opinions on the Transfer of Companies Listed on the National Equities Exchange and Quotations (NEEQ) to Stock Exchanges were issued, optimizing the issuance and financing system, improving the existing private placement mechanism, and allowing eligible companies in the Innovation Tier to conduct public offerings of shares to unspecified qualified investors.

On June 12, the ChiNext board released its Initial Public Offering (IPO) measures, clarifying listing criteria. In August, the ChiNext board officially launched following the implementation of the registration-based IPO system reform.

On December 14, the Shanghai Stock Exchange and the Hong Kong Stock Exchange introduced new delisting regulations, improving four categories of mandatory delisting. The revisions include adding quantitative indicators for financial fraud, removing single delisting criteria, introducing combined financial metrics, adding market capitalization-based delisting criteria, incorporating disclosure and operational compliance as delisting grounds, clarifying standards for delisting due to financial fraud, streamlining the delisting process, and abolishing the mechanisms for suspension and reinstatement of listings.

A more efficient capital market with clearer rules has laid the foundation for the IPO boom.

Throughout 2020, 71 healthcare and medical projects went public, with a combined IPO market capitalization of RMB 1.56 trillion. Among them, JD Health, which listed on the Hong Kong Stock Exchange in early December, had an IPO market cap of RMB 289.9 billion, making it the healthcare stock with the highest market valuation among new listings in 2020. As of press time, the total market capitalization of these 71 newly listed pharmaceutical and healthcare stocks has grown to RMB 1.75 trillion, with JD Health’s market cap exceeding RMB 400 billion.

71 Healthcare Stocks That Went Public in 2020

(Note: The above data is extracted based on the GICS industry classification and does not include companies not classified under GICS Healthcare.)

It is evident that in 2020, companies going public were primarily from the biotechnology and medical device sectors, with 42 and 20 IPOs respectively. Among biotechnology IPOs, innovative drug projects accounted for 25 cases, making them the predominant category. Medical device IPOs were mainly driven by in vitro diagnostics (IVD) projects, totaling 10.

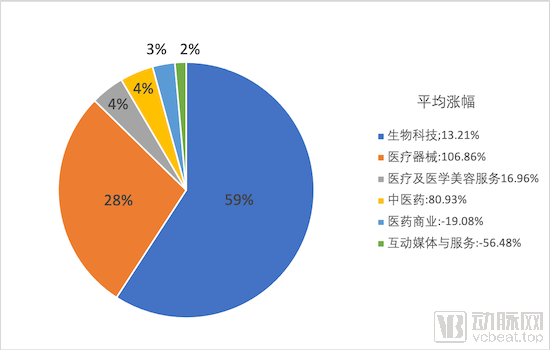

Distribution and Average Growth of 71 Healthcare Stocks by Sector in 2020

Since 2018, domestically developed innovative drug projects have entered a fast track for initial public offerings (IPOs), with a surge in listings in 2020 that saw an average of two projects entering the capital market each month. Since their IPOs, the average market capitalization growth for these innovative drug projects has been 12.33%, significantly lower than that of vaccines (223.08%), traditional Chinese medicine (49.97%), and contract research organizations (CROs) (58.52%).

Subsectors, Market Capitalization, and Price Gains of 42 Biotech Stocks

Further data analysis reveals that innovative drug IPOs listed on the Hong Kong Stock Exchange (12 projects, 10 of which were unprofitable) and the STAR Market (11 projects, 4 of which were unprofitable)—which accounted for the largest proportions—have demonstrated relatively weak ability to preserve or increase value post-listing. Specifically, the average market capitalization growth for Hong Kong-listed projects was 11.08%, with five stocks rising and seven falling. In contrast, the average market capitalization of STAR Market projects declined by 34.77%, with all 11 stocks experiencing a shrinkage in market value. Thus, it is evident that not only does innovative drug R&D face daunting odds, but so does investment in this sector. Nevertheless, we prefer to view this as a transitional phase rather than the final outcome.

The underlying reasons are multifaceted, with one key factor being the high market capitalization at IPO. A secondary-market investor who has long specialized in healthcare stocks told VCBeat that investing in healthcare equities entails a high professional threshold, making it a challenging decision for most secondary-market investors. Nevertheless, the market remains relatively optimistic about the healthcare sector, assigning lofty valuations. This has also exerted upward pressure on the share prices of newly listed healthcare companies, leading to pronounced divergence among individual stocks.

On the other hand, this is due to the high uncertainty surrounding the operating performance of innovative drug companies. For pre-revenue biotech firms, the R&D pipeline serves as one of the few reliable indicators for assessing business performance. Beyond the optimism driven by technological advancement and potential market size, investors who have evaluated a growing number of innovative drug projects are increasingly relying on more quantifiable operational metrics to refine valuations and eliminate overestimation. These metrics include: Has the drug entered Phase II clinical trials? Is the development progress leading within its class? Is it a first-in-class novel drug? Is it an in-house developed project? Are international multi-center clinical trials being conducted?

Take Sinocelltech, which has seen a significant decline in its market value on the STAR Market, as an example. Its faster-moving R&D projects are biosimilars already marketed in China, such as rituximab (submitted for registration) and bevacizumab and adalimumab (in Phase III clinical trials). However, there are more than 33 competing products that are either already launched or further along in development. Coupled with the national centralized procurement of biosimilars, losses in the secondary market are inevitable. Meanwhile, Aivita Biopharma, another company with lackluster stock performance, is advancing its core product through Phase II clinical trials in the United States and Phase I trials in China. While expected R&D expenditures are substantial, commercialization remains distant, fitting squarely into the “de-bubbling” conditions affecting valuations of innovative drugs.

The “squeeze-out” logic is also affecting Hong Kong-listed stocks. For instance, Jianeng Biologics’ R&D pipeline faces a predicament similar to that of SinoCellTech, with more than 10 investigational products in the early stages of clinical trials and making only modest progress; its share price has remained in a long-term downtrend since its IPO. Ditto Therapeutics and Harbour BioMed, both having been listed for a relatively short period, also lack impressive capabilities in developing original pipelines, resulting in sluggish stock price appreciation.

But is it truly necessary to completely squeeze the valuation bubble out of innovative drug projects based solely on operational details? Or to what extent should such adjustments be made? This remains a debatable issue. From an economic perspective, “no bubble, no prosperity,” which is particularly true in the new drug R&D industry that requires substantial capital, long investment cycles, and entails high risks. Painting a broad prospect for innovative drugs is, in essence, another form of “quenching thirst by thinking of plums.” Although “one general’s success is built upon ten thousand withering bones,” as long as investors enter the market with a set of “bubble-squeezing logic,” all attempts are worthwhile.

In 2020, ten IVD companies went public. By then, each subsector—from chemiluminescence and immunoassays to molecular diagnostics, and from instruments and reagents to medical services—had at least two listed companies. From a quantitative perspective, the growth potential of the IVD industry has become limited. Among these ten IVD companies, except for Burning Rock Biotech and Genetron Health, which adopted next-generation sequencing (NGS) technology, the others were primarily suppliers of traditional molecular diagnostics. However, based on secondary market reactions, the market penetration capability of NGS-based products has not yet gained sufficient recognition.

Another promising sector in the medical device industry that may see IPO “clearing” is heart valves. In May, Peijia Medical, one of the “Four Little Dragons” in the heart valve space, went public, reaching a latest market capitalization of RMB 16.614 billion. Earlier listings MicroPort and Venus Medtech have achieved market caps of RMB 95.815 billion and RMB 31.152 billion, respectively, while another member of the “Four Little Dragons,” Jiecheng Medical, has been embroiled in bankruptcy turmoil since early 2020. Peijia Medical received backing from top-tier institutions such as Hillhouse Capital and Matrix Partners China. Its IPO was oversubscribed more than 1,000 times, briefly making it the “king of frozen funds.” However, Peijia Medical’s performance in the secondary market has not been particularly impressive, which may reflect that public investors remain far from satisfied with the penetration rate of minimally invasive vascular intervention products.

On the IPO track for medical devices, the new star project is undoubtedly Tinavi. As the first surgical robotics company listed on the STAR Market, Tinavi’s market capitalization surged fivefold on its IPO debut day. However, by year-end, its market cap had fallen to just over 40% of its initial IPO valuation. For medical device companies, the secondary market is far more stringent than the primary market. Although Tinavi has achieved considerable penetration, covering nearly 80 Grade A tertiary hospitals and accumulating a surgical volume exceeding 5,000 procedures—impressive figures given the overall low market share of domestically produced medical robots—this performance is still insufficient.

Certainly, there were also sectors favored by the secondary market during the 2020 IPOs. Driven by JD Health, the average market capitalization of IPOs in the healthcare commerce sector reached RMB 147.7 billion in 2020, with JD Health’s IPO valuation at RMB 289.8 billion and Jianzhijia’s at RMB 5.562 billion. As of press time, JD Health’s market cap had once surpassed RMB 400 billion, demonstrating how the boundless potential of internet healthcare is being realized in the capital markets.

From 2017 to 2019, JD Health’s sales revenue from self-operated pharmaceuticals and health products was RMB 4.907 billion, RMB 7.254 billion, and RMB 9.434 billion, respectively, representing a compound annual growth rate (CAGR) of 38.65%. In 2019, the retail business sales revenues of the four listed offline pharmacy chains—Laobaixing Pharmacy, Dashenlin Pharmaceutical Group, Yixintang Pharmaceutical Group, and Yifeng Pharmacy—were RMB 10.289 billion, RMB 10.664 billion, RMB 9.934 billion, and RMB 9.589 billion, respectively, with corresponding year-on-year growth rates of 22.41%, 25.72%, 14.19%, and 46.55%.

Yifeng Pharmacy, whose retail pharmaceutical operation data most closely resembles that of JD Health, has a latest market capitalization of RMB 51.743 billion, while the market caps of several other peers range between RMB 20 billion and RMB 60 billion. This indicates that a significant portion of JD Health’s high valuation is attributable to its online platform, advertising, and other income streams, which currently account for approximately 12% of its total revenue.

In fact, as a technology-driven company, JD Health has been increasing its R&D investment year by year, with a cumulative investment of nearly RMB 700 million from 2017 to 2019. These funds have helped JD Health integrate new technologies such as intelligent assisted consultation and intelligent prescription review into its own business, and leverage its technological advantages to provide digital solutions for other participants in the industry chain. Currently, JD Health, with its internet DNA, has demonstrated strong momentum in online services. Building on its self-operated JD Pharmacy, it has onboarded more than 9,000 third-party merchants, providing users in over 200 cities with around-the-clock service featuring delivery in as fast as 30 minutes, thereby rapidly aggregating its large user base in the post-pandemic era.

Some investors once joked that if they didn’t have any portfolio companies go public in 2020, they would be too embarrassed to claim they were engaged in healthcare investment. VCBeat compiled primary-market financing information for the aforementioned 70 healthcare stocks from its Artery Orange database, and combined this with other publicly available data to identify 236 investment firms that had portfolio companies complete IPOs in 2020. These investments were predominantly made at Series A and Series B stages, covering the full spectrum from early-stage angel rounds to late-stage strategic financings and private placements.

Among 236 investment institutions, 39 had two or more portfolio companies undergo initial public offerings (IPOs) in 2020. Hillhouse Capital (11), Sequoia Capital China (10), and Qiming Venture Partners (9) ranked top three in the number of IPO projects.

Number of IPOs by Selected Investment Institutions in 2020

Hillhouse Capital

I-Mab: Series C, Equity Financing

Peijia Medical: Series A

Gan & Lee Pharmaceuticals: Strategic Financing

Junshi Biosciences: Private Placement

Tigermed: Private Placement

Everest Medicines: Series C

JD Health: Series B

Jiahui Biopharma: Series B

Jacobio: Series C

Antengene: Series C

TC Medical: Early Stage

(Not included in I(PO Cornerstone Investment Project)

Sequoia Capital China

Snibe: Series A, Series B

Burning Rock Biotech: Series A+, Series B, Series C, IPO

Ocuvist: Cornerstone Investment

Tigermed: -

Winner Medical: Series A

iRay Technology: -

JW Therapeutics: Series A, Series B

Antengene: Cornerstone Investment

JD Health: -

Zai Lab: Series A, Series B

(In addition, Beam Therapeutics, which is invested in by Sequoia Capital China Fund, was founded overseas by Chinese scientist Feng Zhang and also listed on the U.S. stock market in 2020.)

Qiming Venture Partners

Sanyou Medical

SinoCellTech: Series A

Gan & Lee Pharmaceuticals: Angel Round, Series B

Tigermed: Series A, Series B

CanSino Biologics: Series B, Series C

Zai Lab: Series A, Series B

Genor Biopharma: -

Antengene: Series A, Series B, Series C

Jacobio: Series B, Series C

(Investment round data is primarily based on news coverage.)

Eli Lilly Asia Venture Fund

Peijia Medical: Series B, Series C

Burning Rock Biotech: Series C

CanSino: Series B, Series C, Strategic Financing

Sansure Biotech: Strategic Financing

RemeGen: Undisclosed

Allist: Equity Financing

Jacobio: Series B

Legend Biotech: Strategic Financing

CDH Investments

SinoCellTech: Series B

Harbour BioMed: Series A+ Round

InnoCare Pharma: Series C

Nanxin Pharmaceutical: Series C

Chengdu HitGen: Series B

Fudan Zhangjiang: Series A

Shenzhen Capital Group

Zelgen Biopharmaceuticals: Series B

Akeso: Series A, Series B, Series C, Series D

Huisheng Biotechnology: Series A, Series C

Frontier Biotechnologies: Series C

RemeGen: -

Winner Medical: -

Among the 39 biopharmaceutical companies that went public in 2020, 20 had not yet achieved profitability; among the 20 medical device companies, 2 were unprofitable. The aforementioned nine investment firms placed significant bets on these unprofitable ventures.

Among Hillhouse Capital’s 11 projects, Akeso, Peijia Medical, Junshi Biosciences, Everest Medicines, Genor Biopharma, Jacobio Pharmaceuticals, and Antengene were all unprofitable at the time of their IPOs. Most of the 10 IPO projects backed by Sequoia China also received investment starting from Series A, with continued support throughout; the longest-held portfolio company was Snibe Diagnostics, which took nine years from initial investment to listing, delivering a 70-fold return for Sequoia China. Among Qiming Venture Partners’ nine projects, four—SinoCellTech, CanSino Biologics, Zai Lab, and Antengene—were unprofitable, and additional investments were made in all except SinoCellTech. The core products of these unprofitable companies are mostly still in clinical trials, with commercialization yet to begin.

For startups, the infusion of venture capital provides the essential financial support for early-stage research and development, enabling products to take shape. From the perspective of investment institutions, this represents a forward extension of the value chain. In 2020, Value, authored by Zhang Lei, founder of Hillhouse Capital, became a sensation in the investment community. A quote from the book aptly elucidates the fundamental logic behind investing in pre-profitability projects: “We are entrepreneurs, who just happen to be investors.”

Compared with pure financial investors, these investment institutions possess an additional incubation-oriented attribute. They typically establish medical investment teams with professional academic and industrial backgrounds, which not only identify high-quality targets but also provide diversified post-investment services. It is common for investors to meet founding teams in laboratories, with numerous investment stories emerging from their joint exploration of technology commercialization strategies. Some investors even assist startups in refining their organizational structures and leverage the power of their investment portfolios to drive the commercial implementation of entrepreneurial projects.

Extending the value chain forward amplifies both the risks and returns of investment, while adding post-investment services reduces information asymmetry between investors and entrepreneurial teams. This venture capital ecosystem, which is approaching the maturity of established capital markets, has invigorated China’s innovation and entrepreneurship landscape and has become a significant driver behind the recent surge in IPOs.

Furthermore, the elongation of the investment chain has emerged as a major trend in healthcare venture capital in recent years. At the project level, this translates to a lower frequency of transactions by investment firms, with leading investors gradually abandoning the former “sector-betting” model. In fact, in the secondary market, frequent trading is indicative of an immature investment style. The prerequisite for a “buy-and-hold” strategy is long-term observation and accurate analysis of the target assets.

Among healthcare stocks that went public in 2020, Shenzhen Capital Group increased its stakes in Akeso through Series B, C, and D rounds after initially investing in its Series A; Lilly Asia Ventures continuously participated in CanSino Biologics’ Series B, Series C, and strategic financing rounds; Qiming Venture Partners followed up on ATG Therapeutics’ Series A, Series B, and Series B+ rounds; and Sequoia Capital China invested in Burning Rock Biotech’s Series A+, Series B, and Series C rounds. These cases demonstrate the strong confidence of institutional investors in their selected portfolio companies.

Lilly Asia Ventures, which ranked second in the number of portfolio companies that went public in 2020, is a typical corporate venture capital (CVC) firm. Originating from Eli Lilly and Company’s venture investment division in 2008, it became an independent investment management company in 2011. As one of the earliest biopharmaceutical-focused funds to deeply cultivate China’s innovation market, it has emerged as a leading life sciences and healthcare CVC in the industry and serves as a vital source of information and products for Eli Lilly and Company to sustain its innovative capabilities.

In China, corporate venture capital (CVC) investment is becoming increasingly prevalent and has begun to influence the business models of core enterprises. Unlike Lilly Asia Ventures, which operates its venture capital activities independently, leading Chinese pharmaceutical companies that represent CVC investors—such as Sinopharm, WuXi AppTec, and Tigermed—integrate CVC investments with the development of their core businesses. In recent years, some startups have also attempted to rapidly expand their business scope through selective CVC investments; examples include Medlinker’s investment in Senmei Medical and XtalPi’s incubation of Jitai Pharmaceuticals.

In August 2020, Tigermed listed on the Hong Kong Stock Exchange, achieving a dual “A+H” listing. Its H-share price rose steadily from around RMB 100 to approximately RMB 200. According to public information, Tigermed has seen two of its venture capital portfolio companies complete initial public offerings (IPOs): Tianjing Biologics, which listed in January, and Antengene Corporation, which listed in December. Their latest market capitalizations are HKD 3.9 billion and HKD 11.6 billion, respectively.

According to the prospectus dated April 2020, Tigermed has acquired minority stakes in early-stage projects through strategic investments in innovative initiatives and participation in the establishment of investment funds. To date, it has made strategic investments in 53 pharmaceutical innovation enterprises and co-established 35 investment funds with partners such as Taifu Capital.

CVC investment not only brings potential investment returns to enterprises through the commercialization of new technologies, but also enables them to establish long-term strategic relationships with investee companies, fostering closer ties in business collaborations. However, the strategy of building investment barriers through CVC has been criticized by some practitioners, who argue that it may gradually weaken the market expansion capabilities of commercial teams and lead to intensified internal competition within the industry. VCBeat has learned from industry insiders that WuXi AppTec may merge its three CVC investment funds, thereby scaling down this business segment.

2020 marked the first full year of operation for the Shanghai Stock Exchange’s STAR Market. A total of 28 healthcare-related stocks were listed during the year, the highest number among the six major capital markets. These 28 stocks collectively generated a market capitalization of RMB 628.52 billion for the STAR Market, with an average IPO market cap of RMB 22.447 billion per stock. However, by year-end, only three of these 28 stocks—Orient Gene, Yitu Technology, and Sanyou Medical—maintained their IPO-level valuations. The total market capitalization of newly listed healthcare companies on the STAR Market had shrunk to RMB 423.543 billion, representing a one-third decline, making it the only segment among the six capital markets to experience an overall decrease in market value.

Number of IPOs, Market Capitalization, and Price Gains Across Different Markets in 2020

Nevertheless, the price mechanism of the STAR Market continues to be refined. After the market close on July 22, 2020, the Shanghai Stock Exchange (SSE) and China Securities Index Co., Ltd. released historical data for the SSE Science and Technology Innovation Board 50 Index (STAR 50), with real-time quotations officially launched the following day. The STAR 50 uses December 31, 2019, as its base date, with a base value of 1,000 points. New listings become eligible for inclusion in the STAR 50 sample space six months after their listing. The initial healthcare constituents included Haier Biomedical, Borui Medicine, Chipscreen Biosciences, Hotgen Biotech, MicroPort Endovascular, Shenlian Biological Engineering, Bloomage Biotechnology, and MicroTech Medical. The SSE stated that, to adapt to the characteristics of the board’s rapid development phase and timely incorporate representative listed companies, a quarterly regular adjustment mechanism would be established.

In late December, the Shanghai Composite Index underwent its first major overhaul in 30 years. Key indices, including the CSI 300, SSE 380, CSI 500, SSE 180, and CSI 1000, adjusted their constituent stocks. Thirty-three leading high-quality companies from the STAR Market were included in these major indices. These include Haier Biomedical, Microchip Biology, Nanxin Medicine, MicroPort Endovascular, and Shenlian Biology, which had previously been added to the STAR 50 Index, as well as Haihai Bio-Science and Sinomed Medical Technology, which were newly promoted to index constituents. Inclusion in the Shanghai Composite Index signifies that, compared to the average level of the STAR Market, these companies feature larger market capitalization, higher valuations, stronger profitability, and substantial R&D investment. This serves as an endorsement in the capital markets and provides incentive for corporate management.

Companies Affected by the 2020 Adjustment of the Shanghai Composite Index

In addition, the Hong Kong Stock Exchange (HKEX) has opened its doors to new listings, injecting greater liquidity into companies that have pursued intensive IPOs in recent years. On December 25, the Shanghai Stock Exchange (SSE) and the Shenzhen Stock Exchange (SZSE) simultaneously issued the “Announcement on Adjustments to the List of Stocks Eligible for Southbound Trading via the Stock Connect.” Six Class B biopharmaceutical stocks were added to the Stock Connect list, including Peijia Medical, Akeso, and InnoCare Pharma, all of which listed in 2020. On the first trading day following the announcement, the share prices of Venus Medtech, Ascentage Pharma, Alphamab Oncology, InnoCare Pharma, and Peijia Medical rose to varying degrees. Since its initial launch in November 2014, the Stock Connect has been operational for six years, with many of the most significant rallies in Hong Kong-listed stocks commencing upon their inclusion in the Stock Connect program.

Companies Affected by the 2020 Adjustment of the Stock Connect Program for Hong Kong Shares

Since the beginning of 2021, medical innovation companies have accelerated their entry into capital markets. On January 7, Huitai Medical, the first domestically produced cardiac electrophysiology company to go public, listed on the STAR Market. Two days later, Gracell Biotechnologies, a cell therapy manufacturer, went public in the U.S. stock market. Behind them, a large number of companies have submitted listing applications, or have completed hearings and reviews, and are about to go public. As the rules for listing, delisting, pricing, and information disclosure in the capital market gradually improve, more medical innovation companies will undoubtedly come into the view of public investors.

2020 was undoubtedly a bumper year for medical IPOs. However, going public is far from the endgame. How regulators, investors, and operators can each fulfill their respective roles to turn the promising visions of many innovative healthcare enterprises into reality remains a question that warrants continuous reflection.