2020 Global Healthcare Industry Capital Report: Record-Breaking Investment Amid Pandemic-Driven Transformation

I. In 2020, global healthcare financing reached a record high, with a year-on-year increase of 41%; there were 205 financing deals exceeding $100 million throughout the year, accounting for 9% of the total. II. In 2020, China's healthcare financing also hit a record high, with a year-on-year increase of 58%.

III. Global biopharmaceutical financing topped the list, surpassing the combined total of digital health and medical devices; digital health emerged as the hottest sector abroad, while frequent financing activities occurred in the domestic medical device and consumables sectors.

IV. Neurodegenerative diseases become a focal point abroad, with financing projects concentrating on small-molecule drugs; the pandemic accelerates the maturation of “on-demand healthcare” companies

V. The Battle for Medical AI in China Reignites, with a Surge in Large-Scale Financing Deals; The Surgical Robotics Industry Booms, Promising Prospects for Domestic Substitution

VI. OrbiMed Sets Record with 50 Investments in 2020, as Top-Tier Firms Significantly Increase Deal Activity

VII. In 2020, a total of 179 companies were listed on the US, Hong Kong, and A-share markets, with 76 Chinese companies going public, setting a new historical record.

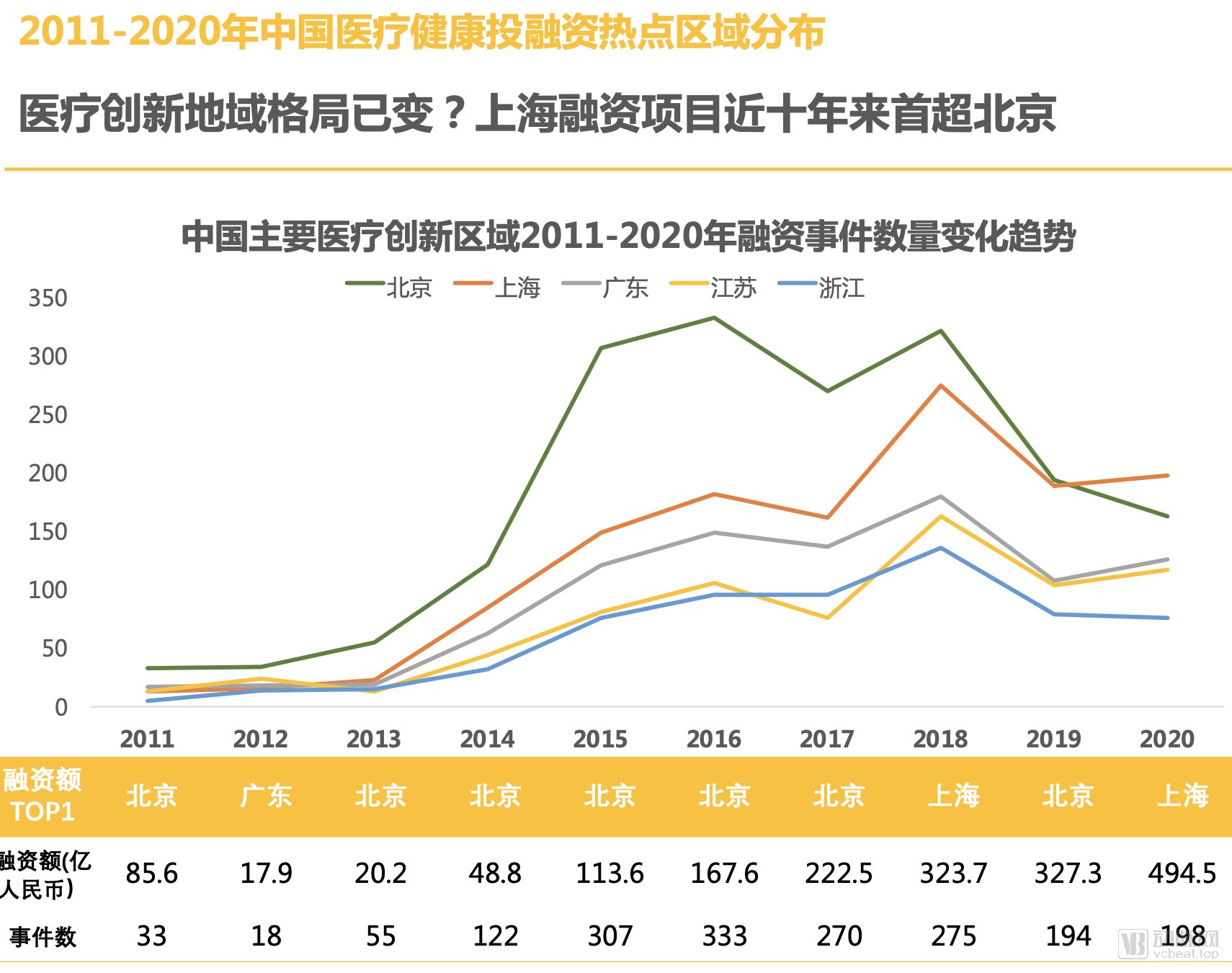

VIII. Shanghai Becomes the Top Choice for Healthcare Capital in China, with the Number of Financing Projects Surpassing Beijing for the First Time in the Past Decade

9. BGI Manufacturing Leads Globally with a Single $1 Billion Financing Round; 19 Companies Secure Funding Three or More Times Within a Year, Keya Medical Sets Historical Record with Four Rounds in One Year

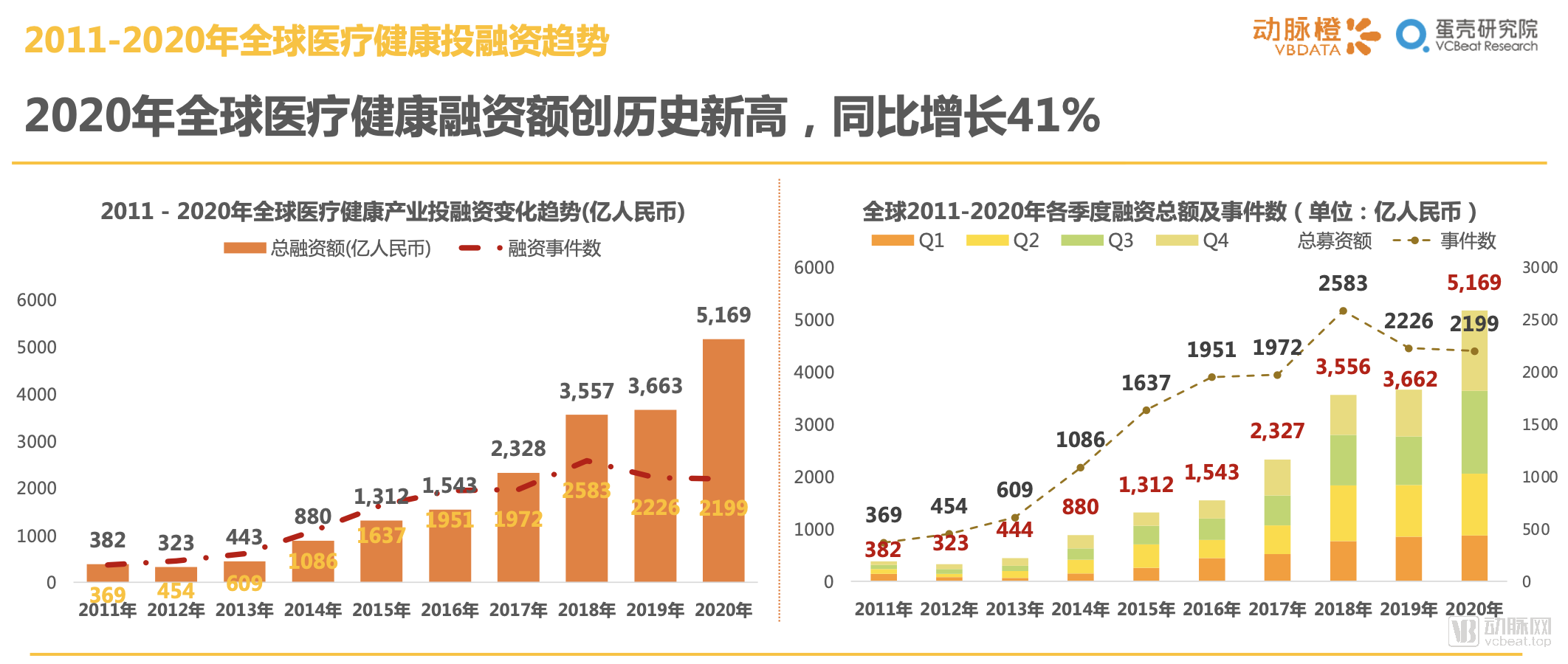

1.1 Global healthcare financing reached a record high in 2020, with a year-on-year increase of 41%

In 2020, the global healthcare industry saw a total of 2,199 financing deals, with the total funding amount reaching a record high of $74.9 billion (approximately RMB 516.93 billion), representing a year-on-year increase of about 41%. However, the number of financing deals experienced a slight decline, marking the second consecutive year of decrease since 2018. Meanwhile, in Q3 2020, a new quarterly record was set with financing totaling $22.93 billion (RMB 158.2 billion).

Taking multiple factors into account, we judge that the COVID-19 pandemic has acted as a catalyst for the influx of capital into the healthcare sector. Moreover, amid subdued global economic performance, the defensive nature of the healthcare industry has further driven capital consolidation. The substantial inflow of funds into the healthcare sector, without a corresponding increase in the number of financing deals, also indicates that investment institutions tend to favor high-quality targets with clearer business models and greater stability in a market environment characterized by heightened uncertainty.

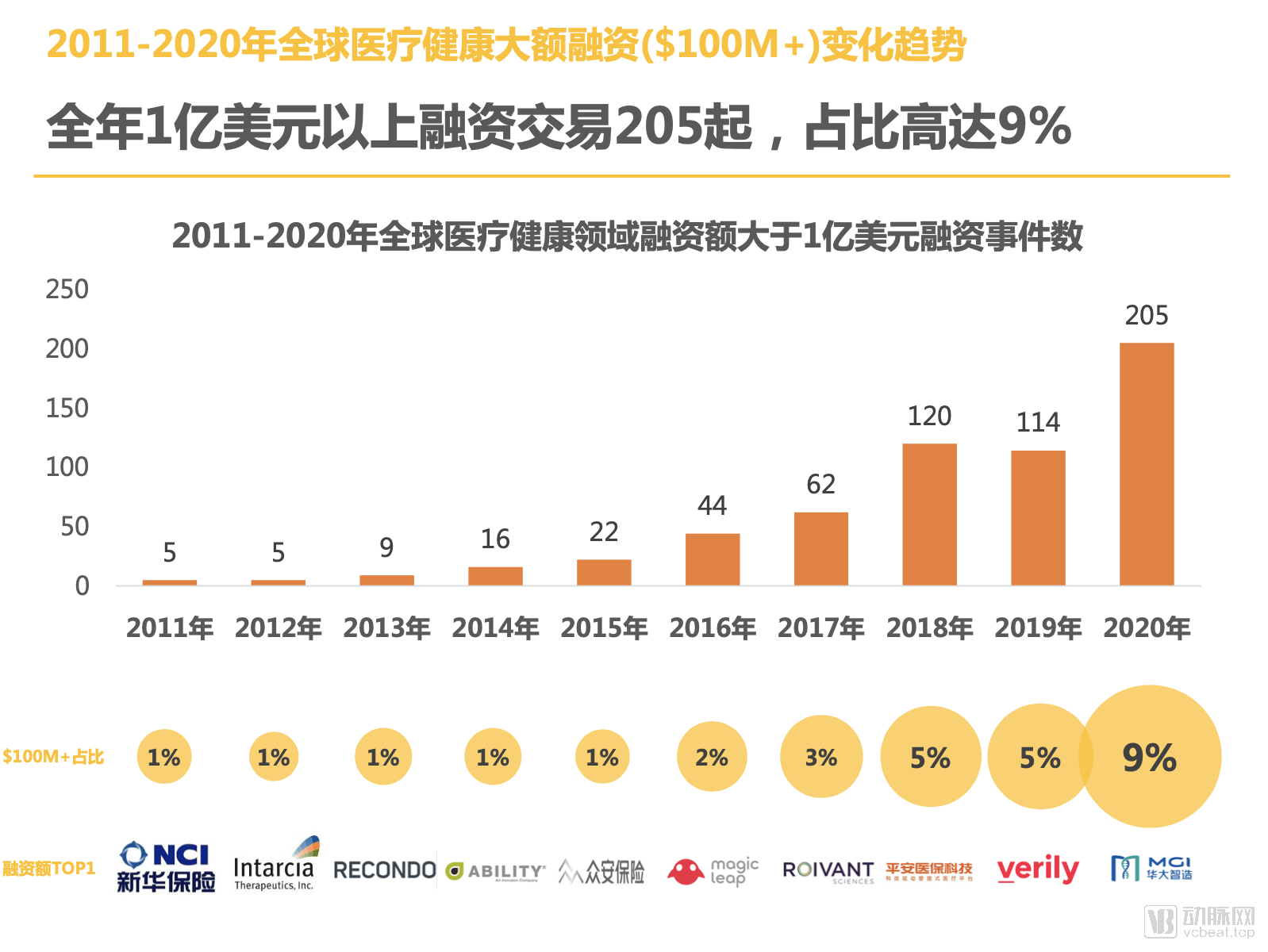

1.2 There were 205 financing transactions exceeding $100 million throughout the year, accounting for a significant 9% of the total.

In 2020, the number of individual financing rounds exceeding $100 million reached an unprecedented 205, representing a year-on-year increase of nearly 80%.

According to statistics, the total financing amount for these 205 companies reached $36.19 billion. This means that globally, nearly half of the funds invested in the healthcare industry are concentrated in less than 10% of enterprises.

Amid the shadow of the COVID-19 pandemic, global primary markets have witnessed a trend of capital consolidation, with funds flocking to leading companies, thereby further exacerbating market divergence.

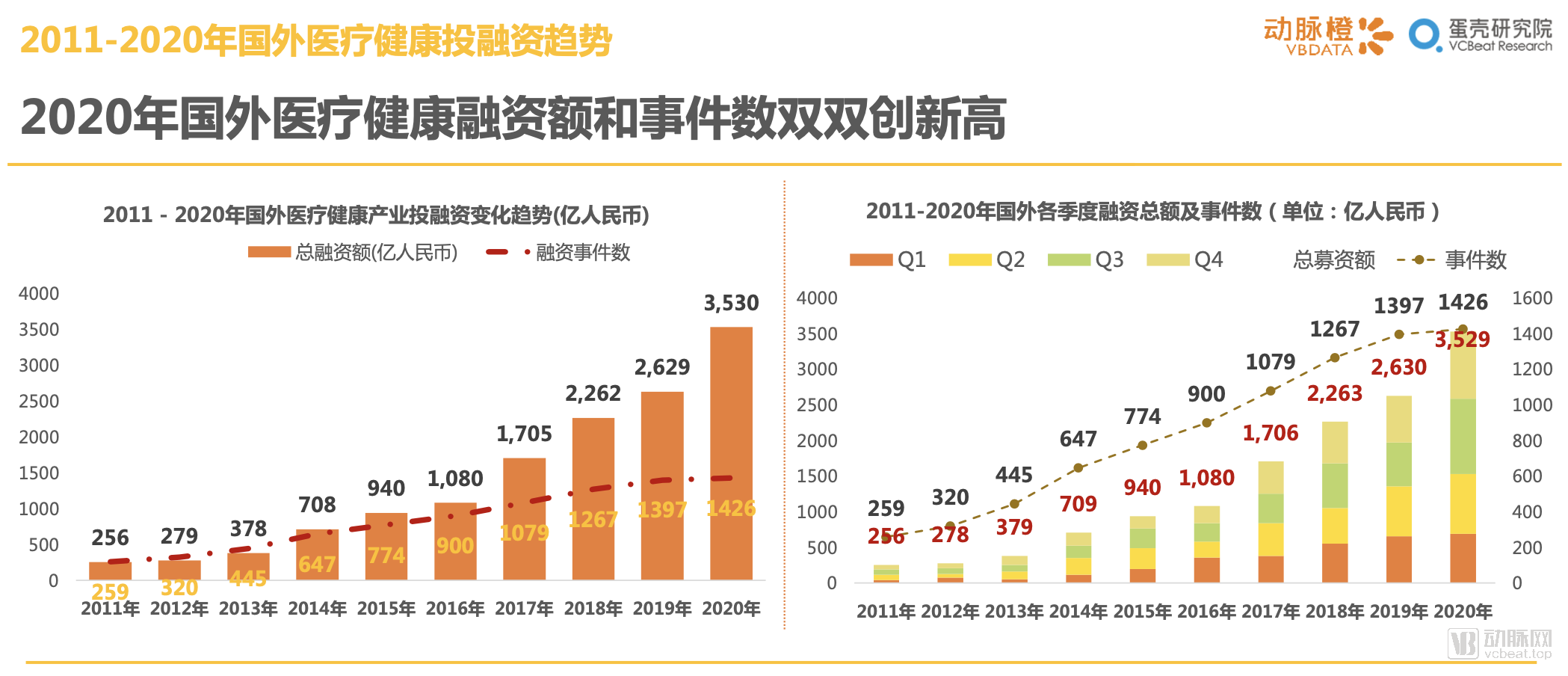

1.3 In 2020, Overseas Healthcare Financing Amount and Number of Deals Both Hit Record Highs

Abroad, the healthcare industry continued to thrive in 2020, marking its tenth consecutive year of steady growth. Although the growth rate in the number of financing deals slowed, the total financing amount reached $51.16 billion (approximately RMB 352.98 billion), representing a year-on-year increase of about 34%.

In line with global financing trends, the COVID-19 pandemic has accelerated responses to many unmet medical needs, driving increased investment in areas such as telemedicine, in vitro diagnostics (IVD), home care, and vaccine development. Coupled with the ongoing wave of global monetary easing, foreign venture capital has also significantly increased its investment in the healthcare industry.

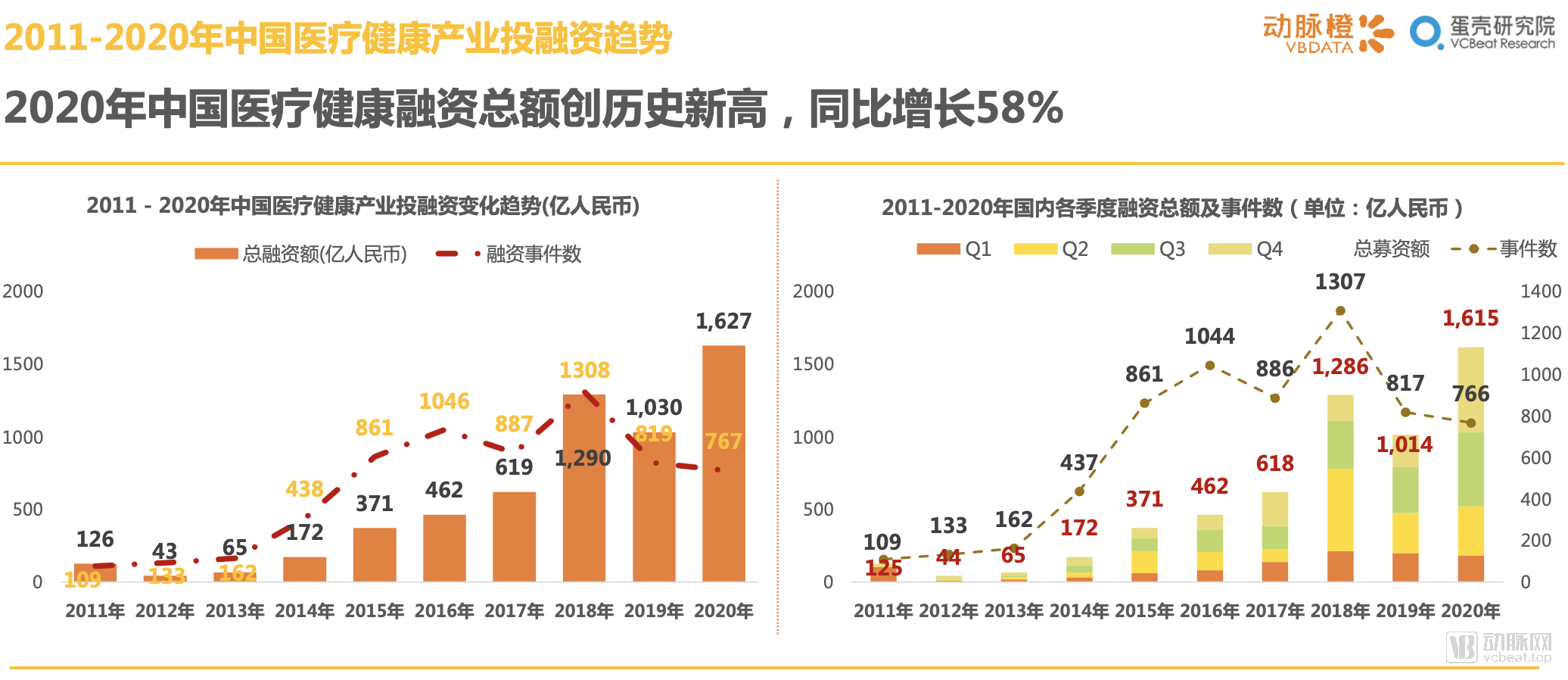

1.4 Total Healthcare Financing in China Hit a Record High in 2020, Up 58% Year-on-Year

In 2020, the total investment and financing in China's healthcare industry reached a record high of RMB 162.65 billion, a year-on-year increase of 58%; however, the number of financing transactions was only 767, a year-on-year decrease of 6%.

In the first half of 2020, the COVID-19 pandemic led to a short-term tightening of capital, causing a significant decline in healthcare financing deals in China. During H1, there were only 297 transactions, raising RMB 52 billion. In contrast, capital flowing into the healthcare sector rebounded strongly in the second half of the year, with 470 financing rounds raising over RMB 100 billion, pushing the total annual financing volume to a historic high. Meanwhile, the surge in large-scale financing deals in the fourth quarter of 2020 drove Q4’s total to RMB 58.5 billion, setting a new record for single-quarter healthcare financing in China.

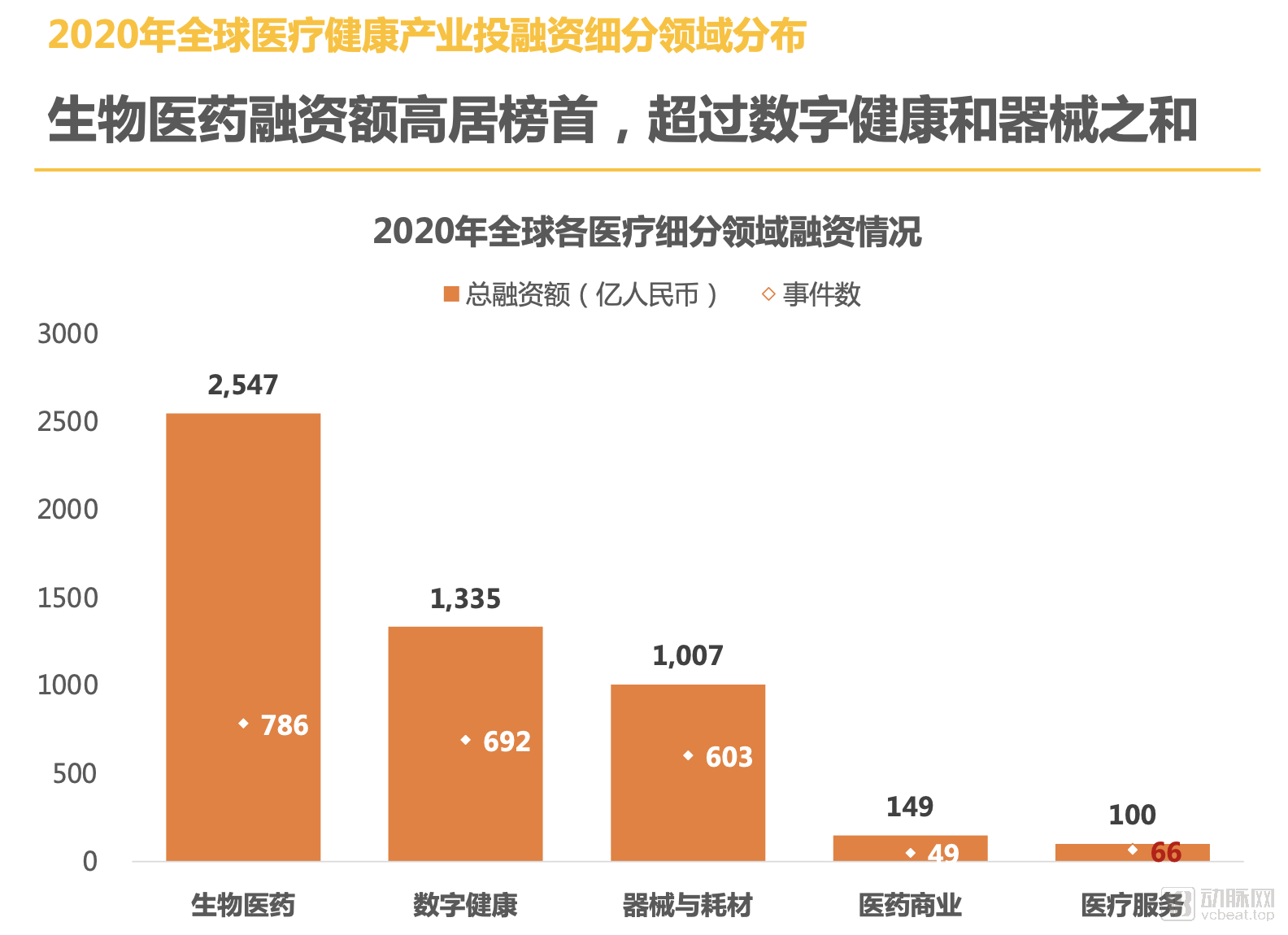

2.1 Biopharmaceutical Financing Tops the List, Surpassing the Combined Total of Digital Health and Medical Devices

In 2020, the global biopharmaceutical sector once again led all subsectors with 786 deals totaling $36.9 billion (approximately RMB 254.7 billion).

The digital health sector followed closely with 692 transactions, while medical devices and consumables ranked third.

Although the number of financing events in the biopharmaceutical sector is not significantly different from that in the other two sectors, its total financing amount exceeds the sum of the latter two. This indicates that the average financing amount for biopharmaceutical companies is far higher than that of companies in other sub-sectors.

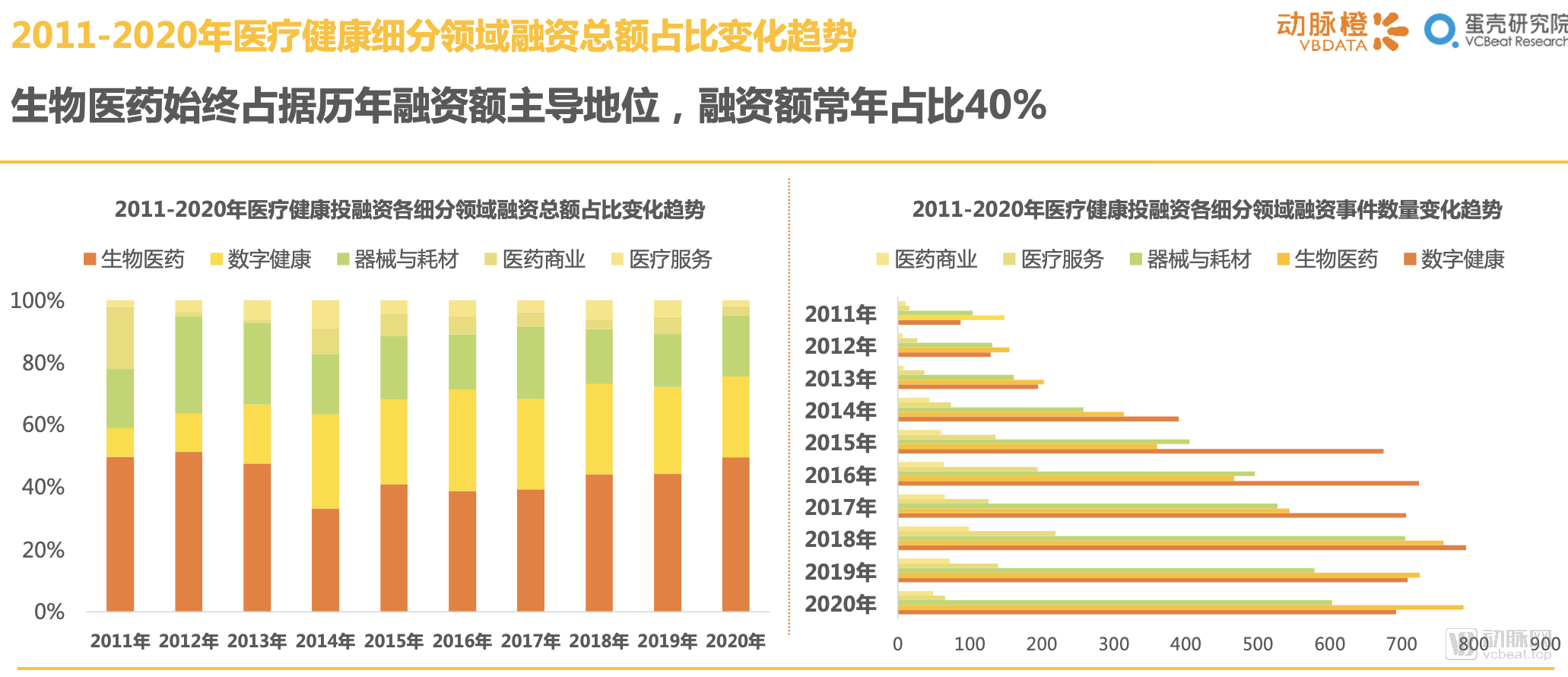

2.2 Biopharmaceuticals have consistently dominated annual financing amounts, accounting for 40% of the total year after year

In terms of the proportion of financing across the five major sub-sectors, biopharmaceuticals have consistently dominated total financing due to their large market size and high capital requirements driven by R&D investment. Their share of financing has remained above 40% for years, nearly equaling the combined total of the digital health and medical devices & consumables sectors.

In terms of the number of projects across various sectors, there is not a significant disparity in the volume of transaction events among biopharmaceuticals, digital health, and medical devices & consumables. Since 2018, the annual number of transactions in these three major sectors has consistently remained between 600 and 800.

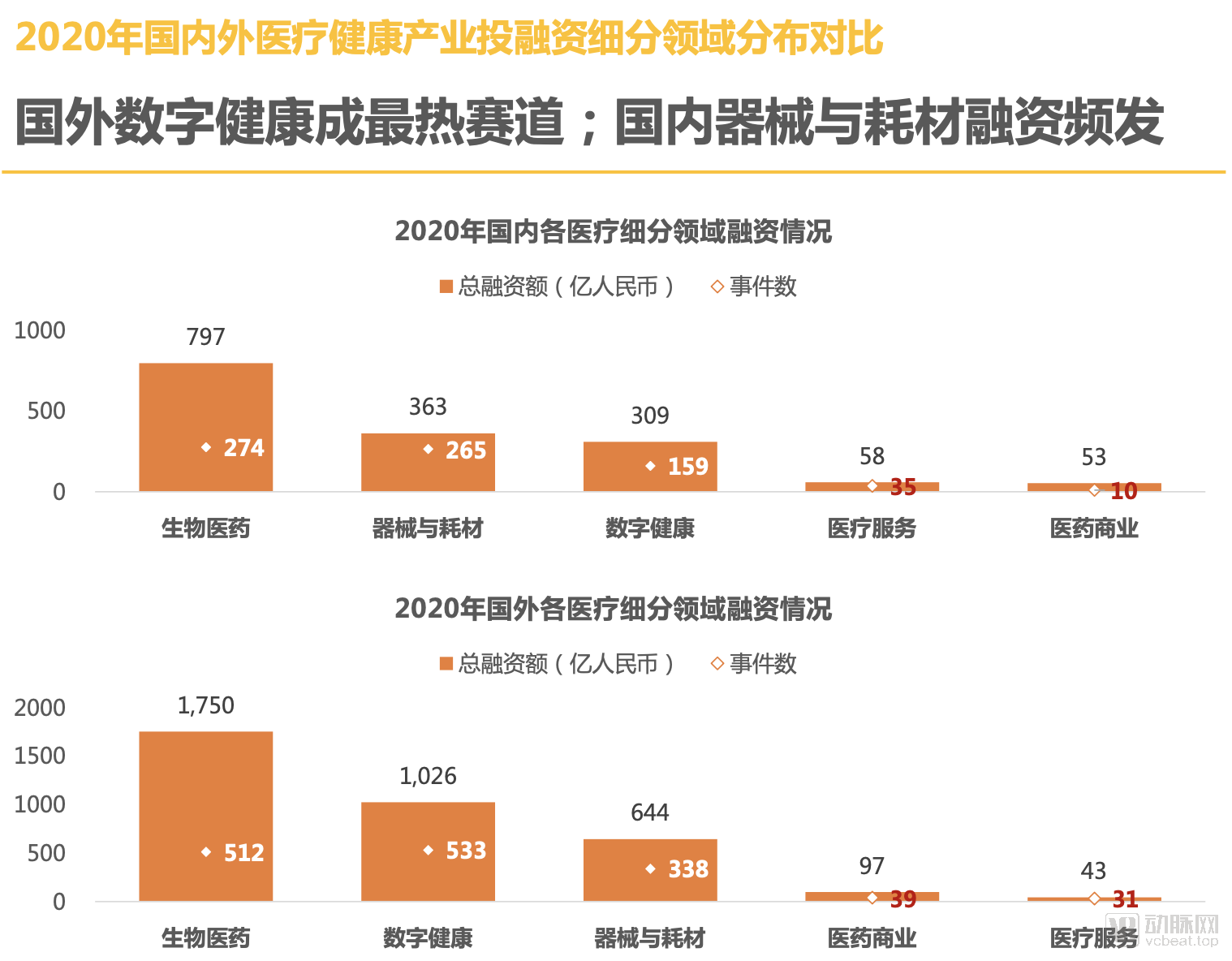

2.3 Digital Health Emerges as the Hottest Sector Abroad; Frequent Financing Rounds for Medical Devices and Consumables in China

In 2020, there was a significant divergence between domestic and international markets in terms of financing projects within niche sectors.

In China, the biopharmaceutical sector continues to lead in both transaction volume and financing amount. Abroad, digital health has emerged as the hottest track. This trend is likely driven by the persistent COVID-19 pandemic overseas, which has spurred a surge in demand for digital health-related medical services, including telemedicine, online fitness, and virtual consultations. Coupled with the strong performance of digital health companies in the secondary markets, the digital health sector has become the top choice for international capital.

Meanwhile, medical devices and consumables—sectors with lackluster performance overseas—are being heavily pursued by capital in China. The surge in interest in domestic medical devices and consumables is driven, on one hand, by the significant revenue growth in pandemic-related segments such as in vitro diagnostics; on the other hand, factors including the implementation of volume-based procurement for medical devices, lowered listing thresholds, relatively lower risk and higher certainty compared to innovative drugs, and substantial room for import substitution have collectively made the medical device sector a key target for capital allocation once again.

2.4 Trending Tags: Biopharmaceuticals, Healthcare Informatics, Internet+ Healthcare, IVD

In 2020, biopharmaceuticals, healthcare informatics, Internet Plus Healthcare, and IVD were among the most trending topics.

In terms of funding round distribution, Series A financing events occurred most frequently, totaling 601 deals. The number of Series C deals surpassed that of angel rounds, indicating that companies with relatively mature business models are more favored by capital than early-stage startups—a trend particularly pronounced in the biopharmaceutical sector.

3.1 Neurodegenerative Diseases Become a Focus Abroad, with Financing Projects Centering on Small-Molecule Drugs

In 2020, investment and financing activity in the field of neurodegenerative diseases abroad continued to rise, with 51 financing deals occurring throughout the year, totaling approximately $2.379 billion.

Companies developing treatments for neurodegenerative diseases are primarily targeting conditions such as Alzheimer’s disease, rare diseases, Parkinson’s disease, epilepsy, and pain. In terms of therapeutic approaches, small-molecule drugs have returned to the spotlight, with 17 financing rounds focused on their development, followed closely by gene therapies, which accounted for 11 financing rounds.

Drug development for neurological disorders has repeatedly encountered setbacks, resulting in a limited arsenal of therapeutic agents with suboptimal clinical efficacy and few breakthroughs in recent years. However, as industry understanding of neurological diseases becomes increasingly refined, PROTAC technology redefines small-molecule drugs, gene therapy continues to advance, and digital therapeutics emerge... with clinical trials by innovative companies progressing steadily, the challenges posed by neurodegenerative diseases are being overcome.

3.2 Surge in Capital Inflows During Pandemic Lockdowns: Overseas “On-Demand Healthcare” Companies Reach Maturity

In 2020, amid overseas pandemic lockdowns, on-demand healthcare companies—such as those in telemedicine, home care, and prescription drug delivery—experienced rapid growth, with 16 related firms securing cumulative financing exceeding $100 million.

Among on-demand healthcare companies, Amwell and GoodRx successively entered the secondary market after completing their financing in 2020, and both have successfully gone public.

The COVID-19 pandemic has ignited demand for on-demand healthcare services, driving primary-market companies toward maturity. Meanwhile, the strong performance of on-demand healthcare firms led by Teladoc in the secondary market in 2020 has bolstered confidence in the sector. It is expected that more companies in this field will complete late-stage financing rounds or even go public in 2021.

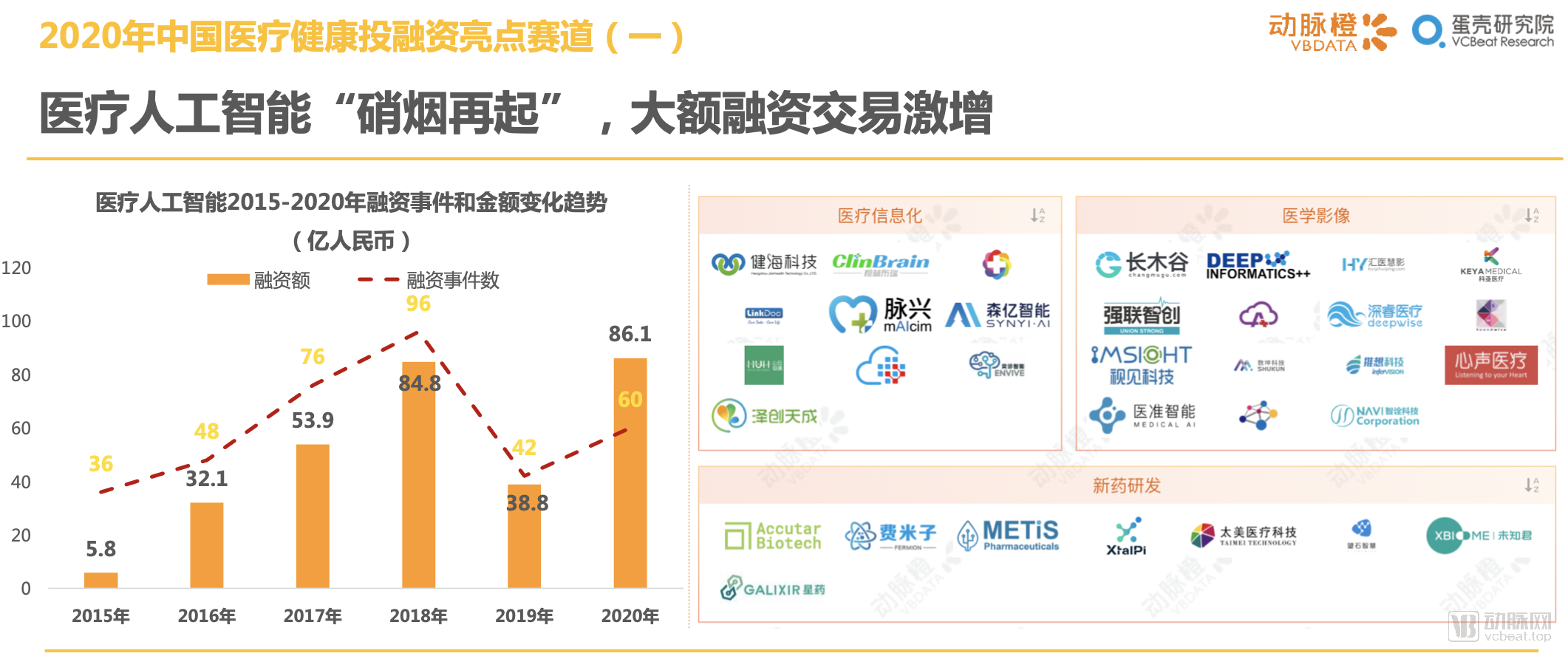

3.3 China’s Medical AI Sector Reignites, with a Surge in Large-Scale Financing Deals

After the 2018 hype, medical AI cooled in China’s primary market in 2019, with only 42 financing rounds totaling RMB 3.88 billion. In 2020, however, the sector appeared to rebound, recording 60 financing deals and a record-high total of RMB 8.6 billion.

Financing for leading enterprises played a pivotal role in the 2020 funding boom in medical AI. Key deals included LinkDoc Technology’s RMB 700 million D+ round and Taimei Medical’s RMB 1.2 billion financing in September, as well as XtalPi’s USD 318.8 million Series C round. In December, significant rounds such as Deepwise Healthcare’s multi-hundred-million-yuan C+ round, Senyi Intelligence’s RMB 350 million Series D, Shukun Technology’s RMB 500 million financing, and Keya Medical’s RMB 300 million Series D collectively accounted for a substantial share of total investment. With the completion of these later-stage financing rounds, this cohort of medical AI companies is entering a critical period focused on commercial implementation and market expansion.

3.4 Chinese AI+Medical Imaging Companies Reborn After Approval of Class III Certificates

In 2019, the AI healthcare sector entered a winter in the primary market, with only a handful of financing deals throughout the year. The main reason for the stagnation in financing was hindered commercialization.

In 2020, AI-powered medical imaging finally broke through the barriers of regulatory review and approval, with a total of nine AI products receiving Class III certification from the National Medical Products Administration (NMPA) throughout the year.

Keyo Medical, which completed four rounds of financing in 2020, was the first to break the deadlock. In addition, Shukun Technology, Deepwise Healthcare, and Infervision have all secured funding, and their respective AI products have received regulatory approval. Among AI-powered medical imaging companies, the AI healthcare market exhibits a pronounced trend of concentration among leading players. Companies that have obtained regulatory certifications enjoy smoother fundraising processes, with some even completing multiple financing rounds within a single year.

3.5 The Surgical Robotics Industry in China is Booming, with Promising Prospects for Domestic Substitution

In 2020, the Chinese medical robotics sector recorded a total of 24 financing rounds, with the total amount exceeding RMB 4.3 billion. In contrast, only 12 financing rounds occurred in 2019, raising RMB 131 million.

Tinavi Medical Technologies, the first medical robotics company to list on the STAR Market in July, was among these 24 financing deals. Jingfeng Medical, Keya Robotics, Rosenbot, and Fourier Intelligence each secured two rounds of funding consecutively in 2020. All four companies were established around 2017 and capitalized on sector-specific opportunities in 2020, thereby earning investor confidence.

Furthermore, previous medical robot financing events in China were predominantly focused on rehabilitation robots and service robots. The surge in surgical robot financing projects this quarter represents another breakthrough in the intelligence and precision of China’s medical device industry, with promising prospects for domestic substitution.

4.1 OrbiMed Sets Record with 50 Investments in 2020, as Top-Tier Firms Significantly Increase Deal Activity

In 2020, OrbiMed was the most active investor in global healthcare, making a record-breaking total of 50 investments throughout the year, primarily targeting biopharmaceutical companies.

Hillhouse Capital ranked second with 48 investments throughout the year, representing a 140% year-on-year increase. In 2020, Hillhouse Capital established Hillhouse Ventures, a dedicated vehicle for investing in early-stage startups, focusing on four key sectors including biopharmaceuticals and medical devices. With a total fund size of approximately RMB 10 billion, this move significantly heightened its focus on the primary market.

Compared with previous years, the number of investments made by top-tier institutions saw a significant increase in 2020. Even Qiming Venture Partners, ranked tenth, recorded 26 investments, surpassing the investment record set by the top-ranked institution in 2019.

Four Chinese firms—Sequoia Capital China, Hillhouse Capital (including Hillhouse Ventures), Lilly Asia Ventures, and Qiming Venture Partners—have entered the Top 10 Most Active Investors.

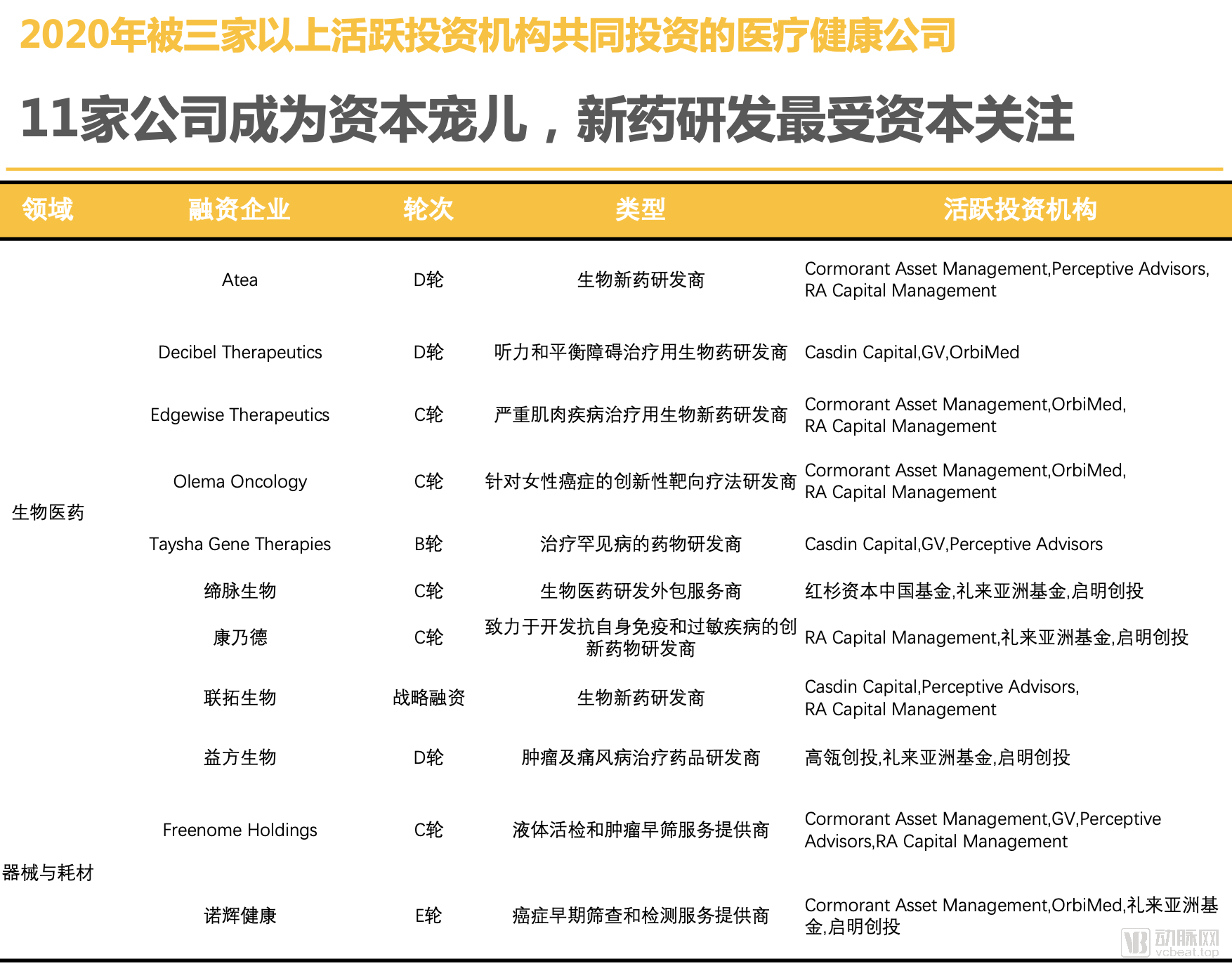

4.2 Eleven Companies Become Capital Favorites, with New Drug R&D Receiving the Most Attention from Investors

Among the top ten healthcare investment institutions by number of investments in 2020, 11 companies received backing from three or more of these firms, reflecting the potential and strength of these startups.

It can be observed that financing rounds backed by multiple active institutional investors typically occur at Series C or later, with a focus on the biopharmaceutical sector, particularly new drug development. Notably, the only two companies in the medical devices and consumables sector, Freenome and New Horizon Health, both operate in the field of early cancer screening.

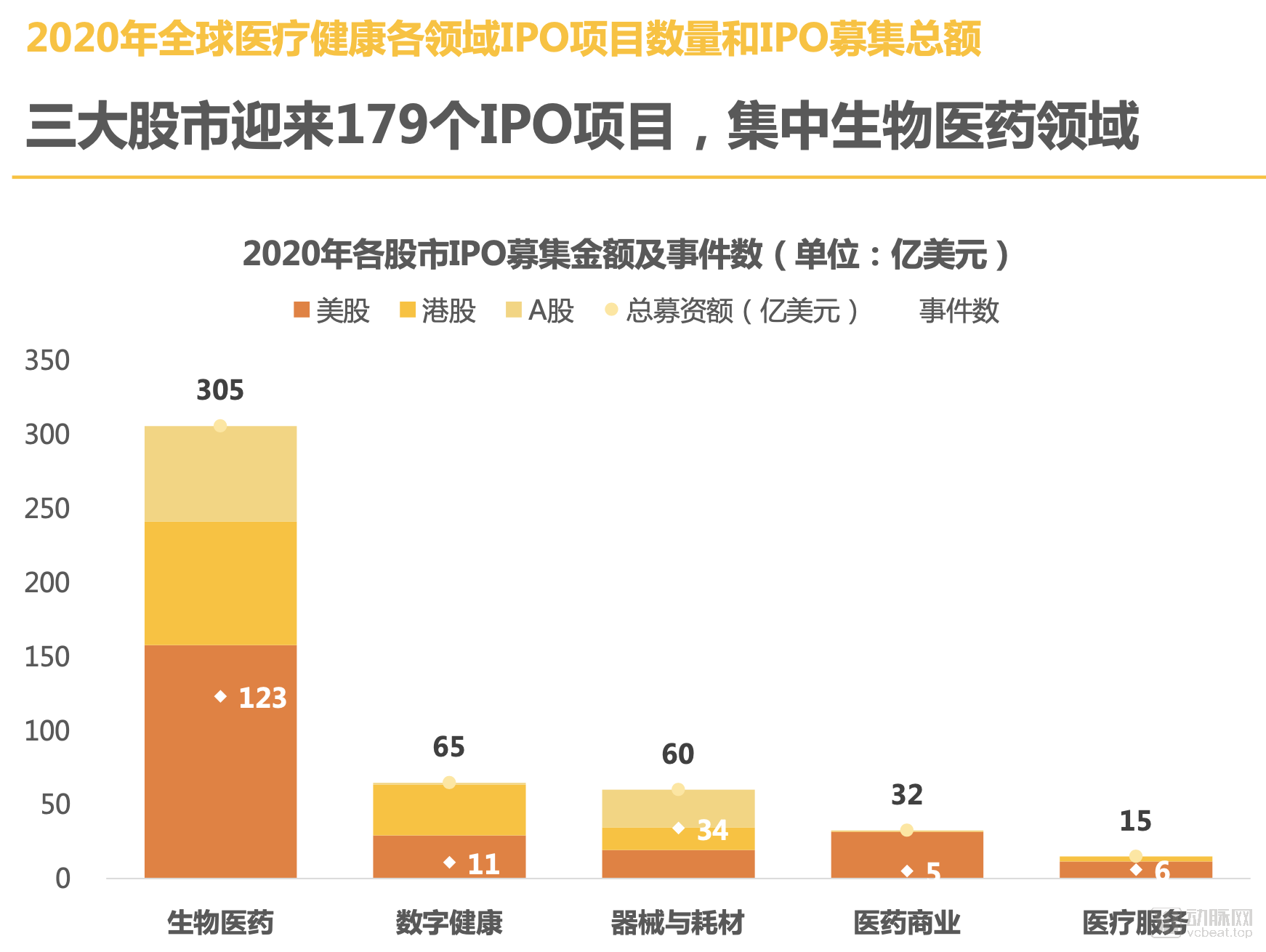

5.1 The three major stock markets welcome 179 IPO projects, concentrated in the biopharmaceutical sector

In 2020, the three major stock markets—U.S. stocks, A-shares, and Hong Kong stocks—welcomed 179 newly listed companies, a 28% year-on-year increase. Among them, 110 companies listed in the U.S. market, maintaining an absolute lead among the three markets, while 45 companies listed on the A-share market and 24 on the Hong Kong stock market.

Among the five major subsectors, biopharmaceutical IPOs led by a wide margin with 123 deals. Capital raised also remained at a high level; the medical devices and consumables sector followed closely with 34 transactions.

5.2 76 Chinese Companies Go Public, IPO Count Hits Record High

Despite the impact of the pandemic in 2020, which temporarily slowed the pace of IPO filings, enthusiasm for healthcare IPOs continued to rise as the pandemic’s effects gradually receded. In 2020, the number of healthcare IPOs in China reached 76, a record high, representing a 73% year-on-year increase.

Among the 76 Chinese healthcare companies listed on secondary markets, 45 are listed on China’s A-share market (including 36 on the STAR Market), followed by 24 on the Hong Kong Stock Exchange and 7 on U.S. stock exchanges.

The phased surge in healthcare IPOs in China can be described as the result of multiple converging factors, including new listing regulations for healthcare companies on the Hong Kong Stock Exchange, the STAR Market, and the ChiNext Board; pandemic-driven stimulus; and the substantial global liquidity injection under loose monetary policies.

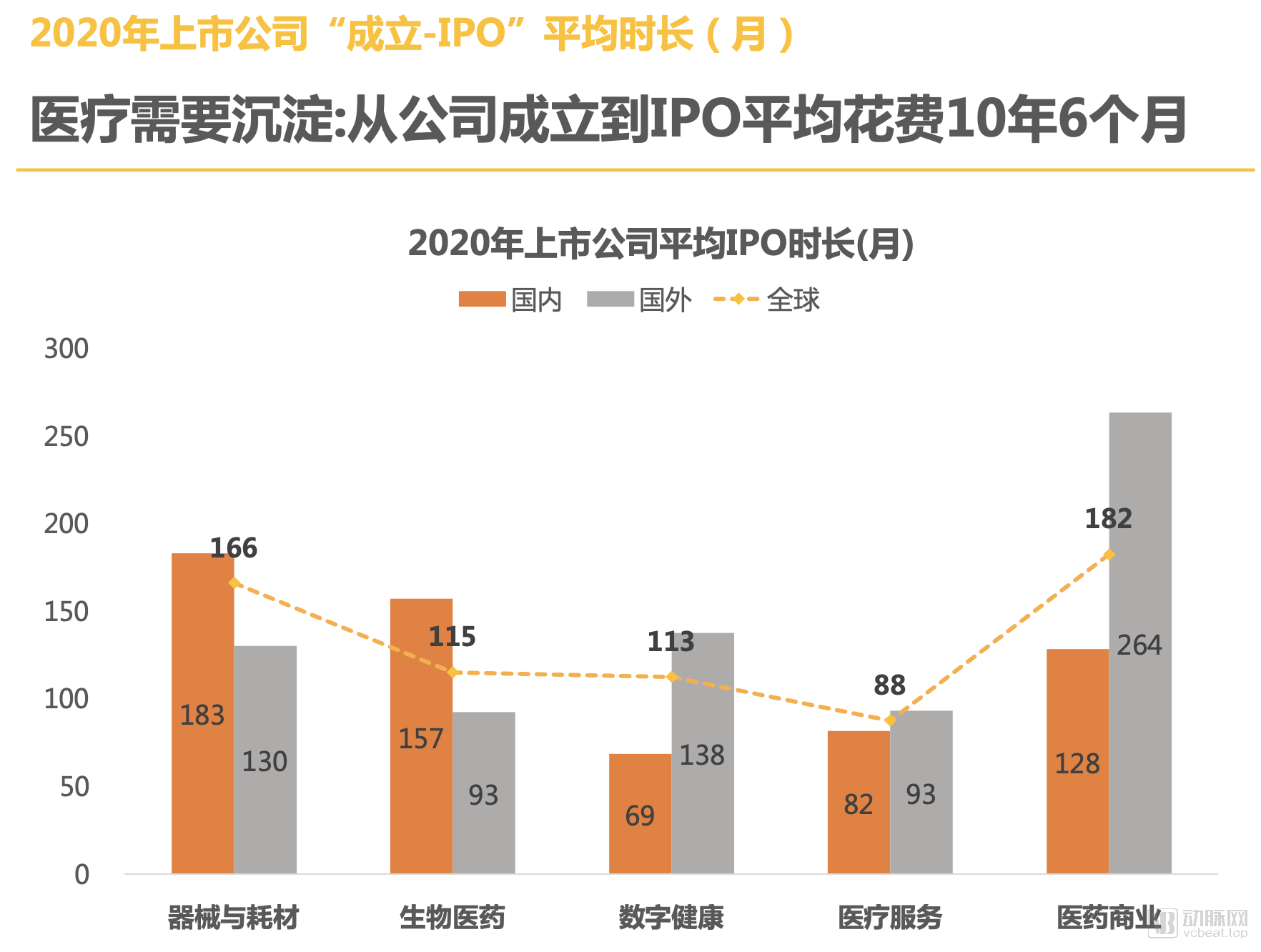

5.3 The Need for Accumulation in Healthcare: It Takes an Average of 10 Years and 6 Months from Company Founding to IPO

Among the 179 healthcare companies that went public in 2020, the average time from establishment to IPO was approximately 10 years and 6 months. Even the fastest-listing medical service companies took an average of 7 years and 4 months to go public.

A comparison of the average time to IPO for domestic and international companies reveals that Chinese firms in the medical devices, consumables, and biopharmaceutical sectors require relatively longer development periods; however, digital health companies in China demonstrate greater IPO efficiency than their foreign counterparts.

Finally, comparing the average IPO duration for healthcare companies across the three major stock markets, the U.S. and Hong Kong markets—with more lenient listing requirements—have an average listing timeline that is only half that of China’s A-share market.

6.1 U.S. Funding Leads the World, with China and the U.S. Accounting for 86% of Global Funding

In 2020, the five countries with the highest number of global healthcare financing events were the United States, China, the United Kingdom, Israel, and India.

In 2020, the United States led the world with 980 financing deals and $44.39 billion (RMB 284.17 billion) in capital raised, followed closely by China. Together, the U.S. and China accounted for 86% of the total global financing amount and 79% of all financing deals.

Meanwhile, Asia is playing an increasingly indispensable role in driving innovation within the healthcare industry. In addition to China, India also emerged in 2020 as one of the top five global hotspots for healthcare investment and financing. The widespread adoption of smartphones and the internet in India has spurred a surge in “Internet + Healthcare” innovations across the region.

6.2 Shanghai Becomes the Top Choice for Chinese Capital, with Jiangsu, Zhejiang, and Shanghai Accounting for 51% of China’s 2020 Financing Deals

In 2020, the five regions in China with the highest concentration of healthcare investment and financing activities were Shanghai, Beijing, Guangdong, Jiangsu, and Zhejiang, in descending order. Shanghai recorded a cumulative total of 198 financing deals, raising RMB 49.45 billion, nearly RMB 10 billion more than Beijing, which ranked second.

The Jiangsu-Zhejiang-Shanghai region has emerged as a cornerstone of healthcare innovation, accounting for half of China’s healthcare financing deals in 2020 with 392 transactions. Apart from Beijing, the other four top regions for healthcare financing are all located in the southern coastal areas, closely correlating with the level of economic vitality.

6.3 Has the Regional Landscape of Medical Innovation Shifted? Shanghai’s Funded Projects Surpass Beijing’s for the First Time in a Decade

An overview of the geographic distribution trends in investment and financing within the healthcare industry over the past decade reveals that Beijing has long held a dominant position as China’s primary hub for medical and health innovation. Prior to 2020, Beijing had ranked first in the number of healthcare financing deals in China for many consecutive years.

After 2017, Shanghai gained strong momentum, gradually narrowing the gap with Beijing, and in 2020 surpassed Beijing for the first time to become the most active region in China for healthcare financing transactions.

Guangdong, Jiangsu, and Zhejiang exhibit minimal disparities, with steady year-on-year development.

6.4 California Dominates, with Massachusetts and New York Emerging as Secondary Hubs

In 2020, California, USA, recorded a total of 358 financing deals, raising $20.66 billion (approximately RMB 132.25 billion), making it the most active region globally for venture capital transactions in healthcare and life sciences.

Leveraging its renowned biotechnology industry cluster and abundant medical resources, Massachusetts has surpassed the more economically developed New York State to become the second-largest U.S. state for healthcare investment and financing, although it still lags far behind California in terms of scale.

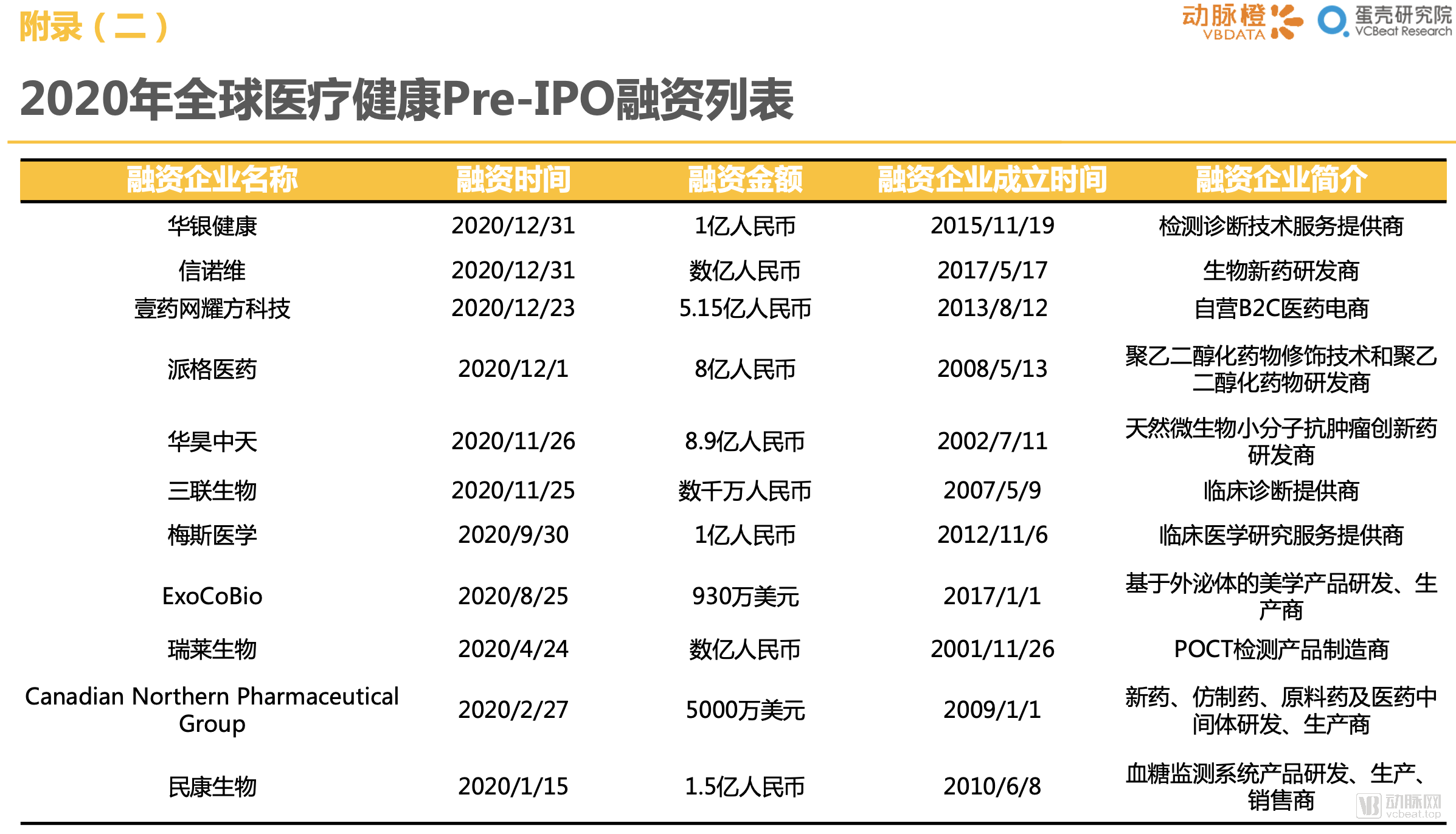

>>>>

7.1 Top 10 Most-Funded Companies in the Global Healthcare Industry

7.2 Top 10 Most-Funded Companies in China's Healthcare Industry

7.3 19 Companies Worldwide Raised Funds More Than Three Times Within One Year