Domestic Clinical Mass Spectrometry Poised for Takeoff as Players Race to Capture Market Share

By Dai Shiwen, Star VC

One winter day in 2008, I was running mass spectrometry in my laboratory at the Department of Chemistry on South Parks Road, Oxford, designing a polymer for my thesis.

Mass spectrometers are essential equipment in every chemistry laboratory, enabling the determination of the specific composition and content of unknown compounds. I was overwhelmed when faced with the latest mass spectrometry report; despite repeated synthesis experiments, the results varied significantly each time.

In the UK, winter days end early; it was only upon leaving the laboratory that I realized night had already fallen. The crisp, cold air filled my nostrils, and the streetlights of Oxford cast a dim, yellowish glow.

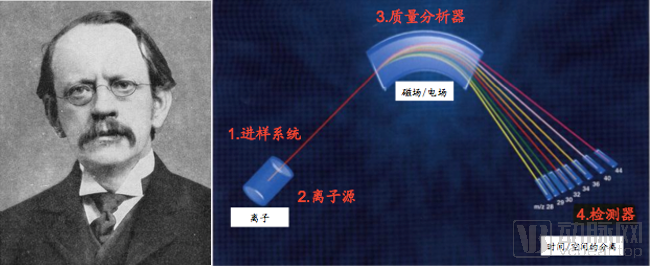

As early as 1912, British physicist J.J. Thomson discovered that the trajectory of charged ions in electromagnetic fields is related to their mass-to-charge ratio (m/z). In 1922, Francis William Aston was awarded the Nobel Prize in Chemistry for inventing the first mass spectrograph for isotopes.

Figure 1: J.J. Thomson and the Principles of Mass Spectrometry

In the following decades, with the revolution in ion source technology and mass analyzer technology, mass spectrometry instruments underwent rapid iteration and gradually became one of the most effective analytical tools in the field of life sciences.

Clinically, mass spectrometry is more sensitive and accurate than biochemical and immunological methods, holding the potential to replace many current biochemical and immunological assays. Some diseases that cannot be detected by traditional methodologies can be identified using mass spectrometry. More notably, mass spectrometry can simultaneously and precisely detect dozens or even hundreds of biomarkers in a single test. Elizabeth Holmes’ Theranos, once a celebrated startup from Silicon Valley, is now widely known as a fraud; however, in theory, the vision she proposed—detecting a wide range of diseases using only small blood samples—can indeed be realized through mass spectrometry-based methodologies.

Figure 2: Elizabeth and Her Theranos

Leveraging the distinct advantages of mass spectrometry, companies worldwide began developing and producing commercial mass spectrometers starting in the 1970s. After decades of market competition, mergers, and acquisitions, the five leading mass spectrometry manufacturers today are Shimadzu, SCIEX, Thermo Fisher Scientific, Agilent, and Waters.

Shimadzu: With a long history dating back to its founding in 1875, Shimadzu holds the most patents in the field of mass spectrometry. In 1970, Shimadzu collaborated with the Swedish company LKB to manufacture the first sector-magnet GC/MS instrument. The year 2020 marked the 50th anniversary of Shimadzu’s mass spectrometry business.

Figure 3 Genzo Shimadzu I and the First GC/MS

SCIEX: Founded in 1970, SCIEX specializes in the research, development, and manufacturing of mass spectrometry instruments and is now a part of the Danaher Corporation. In 1981, it launched the first commercial triple quadrupole mass spectrometer.

Thermo Fisher Scientific: In 1990, Thermo Electron, the predecessor of Thermo Fisher Scientific, acquired Finnigan Corporation, a leading global manufacturer of mass spectrometers, successfully entering the mass spectrometry market.

Figure 4: Chester Garfield Fisher & George Hatsopoulos

Agilent: In 1994, Hewlett-Packard launched its first inductively coupled plasma mass spectrometer (ICP-MS). In 1999, Agilent spun off from HP to focus on test and measurement components, chemical analysis, and healthcare businesses.

Waters: Founded in 1958, the U.S. scientific instrument company Waters initially focused on chromatographs. In 1997, Waters acquired Micromass, a UK-based company based in Manchester that specialized in mass spectrometers. Through close collaboration between Waters and Micromass, chromatography was integrated with mass spectrometry.

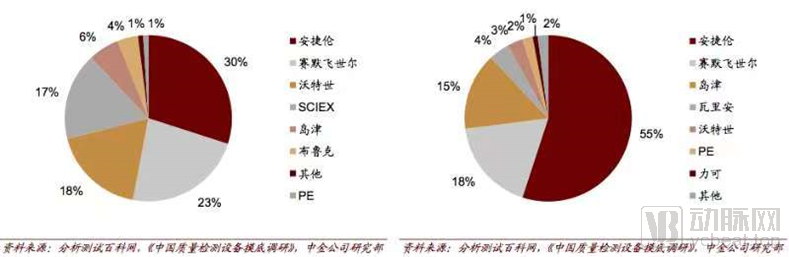

In 2016, CICC’s statistics on the sampled market share of various brands in China’s LC/MS and GC/MS markets were as follows:

Figure 5: CICC’s Sample Statistics on LC-MS and GC-MS Results in China

In contrast, China’s mass spectrometry manufacturing sector has been characterized by slow development, low technological sophistication, and a shortage of talent. As early as the 1950s, Professor Yang Chengzong’s research team, which traced its academic lineage to Marie Curie, successfully developed China’s first magnetic-sector mass spectrometer. However, due to various historical reasons, the research, development, and production of mass spectrometers in China were discontinued, which is highly regrettable. It was not until after 2000 that China gradually began to accumulate expertise in mass spectrometry technology. In 2006, Beijing East-West Analytical Instruments Co., Ltd. launched the GCMS-3100 quadrupole gas chromatography-mass spectrometry (GC-MS) system, marking the first commercially available mass spectrometry product in China.

Figure 6: Yang Chengzong’s research group, Marie Curie, and the model of China’s first mass spectrometer

China’s IVD industry has long followed the development logic of import substitution. Overseas giants first cultivated usage habits through academic and marketing investments, while domestic companies initially entered the market as distributors and service providers. They typically began by manufacturing reagents in-house, expanded into OEM equipment, and then further broke through technical barriers to independently develop and produce instruments, thereby gradually achieving domestic substitution. This pattern holds true for mature IVD sub-sectors such as clinical chemistry and immunoassay.

Currently, over 50% of clinical biochemistry products in China have been replaced by domestically produced alternatives, giving rise to several listed companies such as Kehua Bio-engineering and Medconn Biotech. Immunoassay technology has a higher barrier to entry than biochemical analysis and started later in China. Currently, enzyme-linked immunosorbent assay (ELISA) has achieved 70% import substitution, while the market share of domestic chemiluminescence immunoassay is approximately 20%. Mindray Medical, Autobio Diagnostics, and Maccura Biotechnology are leaders in this niche sector.

With the advancement of precision medicine and breakthroughs in multi-omics, clinical sequencing and mass spectrometry have ushered in new opportunities.

Sequencing, pioneered by NIPT’s inclusion in clinical guidelines, has driven the rapid development of NGS and subsequently expanded into oncology, metagenomics, and early screening. However, due to persistent technical barriers in sequencer development, most Chinese companies have been confined to operating as third-party service providers. In 2014, MGI Tech’s BGISEQ-1000 received certification from the CFDA, and MGI Tech now has four sequencer models approved. The stability of domestically produced instruments is gradually improving, and it is believed that the monopoly held by overseas manufacturers in the sequencer market will soon change.

Looking at the development of mass spectrometry in China, we see a different landscape. As early as 2015, voices within the industry predicted that mass spectrometry would be the next gene sequencing. Five years later, while mass spectrometry is already thriving in the United States, it has made little impact in clinical practice in China. What are the reasons for this?

Some attribute it to the high cost of mass spectrometers, while others point to their operational complexity. Yet the da Vinci Surgical System, which costs tens of millions of yuan per unit and is both expensive and difficult to operate, has achieved strong sales in China through Fosun Intuitive.In the author’s view, the slow development of mass spectrometry in China is still attributable to the differing “soils” between China and the United States.

In the United States, large general hospitals account for only 14% of medical institutions, with the remainder consisting of community hospitals and private clinics operated by non-governmental entities or the government. Within this healthcare landscape, policy incentives have encouraged cost reduction and containment of total healthcare expenditures, resulting in 64% of medical tests being conducted outside hospital settings. Of these out-of-hospital tests, 54% are outsourced to Independent Clinical Laboratories (ICLs), driving the overall ICL market size to $31.4 billion. The ICL market is highly concentrated, with LabCorp and Quest Diagnostics as the two dominant players, jointly holding over 50% of the market share.

Figure 7: LabCorp & Quest

Mass spectrometers are expensive. Taking an instrument priced at approximately RMB 2 million as an example, assuming a five-year depreciation period and a charge of RMB 100 per test, the minimum annual sample volume required would be 3,000. This naturally deters private clinics and community hospitals. However, Independent Clinical Laboratories (ICLs) can make mass spectrometry testing feasible by collecting samples and operating equipment at scale, thereby alleviating the pressure of procurement costs. Furthermore, ICLs in the United States can independently develop Laboratory Developed Tests (LDTs) without FDA approval, needing only to comply with LDT regulatory requirements. This has further accelerated the clinical adoption of mass spectrometry technology. In this favorable environment, clinical mass spectrometry has rapidly developed in the U.S., with mass spectrometry currently accounting for 15% of tests in the American medical laboratory market.

Due to a combination of factors, including the political system and cultural traditions, China’s healthcare service landscape is dominated by large public tertiary hospitals (Grade 3, Class A). Although the national government has been continuously promoting tiered diagnosis and treatment, the extreme imbalance in supply has not only prevented these major tertiary hospitals from downsizing but has also led to an intensified siphoning effect in the short term.

Under this landscape, the domestic clinical testing market is still dominated by the laboratory departments of public hospitals, with third-party providers such as KingMed Diagnostics and Dian Diagnostics playing a supplementary role (third-party providers account for approximately 5% of China’s medical testing market). The relatively fragmented and independent nature of the public hospital market gives rise to the following issues:

●Access to the Fee Schedule: Public hospitals must conduct laboratory tests and employ methodologies in accordance with the “National Medical Service Price Item Specifications” periodically issued by the Ministry of Health. The approval of new laboratory tests and their inclusion in the billing code system are subject to varying regional policies and procedures. Currently, mass spectrometry is not included in the national catalog; apart from its application in microbial identification, other applications cannot be widely implemented, which severely restricts its development.

●Reagent Registration and Market Access: Unlike the LDT model employed by third-party laboratories, hospital clinical laboratories most commonly adopt the IVD model for mass spectrometry projects, which requires the procurement of registered reagent products. However, the domestic market is currently dominated by Class I reagents. This is primarily because clinical mass spectrometry, as an emerging medical device, is not yet fully supported by current registration regulations in leveraging its advantages. Industry pioneers are still exploring appropriate pathways for the registration of mass spectrometry-specific reagent products.

●Methodological Standardization: Currently, most detection methods are laboratory-developed tests (LDTs). Different biological samples require mass spectrometers of varying brands and models, necessitating optimization of corresponding methodological parameters and conditions. There are significant disparities among different detection methods in terms of the number of analytes measured per test, precision, and turnaround time; however, there are currently no industry standards for evaluating the quality of these methods. Different detection methods also pose challenges for internal quality control, and inter-laboratory quality assessment for mass spectrometry-based methods has not yet been fully implemented.

●Insufficient Laboratory Conditions: Mass spectrometry equipment has stringent requirements for temperature and humidity during operation, and the volatile organic solvents used in the analysis process may pose health risks to personnel. Therefore, laboratories must be equipped with exhaust ventilation systems as well as temperature and humidity control systems. Currently, mass spectrometers are generally large in size, require gas supply lines (such as nitrogen), and need to be paired with uninterruptible power supplies (UPS), resulting in significant floor space requirements. As conditions vary across hospital clinical laboratories, the barrier to entry is relatively high.

●Talent Shortage: Currently, mass spectrometers require relatively complex procedures such as sample pretreatment and manual injection, imposing significantly higher demands on laboratory technicians than existing conventional equipment. In addition to professionals proficient in both clinical practice and mass spectrometry testing, there is an urgent need for personnel skilled in equipment maintenance and laboratory management.

The vastly different “soil” for survival has posed significant challenges to China’s clinical mass spectrometry industry.

Between 2004 and 2020, dozens of innovative clinical mass spectrometry companies emerged in China. From the perspective of the industry chain, they can be broadly categorized into two groups: upstream instrument/reagent manufacturers and midstream third-party medical laboratories.

Third-party medical laboratories: KingMed, Dian Diagnostics, Beijing Hehe, etc.

Upstream Instrument Manufacturers: In China’s clinical practice, two types of mass spectrometers are commonly used: MALDI-TOF, which focuses on microbial detection, and LC/MS, which is primarily used for detecting small-molecule metabolites. Chinese manufacturers were the first to achieve breakthroughs in MALDI technology. Currently, a number of domestic companies, including Yixin Bochuang, Xiamen Mass Spectrometry, Rongzhi Biology, and Hexin Instruments, have obtained CFDA approvals for their instruments, reflecting a relatively lower barrier to entry. LC/MS accounts for the vast majority of the clinical mass spectrometry market and represents the segment with the broadest market prospects; however, it entails a higher technical threshold. At present, some domestic manufacturers are actively strategizing and collaborating with major overseas companies to promote the localization of mass spectrometry instruments, achieving certain results. For instance, Pingsheng Medical’s miniaturized clinical-grade mass spectrometry detection system, Qlife Lab 9000, received approval this year. Similar to the chemiluminescence sector, whether domestically produced mass spectrometers can successfully replace imported ones remains to be tested by the market.

Upstream Reagent Manufacturers: Major foreign mass spectrometry instrument manufacturers are primarily scientific instrument companies and do not offer original manufacturer-supported IVD reagents in China. Consequently, no IVD giants such as Roche or Abbott have emerged in the clinical mass spectrometry field, creating opportunities for domestic clinical mass spectrometry companies. A number of reagent manufacturers have already appeared in China; however, due to the lack of industry standards, their quality varies significantly. Some manufacturers with robust technologies that have successfully implemented mass spectrometry testing projects in hospital laboratories have gained recognition from benchmark hospitals, with their products included in hospital procurement lists. For example, Pingsheng Medical’s test kits have been added to the procurement lists of West China Hospital and Zhongshan Hospital Fudan University. Manufacturers that effectively resolve the compatibility issues between instruments and reagents will hold a competitive advantage.

Over the past 16 years, China’s “soil” has also undergone a transformation from quantitative to qualitative change:

● Industry StandardsDr. Wang Chengbin, Director of the Clinical Laboratory Center at the Chinese PLA General Hospital, is known for his witty and humorous demeanor. As the then-Chairman of the Laboratory Medicine Branch of the Chinese Medical Association, he has been a pioneering figure in promoting the clinical application of mass spectrometry in China. In October 2017, Dr. Wang led a team of experts in drafting and publishing the “Recommendations for the Clinical Application of Liquid Chromatography-Mass Spectrometry,” providing standardized guidelines for clinical use and facilitating the gradual improvement of industry norms. Professor Fu Weiling from the First Affiliated Hospital of Army Medical University, who served as the then-Vice Chairman of the Laboratory Medicine Branch of the Chinese Medical Association and Chairman of the Laboratory Medicine Committee of the Military Medical Science Committee, also collaborated with industry experts to actively advance the standardization, normalization, and industrialization of clinical mass spectrometry through academic societies, associations, and industry alliances.

● Popularization of Technology: There is a growing number of third-party laboratories equipped with mass spectrometry testing platforms, expanding in both scale and the range of services offered. A cohort of third-party laboratories specializing in clinical mass spectrometry has emerged, positioning themselves at the forefront of technological and application innovation. Most benchmark hospitals in China have already implemented mass spectrometry programs. Leading institutions such as the Chinese PLA General Hospital, Zhongshan Hospital Fudan University, and West China Hospital of Sichuan University boast mass spectrometry platforms that are domestically leading in terms of technical proficiency, instrument scale, and the variety of tests performed. These benchmark hospitals play a significant demonstrative role, driving the adoption of mass spectrometry testing in a large number of tertiary and secondary hospitals. Whether through establishing in-house mass spectrometry platforms or outsourcing samples for testing, the penetration of clinical mass spectrometry projects in end-user hospitals is increasing. It is reported that in certain provinces, the presence of a mass spectrometry platform has become a plus factor in the accreditation of tertiary hospitals, reflecting a strong demand for broader technological adoption.

● Development of the Industrial Chain: Across the instrument, reagent, and service sectors, a cohort of enterprises has emerged, dedicated to driving innovation and development within the industry. The introduction of domestically produced mass spectrometry instruments has created a significant price advantage over imported brands, lowering entry barriers; furthermore, as the level of localization continues to rise, instrument costs are expected to decline further. Mass spectrometry reagent kits have evolved from non-existence to widespread availability, with the number of approved kits rapidly increasing, thereby reducing the complexity of clinical operations. The clinical application of mass spectrometry has developed rapidly, expanding from initial uses in newborn screening and vitamin analysis to numerous other fields, including hormone profiling, amino acid analysis, fatty acid analysis, and therapeutic drug monitoring. The number of detectable items has grown to hundreds and continues to increase.

● Technical Staff Training: In recent years, an increasing number of clinical mass spectrometry sub-forums have emerged at major industry conferences on clinical laboratory testing and in vitro diagnostic (IVD) medical devices. Various collaborations among industry, academia, and research institutions are actively promoting the training of mass spectrometry professionals. Benchmark hospitals such as Zhongshan Hospital Affiliated to Fudan University and West China Hospital of Sichuan University have conducted multiple rounds of training courses on clinical mass spectrometry technologies. In 2017, KingMed Diagnostics participated as the lead editor in the publication of the first domestic textbook titled Clinical Chromatography and Mass Spectrometry Laboratory Techniques for higher education institutions in China, and practical training programs on the clinical application of mass spectrometry technologies have been launched across various regions.

Faced with the various challenges of implementing clinical mass spectrometry in China, each company has adopted its own unique strategy: some are heavily investing in hardware and pursuing automation, others are focusing on reagent R&D and manufacturing along the IVD (In Vitro Diagnostics) pathway, some are offering third-party testing services, and others are actively establishing co-built laboratories with hospitals. Whether these directions are correct remains uncertain for many at present. However, in ten years’ time, the widespread adoption of clinical mass spectrometry will likely be taken for granted, and it will undoubtedly play a pivotal role in medical laboratory testing.

Currently, domestic mass spectrometry players are racing to secure their footholds in hospitals. With its large market size, substantial potential, and rapid growth, China’s clinical testing market is riding the wave of this technological transformation in laboratory medicine. Clinical mass spectrometry is finally emerging into the spotlight, with leading players poised to rise to prominence in 2021.Compared with other segments of the traditional in vitro diagnostics (IVD) industry, the core of competition in the mass spectrometry sector lies in the clinical implementation of technology platforms and products. Currently, no more than three companies in China truly meet this standard.

Amid intensifying competition, companies that can offer diversified product portfolios and service solutions to meet the personalized needs of end-user hospitals, and that have passed the scrutiny of benchmark hospitals through robust technology and comprehensive services—thereby enabling mass spectrometers to operate effectively within clinical laboratories—will gain a competitive edge. Furthermore, as the future trend in IVD shifts toward multi-omics, only enterprises capable of mastering precise operational data, leveraging advanced analytics, and continuously developing innovative products will be able to “befriend time” and emerge as the ultimate winners.

After more than a century, mass spectrometry remains a young technological platform. Future mass spectrometers will see further functional upgrades in ion sources and detectors, while operational workflows will evolve toward automated assembly lines, similar to those in biochemistry and immunology. Meanwhile, major manufacturers are also developing miniaturized, simplified, and intelligent products.

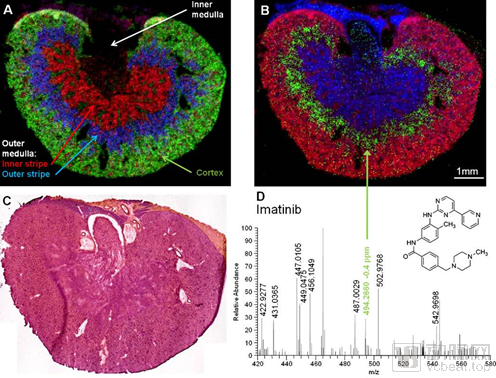

In terms of applications, mass spectrometry (MS) can not only replace traditional biochemical and immunoassay tests but also leverage its advantages in multi-omics testing. By integrating data analysis, a range of innovative diagnostic applications will be developed. Mass spectrometry imaging (MSI) is likely to become an exciting clinical focus in the future, where cellular images can be represented by ion intensity signals from MS, enabling intuitive and clear comparisons between cells from patients and healthy individuals.

Figure 8: Distribution map of histological features in mouse kidney tissue obtained by mass spectrometry imaging technology