The Collapse of Haven: Why America's Healthcare System Couldn't Be Fixed by Amazon, JPMorgan, and Berkshire Hathaway

Haven Healthcare

Healthcare Company

On the morning of January 30, 2018, stock prices in the U.S. healthcare sector plummeted, with market capitalization rapidly evaporating by nearly $10 billion. Among them, CVS Health, a giant in the U.S. chain pharmacy industry, fell by 5.5%, while UnitedHealth Group, the largest health insurance company in the United States, dropped by 4.2%.

A significant shift in stock price is invariably driven by a major event, and this “trigger” stemmed from the establishment of a company, which was founded byHaven, the health insurance company jointly established by the three giants Amazon, JPMorgan Chase, and Berkshire Hathaway。

Data source: Hurun Global 500; chart by VCBeat

The reason Haven’s establishment shook the entire stock market is that it was born with a “silver spoon.” Amazon is the largest e-commerce company in the United States, ranking third on the 2020 Hurun Global 500 List; Berkshire Hathaway is an insurance company founded by “Oracle of Omaha” Warren Buffett, ranking eighth on the 2020 Hurun Global 500 List; JPMorgan Chase is a leader among U.S. commercial banks, with total assets reaching $2.5 trillion, ranking fifteenth on the 2020 Hurun Global 500 List.

With such powerful “backing,” the emergence of Haven has also given hope to Americans plagued by high insurance costs, and it was once regarded as the “golden straw” for saving the U.S. healthcare system.

Three years have passed, yet reality has not unfolded as people had hoped. On January 5, 2021, U.S. media outlet Insurance Journal reported that Haven would officially cease operations at the end of February 2021.

The announcement sent shockwaves around the globe, as many found it hard to believe that this giant vessel, backed by the “Big Three” and carrying the American dream of health insurance, had ultimately “sunk.” Was this due to poor corporate management, or does the U.S. healthcare system prove truly unbreakable? Benchmarking against the Chinese market, what lessons can be drawn from Haven’s “disappointment”?

Warren Buffett has publicly criticized the exorbitant cost of healthcare in the United States, explicitly stating that the rising cost of health insurance is like a ravenous tapeworm, devouring the U.S. economy.

This is by no means alarmist.According to data from the U.S. National Bureau of Statistics, in 2019, U.S. healthcare spending approached $3.6 trillion—five times its military expenditure—accounting for 18% of its Gross Domestic Product (GDP). This figure even exceeded the GDPs of developed economies such as the United Kingdom, France, and Russia.

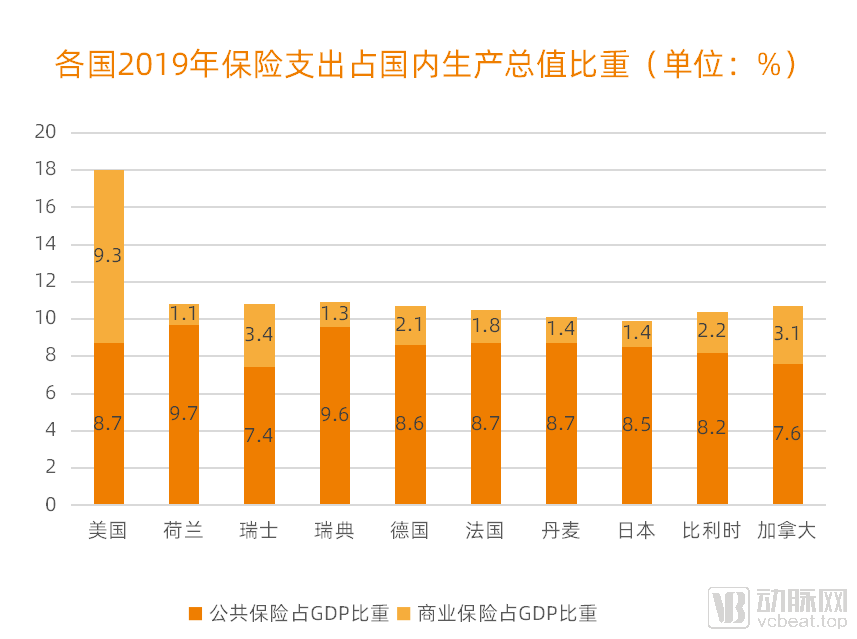

Data source: OECD Health; chart by VCBeat

However, the primary factor contributing to this situation is the commercial health insurance that Americans both “love” and “hate.” According to data from the Kaiser Family Foundation, in 2019, U.S. public health insurance expenditure accounted for 8.7% of the national GDP, a figure not significantly different from that of other countries,What truly creates the disparity is commercial health insurance expenditure, which accounts for as high as 9.3%, far exceeding that of other countries.

Why Do Americans Have a Love-Hate Relationship with Private Health Insurance, and What Drives Its Exorbitant Costs? A Glimpse into the U.S. Insurance System Offers Some Insights.

The United States is one of the few countries that does not implement a “universal healthcare system.” While the public has considerable choice in purchasing insurance, this seemingly free right is rendered less than pure by exorbitant medical costs. According to the Los Angeles Times,The United States is the country with the highest healthcare costs in the world,If individuals do not purchase any health insurance, their medical expenses will be as much as five times those of insured individuals, making insurance particularly important for the vast majority of Americans.

U.S. health insurance is divided into public health insurance and commercial health insurance. Public health insurance primarily targets elderly individuals, people with disabilities, low-income populations, and other special groups who hold U.S. citizenship; these programs are generally supported by federal and state governments. In contrast, commercial health insurance involves contracts between individuals or institutions and insurance companies.

Public health insurance primarily includes Medicare, Medicaid, and the Children’s Health Insurance Program (CHIP). Different types of insurance systems offer varying service models and cover different populations.

Due to the "exorbitantly high threshold" of public medical insurance,Insurance coverage rate stands at only 16.3%., which has also led to a highly developed commercial insurance market in the United States.According to statistics, more than 80% of Americans have purchased various types of private health insurance products. Among these commercial health insurance plans, 90% are provided by employers for their employees, with only a small fraction being purchased individually.

To date, the U.S. government has not enacted any policies mandating employers to provide health insurance for their employees. However, under pressure from American labor unions, it has become a social consensus for companies to offer health insurance not only to their employees but also to their spouses and children.

Source: U.S. Census Bureau; Graphic by VCBeat

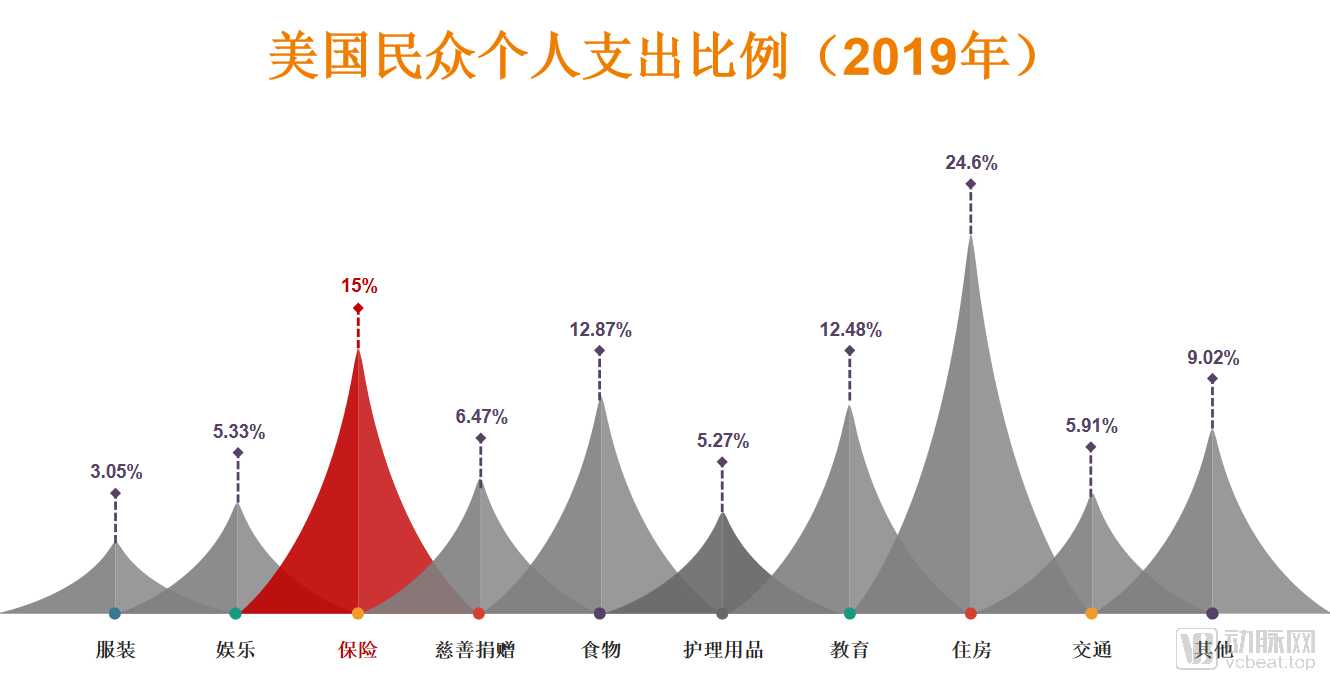

Data shows that the average annual premium for individual health insurance in the United States is $20,000, with employers covering 70% of this cost and individuals responsible for the remaining 30%. Such a straightforward statement may not fully convey the magnitude of these expenses; therefore, it is helpful to compare this figure with another key statistic. According to information released by the U.S. Census Bureau in mid-September 2020,In the United States, the average annual per capita income in 2019 was approximately $39,000, with insurance expenditures accounting for as much as 15% of personal income.

Consequently, for any enterprise, insurance expenditures constitute a heavy burden and are often the “fatal factor” leading many businesses to bankruptcy.

Public data indicate that Amazon, Berkshire Hathaway, and JPMorgan Chase collectively employ nearly one million people in the United States. Specifically, Berkshire Hathaway employs over 360,000 individuals, Amazon more than 300,000, and JPMorgan Chase upwards of 240,000. Annually, these companies spend over $4 billion on employee health insurance premiums.

Facing immense pressure from insurance payments, the three companies have been cautiously venturing into the healthcare sector in recent years, eager to escape their precarious situation as soon as possible. It is precisely for this reason that they jointly established Haven.

At the inception of Haven, Warren Buffett, the “Oracle of Omaha,” issued a statement saying, “We believe that by pooling our resources and entrusting them to some of the best talent in the country, we can curb the rise in healthcare costs in a timely manner, while improving patient satisfaction and health outcomes.”

Amazon founder Jeff Bezos shared the same view, stating, “It was clear from the outset that achieving our desired goals would be challenging, but the effort was worthwhile.” JPMorgan Chase CEO Jamie Dimon added, “Each of our three companies possesses extraordinary resources, and our aim is to develop healthcare solutions that benefit American employees and their families, and potentially all Americans.”

Image source: Haven official website

Headquartered in Boston, Massachusetts, Haven is a nonprofit healthcare company dedicated to providing low-cost, high-quality medical services to the nearly one million employees of its three founding shareholders, while also offering more accessible primary care, easier-to-understand insurance benefits, and more affordable prescription drugs.

Haven was jointly managed by three companies, with its core staff comprising elites selected from these three organizations. In June 2018, the company finally welcomed its first leader since its inception—Atul Gawande.

Atul Gawande is an American surgeon and a professor of surgery at Harvard University’s School of Public Health and Medical School. He authored influential books on the U.S. healthcare industry and contributed to The New Yorker. Regrettably, he announced his resignation in May 2019 due to excessive commute times, leaving the position of CEO vacant ever since.

In October 2019, Haven launched its first operational initiative, “Amazon Care,” a virtual primary care service designed to improve care and reduce healthcare costs for employees with chronic conditions.

In November 2019, Haven announced a partnership with Cigna and Aetna (a subsidiary of CVS Health) to provide health plans for 30,000 JPMorgan Chase employees in Arizona and Ohio. The operational model involved the technical team analyzing data on performance, cost, and other factors to establish a curated network of physicians. Building trust with employees, the initiative then guided them toward appropriate care options based on their individual conditions, such as urgent care clinics, medical specialists, or telemedicine appointments.

Since then, Haven had not issued any further announcements. It was not until January 5, 2021, that news of “Haven’s announcement to dissolve by the end of February 2021” rapidly spread worldwide. Haven once again garnered the level of attention it had received at its inception; however, unlike the anticipation and excitement of that earlier period, the public response this time was characterized predominantly by disappointment and regret.

Haven’s “strong start but weak finish” is inevitably lamentable, yet every event has its underlying causes. For a well-backed and highly anticipated innovative enterprise, what exactly was the final “straw” that broke its back?

Identifying internal causes first is the most critical step in discerning the essence of a matter. Based on Haven Healthcare’s specific circumstances, VCBeat has outlined the following key points.

1Highly Overlapping Businesses: The “Big Three” Operate Independently

Take Amazon as an example. Since 2019, the tech giant has proactively positioned itself in the healthcare sector by launching Amazon Pharmacy, which provides prescription drug delivery services across 48 U.S. states. It also offers its employees access to telemedicine and primary care providers, as well as wearable devices capable of tracking health metrics. Berkshire Hathaway, led by Warren Buffett, has also been actively seeking promising investment opportunities in the healthcare industry. Regulatory filings reveal that in the third quarter of last year, the company took new stakes in Merck & Co. and Pfizer, while increasing its holdings in AbbVie and Bristol Myers Squibb. JPMorgan Chase, the most influential commercial bank in the United States, has likewise remained active, leveraging its keen business acumen to make multiple investments in the healthcare sector.

As can be seen,The three major shareholders each have their own plans and projects for entering the healthcare sector. As a joint venture, Haven’s development strategies often conflict with or are heavily duplicated by those of its parent companies., ultimately leading to an operational shutdown.

2The goals are overly idealistic and lack practical implementation.

At its inception, Haven’s corporate vision was to create healthcare solutions that would benefit American employees and their families, and potentially all Americans. However, beyond the clear objective of reducing healthcare costs, Haven did not define a specific focus area, resulting in a lack of core strategic anchor across its business segments.

On the other hand, Haven over the past three yearsBusiness progress is sluggish, and the company's mission has not been truly realized.Present. Bloomberg reported that since its inception, Haven has not proposed any solutions capable of substantially addressing healthcare costs or methods that could potentially improve medical care.

3Fragmented workforce, insufficient overall market power

Despite the three companies employing nearly one million staff,Haven still lacks sufficient market power to secure lower prices from suppliers.. The primary reason is that the U.S. healthcare system is deeply entrenched; suppliers will not make any concessions on pricing unless employer groups hold a significant share in the local market. As for Haven Healthcare, although it serves a large population, its employees are dispersed across the country, resulting in weak leverage in each region and an inability to dominate any single market.

Beyond internal factors, the external environment also appears to be working against this emerging enterprise.

1“The Medicine-Insurance” System Is Hard to Break

Controlling drug prices is a crucial component in reducing healthcare costs and a key factor behind the success of many commercial insurance companies, yet it is far from easy to implement in practice. It is reported that numerous U.S. pharmaceutical companies have long monopolized the pharmaceutical market by leveraging an unconstrained domestic drug pricing and patent system, selling medications at high prices. To consolidate their position, these companies allocate a portion of their profits to government lobbying efforts aimed at blocking the passage of new laws unfavorable to the pharmaceutical industry. Furthermore,Healthcare institutions, pharmaceutical and medical device companies, and health insurance providers have also formed an “iron triangle,” engaging in both competition and cooperation while jointly exerting pressure on the government and parliament.

2# Improper Incentives Still Exist in the Healthcare Industry

Although the healthcare industry is striving to transition toward a “low-cost, high-efficiency” operational model, the sector as a whole remains largelySign a Reimbursement Agreement for Paid Services, since payers and providers have reaped substantial profits through the fee-for-service system, few are willing to adopt these new and risky payment models.

3“The COVID-19 Pandemic” Shifts Public Attention, Insurance Falls Out of Favor

According to data from the World Health Organization, as of January 17, 2021, the cumulative number of confirmed COVID-19 cases in the United States exceeded 24.3 million, with active cases reaching as high as 9.56 million. The pandemic has become a focal point of concern for the American public. Consequently, healthcare providers have had to devote all their resources to managing the crisis. Due to the postponement or cancellation of elective and non-urgent procedures, healthcare providers have suffered significant financial setbacks. Therefore,They will not consider new ideas until the crisis subsides, and even then, they are unlikely to entertain taking on new risks.

Healthcare reform has never been an easy endeavor. For Haven, internal challenges such as unclear business objectives, internal competition, and ineffective leadership were already present. Externally, in a country like the United States, where the healthcare system is deeply entrenched, the path to reform is inevitably fraught with obstacles. Compounded by the immense pressure of the COVID-19 pandemic, which further shifted focus toward clinical care, it became even more difficult for healthcare companies to make meaningful progress during this period.

Image source: Haven official website

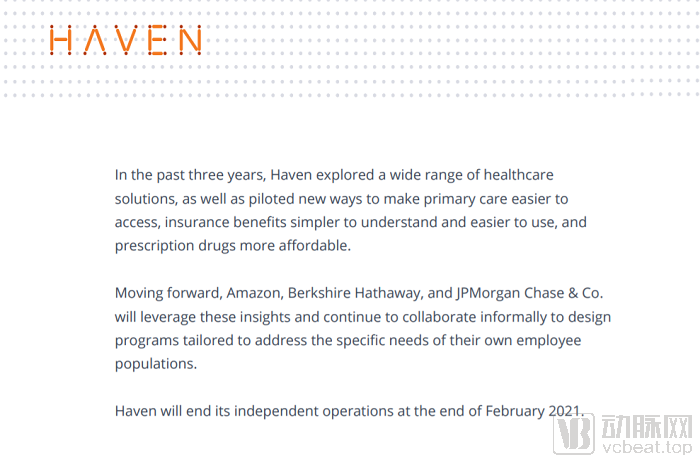

Visit the Haven Healthcare website, and all you can see now is this statement:“Over the past three years, Haven has explored a broad range of healthcare solutions and piloted new approaches to provide users with more accessible primary care services, easier-to-understand insurance benefits, and more affordable prescription drugs. Looking ahead, Amazon, Berkshire Hathaway, and JPMorgan Chase will leverage these insights to continue their informal collaboration, designing programs that meet the specific needs of their employee populations.”

Clearly, Haven, the “experimental plot” jointly created by the three giants, has failed to “bear fruit” in the healthcare sector. However, this does not mean that companies will abandon their exploration of the insurance field; on the contrary, it was a valuable attempt that has laid a solid foundation for identifying future breakthroughs in the U.S. insurance system.

There are significant differences between the insurance systems in China and the United States. The failure of Haven Healthcare has had little substantive impact on China’s domestic health insurance market, and we have not identified any directly comparable domestic enterprises. Nevertheless, we can draw valuable lessons from its experience, offering important insights for China’s insurance industry, which is currently undergoing reform, thereby accelerating its development and delivering high-quality medical insurance services to a broad customer base.

Health is an enduring topic. As human society continues to advance, health has garnered increasing public attention. In light of this, people have placed higher demands on the insurance industry. For insurance companies, these heightened expectations represent both opportunities and challenges. The ability to meet current and long-term needs will determine the future development prospects of medical insurance enterprises.