Digital Solutions for National Health Insurance, Long-term and Short-term Health Insurance: A Prospectus

Since the State Council issued the Decision on Establishing a Basic Medical Insurance System for Urban Employees in December 1998, national medical insurance has become the primary reliance for the majority of citizens in healthcare over the past two decades. “Relying on medical insurance for medical care” has become a widespread consensus among the public, leading to the formation of a healthcare payment system in China centered on national medical insurance.

However, in recent years, this long-established pattern has gradually begun to change.

In 2016, the Ministry of Human Resources and Social Security stated in an official announcement that, against the backdrop of rapidly rising medical costs, the basic medical insurance fund, like the pension fund, was facing increasing pressure, with expenditure growth outpacing revenue growth. A significant number of provinces even experienced current-period deficits, making the risk of fund insolvency increasingly prominent.

Thus, in recent years, centered on the core issue of basic medical insurance fund deficits, the state and commercial insurance institutions have jointly driven the transformation of China’s insurance payment system.

At the national level, first establishing the National Healthcare Security Administration at the end of 2018, and subsequently rolling out a series of measures related to healthcare cost containment; meanwhile, multiple policies have been actively encouraging the rapid development of commercial health insurance.

Commercial Health InsuranceIn addition to long-term health insurance, represented by critical illness insurance, various short-term health insurance products tailored to the needs of different demographics and payment scenarios—such as high-limit medical insurance, specific drug insurance, short-term critical illness insurance, and inclusive supplementary medical insurance (Huiminbao)—have successively led several waves of development in the commercial health insurance sector.

As a result, medical insurance has evolved from a system solely reliant on national basic medical insurance into a comprehensive payment solution centered on national basic medical insurance and supplemented by commercial health insurance.

Thus, as we re-examine the current landscape of health insurance, we find that at this stage of development, different product types are facing distinct challenges.

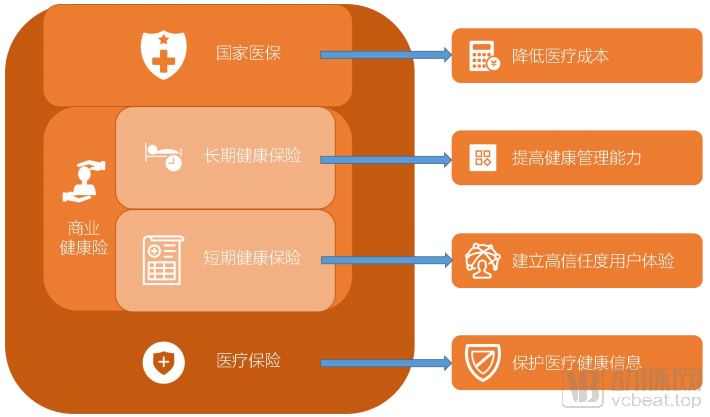

National Medical Insurance — Reducing Healthcare Costs: The national medical insurance system faces virtually no challenges in terms of coverage scope, financial capacity, or public trust. The only issue confronting it is the cost of healthcare. As reflected by the frequent initiatives undertaken by the National Healthcare Security Administration in recent years, there is an urgent need to further control medical costs within its covered benefits. This is essential to continue providing affordable and high-quality healthcare coverage to the population without raising contribution rates.

Long-Term Health Insurance: Enhancing Health Management Capabilities: The long-term health insurance sector, typified by critical illness insurance, has undergone years of development and accumulated a strong reputation among users. Building on this foundation, the future development of long-term health insurance should shift its focus from customer acquisition to health management for insured individuals. This transition aims to further enhance the user experience, reduce claim frequency, and ultimately achieve cost control.

Short-Term Health Insurance: Building a High-Trust User Experience: As an emerging product, the immediate priority for short-term health insurance is to enhance user trust. New offerings inevitably face ongoing external scrutiny regarding their credibility. Factors such as the reasonableness of claims processing procedures and the smoothness of user communication significantly influence the word-of-mouth reputation of short-term health insurance.

Health Insurance — Protecting Health and Medical Information: Safeguarding medical and health information is a critical concern for all health insurance providers, including national basic medical insurance and commercial health insurers. Particularly as cloud migration becomes the prevailing trend in the healthcare industry, insurance companies holding vast amounts of user data may soon become the next target of cyberattacks by malicious actors.

As digitalization becomes the bellwether of the healthcare industry, awareness of digital transformation within the insurance sector is gradually awakening, drawing it into this sweeping transformation encompassing the entire healthcare landscape. This report will dissect four key scenarios while discussing the roles and impacts of digital technologies in each specific context, aiming to offer potential directions for the future of this digital transformation journey.

Regarding payment issues, there is a high degree of alignment among national basic medical insurance, commercial health insurance, and insured individuals. Both insurers and policyholders seek to access more affordable, accessible, and higher-quality healthcare services.

In terms of controlling healthcare costs, commercial health insurance has limited bargaining power due to its current small scale, resulting in relatively fewer actions taken. In contrast, the national basic medical insurance system has been actively implementing various measures in recent years to curb healthcare expenditures.

In China, the medical insurance system is centered on the national basic medical insurance. Over the past two decades, only a handful of commercial health insurance products have achieved success. According to the 2019 Statistical Bulletin on the Development of National Medical Security released in 2020, approximately 1.35 billion people were enrolled in the national basic medical insurance scheme in 2019, with an enrollment rate consistently exceeding 95%.

With its extensive coverage and strong payment capacity, the National Medical Insurance has become virtually the cornerstone of healthcare financing for Chinese citizens since its inception. Consequently, when it comes to pricing decisions for products from medical institutions and pharmaceutical and medical device companies, the National Medical Insurance is nearly the sole stakeholder with significant influence.

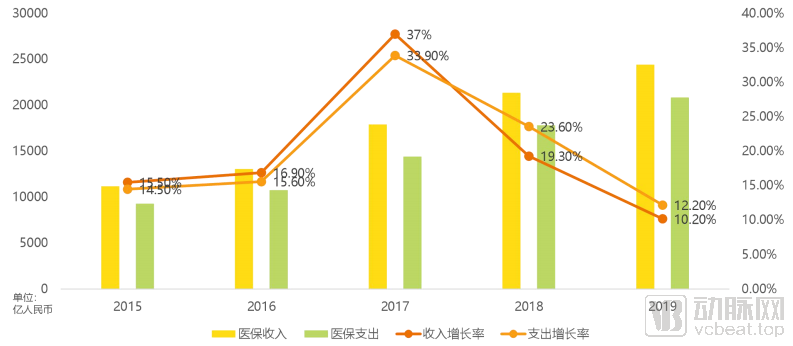

In recent years, as the aging population has continued to increase, the pressure on medical insurance has gradually risen. According to data from the Medical Insurance Statistical Bulletin, although current medical insurance revenue still significantly exceeds expenditures, the growth rate of revenue was lower than that of expenditures for two consecutive years from 2018 to 2019. If this trend continues, medical insurance may no longer be able to maintain a balance between income and expenditure in a few years.

Therefore, since the establishment of the National Healthcare Security Administration (NHSA) in late 2018, a series of measures related to healthcare cost containment have been implemented. It is fair to say that the NHSA’s initiatives in recent years have primarily focused on controlling medical costs. By addressing both pharmaceutical/medical device products and medical services, the NHSA has reduced the prices of high-cost innovative drugs through reimbursement negotiations; gradually controlled the prices of generic drugs and certain high-value consumables through volume-based procurement (VBP); and regulated the pricing of medical services through DRG/DIP payment reforms.

In the process of controlling healthcare insurance costs, the integration of big data and artificial intelligence technologies has provided novel solutions. This is particularly evident in the concrete implementation of the DRG/DIP payment system.

First, DRG payment requires adjustments to the specific disease groupings based on local conditions, and the payment standards must be determined according to local disease diagnosis and treatment practices. By leveraging big data analytics on local healthcare data, DRG payment standards can be established in a more scientific manner.

SecondFollowing the implementation of DRG-based payment, hospitals must also make data-driven decisions leveraging their own big data. Through intelligent analytics, they can monitor physicians’ medication and prescribing practices. Meanwhile, by adopting refined operational management and centralizing hospital-wide data, they can achieve rapid and convenient data collection and analysis, objectively analyze the structure and costs of various disease categories, optimize clinical pathways, and reduce hospital costs.

Third, the implementation of DRG has also created new application scenarios for artificial intelligence technology. For instance, in data collection, AI assists medical records departments in performing quality control on medical records completed by physicians, thereby preventing issues such as difficult case grouping, incorrect grouping, or failure to group due to human factors.

Overall, artificial intelligence and big data technologies have played a significant supporting role in the implementation of DRG/DIP payment systems, whether by assisting health insurance authorities in formulating payment strategies or by helping hospitals improve management efficiency. As the rollout of DRG/DIP payment reforms continues to advance, their application value will be further demonstrated.

From the perspective of basic commercial health insurance classification, health insurance can be divided into long-term health insurance and short-term health insurance based on the policy term. According to the explicit provisions in the "Administrative Measures for Health Insurance" updated in December 2019, long-term health insurance refers to health insurance with a policy period exceeding one year, or with a policy period of one year or less but containing guaranteed renewal clauses; short-term health insurance refers to health insurance with a policy period of one year or less and not containing guaranteed renewal clauses.

Due to differences in policy duration and renewal requirements, the long-term and short-term insurance sectors have developed along distinctly differentiated paths. Long-term insurance features extended renewal cycles and high per-claim payout amounts, with main policies often incorporating dividend or cash-value return components; thus, in addition to providing medical coverage, they offer an additional wealth-management benefit. Consequently, over the past two decades, long-term health insurance—dominated by critical illness coverage—has maintained a significant market presence despite the availability of universal payment schemes such as basic medical insurance.

In 2020, critical illness insurance witnessed new policy changes. The newly revised "Standard for the Definition of Diseases in Critical Illness Insurance (2020 Revision)" supplemented and optimized the coverage scope and classification of critical illnesses. In general, on one hand, the grading system for critical illnesses was optimized by introducing definitions for mild conditions, making the compensation standards more scientific; on the other hand, the coverage scope was moderately expanded, refining and extending the original 25 defined critical illnesses to 28 severe diseases and 3 mild diseases. Overall, there was no significant expansion in the compensation scope of critical illness insurance, but the diseases within the compensation scope were described in greater detail.

The refinement of regulatory rules often reflects that industrial development has entered a new phase. As a “legacy” commercial health insurance product, critical illness insurance faces increasingly fierce industry competition and rising demands from existing policyholders. The development of critical illness insurance has reached a critical crossroads; how to stand out among highly homogenized products has become the biggest challenge for insurance companies.

In the future development of critical illness insurance, health management for policyholders may become the core strategy for breakthrough growth. The newly revised Administrative Measures for Health Insurance, implemented at the end of 2019, proactively addressed this trend by increasing the allowable allocation of costs for health management services provided under health insurance products from 12% to 20% of net premiums, thereby effectively enhancing insurers’ incentives and feasibility in delivering health management services to customers.

On the other hand, in September 2020, the China Banking and Insurance Regulatory Commission (CBIRC) also issued the *Notice on Regulating Health Management Services of Insurance Companies*, which outlined four key components: first, clarifying the concept and objectives of health management services; second, specifying the principles and requirements to be followed in providing such services; third, improving the operational rules for health management services; and fourth, strengthening supervision and oversight of these services.

Taken together, the regulatory authorities’ stance on health management initiatives by insurance companies is largely clear: they encourage the provision of health management services while simultaneously ensuring their quality.

In the evolution of health management, integrating internet-based healthcare for digital health management is clearly a superior option compared to directing patients to offline medical institutions for examinations and consultations.

Some insurance companies and internet healthcare enterprises have already begun their explorations in this direction. For instance, one of the features of Ping An Good Doctor’s “Ping An Medical Home,” launched in September 2020, is to provide robust insurance coverage through synergy with insurance products, thereby alleviating concerns for both patients and healthcare providers and enhancing the level of protection in online medical services. Meanwhile, ZhongAn Online obtained an internet hospital license in 2019, connecting medical institutions, pharmacies, patients, and insurance products through its internet hospital platform to create a complete closed-loop insurance protection system.

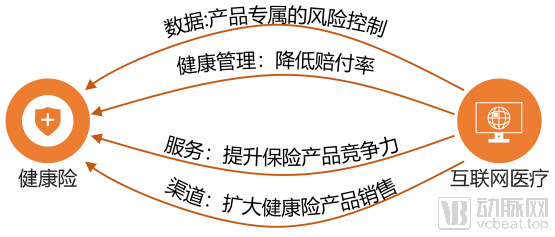

Internet healthcare’s entry into the health insurance sector can enhance the value of health insurance in several aspects:

1. Product-Specific Risk Control: Leveraging the vast amount of patient data accumulated through internet-based healthcare, and empowered by artificial intelligence technologies, to assist insurance companies in rationally designing corresponding insurance products.

2. Ensure customer health and reduce claim ratios: Especially for patients with chronic diseases, long-term digital patient management can help them better manage their conditions and reduce the incidence of severe complications.

3. Additional Value-Added Services to Enhance the Competitiveness of Insurance Products: The product comes with complimentary internet-based medical consultation services, which can effectively enhance its competitiveness among similar products in the highly homogenized critical illness insurance sector.

4. Directly serve as a channel to build a platform for the display, sales, and information of insurance products: With the rapid development of the internet healthcare industry, the model of “online hospital consultations + online medication purchases” has gradually emerged as a new patient traffic entry point, holding the potential to precisely channel users to insurance services.

When the perspective shifts to short-term health insurance, the pressures it currently faces are distinctly different from those of long-term health insurance.

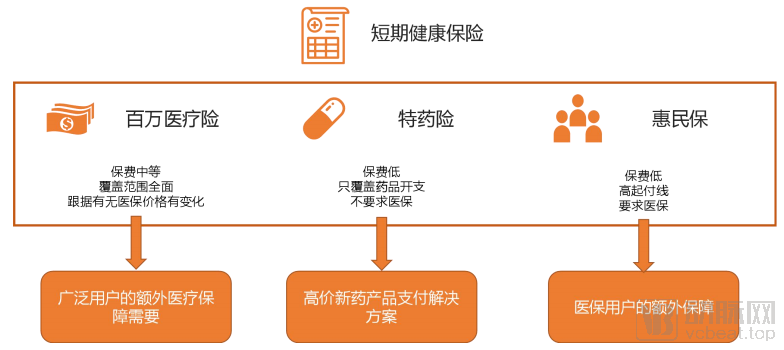

From the wildly popular million-yuan medical insurance plans of previous years, to the gradually warming specialty drug insurance in recent years, and then to the Huimin Bao (inclusive supplementary medical insurance) launched by various provinces starting in 2020, short-term health insurance has witnessed a surge in development over the past two years, in contrast to the steady growth of long-term critical illness insurance.

Short-term health insurance is characterized by low premiums and high coverage limits. Taking critical illness insurance and million-yuan medical insurance as examples, the annual premium for a critical illness policy with a coverage limit of RMB 500,000 can reach around RMB 5,000; whereas the price of million-yuan medical insurance fluctuates based on age, remaining mostly under RMB 1,000 for individuals under 50 years old, and generally exceeding RMB 5,000 annually only after age 80.

Moreover, million-yuan medical insurance offers broader coverage than critical illness insurance and allows for policy renewal even after standard claims have been settled. However, compared to critical illness insurance, million-yuan medical insurance is more purely protective in nature, reimbursing only incurred medical expenses rather than providing a fixed benefit payout, and it lacks the investment or savings component associated with critical illness insurance.

For some individuals, the purpose of purchasing medical and health insurance products is to find a solution for the substantial medical expenses incurred from sudden critical illnesses. For this group, million-yuan medical insurance policies are sufficient to meet this need.

Other medical insurance products follow a similar pattern. For instance, the specialty drug insurance sector primarily provides payment solutions for high-cost innovative drugs. As annual national reimbursement drug list (NRDL) negotiations continue, fewer products remain excluded from coverage, gradually diminishing the value of specialty drug insurance plans that cover only domestically launched new drugs. Consequently, in 2020, leveraging the open policies of the Hainan International Medical Tourism Pilot Zone, six international specialty drug insurance products were sequentially launched in Hainan. Building upon coverage for high-cost innovative drugs available in China, these plans further extended coverage to new drugs approved abroad but not yet authorized in China, thereby establishing a new value proposition for specialty drug insurance.

Huiminbao primarily targets individuals who have already enrolled in the national basic medical insurance, particularly those covered by the Urban and Rural Resident Basic Medical Insurance (URRBMI). Compared to the Employee Basic Medical Insurance, URRBMI offers a lower reimbursement rate. For high-cost treatment regimens, patients may still face substantial out-of-pocket expenses even after insurance reimbursement. Huiminbao products, characterized by low premiums and high deductibles, are specifically designed to address this issue, ensuring that insured individuals’ medical expenditures remain within an affordable range.

The value of short-term medical insurance in real-world scenarios is beyond doubt; however, for this category of products, the greatest challenge they currently face is building trust with users.

Short-term medical insurance is frequently sold through online platforms, which inherently suffer from disadvantages in ensuring user awareness. Users are required to independently understand the policy terms and claims procedures; if certain clauses are not fully comprehended, leading to a cumbersome claims process, users can easily develop distrust toward insurance products.

In fact, the application of chatbots can effectively address this issue. Leveraging artificial intelligence technology, chatbots can replace human agents in communicating with users, helping them fully understand the relevant terms of insurance products before purchasing policies and during the claims process. This enhances the efficiency of underwriting and claims settlement, thereby establishing a bond of trust between insurance companies and their customers.

As early as 2017, Microsoft CEO Satya Nadella recognized the potential of chatbots in the insurance industry. Speaking at the “FinTech Ideas Festival” in San Francisco, he stated, “Chatbots can be applied in multiple areas such as sales and customer service. The chatbots being developed today already possess strong natural language understanding capabilities, enabling them to perform a wide range of tasks.”

Microsoft offers a variety of chatbot solutions based on the Microsoft Azure cloud platform, which can be integrated into diverse enterprise application scenarios. These include informational chatbots that provide cognitive search capabilities, enterprise productivity chatbots that streamline common work activities, and commercial chatbots that directly handle business communications and process customer requests.

The above content is excerpted from the report “Quarterly Review of Digital Innovation in Healthcare: Reimagining Health Insurance with Digital Solutions for Four Key Scenarios.” Scan the mini-program QR code below to access the full report.