Annual Analysis of Over 400 Healthcare Policies in 2020: Seven Key Themes Shaping China's Medical Reform

2020 was undoubtedly a year dedicated to all-out pandemic response; however, as epidemic prevention and control entered a normalized phase and social operations returned to normal, the new healthcare reform—the central policy thread in the medical sector—remained no exception.

Since the launch of the new healthcare reform in 2009, the General Office of the State Council has annually released key tasks for the year and assigned them to various departments. In accordance with these priority tasks, State Council departments have formulated corresponding policy documents to facilitate their implementation. Therefore, examining the annual key tasks for deepening healthcare reform provides insight into the policy direction and underlying logic for each year.

Affected by the pandemic, the key tasks for 2020 were released in the second half of the year. VCBeat analyzed the 2020 healthcare policies based on the “Notice of the General Office of the State Council on Key Tasks for Deepening Healthcare System Reform in the Second Half of 2020” (hereinafter referred to as the “Tasks”). After conducting a word frequency analysis of the full text of the “Tasks,” VCBeat identified the seven most frequently occurring keywords (excluding terms with broad macro-level connotations such as “reform” and “health”): epidemic prevention and control, public health, procurement, payment, medical service pricing, medical security, and performance evaluation.

Panoramic View of 2020 Healthcare Policies, Chart by VCBeat

These keywords are closely related to the key policy priorities throughout the year. VCBeat compiled 407 healthcare policies issued in 2020 from the official websites of relevant regulatory authorities, including 306 from the National Health Commission, 44 from the National Healthcare Security Administration, and 57 from the National Medical Products Administration. By integrating these policies with key terms related to healthcare reform, we analyzed the implementation progress of such reforms. From a macro perspective, epidemic prevention and control along with the improvement of the public health system have enabled the healthcare system to resume and maintain normal operations, thereby enhancing public health levels, which serves as a prerequisite for implementing reforms. Centralized procurement and payment reforms help create fiscal space within the medical insurance fund, allowing for increased expenditure on technical and labor services in healthcare delivery and strengthening medical security coverage for patients. Furthermore, the effectiveness of corresponding reform measures can be evaluated and methodologies improved through performance assessments.

Recently, the COVID-19 epidemic has resurged in many parts of China. Unlike the early days of 2020, both authorities and the public are responding with greater calmness and confidence. Highly efficient mass nucleic acid testing within localized areas has become the most effective and safest screening measure. COVID-19 vaccines have been launched and are being administered to priority populations, with 10 million doses already administered.

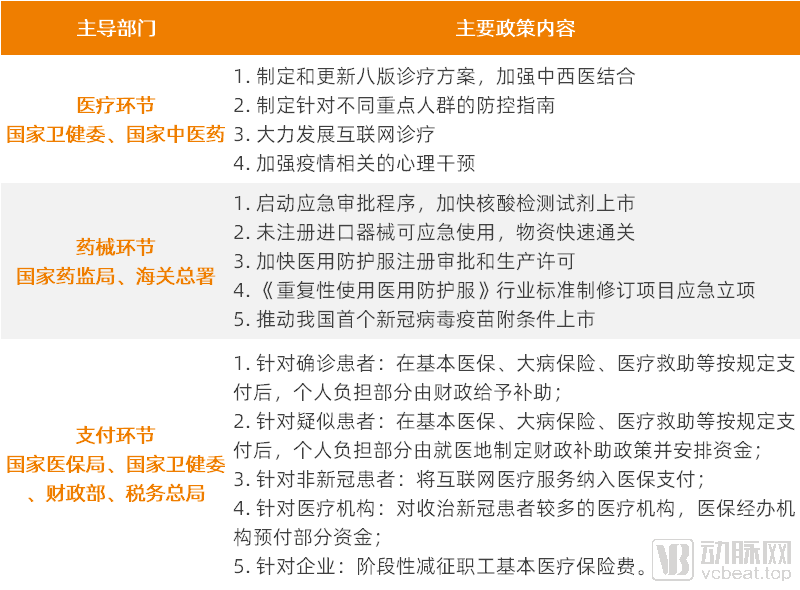

These achievements reflect the progress made in combating the pandemic over the past year, underpinned by epidemic prevention and control policies. In 2020, a total of 87 such policies were introduced, with the highest concentration in several key areas. These policies primarily supported epidemic prevention efforts across three critical segments—healthcare services, pharmaceuticals, and payment systems—and achieved breakthroughs in 14 specific aspects.

Major Policy Breakthroughs Related to Epidemic Prevention and Control, Source: Official Websites of Various Departments, Compiled and Charted by VCBeat

In the healthcare sector, the National Health Commission has led the development of various regulatory documents, work plans, and guidelines, focusing on public protection, community-based prevention and control and grassroots screening, medical treatment and scientific research breakthroughs, as well as healthcare worker support and incentives. Among these, the Diagnosis and Treatment Protocol for Novel Coronavirus Pneumonia has been updated as healthcare professionals’ understanding of the virus and the disease has continued to deepen.

It is worth noting that the National Health Commission issued two directives within four days, encouraging the provision of internet-based medical consultations. This initiative aimed to alleviate the treatment burden on hospitals while preventing cross-infection among ordinary patients during offline visits. As a result, digital healthcare became an “aerial battlefield” in epidemic prevention and control, penetrating daily life to an unprecedented extent and ushering in a year of explosive industry growth.

In the pharmaceutical and medical device sectors, in accordance with the Emergency Approval Procedures for Medical Devices, drug regulatory authorities may implement emergency approval for required medical devices when there is a threat of public health emergencies. The National Medical Products Administration (NMPA) accordingly activated the corresponding emergency approval mechanism, particularly by expediting the approval of nucleic acid testing kits and protective supplies to alleviate the demands on the front lines of the epidemic response.

For COVID-19 drugs and vaccines, the National Medical Products Administration (NMPA) also innovatively established a collaborative mechanism integrating research and review. By adopting a parallel approach of “simultaneous R&D, submission, and evaluation,” the NMPA minimized the time required for review and approval, thereby facilitating the conditional marketing authorization of China’s first COVID-19 vaccine and advancing clinical trials for a batch of drugs intended for epidemic prevention and control.

During the payment phase, the National Healthcare Security Administration, the National Health Commission, the Ministry of Finance, and the State Taxation Administration implemented measures to provide financial support for pandemic treatment. Free treatment was provided for both confirmed and suspected COVID-19 patients. For non-COVID-19 patients, internet-based medical services were included in the medical insurance reimbursement scheme. To alleviate the burden of advancing funds for medical institutions, medical insurance agencies provided advance payments. For enterprises, employee basic medical insurance premiums were temporarily reduced to relieve corporate financial pressure.

According to data from the National Healthcare Security Administration, a total of RMB 165 billion in employee basic medical insurance premiums were waived for 9.75 million participating entities in 2020. The cumulative settlement of patient expenses amounted to RMB 2.84 billion, with medical insurance payments covering RMB 1.63 billion.

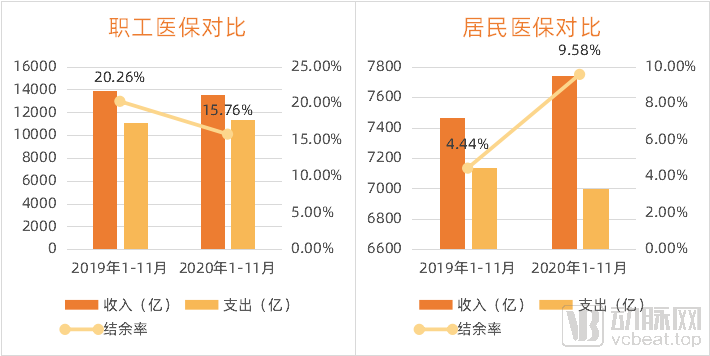

As both revenues and expenditures underwent changes, the surplus status of the medical insurance fund in 2020 also exhibited corresponding characteristics.

Changes in the Revenue and Expenditure of the Medical Insurance Fund; Data Source: National Healthcare Security Administration; Chart by VCBeat

As shown in the figure above, revenue from the Employee Basic Medical Insurance declined significantly in 2020, while expenditures rose markedly, leading to a decrease in the overall surplus ratio. In contrast, revenue from the Resident Basic Medical Insurance showed an upward trend, accompanied by a decline in expenditures. VCBeat attributes this primarily to heightened public awareness of preventive care, which reduced the frequency of medical visits, particularly for pediatric respiratory diseases.

Therefore, against the backdrop of a declining surplus rate for the Employee Basic Medical Insurance and a rising surplus rate for the Resident Basic Medical Insurance, the overall decline in the surplus rate of the medical insurance fund was modest, decreasing from 14.73% in January–November 2019 to 13.31% in January–November 2020, thereby exerting limited impact on subsequent reforms involving medical insurance participation.

It is evident that the healthcare system, by mobilizing its full capacity, played a pivotal role in turning the tide after the widespread outbreak of the epidemic. This achievement serves as the foundation for restoring normal socioeconomic operations and as a prerequisite for the continued and smooth advancement of healthcare reform.

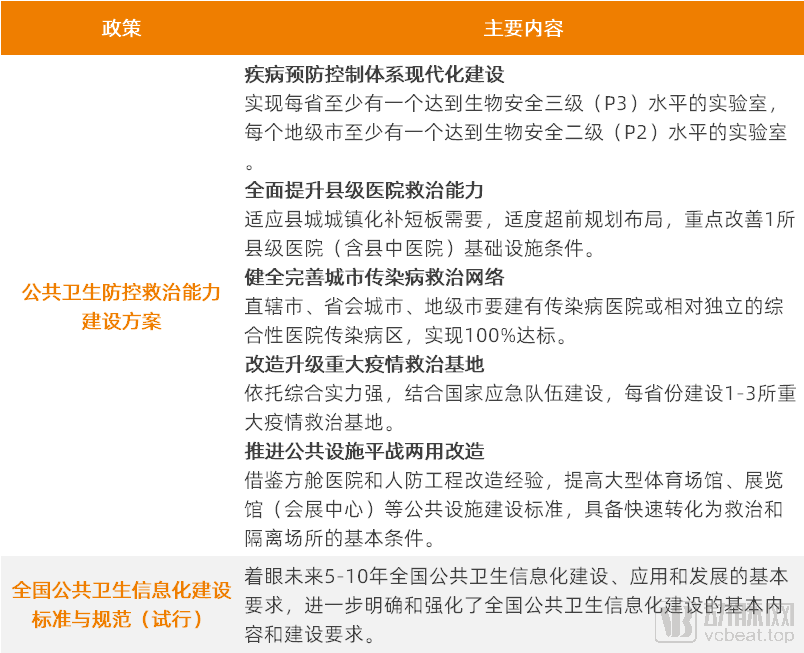

The outbreak has elevated the improvement of public health systems to a more prominent position, with “strengthening the construction of public health systems” listed as the top priority in deepening healthcare reform. In 2020, relevant public health policies, drawing on lessons learned from epidemic prevention and control, primarily addressed weaknesses by enhancing both hardware infrastructure and software capabilities.

Policy Requirements for the Development of Software and Hardware Infrastructure in the Public Health System. Source: National Health Commission; Graphic by VCBeat

In terms of hardware, in May 2020, the National Development and Reform Commission, the National Health Commission, and the National Administration of Traditional Chinese Medicine jointly formulated the “Plan for Strengthening Public Health Prevention, Control, and Treatment Capabilities,” which outlined five major construction tasks: modernizing the disease prevention and control system, enhancing the treatment capabilities of county-level hospitals, improving and perfecting urban infectious disease treatment networks, upgrading and transforming major epidemic treatment bases, and promoting the dual-use (peacetime and emergency) retrofitting of public facilities.

The Plan specifies concrete construction standards for each task, emphasizing the integration of peacetime and emergency operations to maximize resource utilization.

Taking the construction of major epidemic treatment bases as an example, the document specifies the stockpile quantities for centralized care of critically ill patients and emergency supplies, which will generate corresponding equipment procurement demands.

Reference List of Emergency Medical Supplies for Major Epidemic Treatment Bases (Calculated per Base), Source: National Health Commission, Graphic by VCBeat

In terms of software, the National Health Commission and the National Administration of Traditional Chinese Medicine issued the "Standards and Specifications for National Public Health Informatization Construction (Trial)," which focus on the basic requirements for construction, application, and development over the next 5–10 years, further clarifying and strengthening the fundamental content and requirements for public health informatization construction.

Furthermore, within the framework of basic public health services, the per capita subsidy standard was raised to RMB 74 in 2020. The additional RMB 5 in funding was fully allocated to rural areas and urban communities, where it was pooled to cover expenditures such as personnel costs and operational expenses for grassroots medical and health institutions engaged in COVID-19 prevention and control. This measure aimed to strengthen financial guarantees for epidemic prevention at the grassroots level, enhance pandemic response capabilities, and reinforce primary healthcare-based epidemic prevention and control.

Under policy guidance, public health institutions at all levels have begun to undertake renovations, upgrades, or new construction. According to the China Government Procurement Network, there were over 1,000 procurement projects in 2020 that included “public health” in their descriptions, with project requirements primarily focused on construction and medical equipment. The purchasers were mostly large hospitals and county-level health commissions.

Some projects have also commenced construction or begun to show initial results. For example, the National Medical Center for Major Public Health Emergencies, established with Tongji Hospital affiliated to Tongji Medical College of Huazhong University of Science and Technology as the main entity, began construction in July 2020 and is expected to be completed in June 2022.

It is imperative to improve the public health system, which is a long-term, large-scale undertaking and serves as a guarantee for the sustained and smooth advancement of healthcare reform. Over the next three to five years, public health infrastructure development will remain a critical priority. Demand from institutions at all levels for emergency treatment equipment, information systems, and even intelligent applications will drive growth in corresponding industries.

In the “Tasks,” “procurement” primarily refers to centralized volume-based procurement. In 2020, the national centralized procurement program expanded from pharmaceuticals to high-value medical consumables, beginning with coronary stents.

From Local to National: Centralized Procurement of Medical Consumables Leads to Significant Price Reductions

In fact, multiple regions, including Jiangsu, Shandong, and Zhejiang, have already implemented centralized procurement of medical consumables through inter-provincial alliances, provincial-level programs, prefecture-level alliances, and city-level centralized bidding. These initiatives cover high-value consumables in fields such as cardiology, orthopedics, and ophthalmology, as well as low-value consumables like infusion sets, indwelling needles, and syringes, thereby accumulating experience for national-level centralized procurement.

2020 Regional Centralized Procurement of Medical Consumables: Data from Public Reports; Chart by VCBeat

In the first batch of centralized procurement of high-value medical consumables organized at the national level, the procurement cycle for coronary stents was two years, with an intended total purchase volume of over 1.07 million units in the first year. Ultimately, 10 coronary stent products from seven companies were selected. The average price of the selected stents dropped from RMB 13,000 to around RMB 700, representing a reduction of more than 90%, and is expected to save RMB 11.7 billion in medical expenses annually.

Medical consumables are complex to classify, and even those within the same category possess diverse functional attributes. Due to individual patient differences, the use of the same type of consumable often requires different specifications and models. Coronary stents, as standardized products, are relatively less complex among medical consumables; coronary stents of the same brand and type but with different specifications are priced uniformly. Furthermore, it is estimated that in 2019, approximately 1.5 million coronary stents were used nationwide in China, incurring costs of around RMB 15 billion, which accounted for one-tenth of the total expenditure on high-value medical consumables across the country.

The high degree of standardization and the substantial proportion of expenditure are likely the reasons why coronary stents marked the beginning of centralized procurement for high-value medical consumables; these two characteristics also determine the direction for future categories included in centralized procurement.

Undoubtedly, the centralized procurement of high-value medical consumables follows a logic similar to that of pharmaceutical centralized procurement, namely: driving down artificially inflated prices and eliminating inefficiencies in the distribution chain. For enterprises, it is particularly crucial to build a multi-tiered product portfolio. Leveraging products included in centralized procurement to gain market share, while developing high-end products to meet the needs of patients with varying purchasing power, represents a viable strategy.

However, high-value consumables differ significantly from pharmaceuticals. High-value consumables often require surgical manipulation by physicians and involve physician training. Following the implementation of centralized procurement, how to reflect the labor value of physicians and how to conduct physician education are issues that must be taken into consideration.

Drug Centralized Procurement Enters Normalization Phase; Pharmaceutical Companies Pivot to Innovation

In terms of centralized drug procurement, the second and third rounds of national centralized drug procurement were launched in 2020, gradually entering a normalized phase. Among them, 32 drugs were selected in the second round, and 55 drugs were selected in the third round, with an average price reduction of 53% for both rounds.

Two years have passed since the first round of centralized procurement, namely the “4+7” pilot program. This prompts the question: How are the drugs and companies that won bids at that time faring? Among the winning enterprises in the “4+7” centralized procurement, four were publicly listed companies. These companies released their 2019 annual performance reports in 2020, which may provide some insights.

Huahai Pharmaceutical had six products selected in the “4+7” centralized procurement program. According to its annual report, the company’s selling expenses decreased by 25.79% year-on-year in 2019, primarily due to the advancement of national centralized procurement, which led to reductions in corresponding market promotion fees, labor costs, and other expenses. Notably, product promotion service fees declined significantly.

Kelun Pharmaceutical’s Bailuote was also selected in the “4+7” centralized procurement program. Its annual report showed that Bailuote’s market share rose rapidly after winning the bid. In 2019, Bailuote generated annual sales revenue of RMB 329 million, a year-on-year increase of 58.28%.

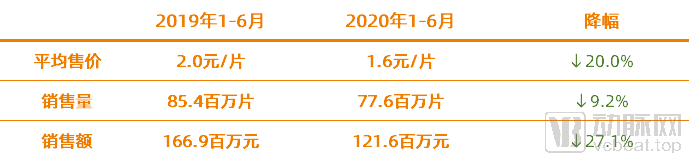

In the “4+7” volume-based procurement program, Simcere Pharmaceutical’s Bici won a bid; however, its prospectus did not separately disclose changes in revenue for this product. Nevertheless, Simcere disclosed sales changes for Shufutan, a product that failed to win bids. Shufutan did not secure winning bids in either the “4+7” or the second round of centralized procurement, which adversely affected both its sales volume and average selling price due to downward pricing pressure associated with the procurement policy. As a result of declines in both price and volume, Shufutan’s sales revenue decreased by 27.1% in the first half of 2020.

Sales Performance of Simcere Pharmaceutical’s Shufutan; Data Source: Simcere Pharmaceutical Prospectus; Chart by VCBeat

From a policy perspective, the normalization of centralized drug procurement and the implementation of centralized procurement for medical consumables have further created room to enhance the protective capacity of medical insurance and increase the service-based income of healthcare professionals.

From an industry perspective, pharmaceutical companies are gradually increasing their R&D investment and optimizing their organizational structures. The industry-optimizing effects brought about by centralized procurement are beginning to manifest, and this impact may similarly be reflected in the medical consumables sector.

While centralized volume-based procurement has created greater fiscal space, reforms to medical insurance payment mechanisms are being advanced in parallel. At the current stage, the overarching direction of reform is to explore more refined, composite, and diversified payment methods within the existing global budget framework, including Diagnosis-Related Group (DRG)-based payment, regional point-based global budgeting, and Diagnosis-Intervention Packet (DIP)-based payment.

In 2020, pilot programs for Diagnosis-Intervention Packet (DIP) payment were launched, conducted separately from the Diagnosis-Related Group (DRG) payment pilots. The National Healthcare Security Administration issued documents including the work plan for DIP payment, technical specifications, and the DIP disease category directory.

Pilot Arrangements for DIP and DRG | Data Source: National Healthcare Security Administration; Chart Compiled by VCBeat

In terms of pilot arrangements, apart from the difference in pilot cities, there is also a significant disparity in implementation progress between DIP and DRG, with DIP advancing notably faster than DRG. This is primarily attributable to the differences in their operational mechanisms.

DIP is a big data-based diagnosis-intervention packet payment method that leverages comprehensive data to objectively reflect the real-world dynamics of clinical disease patterns. It employs exhaustive enumeration and clustering of disease diagnoses and treatment modalities within the data to rapidly form groups, mines data insights to understand the objective relationships between disease-treatment combinations and medical costs, establishes quantitative standards for diseases and treatments, and determines pricing mechanisms based on stochastic averages, health insurance payment methods, and fund supervision models.

DRG grouping classifies cases into several related groups based on comprehensive factors such as patient age, gender, length of stay, clinical diagnosis, surgical procedures, comorbidities, and complications, with an emphasis on reliance on clinical pathways. In contrast, DIP is based on full-sample, massive data to classify all disease types and technical procedures, with an emphasis on reliance on clinical data.

Since grouping results can be obtained through big data computation, DIP features high case assignment rates, rapid implementation, and the potential for gradual refinement.

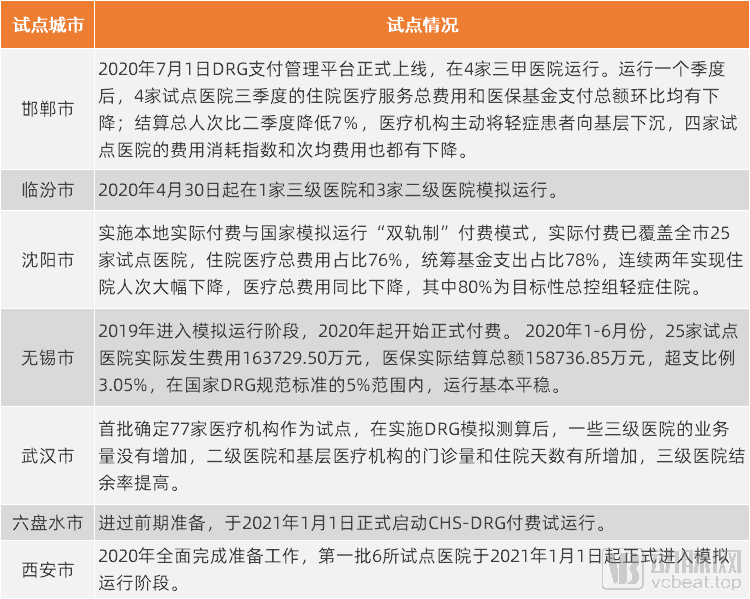

The implementation effectiveness of DIP remains to be verified; how has the DRG system, which began pilot programs in 2020, been performing?

According to the “Monitoring and Evaluation Report on the National Pilot Program for Diagnosis-Related Groups (DRG) Payment in the Third Quarter of 2020” released by the National Healthcare Security Administration Research Institute, although there were significant differences in the progress of pilot implementation across cities, notable advancements were made compared with 2019. Among the 30 pilot cities, 29 largely met the requirements set by national authorities and were ready for simulated operation. The main challenges encountered during implementation in pilot cities included poor quality of historical data, limited accuracy of patient classification into DRGs, inconsistent versions of medical institution coding systems, and integration issues arising from fragmented development of information systems.

Pilot Implementation of DRG in Selected Cities, Source: Public Reports, Graphic by VCBeat

However, as can be seen from the chart above, cities such as Handan and Wuxi have already achieved results in healthcare cost containment under medical insurance and in the implementation of tiered diagnosis and treatment.

In any case, the reform of medical insurance payment has taken a critical step, with the simultaneous pilot implementation of DRG and DIP serving as a “double safeguard.”

As healthcare reform advances, the entrenched practice of hospitals relying on drug sales to subsidize operations is gradually being dismantled, while prices for medical services are steadily rising.

According to data released by the National Healthcare Security Administration, during the 13th Five-Year Plan period, more than half of the medical service items reflecting technical value had their prices increased across various provinces. Compared with the end of the 12th Five-Year Plan period, price increases for diagnostic and treatment services ranged from 20% to 100%, surgical services from 40% to 150%, nursing services from 50% to 200%, and traditional Chinese medicine (TCM) services from 20% to 60% across different provinces.

However, to date, the pricing of diagnostic, therapeutic, and surgical services has still failed to fully reflect the service value provided by healthcare professionals.

The Prerequisite for Medical Service Price Reform Is the Standardization of Service Items.

In 2000, China’s price control authorities first formulated the “National Specifications for Medical Service Price Items,” establishing it as the primary pricing unit system for charges and payments by medical institutions, permitting provincial-level supplements, and comprehensively revising and expanding it in 2012.

Development of National Standards for Medical Service Pricing Items Over the Years; Source: National Healthcare Security Administration, National Development and Reform Commission; Chart compiled by VCBeat

In 2020, the National Healthcare Security Administration accelerated the reform of medical service pricing, initiated the development of the “National Standard for Medical Service Price Items,” and organized its compilation through open public tendering.

The National Healthcare Security Administration pointed out in the bidding documents that medical service pricing items serve as the fundamental basis for pricing medical services and constitute the prerequisite foundation for deepening the reform of medical service prices and leveraging price mechanisms to regulate the supply and demand of medical services. However, feedback from various stakeholders indicates that the current specifications for medical service pricing items no longer adequately meet the needs of furthering these reforms.

Specifically, the current medical service pricing items have the following issues:

First, the classification and hierarchical structure of items need to be streamlined. The logical framework for item initiation lacks rigor, as evidenced by practices such as establishing cost elements as independent pricing items or initiating new projects solely due to changes in delivery method, target population, or clinical scenario for the same service. These practices artificially increase the complexity of item management and elevate the risk of overcharging.

Secondly, the standardization and normalization of pricing items remain inadequate. There are inconsistencies in the scope of pricing items implemented across different regions; the number of pricing items corresponding to the same service output varies, leading to phenomena such as “different names for the same item” and “same name for different services.” A disconnect exists among item configuration, patient experience, and clinical needs, thereby increasing the costs associated with clinical application and price management.

Furthermore, the project content exhibits poor compatibility with clinical changes and technological advancements. The projects are excessively tied to specific clinical procedures; once there are slight changes in the equipment, reagents, anatomical sites, steps, or methods used, it may become difficult to map them to existing priced items. This creates a dilemma where hospitals either cannot charge for the services or risk non-compliant billing practices, a situation that has drawn strong complaints from hospitals.

Furthermore, the project pricing framework emphasizes bundling medical consumables within the scope of service items, causing material costs to become the primary driver of price changes and making it difficult to fully reflect the value of technical labor. Over time, this approach also fails to accurately capture the distinct trends in labor costs versus material consumption costs in healthcare services. When technological monopolies lead to price hikes for medical consumables, hospitals struggle to effectively control costs, which hampers service delivery and may even distort clinical practices.

Therefore, in the development of the new edition of the National Specifications for Medical Service Price Items, the National Healthcare Security Administration requires that, based on the actual items currently implemented across provinces and drawing on domestic and international experience, the criteria for establishing price items and management rules for converting medical technologies or activities into priced items be standardized. This aims to reasonably reduce the number of items, achieve decoupling of price items from technical details, separate services from consumables, and ensure alignment between items and coding rules.

According to the China Government Procurement Network, the Chinese Society of Social Security has won the bid for this project, with a two-year implementation period.

From the perspective of the new regulatory compilation requirements, the separation of pharmaceuticals from medical services, the decoupling of surgical fees from consumables, and the implementation of centralized volume-based procurement for both drugs and medical consumables have created room for streamlining the medical service pricing system and reforming the compensation structure for healthcare professionals. Over time, the value of medical services will be more fully reflected in the future.

In 2020, the Central Committee of the Communist Party of China and the State Council formulated the “Guiding Opinions on Deepening the Reform of the Medical Security System,” which has become a programmatic document for the medical security system. The “Opinions” propose that by 2030, a comprehensive medical security system will be fully established, with basic medical insurance as the mainstay, medical assistance as the safety net, and complementary development of supplementary medical insurance, commercial health insurance, charitable donations, and mutual medical aid.

Within the healthcare security system, social health insurance and commercial health insurance are two key components.

Key Policies of the Healthcare Security System; Data Sources: National Healthcare Security Administration, China Banking and Insurance Regulatory Commission; Graphic by VCBeat

Outpatient Mutual Aid Reform Launches, Changes in Medical Insurance Payment Scenarios

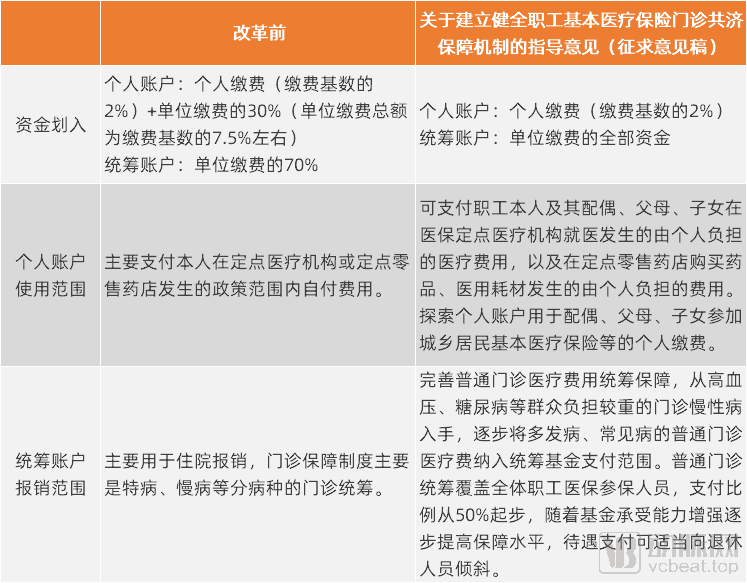

Regarding medical insurance, the reform of individual accounts under the employee basic medical insurance scheme was officially launched in 2020, marking a significant transformation after more than two decades of implementation. In 1998, the State Council issued the Decision on Establishing the Basic Medical Insurance System for Urban Employees, establishing a “combined pooling and individual account” system. Under this framework, individual accounts were funded by employee contributions plus 30% of employer contributions, primarily used to cover outpatient visits and medication expenses for the insured employees themselves; pooled accounts were funded by the remaining 70% of employer contributions, mainly used to reimburse hospitalization costs for the insured employees.

Under the previous system, healthy individuals accumulated substantial balances in their personal accounts, whereas the elderly and those in poor health found their personal account funds insufficient, thereby failing to achieve the function of risk pooling.

In August 2020, the National Healthcare Security Administration released the “Guiding Opinions on Establishing and Improving the Outpatient Mutual Aid Mechanism for Employee Basic Medical Insurance (Draft for Comments),” which proposed adjustments to the inflows and outflows of individual accounts. The overarching principle can be summarized as follows: reduce the amount credited to individual accounts, with the reduced funds primarily allocated to outpatient mutual aid.

Comparison of Personal Account Reforms Before and After. Source: National Healthcare Security Administration; Graphic by VCBeat

As shown in the figure above, according to the current policy documents, there are changes in the allocation of funds to medical insurance accounts. Previously, a portion of the employer’s contributions was credited to individual accounts, while the remainder was allocated to the pooled fund; following the reform, all employer contributions are directed into the pooled fund. Individual accounts, which were previously restricted to use by the account holder only, may now be used by family members after the reform. The pooled fund, originally primarily covering inpatient reimbursement and outpatient reimbursement for special chronic diseases, will gradually expand to include reimbursement for common and frequently occurring diseases.

Although the current document is a draft for public comment and specific measures have yet to be finalized, it is evident that optimizing account structures and enhancing the efficiency of medical insurance fund utilization will undoubtedly be the overarching direction.

The reform of personal accounts will not only change the scope of coverage for insured individuals but also alter payment scenarios.

In 2020, the integration of internet-based healthcare services into medical insurance payment systems accelerated, with as many as 28 relevant policies issued throughout the year. The National Healthcare Security Administration released the Guiding Opinions on Actively Promoting Medical Insurance Payment for “Internet+” Medical Services, which outlined detailed plans for incorporating internet-based medical services into medical insurance coverage, prompting follow-up actions across various regions. Beijing, Shanghai, Zhejiang, Jiangsu, Tianjin, Sichuan, Guangdong, Ningxia, and other areas have taken the lead in implementing initiatives to connect online consultations and online medication purchases with medical insurance reimbursement.

Internet-based medical consultations are primarily positioned for the follow-up treatment of common and chronic diseases, with a high degree of overlap in the scope of covered conditions with the outpatient mutual aid system implemented following the reform of individual medical savings accounts. In the future, the expansion of internet-based consultation coverage will drive the shift of outpatient payments to online channels, while enhanced outpatient insurance coverage will further promote the widespread adoption of internet-based medical services.

While enhancing coverage capacity at the fund level, China’s basic medical insurance system is also strengthening supply-side assurance capabilities. The Interim Measures for the Administration of Drugs under Basic Medical Insurance, issued in 2020, established management measures for the National Reimbursement Drug List (NRDL), instituted a robust dynamic adjustment mechanism—with adjustments原则上 made annually—and implemented negotiated access for exclusive drugs.

In fact, since 2018, the National Reimbursement Drug List (NRDL) has been adjusted three consecutive times, and a dynamic adjustment mechanism has been basically established. The 2020 NRDL adjustment involved price negotiations for 162 drugs, with 119 successfully included, resulting in an average price reduction of 50.64%. This adjustment also marked the first attempt to conduct price reduction negotiations for drugs already included in the NRDL. Following established procedures, review experts selected 14 exclusive drugs with relatively high prices or costs and significant fund utilization for price reduction negotiations; each of these drugs had annual sales exceeding RMB 1 billion. All 14 drugs successfully reached agreements through negotiations and remained in the NRDL, with an average price reduction of 43.46%.

New Policies Drive Expansion of Commercial Health Insurance Coverage

In 2020, the China Banking and Insurance Regulatory Commission (CBIRC) and twelve other departments jointly issued the “Opinions on Promoting the Development of Commercial Insurance in the Social Services Sector,” proposing to strive for a commercial health insurance market size exceeding RMB 2 trillion by 2025, thereby making it an important component of China’s distinctive medical security system. The Opinions also call for exploring the promotion of information sharing between the commercial health insurance information platform and the National Healthcare Security Administration’s information platform in accordance with relevant regulations.

In the past, information asymmetry between commercial insurance institutions and the healthcare and medical insurance sectors has been a major obstacle hindering the further development of commercial health insurance. This information asymmetry poses significant challenges to risk control management for commercial insurers. Although premium income from health insurance has grown rapidly in recent years, corresponding claims payouts have also increased at a fast pace.

In October 2020, the main construction of the National Healthcare Security Administration’s healthcare security information platform was completed. In November, the nationally unified healthcare security information platform was first implemented in Guangdong Province, with nationwide rollout expected by the end of 2021. Achieving interconnectivity and data exchange within the healthcare security system will lay the foundation for information sharing between public health insurance and commercial health insurance.

Medical insurance and critical illness insurance are the primary types of commercial health insurance, and policies related to both underwent changes in 2020.

According to data from the China Banking and Insurance Regulatory Commission (CBIRC), in 2019, the original premium income for medical insurance reached RMB 244.2 billion, a year-on-year increase of 32%, which was approximately 20 percentage points higher than the overall premium growth rate of the industry, accounting for 34.6% of total health insurance premiums. However, in terms of policy term, the vast majority were one-year products, with few long-term medical insurance offerings available, failing to effectively meet actual market demands.

To this end, in 2020, the China Banking and Insurance Regulatory Commission issued the “Notice on Issues Concerning Premium Rate Adjustments for Long-Term Medical Insurance Products,” which clarified the scope of products with adjustable premium rates and encouraged insurance companies to develop and sell long-term medical insurance products.

In the realm of critical illness insurance, the Insurance Association of China and the Chinese Medical Doctor Association issued the "Standard for the Use of Disease Definitions in Critical Illness Insurance (2020 Revised Edition)." Building upon the original 25 defined critical illnesses, the new definitions add three severe conditions: severe chronic respiratory failure, severe Crohn’s disease, and severe ulcerative colitis. Meanwhile, it introduces a scientific stratification for three core critical illnesses—malignant tumors, acute myocardial infarction, and sequelae of stroke—and adds corresponding definitions for three mild forms of these conditions. For example, under the previous definitions, all thyroid cancers were compensated as critical illnesses; under the new definitions, compensation may be provided either as a critical illness or as a mild disease, depending on the severity of the condition.

Overall, the new policies for commercial insurance are vigorously promoting a richer supply of health insurance products, expanding coverage scope, and enhancing protection capabilities, while information interoperability can have a positive impact on risk control management in health insurance. In the future, commercial health insurance will play an even more important role in the medical security system.

As a key mechanism for evaluating the effectiveness of healthcare reforms, performance assessment in public hospitals continued to advance in 2020, expanding from tertiary hospitals to secondary hospitals and primary care institutions.

Performance evaluation metrics for medical institutions at all levels encompass dimensions such as healthcare quality, sustainable development, and patient satisfaction. Due to significant differences in their positioning within the tiered diagnosis and treatment system, the indicators related to functional orientation vary considerably. Tertiary hospitals focus on the treatment of inpatients and the performance of complex surgeries; secondary hospitals prioritize simpler surgical procedures; while primary care institutions concentrate on providing basic public health services.

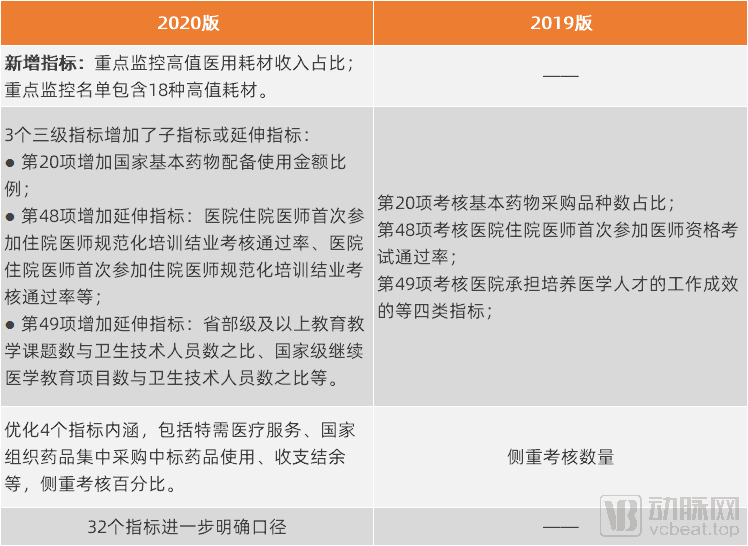

In 2020, tertiary public hospitals ushered in the second round of performance appraisal, conducted in accordance with the National Operational Manual for Performance Appraisal of Tertiary Public Hospitals (2020 Edition). Compared with the 2019 edition, the 2020 edition maintained the same indicator framework and sequence, with indicator names, attributes, data sources, and orientations remaining largely unchanged; however, details of certain indicators were adjusted:

Changes in Performance Assessment Indicators for Tertiary Public Hospitals; Source: National Health Commission; Graphic by VCBeat

Recently, the "Operational Manual for Performance Appraisal of National Tertiary Public Hospitals (2020 Edition)" has once again adjusted certain indicators, resulting in a revised version. The dynamic updating of assessment indicators not only ensures standardization, normalization, and homogenization of the appraisal process but also better aligns with the actual operational realities of hospitals.

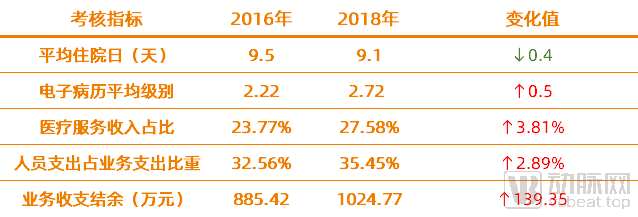

In 2020, the National Health Commission also released the results of the first round of performance evaluations for tertiary public hospitals. The evaluation data indicate a continuous improvement in the quality of medical services and management standards at tertiary hospitals.

Partial Data from the Performance Assessment Results of Tertiary Hospitals (Note: The 2019 assessment data were sourced from 2016–2018). Source: National Health Commission; Chart by VCBeat

Particularly in terms of revenue structure, the proportion of income from medical services has gradually increased, while the average drug cost per inpatient visit and per outpatient visit have both declined. This indicates that the goals of deepening healthcare reform—namely, curbing drug expenses and increasing compensation for healthcare professionals’ labor—are beginning to show initial results.

With the establishment of performance indicators and the advancement of evaluation efforts across medical institutions at all levels, hospitals will demonstrate greater initiative and proactivity in implementing healthcare reform tasks, enabling continuous improvements to the reform through the resolution of phased challenges.

Despite the challenges posed by the pandemic in 2020, the deepening of healthcare reform did not halt. On the contrary,Measures and Experience in Epidemic Prevention and Control Have Promoted Institutional Breakthroughs and Addressed Weaknesses: Emergency review and approval processes accelerated the market launch of epidemic prevention supplies, pharmaceuticals, medical devices, and COVID-19 vaccines. Despite covering treatment costs for COVID-19 patients and reducing premium collections, the medical insurance fund maintained a stable overall surplus rate. Guided by the principle of integrating routine operations with emergency response, strengthening the public health system became the top priority in the second half of the year. The value of “Internet + Healthcare” and “Internet + Medical Insurance” was highlighted through temporary measures implemented during epidemic prevention and control, leading to their widespread adoption in public hospitals.

Meanwhile, measures carried over from 2019—such as centralized procurement, payment method reforms, the medical security system, and performance-based reforms in public hospitals—have been vigorously advanced. Centralized procurement of medical consumables proceeded as scheduled, with coronary stents dropping in price from tens of thousands of yuan to just a few hundred yuan. Payment method reforms expanded the pilot programs for Diagnosis-Intervention Packet (DIP), forming a “dual safeguard” alongside the Diagnosis-Related Group (DRG) pilots. The medical security system launched outpatient mutual aid reforms for employee basic medical insurance, encouraging commercial insurers to broaden their coverage. Performance assessment indicators have been continuously optimized and refined through practical implementation. Assessment data indicate that the healthcare reform strategy of “making room for new initiatives by phasing out outdated practices” is beginning to yield results.This series of tasks, originally scheduled to be completed over the course of a year, was largely accomplished in the second half of the year due to the impact of the pandemic, underscoring the government’s strong resolve and considerable power in driving reforms.

Where Is the Deepening of Healthcare Reform Headed? VCBeat Believes It Lies Mainly in the Continuously Strengthening Driving Role of Medical Insurance.As the payer, China’s National Healthcare Security Administration (NHSA) has already demonstrated its substantial influence on the supply of medical services and pharmaceuticals through initiatives such as centralized volume-based procurement, negotiations for inclusion in the NHSA reimbursement drug list, and reforms in payment methods. With these efforts becoming routine and the future implementation of the new edition of the National Specifications for Medical Service Price Items,The changes brought by medical insurance to the supply side will become even more pronounced.

Furthermore, according to the official website of the National Healthcare Security Administration, the initial draft of the Healthcare Security Law (Draft Proposal) has been completed, and it has been proposed to the Social Development Affairs Committee of the National People’s Congress that the Healthcare Security Law be included in the NPC’s 2021 legislative plan.

With the establishment and improvement of the legal framework for medical security, law-based administration in the field of medical insurance will be strengthened, governance capabilities will be further enhanced, and various reform measures driven by medical insurance will be implemented more effectively.