Two Decades of Internet Giants in Healthcare: Insights and Warnings from Amazon’s Journey

Internet giants have never hidden their ambitions, especially in the healthcare sector.

Whether it is domestic giants such as Alibaba, Tencent, Baidu, JD.com, and ByteDance, or international players like Google and Microsoft, as well as Amazon, the focus of this article, all have demonstrated significant interest in the healthcare sector. They either enter the market indirectly by investing in healthcare companies or directly by establishing subsidiaries. Each move has drawn industry attention, scrutiny, and even caution.

The reason behind this is that,Armed with abundant resources such as a vast pool of tech talent, ample capital, massive traffic, and powerful distribution channels, internet giants can always make rapid headway when initially entering a specific niche market.

What followed was internet giants siphoning off industry talent with higher-premium salaries and squeezing industry profits through lower sales prices. These internet-driven tactics have placed immense pressure on many healthcare startups and introduced greater uncertainty into the development of leading companies in the traditional healthcare sector.

Meanwhile, as internet giants continue to expand and stake out strategic positions, people have begun to raise questions: After leveraging massive resources to disrupt the market, have these tech behemoths truly delivered sufficient incremental value to the industry? How should the healthcare sector integrate with the capital and technology brought by these cross-industry entrants? And where exactly lie the boundaries of these internet giants?

As one of the top three internet companies globally by market capitalization, Amazon, with over two decades of involvement in the healthcare sector, undoubtedly serves as a compelling case study: its footprint spans telemedicine, pharmaceutical e-commerce, drug research and development, intelligent medical hardware, health management, and health insurance. Moreover,In the past few years, Amazon has continued to increase its investment in the healthcare sector.

Therefore, reviewing and analyzing Amazon’s strategic layout and progress in healthcare, as well as examining its successes and setbacks during development, will help us answer the aforementioned questions and provide relevant insights and warnings for China’s internet giants.

For e-commerce platform companies, the fastest and most advantageous path into the healthcare sector is selling pharmaceuticals. However, as pharmaceuticals are special commodities subject to stringent regulation, their market share is predominantly concentrated in the prescription drug segment. Therefore,The ability to capture a share of the prescription drug market has become the key for companies to establish a firm foothold in their respective sectors.

As early as during the dot-com bubble in 2000, Amazon invested in Drugstore.com with the aim of expanding its e-commerce business into the pharmacy sector. However, due to regulatory and other reasons, the plan ultimately stalled.

It was not until 20 years later that Amazon officially announced its entry into the prescription drug retail business last November. The timing was chosen because demand for mail-order pharmacy services surged amid the worsening COVID-19 pandemic in the United States, allowing Amazon to significantly reduce customer education costs and facilitate business growth.

Additionally, from a market perspective, due toThe U.S. prescription drug retail sector is a business-to-business (B2B) market, where Amazon, despite its strengths in the consumer-to-consumer (C2C) segment, currently lacks significant advantages in terms of distribution channels and resources.This is also one of the key reasons why Amazon has made slow progress in its healthcare business segment over the years.

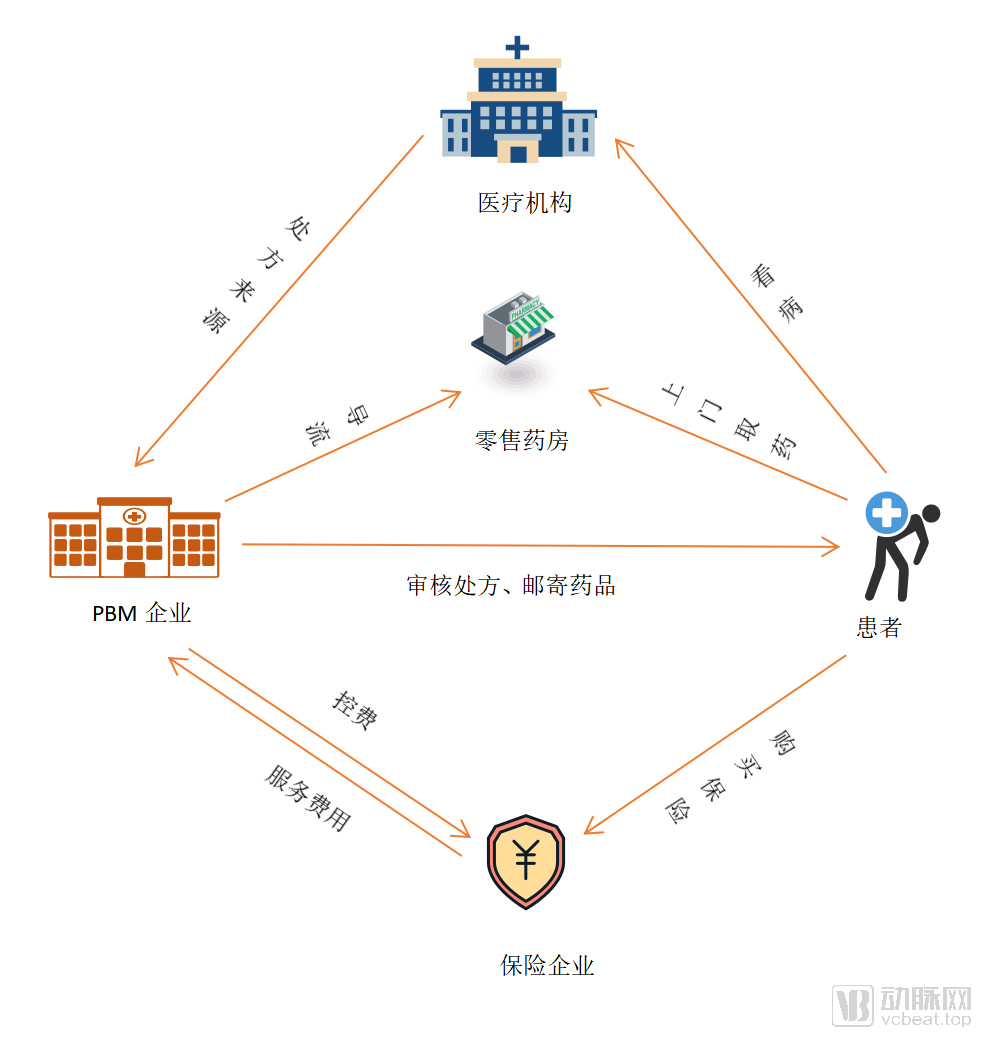

It is important to note that in the development of the U.S. retail prescription drug market, Pharmacy Benefit Managers (PBMs) have played a significant role as intermediary coordination entities among insurance providers, hospitals, pharmacies, and pharmaceutical manufacturers. PBMs undertake a wide range of core responsibilities, such as establishing retail pharmacy networks, through which insured members can enjoy discounts when purchasing medications at designated PBM-affiliated pharmacies. For patients with chronic conditions, whose prescriptions tend to remain relatively stable, PBMs offer mail-order pharmacy services, enabling home delivery of prescription medications without the need for face-to-face consultations with pharmacists.

Over decades of development, the U.S. PBM industry has become highly mature, with a high level of market concentration; the top three leading companies account for approximately 80% of the market share. More importantly,In the United States, Pharmacy Benefit Managers (PBMs) hold authority over prescription verification in drug retail channels and control health insurance formularies.

(The Role of PBM in the U.S. Healthcare System | Graphic by VCBeat)

(The Role of PBM in the U.S. Healthcare System | Graphic by VCBeat)

In principle,When Amazon entered the pharmaceutical e-commerce sector, partnering with leading Pharmacy Benefit Managers (PBMs) was the quickest and most convenient approach. However, since mail-order prescription drug services constitute a significant revenue stream for PBMs, Amazon’s entry inevitably faced substantial obstacles from these traditional channel partners.

For example, after Amazon announced its entry into the pharmaceutical sector in 2017, major U.S. pharmacy benefit managers (PBMs) rushed to merge with health insurers to preempt potential industry disruptions that Amazon might bring. In March 2018, Cigna, the fourth-largest health insurer in the United States, acquired Express Scripts (ESI), the largest independent third-party PBM in the country. Later that November, CVS Health, the largest prescription drug retailer in the United States, acquired Aetna, the third-largest health insurer. Since then, there have been no large independent PBMs remaining in the United States. ThisFor Amazon, the challenge of rapidly scaling prescription volume and advancing its business by partnering with large commercial health insurers as payers has become increasingly difficult.

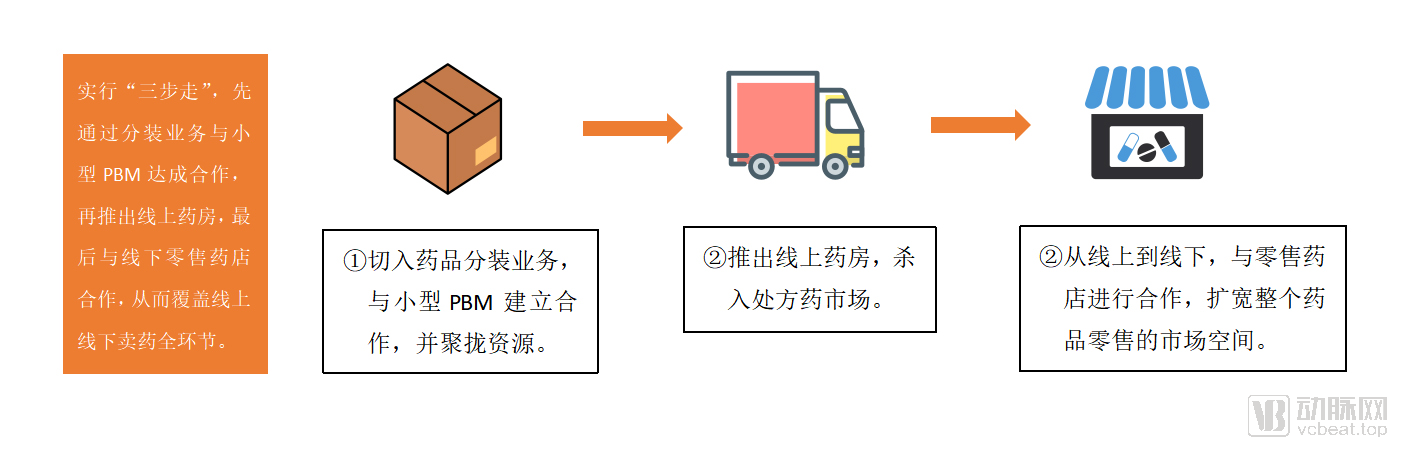

So, what strategy did Amazon adopt to enter the “cake” of prescription drug retail? The answer is “an indirect approach.” Simply put, it isAdopting a three-step approach to progressively penetrate the prescription drug market, thereby achieving comprehensive online and offline coverage.

Step 1: Enter the pharmaceutical repackaging business, establish partnerships with small-scale PBMs, and consolidate resources.In June 2018, Amazon completed its acquisition of the online pharmacy PillPack for $753 million. As a company serving Pharmacy Benefit Managers (PBMs), PillPack was founded in 2013 and launched its products in 2014. Over the four years from its inception to its acquisition, PillPack’s customer base surged from 50 to 40,000.

Pillpack’s primary customers are chronic disease patients requiring long-term medication. Due to the need for multiple complex medications, regular prescription updates by physicians, and the predominance of elderly patients among this population, patients often end up taking duplicate medications or failing to adhere to their prescribed regimens. Pillpack addresses this issue by having users create an account and provide relevant information, including their treating physicians and current medications. Pillpack then packages each dose of the user’s prescribed medications into individual pouches, clearly labeled with the corresponding administration time. Users can only remove one pouch at a time from Pillpack’s customized medication dispenser. Additionally, Pillpack offers a companion app to send medication reminders. This approach significantly simplifies medication management for chronic disease patients.

Because Pillpack’s primary customers were pharmacy benefit managers (PBMs), particularly smaller PBMs, it accumulated substantial industry resources. Additionally, Pillpack maintained strong relationships with insurers, secured mail-order pharmacy licenses in all 50 U.S. states, and built out infrastructure such as pharmacy software and distribution centers. These assets laid a solid foundation for Amazon to establish its online pharmacy and mail-order services after acquiring Pillpack.

Step 2: Launch an online pharmacy to penetrate the prescription drug market.More than two years after acquiring PillPack, Amazon launched Amazon Pharmacy, an online and mobile platform for ordering prescription medications. Reportedly, Amazon Pharmacy offers U.S. customers the ability to order prescription drugs with home delivery, and Amazon Prime members enjoy free shipping on these orders.

Specifically, Amazon Pharmacy users can purchase medications via the Amazon app on computers or mobile devices. Users can also add insurance information and payment methods before checkout. Upon receiving a user’s order, the physician sends the prescription directly to Amazon Pharmacy, which then uses relevant tools to verify that each prescribed medication was legally issued by the physician. Once this process is completed, the user receives the prescribed medications via home delivery.

Amazon Pharmacy offers both brand-name and generic prescription medications, allowing users to purchase common prescriptions online—such as contraceptives, insulin, steroid creams, and medications for blood sugar control and migraine management. However, it does not provide most controlled opioid medications, nor does it sell the vitamins and supplements typically found in health and personal care stores.

At this stage, Amazon has officially stepped into the pharmaceutical sales arena. The next question to consider is how Amazon can strongly integrate its core business with its online pharmacy segment to create synergies and drive scalable growth.

Currently, Amazon’s strategy in the mail-order pharmacy sector is to leverage its vast base of Prime members to drive growth in its online pharmacy business. For instance, it offers free two-day shipping on medications for paid Prime members, while non-members can choose free delivery within five days or pay $5.99 to upgrade to two-day delivery.

As many U.S. PBM companies have merged with insurance companies on the payer side,It is not easy for Amazon to collaborate with insurance companies to gain customer traffic.. To this end,Amazon primarily targets self-pay users.To attract this demographic, Amazon has offered substantial discounts and promotions, thereby driving down drug prices. Among these, certain generic drugs available to self-pay patients are discounted by up to 80%.

It is worth noting that large e-commerce platforms like Amazon, with their mature logistics and digital warehousing systems, coupled with the advantages of offering a comprehensive product range, are not afraid of price wars when expanding into other categories. Leveraging their massive scale and business synergies, these platforms can confidently extend their reach. To fully capture market share, Amazon is highly likely to continue driving down drug prices, subsidizing this strategy with profits from its other business segments. This approach serves as a key “disruptive weapon” in the internet giants’ arsenal of “dimensional reduction attacks.”

Step 3: Expand from online to offline by partnering with retail pharmacies to broaden the overall market space for pharmaceutical retail.Once Amazon’s online pharmacy business matures, it will inevitably expand into offline channels to grow the overall pharmaceutical retail market.

Of course, Amazon will not replace offline chain pharmacies. This is because offline chain pharmacies have a specific community coverage radius, within which users exhibit strong loyalty. First, the short travel distance makes it convenient for users to purchase medications. Second, face-to-face consultations and advice in physical stores provide users with a greater sense of trust and security. Third, for elderly users, the learning curve associated with online medication purchasing is steep, making it difficult to change their established behavioral habits.

Therefore, Amazon’s more likely strategy in the future is to partner with offline retail pharmacies, seamlessly integrating the immediacy and convenience of online services with physical store operations. In other words, Amazon will act as an enabler for pharmacies, providing them with customer traffic and digital technology solutions to help reduce costs, improve efficiency, and deliver a better medication-purchasing experience for users.

(Amazon’s “Three-Step” Sequential Chart, Graphic by VCBeat)

(Amazon’s “Three-Step” Sequential Chart, Graphic by VCBeat)

In summary, as an internet giant with a current market capitalization of approximately $1.66 trillion, Amazon’s e-commerce platform attributes provide it with inherent advantages in expanding its pharmaceutical e-commerce business. Prescription drugs account for the largest share of the entire pharmaceutical e-commerce market; therefore, dominating the prescription drug segment is key to prevailing in the industry.

However, since Pharmacy Benefit Managers (PBMs) have dominated the U.S. pharmaceutical distribution channel over years of development, Amazon cannot directly become an intermediary that resells drugs to consumers by negotiating with pharmaceutical companies. Moreover, as mail-order prescription drug services constitute a significant revenue source for PBMs, the likelihood of Amazon collaborating with leading PBM players is minimal. Consequently, Amazon has bypassed PBMs and adopted an indirect strategy—a “three-step approach”—to enter the prescription drug retail market.

It is undeniable that,Amazon’s current user base, accessed through its small-scale PBM offerings, primarily consists of approximately 20 million self-pay, uninsured individuals in the United States.Thus, upon completion of the “three-step” strategy, Amazon’s addressable market will reach saturation, forcing it into direct competition with leading Pharmacy Benefit Managers (PBMs).

As mentioned above, in its prescription drug business layout, Amazon has had to engage in a co-opetitive relationship with PBMs, which has constrained its rapid business expansion. Is there an alternative path available? For example,Amazon bypasses insurance companies to negotiate and collaborate directly with users.

Such initiatives do exist. In 2018, three corporate giants—Amazon, JPMorgan Chase, and Berkshire Hathaway—jointly established Haven, a healthcare company. Haven’s objective was to provide low-cost, high-quality medical and health services to the nearly one million employees of its three parent companies, while also offering more accessible primary care, easier-to-understand insurance benefits, and more affordable prescription drugs. In other words,Haven can serve as both the customer channel and the payer within Amazon’s entire healthcare ecosystem.

However, the challenge lies in the significant differences between B2B and B2C business logics. Apart from serving approximately one million employees across its three shareholder companies, Haven must continuously invest in offline infrastructure and market development to acquire additional corporate clients, which makes it difficult for the platform to achieve substantial user growth. Consequently, Haven also struggles to secure more competitive drug pricing from suppliers.

From a longer-term perspective, Haven also stands a significant chance. After all, leveraging Amazon’s robust supply chain integration capabilities and substantial financial backing, Haven can gradually accumulate industry resources. However, this path is inherently slow and yields results that are not immediately visible. Consequently, in January of this year, due to issues such as unclear business objectives and divergent views among shareholders,Haven, plagued by poor management, announced that it would finally shut down by the end of February 2021.

At present, the strategy of bypassing PBMs to collaborate directly with users by establishing self-owned payers has also temporarily been declared a failure.

As a high-growth sector, the healthcare industry generates vast amounts of data every day. In traditional healthcare settings, such data are often overlooked, primarily because most medical institutions lack effective methods for collecting and processing them. Leveraging their technological expertise, internet giants are well-positioned to provide robust health information systems and high-performance computing capabilities, thereby enabling enterprises to collect and process these data efficiently.

Amazon's approach is,Leveraging its cloud computing services, it has provided various AWS solutions to healthcare enterprises, particularly in the areas of security and compliance.

For example, at the end of last year, Amazon releasedAmazon HealthLake Solution for Big Data Services Targeting Medical InsuranceThis solution leverages Amazon’s cloud capabilities to store, transform, and analyze human health data and biotechnology data. As a “data lake” product tailored for healthcare payers, HealthLake enables a centralized repository that allows users to store all structured and unstructured data.

According to the official AWS website, the advantages of Amazon HealthLake include its ability to automatically understand and extract meaningful medical information from fragmented raw data, including processes such as prescriptions and diagnoses. Compared with traditional manual data searches, the Amazon HealthLake solution is more time-saving, labor-efficient, and cost-effective. Integrating these scattered pieces of information can help healthcare professionals gain a more comprehensive understanding of patients’ conditions. For example, initial diabetes diagnosis requires reviewing hundreds or even thousands of data points, which is extremely time-consuming; Amazon HealthLake can significantly reduce the time required for this process.

Second, Amazon HealthLake can also summarize trends and make predictions. For example, Amazon HealthLake can display a series of medical events based on time series, including care pathways and population health trends. In addition, users can build machine learning models using Amazon SageMaker to detect abnormalities in patients’ physical conditions. According to public information, well-known medical supply manufacturers such as Philips have already adopted this solution.

In October 2018, Amazon AWS joined the NIH (National Institutes of Health) STRIDES (Science and Technology Research Infrastructure for Discovery, Experimentation, and Sustainability) initiative,Leveraging Advanced AWS Cloud Technologies to Drive Innovative Biomedical Research.

Under this initiative, AWS provides cloud computing services to NIH biomedical researchers. The NIH’s efforts focus on helping researchers access high-value datasets and exploring new approaches to optimize technology-intensive research. The STRIDES Initiative is a component of the NIH Common Fund’s New Model for Data Sharing (NMDS). Another component of the NMDS is the NIH Data Sharing Pilot Program, which aims to test the integration of high-value biomedical datasets into cloud computing systems and to establish and evaluate best practices for data utilization. The three pilot datasets funded by the NIH were selected based on their value to the biomedical research community, data diversity, and coverage of both basic and clinical research.

Currently, these three datasets include the following: the Genotype-Tissue Expression (GTEx) dataset, which explores the expression and regulation of human genes across different tissues, as well as the role of genomic variation in altering gene expression; the Alliance of Genome Resources (AGR), which comprises six Model Organism Databases (MODs) that provide in-depth biological data for advanced research on model organisms; and the Trans-Omics for Precision Medicine (TOPMed) program, whose dataset collects and pairs whole-genome sequencing (WGS) data.

It is reported that,AWS is the second cloud service provider to join the STRIDES initiative, following Google Cloud.Although AWS has not yet publicly disclosed data on its healthcare customers, the company maintains a strong presence in the overall market. According to the “Market Share of Public Cloud IaaS and PaaS Worldwide, 2019” report released by the consulting firm Gartner in August 2020,AWS holds a 45% market share, surpassing the combined total of the second, third, fourth, and fifth largest players (34.3%).。

Driven by its vast population base and growing economy, the Chinese market has also become an important “territory” that Amazon seeks to expand into. Unlike heavily regulated sectors such as pharmaceutical e-commerce,AWS’s standardized advantages and high technological barriers have made it a key business line for Amazon’s international expansion.

In January 2020, AWS Marketplace was officially launched in the China Regions. Since then, users have been able to more easily discover, test, deploy, and manage third-party software required for running systems in the AWS China (Beijing) Region and the AWS China (Ningxia) Region.

However,To tap into the localized market, relying solely on high-quality products and technology is far from sufficient. How to align with the needs of Chinese medical enterprise users and achieve localized operations presents a significant challenge for Amazon.For example, how to resolve payment issues and address user trust concerns.

To this end, Amazon announced last March that AWS customers could pay for services in the US region using RMB online banking, marking a positive step toward resolving cross-border payment issues. In June of the same year, offline AWSome Day events resumed as the pandemic stabilized, with the AWS team meeting and sharing insights with AWS users in Zhengzhou, Fuzhou, Qingdao, Chongqing, Tianjin, Nanjing, and Kunming.

According to publicly available information, many Chinese healthcare and medical enterprises have adopted AWS services. For example, Amazon and Hejing Technology, a provider of “data science collaboration platforms,” have jointly built a cloud-based data collaboration platform on AWS. According to official AWS information, leveraging the mainstream machine learning frameworks supported by Amazon Elastic Compute Cloud (Amazon EC2), Hejing Technology’s K-Lab collaboration platform enables flexible selection of application frameworks tailored to the needs of healthcare industry clients.

For another example, New Century Healthcare has established connectivity between its entire medical network and AWS by setting up two redundant dedicated lines via AWS Direct Connect from Beijing New Century Children’s Hospital to two Availability Zones in the AWS China (Beijing) Region, operated by Sinnet. It is reported that New Century Healthcare has fully migrated the HIS/LIS systems of its five clinics to AWS, and the core HIS/LIS systems of any newly added chain clinics will be deployed directly on the AWS cloud in the future. In Phase II of the project, New Century Healthcare will also migrate its group-wide unified medical imaging platform, electronic film services, 3D-assisted diagnosis tools, and CRM system to the cloud.

From the perspective of progress,Amazon’s AWS is still in the phase of local adaptation. Whether it can rapidly expand its market share in the future remains to be seen.

In August 2020, Amazon released a smart wristband named “Halo,” which isAmazon's first wearable device, primarily designed for health and fitness tracking.At the same time, Amazon also launched a companion mobile app and subscription service.

“Halo” not only features health monitoring capabilities but also works in conjunction with a mobile app to provide users with five health monitoring functions, including activity assessment, sleep tracking, and body fat measurement, thereby helping them improve their personal health. Additionally, “Halo” can score and evaluate users’ exercise performance.

By combining hardware and software, Amazon aims to enter the health management market, starting with wearable devices. To this end, Amazon has partnered with renowned healthcare institutions such as Mayo Clinic and Harvard Health Publishing to provide users with daily exercise tasks. The company also plans to implement a points-based incentive system to encourage users to engage in more effective workouts.

To maximize new user acquisition, Amazon adopted a subscription model for Halo: $99 covers the device and six months of free service, after which a monthly subscription fee of $3.99 applies. Whether the smart wristband business line can gain strong momentum remains to be seen.

However, it is worth noting that,Binding with Prime membership may become an important means for Amazon to promote its smart hardware in the future.In other words, from the business perspective of Amazon Prime membership, users will have access to an increasingly diverse range of services in the future. This further strengthens user stickiness to the Prime membership service, thereby enhancing its competitiveness.

Furthermore, from the perspective of healthcare services,Amazon’s foray into wearable devices also paves the way for more in-depth health management in the future.Imagine users wearing Amazon’s smart devices, with their daily health data continuously transmitted via AWS cloud to Amazon’s backend. These user-authorized data streams converge into a “data lake.” Upon obtaining authorization for these data, pharmaceutical R&D companies can conduct targeted new drug development, significantly improving R&D efficiency. When users experience health issues, they can simply click a button to have medications delivered to their doorstep through Amazon’s online pharmacy or its partnered offline pharmacies. This undoubtedly offers the possibility of comprehensive, lifecycle-based health management for users.

Of course,To close this loop, numerous practical challenges remain, including regulation, privacy rights, conflicts of interest among stakeholders, and payer-related issues.However, for internet giants like Amazon, the likelihood of successfully pursuing this path is significantly higher, given their substantial accumulation of capital and technological expertise. This explains why the entry of such tech titans into the healthcare sector invariably triggers considerable disruption.

With these advantages, can internet giants truly reach every corner of the globe?

Looking back on Amazon’s 20-year journey into the healthcare industry, the path has been both smooth and winding.

The advantage lies in the fact that Amazon, leveraging its robust infrastructure accumulated in the e-commerce sector, can establish its pharmaceutical e-commerce operations more quickly and effectively than other startups., and its massive user base combined with a comprehensive product portfolio confer even stronger economies of scale. This explains why leading pharmacy benefit managers (PBMs) promptly pursued mergers and acquisitions with insurers after Amazon announced its entry into the healthcare sector, as Amazon’s rapid advancement would inevitably bring about significant changes to the overall landscape of the pharmaceutical retail market.

Additionally,Amazon’s accumulated expertise in cloud services and smart hardware has enabled it to build a deep technological moat.Unlike the business-model-oriented operations of pharmaceutical e-commerce, businesses such as cloud computing and smart hardware test a company’s product and technological capabilities, which require both ample talent and substantial capital. Judging from current market competition, only a few tech giants—such as Google, Microsoft, and Alibaba—are capable of competing with Amazon in the cloud computing market. And this, alsoThis has strengthened Amazon’s bargaining power in providing medical data services, enabling it to penetrate upstream segments such as drug R&D and achieve a broader layout across the healthcare industry chain.

The twist is that, although Amazon already ranks among the leaders in the technology industry in terms of technology, capital, and talent,When it comes to the specific sector of healthcare, one must still adhere to the inherent dynamics of this field.For example, when Amazon first entered the pharmaceutical e-commerce sector 20 years ago, it also stumbled due to regulatory hurdles. Similarly, Haven, a health insurance company jointly established by three giants—Amazon, JPMorgan Chase, and Berkshire Hathaway—to seize the role of payer, ultimately failed due to poor management and other reasons.

It is worth emphasizing that even in pharmaceutical e-commerce, Amazon’s area of greatest strength, it has encountered significant setbacks during its expansion. Viewed through the lens of its “three-step strategy for selling drugs,” this approach reflects less a strategic maneuver to bypass large pharmacy benefit managers (PBMs) and more an inevitable outcome of Amazon’s inability to directly apply its traditional internet mindset to achieve rapid, incremental progress in the healthcare sector.

This is because, in addition to the deeply entrenched and intertwined interests within the U.S. healthcare system, more importantly, it encompasses a relatively complex yet safety-assuring medical commercial framework that has evolved over nearly a century: whether patients, regulators, or retailers, all parties work to ensure that every prescription medication reaches patients in full compliance with regulations.The emergence of new approaches and models inevitably requires withstanding the test of time before gaining regulatory approval and market acceptance.After all, every single pill concerns the health and safety of users.

Therefore, based on Amazon’s 20 years of experience in the healthcare sector,Domestic internet giants should note that by identifying their proper positioning and leveraging their inherent “genetic” advantages, they can rapidly expand into the healthcare sector.For instance, Baidu has leveraged its vast user search data to establish Baidu Health Medical Encyclopedia, an authoritative medical encyclopedia service. Similarly, Alibaba and JD.com have capitalized on their mature e-commerce ecosystems to launch Yilu and JD Health, respectively, as pharmaceutical e-commerce platforms. Current outcomes indicate that these initiatives have rapidly flourished, achieving notable success.

Similarly, companies like Amazon and Alibaba secured early positions in cloud computing, establishing a strong foothold in the data processing sector. This holds significant application value for the healthcare industry, which manages vast amounts of data. It is precisely this advantage that has enabled Amazon to rapidly expand its business through AWS, even extending into upstream areas such as new drug development.

ButIt is still worth noting that the businesses currently being rapidly advanced in the healthcare sector are merely extensions of the internet giants’ core operations.For instance, pharmaceutical e-commerce represents an expansion of product categories within the e-commerce business, while AWS’s support for new drug development exemplifies a specialized application in the cloud computing services sector.

In contrast, Amazon’s foray into the insurance market failed because its inherent “DNA” could not be extended to businesses outside its core expertise. Typically, after achieving modest success in the healthcare and medical sector, internet giants tend to spin off these operations, aiming to transform them into the next mega-unicorns valued at tens or even hundreds of billions of dollars. However,If industry norms are neither understood nor adhered to, even trillion-dollar valuation giants will stumble.

After all, the combination of capital, talent, technology, and traffic is not a panacea for internet giants entering the healthcare industry. The biggest difference from other industries is that healthcare is related to people's lives and safety. Therefore,In addition to a deep understanding of the industry and the patience to wait, every participant must also approach this sector with compassion, humility, and reverence.

References:

《Amazon is going deeper into the prescription drug business.》Blake Dodge

《How Amazon is making strides in the healthcare space.》 Mackenzie Garrity

《Orion Health Teams Up With AWS For Amazon HealthLake》Orion Health

“JD Health (06618) with a Market Cap of HK$380 Billion: Examining How Amazon (AMZN.US), Valued at US$10 Trillion, Strategizes in the Pharmaceutical and Healthcare Sector” E-Drug Manager

“Exploring New Frontiers in Healthcare and Life Sciences with Data” AWS Cloud Computing