Global Healthcare Big Data Industry Value Trends Report 2015–2020: Prospectus Summary

I. Key Perspectives

1. The global healthcare big data sector has seen vigorous development over the past six years. Among the earlier-established enterprises, a number of companies have matured their business models, with some successfully going public; meanwhile, emerging startups continue to proliferate.

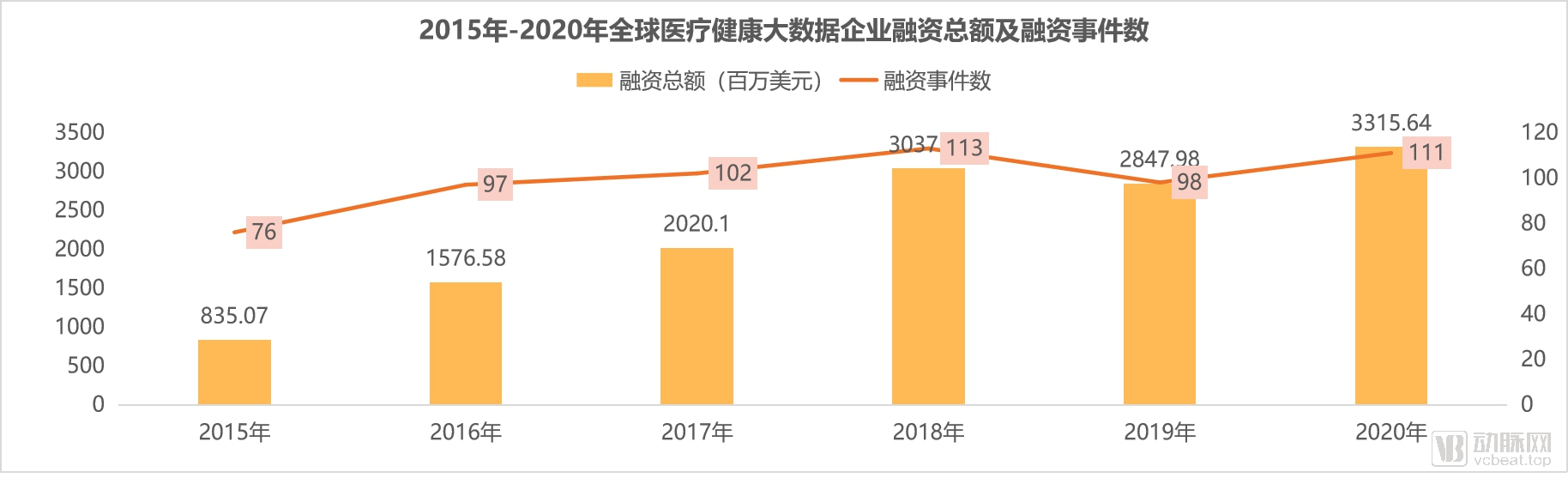

II. In 2020, there were 111 financing events in the field of health and medical big data, with cumulative financing exceeding USD 3.3 billion, a year-on-year increase of 17%. The average amount per financing round approached USD 30 million, remaining basically flat compared to 2019, indicating relatively stable development.

III. Within the niche segments of big data in healthcare, companies adopting the “AI + Big Data” model demonstrate relatively stronger capital-raising capabilities. In China, such companies with mature business models are taking the lead and are approaching initial public offerings. Overseas, the number of startups in this category continues to grow, with a trend toward further segmentation by disease-specific data domains.

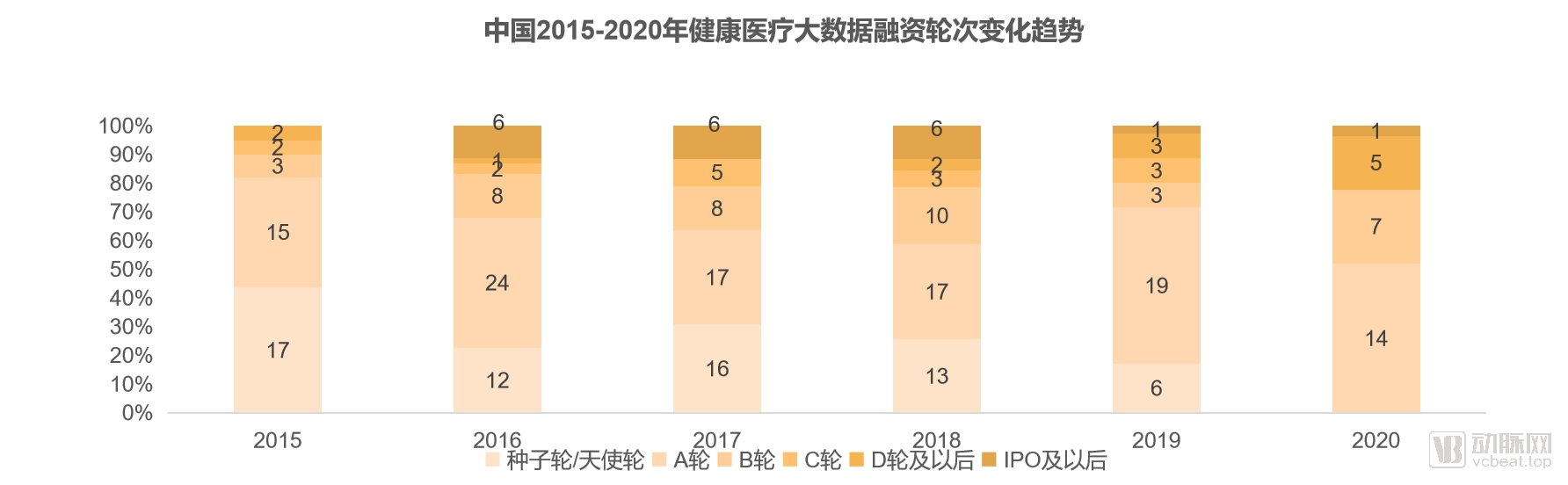

IV. The big data sector in health and medical care in China has gradually entered a stage of development, with the overall proportion of startups beginning to decline, while an increasing number of companies are securing Series D and later rounds of financing.

V. Latest Financing Trends in Health and Medical Big Data in 2020: Increasing Granularity of Data and Refinement of Disease-Specific Segments.

II. Trends in Global Healthcare Big Data Financing from 2015 to 2020

Overview of the Medical Big Data Industry

The development of big data in health and medical care in China can be traced back to the 2009 healthcare reform, which marked the beginning of medical informatization initiatives represented by electronic medical records. In recent years, the government has successively introduced relevant standards and regulatory requirements through policy measures to break down “information silos.” The domestic health and medical big data industry has progressed through early stages including data generation, collection, storage, and processing. However, the true value of industrial application lies in data analytics and utilization. This also necessitates that enterprises engage in specific application scenarios to reduce research and development as well as operational costs.

According to statistics from VBInsight, there are now more than 300 healthcare big data companies worldwide that have secured financing and specialize in collecting, integrating, and analyzing healthcare big data to provide solutions.

The changes in investment and financing events and amounts in the global health and medical big data sector over the past six years reflect the following trends:

Financing deals for startups in this sector continue to emerge in large numbers, maintaining a stable level of approximately 100 transactions per year since 2016. This trend is driven, on the one hand, by the sustained investor appeal of earlier-established companies such as LinkDoc Technology; on the other hand, new health and medical big data enterprises are continually emerging both domestically and internationally, reflecting strong demand for applications in this field.

Furthermore, impacted by the pandemic in 2020, relevant institutions have become increasingly reliant on big medical data, resulting in a year-on-year doubling of average corporate financing amounts, while the maturity of business models has continued to advance.

Overall, companies in the big data for health and healthcare sector are in a growth phase: Since 2016, there have been initial public offerings (IPOs) every year, while companies at the seed to Series A stages account for more than 60%, indicating that new enterprises continue to emerge frequently; the most advanced companies have reached Series G funding.

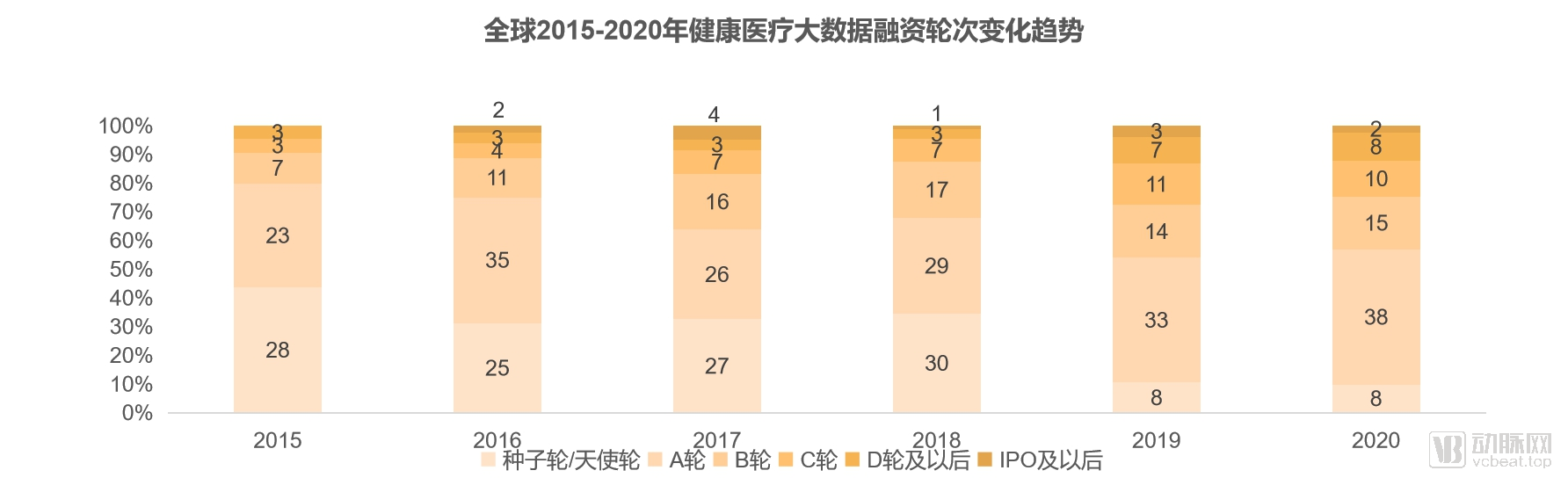

Currently, seed/angel-stage and Series A companies account for the largest proportion. However, over the past six years, early-stage financing has declined sharply over time, as companies in the global healthcare big data sector have entered the growth stage; meanwhile, the number of companies completing Series D and later financing rounds has been increasing year by year.

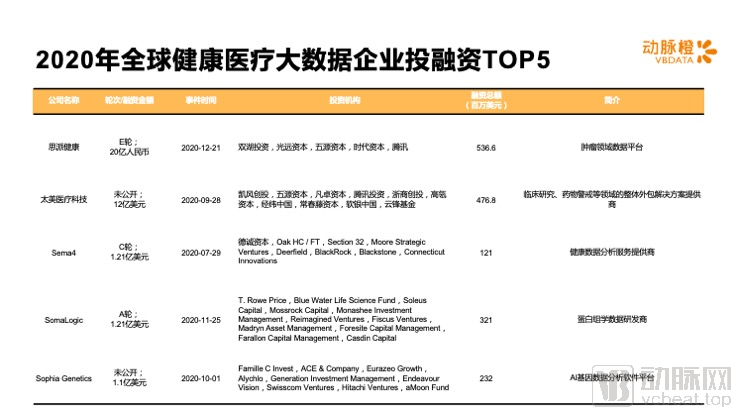

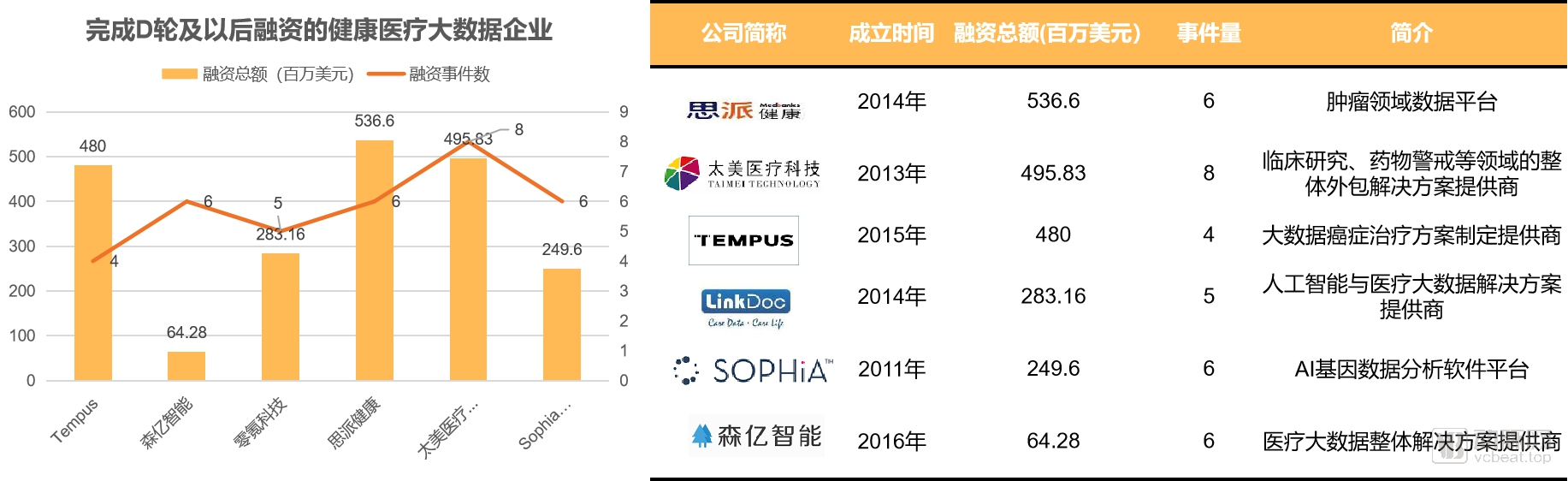

Among the six companies mentioned above, some offer artificial intelligence and algorithmic analytics services in addition to their core big data platform operations, while Sipei Health places greater emphasis on the granularity of big data within specialized healthcare segments. This indicates that capital markets currently favor the business models of companies integrating AI with big data, as well as those focusing on big data in niche sectors.

Si Pai Health, which secured the highest total funding, was established in 2014; meanwhile, LinkDoc Technology has continued to attract financing since its inception, indicating strong demand for big data and data analytics technologies in this niche sector and its faster growth trajectory.

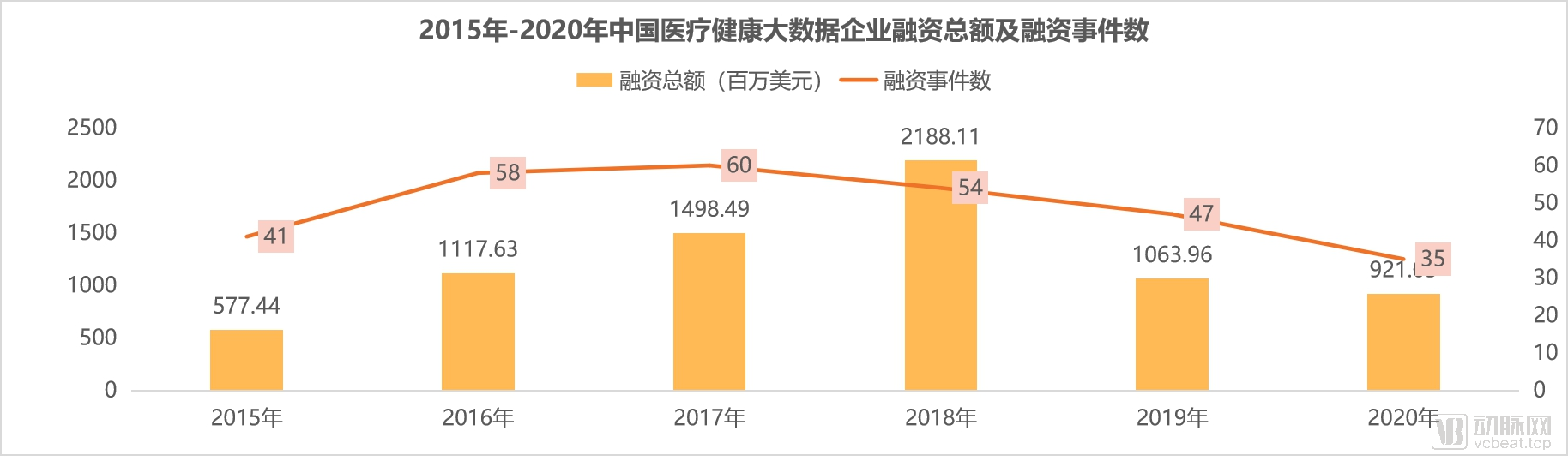

Unlike the global trend, China’s healthcare big data financing boom peaked in 2018. In contrast to the global surge in healthcare big data investment in 2020, domestic financing in this sector remained relatively stable in 2020, with the average funding amount showing a steady increase. Furthermore, although few healthcare big data companies went public in 2020, three companies completed Series D financing rounds, and Si Pai Health completed its Series E round, indicating that the number of domestic healthcare big data enterprises with mature business models continues to grow.

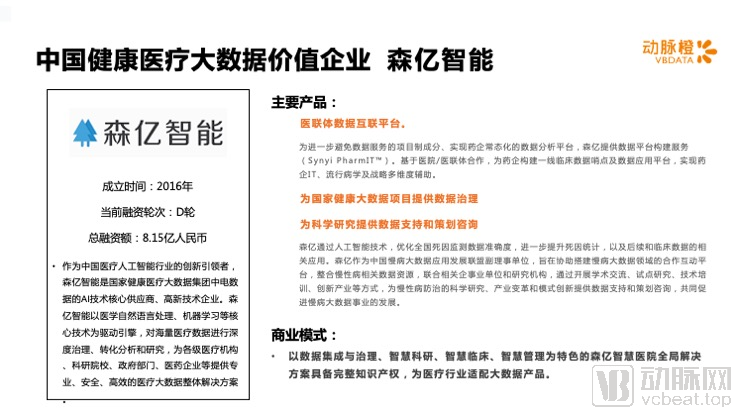

Compared with the global landscape, a greater number of Chinese healthcare big data companies remain in the early stages of development. With the exception of a few enterprises that have completed Series C or later financing rounds and are leading the market with relatively mature business models (such as SiMai Health, LinkDoc Technology, Senyi Intelligence, Kyee Group, Taimei Medical Technology, and DBAppSecurity), the majority of companies are still at the Series A financing stage. It is worth noting that in 2020, due to the impact of the pandemic, the number of domestic companies completing early-stage financing rounds decreased significantly, with capital increasingly flowing toward enterprises with larger data scales and more refined profitability models.

Financing Trends in Big Data for Healthcare2020 (1): Rapid Development of Companies Adopting the “AI + Big Data” Model

As of December 31, 2020, nearly 20 global companies specializing in AI and healthcare big data had completed new rounds of financing. These included mature firms such as Synyi AI and LinkDoc Technology, which secured Series D funding, while a number of startups were also on the rise.

These companies offer products and services to enterprises, relevant medical institutions, government agencies, and research organizations, with businesses purchasing the services and employees choosing to use them. Previously, Quartet and Talkspace have completed their Series D financing rounds. Such companies are growing rapidly, demonstrating that the strength of their business model lies in the diversity and stability of their B-side clients. Whether in terms of financing stages or user scale, enterprises entering the market through employers, health plans, and medical institutions are better positioned to gain a competitive advantage. In China, due to barriers such as technical thresholds, few companies operating under this model have managed to break out, but they still maintain a certain ability to attract capital.

Financing Trends in Healthcare Big Data2020 (2): Subdivision of Tracks, with Data in Niche Segments Gaining Attention

Increasingly granular big data in healthcare is gaining favor in practical applications, indirectly demonstrating that personalized diagnosis will become the new normal for the future trajectory of medical development. This shift toward a personalized model is inextricably linked to gene sequencing. Driving this advancement are innovations in human genomics technology and the emergence of big data analytics tools.

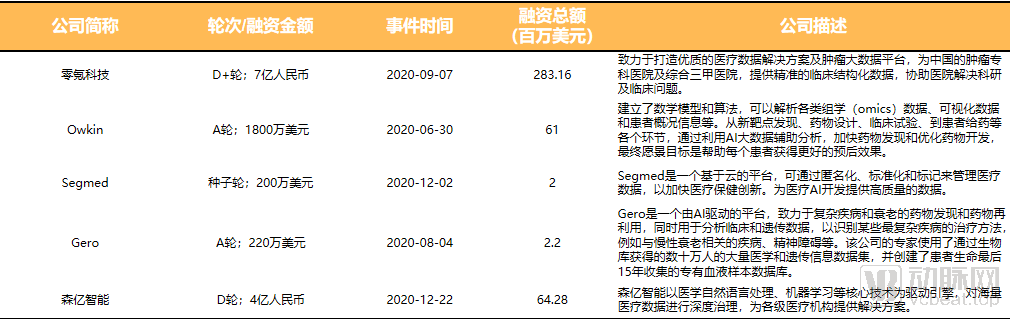

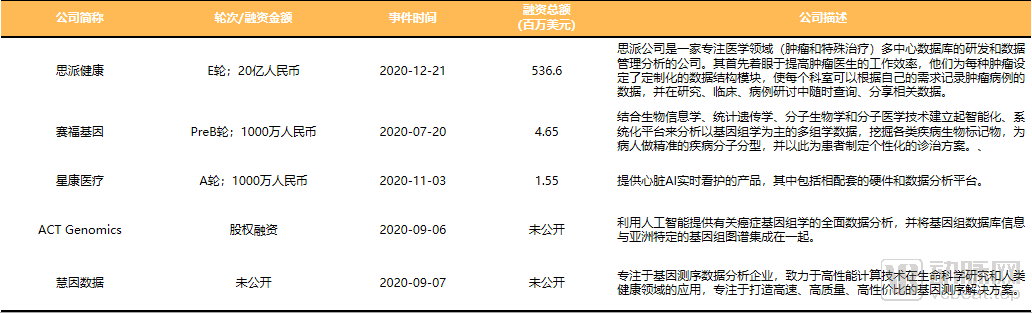

In China, taking genetic big data as an example, Si Pai Health, which focuses on genetic big data, has taken the lead in breaking through, completing its Series E financing and moving one step closer to going public; meanwhile, this niche sector has also attracted startups backed by technological infrastructure, with companies such as Saifu Gene and Xingkang Medical completing new rounds of financing in 2020, injecting fresh blood into the market.

III. Major Events and High-Value Companies in Global Healthcare Big Data Trends for 2020