Where Is the Next Billion-Dollar Market in Healthcare IT? An Analysis of China's 22 Medical Informatization Policies

At times, change arrives with such earth-shattering force that it becomes difficult to discern at a glance whether it spells disaster or opportunity.

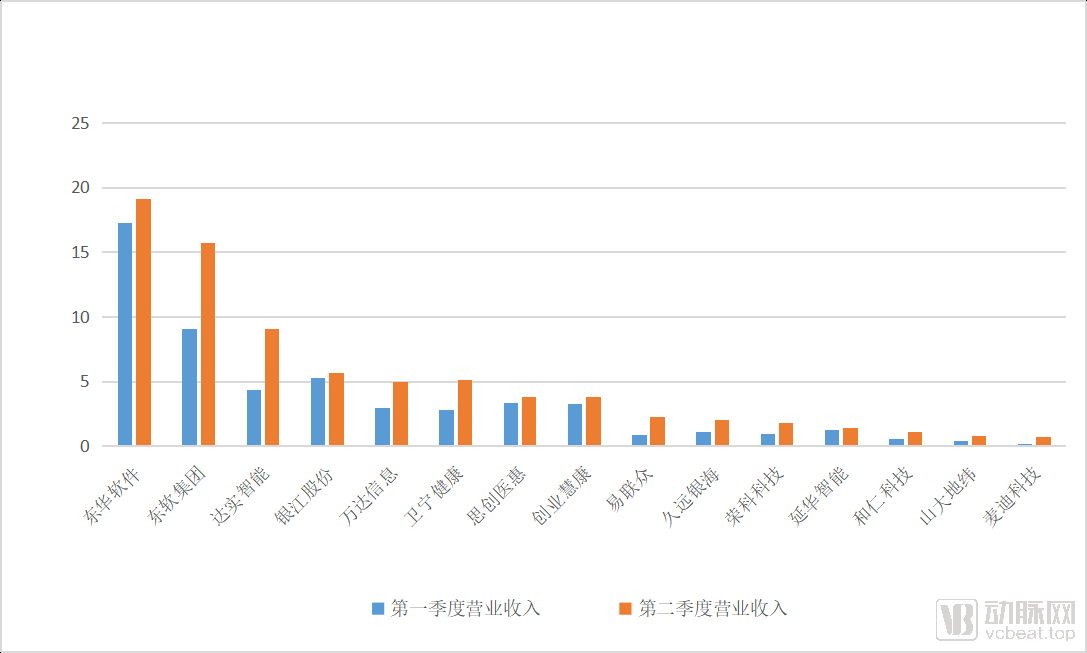

In early 2020, an unusual epidemic rapidly swept across the globe, and the boom in healthcare informatization construction cooled down sharply due to personnel isolation. After the first-quarter financial reports were released, more than half of the few dozen listed informatization companies reported losses.

However, the ultimate outcome is not always what it seems. While the pandemic indeed halted the construction of physical hospitals, it also served as a catalyst, making hospital administrators acutely aware of the numerous shortcomings of traditional health information systems. Coupled with policy-driven initiatives, this has sparked a sweeping transformation in healthcare informatics.

Hospital information technology (IT) infrastructure resembles a public good: hospitals bear the costs, while the benefits of digitalization are enjoyed by all. Although hospitals stand to gain from IT investments in the long run, for most ordinary hospitals, the opportunity costs and risks associated with deferred returns have become major barriers to proactively pursuing digital transformation. Only a small number of large, tertiary Grade A hospitals with stable cash flows are willing to deviate from government guidance and engage in innovative initiatives. Therefore, it is undeniable that policy remains the primary driver of healthcare IT development.

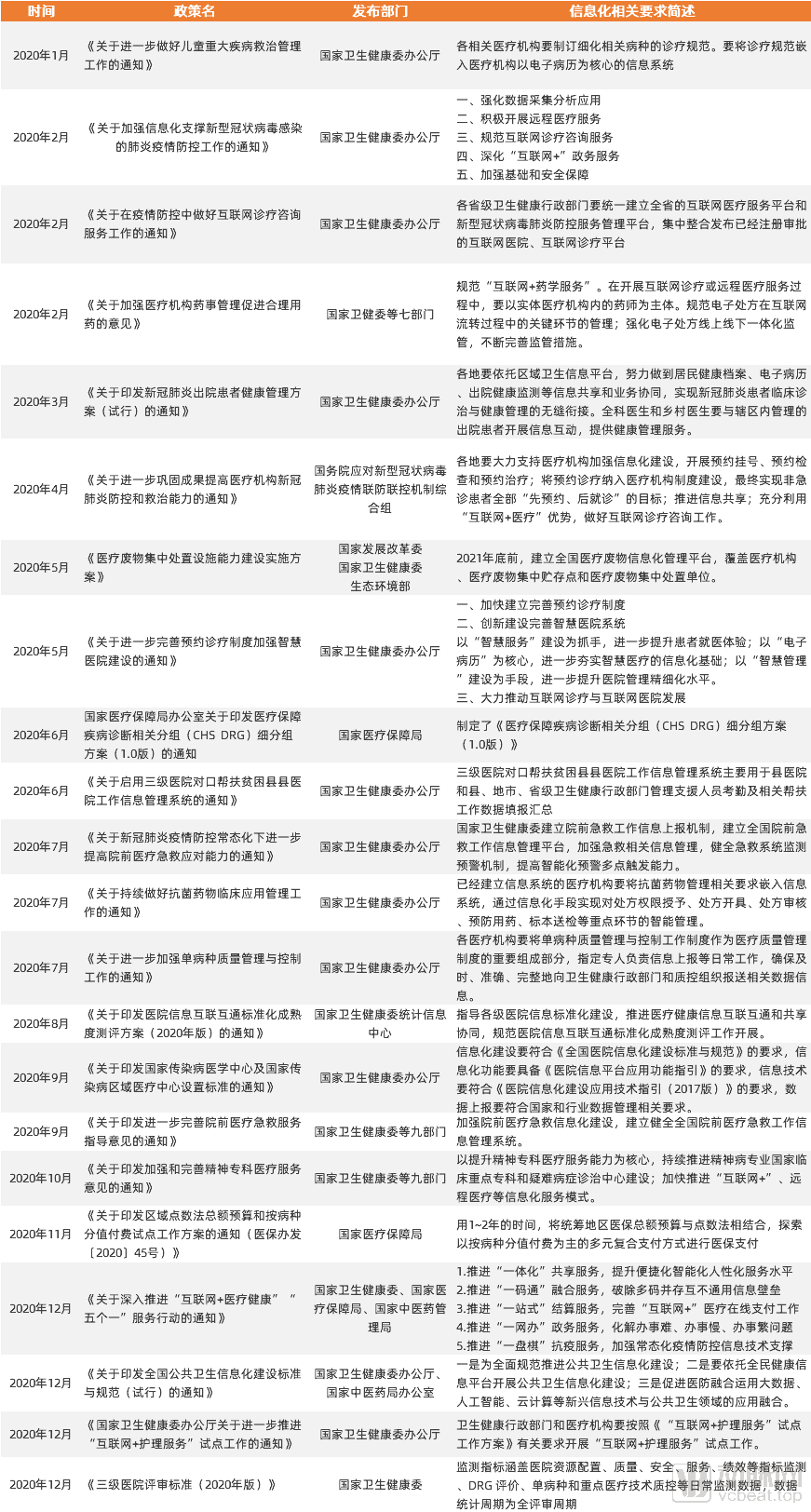

Looking back at 2020, a total of 22 policies outlined the challenges and reform directions in healthcare informatization from multiple perspectives. Most of these policies pertained to foundational infrastructure for informatization, while also covering health insurance payment reforms such as DRG (Diagnosis-Related Groups) and DIP (Big Data Diagnosis-Intervention Packet), public health informatization development, and standard-setting initiatives including tertiary hospital accreditation criteria. VCBeat has summarized these policies as follows.

Analyzing the overall policy trajectory, we can broadly categorize the development of healthcare informatization into five main threads: first, the upgrading of information infrastructure based on interoperability ratings; second, the construction of foundational information systems centered on specific clinical scenarios; third, payment system reforms driven by DRG and DIP; fourth, HIS upgrades spurred by policy implementation; and fifth, data collection and reporting aligned with the performance evaluation of tertiary public hospitals.

Interconnectivity construction serves as the bridge between medical databases and various in-hospital applications, aiming to aggregate medical information across an entire hospital or region. The scope of the hub’s capabilities determines the depth of a hospital’s digitalization and intelligence, while the continuous advancement of information technology constantly expands these capabilities. Therefore, interconnectivity construction is essential and unending.

In August 2020, the Statistical Information Center of the National Health Commission issued the “Standardization Maturity Assessment Scheme for Interconnectivity of Regional Population Health Information (2020 Edition)” and the “Standardization Maturity Assessment Scheme for Interconnectivity of Hospital Information (2020 Edition),” which detailed the new objectives for in-hospital information infrastructure development in the next phase and broadly outlined its future direction. Compared with the 2017 standards, we identified three key differences.

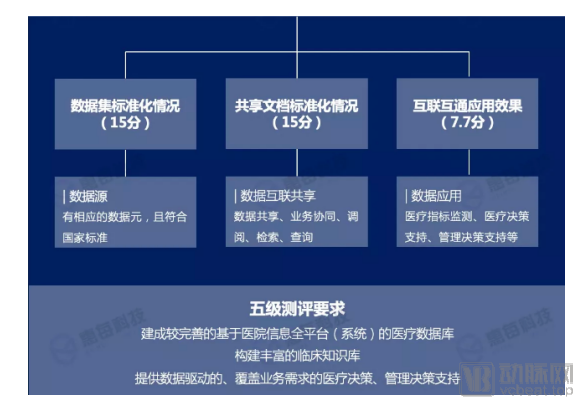

Requirements for the Application of Data and Data Intelligence in the 2020 Edition

First, there are significant changes in both the assessment process and content. The assessment environment has shifted from laboratory simulations to actual production environments. Furthermore, the hospital information platform (or system) under evaluation must hold a Software Copyright Certificate, have been in operation for more than one year, and have passed preliminary acceptance. This indicates that the focus of the new version of the assessment has shifted from "methodology" to "practicality."

Secondly, previous assessments were mostly conducted by third-party testing agencies. However, under the new framework, these third-party agencies have been excluded, with review responsibilities transferred to national and authorized tiered management bodies. Furthermore, the new tiered management mechanism more clearly defines the responsibilities and coordination mechanisms between national and local tiered management bodies. Assessment tasks for Grade 4A and below are directly delegated to the tiered management bodies for determination, while applications for Grade 5 and above must be submitted to the national-level management authority.

Finally, the standardization and application of “medical data” have increasingly become the “sinew” guiding hospital informatization at the national level. The new assessment framework strengthens the intelligent application of big data and the adoption of emerging artificial intelligence technologies, imposing higher requirements on the coverage (completeness) and standardization (accuracy) of hospital operational data. Transforming the once-accumulated piles of in-hospital medical data into actionable “knowledge” is set to become a “standard” capability for hospitals.

Nowadays, many hospitals have already reached the Level 4A or even Level 5B standards, which means that the era of a rapidly expanding rating market is over. Under the demand for high-level ratings, interoperability certification has become a service with high technical barriers. Currently, only a few companies such as Ewell Technology, Winning Health, B-Soft, Peking University Medical Information, Huimei Technology, and Senyi Intelligence provide mature solutions in this market.

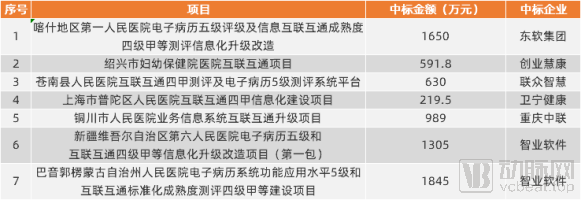

Publicly Disclosed Bid Winning Results for Interconnectivity in 2020 (Partial)

How large is this market? In the 2019 assessment results for the standardization maturity of interoperability, a total of 31 regions participated in the evaluation, and 164 hospitals were rated at Level 4 Grade B or above. There are not many publicly available bidding data; the average winning bid amount for the three tiers—Level 4 Grade A, Level 4 Grade B, and Level 5 Grade B—was RMB 10.84 million. Based on this data, it is roughly estimated that the interoperability market will exceed RMB 2.5 billion in 2021.

The February 2020 “Opinions on Strengthening Pharmaceutical Affairs Management in Medical Institutions to Promote Rational Drug Use,” the July “Notice on Continuously Improving the Clinical Application Management of Antibacterial Drugs,” the September “Notice on Issuing the Guiding Opinions on Further Improving Pre-hospital Emergency Medical Services,” and the October “Notice on Issuing the Opinions on Strengthening and Improving Psychiatric Specialist Medical Services,” among other policies, all signal that medical information infrastructure development has expanded from central hubs to regional levels, with smart healthcare solutions being implemented in specific departments and for specific diseases.

Compared to departments such as outpatient and surgical units, which have seen substantial investment in information system development and achieve high efficiency in data collection, other departments often suffer from data vacuums due to inadequate oversight. This makes it difficult for the National Health Commission to obtain a reasonable evaluation of relevant hospital departments based on reported data, thereby leading to policy ineffectiveness. For instance, when a decline in the drug-to-revenue ratio adversely affects the interests of certain groups within hospitals, these groups tend to shift revenue generation from strictly regulated medical processes to those lacking effective supervision. Consequently, this results in continuous increases in expenditures on antimicrobial agents, oncology drugs, and diagnostic tests. Therefore, to effectively control in-hospital costs, it is essential to strengthen information technology infrastructure in every fundamental operational link, ensuring the rationality of diagnosis and treatment across the board.

To further deepen the diagnostic and treatment process, the National Health Commission officially released the "Notice on Further Strengthening Quality Management and Control of Single Diseases" (hereinafter referred to as the "Notice") in July 2020. Compared with the past, the number of monitored diseases increased from 13 to 51, and the number of data reporting items increased from 111 to over 7,000. Furthermore, the "Notice" requires that hospitals at the secondary level or above must report all data information related to the monitored diseases conducted by their institution within 10 working days after completing the diagnosis and treatment of each relevant case.

Under this policy, the hospital’s Medical Affairs Department and Information Technology Department will primarily face three challenges: a large volume of data items to collect and report, cumbersome entries, insufficient data quality, and poor process oversight.

Addressing these three issues is not difficult. For hospitals that already have effective single-disease quality control protocols in place, the IT department can recruit talent to develop custom code for data reporting. In contrast, for hospitals lacking such quality control processes, purchasing a comprehensive solution from healthcare IT vendors may be a better option.

Taking Jiande First People’s Hospital as an example, after replacing manual screening and automatic reporting of full-volume data with the Huimei Single-Disease Quality Control Reporting System, clinical reporting efficiency increased by up to approximately 66.67%, and reporting accuracy (data extraction quality) exceeded 95%.

Huai'an Second People's Hospital has similarly benefited from this. According to feedback from physicians,In 2020, the hospital had over 15,000 cases to report. The fastest time to report one case was 20 minutes, with an average of 30 minutes per case. The reporting process was extremely time-consuming, resulting in a substantial workload. Since the National Health Commission issued the "Notice on Single-Disease Management and Control" in July 2020, the hospital has mobilized physicians from all departments to submit case reports via the national external web portal. Due to limited reporting efficiency, only 552 cases were reported over a period of more than four months.

After the launch of Senyi Intelligent's single-disease intelligent system, merelyWithin four days, healthcare personnel reported 3,455 cases, with an average of nearly 900 reports per day. In comparison, the current daily average number of cases reported by hospitals is approximately 138 times higher than before.

However, from a long-term perspective, as an increasing number of single-disease conditions fall within the scope of mandatory reporting, the core of this market will shift toward personalized solutions for specific diseases, such as the currently mature VTE quality control systems. To achieve connotative quality control for each disease condition, health IT enterprises must gain an in-depth understanding of every clinical scenario. Consequently, how to reduce the development costs for new scenarios will become a major challenge facing these companies.

Whether DIP or DRG, the goal is to control healthcare insurance costs, but both face the problem of lacking data quality.

To achieve the widespread adoption of DRG, two steps are required: first, establish an effective system for collecting medical record data; second, implement quality control over the collected data to ensure that reimbursement evidence is reasonable and valid.

To date, most hospitals have completed the initial phase of establishing their medical IT systems. However, the data collected during this phase has not adequately met the requirements of Diagnosis-Related Groups (DRG). An analysis of medical record issues reveals that quality defects are primarily attributable to four factors: incomplete completion of the medical record face sheet and improper selection of diagnoses; non-standardized use of medical terminology, resulting in varying descriptions for the same disease; overly simplistic progress notes that render physicians’ diagnostic and therapeutic actions untraceable, thereby posing legal risks; and incomplete medical record information. Through its implementation of Clinical Decision Support Systems (CDSS) in hospitals, Huimei Technology has found that data deficiencies and errors at the source are prevalent, manifesting as missing values and mapping errors. On average, some hospitals exhibit 4.73 data defect instances per medical record.

To address the aforementioned four issues, it is essential to both enhance physicians’ efficiency and implement post-hoc quality control of medical records. The key lies in focusing on three core aspects: standardization, digitalization, and effective quality control.

Given that medical records departments have long been situated in peripheral areas of hospitals and suffer from insufficient human resources, the first step for many small and medium-sized hospitals is to procure various software and hardware solutions to achieve paperless and standardized entry of medical record data. Typically, investment at this stage ranges from RMB 50,000 to 200,000, with a short implementation cycle; the primary challenges faced are talent shortages and institutional neglect of the department.

With the infrastructure in place, the second step involves analyzing and uploading medical record data, a stage at which a large number of hospital medical records departments currently find themselves. This phase also faces a shortage of talent, with demands extending beyond mere quantity to encompass quality as well. To meet this need, health IT vendors offer solutions priced between RMB 200,000 and RMB 1 million.

As national requirements for medical records become more stringent, standardized and digital data entry still face inherent limitations. After all, the completion of medical records is highly complex; information systems vary across specialties, there is a lack of standardized terminology guidelines, and medical knowledge itself is both broad and intricate. A single symptom can often suggest multiple potential etiologies. These factors collectively contribute to fundamental issues in the quality and reliability of medical record data.

Under these circumstances, intelligent medical record systems have become virtually the only viable option for hospitals to meet the national data entry requirements (rule-based recommendations often fail to cover all possible scenarios, necessitating the use of NLP technology). According to bidding data, the average unit price for such products typically ranges in the millions of yuan. There are few enterprises engaged in related R&D, and current demand remains limited. However, as the development of medical record systems progresses, the market size in the third phase is expected to expand continuously.

Publicly Disclosed Bid Award Results for Interconnectivity in 2020 (Partial)

Overall, the medical record market is characterized by fragmented operations, low average transaction value, and a large customer base. Based on these factors, the current market size for medical records is estimated at approximately RMB 10 billion. However, as the development of medical record systems deepens, there remains significant room for future market growth. In contrast, while Diagnosis-Related Groups (DRG) represent a major industry trend, corporate participation is limited in scope, resulting in a similarly constrained market size.

HIS upgrade services have long been available, but with the emergence of disruptive technologies such as AI and 5G in recent years, the patchwork fixes applied to legacy integration architectures can no longer meet the demands of ever-proliferating applications.

Specifically, the lack of flexibility in IT architecture caused by rigid application architecture and non-standardized data management; the significant gap between big health and medical data and the resulting "knowledge" and "medical skills"; the management challenges brought about by the surge in diversity of hospital IT services; the challenges faced by medical staff regarding the portability of operating systems across multiple systems; and more critically, the requirements for data storage and interoperability in the interconnectivity rating.

All these issues require fundamental solutions from medical IT, but the continuous iteration of technology alone has not been sufficient to drive hospitals to make substantial investments in informatization. The true catalyst that has forced hospitals to make decisive choices is the pandemic.

Taking NovaTech’s next-generation Hospital Information System (HIS), VarMix, as an example, the system is designed around a “data-centric” approach. By adopting a middle-platform architecture, it decouples four key components—the business platform, technology platform, real-time exchange platform, and foundational business applications—enabling each module to be backed up and upgraded independently. In terms of data services, the system supports WS445 and WS500, which are essential for achieving interoperability certification, thereby facilitating data storage and exchange across various systems.

Winning Health’s WiNex emphasizes the “middle-platform model,” which dismantles previously redundant integrated information systems, reclassifies complex business-module-based systems, and consolidates them into three interconnected platforms: the technology middle platform, the data middle platform, and the business middle platform, ultimately achieving an optimal solution for business collaboration and data integration.

Sichuan Medwin emphasizes intelligent micro-architecture, aiming to build the “Android” of the healthcare industry. Specifically, the company has further developed its mature open architecture into a microservices framework system, decomposing previously integrated systems into independent micro-modules with clear business boundaries. By reconstructing hospital business systems using a microservices framework and functionalizing services, it enables rapid deployment, refactoring, and one-stop lifecycle management of hospital operations. This approach supports personalized and specialty-specific applications in medical informatics, thereby enhancing user experience.

Many enterprises have developed cloud-based Hospital Information System (HIS) models. Characterized by convenient and rapid deployment as well as strong targeted applicability, this model has demonstrated significant effectiveness in makeshift hospitals and is also widely adopted in private hospitals and primary healthcare settings. However, due to data security concerns, the current cloud storage model still requires further exploration.

From a market perspective, the market share of HIS systems was around RMB 5 billion in 2019, with a compound annual growth rate (CAGR) of approximately 18%. The new generation of HIS systems is expected to further accelerate the expansion of the market size on this basis. If upgrading from an existing HIS system, the cost for purchasing a new-generation HIS system would be around RMB 1 million; however, if deploying a completely new HIS system, the cost could reach several million yuan. Cost factors may hinder the sales of this system.

The performance appraisal of tertiary public hospitals can be regarded as an incentive mechanism for hospital development, serving both as a guideline for the management and growth of tertiary hospitals and as a benchmark for future assessments of secondary hospitals. However, based on the implementation in the first year, certain limitations of the performance appraisal system have become apparent.

From the perspective of final rankings, many hospitals that are not outstanding in specialty development and informatization levels still rank among the top. Some physicians have stated that due to limitations in data submission practices, numerous hospitals’ exam-oriented strategies have enabled them to secure high scores effectively.

Therefore, the performance appraisal system for the new year has optimized the evaluation process and specified detailed requirements for assessment targets in subsequent policies. Baidu Lingyi Zhihui told VCBeat: “Taking medical record quality control as an example, the 2020 performance appraisal of tertiary public hospitals included random inspections of hospital medical records. However, such spot checks are limited by sample bias, and future assessment indicators will become increasingly complex. This means that to shift from inspection-based practices centered on ‘educating hospitals’ to daily operations centered on ‘quality control,’ it is essential to introduce next-generation information processing methods such as Natural Language Processing (NLP).”

Although no definitive products have yet emerged, companies have begun designing standardized solutions for performance appraisal in response to clear market demand; the ultimate market size remains to be validated over time.

Reviewing the five areas, we can summarize the following trends:

I. Regardless of the specific direction, AI-driven intelligence has become a shared objective for development across numerous health informatics sectors. Both tertiary hospitals and primary healthcare institutions have benefited from advancements in AI.

II. The trend toward intelligentization is driving the continuous specialization of services offered by information technology companies. In this context, traditional IT enterprises need to accelerate technological R&D or collaborate with next-generation information technology firms. Small regional IT companies may be eliminated due to a lack of specialization, leading to market consolidation.

3. The niche yet promising smart medical record sector, bolstered by policy support, has already achieved a market scale of millions. Coupled with the analytics market following data standardization, this sector is poised to become the most likely candidate to break through a trillion-yuan market valuation in the future.

Overall, the development of healthcare informatization will never stagnate. Clarifying how to interpret policies, understand hospital needs, and thereby formulate future development strategies remains the most critical step for all medical IT enterprises at present.