2020 Global Healthcare and Life Sciences Report: Annual Transactions Surpass $45 Billion, Embracing Innovation to Navigate a Volatile Landscape

2020 was the year when investment enthusiasm in the healthcare market was fully ignited. Unlike other industries that faced severe challenges, China’s healthcare sector instead surged amid the pandemic—private equity financing, IPOs, and M&A transaction volumes reached an unprecedented high of over $45 billion for the full year. This remarkable achievement would not have been possible without the dedication and efforts of all entrepreneurs, investors, and investment banks.

While fueling a surge in capital investment, China’s healthcare industry is also confronting increasingly fierce competition in the global market. For medical enterprises across various specialized sectors, it is imperative to promptly master core underlying technologies and pursue innovative upgrades. Grounded in the present and looking toward the future, how should the healthcare industry define innovation and upgrading in this new era? What new trends and turning points will emerge in the industry’s development?

At a time when all things are being renewed, the Huaxing Medical team, deeply rooted in the industry, continues its tradition. Starting from the four major fields of pharmaceuticals and biotechnology, IVD, medical devices, and smart healthcare, as well as the performance of capital market transactions throughout the year, we will review the development trends in the global healthcare sector in 2020 and look forward to a broader future of innovation and upgrading in the healthcare field.

Induced Pluripotent Stem Cell-Engineered NK Cell Therapy (iPSC-NK)

In 2017, the FDA successively approved Kymriah and Yescarta for marketing, ushering in the inaugural year of cell therapy represented by CAR-T. In 2020, a wave of initial public offerings swept through numerous domestic cell therapy companies, including Legend Biotech, Yongtai Biopharma, and JW Therapeutics, marking a new chapter in the close integration of China’s cell therapy sector with capital markets.

Subsequently, at the end of 2020, the field of cell therapy sounded the charge for NK cell therapy. A landmark event occurred at the 62nd American Society of Hematology Annual Meeting (ASH 2020): Fate Therapeutics, a U.S. biotechnology company focused on induced pluripotent stem cell-derived NK cell therapies (iPSC-NK), announced early clinical data for two of its iPSC-NK cell products. The remarkable efficacy and safety profile greatly encouraged the industry, leading to a nearly 40% surge in Fate Therapeutics’ stock price.

Moreover, under a global collaboration agreement with Janssen reached in April 2020, Fate Therapeutics received a $50 million upfront payment and $50 million in equity investment, and is also eligible for up to $3 billion in potential milestone payments. This deal was ranked among the Top 10 Global Biopharmaceutical Deals of 2020.

Why Has iPSC-NK Cell Therapy Generated Significant Industry Buzz? What Are Its Technical Advantages and Clinical Application Potential? Building on our understanding of CAR-T cell therapy, we will provide a concise analysis of iPSC-NK cells from the following two dimensions:

Why Are iPSCs Needed?

Currently, cell therapy is predominantly based on autologous treatments, which are limited by challenges such as lack of scalability, low engineering efficiency, limited cell availability, and cellular heterogeneity. Consequently, the field faces significant industrialization hurdles in areas including manufacturing quality control, clinical trial applications, safety, and cost management.

Currently, the relatively ideal improvement strategy is to leverage stem cells to obtain standardized, off-the-shelf cell products. Within the realm of stem cells, induced pluripotent stem cells (iPSCs) are considered the most optimal technical approach, as they avoid the ethical concerns associated with embryonic stem cells and the source limitations of adult stem cells, while also possessing robust differentiation and engineering potential.

Why Are NK Cells Needed?

Currently, cell therapy is primarily based on cytotoxic T cells. A new study published in the journal Cell in December 2020 found that cytotoxic T cells typically remain in the bloodstream and do not enter organs and other tissues. This finding partly explains why CAR-T therapy is ineffective against solid tumors and why certain pathogenic viruses (such as HIV and SARS-CoV-2) can indefinitely evade immune cell attack by relying on systems outside the bloodstream.

NK cells are a crucial component of innate immunity and serve as the first line of defense in the immune system. Theoretically, they do not cause graft-versus-host disease (GVHD), making them natural off-the-shelf therapeutic candidates. Furthermore, NK cells can function immediately within the tumor microenvironment of solid tumors, acting as pioneers for T-cell activation. More importantly, through CAR engineering for targeting and fine-tuning, NK cells allow for more precise definition of clinical indications in both oncology and viral infectious diseases. Additionally, they are less prone to adverse effects such as cytokine release syndrome (CRS) and neurotoxicity commonly associated with CAR-T therapy.

As the old saying goes, “To do a good job, one must first sharpen one’s tools.” By leveraging iPSCs as the interface tool for industrialization, NK cells as the interface tool for clinical applications, and CARs to unleash the biotechnological imagination of genetic engineering, iPSC-(CAR)-NK has emerged. Individually, each component belongs to history; together, they represent the future.

For example, the current ex-factory price of CAR-T cell therapy is $400,000–$500,000, whereas Fate Therapeutics’ current technology can achieve a cost of $3,000 per dose, with the ex-factory price of off-the-shelf products at only $20,000–$30,000, leaving room for further cost reductions in the future. Global Info Research released the latest market information on NK cell therapy in late September 2020, predicting that the market size would reach $630 million by 2025, with a compound annual growth rate (CAGR) of 16.4% from 2018 to 2025. However, this report did not incorporate other data, including those presented at ASH 2020, suggesting additional potential for market growth. Although delayed in arrival, the sector shows robust prospects, and the field of cell therapy may undergo a profound transformation in the future.

AI Drug Discovery: Traditional Pharmaceutical Industry Faces Bottlenecks.

In early-stage R&D, development cycles have been lengthening, the overall success rate of innovative drug development has repeatedly hit new lows, and the average investment per new molecular entity (NME) has surged from $300 million in 1995 to $1.3 billion in 2020. In clinical development, patient recruitment is inefficient, challenging, and costly. Given these industry pain points, the integration of AI appears to be a natural progression:

· AI assistance is poised to discover new targets by leveraging its higher-dimensional understanding of biology, and to conduct high-throughput drug screening and optimization to enhance R&D efficiency;

· Reduce the time, cost, and uncertainty in experimental planning through automated selection, operation, and analysis, as well as by leveraging robotic cloud laboratories for sample analysis;

· For difficult-to-drug targets, leverage high-performance computing, efficient algorithms, and high-quality databases to efficiently optimize drug molecules.

In the realm of clinical trials, the integration of AI technology can effectively address many of the current pain points:

· By integrating patients' electronic health records and extracting medical history information, match patients with suitable clinical trials to reduce recruitment costs in terms of both funding and time;

· Digitize real-world and massive clinical trial data, and leverage AI for data mining to design clinical trials that are more efficient and better balanced in terms of risk;

· Can be applied to virtual clinical trials and the precision development of biomarkers for matching with new indications;

· It can also support post-launch lifecycle management, extending patent protection and the drug’s lifecycle.

From 2016 to 2020, AI-driven drug discovery has garnered increasing attention worldwide, with global pharmaceutical companies becoming more actively involved in the application and investment of AI. A survey by Global Data of CEOs from 156 sample companies worldwide revealed that more than half of the executives believe that AI should be a key strategic focus over the next two years.

Currently, leading global pharmaceutical companies are actively strategizing in the field of AI-driven drug discovery and development, primarily through external collaborations and investments/acquisitions, supplemented by the establishment of in-house teams. In 2020 alone, 28 new collaborative deals emerged, including a three-year partnership between Exscientia and Bayer valued at nearly $300 million, as well as key strategic initiatives such as AstraZeneca’s establishment of an AI-based new drug R&D center in China. Looking domestically, it is encouraging to observe the gradual rise of Chinese pharmaceutical companies and AI-driven drug discovery firms. Domestic pharmaceutical enterprises are not only partnering with international AI companies but also increasingly choosing to collaborate with local AI firms.

Meanwhile, some AI-driven pharmaceutical companies achieved breakthroughs in 2020 and gradually expanded into the international market. XtalPi entered into collaborations with Huadong Medicine, 3SBio, Porton Pharma Solutions, and PhoreMost in 2020, underscoring its leading position in the field of AI-enabled drug discovery. Furthermore, numerous technology companies have also crossed industry boundaries to establish a presence in the AI drug development sector.

They possess mature expertise in building and integrating super-platforms, and are gradually extending this know-how to the field of drug research. In China, ByteDance established the ByteDance AI Lab, Huawei launched its pharmaceutical intelligent agents, Tencent founded Yunshen Zhiyao (Insilico Medicine), Alibaba’s Cloud division partnered with the Global Health Drug Discovery Institute (GHDDI) to develop AI-driven drug discovery and big data platforms, and Baidu established Bioto Life Sciences.

With the accumulation of data and advancements in technology, an increasing number of pharmaceutical companies have begun to strategize their pipeline development and enter the clinical development stage. As of December 2020, among the top 10 AI-driven drug discovery companies in terms of total financing domestically and internationally, seven leading enterprises were either engaged in self-developed pipelines or involved in pipeline development through joint ventures and out-licensing arrangements. Although AI-enabled drug discovery is gaining significant momentum, skepticism persists within the industry regarding its true value. For instance, some argue that Exscientia’s DSP-1181 is merely an analog of haloperidol, and that Insilico Medicine’s DDR1 inhibitor does not feature a entirely novel scaffold.

Furthermore, although pharmaceutical companies are currently engaged in numerous collaborations, there have been few publicly disclosed large-scale transactions. Therefore, their foray into the AI sector can be interpreted as a low-cost trial of emerging technologies. While the concept of AI-driven drug discovery is gaining significant traction in China, apart from leading enterprises such as XtalPi, SiliconCon Medicine, and Insilico Medicine, most other AI drug discovery companies are still being incubated within research institutions and remain some distance away from true commercialization.

In summary, although AI-driven drug discovery is still some way from truly disrupting traditional R&D pathways, given its unparalleled computational power and breakthroughs achieved in other fields, we remain optimistic that AI technology will become an indispensable and critical component of future new drug development.

Spurred by the outbreak and global pandemic of COVID-19, the healthcare and life sciences technology sector became the undisputed focus of market attention in 2020, with the in vitro diagnostics (IVD) segment also receiving strong enthusiasm from capital markets. Judging from transaction activities in both primary and secondary markets, IVD attracted substantial capital inflows in 2020, with private equity financing and initial public offerings (IPOs) advancing side by side and both reaching historic highs.

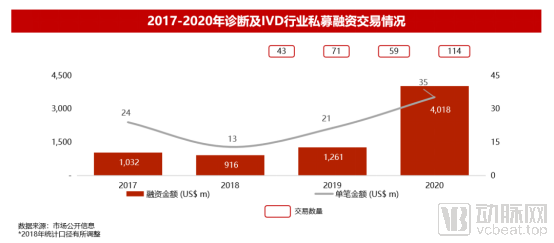

According to statistics, in 2020, both the transaction value and volume in the IVD sector of the private equity financing market reached historic peaks. There were a total of 114 private equity financing transactions throughout the year, representing a nearly twofold year-on-year increase; the total transaction value exceeded $4 billion, up by 219% year on year; and the average funding amount per transaction was approximately $35 million, marking a 66.7% year-on-year growth.

By subsector, genetic testing led by a wide margin in both the number of financing deals and total capital raised, with oncology companion diagnostics and early cancer screening and diagnosis being particularly favored by investors. Among the financed companies, the head effect has become increasingly pronounced. There were seven single deals exceeding $100 million each, accounting for 53% of the total annual financing amount. Notably, MGI Tech secured the largest single deal, raising over $1 billion.

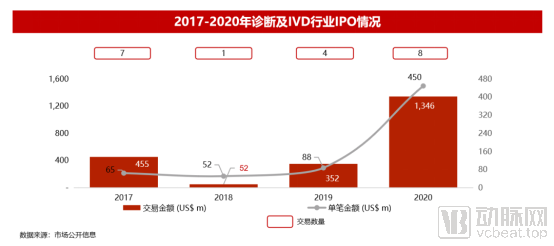

Furthermore, the introduction of new listing rules on the Hong Kong Stock Exchange, the STAR Market, and the ChiNext Board, coupled with improved corporate performance driven by the pandemic and heightened capital market attention to the healthcare sector, have fueled robust trading activity for in vitro diagnostics (IVD) companies in the secondary market. In 2020, eight IVD companies went public, raising a total of over USD 1.3 billion through initial public offerings (IPOs), representing a 282% increase from 2019. Notably, Burning Rock Biotech and Genetron Health listed on the NASDAQ successively, marking a significant milestone in China’s precision diagnosis and treatment of cancer. Additionally, the successful IPOs of COVID-19-related stocks such as Sansure Biotech, Orient Gene, Snibe, and Wantai BioPharm underscored the substantial potential and development opportunities within the industry.

Behind the industry's explosive growth lie three major driving forces:

1. The COVID-19 Pandemic: Overtaking on the Bend Across the Entire IVD Industry Chain

Driven by the substantial demand for COVID-19 prevention and control both in China and globally, the entire IVD (In Vitro Diagnostics) industry chain has experienced rapid development. In particular, sectors related to microbiological testing—including upstream instruments and raw materials, midstream testing products and solutions, and downstream third-party testing services—have become focal points for capital investment. Over the past year, the National Health Commission and the State Council have repeatedly issued directives emphasizing the need to strengthen nucleic acid testing capabilities in primary healthcare institutions, disease control and prevention systems, and regional biosafety testing centers, while also setting forth requirements for the construction of gene amplification laboratories. In the short term, these policies benefit manufacturers of genetic testing instruments and their ancillary equipment. In the long run, novel diagnostic products centered on genetic testing technologies will reach a broader patient base at the primary care level.

Chinese IVD companies responded proactively at the outset of the pandemic, racing against time to develop COVID-19 testing products that empowered global epidemic prevention and control efforts. This not only expanded their footprint in the domestic market but also accelerated their overseas expansion. BGI’s “Fire Eye” laboratories took a leading role on the front lines of the anti-epidemic effort, with coverage across all six continents. To date, 58 Fire Eye laboratories have been established in nearly 17 countries and regions, demonstrating “China speed.” Other companies, such as Sansure Biotech and Fapon Biotech, have also entered a fast lane of development. Sansure Biotech, known as the “first stock of the anti-epidemic campaign,” reported revenue of RMB 3.605 billion in the first three quarters, representing a year-on-year increase of 13.8 times, and net profit of RMB 1.992 billion, a year-on-year surge of 155 times.

The COVID-19 pandemic has elevated attention to pathogenic microorganism testing to unprecedented levels across government, clinical, industrial, and general public sectors. Nucleic acid-based pathogen detection, characterized by its broad pathogen coverage, short turnaround time for reporting, and high detection rates, has demonstrated increasing efficacy in clinical diagnosis and treatment. Since BGI Genomics completed over RMB 500 million in financing at the end of 2019, several peer companies in the industry have also secured financings exceeding RMB 100 million in 2020. We believe that this sector will continue to attract strong investor interest, and companies capable of offering a comprehensive and robust product portfolio that addresses high-, medium-, and low-throughput pathogen testing needs will emerge as winners in the competitive landscape.

Third-party testing agencies have also emerged prominently in this wave. In addition to listed companies KingMed and Dian Diagnostics, whose performance was boosted by COVID-19 testing services and which saw outstanding secondary market performance, other third-party testing institutions that played a significant role in epidemic prevention, such as Huayin Capital and BioCapital Genomics, have also completed substantial financing rounds.

We believe that third-party clinical laboratories will be a key force in enhancing the quality of primary healthcare in the future. Under the guiding principle of “ensuring basic coverage and strengthening primary care,” such enterprises are poised for greater growth opportunities.

2. Decoupling between China and the US, domestic substitution becomes an inevitable trend

Amid an increasingly complex international landscape, a new era of domestic economic circulation and import substitution has arrived across the economy, including the healthcare sector. On one hand, the state is intensifying talent development, research funding, and support for the commercialization of industry-academia-research outcomes in high-end instrumentation. On the other hand, policies are encouraging the R&D and market launch of domestically produced instruments. In tandem with healthcare reforms and volume-based procurement aimed at cost containment, cost-effective domestic medical products can penetrate grassroots healthcare settings and capture larger market shares. In the wave of import substitution, manufacturers of instruments and raw materials previously subject to foreign supply bottlenecks will emerge as two primary driving forces.

Among instrument manufacturers, a typical representative is MGI Tech, which has championed domestically produced high-end life science instruments, drawn intense industry attention, and completed a financing round exceeding $1 billion—a record in the startup world.

In addition, 20,000 domestically produced PCR instruments are sold annually in China, with models from manufacturers such as Shanghai Hongshi, Hangzhou Bioer, and Xi’an Tianlong being in such high demand that they are difficult to obtain.

Among raw material suppliers, companies such as Fapon, Vazyme, and Kangwei Century have successfully secured substantial financing rounds. The quality of diagnostic raw materials is critical to the performance of diagnostic reagents and downstream applications; however, we currently remain heavily reliant on upstream products from overseas giants, such as Roche Diagnostics.

Therefore, we look forward to domestic enterprises gradually building comprehensive technical platforms, enhancing upstream product portfolios, and breaking the monopoly held by foreign companies in the industry.

3. Innovation-Driven: The Oncology Sector Remains a Hot Investment Target

In 2020, within the IVD industry’s financing transactions, genetic testing in the oncology sector—particularly companion diagnostics and early screening and diagnosis—was most favored by capital.

As innovative oncology drug development continues to achieve new breakthroughs, attention toward tumor companion diagnostics companies—critical players in the drug development process—has been steadily increasing. Several leading firms, represented by Genetron Health, completed substantial financing rounds in 2020. Meanwhile, Burning Rock Biotech and Geneseeq successfully conducted overseas initial public offerings (IPOs), raising hundreds of millions of dollars. The sector has demonstrated a pronounced "winner-takes-all" effect across capital, assets, distribution channels, and talent.

Companies in the second tier of the industry can also carve out a niche by cultivating differentiated advantages through deep specialization in vertical fields and refined operational strategies. In the future, enterprises will evolve toward comprehensive disease management across the entire care continuum, where product commercialization capabilities, regulatory compliance, and collaborative R&D with pharmaceutical companies will all influence their standing within the industry.

China’s capital markets have also been influenced by the product advancements and the wave of financing and M&A activity among U.S. peers (Grail, Exact Sciences, ArcherDx), resulting in increased financial support for leading domestic companies in this sector. For instance, both Kangliming and New Horizon Health completed financing rounds amounting to hundreds of millions of RMB in 2020. The industry is currently in the early stages of rapid development; with the approval of single-cancer-type products, it is expected to evolve toward multi-cancer and pan-cancer early screening.

The “post-genomic” era has arrived. Novel diagnostic technologies—including new biomarkers, innovative methodological approaches, and combined testing panels—will bring about transformative changes to the industry. The application scenarios for diagnostics will gradually shift from patients to healthy populations, and medical care will increasingly evolve toward health management.

In emerging diagnostic fields represented by proteomics and metabolomics, single-cell omics, and nanopore sequencing technologies, overseas technological trends strongly guide the development of domestic enterprises. As comparable overseas companies launch mature products and achieve strong performance in capital markets, Chinese firms are encountering new opportunities. In the future, the integration of multi-omics, multi-platform systems, and big data will empower innovative diagnostics, with digital healthcare becoming an inevitable trend.

The COVID-19 pandemic has also transformed many habits and mindsets among the Chinese population, boosting national confidence to an unprecedented level. Consequently, investor confidence in medical device entrepreneurs operating in high-barrier, emerging sectors has surged. Furthermore, the STAR Market and Chapter 18A of the Hong Kong Stock Exchange have opened IPO pathways for a cohort of small yet sophisticated medical device companies. In 2020, the valuation logic and investment preferences within the medical device sector underwent significant shifts. While many investors lamented their inability to commit capital due to soaring valuations, others felt that medical device projects had never been closer to an initial public offering.

In this article, we select three sub-sectors of the medical device industry to elucidate the changes in the device sector in 2020: medical robotics, neurointervention, and structural heart disease.

First, let’s take a look at this set of historical events:

Intuitive, the manufacturer of the da Vinci system, was founded in 1995.

The world’s first percutaneous mitral valve company, Evalve, was founded in 1999.

The world’s first transcatheter aortic valve company, Percutaneous Valve Technologies, was founded in 1999.

Concentric Medical, the world’s first company to develop a mechanical spiral thrombectomy device, was founded in 1999.

……

The most dynamic innovative companies and technological products in the Western world emerged more than two decades ago. In contrast, the leading medical device companies that garnered significant enthusiasm in China’s primary market in 2020 were mostly established after 2010, or even after 2015. Thus, 2020 marked a turning point for the industry. China’s late-mover innovation and manufacturing capabilities finally gained the trust and confidence of investors in three sectors that remain exploratory even on a global scale, thereby accelerating their progress.

Medical Robots

In 2020, China’s private equity market saw more than 30 financing rounds related to medical robots, second only to the cardiovascular and cardiac devices subsector, which has consistently maintained its leading position. Medical robots across various categories cater to the diverse investment preferences of professional institutional investors, including the near-term certainty associated with regulatory approval for hard-tissue surgical robots, the high technical barriers of soft-tissue surgical robots, the practical infection-prevention application scenarios for service robots amid the pandemic, and the proven strong demand for rehabilitation robots in Japan, a neighboring country with an aging population.

The expiration of certain patents for the da Vinci Surgical System, Tinavi’s capital boom, MicroPort MedBot’s RMB 3 billion Series A financing round, and multinational corporations leveraging orthopedic robots to hedge against risks from centralized volume-based procurement of consumables are external factors driving the sudden rise of this industry. However, the true large-scale application of medical robots will still require 5–10 years of hands-on validation by clinicians.

Neurointervention

Like a sudden spring breeze, nearly 30 startups have flooded into the niche field of neurointervention in recent years, with more than 15 securing private equity financing in 2020 alone. Most companies have converged on similar product portfolios focused on ischemic stroke, hemorrhagic stroke, and vascular access solutions; their key differentiators lie in manufacturing sophistication, clinical trial progress, and regulatory approval speed.

Thereafter, the high-level balance required in craftsmanship, materials, and mechanics for neurointerventional consumables—described as “performing a grand ritual in a snail’s shell”—will likely serve as the touchstone for gaining clinical trust and achieving widespread adoption after regulatory approval. It is expected that by 2021, the market will see nearly ten thrombectomy stents receive regulatory clearance, with capital attention gradually shifting toward aspiration catheters, flow diverter stents, and even back to coils. Capital markets are also increasingly accepting that superior craftsmanship may originate from the United States, Japan, or Israel, no longer insisting on mandatory local independent innovation.

Structural Heart Disease

The successive IPOs of Venus Medtech, Peijia Medical, and MicroPort CardioFlow have popularized institutional investors’ understanding of transcatheter heart valves. In 2020, as the aortic valve sector (TAVR) became increasingly crowded, industry spotlight shifted to new blue-ocean areas—mitral valve (MV) and tricuspid valve (TV) repair and replacement.

On January 30, 2020, Abbott’s Tendyne transcatheter mitral valve replacement system received CE approval; on June 15, 2020, Abbott’s MitraClip mitral valve repair system was approved for market launch in China. The gradual introduction of these blockbuster products in the global mitral valve field has ignited enthusiasm among Chinese investors. Domestic companies developing mitral valve replacement technologies (Nuomai, Yixin Medical, Jian Shi Medical, and Peijia Medical) and those focused on mitral valve repair (Dejin Medical, Hanyu Medical, Kokai Medical, Shenqi Medical, and Puchuang Medical) have successively entered the scene, narrowing the R&D gap between China and Western markets to less than five years. In contrast, tricuspid valve repair and replacement remain at a relatively earlier stage, with only Jian Shi Medical and Dejin Medical having initiated clinical trials.

Multiple products are in clinical development both domestically and internationally. Similar to the biopharmaceutical sector, domestic brands benefit from a late-mover advantage. Meanwhile, technological pathways in the overseas structural heart disease field are becoming increasingly clear. In addition to the conventional hotspots in China, such as transcatheter interventions for the aortic and mitral valves, tricuspid valve interventions and cardiac assist devices are attracting greater capital attention. Abbott’s tricuspid valve repair product, TriClip, was launched in Europe in 2020, drawing increased capital inflow due to the large patient population affected by this condition.

European and American companies such as Abbott, Edwards, and Trialign are prioritizing the development of their product pipelines. In the field of cardiac assist devices, Medtronic’s HeartWare (FDA-approved in 2018) and Abbott’s HeartMate (FDA-approved in 2020) have driven a surge in capital investment. Recently, French developer CorWave announced the completion of a $40 million Series C financing round to accelerate initial product development and initiate human clinical trials. Domestic startups such as Tongxin Medical, Magenta Medical (Xinqing), and Shenzhen Core Medical have all entered early-stage financing rounds. By leveraging existing advancements in Europe and the United States, China can significantly save time and labor costs. Coupled with advantages in clinical trial costs, Chinese manufacturing is well-positioned to achieve overtaking growth in the future.

Capital Markets Reignite the Battle

The COVID-19 outbreak in early 2020 subjected China’s healthcare system to an unprecedented stress test. While further underscoring the critical importance of the healthcare sector, it also highlighted growing demands for remote, contactless care and enhanced efficiency across the entire diagnosis and treatment workflow. These needs have since shaped the development trajectory of the healthcare system in the post-pandemic era, creating transformative opportunities for internet healthcare and smart healthcare industries. In response, relevant companies have ramped up their efforts, emerging as pioneers in the technological fight against the epidemic.

In the secondary market, JD Health (06618.HK), after its listing on the Hong Kong Stock Exchange in December 2020, has joined Alibaba Health (00241.HK) and Ping An Good Doctor (01833.HK) in leading the internet healthcare sector. In the field of medical big data, Yidu Cloud (02158.HK) submitted its IPO application to the Hong Kong Stock Exchange in September 2020 and successfully listed in January 2021. In the artificial intelligence sector, following Cambricon’s (688256.SH) pioneering listing in July 2020, five AI companies—Unisound, Yitu Technology, CloudWalk Technology, Intellifusion, and DeepGlint—have advanced their IPOs to a substantive stage. Among them, Unisound and Yitu Technology have both made in-depth layouts in the smart healthcare industry.

Moreover, in 2020, several leading enterprises in the fields of AI medical imaging and healthcare big data secured substantial financing rounds. Many of these companies are poised to become major contenders for listing on secondary markets within the next two years.

Following the approval of the first Class III medical device certificate for AI healthcare by the National Medical Products Administration (NMPA) in January 2020, the regulatory approval process accelerated significantly. In 2020, a total of nine Class III certificates were granted to Keya Medical, Lepu Medical, Ande Yizhi, Airdoc, Silicon Intelligence, Shukun Technology, Infervision, United Imaging Intelligence, and Deepwise Healthcare, igniting enthusiasm in the capital market for this sector. Many leading AI medical imaging companies secured substantial financing in 2020, with the cardiovascular sub-sector of AI medical imaging—where companies such as Keya Medical, Shukun Technology, and Ruixin Intelligence operate—garnering particular attention and accounting for more than half of the total financing amount.

In October 2020, cardiovascular stents were included in the national volume-based procurement (VBP) program in China. Following the VBP, prices for cardiovascular stents plummeted by more than 90%, accelerating the transformation of in-hospital cardiovascular diagnosis and treatment practices. Hospitals and physicians are shifting away from past reliance on consumables toward placing greater emphasis on precise pre-treatment diagnosis, thereby creating opportunities for the widespread adoption of fractional flow reserve (FFR) for functional assessment.

Fractional Flow Reserve (FFR)

In clinical cardiovascular practice in China, the need for coronary stent placement is typically determined via coronary angiography. If moderate-to-severe coronary stenosis is present, clinicians usually opt for percutaneous coronary intervention (PCI) with stent implantation. However, the actual impact of such stenosis on distal blood flow (functional assessment) and whether it causes myocardial ischemia remain unclear, potentially leading to overestimation or underestimation of lesion severity. As a functional indicator for assessing coronary hemodynamics, fractional flow reserve (FFR) has become an accepted metric for guiding PCI by measuring pressure changes across coronary stenoses, and it has been incorporated into the guidelines for the diagnosis and treatment of coronary artery disease in the United States.

FFR can be categorized into invasive FFR measurements based on pressure wires or microcatheters (invasive, more accurate) and non-invasive or minimally invasive imaging-based FFR measurements. Among these, invasive FFR measurement using pressure wires primarily involves high-value consumable products, which were previously monopolized by foreign manufacturers such as Abbott and Philips. In 2020, the FFR microcatheter developed by the Chinese manufacturer LifeTech Scientific received the first NMPA Class III certification for a domestically produced FFR device, providing clinicians with more options for FFR measurements. Imaging-based FFR can be further divided into CT-FFR based on coronary CTA, QFR (also known as FFRAngio) based on coronary angiography, and UFR/OFR (also known as FFRIVUS and FFROCT) based on IVUS or OCT.

CT-FFR has been extensively studied by the research and clinical communities due to its non-invasive nature and lower cost. CT-FFR products from Keya Medical and Shukun Technology have previously been widely promoted in multiple countries by comparable U.S. products (HeartFlow), with both their clinical and commercial value successfully validated. In addition, companies such as Pulse Medical Imaging and Runmai De have obtained Class III certification from the National Medical Products Administration (NMPA) for their angiography-based FFR-angio products.

In 2021, we anticipate significant advancements from leading companies in the field of Fractional Flow Reserve (FFR).

First, the CRP medical team summarized transaction activities in 2020 across five major sectors: pharmaceuticals and biotechnology, medical devices, diagnostics and IVD, smart healthcare, and healthcare services. Through intuitive data, we aim to provide a quick overview of the transaction volume and market vitality in these industries over the past year.

Pharmaceuticals and Biotechnology

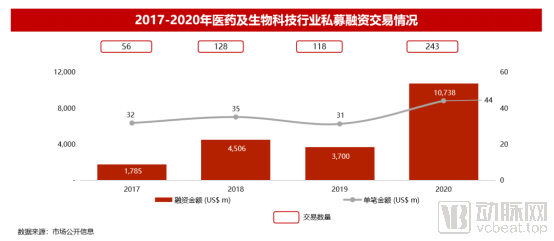

In 2020, private equity financing in the pharmaceutical and biotechnology sectors flourished, with a total of 243 transactions recorded for the year, representing a year-on-year increase of over 100%. The total financing amount exceeded USD 10.7 billion, a year-on-year growth of approximately 190%, while the average size per financing round was around USD 44 million, marking a year-on-year increase of about 42%.

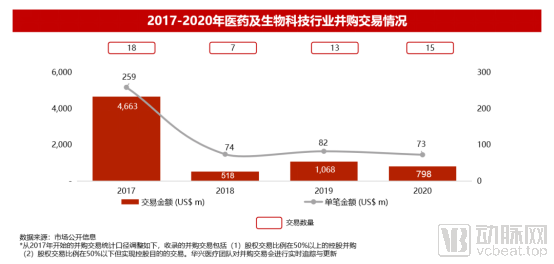

There were a total of 15 mergers and acquisitions (M&A) transactions in the pharmaceutical and biotechnology sectors throughout the year, representing a year-on-year increase of approximately 15%. The total transaction value amounted to nearly USD 800 million, a year-on-year decrease of approximately 25%. The average transaction value per deal was approximately USD 73 million, reflecting a year-on-year decline of approximately 11%.

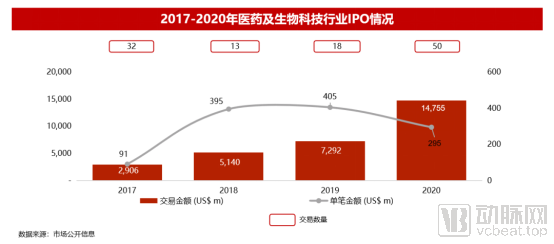

In terms of IPOs, more than 50 companies went public throughout the year, double the number in 2018; the total amount of IPO financing exceeded $14.7 billion, a year-on-year increase of approximately 102%; the average financing size per IPO was about $300 million, a year-on-year decrease of 27%.

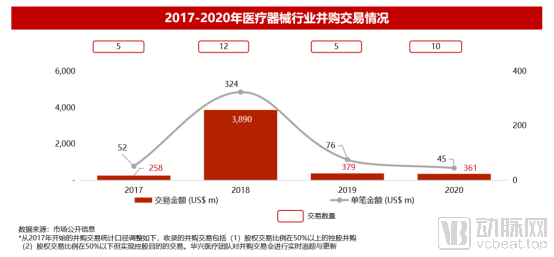

Medical Devices

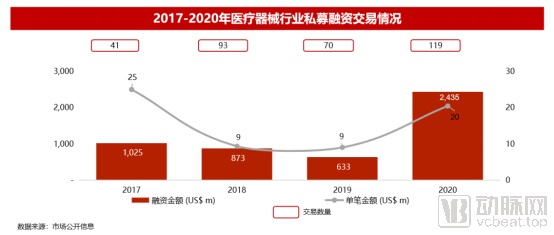

In 2020, there were 119 private equity financing transactions in the medical device sector, a year-on-year increase of 70%; the total financing amount exceeded US$2.4 billion, a year-on-year increase of nearly 300%; the average financing size per transaction was approximately US$20 million, more than doubling year on year.

A total of 10 M&A transactions occurred in the medical device sector throughout the year, representing a year-on-year doubling; the total transaction value was approximately USD 360 million, with an average deal size of around USD 45 million. Both the total transaction value and the average deal size declined compared to 2019 levels.

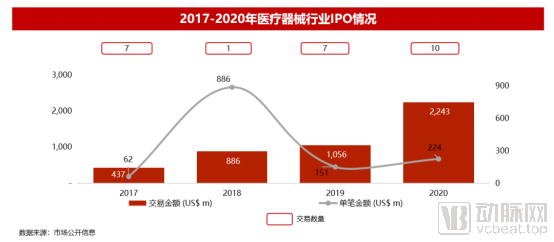

In the past year, there were 10 IPOs in the medical device sector, a year-on-year increase of 43%; total financing exceeded $2.2 billion, a year-on-year increase of 112%.

Diagnostics and IVD

In 2020, a total of 114 private equity financing transactions occurred in the diagnostics and IVD sectors, representing a near doubling year-on-year; the total financing amount exceeded USD 4 billion, a year-on-year increase of 219%; the average financing size per transaction was approximately USD 35 million, reflecting a year-on-year growth of about 66%.

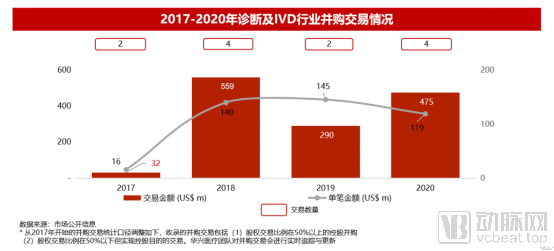

There were four M&A transactions in the diagnostics and IVD sectors throughout the year, double the number from the previous year; the total transaction value amounted to nearly $500 million, representing a 64% year-on-year increase; the average transaction size was approximately $120 million, marking a year-on-year decrease of about 20%.

In 2020, the industry completed a total of eight IPO financings, doubling year-on-year; the total financing amount exceeded US$1.3 billion, representing a 282% increase from 2019.

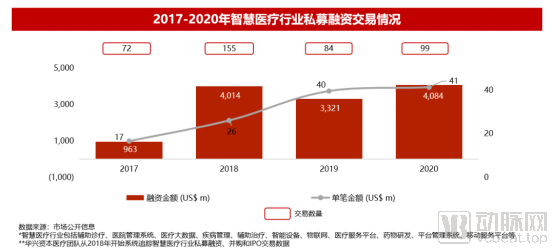

Smart Healthcare

In 2020, there were a total of 99 private equity financing transactions in China’s smart healthcare sector, representing a year-on-year increase of nearly 20%; the total financing amount reached approximately USD 4.1 billion, up by about 23% year on year; the average financing amount per transaction was around USD 41 million, showing a slight year-on-year increase and remaining largely stable.

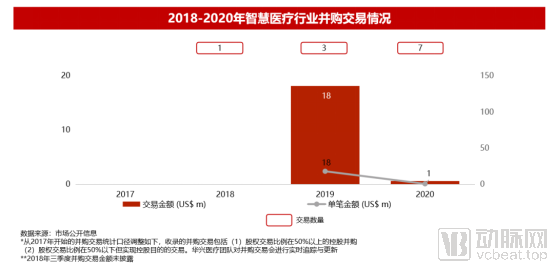

In terms of mergers and acquisitions, a total of seven transactions occurred in the smart healthcare sector throughout the year, representing a 133% increase compared to 2019. Notable M&A deals include ByteDance’s acquisition of Baike Mingyi Network and 1024 Technology; Jianhai Technology’s acquisition of Siyuan Technology and 317 Hu; Fosun Pharma’s acquisition of Yiyan Cloud; Qingsongchou’s acquisition of Yinchuan Duoer Internet Hospital; and Huanuo Zhisheng’s acquisition of Yikang Damei.

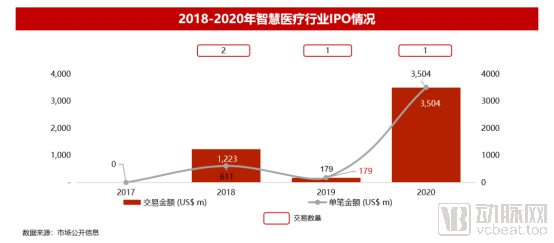

In terms of IPOs, in the fourth quarter of 2020, JD Health, an online medical and health platform and the largest online retail pharmacy, listed on the Hong Kong Stock Exchange, raising $3.5 billion.

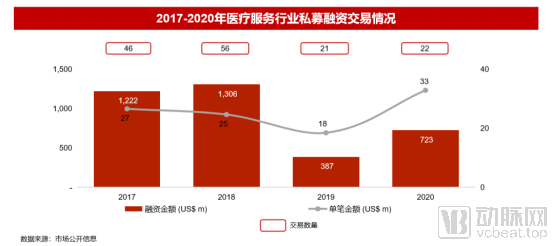

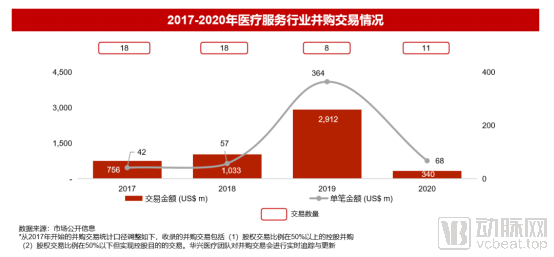

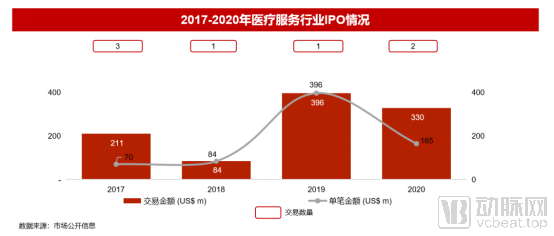

Medical Services

In 2020, there were 22 private equity financing transactions in the medical services sector, representing a slight year-on-year increase; the total financing amount was approximately USD 700 million, nearly doubling year-on-year; the average financing size per transaction was about USD 33 million, an increase of approximately 83% year-on-year.

A total of 11 mergers and acquisitions (M&A) transactions occurred in the healthcare services sector throughout the year, representing a 37.5% year-on-year increase; the total transaction amount was $340 million, an 88% decrease from 2019; the average transaction value was approximately $68 million.

A total of two IPO financings were completed in the healthcare services sector throughout the year, with a total financing amount reaching $330 million.

In 2020, all sectors within healthcare and life sciences demonstrated robust performance in the private equity financing market. Driven by the synergistic efforts of industry players and capital investors, healthcare deals experienced a concentrated surge starting in April. Both the number of transactions and the total amount of capital raised doubled throughout the year, propelling the market to a significantly higher level of activity.

Pharmaceuticals and Biotechnology

In 2020, the pharmaceutical and biotechnology sectors remained the primary focus of healthcare investment, with a total of 243 private financing transactions recorded throughout the year, disclosing a cumulative transaction value of up to $10.7 billion. Projects involving small-molecule targeted drugs and large-molecule biologics (including vaccines) accounted for half of all financing deals, followed closely by gene and cell therapies and CXO (contract research and manufacturing organizations). These major segments collectively represented 86% of the total number of transactions. The most notable performers were Sinovac Biotech and Reikoo Biologics, two vaccine companies that together raised $740 million in 2020.

Beyond this, the pharmaceutical and biotechnology sectors remain vibrant and diverse: new therapeutic areas and technology platforms are continually emerging. Startups in fields such as innovative antibody platforms, AI-driven drug discovery, gene editing, mRNA, and PROTACs are poised for growth, fueled by capital investment and ambitious aspirations. We believe that China’s innovative pharmaceutical industry is on the verge of entering an even more remarkable new chapter.

Medical Devices

If the seven IPO projects on the Hong Kong Stock Exchange and the STAR Market in 2019 awakened the private equity market for medical devices in 2020, then the enhanced technological attributes of device startups, their rapid follow-up on overseas products, and the differentiated market space opened up by the implementation of volume-based procurement further stimulated investors’ interest in the medical device industry.

Compared with innovative drugs, the medical device sector has become a key target for capital to balance risk allocation, owing to its relatively lower industry risks and higher clinical certainty. Although valuations continued to rise throughout the year, the detailed implementation rules for the fifth set of listing standards applicable to the medical device industry on the STAR Market did not arrive as expected in the fourth quarter, which may have contributed to the slight decline in transaction volume and value during that period.

Furthermore, news that MicroPort MedBot intended to list on the STAR Market reignited market enthusiasm for investments in medical robotics by year-end. Several other companies, including Edge Medical Robotics and Fourier Intelligence, also completed financing rounds in 2020. Whether this phased surge in funding for medical robotics projects signals the dawn of the digital surgery era may still require time to verify; nonetheless, it undoubtedly marks a step closer to global leadership in the sophistication of medical device entrepreneurship.

Diagnosis and IVD

In 2020, the value of private equity transactions in the diagnostics and in vitro diagnostics (IVD) industry more than tripled, with the number of recorded deals nearly doubling compared to 2019, reaching a total of 114. Companies associated with COVID-19-related concepts secured capital injections, leveraging this financial “tailwind” to rapidly achieve expansion and operational standardization while avoiding the risk of being “shuffled out” of the market. Meanwhile, although companies in the fields of tumor companion diagnostics and early disease screening were impacted by the pandemic in the first half of the year, the widespread establishment of PCR laboratories across hospitals at all levels in China created favorable conditions for their expansion.

Notably, MGI Tech’s single financing round of over $1 billion led globally, making it highly likely to drive prosperity in the R&D sector for high-end life science instruments. The industry is expected to demonstrate strong capital market potential in 2021. Furthermore, despite the presence of major players such as Fapon Biotech, there remains a significant gap in China’s domestically developed diagnostic raw materials market. Although high industry barriers exist, they also provide ample entrepreneurial opportunities for local enterprises.

Smart Healthcare

Since 2019, the average single-round financing amount for companies in the smart healthcare sector has approached that of the biopharmaceutical sector, remaining at the level of US$40 million. This trend reflects, to some extent, two characteristics of the industry: the adoption of platform-based business models and the entry into the commercialization stage.

In 2020, the AI + medical imaging industry successfully navigated the regulatory approval stage. A total of nine AI products received Class III medical device certification from the National Medical Products Administration (NMPA) throughout the year. Companies such as Keya Medical, Shukun Technology, and Deepwise Healthcare completed financing rounds, and their corresponding AI products all obtained approval. The market exhibited a pronounced trend toward consolidation among leading players. As these later-stage funding rounds were completed, this cohort of medical AI companies faced critical tests in commercial implementation and market expansion.

Furthermore, the emergence of niche sectors such as AI-assisted healthcare and AI-driven health management complements the deregulation of internet hospitals. With advancements in big data applications, AI technologies, and medical imaging, the penetration of related industries into the healthcare sector is expected to accelerate in the future.

Secondary Market

Biotech Sector Remains ActiveIn 2020, healthcare companies listing in Hong Kong experienced a surge, with 21 companies successfully going public on the Hong Kong Stock Exchange and raising a total of USD 11.35 billion. This represents a 154% increase compared to 2019, when 15 listed companies raised a combined USD 4.46 billion. An increasing number of institutional investors, including traditional secondary market investors, have turned their attention to the healthcare sector, extending their investment scope into the private equity market. Furthermore, the secondary market in Hong Kong remains optimistic about the healthcare industry: since the end of 2020, eligible companies listed under Chapter 18A have been included in the Stock Connect program. Therefore, the healthcare sector in the Hong Kong stock market is expected to remain active throughout 2021.

Innovation-Driven Biopharmaceutical Companies March Toward the Capital Markets

In 2020, the Hong Kong and U.S. stock markets attracted numerous innovative biopharmaceutical companies focused on oncology and immunotherapy. Most companies listed under Chapter 18A of the Hong Kong Stock Exchange’s listing rules possess industry-leading platform technologies and hold product pipelines featuring Best-in-Class or First-in-Class assets. Meanwhile, advanced enterprises have distinguished themselves from fierce domestic competition by expanding into overseas markets and pursuing cutting-edge technologies and targets. This trend is also reflected in the growing number of collaborative development and out-licensing deals. In 2020 alone, several Hong Kong-listed companies, including CStone Pharmaceuticals, Junshi Biosciences, Hua Medicine, and Innovent Biologics, out-licensed their self-developed products to internationally renowned pharmaceutical companies such as Roche, Pfizer, Bayer, and Eli Lilly.

Rising Attention on Medical Devices: Domestic Technologies to Take Center Stage

In 2020, medical device companies saw increased attention from the capital markets. Peijia Medical and Kangji Medical raised a combined $770 million through their initial public offerings (IPOs). MicroPort CardioFlow was listed in February 2021, and Acandis Medical submitted its A1 application in January 2021. The improvement of domestic devices in terms of brand, technology, and quality has also accelerated the process of import substitution. Furthermore, an increasing number of device companies are no longer satisfied with merely replacing imports but are striving to further enhance their level of innovation.

Specialized Subspecialties in the Healthcare Services Industry Will Present Opportunities

Following the listing of Jinxin Fertility, Hygeia, a specialized oncology treatment services company, also successfully listed on the Hong Kong Stock Exchange in 2020. It is expected that more specialized healthcare service providers will list in Hong Kong in the future.

More diagnostic companies are expected to list on the Hong Kong Stock Exchange

Currently, companies in the diagnostics sector remain scarce on the Hong Kong stock market. In early 2021, Berry Genomics, which is dedicated to building a high-throughput sequencing technology platform in the field of reproductive health, listed on the Hong Kong Stock Exchange. New Horizon Health, which focuses on early cancer screening, has also submitted its A1 application. It is believed that, leveraging the strong potential of the Chinese market and the growing public awareness of health, more high-quality enterprises in the diagnostics track will enter the secondary market in the future.

The Rise of Internet Healthcare and Smart Healthcare

In 2020, online channels gradually gained prominence, and the internet healthcare industry showed a trend of rising. For example, JD Health became the company with the largest fundraising amount and market capitalization in the Hong Kong stock market's healthcare sector in 2020. On the other hand, the smart healthcare sector also sparked an investment boom. Yidu Tech, characterized by its self-developed artificial intelligence platform, listed on the Hong Kong stock market in early 2021.

Review of IPOs in the Pharmaceutical Industry on China’s A-Share Market in 2020

In 2020, a total of 395 companies were successfully listed on China’s A-share market, raising nearly RMB 470 billion. Among them, 45 companies were from the healthcare industry, raising approximately RMB 63.5 billion. The number of listed healthcare companies and the amount of capital raised accounted for approximately 11.4% and 13.5%, respectively, representing significant increases compared to 2019.

Among these 45 healthcare-related companies, 15 are medical device manufacturers and 12 are chemical pharmaceutical and biologic products companies. In terms of listing venue, 30 companies chose the STAR Market, raising a total of approximately RMB 49 billion, accounting for 66.7% and 77.2% of the total number and amount, respectively.

More Inclusive Systems

The current institutional design of the STAR Market has significantly enhanced the inclusiveness of China’s capital market toward pharmaceutical companies. Benchmarking against the listing requirements of Chapter 18A of the Hong Kong Stock Exchange, the STAR Market has removed regulatory barriers for pre-revenue pharmaceutical enterprises. On January 23, 2020, Zeltex Pharmaceuticals became the first unprofitable pharmaceutical company to list on the A-share market. By the end of 2020, a total of eight unprofitable healthcare companies had successfully listed on the STAR Market, including seven biopharmaceutical firms under Listing Set 5 and Tinavi Medical Technologies under Listing Set 2.

Diversification of IPO Pathways

In April 2018, the Hong Kong Stock Exchange introduced new policies allowing biotech issuers that had not yet passed any of the Main Board’s financial eligibility tests to list in Hong Kong; at that time, unprofitable biotech companies were still unable to access the domestic capital markets. In March 2019, the establishment of the STAR Market removed listing barriers for unprofitable pharmaceutical enterprises, creating a competitive landscape between the two markets. In April 2020, the ChiNext Board initiated registration-based IPO reforms, further diversifying the pathways for pharmaceutical companies to go public. With the comprehensive advancement of registration-based reforms in China’s capital markets, eligible pharmaceutical firms now enjoy more diverse listing options.

Penetration of the Secondary Market into the Primary Market

Under the approval-based system, listing standards required companies to achieve a substantial level of profitability; in other words, most companies would only consider an initial public offering (IPO) after reaching the mature stage. Benefiting from the registration-based IPO reform, high-quality companies can prepare for listing at an earlier stage, as long as they meet the requirements for public offering and listing, thereby allowing the secondary market to penetrate into the primary market. As the registration-based system opens new listing windows for a growing number of high-quality enterprises, the “faith” in IPOs within China’s capital markets is gradually fading.

Internet Healthcare Companies’ A-Share IPOs Remain Rocky

In recent years, internet healthcare in China has entered a phase of rapid development. Through the exploration of various business models, the pharmaceutical e-commerce and digital health industries have achieved high-speed growth. A number of unicorn companies have emerged in the internet healthcare sector, driving significant expansion in both market size and corporate scale.

Since 2018, prominent internet healthcare companies such as Ping An Good Doctor and JD Health have listed on the Hong Kong Stock Exchange. However, in contrast to the bustling activity in the Hong Kong market, the path to A-share initial public offerings (IPOs) for internet healthcare firms remains fraught with challenges.

Pharmaceutical Companies’ Transformation Urgently Needs Innovation Boost; Proactive Changemakers Will Seize Development Opportunities

The development of China’s pharmaceutical industry in recent years can be reviewed from two perspectives: On one hand, Chinese innovative drug companies, backed by venture capital (VC) and private equity (PE), have experienced rapid growth, achieving significant progress in both business expansion and financing; on the other hand, traditional Chinese pharmaceutical enterprises have been striving to break through amid multiple pressures, including the “4+7” volume-based procurement program, innovation-driven transformation, internationalization, and stock price volatility.

However, the two ecosystems remain relatively independent. Taking the Taizhou region as an example, many listed pharmaceutical companies that initially built their businesses on active pharmaceutical ingredients (APIs), intermediates, or generic drugs are now facing critical decisions regarding corporate transformation. In an era driven by capital, innovative technologies and products are emerging in rapid succession. Management teams at these listed companies must grapple with key questions: how to design a transformation pathway, how to leverage capitalization tools, how to integrate and assimilate new technologies and products into existing R&D systems, and how to align production and marketing infrastructures with innovative offerings.

On the other hand, the market for unlisted biotechnology companies and IPO channels has initially shown a state of oversupply. For many startups, forming equity and business collaborations with listed companies that possess stronger comprehensive capabilities will become a more favorable option. Meanwhile, biotechnology firms with a global perspective can leverage advanced concepts to further upgrade the infrastructure of the traditional pharmaceutical industry, including its R&D, production, and marketing systems. For institutional shareholders, beyond achieving exit returns, listed companies can also be considered as platforms for strategic industrial layout.

The transformation journey for pharmaceutical companies is bound to be challenging, but proactive change is preferable to reactive adaptation. The infrastructure of the pharmaceutical industry urgently requires innovation. CRP-FANYA is committed to building a bridge between pharmaceutical enterprises and biotechnology companies, promoting the integration of these two ecosystems through strategic design and transaction tools. We believe that pharmaceutical companies with clear strategies, strong execution capabilities, and the courage to take risks will stand out and lead industrial development.

CROs Need to Flourish and Step onto the Global Stage

The pandemic posed certain challenges to the progress of clinical trials in China’s CRO industry in 2020, yet it failed to halt the market’s expansion to a scale nearing RMB 100 billion. Among all segments, clinical CROs constitute the largest market; however, this segment is characterized by relatively low concentration and a limited number of leading enterprises within the industry chain.

Among clinical CRO companies, Tigermed stands out. However, the CRO industry chain is replete with capable and keenly perceptive enterprises that have already laid the groundwork or are actively preparing to enter the clinical CRO business, striving to capitalize on growth in the domestic market and expand into the global arena.

Industry Landscape: The Strong Get Stronger—Several New Norms of M&A Are Gradually Taking Shape in the CRO Industry. First, preclinical CROs are moving toward synergistic development with clinical CRO services. For instance, emerging preclinical CRO companies such as Joinn Laboratories are planning to expand into comprehensive clinical CRO operations.

Secondly, clinical CRO companies are actively expanding into specialized segments to become full-service clinical CRO providers. For instance, SmartMed and Dima, which originally specialized in biostatistics and data management, have expanded into clinical operations; Wuhan Hongren acquired the statistical CRO Xinlida to enhance its clinical CRO capabilities. Furthermore, against the backdrop of big data and AI-driven innovation empowering the healthcare industry, companies such as Taimei, Yidu Cloud, and LinkDoc have strategically positioned themselves in areas including patient recruitment, data management, biostatistics, and regulatory submissions, aiming to develop innovative and efficient CRO services. Beyond pharmaceutical CROs, companies like Pharmaron have also expanded into medical device CRO services through acquisitions such as that of Fahui.

The pharmaceutical industry in China and worldwide has witnessed unprecedented, vigorous growth. A diverse array of leading players has converged in the clinical CRO market, where only through strength-consolidating mergers and acquisitions can they rapidly enhance their capabilities, secure a foothold in China’s CRO market, and subsequently compete on the global stage.

Currently, WuXi AppTec, Pharmaron, and Tigermed have already emerged as prominent players on the international stage. In the near future, we hope to see more Chinese CRO companies leveraging their respective strengths to capture greater international market share, rather than merely chasing or imitating existing global leaders. By offering internationally competitive service capabilities and cost-effective solutions, Chinese CROs should become trusted service providers for global pharmaceutical companies.

Disclaimer

This report is provided for your reference only and does not constitute, nor shall it be construed as, an offer or invitation to sell, purchase, or subscribe for securities, nor as an invitation directed at any specific person. The investments mentioned herein may not be available in certain jurisdictions. Any investment referenced in this report may involve significant risks; some investments may be illiquid and may not be suitable for all investors. The value of the investments mentioned in this report, or the income derived therefrom, may fluctuate due to exchange rate movements. Past performance is not indicative of future results. This report does not take into account the investment objectives, financial situation, or particular needs of any investor. Investors should not rely solely on this report but should make investment decisions based on their own judgment. Before taking any investment action based on the recommendations in this report, investors should seek professional advice.

This report has been prepared by China Renaissance Holdings (“China Renaissance”). The sources of the information contained herein are considered reliable by China Renaissance. The opinions, analyses, forecasts, projections, and expectations presented in this report are based on such reliable data but represent views only. China Renaissance, its holding companies and/or subsidiaries and/or related individuals do not warrant the accuracy or completeness of this report. The information, opinions, and estimates contained in this report reflect the judgments of China Renaissance as of the initial date of publication of this report and are subject to change without prior notice. China Renaissance, its holding companies and/or subsidiaries and/or related individuals shall not be liable for any direct, indirect, or consequential losses incurred by any person arising from the use of the materials contained in this report.

This report is fully protected by copyright and proprietary data rights. No person may reproduce, distribute, or publish this report for any purpose without the authorization of China Renaissance Capital. China Renaissance Capital reserves all rights.