2020 Invisible Aligners Market Research Report: Domestic Innovation Continues, DTC Model Injects Market Vitality

This report is jointly released by haodeya_DX and VCBeat.

The domestic clear aligner market has evolved from its nascent stage to explosive growth, paralleling the coming-of-age of the millennial generation. Similar to most new products, clear aligners have progressed through various stages of their product lifecycle, including skepticism, controversy, and eventual acceptance. In the post-pandemic era, the beauty economy and domestic consumption circulation remain major trends in the new era.

Over the past two decades, the landscape of innovative orthodontic consumables has evolved significantly—from the emergence of the leading brand Invisalign, to Angelalign, a standout Chinese domestic brand, capturing a share of China’s orthodontic market, and now to the rapid rise of new direct-to-consumer (DTC) brands. Undoubtedly, this is a highly competitive commercial arena. In this study, we aim to map out the evolving trajectory of the clear aligner sector and review the twenty-year development journey of China’s clear aligner industry.

Under the traditional model, clear aligner brands do not provide medical services directly to orthodontic patients; instead, they collaborate with downstream healthcare institutions and dentists. With the rise of the internet, some clear aligner brands have begun to establish a presence on online platforms, leveraging these high-traffic channels to showcase their products to patients. However, the final medical services are still delivered by each brand’s partner clinics, giving rise to the O2O (Online-to-Offline) and new retail models.

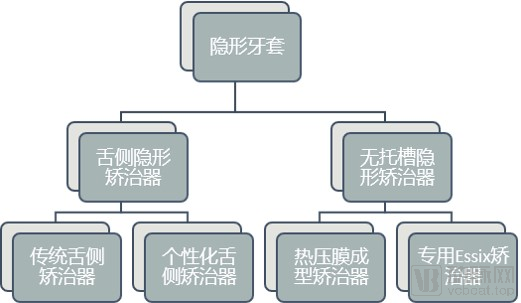

Invisible Braces (Invisible Aligners), also known as invisible appliances, are orthodontic devices used in the process of orthodontic diagnosis and treatment that are not visibly apparent, includingLingual Invisible AlignersandClear Aligners。

Currently, the clear aligner industry in China is in its growth phase. Driven by rising oral health awareness and the booming "appearance economy," demand for clear aligner treatment is growing rapidly, resulting in a high overall market growth rate for the industry.

In 1970, the world’s first physical clear aligner was introduced. Since 2001, the nascent stages of domestic clear aligner research have emerged. Over the past two decades in China, local clear aligner brands have undergone four critical phases: inception, exploration, growth, and intense competition.

In 2010, overseas returnees paved the way, and the international brand Invisalign was approved to enter the Chinese market.

In 2011, as Chinese brands expanded overseas, eBrace, the first domestic brand of personalized lingual clear aligners, also embarked on its global market expansion. As key patents for clear aligners gradually became transparent and the "Internet Plus" model continued to evolve, the traditional business model of bracketless clear aligners has been continuously reshaped.

Upstream: membrane, equipment, and software manufacturers.The aligner films are primarily imported from abroad, supplemented by domestic independent R&D; the equipment involves intraoral scanners, vacuum-forming machines, cutting machines, and 3D printers; the software mainly covers simulation of orthodontic tooth movement and automated production, with early reliance on third-party software outsourcing firms and a later shift to in-house development.

Midstream: Clear aligner manufacturers. Aligners are mainly categorized into two types: lingual and bracketless.Most early entrants in the clear aligner market adopted an integrated model encompassing R&D, manufacturing, and sales. In contrast, direct-to-consumer (DTC) brands that have entered the market in recent years largely rely on outsourced manufacturing, focusing their efforts on marketing and sales; some even leverage mass-traffic platforms to sell aligners directly to consumers. Due to differences in proprietary software systems and other factors, clear aligner manufacturers have increasingly taken the initiative to train, educate, and certify orthodontists. Furthermore, some clear aligner brands have already filed IPO applications with the Main Board of the Hong Kong Stock Exchange.

Downstream: Various medical service institutions.General hospitals and specialized dental hospitals account for a relatively small proportion, with the vast majority being private dental medical institutions. Currently, these are predominantly regional chain brands and independent clinics, with no national brands having achieved significant mainstream prominence. Meanwhile, regional brands specializing in clear aligner therapy have emerged, and some leading brands have begun preparing for initial public offerings (IPOs).

Platforms: Primarily vertical oral care platforms, broad healthcare platforms, and general traffic platforms.As a high-value dental care service, orthodontics has seen the emergence of vertical platforms based on user-generated content (UGC) and professional-generated content (PGC), which promote aligner brands and orthodontists/clinics through popular science education on tooth correction and experience sharing. In contrast, general medical and high-traffic platforms primarily facilitate online purchases of orthodontic packages or vouchers, followed by offline clinical visits.

Orthodontist: A master's degree is the educational threshold for orthodontists.Some clinicians are proficient in both traditional orthodontic techniques and various clear aligner therapies, and they have begun to provide tailored treatment plans based on individual patient differences and clinical requirements.

Clear aligner technology involves the intersection of multidisciplinary knowledge from stomatology, biomechanics, computer science, and other fields. Among domestic clear aligner brands, whether in the field of personalized lingual orthodontics or bracketless systems, the leading brands that entered the market early initially relied on collaborations between their internal technical teams and external universities.

Currently, the R&D sector is exhibiting a diversified development pattern characterized by integrated domestic and international collaboration., mainly in the following forms:

● Brand’s In-House Technical Team + Universities

● In-house technical team + renowned orthodontic specialists

● In-house technical team + dental industry enterprises

In the production and sales segments, this is manifested as an interweaving of OBM, ODM, and OEM models:

*Data sources: State Council, National Medical Products Administration, National Health Commission, Haodeya DataLab

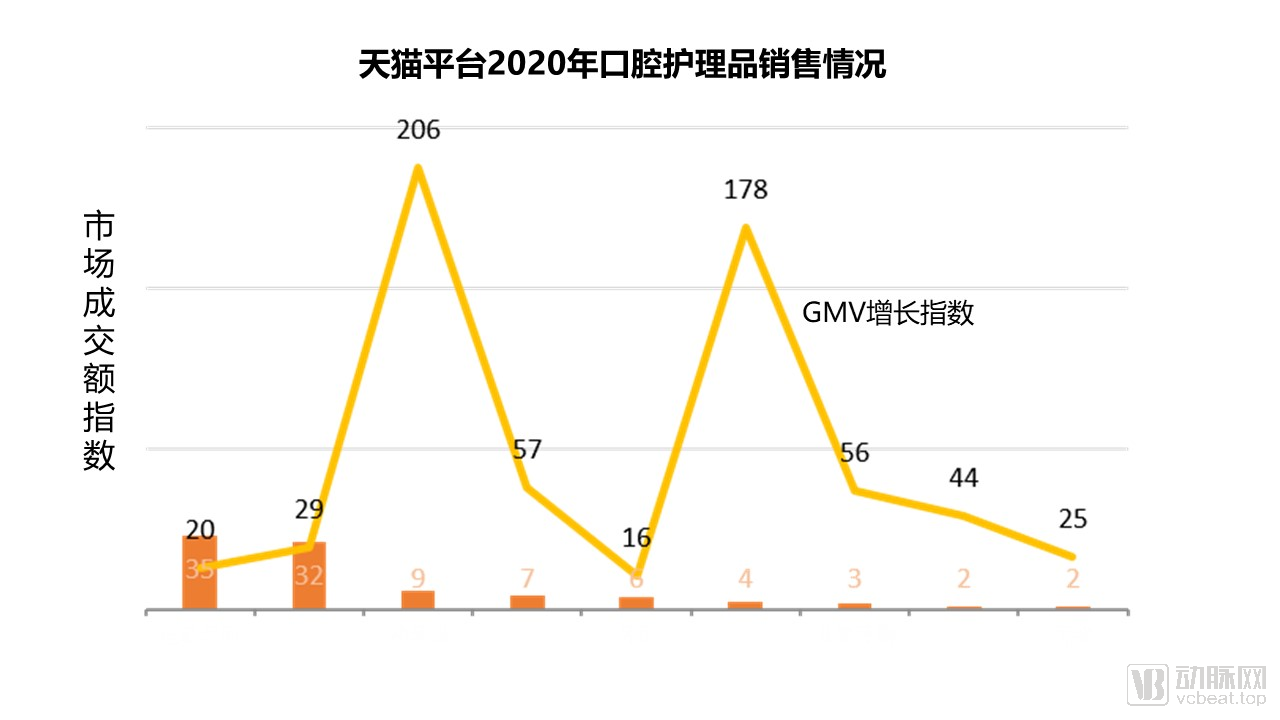

According to the “Latest Trends Report on the Oral Care Industry in 2020,” major categories within oral care have all experienced growth. Basic consumer demands now include tartar removal, yellow stain reduction, bad breath elimination, freshening of breath, and teeth whitening, indirectly reflecting a gradual increase in national awareness of oral health.

The rise and development of the Internet have spurred the prosperity of the “camera economy,” characterized by short-form videos and live streaming. According to the 2020 Douyin Entertainment White Paper, Douyin currently boasts 600 million daily active users, with over 3,000 celebrities and artists joining the platform in 2020. Overall, ordinary individuals are gradually emerging as a vibrant and dominant force in the camera economy.

Sales data from the Tmall New Product Innovation Center (TMIC) over the past year reveals growth across nearly all major oral care categories. The shift of certain traditional segments toward premiumized categories—such as water flossers and children’s electric toothbrushes—reflects, to some extent, a growing consumer emphasis on dental health among the Chinese population.

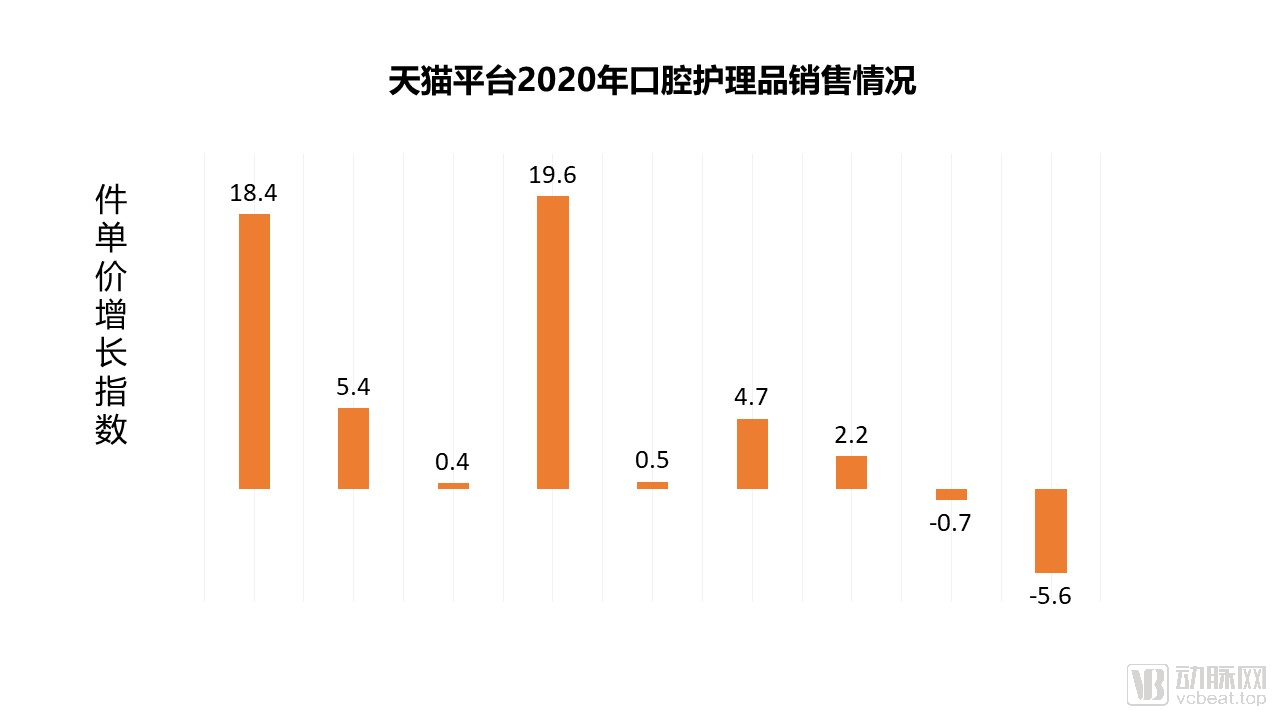

The unit prices of most oral care product categories have shown positive growth, with significant price upgrades in core categories such as electric toothbrushes and mouthwashes. This indirectly reflects the enhanced consumption capacity and willingness of Chinese consumers regarding oral health.

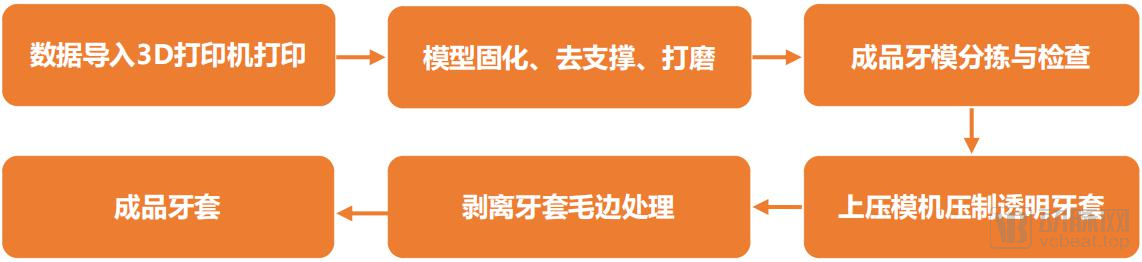

3D Printing Technology:With the development of 3D printing technology in recent years, this technology has been widely used in the field of invisible braces. Customized 3D-printed braces have moved from possibility to reality and gradually become an important part of the production process for invisible braces.

Intraoral Scanning Technology:The further application of digital technology in dentistry has also led to intraoral scanning gradually replacing traditional alginate impression taking. With the launch of increasingly compact intraoral scanners, traditional clinical workflows are being transformed, and some direct-to-consumer (DTC) clear aligner brands are gradually reshaping their business models through at-home intraoral scanning services.

Automatic Cutting:Currently, few domestic clear aligner brands have mastered this technology, and most equipment still relies on imports from abroad. However, leading brand manufacturers have already invested in and developed automated cutting tools to further improve their production efficiency and profit margins.

Oral Database:As the number of orthodontic correction cases accumulates, leading domestic clear aligner brands have each built substantial oral health databases specific to China and Asia. Further data mining of these accumulated case records has the potential to drive further development in the clear aligner industry.

Chairside Digitalization:According to data from the "Report on China's Dental Industry in the Global Context and China's First Dental Industry Survey," chairside digitalization ranked first in the 2018 Dental Industry Prosperity Index. The application of chairside digitalization has also been one of the industry hotspots in recent years. Currently, clear aligner brands have officially launched chairside digital systems, achieving chairside fabrication of clear aligners.

December 25, 2019,First Domestically Produced Membrane Material Approved for Market Launch, this material is held by a wholly-owned Japanese subsidiary in China. Currently, there are a total of five membrane raw materials that have obtained valid registration certificates and are approved for marketing in China, with an additional four imported from two German companies. Furthermore,Some startup teams are also continuing to exert efforts in materials research and development.。

Since the first imported membrane material was approved for market launch in 2008, six overseas raw membrane materials have entered the Chinese market, all supplied by two German companies. Domestic membrane materials were once heavily reliant on imports from Germany, highlighting a significant “chokepoint” issue in upstream materials.

Nowadays, some leading domestic clear aligner brands have also begun to collaborate with companies specializing in the research and development of clear aligner materialsCollaborative R&DNew medical-grade polymer membrane materials aim to alleviate the bottleneck constraints in upstream raw material supply, thereby reducing procurement costs for membrane materials.

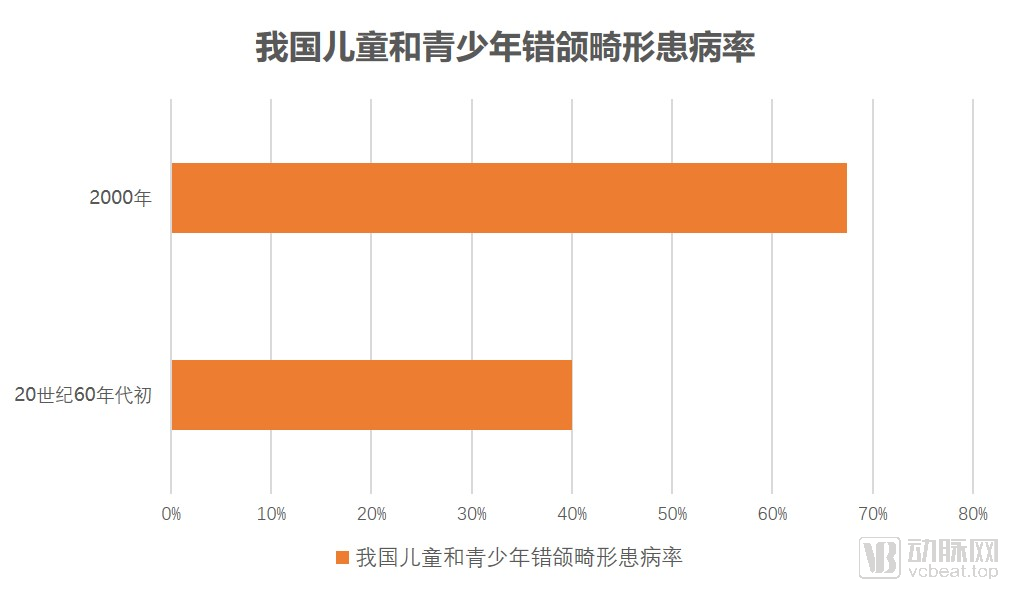

Due to the lack of globally unified epidemiological survey standards for malocclusion, reported prevalence rates vary significantly between domestic and international studies.The prevalence of malocclusion among children and adolescents in China has increased significantly over the past four decades, rising from 40% in the early 1960s to 67.82% in 2000., which may be primarily attributed to the persistently high incidence of dental caries among children and adolescents.

*Data sources: Orthodontics, Haodeya DataLab, VBInsight Database

*Data sources: "Orthodontics," Haodeya DataLab, VBInsight Database

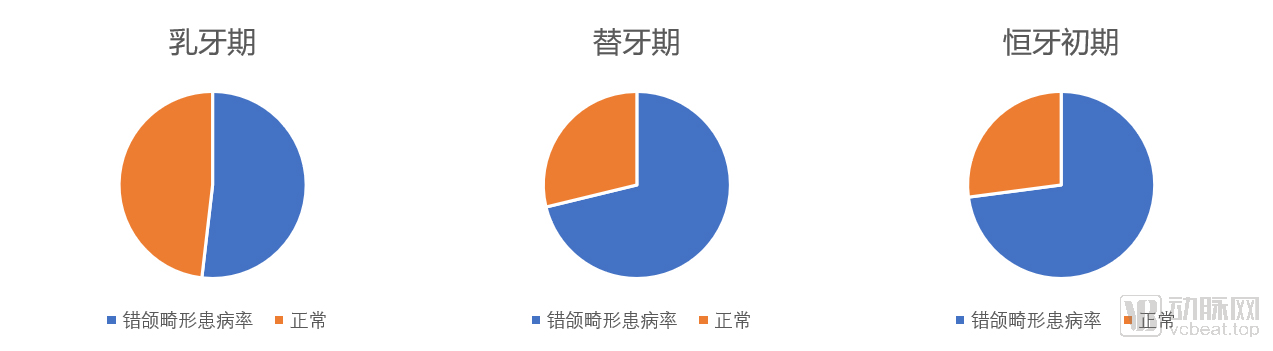

The survey results released by Professor Fu Min Kui et al. show that the prevalence of malocclusion in children and adolescents is 51.84% during the primary dentition stage, 71.21% during the mixed dentition stage, and 72.92% during the early permanent dentition stage.

Internet Hospital:According to data from the Digital Health Sub-forum of the 3rd Digital China Summit,China has established over 900 internet hospitals nationwide., over 2,200 tertiary public hospitals have achieved interoperability and sharing of in-hospital medical service information, and more than 7,000 secondary hospitals provide online services.

Online Triage Platforms: As internet hospitals and healthcare platforms expand into dentistry, the landscape of traditional online triage platforms is being reshaped.. However, as it stands, Dianping and So-Young remain the primary forces in online patient triage, having launched services such as onboarding medical service providers and online dental consultations. JD Internet Hospital has also introduced direct onboarding for clear aligner brands within its Dental Center, and withOnline Voucher Sales, Offline Consultations at Partner Clinicsin the form of a closed-loop service.

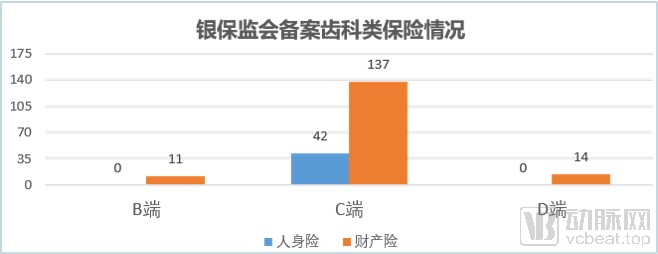

Since the launch of China’s new healthcare reform in 2009, 61 of the currently registered 101 life insurance companies and 88 property insurance companies in China have (at some point) introduced commercial dental insurance products, totaling 204 offerings. In the early stages of commercial dental insurance, most products were offered as riders, with only occasional standalone primary policies. Public Grade-A tertiary hospitals and leading private dental clinic chains have both piloted collaborations with insurance companies to launch a variety of dental-specific insurance products.

Over the past eleven years, dental commercial insurance has evolved from annual coverage models to service-based plans. Covered services have expanded from simple preventive care, such as dental cleaning, and basic treatments to complex procedures like dental implants and orthodontics. Among these offerings, there are 10 joint insurance products covering both dental implants and orthodontics, 11 exclusive insurance products specifically for dental implants, and only one exclusive insurance product specifically for orthodontics.

In April 2009, the new healthcare reform plan was officially released, proposing for the first time to actively develop commercial health insurance and encourage commercial insurance institutions to develop health insurance products tailored to diverse needs. In September 2009, Aviva-COFCO Life Insurance Co., Ltd. filed its domestic inaugural dental insurance product with the China Insurance Regulatory Commission (CIRC). In the same month, Ping An Health Insurance Company of China, Ltd., AIA Insurance Company Limited Shanghai Branch, and Ping An Property & Casualty Insurance Company of China, Ltd. also launched their respective offerings.

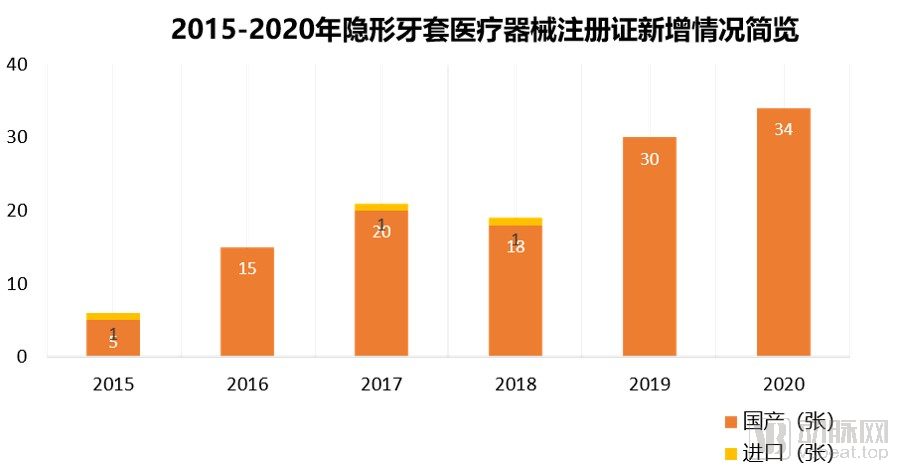

Currently, there are 125 valid registration certificates in force, held by 104 companies respectively, with 97.6% of the certificates related to domestically produced dental aligners. Among them: 122 are registration certificates for domestic medical devices, held by 102 domestic companies respectively; 3 are registration certificates for imported medical devices, held by 2 overseas companies respectively.

*Data sources: National Medical Products Administration, Haodeya DataLab, VCBeat Orange Database

According to data from the National Medical Products Administration, medical device registration certificates for clear aligners are predominantly for domestically produced products, with imported products playing a supplementary role. Nearly 95% of these registration certificates fall under the category of bracketless clear aligners, while only seven are related to lingual orthodontic products.

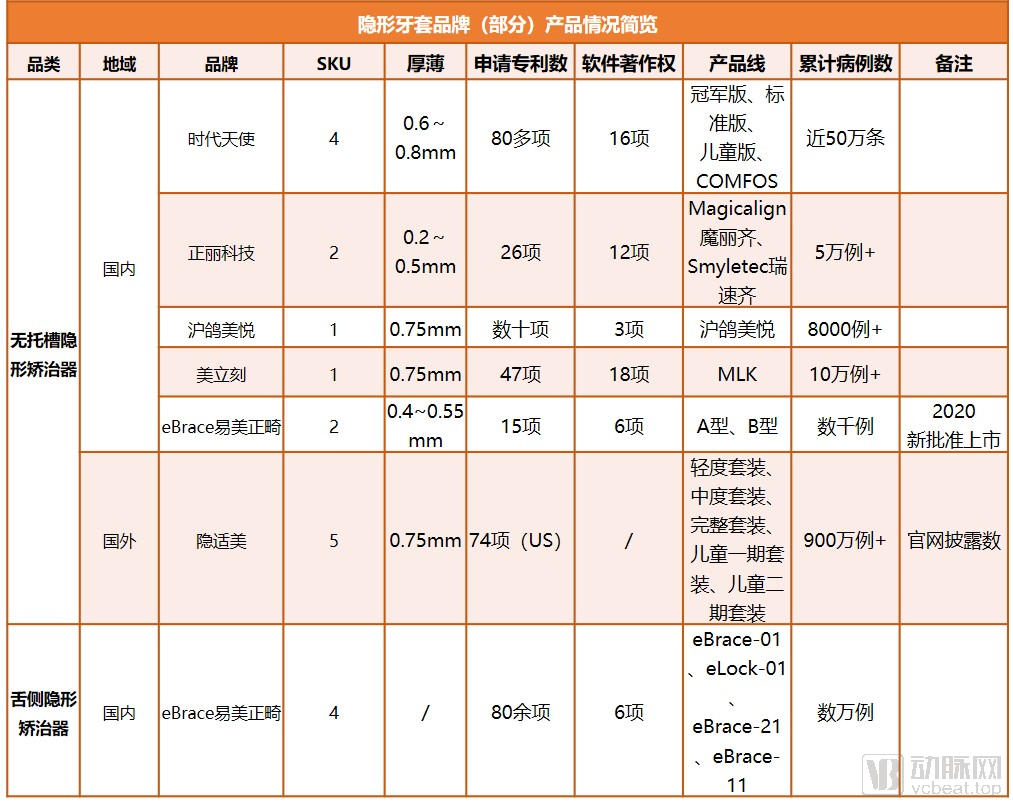

While some brands have launched distinct clear aligner products for adults and children, the vast majority remain focused on the adult clear aligner market. Based on a survey of select brands, the thickness of the aligners is generally around 0.75 mm. Furthermore, some clear aligner brands now offer product lines that span both clear aligner and lingual orthodontic categories.

Currently, the operational and communication matrix for clear aligner brands remains predominantly focused on public-domain platforms. The "Two Weis" (WeChat Official Accounts and Sina Weibo) have become standard operational channels for most brands. In particular, on WeChat Official Accounts, some brands have launched functional modules such as case management via Mini Programs, aiming to bridge the "last mile" of service delivery. Meanwhile, certain brands collaborate with downstream clinics and dentists, establishing a presence on vertical niche platforms like Beizhi, Aiyouya, and Yatao Zhijia. Some brands are also becoming active on emerging traffic platforms such as Xiaohongshu (Little Red Book) and Bilibili. New initiatives have emerged, including driving traffic from public domains to private domains and adopting Enterprise WeChat.

Since the emergence of SmileDirectClub (SDC), the pioneer of the direct-to-consumer (DTC) model for clear aligners, a new wave of startups in China’s clear aligner sector has emerged, seeking to replicate the SDC model. According to incomplete statistics, there are approximately 20 Chinese DTC brands frequently visible in the market, with nearly one-fifth of them having secured financing.

With the emergence of the direct-to-consumer (DTC) orthodontic model, traditional orthodontic models and online-to-offline (O2O) orthodontic models have also been impacted to varying degrees. However, as clear aligners are classified as Class II medical devices and domestic regulatory policies remain unclear, some clear aligner brands have begunExploring the Localization of the DTC Model。

DTC Orthodontic Model: Refers to the direct-to-consumer (DTC) model, where clear aligner brands reach end-user orthodontic consumers via internet channels.Provide remote/semi-remote medical services and sell alignersCurrently, some direct-to-consumer (DTC) clear aligner brands have begun exploring business models with Chinese characteristics. By leveraging online-to-offline (O2O) platforms, they channel patients to partner clinics or self-operated clinics, where preliminary procedures such as intraoral scanning are performed for certain users, while the remaining steps continue to be directly managed by the clear aligner manufacturers.

The above is a brief summary of the report. Scan the QR code below to access the full version.