MicroPort CardioFlow IPO Valued at HK$44 Billion as Hillhouse-Backed TAVR Sector Enters Commercialization Battle

On February 4, 2020, MicroPort CardioFlow, a subsidiary of MicroPort Scientific Corporation focused on the research, development, and commercialization of comprehensive solutions for heart valve diseases, was listed on the Hong Kong Stock Exchange. Its opening price on the first day was HK$21.5, its closing price was HK$18.8, and its market capitalization exceeded HK$44 billion.

MicroPort is the third domestic company to go public in the field of heart valves. Previously, Venus Medtech and Peijia Medical were listed on the Hong Kong Stock Exchange in 2019 and 2020, respectively. As of February 4, 2021, Venus Medtech’s market capitalization exceeded HK$35 billion, while Peijia Medical’s market capitalization surpassed HK$18 billion.

The primary products of the three companies are transcatheter aortic valve replacement (TAVR) devices. In China, the main indications are for patients with symptomatic severe calcific native aortic stenosis who are at high risk for or contraindicated to surgical intervention.

Heart valves serve as the “doors” of the heart. This “door” represents a rapidly emerging segment within China’s high-value medical consumables industry and a sector that attracts billions in capital flows.

In the field of transcatheter heart valve interventions, Venus Medtech, Peijia Medical, and MicroPort CardioFlow have all received investments from Hillhouse Capital, leading some in the industry to remark that Hillhouse has effectively bought up the entire sector. Beyond Hillhouse, this domain has also attracted strategic investments from a host of top-tier domestic and international firms, including Goldman Sachs, Sequoia China, OrbiMed, Matrix Partners China, Qiming Venture Partners, and Lilly Asia Ventures, underscoring the significant potential of the TAVR market.

High-value cardiovascular consumables represent the most dynamic segment of China’s medical device industry. Within the field of cardiovascular intervention, there are multiple subsectors, including coronary stents, heart valves, cardiac rhythm management, and cardiac electrophysiology. Why have heart valves emerged as a standout sector in recent years, giving rise to three companies with market capitalizations exceeding RMB 10 billion? Is this subsector inherently advantaged, or are expectations overly optimistic? The listing of MicroPort CardioFlow provides an opportunity to observe this market.

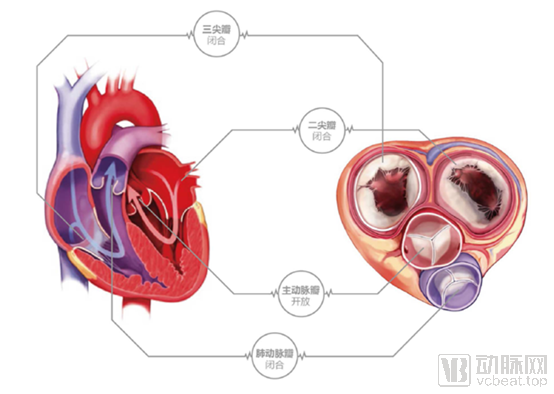

Our heart consists of four “chambers”: the left atrium and right atrium are located in the upper part, while the left ventricle and right ventricle are situated in the lower part. The heart’s daily function is to supply oxygen-rich blood to itself and all organs throughout the body. Blood flows through these four cardiac chambers, regulated by “four doors” known as “heart valves,” which control the direction of blood flow. The four valves are the aortic valve, mitral valve, tricuspid valve, and pulmonary valve.

Currently, in terms of product portfolio, MicroPort CardioFlow, Qiming Medical, and Peijia Medical have commercialized and pipeline products covering the aortic, mitral, and tricuspid valves; however, transcatheter intervention for aortic valve disease remains the primary competitive arena.

Any condition that impairs the normal opening and closing of the valve places a burden on the heart. Two common severe aortic valve diseases are severe aortic regurgitation (insufficiency) and severe aortic stenosis (incomplete leaflet opening).

When valvular heart disease occurs, in addition to pharmacological treatment, it can be treated with heart valve replacement surgery, which involves removing the diseased heart valve and replacing it with a prosthetic valve. Prosthetic valves can be biological (such as porcine valves) or mechanical.

There are also two treatment options for heart valve replacement: one is traditional open-heart surgery, and the other is minimally invasive transcatheter valve intervention. The interventional valve device consists of a valve delivery system and a specially designed heart valve.

TAVR has garnered significant attention as a groundbreaking minimally invasive interventional technique. By delivering and implanting a prosthetic valve into the diseased aortic valve via a minimally invasive approach—rather than through open-chest and open-heart surgery—it aims to treat aortic regurgitation (insufficiency) and stenosis, thereby restoring cardiac function.

Since 2002, this technology has been implemented in European and American countries. In 2010, a team led by Academician Ge Junbo from Zhongshan Hospital Affiliated to Fudan University and Academician Gao Runlin from Fuwai Hospital, Chinese Academy of Medical Sciences, pioneered the first three TAVR procedures in China.

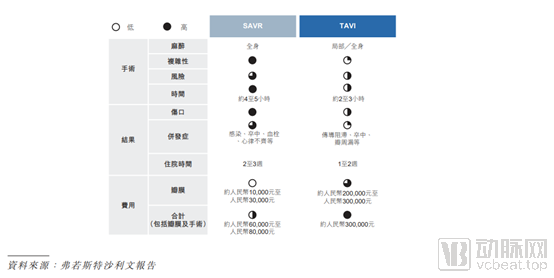

Comparison of Surgical Aortic Valve Replacement (SAVR) and Transcatheter Aortic Valve Replacement (TAVR)

The reason these small doors have attracted the focus of so many institutions lies in the enormous market for structural heart disease.

Valvular heart disease is a structural heart disease. According to data from MicroPort CardioFlow’s prospectus, in 2019, there were approximately 213 million patients with valvular heart disease worldwide, resulting in 2.6 million deaths.Among these, aortic stenosis and mitral regurgitation are the most common types of valvular heart disease, accounting for 9.2% and 45.4% of global patients with valvular heart disease, respectively, in 2019.Tricuspid valve disease (including tricuspid stenosis and tricuspid regurgitation) is another common type of valvular heart disease.

In China, this disease is also highly prevalent; in 2019, the number of patients with valvular heart disease in China reached 36.3 million.Among patients with valvular heart disease, those with aortic stenosis, mitral regurgitation, and tricuspid regurgitation accounted for 11.8%, 29.2%, and 25.1%, respectively.

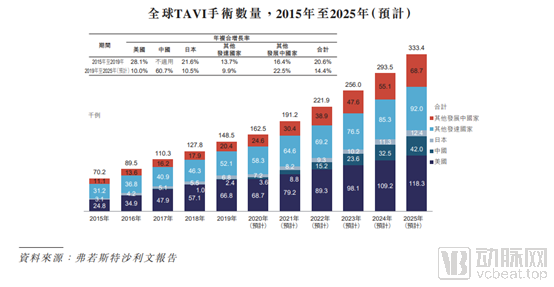

In the field of TAVR, according to Frost & Sullivan data, the global TAVR market has grown rapidly from $2 billion in 2015 to $4.8 billion, and is projected to continue its growth trajectory, reaching $10 billion by 2025.

The revenues of the two giants in the heart valve sector, Medtronic and Edwards Lifesciences, may provide a more intuitive sense of the potential of the TAVR market.

Edwards Lifesciences holds approximately 60% of the global heart valve market share. In 2019, its heart valve sales revenue reached $2.74 billion, representing a year-on-year increase of 19.7%. This suggests that among MicroPort HeartFlow, Venus Medtech, and Peijia Medical, there is potential for one Chinese company to emerge as the “Edwards Lifesciences of China.”

The three domestic valve companies are currently primarily competing for the domestic TAVR market.

In 2019, approximately 2,000 TAVR procedures were performed in China, with a penetration rate of only 0.3%.Developed countries have performed over 80% of TAVR procedures worldwide, with an average of one in five eligible patients receiving TAVR treatment.

Driven by the large patient population, increasing patient acceptance of TAVR procedures, a growing number of qualified hospitals and practitioners, and population aging, China is expected to experience the highest growth rate, with a compound annual growth rate (CAGR) of 60.7% from 2019 to 2025.

Major TAVR Products in China Under Commercialization or in Clinical Trials

BP refers to bovine pericardium; PP refers to porcine pericardium. Data source: MicroPort CardioFlow prospectus

Currently, five TAVR products have been approved for marketing in China: VenusA-Valve and its second-generation product, VenusA-Plus, from Venus Medtech; J-Valve from Suzhou Jiecheng; SAPIEN 3 from Edwards Lifesciences; and VitaFlow from MicroPort CardioFlow.

There are significant differences among these five products. VenusA-Plus from Venus MedTech and SAPIEN 3 from Edwards Lifesciences belong to the improved second-generation products, while the products from the other three companies belong to the first generation.

In terms of valve type, only Edwards Lifesciences’ SAPIEN 3 is a balloon-expandable valve, while the other four products are self-expanding valves. Medtronic’s Evolut R and Pro, which are also self-expanding valves, have not yet entered the Chinese market.

Balloon-expandable valves are expanded at the annular plane (i.e., intra-annular valves) with balloon inflation during deployment; self-expanding valves spontaneously expand and deploy upon retraction of the delivery sheath, with the functional zone positioned above the native annulus (i.e., supra-annular valves).

Balloon-expandable valves offer a higher degree of controllability, allowing physicians to adjust the valve deployment size. They cause less damage to cardiac structures and are associated with a lower pacemaker implantation rate, making them more suitable for cases with uniform calcification distribution. Balloon-expandable valves are the mainstream choice abroad.

VCBeat has learned that in the R&D layout of balloon-expandable valves, New Pulse Medical's Prizvalve transcatheter aortic valve system has officially entered into registration clinical trials, marking it as the first domestically produced balloon-expandable valve.

Self-expanding valves are more suitable for cases with uneven calcification distribution, as the skirt can better conform to the anatomical structure. Self-expanding valves can be implanted in a supra-annular position, have lower requirements for circular expansion, and provide stronger radial support; however, they are relatively more difficult to control and may easily damage myocardial structures.In the clinical data for first-generation self-expanding valves, the incidence of permanent pacemaker implantation associated with self-expanding valves was several times higher than that with balloon-expandable valves. With the introduction of second-generation self-expanding valves, the pacemaker implantation rate has decreased significantly.

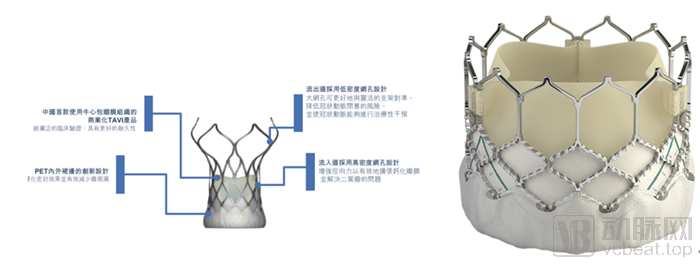

MicroPort CardioFlow’s self-expanding valve (left) Edwards Lifesciences’ balloon-expandable valve (right)

When selecting TAVR devices, physicians consider not only the valve type but also focus on key factors such as radial force, incidence of paravalvular leak post-implantation, pacemaker implantation rate, valve deployment depth and positioning, and durability.

Paravalvular leak is a major complication following transcatheter aortic valve replacement (TAVR), which can lead to atrial fibrillation, pulmonary hypertension, and even heart failure. To address this challenge, some transcatheter heart valve products feature a skirt attached to the outer periphery of the stent frame; this skirt design optimizes sealing efficacy, thereby reducing paravalvular leak and regurgitation.

The pacemaker implantation rate has drawn attention because mechanical compression of the cardiac conduction system by prosthetic valves, particularly self-expanding valves (at the inflow end), can lead to new-onset conduction block after TAVR (referring to slowed or blocked impulse conduction at any site within the cardiac conduction system).

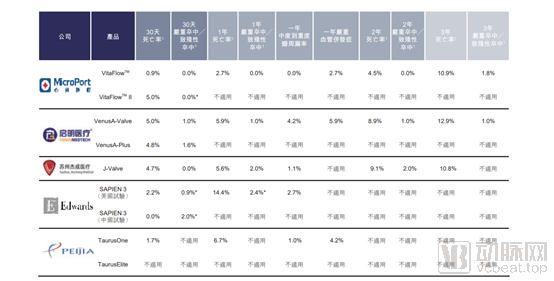

Having understood the key performance indicators of TAVR products can help us better understand the differences among several major domestic products. Based on clinical trial data and expert presentations from the TAVR special session at the 2019 Chengdu International Conference on Interventional Treatment of Valvular Heart Disease, VCBeat has summarized the characteristics of the currently major valve products in China.

VenusA by Venus MedtechIt was the first valve in China to undergo clinical trials. Due to the high prevalence of severe calcification and bicuspid aortic valves among Chinese patients, a self-expanding valve was chosen for development. Professor Wu Yongjian from Fuwai Hospital commented that VenusA exhibits strong radial force, with an overall five-year mortality rate of 20% (cardiovascular mortality approximately 15%). A key feature of Venus MedTech’s second-generation product is its retrievability, which holds significant importance for market promotion in China. For beginners, inadequate deployment or positional shifts during release can lead to substantial paravalvular leakage; therefore, retrievable products are more user-friendly for novices. Furthermore, successful implantation in complex lesions is difficult to achieve in a single attempt. Retrievable products enable more precise implantation, reduce the need for pacemakers and surgical assistance, and lead to better prognostic outcomes.

Edwards Lifesciences' SAPIEN 3As an advanced version, the SAPIEN 3 is taller than its predecessor, facilitating easier positioning by physicians. Its peripheral skirt significantly reduces paravalvular leakage. Compared with other self-expanding valves, the SAPIEN 3 is shorter; its greatest advantage lies in providing favorable access for future coronary interventions when used in low-risk patients. Additionally, the annulus size can be controlled via balloon expansion, and the delivery system features adjustable deflectability, offering advantages in navigating tortuous aortic anatomy and substantially reducing perioperative mortality.

Peijia's TaurusOneIn terms of design, it is a self-expanding valve made from bovine pericardium and features a sealing skirt. Additionally, considering that some patients may require re-intervention due to coronary artery issues, the TaurusOne valve leaflets are designed with a lower profile to facilitate future coronary access. Currently, Peijia’s second-generation product is also undergoing clinical trials and likewise features retrievability.

MicroPort CardioFlow's VitaFlowThe system features an electric handle that enables more precise deployment and offers easier operation for physicians. VitaFlow has also developed a double-skirt design, which achieves lower all-cause mortality and reduced rates of postoperative complications. The second-generation VitaFlow product incorporates a recapturable feature, making TAVR procedures safer and more precise.

Clinical Trial Data of Major TAVR Products in ChinaData Source: MicroPort CardioFlow Prospectus

Overall, clinical trial data indicate that domestically produced valve prostheses each have their own characteristics. Clinicians typically select a valve based on a thorough understanding of the product’s features and the patient’s specific disease profile.For TAVR products already on the market, long-term postoperative follow-up and market surveillance are still required to further monitor the long-term safety and effectiveness of the products. Meanwhile, valuable long-term clinical data also help enhance physicians’ acceptance of the products.

Currently, domestic companies are focusing on their second-generation products, but these have generally not yet been launched on the market, and TAVR products are still undergoing iterative updates.According to the product life cycle of vascular interventional devices, the market typically experiences an explosive growth within five years after the launch of high-quality products.

H1 2020 Operating Data Comparison (MicroPort CardioFlow data covers January–July 2020)

From an operational perspective, all three companies remain in deficit, with substantial R&D expenditures.

Therefore, we believe that from the perspectives of product offerings, procedural volume, and market size, the TAVR market is still in its nascent stage, currently in a growth phase, with an unsettled competitive landscape.

From the nascent stage of intense competition to a landscape of fragmented dominance in the TAVR market,We believe that commercial promotion capabilities in Grade A tertiary hospitals located in first- and second-tier cities are core.

According to Frost & Sullivan, it is estimated that 73.5% of TAVR procedures in China will be performed at the top 20 TAVR hospitals in 2020.

According to relevant expert consensus,Compared with SAVR, TAVR imposes higher requirements on hospital qualifications and infrastructure.TAVR procedures should be performed in hybrid operating rooms or modified cardiac catheterization laboratories, which must be equipped with DSA, anesthesia, echocardiography, and cardiopulmonary bypass equipment.

Furthermore, hospitals performing more than 400 percutaneous coronary interventions (PCIs) annually are considered qualified to conduct transcatheter aortic valve replacement (TAVR) procedures. TAVR procedures should be performed by a multidisciplinary heart team comprising 2–3 interventional cardiologists (each performing more than 200 interventional procedures annually), 1–2 cardiac surgeons, one radiologist, one anesthesiologist, one echocardiographer, and 2–3 nurses. Physicians must also complete 20–30 TAVR procedures as part of the learning curve to master the core skills required for TAVR.

According to data from a paper by Director Zhang Haibo of Anzhen Hospital, there are currently 150 centers in China capable of performing transcatheter aortic valve replacement (TAVR) procedures, with approximately 10 institutions having cumulatively performed more than 100 cases. (Zhang Haibo, Meng Xu. History and Current Status of Transcatheter Aortic Valve Replacement. Chinese Journal of Cardiovascular Research, 2020, 18(4): 289-294)

These stringent prerequisites dictate that TAVR procedures are currently primarily conducted at core hospitals in first- and second-tier cities, and consequently, commercialized TAVR products in China will mainly compete within these institutions.

Unlocking the Chinese market and increasing TAVR penetration rate have become challenges currently faced by all TAVR manufacturers.

To increase penetration in the Chinese market, MicroPort CardioFlow leverages the strong brand recognition of its parent company, MicroPort Medical, in the cardiology field, and has adopted two major strategies:First, target the top 20 hospitals performing TAVR to accelerate penetration into these key institutions; second, maintain long-term engagement and communication with key opinion leaders.

Prospectus data show that MicroPort CardioFlow’s VitaFlow received approval two years later than Venus MedTech, launching in July 2019. As of July 31, 2020, domestic shipments of VitaFlow reached 872 units. Of these, 601 units were shipped in the first seven months of 2020, covering 120 hospitals, including 18 of the top 20 hospitals by TAVR procedure volume.

MicroPort CardioFlow has demonstrated strong performance in its core markets. In September 2020, VitaFlow became the first TAVR product to receive a settlement code for medical equipment/devices under the Shanghai Basic Medical Insurance scheme. Shanghai is one of the cities in China with the highest number of hospitals qualified to perform TAVR procedures. VitaFlow has successfully penetrated the majority of these qualified hospitals in Shanghai.

Venus Medtech’s performance is equally impressive. According to data released by Venus Medtech, the company completed approximately 2,200 transcatheter aortic valve replacement (TAVR) procedures in China in 2020, representing a year-on-year increase of more than 50% compared with 2019 (Note: Sales figures are based on the number of implants at end-user hospitals, not shipment volumes). Since its product launch, nearly 5,000 patients have benefited from the cumulative number of procedures performed.

Regarding the pace of TAVR procedure adoption, an industry investor interviewed by VCBeat stated that hospitals and physicians in China have gained considerable recognition for TAVR, using the ability to perform TAVR procedures as a benchmark for assessing physician competency and hospital capability. This consensus will accelerate the promotion of TAVR procedures in China.

TAVR is the primary battlefield at present, but in the future, we believe the yet-to-be-developed mitral and tricuspid valve markets hold greater promise.

As previously mentioned, in 2019, patients with aortic stenosis, mitral regurgitation, and tricuspid regurgitation accounted for 11.8%, 29.2%, and 25.1% of all valvular heart disease cases in China, respectively. Compared with aortic valve diseases, mitral and tricuspid valve diseases exhibit higher incidence rates. With technological breakthroughs and continued refinement, this market is poised to unleash significant potential in the future.

However, the field of mitral regurgitation still faces numerous challenges and difficulties that require technological innovation and breakthroughs for resolution. Currently, only six approved transcatheter mitral valve repair products and one approved transcatheter mitral valve replacement product have reached the commercialization stage globally, among which only one transcatheter mitral valve repair product has been approved in China. Furthermore, the approved mitral valve replacement product is suitable only for patients with mitral regurgitation exhibiting specific characteristics, representing a limited subset of the overall patient population. Most existing transcatheter mitral valve technologies suffer from several clinical limitations.

In the mitral valve market, which faces significant unmet needs, both Edwards Lifesciences and Abbott have identified mitral valve therapies as a key strategic focus for the next decade. The global mitral valve market is projected to reach $3 billion by 2025.

Abbott is currently the leader in the mitral valve market. Its mitral valve repair device, MitraClip, was launched in the United States in 2013 and remains the only transcatheter mitral valve repair product approved in the U.S. MitraClip is also a primary growth driver for Abbott’s structural heart disease business. According to JP Morgan data, MitraClip generated approximately $690 million in sales in 2019 and is expected to generate approximately $670 million in revenue in 2020.

This market is also a key focus for companies in the valve sector. By reviewing the main pipeline layouts of MicroPort CardioFlow, Qiming Medical, and Peijia Medical, we found that both mitral and tricuspid valves are central to their strategies. Notably, MicroPort CardioFlow has strategically prioritized common mitral valve diseases through targeted investments.

MicroPort CardioFlow Makes Strategic Investments in ValCare and 4C Medical. 4C Medical is primarily engaged in the research and development of mitral and tricuspid valve devices in the United States. By investing in ValCare and 4C Medical, MicroPort CardioFlow has enriched its product portfolio in the mitral and tricuspid valve markets, which may help the company secure a first-mover advantage in these sectors in the future.

Note: Black text indicates products that have been approved for marketing in China. In addition to its valve product line, Peijia Medical also has a neurointerventional product line; only its valve products are listed in the figure.

Behind these cardiac “doors,” more stories await. For the three Chinese companies, their products have not yet achieved large-scale commercialization; market launch is not the end point, but merely a new beginning.