Aohua Endoscopy and Shenda Endoscope File for IPO to Challenge Olympus, Whose Endoscopy Revenue Exceeds RMB 26.3 Billion

Endoscopes are commonly used medical devices that can access the human body through natural or artificially created pathways, assisting physicians in diagnosing or treating localized lesions more efficiently and conveniently.

Since its inception in the 19th century, endoscopy has undergone continuous development and is now widely applied across various medical specialties, including gastroenterology, pulmonology, general surgery, otolaryngology, orthopedics, urology, and gynecology, becoming a vital tool for medical diagnosis and treatment. To date, four generations of endoscopes have been developed: rigid endoscopes, semi-flexible endoscopes, fiber-optic endoscopes, and electronic video endoscopes. Owing to their superior image quality, electronic video endoscopes have become the mainstream products in the market.

The “Latest National Cancer Report 2019” released by the National Cancer Center showed that in 2015, the estimated number of new cases of malignant tumors in China was 3.929 million, among whichOver 1 Million New Cancer Cases in the Gastrointestinal Tract. Gastric cancer, colorectal cancer, and esophageal cancer are the three most common gastrointestinal cancers, ranking second, fourth, and fifth, respectively, in China, with their incidence rates all showing an upward trend.

Gastrointestinal endoscopy is the gold standard for screening and diagnosing gastrointestinal diseases.. According to professional physicians,Gastrointestinal cancers, including gastric cancer, colorectal cancer, and esophageal cancer, are all mucosal lesions; early detection yields an extremely high cure rate.. However, the penetration rate of gastrointestinal endoscopy screening in China is extremely low, with an early diagnosis rate for gastrointestinal cancers of less than 10%, whereas the rates in Japan and South Korea are as high as 70% and 55%, respectively.Therefore, the widespread adoption of gastrointestinal endoscopy screening is urgently needed.。

In addition, with the growing demand for minimally invasive treatments, endoscopes used in minimally invasive surgeries are once again poised for significant growth. According to data released by Evaluate MedTech,The global endoscope market reached a sales volume of $20.9 billion in 2019, and is expected to continue growing at a compound annual growth rate (CAGR) of 6.3% over the next five years, reaching $28.3 billion by 2024.。

Despite the booming endoscopy market, domestic endoscopy companies in China still face significant challenges. In the Chinese market, overseas giants such as Olympus, Karl Storz, and Stryker collectively account for 90% of the endoscopy market share, making it a major challenge for domestic brands to break through this dominance.

To explore the future of gastrointestinal endoscopy, VCBeat has compiled an overview of companies, products, and development roadmaps in China’s gastrointestinal endoscopy sector, aiming to provide reference for the industry.

Undoubtedly, numerous factors—including China’s economic development, rising health awareness and consumption levels among residents, advancements in supporting manufacturing processes, and policies encouraging innovation—are favorable to the healthcare industry and related sectors. We focus on the endoscopy industry, first because of its rapid market growth:From 2013 to 2017, the endoscopy market size grew from RMB 10.2 billion to RMB 19.9 billion, with a compound annual growth rate (CAGR) of over 18.23%. Frost & Sullivan projects that the endoscopy industry will reach RMB 32 billion by 2022.。

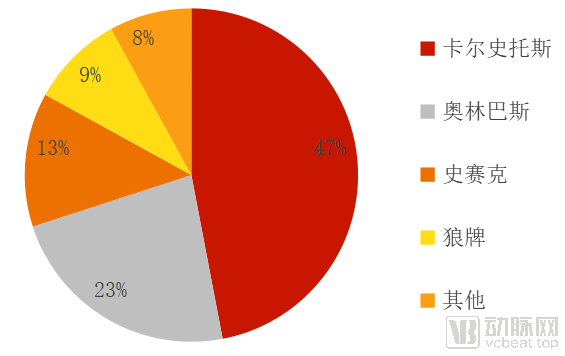

Second, there is significant potential for domestic substitution in this industry. Endoscopes are categorized into rigid and flexible endoscopes based on whether the scope body can be steered. According to the "2019 Report on the Development of China's Medical Device Industry," overseas giants hold more than 90% of the market share for rigid endoscopes in China. Specifically, Karl Storz, Olympus, Stryker, and Wolf account for 47%, 23%, 13%, and 9% of China's rigid endoscope market, respectively.

Data Source: China Medical Device Industry Development Report 2019

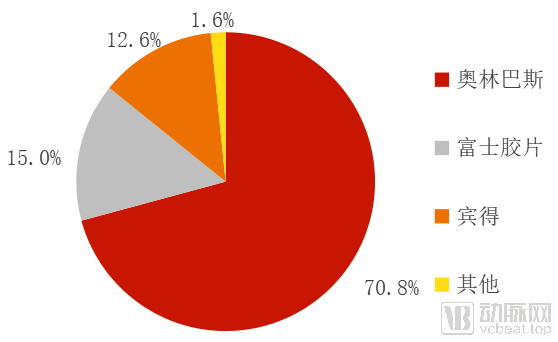

Compared with rigid endoscopes, flexible endoscopes present higher technical barriers. Overseas giants such as Olympus, Fujifilm, and Pentax hold 70.8%, 15%, and 12.6% of the Chinese market for flexible endoscopes, respectively.

Data Source: 2019 Report on the Development of China's Medical Device Industry

It is evident that,China’s endoscopy market offers substantial room for domestic substitution, presenting significant growth opportunities for Chinese brands.。

Currently, China has achieved domestic substitution in multiple high-value consumable sectors, including coronary stents, with domestic companies capturing over 60% of the market share. Based on the trajectory of domestic substitution in these sectors, China’s endoscopy field is currently in the early stages of domestic substitution.Domestic brands are poised to capture the majority share of the endoscopy market, yielding substantial returns for industry players.。

Customs data show that both the import and export values of endoscopes in China are on an upward trend; however, import values exceed export values, leading to a widening trade deficit year by year.

(Import and Export Situation of China's Endoscopy Industry)

Based on the above data analysis,China's endoscope market size is expanding year by year, and the penetration rate of endoscopes is steadily increasing.. With the improvement of China's economic level and residents' consumption level, the endoscope market will continue to grow. In addition, Chinese endoscope companies are continuously upgrading technology, innovating products, and accelerating promotion, which has led to a year-on-year increase in export value and an increased likelihood of domestic substitution.

To achieve domestic substitution, Chinese companies must surpass their international counterparts technologically. Therefore, we must understand what innovations overseas giants are currently pursuing and in which directions they are heading.

Olympus

Olympus entered the Chinese market as early as the 1970s and now holds a 23% share of China’s rigid endoscope market and a 70.8% share of the flexible endoscope market. In 2019, Olympus’s endoscopy business generated approximately RMB 26.3 billion in revenue.

Currently, Olympus’s endoscopy product portfolio includes gastrointestinal endoscopes, cholangioscopes, laparoscopes, electronic gastrosopes, cystoscopes, ureteroscopes, percutaneous nephroscopes, hysteroscopes, colposcopes, bronchoscopes, and ENT endoscopes. The company primarily focuses on flexible endoscopes and holds the majority of the global market share for flexible endoscopes.

In 2005, Olympus introduced Narrow Band Imaging (NBI) technology. This technique enhances the visibility of early-stage cancerous lesions under specialized blue light illumination, thereby facilitating earlier detection by physicians. Since then, NBI has gradually become the most widely used optical digital method in endoscopic examinations. Leveraging its first-mover advantage, Olympus has maintained a leading position in NBI technology.

In 2017, Olympus applied 3D technology to endoscopes, rendering endoscopic images more three-dimensional and facilitating easier localization. In 2018, Olympus launched its 4K ultra-high-definition endoscopy system in China, delivering clearer endoscopic images. In 2020, Olympus integrated 3D and 4K technologies into its endoscopic systems to assist physicians in performing minimally invasive surgeries more effectively. Also in 2020, Olympus announced the application of AI technology in endoscopic examinations to improve diagnostic speed and efficiency.。

In 2021,OlympusAnnouncementWill acquire Dutch photonics equipment company Quest for $60.7 million, a deal aimed at strengthening its surgical endoscopy capabilities.Quest can provideFluorescence ImagingAmong such technologies, the most mature product is the Quest Spectral Fluorescence Imaging System, which provides fluorescence imaging guidance for both open and minimally invasive surgeries.

Furthermore, Olympus has long been developing its Medical Technology Training Center to train endoscopists and promote the widespread adoption of endoscopy.

Fujifilm

Fujifilm entered the Chinese market in 2001. Unlike Olympus, Fujifilm offers a comprehensive product portfolio including endoscopic ultrasound (EUS) systems, laser endoscopes, electronic gastrointestinal endoscopes, and double-balloon enteroscopes. Products such as endoscopic ultrasound and laser endoscopes integrate ultrasound or laser technologies with endoscopy, respectively, providing physicians with richer imaging information.

Unlike the Narrow Band Imaging (NBI) technology developed by Olympus, Fujifilm’s Linked Color Imaging (LCI) enhances the colors of mucosa and blood vessels to improve color contrast, thereby facilitating precise diagnosis of lesions. Additionally, Fujifilm’s Blue Laser Imaging (BLI) concentrates and amplifies light at specific wavelengths, enhancing the visibility of superficial microvessels and mucosal surface structures, thus enabling more effective diagnosis of early-stage cancer.

In addition to developing higher-definition endoscopes, Fujifilm launched the SYNAPSE VNA medical imaging data platform, the “Fuyi Ruiying” Internet-based cloud film service, and the SYNAPSE 3D three-dimensional image post-processing system in December 2020. SYNAPSE VNA helps healthcare institutions streamline data management, standardize data security, and enrich data applications, while also breaking down data silos and enabling human-computer interaction. The “Fuyi Ruiying” Internet-based cloud film service can be applied in scenarios such as data acquisition, self-service film retrieval, remote image interpretation, and AI analysis, providing diagnostic and treatment support for online healthcare services.

The SYNAPSE 3D post-processing system reconstructs two-dimensional medical images into three-dimensional models, enabling multi-angle stereoscopic visualization. Equipped with Fujifilm’s proprietary recognition engine technology, the system can identify and process various organs. Additionally, it features surgical simulation capabilities, allowing physicians to instantly demonstrate lesion resection plans in 3D mode.

In addition, Fujifilm has long established an endoscopy training center and, like Olympus, is committed to training endoscopists and promoting the widespread adoption of endoscopic applications.

Inventory analysis reveals that endoscopy giants such as Olympus and Fujifilm are increasingly integrating technologies like 3D, 4K, AI, and big data into their endoscopic systems, while launching fewer new hardware products. Additionally, companies like Olympus are heavily investing in training endoscopists to promote the clinical adoption of endoscopy. While these shifts present opportunities for Chinese manufacturers, they will also pose future challenges, particularly in physician education.

Endoscopes are devices that integrate multidisciplinary technologies, including optics, electronics, structural engineering, and materials science, presenting extremely high technical barriers. For domestic companies, challenges persist in talent, technology, patents, manufacturing processes, and brand recognition: overseas giants do not establish R&D centers in China, leading to a shortage of relevant local talent; their early establishment of patent barriers has made it more difficult for Chinese firms to overcome patent restrictions; moreover, most endoscope manufacturers in China are small in scale and have weaknesses in manufacturing processes and optical technologies.

It is evident that numerous factors have constrained the development of domestic endoscope manufacturers. How, then, can Chinese endoscope companies break through technological blockades? How can they address their weaknesses? And how can they achieve import substitution with domestically produced alternatives?

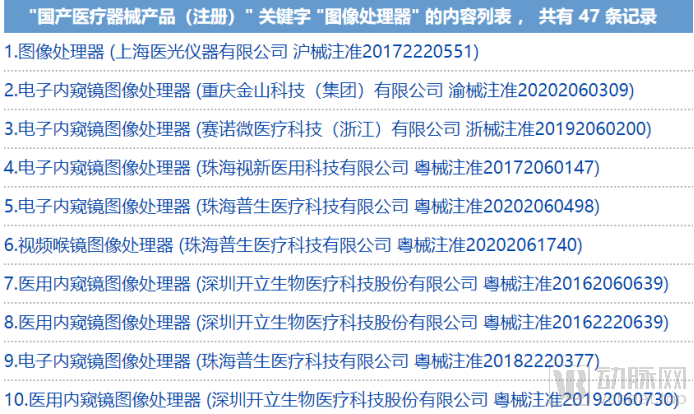

Data indicates that the core components of an endoscope include the lens, image sensor, image processor, and light source. Currently, domestic enterprises in China have achieved breakthroughs in these core components; future efforts should focus on enhancing product performance to facilitate the advancement of domestically produced endoscopes toward the high-end market. For instance, VCBeat searched the National Medical Products Administration (NMPA) website using the keyword “cold light source” and identified 116 approved products; a search using the keyword “image processor” yielded 47 approved products.

(Data source: National Medical Products Administration)

As for image sensors, Chinese companies have also developed solutions. Endoscopic image sensors can be divided into charge-coupled devices (CCD) and complementary metal-oxide-semiconductor (CMOS) devices. CCD technology is monopolized by a few foreign companies, while CMOS technology is gaining momentum globally. Technologically, CMOS offers advantages such as small size, low power consumption, low cost, and high system integration, making it poised to become the mainstream sensor technology. Currently, many companies (including domestic firms and overseas giants) have applied CMOS technology to medical endoscopes and launched multiple new products. Furthermore, Chinese companies are making rapid progress in CMOS technology, narrowing the gap with overseas counterparts, thus presenting significant opportunities for technological breakthroughs through CMOS image sensors.

In summary,Chinese endoscopy companies have significant opportunities to achieve "generational leaps" through innovation in core endoscopic components and to realize import substitution with high-performance domestic products.。

Endoscopes come in various types.

Based on whether the scope can change direction, endoscopes can be divided into rigid endoscopes and flexible endoscopes. The global endoscope market includes rigid endoscopes, flexible endoscopes, endoscopic accessories, and equipment. According to publicly available data, flexible endoscopes account for 27.6% of the total endoscope market, while rigid endoscopes account for 22.20%, with the remaining market share comprising endoscopic accessories and equipment.

Based on the anatomical sites accessed, endoscopes can be classified into sinus scopes, laryngoscopes, neuroendoscopes, cystoscopes, laparoscopes, arthroscopes, gastroscopes, and colonoscopes. Among these, esophagoscopes, gastroscopes, duodenoscopes, colonoscopes, enteroscopes, and cholangioscopes belong to the category of gastrointestinal endoscopes. According to 2016 data from Endoscope BBC Research, thoracoscopes and laparoscopes are currently the most widely used endoscopes, predominantly rigid scopes, accounting for over 30% of the market; gastrointestinal endoscopes account for 14.6%, primarily flexible scopes.

In the field of gastrointestinal endoscopy, according to incomplete statistics from VCBeat, at least 29 companies in China are engaged in the research and development, manufacturing, and sales of gastrointestinal endoscopes. The list of these companies is as follows:

(Data source: VCBeat, compiled from public information)

(Data source: VCBeat, compiled from public information)

Based on the above data, there are 14 upper gastrointestinal endoscopy products, and 12 intestinal endoscopy products such as colonoscopes and sigmoidoscopes. The number of approved capsule endoscopes, choledochoscopes, and esophagoscopes is relatively small. It should be noted that upper gastrointestinal endoscopes can examine the esophagus, stomach, duodenum, and part of the small intestine; lower gastrointestinal endoscopes can examine areas such as the colon and small intestine.

In addition, the products of the aforementioned companies are primarily electronic endoscopes, with only two models of choledochoscopes being fiber-optic endoscopes.

In terms of the market, the aforementioned companies have fully mastered the production and R&D capabilities for low-end gastrointestinal endoscopes; some companies have secured a certain share in the mid-end gastrointestinal endoscope market, while a few have broken the monopoly in the high-end gastrointestinal endoscope market.

Aohua Endoscopy

Aohua Endoscopy, founded in 1994, is one of the earliest companies in China engaged in the research, development, and manufacturing of flexible electronic endoscopes. The company has achieved breakthroughs in multiple key technologies, including optical imaging, image processing, scope design, and electrical control for endoscopes. With certain competitive advantages, it has established a solid presence in the field of flexible endoscopy, and its products have entered markets in developed countries such as Germany, the United Kingdom, and South Korea.

On December 25, 2020, Aohua Endoscopy’s application for listing on the STAR Market was accepted.. According to its prospectus, revenue from its core business grew rapidly from RMB 130 million in 2017 to RMB 290 million in 2019.

(Data source: Aohua Endoscopy Prospectus)

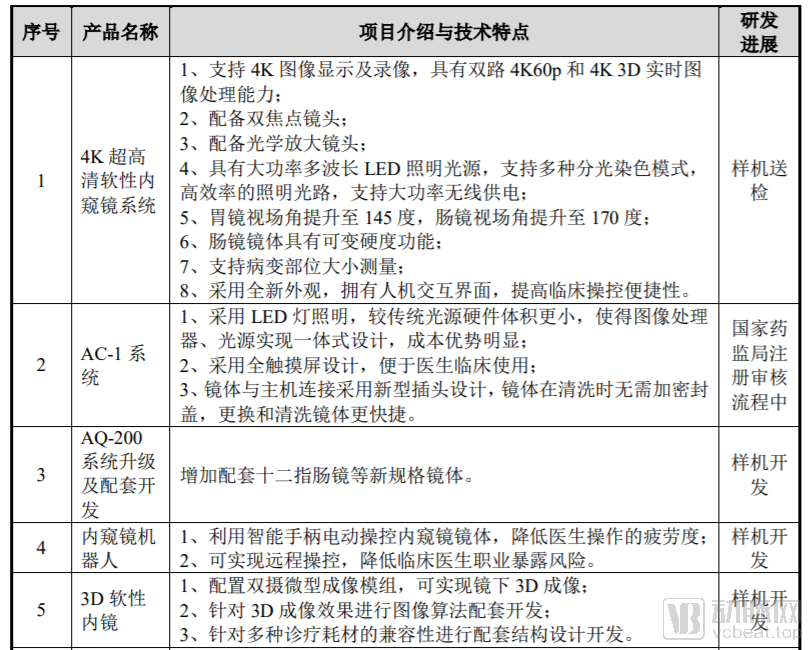

The company’s exceptionally rapid growth is attributable to Aohua Endoscopy’s focus on innovation and continuous enhancement of product performance. In 2013, Aohua Endoscopy launched the AQ-100, China’s first independently developed electronic endoscopy system featuring spectral chromoendoscopy capabilities. In 2018, the company introduced the AQ-200 full-HD optical transmission endoscopy system in the Chinese market. By innovatively adopting laser transmission and wireless power supply technologies, the AQ-200 achieves electrical isolation between devices, significantly improving clinical operational safety and convenience, and offering differentiated competitive advantages compared to mainstream products from foreign manufacturers. In terms of performance, the AQ-200 is equipped with a 1080P imaging module and spectral chromoendoscopy technology, delivering clearer images.

At this stage, Aohua Endoscopy continues to prioritize R&D and is actively developing products such as 4K ultra-high-definition flexible endoscopy systems, 3D flexible endoscopes, AI-assisted diagnostic and therapeutic technologies, and endoscopic robots.

(Partial R&D projects of Aohua Endoscopy; data source: Aohua Endoscopy’s prospectus)

Tiansong Medical

Tiansong Medical, established in 1998, is a high-tech enterprise specializing in the research and development, manufacturing, sales, and service of endoscopic minimally invasive medical devices.Listed on the New Third Board on January 24, 2014In July 2019, Tiansong Medical entered the pre-IPO tutoring period; in August 2020, Tiansong Medical terminated the IPO tutoring process based on the company’s strategic development needs.

Tiansong Medical’s R&D and manufacturing portfolio includes esophagoscopes, sigmoidoscopes, rectoscopes, and other endoscopes that cover multiple specialties such as otolaryngology, surgery, and gynecology, with more than 2,700 specifications and models. Tiansong Medical’s endoscope products not only serve domestic medical institutions and patients in China but are also exported to over 40 countries and regions worldwide.

From 2017 to 2019, Tiansong Medical's revenue from its core business grew from RMB 98.61 million to RMB 115 million, while its R&D expenses increased from RMB 2.698 million to RMB 7.66 million.

(Tiansong Medical’s Revenue and R&D Status, Data Source: Tiansong Medical Annual Report)

Currently, Tiansong Medical possesses multiple independent intellectual property rights and core technologies, having obtained 200 valid patents, including 50 invention patents and 142 utility model patents.

In addition, Tiansong Medical has developed multiple key new products designated at the national level, including intervertebral disc endoscopes, powered sinus surgical knives, and radiofrequency plasma resectoscopes.

Shenda Endoscope

Shenda Endoscopy, established in the 1980s, is an enterprise engaged in the research and development, manufacturing, and sales of medical rigid endoscopes, minimally invasive surgical instruments, and medical electrical products. Currently, Shenda Endoscopy offers more than 1,000 product varieties and specifications, covering departments such as urology, gynecology, and proctology.

Data shows that Shenda Endoscopy completed a RMB 130 million Series B financing round in January 2021, co-led by Jinding Capital and Chuangrui Investment, with Hangshi Investment participating as a follow-on investor. The funds raised will be primarily used for the research, development, and upgrading of new products, as well as channel construction.and join hands with CITIC to accelerate the IPO process。

According to reports, Shenda Endoscopy developed China’s first set of fiber-optic cystoscopes, arthroscopes, and resectoscopes in the field of endoscopy. Additionally, its “Disposable Protective System for Flexible Endoscopes” is a world-first product developed to prevent iatrogenic cross-infection.

Currently, Shenda Endoscopy holds 68 medical device registration certificates and nearly 30 patents.

Sonoscape

Sonoscape Medical was established in 2002, with its business primarily comprising ultrasound diagnostic systems, electronic endoscopy systems, and in vitro diagnostic products.In 2017, Sonoscape Medical was listed on the ChiNext board of the Shenzhen Stock Exchange.。

In the endoscopy field, Sonoscape’s R&D and manufactured product series—including the HD350, HD400, HD500, HD550, SV-M2K30, and SV-M4K30—comprehensively cover the high-, mid-, and low-end markets for flexible endoscopes as well as the rigid endoscope market.

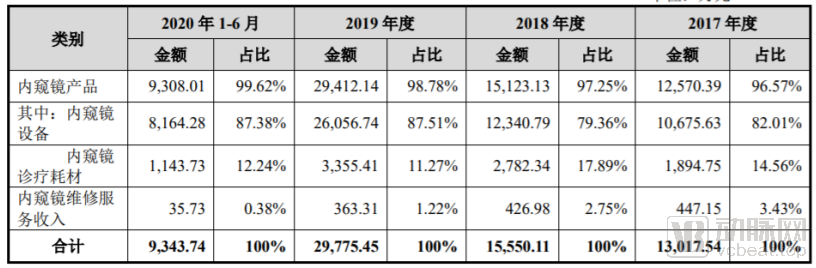

Sonoscape has made substantial investments in research and development (R&D). In 2017, 2018, and 2019, the company’s R&D expenditures amounted to RMB 177 million, RMB 233 million, and RMB 255 million, respectively, accounting for 17.89%, 19.03%, and 20.33% of its total revenue.

Sonoscape’s endoscopy business has seen year-on-year revenue growth, surging from its market entry in 2017 to RMB 292 million in 2019.

(Data source: Sonoscape Medical Annual Report)

Sonoscape Medical’s annual report reveals that, through in-depth development of core technologies, the company has launched products such as a full-HD flexible gastrointestinal endoscopy system, a three-chip 2K rigid endoscope, and a 4K rigid endoscopy system. It currently possesses multiple advanced endoscopic technologies and processes, including spectral imaging technology, photoelectric composite chromoendoscopy imaging, high-definition real-time image processing, optical micro-module packaging, high-performance endoscope body manufacturing, ultrasound probes for endoscopy, and flexible endoscope body fabrication. Its independently developed HD-500 and HD-550 series of high-definition endoscopes represent the leading level of domestically produced endoscopes in China.

In January 2021, Sonoscape Medical developed4K Ultra-HD Medical Endoscopic Camera SystemApproved by the Guangdong Provincial Medical Products Administration. The system employs a low-power 3CMOS ultra-high-definition image sensor chip, delivering video output with a maximum resolution of no less than 4K, and is suitable for all levels of surgery (Grades 1–4).

Anhan Technology

Anhan Technology, established in 2009, is a high-tech enterprise engaged in the research and development, manufacturing, and commercialization of innovative medical devices. Anhan Technology holds nearly 200 authorized patents domestically and internationally, and has achieved multiple breakthroughs in fields such as precise magnetic control technology, artificial intelligence, and telemedicine.

The magnetically controlled capsule endoscopy system, innovatively developed by Anhan Technology, enables patients to undergo endoscopic examination simply by swallowing a capsule-sized endoscope. After entering the patient’s mouth, the capsule endoscope moves along the esophagus, stomach, small intestine, and large intestine, propelled by gastrointestinal motility. It continuously captures images of the lumen and transmits them in real time via wireless signals to an image recorder. Physicians can then analyze the patient’s gastrointestinal conditions using an imaging workstation.

Compared with electronic endoscopy, capsule endoscopy requires no intubation, is wire-free, non-invasive, and painless for patients, earning it the title of a new generation of endoscopic products. Currently, magnetically controlled capsule endoscopy is primarily used to examine digestive tract regions such as the stomach, small intestine, and esophagus.

According to reports, Anhan Technology’s capsule endoscopy products have been widely promoted in China and exported to the United Kingdom, France, Denmark, Sweden, Hungary, the United Arab Emirates, and other regions.

In 2019, AnHan Technology applied 5G technology to capsule gastroscopy and collaborated with experts to conduct demonstrations of remote 5G-controlled magnetic capsule gastroscopy. In 2020, in response to epidemic prevention and control needs, AnHan Technology innovatively developed a mobile examination vehicle for magnetic-controlled capsule gastroscopy, facilitating contactless endoscopic examinations and preventing cross-infection.

Jinshan Technology

Jinshan Technology, established in 1998, is a national high-tech enterprise integrating the research and development, manufacturing, sales, and service of digital medical equipment. Its innovative product, the magnetically controlled capsule endoscope, has been widely used in more than 70 countries and regions, including China, Spain, Italy, the United Kingdom, Germany, Russia, Canada, and India.

In 2020, Jinshan Technology launched its new products: the SC100 HD Small Bowel Capsule Endoscope, the NCG100 HD Magnetically Controlled Capsule Gastroscope, and the NC100 Magnetically Controlled Gastrointestinal Integrated Capsule.

The HD Small Bowel Capsule SC100 features a high-definition resolution of 512×512, delivering threefold clarity to better visualize small bowel details. With a 12-hour operating duration and a 160° field of view, it facilitates accurate capture of small bowel lesions. Additionally, it leverages AI technology to automatically filter out redundant images, thereby reducing the workload for image reviewers and enhancing diagnostic efficiency and accuracy.

The magnetically controlled gastrointestinal capsule NC-100 meets the need for integrated examination of the stomach and small intestine, enabling comprehensive assessment of both the gastric region and small intestinal blind spots with just a single capsule.

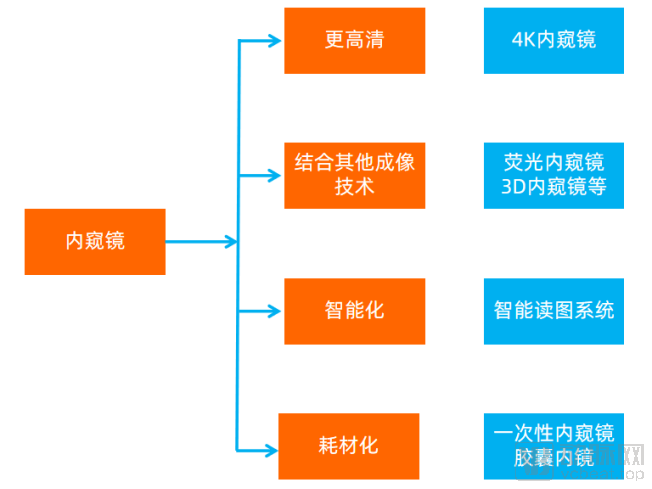

Based on the development of enterprises both domestically and internationally, we can observe that endoscopes are evolving toward higher definition, greater intelligence, and increased disposability.

Currently, companies such as Olympus and Sonoscape have launched 4K endoscopy systems, while other enterprises are accelerating their research and development efforts. The 4K endoscopy system requires upgrades and iterations of core components, including current data acquisition devices and image processing systems, presenting certain technical barriers. Endoscopy manufacturers have introduced 4K endoscopy systems in recognition of the significant application value of ultra-high-definition endoscopy:

As the penetration rate of minimally invasive surgeries continues to rise, the endoscopy market is also expanding rapidly. Meanwhile, physicians are placing higher demands on endoscopic image quality to facilitate more precise execution of minimally invasive procedures. Furthermore, clinicians are continuously innovating surgical techniques based on endoscopic systems, thereby driving the diversification of minimally invasive surgeries. For example, current endoscope-based minimally invasive procedures have already encompassed the removal of foreign bodies from the abdominal cavity,Esophageal Stricture Dilation、Stent Implantation, and various other procedures such as early-stage gastrointestinal cancer resection. In the future, ultra-high-definition endoscopes will enable physicians to innovate more minimally invasive surgical techniques.

Some companies are also pursuing differentiated innovation by integrating other imaging modalities, such as ultrasound, optical coherence tomography, fluorescence, and confocal microscopy, to launch novel hybrid endoscope products, such asEndoscopic Ultrasound (EUS), Optical Coherence Tomography Endoscopy (OCTE), Fluorescence Endoscopy, Confocal Endoscopy。Combining multiple imaging techniques can provide physicians with richer imaging information, facilitatingPrecise Diagnosis, Lesion Localization, and Targeted Treatment。

It is worth mentioning that,Fluorescence EndoscopeDue to the advantages of broadband spectral imaging,The market size is expanding rapidly, with numerous companies accelerating their strategic deployments.For example, in 2021, Olympus acquired Quest, a fluorescence endoscopy company, for $60.7 million to strengthen its research, development, and manufacturing capabilities in fluorescence endoscopy. Fluorescence endoscopes began to be widely adopted in 2016; prior to this, endoscopy was predominantly based on white-light endoscopes. White-light endoscopy generates images of the superficial layers of human tissues using the 400–700 nm spectral range.Fluorescence endoscopy images are based on the 400–900 nm spectrum, displaying surface images of human tissues and fluorescence imaging of sub-surface tissues.

In terms of software, endoscopy companies are applying AI technology to image processing systems to improve diagnostic efficiency and accuracy. For example, Fujifilm’s internet-based cloud film service features AI analysis capabilities, and Jinshan Technology also uses AI technology to eliminate redundant images.Endoscopy companies are prioritizing the development of AI technologies due to the shortage of endoscopists and the varying levels of image interpretation proficiency among them. With AI-assisted support, physicians can improve both diagnostic efficiency and accuracy.

Due to their complex and intricate structures, endoscopes present significant challenges for disinfection and cleaning. This, in turn, leads to a high risk of cross-infection associated with endoscopic procedures. To address this critical pain point, many companies have begunEndoscope ConsumabilizationExploration. For instance, Lensert has developed a single-use electronic endoscope for retrograde cholangiopancreatography (ERCP), Shenda Endoscopy has launched the world’s first disposable protective system for flexible endoscopes, and Guangzhou Ruipai has completed clinical trials for its two models of single-use endoscopes.In fact, driven by pain points such as endoscope-related cross-infection, the shift toward disposable endoscopes has become an industry consensus.Endoscopy companies need to address technical challenges and cost control issues.

Currently,Capsule endoscopy has transitioned into a disposable endoscopic consumable and has achieved successful commercialization.Anhan Technology, Jinshan Science & Technology, Zifu Medical, and Shangxian Minimally Invasive Medical have all launched capsule endoscopy products, which are sold worldwide. Capsule endoscopy not only eliminates the risk of cross-infection but also holds significant clinical value for examining the small intestine, a blind spot in traditional endoscopic procedures. Furthermore, the painless nature of capsule endoscopy is more favored by patients, facilitating the broader adoption of endoscopic examinations.

(Future Development Directions of Endoscopy)

Nowadays, Chinese domestic enterprises have achieved breakthroughs in the field of high-end endoscopes and are rapidly advancing in technologies such as 3D, 4K, and AI. In the area of next-generation capsule endoscopy, domestic companies are making steady progress, continuously strengthening innovation and launching new products with higher precision and broader indications.

Whether in hardware or software, domestic endoscope manufacturers are accelerating their pursuit of overseas giants. We believe that domestic endoscope manufacturers will inevitably win the domestic market and achieve import substitution!