Private Ophthalmology Chains Rush for IPOs as Ocular Drug R&D Gains Market Attention: Is the 'Spring' of Ophthalmology Here?

As the most important organ among the human sensory systems, the eyes are responsible for acquiring at least 80% of external information. In recent years, driven by factors such as population aging, increased exposure to allergens, and unhealthy lifestyle habits in China, the incidence rates of ocular diseases—including cataracts, myopia, and dry eye syndrome—have been rising year by year.

According to data from the Ministry of Health, the incidence of cataracts among elderly people aged 71–80 in China reaches 29%, while it rises to as high as 48% among those aged 81 and above. In addition, the White Paper on Eye Health in China shows that the overall prevalence of myopia among children and adolescents in China is 53.6%, with the rate among university students exceeding 90%.

Behind the massive data lies the vast market potential of the ophthalmology industry.

In 2020, capital interest in the ophthalmology market remained strong. Although it did not replicate the boom seen in the capital markets in 2018, significant large-scale financing rounds emerged. According to data from VCBeat’s Orange Data Center, seven companies in the ophthalmology sector secured investments exceeding RMB 100 million each in 2020. The successive IPO filings by multiple private ophthalmic hospital groups have once again drawn widespread attention to the ophthalmology market.

VCBeat compiled financing data for 70 domestic ophthalmology companies, and analyzed changes and development in China’s ophthalmology market by examining industry subsectors, key policies, and financing events in the ophthalmology sector in 2020.

Analysis of Investment and Financing in China's Ophthalmology Industry

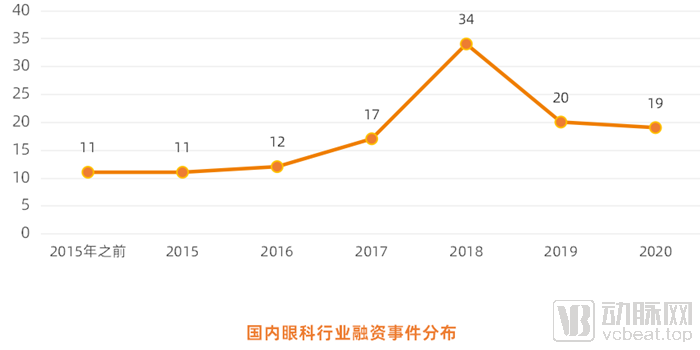

A review of the financing history of domestic ophthalmic companies reveals that funding activities in the ophthalmology sector began to take off in 2015. Prior to 2015, there were only 11 financing events. By 2018, the number of financing deals for Chinese ophthalmic companies surged dramatically, followed by a decline in 2019.

Data Source: VCBeat Data Center

We believe that the sharp increase in total financing in 2018 was largely driven by policy incentives.

In October 2016, the National Health and Family Planning Commission issued the “13th Five-Year Plan for National Eye Health (2016–2020).” The plan outlined seven key measures: improving the service system for prevention and control of eye diseases; strengthening workforce development to promote sustainable growth; preventing and treating major eye diseases that cause blindness and visual impairment; standardizing low-vision rehabilitation services; conducting public education and promotion on eye health; enhancing data collection and informatization; and improving the government-led, multi-stakeholder collaborative working mechanism.

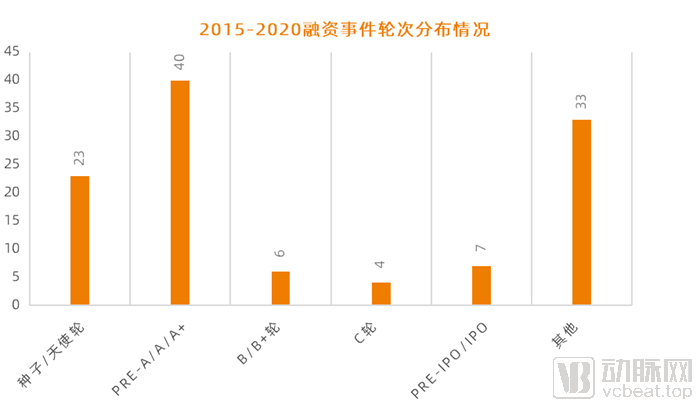

From the perspective of funding round distribution, the vast majority of companies are still in the angel and Series A stages. Although there is already a giant like Aier Eye Hospital in the industry, China's current ophthalmology market still has significant room for growth. As a result, multiple companies have entered the ophthalmology sector, with development remaining in its early stages.

Data Source: Arterial Orange Data Center

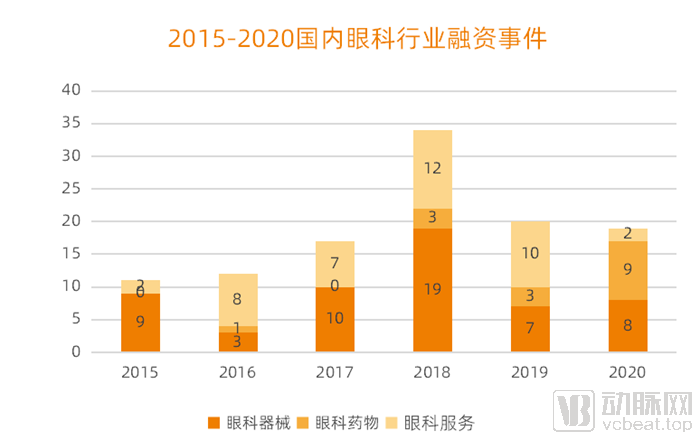

The ophthalmology industry encompasses subsectors such as ophthalmic devices, ophthalmic pharmaceuticals, and ophthalmic medical services. From the perspective of funded enterprises, approximately 49% of financing events between 2015 and 2020 were concentrated in the research and development of ophthalmic devices. Most ophthalmic diseases cannot be cured with medication alone; drugs typically only serve to slow disease progression. Consequently, some patients prefer surgical interventions for definitive treatment. Moreover, given the complexity of ocular anatomy, ophthalmic surgeries are highly dependent on medical devices, making ophthalmic devices play a more critical role compared to ophthalmic drugs.

Data Source: VCBeat Data Center

In terms of the number of financing events, the ophthalmic drug R&D sector is clearly less advantageous; however, from the perspective of financing amounts, it has attracted significant capital attention. To date, among the top five ophthalmic companies by total financing amount, three are engaged in drug R&D (only financing events with publicly disclosed specific amounts are included).

Data Source: VCBeat Orange Data Center (Note: For publicly listed companies, only pre-IPO financing amounts are included)

Zhaoko Ophthalmology is a pharmaceutical R&D company under the listed company Lee's Pharmaceutical Holdings Limited, primarily engaged in the development, manufacturing, and marketing of ophthalmic drugs. Its diversified product portfolio includes small molecules and biologics, as well as novel drugs and generics, covering various ophthalmic indications such as dry eye disease, glaucoma, wet age-related macular degeneration, diabetic retinopathy, corneal injury, and inflammatory diseases.

In October 2020, Zhaokē Ophthalmology completed a $145 million financing round, with investments from institutions including TPG and Hillhouse Capital. In December of the same year, Lee’s Pharmaceutical submitted a listing application to the Hong Kong Stock Exchange, seeking approval for Zhaokē Ophthalmology’s listing on the Main Board of the HKEX.

Founded in 2005, Aier Eye Hospital is a professional chain of ophthalmic medical institutions integrating outpatient services, clinical care, medical treatment, and medical technology development. In 2019, it completed a RMB 400 million Pre-IPO financing round and a RMB 200 million strategic financing round, and submitted its IPO application in July 2020.

Founded in 2016, New Frontier Biosciences is dedicated to the research and drug development of gene therapies for inherited eye diseases. The company has conducted extensive basic research since 2008 and completed the world’s first clinical study of gene therapy for Leber hereditary optic neuropathy (LHON) in 2011. In April 2020, New Frontier Biosciences closed a RMB 130 million Series A financing round led by Sequoia Capital China and Fosun Capital. This February, the company completed a RMB 400 million Series B financing round led by Guofang Capital and Huaxin Capital.

Chaoju Eye Care, formerly known as “Chaoju Eye Clinic,” was established in 1988 and expanded its service network with a focus on North China during its development. As of December 2020, Chaoju Eye Care operated 17 eye hospitals and 23 optometry centers. In January 2021, Chaoju Eye Care made a push for an IPO on the Hong Kong Stock Exchange, filing its listing application on January 4.

Dianjing Biopharma, co-founded by Lilly Asia Ventures and two overseas-returned PhDs, is an ophthalmic biotechnology company dedicated to the development of globally innovative therapies. Headquartered in Suzhou Industrial Park with its R&D center located there, the company also maintains a business office in Shanghai. In November 2020, Dianjing Biopharma completed a $50 million Series A financing round, jointly led by Lilly Asia Ventures, Hillhouse Capital Management (Hillhouse Venture), and Quanchuang Capital.

Policies Continue to Drive Industry Development

In recent years, the state has continuously introduced policy plans targeting specific eye diseases, including goals such as increasing the rate of cataract surgery per million population, strengthening screening and correction of refractive errors in adolescents, and further reducing myopia rates among students of all age groups. Supported by these policies, ophthalmic medical service institutions have gained clear development objectives and policy safeguards, which are conducive to their further growth.

Relevant Policies for the Ophthalmology Industry (Source: Compiled from Public Information)

In June 2020, the National Health Commission released the White Paper on Eye Health in China, stating that it would formulate the 14th Five-Year Plan for National Eye Health by taking into account China’s national conditions and changes in the spectrum of blinding eye diseases. The plan aims to further improve the three-tier blindness prevention and eye health service system, strengthen the development of primary-level ophthalmology professional teams, establish a medical quality control system for ophthalmic services, promote high-quality development of ophthalmic medical services, and strive to meet the growing demand for eye health among the population.

Analysis of the Ophthalmology Market in China in 2020

VCBeat compiled the financing data across all ophthalmology sectors for the full year of 2020, identifying a total of 19 financing events, a figure comparable to that of 2019.

Data Source: VCBeat Orange Data Center

In terms of the distribution of financing amounts, among the 15 companies that have disclosed their figures, 47% secured single-round financing exceeding RMB 100 million.

In terms of the businesses that secured financing, nearly half of the funding events occurred in the field of drug R&D. The ophthalmic services sector, however, deviated from the norm, with only Shikang Ophthalmology and Future Vision, under Shanghai Runer Health Management, obtaining financing. Meanwhile, the ophthalmic devices sector maintained a normal development trajectory.

Ophthalmic Devices: Import Substitution of Mid-to-High-End Consumables and Equipment Begins

Ophthalmic devices encompass two major sectors: ophthalmic surgery and vision care. The ophthalmic surgery sector includes products, consumables, and equipment used in various ophthalmic surgical procedures, while vision care products include contact lenses and eye health products (such as over-the-counter eye drops and contact lens solutions).

Currently, the vast majority of the domestic ophthalmic device market in China is dominated by foreign companies such as Alcon, Essilor, and Johnson & Johnson. For a long time, devices and equipment such as intraocular lenses, contact lenses, and refractive surgery systems have been heavily reliant on imports. Relevant data show that in 2017, China’s imports of ophthalmic devices amounted to RMB 7.56 billion, accounting for approximately 40% of the domestic ophthalmic medical device market size.

In recent years, multiple domestic manufacturers have continuously intensified their efforts in the mid-to-high-end ophthalmic medical consumables market. Companies such as Aierbo Nuode (Aibo Medical), Leiming Shikang, and Oupu Kangshi (Alpha Corporation) have launched a series of products with independent intellectual property rights, including intraocular lenses (IOLs) and orthokeratology (OK) lenses, gradually initiating the path toward import substitution.

In July 2020, Aierbo Nuode listed on the STAR Market, becoming the first ophthalmic medical device company in China to complete an IPO on this board, once again drawing market attention to ophthalmic devices.

In terms of device R&D, domestic enterprises have also embarked on the path of localization. Taking ophthalmic OCT (optical coherence tomography) devices as an example, data from the NMPA shows that 10 products have been approved for market launch in China, with some companies already making moves toward commercialization.

In recent years, with the advancement of AI technology, numerous companies have attempted to apply AI-assisted diagnostic technologies to the diagnosis of ocular diseases. In August 2020, the National Medical Products Administration approved fundus image-assisted diagnostic software for diabetic retinopathy from Shenzhen Silicon Intelligence Technology and Shanghai Airdoc Intelligent Technology, respectively. These applications are suitable for analyzing bilateral color fundus images of adult patients with diabetes and can provide practicing physicians with auxiliary diagnostic recommendations for diabetic retinopathy.

In addition to the two companies mentioned above, enterprises such as Zhiyuan Huitu, Shanggong Yixin, VoxelCloud, and Baidu Lingyi Zhihui are also integrating AI technology into eye disease screening and have developed corresponding diagnostic platforms and software.

Ophthalmic Drugs: Accelerated R&D of Anti-VEGF Agents, Gene Therapy May Become a Breakthrough in Ophthalmic Treatment

Similar to the ophthalmic device market, the domestic ophthalmic drug market in China is still dominated by foreign companies such as Santen Pharmaceutical, Novartis, and Alcon. According to data from Menet, imported drugs accounted for 64.08% of ophthalmic drug usage in public hospitals in key provinces and cities across China in 2018, while domestically produced drugs accounted for only 35.92%.

In the field of new drug development, constrained by the slow progress in basic research on the etiologies of ophthalmic diseases, most companies focus their R&D efforts on developing improved manufacturing processes and novel formulations for already-approved drugs, rather than discovering new targets or mechanisms of action.

In recent years, anti-vascular endothelial growth factor (VEGF) drugs have emerged as a prominent force, widely regarded within the industry as representing the future direction of the ophthalmic pharmaceutical market. VEGF plays a pivotal role in the pathogenesis of various ocular diseases; during disease onset, elevated intraocular VEGF levels promote the formation of abnormal neovascularization, leading to conditions such as macular edema and damage, as well as fibrotic scarring. The use of anti-VEGF agents can inhibit the progression of these ocular diseases, thereby improving vision in the majority of patients with fundus neovascularization.

Currently, there are three anti-VEGF drugs approved for marketing in China: Novartis’s ranibizumab, Kanghong Pharmaceutical’s conbercept, and Bayer’s aflibercept.

According to statistics, in 2019, the sales revenue of ranibizumab injection in Chinese sample hospitals reached RMB 461 million, a year-on-year increase of 44.1%; the sales revenue of conbercept ophthalmic injection in sample hospitals was RMB 422 million, a year-on-year increase of 37.9%.

The potential market opportunities have also prompted companies to compete for strategic positioning. According to data from the Center for Drug Evaluation (CDE) of the National Medical Products Administration (NMPA), a total of 21 applications for clinical trial approvals, production, and other regulatory matters for domestically produced novel ophthalmic drugs were accepted between 2017 and 2020, among which 11 were anti-VEGF agents.

In October 2020, Zhuhai Esun, a subsidiary of Esun Biological, entered into a co-development and exclusive license agreement with Henlius. The two parties will collaborate on the development of ophthalmic indications for HLX04, a bevacizumab biosimilar independently developed and manufactured by Henlius, including wet age-related macular degeneration (wAMD).

Ocunvis, which went public in July 2020, has also entered into a collaboration with Boan Biotech, a subsidiary of Luye Pharma Group, to jointly develop Boan Biotech’s investigational biologic LY09004 in China. Meanwhile, Ocunvis has obtained exclusive rights to promote and commercialize the product in China.

In addition to the market for fundus vascular diseases, dry eye disease is one of the most prevalent ocular conditions in China. According to the "2013 Expert Consensus on Clinical Diagnosis and Treatment Guidelines for Dry Eye," the prevalence of dry eye disease in China ranges from 21% to 30%, with a relatively low consultation rate. The key mechanism underlying dry eye disease at present is ocular surface inflammation, and the primary treatment modality is pharmacological therapy. Artificial tears are commonly used medications, with sodium hyaluronate eye drops, as a common type of artificial tear, achieving annual sales volumes of up to 1 billion units in China.

In the early stages of dry eye disease, progression is primarily managed with artificial tears. When the condition worsens to moderate or severe stages, a combination of artificial tears and anti-inflammatory agents is required; cyclosporine eye drops are currently the most commonly used anti-inflammatory medication. In China, most anti-inflammatory drugs for dry eye disease are either developed as generic versions or introduced through licensing agreements from foreign pharmaceutical companies. In June 2020, Xingqi Eye Pharmaceutical’s Class 3 generic cyclosporine eye drops (II) received marketing approval, becoming the first cyclosporine-based drug approved in China for the anti-inflammatory treatment of dry eye disease.

Due to a shortage of drug types, companies such as Yisheng Biopharma, Grand Pharma, Hengrui Medicine, Zoclar Eye Care, and Weimou Bio are actively advancing the research and development of anti-inflammatory drugs for dry eye disease, with several candidates already entering clinical trials.

In addition, gene therapy has been developing rapidly in the field of ophthalmology in recent years. Due to the unique anatomical structures of the eye, such as transparent refractive media and a relatively closed environment, and because many hereditary eye diseases are associated with genetic mutations, gene therapy is widely recognized as an effective treatment for ocular disorders. Consequently, ophthalmology has gradually become one of the most rapidly advancing indication areas in gene therapy. Currently, domestic companies such as Nuofo Si (Nuofus) and Zhongyin Technology have entered the field of ophthalmic gene drug research and development.

As the first company dedicated to the research and development of gene therapy drugs for ophthalmic diseases, Nuofusi (Visgene) has developed NR082, the first intravitreal injection drug, with Leber’s Hereditary Optic Neuropathy (LHON) as its breakthrough indication. In September 2020, NR082 successfully obtained Orphan Drug Designation from the U.S. FDA. In January of this year, the Center for Drug Evaluation of the National Medical Products Administration (NMPA) accepted Nuofusi’s application for clinical trial registration of NR082.

Indeed, China’s ophthalmic drug industry still faces a scarcity of available medications, leaving substantial unmet clinical needs. However, as numerous domestic pharmaceutical companies intensify their R&D efforts, more breakthrough new drugs and therapies are being developed, which will alleviate the shortage of ophthalmic medications.

Ophthalmic Medical Services: Ophthalmology Chains Race Toward IPOs

The ophthalmic medical services market comprises three major segments: diagnosis and treatment of eye diseases, refractive correction, and medical optometry. Diagnosis and treatment of eye diseases primarily target conditions such as cataracts, glaucoma, and fundus diseases; refractive correction includes various types of laser surgeries; and medical optometry refers to scientifically derived optical prescriptions based on a comprehensive assessment of individual circumstances, distinguishing it from routine refraction performed at standard optical retail stores.

In 2020, China’s ophthalmic medical services sector witnessed significant activity. Three major ophthalmology chain providers—Huaxia Eye Hospital Group, He Eye Specialist Hospital, and Purui Eye Hospital—sequentially submitted their initial public offering (IPO) applications. According to their prospectuses, all three companies had achieved positive net profits in the past two years and met the ChiNext listing requirements of cumulative net profits no less than RMB 50 million. In early 2021, Chaoju Eye Care, another ophthalmology chain provider, also filed for an IPO.

To some extent, ophthalmology bears a strong resemblance to dentistry, with the industry often referring to them as “golden eyes and silver teeth,” suggesting that ophthalmology is a lucrative business. However, according to research reports from Guoyan Securities, the overall revenue levels and profit contributions of ophthalmology departments in public hospitals are relatively low. Moreover, services such as optometry, eyeglass dispensing, and myopia correction surgery fall under consumer healthcare and are not covered by basic medical insurance. Therefore, similar to the dental industry, ophthalmology is well-positioned to establish differentiated competition against public hospitals and has evolved into a highly marketized segment within the consumer healthcare sector.

Top 5 Most-Funded Companies in the Ophthalmology Services Sector (For Publicly Listed Companies, Only Pre-IPO Total Financing Is Counted)

When discussing the ophthalmic medical services market, it is hard not to think of Aier Eye Hospital, the leading chain in the sector. Today, Aier Eye Hospital’s market capitalization has exceeded RMB 300 billion, representing a more than 40-fold increase since its IPO in 2009. Under these circumstances, do other ophthalmic chain institutions still have opportunities?

As the largest segment of the ophthalmology market, the ophthalmic medical services market currently stands at approximately RMB 124 billion. Driven by the rising incidence of eye diseases and increased patient awareness of self-diagnosis, the market is expected to continue expanding in the future. As the industry leader, Aier Eye Hospital holds only about 10% of the market share, indicating substantial growth potential for other ophthalmic chain institutions.

Centralized Procurement of High-Value Consumables May Accelerate Import Substitution

Cataracts are the leading cause of blindness worldwide. According to the World Health Organization, 35% of global blindness and 25% of moderate to severe visual impairment are attributable to untreated cataracts. Currently, the only proven effective treatment for cataracts is intraocular lens (IOL) implantation surgery, making IOLs the most widely used artificial organs and implantable medical devices globally.

On July 31, 2019, the State Council issued the "Reform Plan for the Governance of High-Value Medical Consumables," marking the official commencement of national-level cost containment measures for high-value medical consumables. As a category of high-value medical consumables, intraocular lenses were subsequently included in pilot centralized procurement programs at the local level.

Status of Centralized Procurement for Domestic Intraocular Lenses in Selected Regions (Source: Compiled from Public Information)

Currently, the national coverage of volume-based procurement (VBP) for intraocular lenses across provinces has exceeded 70%. According to overall statistical data, the average price reduction achieved through negotiated procurement programs for intraocular lenses is approximately 34%. In this context, intraocular lenses have emerged as one of the key product categories predicted to be included in future national centralized procurement of high-value medical consumables.

Previously, under the monopoly of imported brands, the advantages of domestic brands were not obvious. However, with the improvement of the technical level of domestic brands, volume-based procurement has highlighted their higher cost-performance advantage, which can bring more market opportunities to domestic brands.

Overall, China’s ophthalmology sector remains a blue-ocean market. In segments such as medical devices and pharmaceuticals, where imported products still command the majority of market share while domestic companies continue to ramp up their efforts, there is substantial room for growth. The ophthalmic medical services segment is also gaining momentum, driven by a wave of initial public offering (IPO) filings by multiple companies. Looking ahead, with advancing technological maturity and supportive policy measures, the ophthalmology industry is poised to sustain rapid growth for the foreseeable future.