Jiang Tianjiao's Interpretation of the Internet Healthcare Chronology: How to Anticipate the Industry's Endgame?

"Reading history makes one wise; learning from the past enables foresight into the future."

Internet healthcare is the sector that VCBeat has tracked and researched for the longest period. Over the past year, spurred by the pandemic, internet healthcare has accelerated its development and once again become the focus of high expectations from various stakeholders. At this juncture, reviewing the developmental history of internet healthcare enables a comprehensive understanding of past extensive trial-and-error processes and a deep grasp of the industry’s underlying logic. It also allows us to empathetically comprehend the strategic evolution and decision-making journeys of industry players in their specific historical contexts, while avoiding cognitive distortions caused by “survivorship bias,” thereby gaining insights into industry trends from a more holistic perspective.

In an industry prone to “frequent outbreaks,” it is even more essential to adhere to “long-termism” and become “friends with time.”

Accordingly, VCBeat has compiled a public speech by Jiang Tianjiao, Dean of the VCBeat Research Institute, titled “Chronicles of Internet Healthcare,” to serve as a reference for industry professionals.

Jiang Tianjiao, current Dean of VCBeat.

Formerly a Senior Analyst covering the Internet and healthcare sectors at Founder Securities Research Institute; member of the first-place teams in the “New Fortune” Best Analyst Awards and the “Crystal Ball” Best Analyst Awards, as well as an individual award recipient; has conducted in-depth research in the fields of internet healthcare and medical services.

Formerly served as a Director in the Industrial Finance Department of Founder Securities, responsible for investment and M&A activities as well as market capitalization management within the healthcare industry;

Concurrently serves as a Distinguished Researcher at the National Internet Institute, a Distinguished Researcher at the Institute of Public Policy of the Chinese Academy of Social Sciences, and a Distinguished Researcher at the School of Social Sciences of Tsinghua University;

Author of the books *Reconstructing Great Health*, *Internet Transformation: Decoding the Chinese Management Model*, and *Internet + Healthcare*.

Jiang Tianjiao

A Chronicle of Internet Healthcare, 2013–2020

“Eight Years of Unwavering Resolve: From Iron-Clad Challenges to Butterfly’s Metamorphosis”

In the blink of an eye, internet healthcare has traversed eight years. Eight is a number rich in symbolism: it marks the year when the arduous War of Resistance Against Japanese Aggression culminated in victory, and it also phonetically echoes “fa” (prosperity) in Chinese culture. Within the context of the internet healthcare industry, we prefer to interpret it as “rising on the strength of accumulated efforts.”

Looking back on the past eight years of internet healthcare, it can be said that the entire industry has progressed through continuous exploration and trial-and-error. The lessons learned and painful setbacks have far outweighed the accumulated experience and achievements. The 2020 pandemic reignited enthusiasm for the development of internet healthcare, prompting a renewed influx of capital and enterprises. At this juncture, conducting a thorough review is critically important.

To this day, even though industry giants such as JD Health, AliHealth, and Ping An Good Doctor have emerged in the capital markets, we cannot definitively conclude that the internet healthcare model has become fixed. The industry is moving into “deep waters.” Regardless of entrepreneurs’ professional backgrounds, regulators’ understanding and support, or the investment directions of capital providers, the internet healthcare sector after 2021 is highly likely to generate new opportunities, with a new generation of industry leaders continuing to emerge.

Below, we invite you to join us on a remarkable eight-year journey through the internet healthcare industry—a path as arduous as iron barriers, yet culminating in a transformative metamorphosis driven by unwavering commitment.

2013—The Tipping Point Approaches: Two Core Logics and a Clear Competitive Landscape

2013 was an era where “disruption” was on everyone’s lips. Internet thinking had largely captured the minds of Chinese entrepreneurs and investors. “Focus, perfection, reputation, and speed” became the secret handshake on Zhongguancun Entrepreneurship Street. At that time, the internet was marching forward triumphantly on its path to “disrupt everything,” and the core strategy for startups was to identify which industries the internet could still penetrate. The healthcare sector, as a “blue ocean,” thus came into the view of capital and entrepreneurs.

Looking back, the rise of internet healthcare in 2013 was indeed inevitable, driven primarily by two macroeconomic logics.

The first logic: From an Internet perspective, digitalization is an inevitable trend in the evolution of various traditional industries. Since 2012, mobile Internet has rapidly permeated diverse sectors, with media, communications, retail, finance, education, and others being successively “disrupted” by the Internet. Can the healthcare industry remain untouched? At that time, the prevailing view within the industry was that since the Internet sector had managed to penetrate these fields, it would inevitably extend its reach into healthcare as part of its evolutionary trajectory.

The healthcare industry boasts a vast market size, yet it has long been plagued by inefficiencies and severe information asymmetry. Isn’t the internet precisely designed to address such inefficiencies and information gaps? Once the internet penetrates the healthcare sector, it will not only facilitate better information matching and enhance efficiency for all stakeholders but also create substantial profit opportunities for itself—making it a rare and valuable opportunity.

The Second Logic: From the perspective of the healthcare industry itself, there has long been an imbalance between supply and demand. With the intensifying aging population, changes in modern lifestyles, and shifts in environmental and dietary factors, public demand for medical and health services has surged, while supply remains extremely limited. Although China trains 600,000 medical students annually, fewer than one-sixth enter clinical practice, and this proportion is still declining. Medical services are not tangible goods; their shortage cannot be addressed through “imports” but only by improving supply-side efficiency. Who will enhance the matching efficiency between supply and demand? Internet healthcare has naturally assumed this critical responsibility.

Driven by two major macroeconomic logics, internet healthcare has ushered in an investment boom in the capital market. However, at this time, there were few industry participants, and the competitive landscape was very clear.

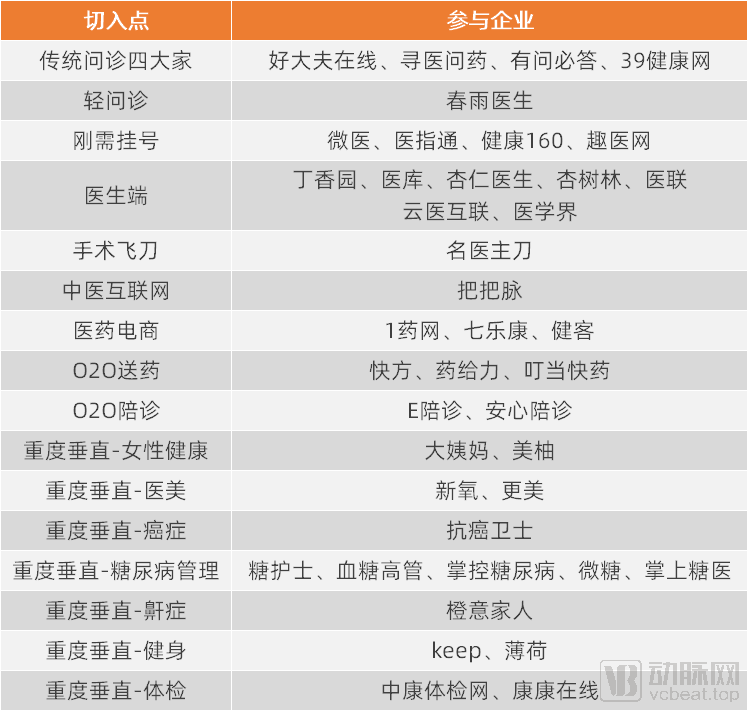

Some Participants in Internet Healthcare in 2013

For example, Haodf Online is distinguished by its roster of physicians from Grade 3A hospitals, Chunyu Doctor by its lightweight consultation services, DXY by its tools for both physicians and patients, Xingshulin primarily by its physician-focused tools, while 39 Health Network and Xunyi Wenyao focus mainly on health information.

Overall, in 2013, the two logical mainlines and the competitive landscape among players were clear. Capital was highly optimistic about the industry, but high-quality projects were scarce, leading to high valuations for individual targets. The industry exhibited a state of “an impending boom,” akin to “the calm before the storm.”

2014: A Hundred Schools of Thought Contend—“Single-Cell Organisms” Emerge Continuously, Species Proliferate, and Ideas Flourish

Looking back at 2014 from the rearview mirror of 2021, one finds that 2014 was a remarkable year. The current leading companies in internet healthcare (or their predecessors) were essentially all founded in 2014.

In 2014, the internet healthcare industry experienced vigorous growth, with a constant emergence of diverse entry points and extensive trial-and-error efforts by various companies. However, an interesting characteristic was that, influenced by the internet philosophy of “focus, perfection, reputation, and speed,” most internet healthcare companies at that time entered the market with a single business model, a phenomenon I liken to the “emergence of unicellular organisms.”

Key Entry Points and Participating Companies in Internet Healthcare in 2014

For example, in the traditional online consultation sector, the dominant players at the time were Haodf Online, Xunyi Wenyao, Youwen Bida, and 39 Health Network, known as the “Big Four” of traditional online consultations. Meanwhile, multiple platforms emerged around appointment registration, a “super essential need,” with both national giants and regional leaders flourishing. At that time, “essential needs” and “high frequency” remained the standard paradigm for understanding the internet within the industry, making appointment registration the most common entry point into internet healthcare. In addition, Chunyu Doctor championed the concept of “lightweight consultations.” This nuanced term helped alleviate, to some extent, the awkward position of “online consultations” being perceived as non-medical.

Not only is Western medicine-based internet healthcare flourishing, but a large number of enterprises have also emerged in the field of Traditional Chinese Medicine (TCM) internet healthcare, with remote pulse diagnosis devices and thermal imaging instruments complementing this trend.

It is not limited to pure online services; the internet healthcare sector cannot afford to miss the major trend of “O2O” (Online-to-Offline). Various models, including O2O medical escort services, O2O medication delivery, and at-home nursing care, have emerged sequentially and all successfully secured financing.

It is worth noting that in 2014, the industry witnessed another significant trend: deep vertical integration. At that time, while working at Founder Securities, I authored an in-depth research report on internet healthcare titled “Deep Vertical Integration: The Closed-Loop Model Reigns Supreme.” So-called deep vertical integration refers to providing end-to-end services covering pre-diagnosis, during-diagnosis, and post-diagnosis stages within a specific disease category or medical specialty. This approach gave rise to various sectors, including women’s health management, medical aesthetics and plastic surgery, oncology, and diabetes management. Due to its characteristics—large market size, strong user stickiness, high frequency, rigid demand, and substantial consumer spending—the diabetes sector attracted considerable capital interest, even leading to an industry phenomenon known as the “Hundred Sugar Apps War,” referring to the emergence of hundreds of diabetes management applications.

In 2014, the term “a hundred schools of thought contend” referred not merely to the emergence of over a hundred startups; it also characterized a period marked by the prolific generation of business ideas. Against the backdrop of fierce industry-wide competition and extensive trial-and-error, a wealth of business concepts emerged, primarily embodied in the “four major debates” surrounding strategic direction within the industry.

The first is the “internal vs. external debate,” namely, the contest between the internet-based model (outside hospitals) and the informatization model (inside hospitals). Should one bypass physical hospitals to conduct out-of-hospital business, or enter hospitals to provide informatization services? This is almost a case of having your cake and eating it too, as the underlying DNA of these two directions is fundamentally different. There was once an internet company in the industry that, after completing an informatization system for a Grade 3A hospital, never managed to make the decision to take on a second one. Meanwhile, informatization vendors’ attempts to develop internet-oriented products often result in only a superficial resemblance, lacking true integration.

The second debate is the “Generalist vs. Specialist” dilemma: whether to opt for a large, comprehensive platform or to pursue a path of deep specialization in specific disease areas. A large, comprehensive platform refers to one that covers as many diseases as possible; heavy verticalization involves building a full-course service chain centered around a specific disease, with intensive deployment within that single disease area. At the time, from a business perspective, the former could cover more diseases and thus attract more users, while the latter often focused on addressing patients’ real needs, thereby generating higher “stickiness.” Both approaches have their merits, but it is difficult to achieve both simultaneously.

The debate between comprehensive platforms and vertical specialists did not arise without cause. In 2014, the fierce competition between Dangdang and JD.com in the book market was startling. Despite Dangdang’s high market share in books, it faced JD.com’s expansion from 3C electronics into a full-category model that included books. JD.com attracted significant traffic by offering books at lower prices. Consequently, Dangdang found itself in a dilemma: lowering prices would lead to losses, while maintaining prices would result in user churn. Clearly, this strategic game had reached an impasse. This episode left a deep impression on entrepreneurs in the internet healthcare sector, giving rise to the “comprehensive vs. vertical” debate. Interestingly, companies that opted for a “deeply vertical” model after this debate have become the current practitioners of the “specialized departments and specific diseases” approach in internet healthcare. In 2020, these companies experienced exceptionally smooth financing rounds.

Third is the “doctor-patient debate,” referring to the contest between physician-facing services and patient-facing services. Should companies focus on the physician side or the patient side? Between doctors and patients, which group constitutes the core resource? This issue was highly contentious at the time. Even now, many companies may still have not clearly identified who their product’s “users” truly are.

Fourth is the “software versus hardware” debate, i.e., the contest between app-based products and wearable devices. In 2014, the smart wearable device market was booming, with participants believing it would become the next-generation intelligent interaction platform and even potentially disrupt smartphones. However, others argued that entering the market via apps was the correct approach, because factors such as high mold costs for hardware made “rapid iteration” unfeasible, whereas rapid iteration was widely regarded in the internet sector as a key to success. Clearly, from today’s perspective, both viewpoints are one-sided. After experiencing their heyday at the time, wearable devices have now been reduced to standalone modules.

2014 was a period of flourishing diversity in internet healthcare, characterized by a multitude of voices and ideas that were rapidly translated into action.

2015: Entering a Frenzy, Baidu Joins In, and Ping An Good Doctor Goes Live

In 2015, the industry entered a phase of “frenzy.” Three indicators reveal that the fervor had pushed internet healthcare, once a blue-ocean market, into a boiling point:

First, while securing substantial financing, many enterprises also embarked on “strategic investments.” Although leading internet healthcare companies had obtained significant funding, they were objectively still in their early stages of development; such capital should have been allocated to expanding operations and exploring through trial and error. Interestingly, however, after receiving large-scale financing, these companies largely established their own strategic investment departments and began making external investments. The phenomenon of startups simultaneously raising funds and investing externally is a classic indicator of industry frenzy.

Second, the capital market applauded, and the industry surged. U.S. internet healthcare companies Teladoc and Fitbit went public one after another, striking a balance between “software” and “hardware.” Teladoc listed in July 2015, and Fitbit in June 2015. These two events greatly stimulated the capital market, reinforcing the belief that both software and hardware hold strong growth prospects.

Third, internet companies that claim to disrupt everything with their “online” models are quietly pursuing “offline” expansion. At that time, enterprises waving the banner of the internet seemed to have coordinated a secret signal, all doing the same thing—exploring offline channels. In December 2015, WeDoctor, Chunyu Doctor, and DXY all began exploring offline clinics. Clearly, a reasonable inference is that most internet healthcare companies encountered bottlenecks in online traffic acquisition, which also reflects the dissipation of traffic resulting from fierce industry competition.

Moreover, two tech giants entered the market in 2015. First, Ping An Good Doctor officially launched its mobile app; second, Baidu leveraged its massive user traffic to enter the internet healthcare sector by addressing the high-demand need for appointment registration. The entry of these industry leaders has injected greater imagination and vitality into the sector.

2016: Industry “Free-for-All,” Evolution of Single-Module Integration, and Policy Cooling

In 2016, single modules within the industry underwent integration and evolution. During this period, 32 internet healthcare companies announced the establishment of internet hospitals. At that time, the distinction between internet healthcare and internet hospitals was not clearly defined within the industry. However, after extensive discussion, a key difference was clarified: internet hospitals are authorized to issue prescriptions, whereas internet healthcare platforms are not necessarily granted this privilege. This constitutes the most significant distinction between the two.

At that time, there were two approaches to internet hospitals. One was exemplified by Alibaba Health, which built internet hospital infrastructure for various hospitals, positioning itself as a platform similar to Tmall, where all internet hospitals could operate by “opening stores” on the platform. The other was WeDoctor’s internet hospital established around the Third People’s Hospital of Tongxiang, Zhejiang Province.

However, that year witnessed a succession of black swan events, leading to a cooling policy environment. In March 2016, Beijing’s health authorities issued a directive prohibiting physicians from collaborating with commercial companies to provide additional appointment slots (jiahao). At the time, many internet healthcare firms relied on such collaborations to attract patients, and this policy effectively severed a critical lifeline for numerous enterprises. Starting in April 2016, the internet healthcare advertising sector was severely impacted by adverse incidents, challenging the industry’s primary revenue model.

On the other hand, the industry began to witness a wave of business closures: in May 2016, the O2O company Yaogeili ceased operations; in July 2016, the O2O company E-Peizhen shut down; and several internet healthcare companies implemented layoffs around the same period...

Therefore, internet healthcare showed signs of peaking and then declining in 2016.

2017: The industry entered a deep freeze, with internet healthcare being the least favored.

In 2017, internet healthcare made progress only in certain areas. For example, in March 2017, the Yinchuan Municipal Government signed agreements with 15 companies, which subsequently obtained licenses for internet hospitals and established operations in Yinchuan. As a result, Yinchuan became the largest hub for the internet hospital industry in China.

This year is widely recognized as the industry’s nadir. A draft for public comment titled “Administrative Measures for Internet-based Diagnosis and Treatment (Trial)” circulated online, stipulating that local health and family planning administrative departments at or above the county level must revoke the approvals previously granted to internet hospitals, cloud hospitals, and network hospitals within 15 days of the measures’ issuance. This development plunged the nascent internet hospital sector into silence, ushering the industry into a deep winter.

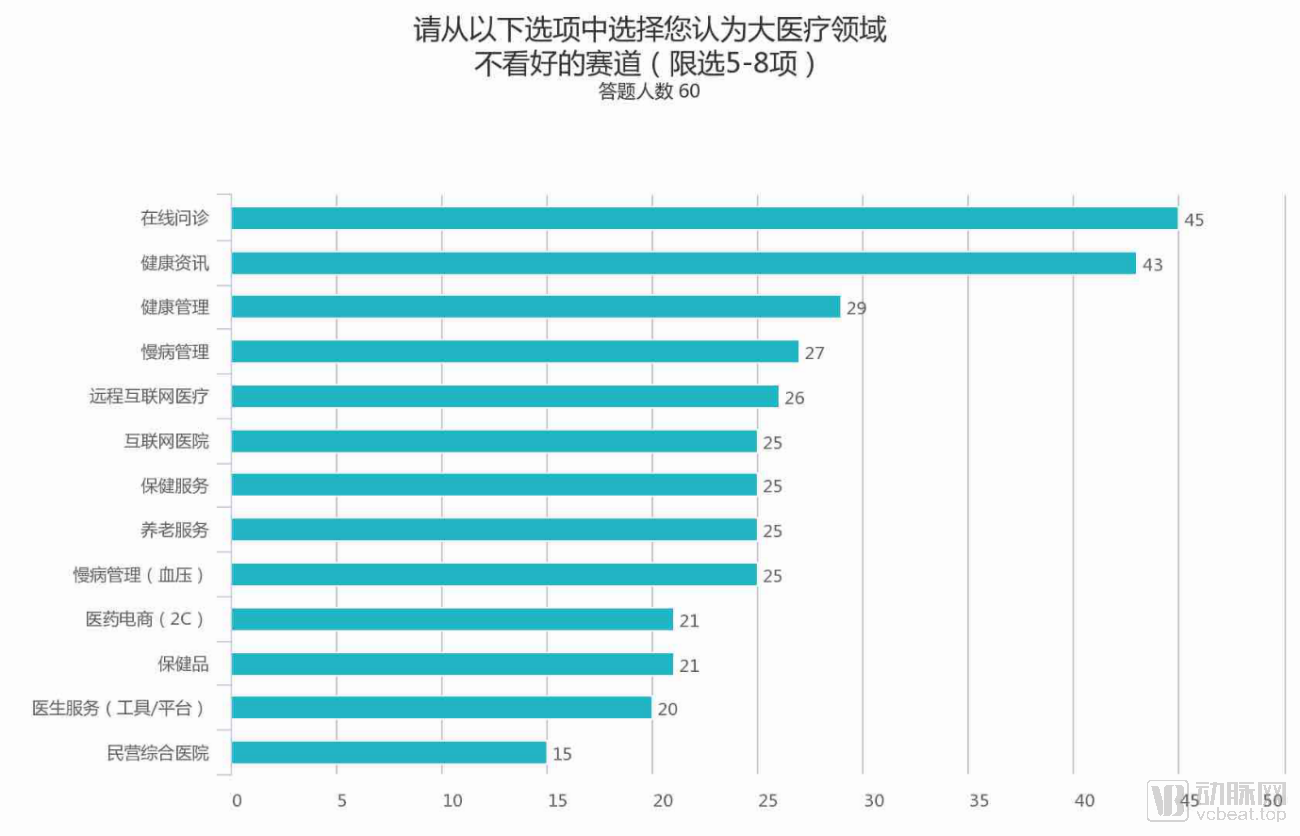

In 2017, a consulting firm conducted a survey at a conference, asking investors present to vote for the most and least promising sectors. Internet healthcare and online consultation were rated as the least promising sectors, with industry sentiment hitting its lowest point.

At that time, buzzwords such as “Friend of Time” and “Long-Termism” had not yet emerged. However, by adhering to “Long-Termism” and becoming a “Friend of Time,” one would likely have recognized that 2017 was the year with the lowest cost for acquiring industry resources in the internet healthcare sector (as competition for patients and physicians had cooled down), making it precisely the optimal moment for internet healthcare companies to launch their aggressive expansion.

The Least Favored Sectors by Investors in 2017

The Least Favored Sectors by Investors in 2017

2018–2019: Industry recovery, dual tailwinds from capital markets and policy, with a solid foundation laid

From 2018 to 2019, the internet healthcare industry gradually recovered.

During this period, internet healthcare companies ushered in a wave of IPOs: Huami Technology, a smart wearable device manufacturer, went public; Ping An Good Doctor listed its shares; and 111 Group, the parent company of 1 Drug Network (Yao Wang), also completed its IPO. Heavily vertical platforms such as BabyTree and So-Young Technology successfully went public as well. These positive developments injected a strong dose of confidence into the capital markets.

Meanwhile, policies related to internet healthcare have received significant attention from the state. In April 2018, the market welcomed major policy benefits, as the "Opinions of the General Office of the State Council on Promoting the Development of 'Internet + Medical Health'" officially recognized the existence of internet healthcare and internet hospitals for the first time. In September 2018, the "Administrative Measures for Internet Hospitals (Trial)," the "Administrative Measures for Internet Diagnosis and Treatment (Trial)," and the "Management Specifications for Remote Medical Services (Trial)" further clarified the regulatory framework for internet hospitals.

The introduction of these policies formally defined online diagnosis and treatment, clarifying that it falls within the scope of medical services, which is a prerequisite for integration with the national medical insurance system. Shortly thereafter, in August 2019, the National Healthcare Security Administration issued the Guiding Opinions on Improving Price Formation and Medical Insurance Payment Policies for “Internet+” Medical Services, announcing that eligible “Internet+” medical services could be included in the medical insurance reimbursement framework, marking this as the most significant policy development to date.

2020: The Pandemic Sparks an Explosion in Internet Healthcare

In 2020, the pandemic spurred another surge in internet healthcare. The primary market saw 16 financing rounds throughout the year (counting platforms that have established their own internet hospitals), with a total financing amount of RMB 16.8 billion, including five rounds exceeding RMB 1 billion each. In December, JD Health went public; based on the public offering price of HKD 70.58 per share, the net proceeds from the global offering amounted to approximately HKD 26.457 billion (approximately RMB 22 billion). According to these statistics, the total industry financing in 2020 reached RMB 38.7 billion.

However, this round of fervor is markedly different from that of 2014 and 2015.

First, internet healthcare has been frequently featured in reports by authoritative media outlets such as CCTV, Xinhua News Agency, and People’s Daily, providing the industry with strong institutional endorsement. Brands like WeDoctor, DXY, and Ping An Good Doctor have become directly associated with this authoritative backing, thereby addressing the long-standing issue of trust in internet healthcare.

Second, public hospitals have been required to launch internet hospital services. Hospital directors have generally undergone training on this new model, gradually recognizing the importance and necessity of internet-based healthcare.

The changes brought by the pandemic to internet healthcare can be interpreted from both short-term and long-term perspectives.

In the short term, there was a surge in demand traffic, as the pandemic fully stimulated users’ demand for online medical services. According to data from the 46th Statistical Report on China’s Internet Development released by the China Internet Network Information Center (CNNIC), the number of online medical service users in China reached 276 million by June 2020, accounting for 29.4% of the total internet user base.

Driven by a surge in demand, collaboration between online multi-platform channels and offline channels has become more seamless, and internet healthcare has gained comprehensive top-down recognition.

At this stage, internet hospitals have become the dominant model. Unlike online consultation services, internet hospitals facilitate follow-up visits and prescription issuance for chronic diseases, constituting formal medical practice. Joint brand endorsements have enhanced the credibility of internet-based healthcare. During this period, industry consolidation has increased significantly; although numerous platforms remain, companies with substantial resources and strong financial backing have gained markedly greater public recognition. Internet healthcare services have been included in medical insurance reimbursement schemes, albeit with limited coverage.

In the long term, internet healthcare has conducted comprehensive market education, helping the public form new medical-seeking habits, such as obtaining doctors’ opinions or prescriptions without physical contact or face-to-face consultations. Meanwhile, increased attention from authorities like the National Health Commission to information technology infrastructure and telemedicine has created incremental opportunities. Hospitals’ recognition of internet hospital platforms has significantly improved, while internet healthcare companies have accelerated product iterations that reflect demand characteristics, facilitating data-driven product optimization. Promotion efforts through hospital channels are also intensifying. In the future, internet healthcare will inevitably achieve extensive coverage under national health insurance schemes, laying a solid foundation for establishing mature and sustainable profit models.

A review of the chronology of internet healthcare clearly reveals that its evolution offers us many insights.

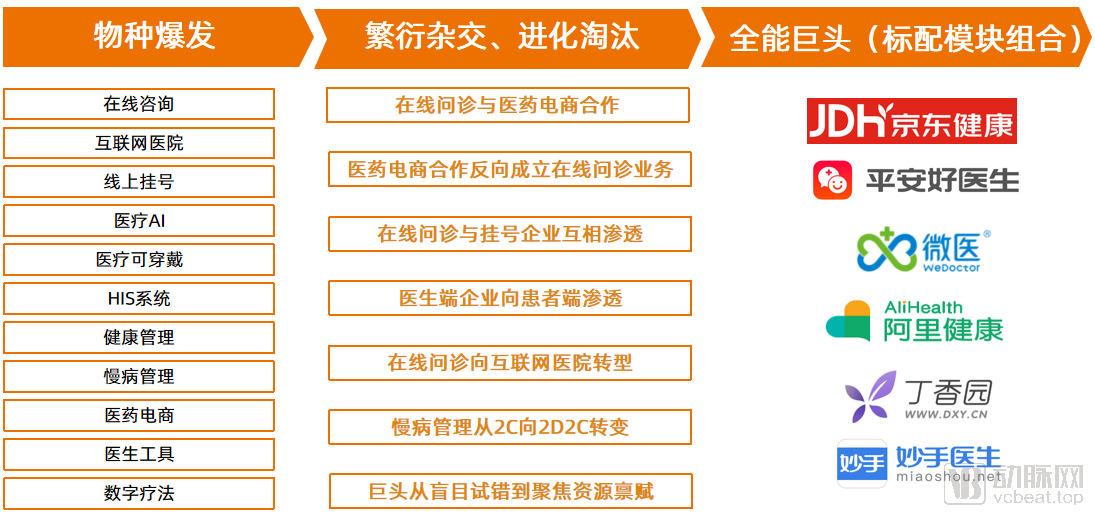

First, the phase of trial-and-error exploration has been completed, with unicellular organisms evolving into multicellular all-encompassing giants. After a series of evolutionary processes following the initial species explosion, these entities have entered stages of reproductive hybridization and evolutionary selection, ultimately forming all-encompassing giants composed of standardized modular combinations. Currently, surviving internet healthcare companies are all implementing chain-based layouts, as there is no viable model based on single-point deployment.

Overview of the Evolution of Internet Healthcare

Overview of the Evolution of Internet Healthcare

For instance, online consultation platforms have partnered with pharmaceutical e-commerce companies, which in turn have expanded into online consultation services. Chronic disease management has gradually shifted from a B2C model to a B2D2C model, and industry giants have moved from blind trial-and-error to focusing on their core resource endowments. As a result, several all-encompassing giants such as JD Health, Ping An Good Doctor, and WeDoctor have emerged, making internet hospitals and pharmaceutical distribution channels standard offerings.

Secondly, the history of the industry is also a history of policy. In fact, all business models in internet healthcare had already been explored before 2017. However, only those enterprises that survived through 2017 and welcomed the favorable policies in 2018 were able to benefit from the subsequent policy dividends. The definition of online medical practices within the policies, as well as the determination of whether online medical services could be covered by medical insurance, were key factors determining the survival and development of the industry or individual enterprises.

Ultimately, the controversies and explorations during the industry’s evolution have generated substantial value. Fortunately, throughout the aforementioned series of evolutionary developments, numerous controversies and explorations emerged, allowing enterprises to engage in extensive trial and error.

For instance, various market entry strategies have been attempted, including targeting physicians, patients, hospitals, or distribution channels. Along the patient service continuum, both single-segment and end-to-end solutions have been explored. In terms of delivery platforms, approaches ranging from software-only and hardware-only to comprehensive software-hardware integration have all been trialed. Regarding disease coverage, both broad, comprehensive models and niche, specialized ones have likewise been implemented.

The greatest value generated by controversy and exploration is the emergence of companies that have endured until policy benefits were realized, as well as the all-around giants we see today.

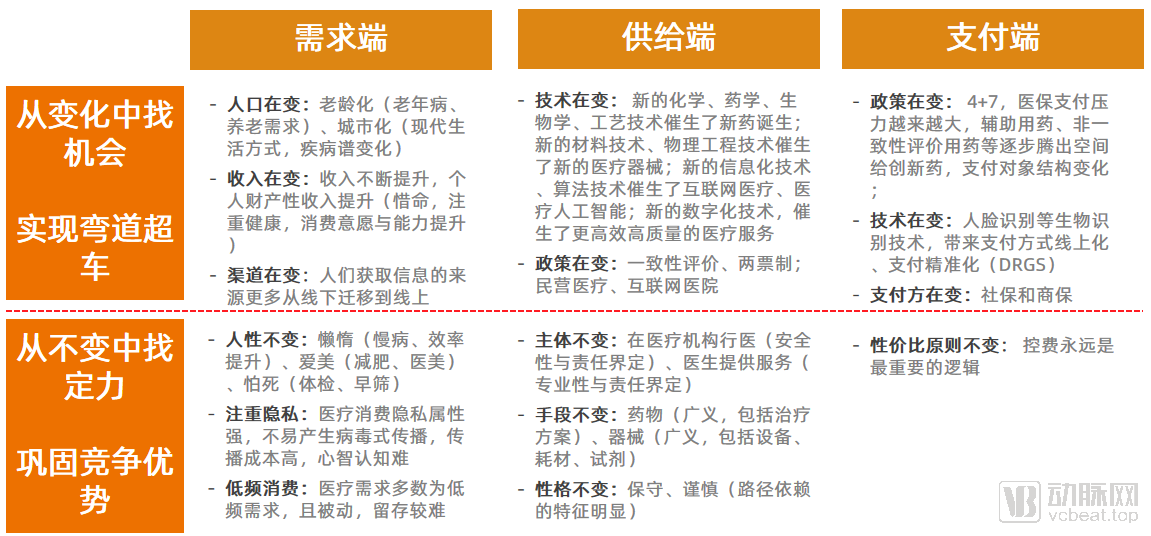

So, what is our prediction for the endgame of internet healthcare? We can analyze it based on the 2-3 model. Whether from the demand side, supply side, or payment side, we must form this mindset: find opportunities in change and find stability in constancy.

The 2-3 Model for Predicting Endgame Trends

The 2-3 Model for Predicting Endgame Trends

Therefore, we believe that the core logic for determining the ultimate model of internet healthcare includes the following aspects:

First, online-driven platforms and offline-driven platforms are likely to coexist in the long term. The foundation of the former lies in the “traffic dividends” from existing major internet platform businesses. Its entry point focuses primarily on common diseases and over-the-counter (OTC) medications, with patient online consultations, medication purchases, and diagnoses/prescriptions via internet hospitals constituting the main revenue streams. Influenced by user perception and economies of scale, online platforms are expected to evolve into an oligopolistic market. The foundation of the latter rests on its reserve of “physician resources,” manifesting as specialized disease- and specialty-specific platforms. Its primary model revolves around prescription refills for chronic diseases and new/specialty drugs, where physicians manage patients, and revenue is mainly generated through internet hospital services combined with medication sales. Due to localized management regulations, offline platforms are highly likely to remain regionally fragmented over the long term. Single-disease platforms may not persist indefinitely, whereas multi-disease integrated platforms will become the mainstream.

Second, as cost containment within the basic medical insurance system will become a pervasive, long-term factor shaping the industry, its crowding-out effect will drive the robust growth of commercial health insurance. Commercial insurance will deeply integrate with internet healthcare across multiple dimensions, including marketing, product design, cost control, underwriting, and claims processing. Traditional commercial insurers, leveraging their strong offline sales heritage, can compensate for the limitations in online conversion rates. Meanwhile, online service delivery and product design will significantly reduce costs. It is foreseeable that China’s payment structure will increasingly resemble that of the United States, with the integration between commercial health insurance and internet healthcare continuing to deepen.

Third, the industry is gradually shifting from exploring “business models” to embracing “professionalism” and “clinical evidence-based practice.” Industry discussions are no longer confined to debating who ultimately bears the costs (“who pays for the wool”), but have begun to focus on how to truly advance from Digital Health to Digital Therapeutics (DTx), enabling apps to play a more significant role from a clinical perspective. International companies such as Pear Therapeutics and Livongo have already set strong examples.

In summary, opportunities always favor those who are prepared. Internet healthcare embodies the fundamental characteristics of the medical industry, requiring a commitment to long-term operations and the cultivation of a strong reputation among both patients and providers. The trials faced during the 2020 pandemic further validated this approach, as several major platforms with years of accumulated experience opened up their consultation interfaces to third parties on a large scale to alleviate urgent demand. Having weathered this challenge, the industry’s future prospects are undoubtedly promising.

In an industry prone to “frequent outbreaks,” it is even more essential to adhere to “long-termism” and become a “friend of time.”