NuoHui Health Rings the Bell at HKEX with Market Cap Surpassing HK$35 Billion: How Loud Was the 'First Ring of the Year of the Ox'?

On February 18, 2021, the seventh day of the first lunar month, New Horizon Health became the first company to list on the Hong Kong Stock Exchange (HKEX) in the Year of the Ox, marking the biopharmaceutical sector’s debut listing for the year. New Horizon Health officially commenced trading on the HKEX with an initial public offering (IPO) price of HK$26.66 per share, raising over HK$2 billion in total.

Image from Tiger Brokers Finance

During the pre-market auction session, the share price of New Horizon Health remained stable at HK$76, representing a 185% increase over the offering price, and maintained this level until the market opened. On its listing day, the stock hit an intraday high of HK$85.9, surging 222.2% above the offering price. At the close, New Horizon Health’s share price stood at HK$84, up 215.08%, with a total market capitalization exceeding HK$35 billion.

Since November 2020, when Changweiqing successfully secured the “first certificate for early screening,” New Horizon Health has been making continuous headlines. Its successful listing now marks the company’s formal entry into a new stage of corporate development.

Over the past few months, we have published multiple articles detailing the regulatory approval journey of Colotect, and promptly provided an in-depth analysis of New Horizon Health’s updated hearing materials. With New Horizon Health’s listing now finalized, there is no need to reiterate the significance of Colotect’s approval for the early screening market, nor to revisit New Horizon Health’s substantial performance surge in the third quarter of 2020. In today’s article, we aim to discuss only one question:Why Is New Horizon Health Valued at HK$35 Billion?

To clarify the answer to this question, the first topic that must be discussed is probablyHow significant is the competitive advantage of New Horizon Health’s flagship product?

New Horizon Health’s mission is “to advance technological innovation and accelerate the adoption of cancer screening technologies in China.” While many companies in China, including publicly listed ones, are developing early cancer screening products, New Horizon Health is the first to focus exclusively on this field and achieve a successful public listing.

Early cancer screening is a lucrative market, and New Horizon Health currently addresses only a segment of it. The company’s objective is clear: to develop user-friendly and accurate early cancer screening products. Consequently, it has opted for stool and urine samples, which are more suitable for home-based testing, rather than the more complex blood tests, mindful of the cautionary tale of Theranos.

New Horizon Health currently offers standalone products for single-cancer screening. While single-cancer tests are more targeted, the early-screening population, primarily composed of healthy individuals, naturally has greater expectations for pan-cancer solutions. However, the development difficulty of pan-cancer early screening products is significantly greater compared to that of single-cancer tests.

The immense development challenges of pan-cancer tests are evident from GRAIL’s trajectory. Since its establishment in 2016, GRAIL has secured four rounds of funding, totaling $1.69 billion. These funds have been entirely dedicated to extensive prospective clinical studies on early pan-cancer screening. In its 2020 IPO prospectus, GRAIL disclosed that its four major prospective clinical trial cohorts had enrolled more than 100,000 participants, with follow-up periods ranging from three to five years. Even so, GRAIL remains in the early stages of research and development; according to its 2020 disclosures, the company planned to launch its first product as a laboratory-developed test (LDT) in 2021.

Simply put, the global pan-cancer early screening company with the largest primary market financing spent five years building a massive cohort of over 100,000 participants before it was ready to offer its services externally. This not only signifies immense technical challenges but also requires substantial capital investment. GRAIL’s annual R&D expenditure ranges from $150 million to $200 million, approximately equivalent to the total amount of financing secured by New Horizon Health in recent years. Although many companies are developing pan-cancer early screening products, few have announced large-scale prospective clinical trials.

When regulatory registration and approval considerations are also taken into account, the path to market for pan-cancer early screening products becomes even more distant. Currently, no pan-cancer screening product has been approved in China. There is a lack of policy guidance on product classification, eligibility criteria for clinical trial participants, and primary endpoints. In the absence of clear regulatory frameworks, pioneers in this field are inevitably prone to encountering detours.

Moreover, pan-cancer testing currently faces a critical challenge. The sensitivity of most pan-cancer testing products is limited; the latest data disclosed by GRAIL’s CCGA study showed a sensitivity of only 55%, which rose to just 67% even among 12 types of highly lethal cancers. In contrast, New Horizon Health’s Colotect Clear achieved a sensitivity of 95.5% in colorectal cancer screening, far exceeding the levels attainable by pan-cancer screening. This single metric alone indicates that, in the field of rectal cancer, the accuracy of pan-cancer screening is unlikely to surpass that of Colotect Clear. Furthermore, Colotect Clear boasts a negative predictive value (NPV) of 99.6%, meaning that only 0.4% of individuals with negative results are false negatives, reflecting a very low miss rate. This data has been a key factor enabling New Horizon Health to secure the “first certification for early cancer screening.”

Therefore, returning to the issue of the early screening market. Although pan-cancer screening products sound very attractive, they are still quite far from being fully rolled out in the domestic market. Even if some products have been launched, their sensitivity for a single type of cancer is currently difficult to match that of New Horizon Health.

In the field of single-cancer early screening, we have explained the differences between Colotect and other fecal colorectal cancer diagnostic products multiple times in previous articles. The Class III medical device certification for Colotect explicitly states that it is “used for screening high-risk populations for colorectal cancer who have poor compliance with colonoscopy,” and does not include a disclaimer such as “cannot serve as the basis for early tumor diagnosis or confirmed diagnosis.” These two statements define the National Medical Products Administration’s (NMPA) recognition of Colotect.

In the field of liquid biopsy, most single-cancer early screening products developed by genetic testing companies currently focus on lung cancer and liver cancer, with few early screening products targeting colorectal cancer.

Pan-cancer early screening products are not yet mature, and liquid biopsy tests targeting single cancer types often overlook colorectal cancer. Among competing products in this space, Changweiqing has already emerged as a standout. It can be said that, assuming the current competitive landscape remains unchanged, Changweiqing is well-positioned to maintain its leading position in the field of early colorectal cancer screening over the next few years.

The only factor capable of hindering the expansion of Changweiqing is market promotion, a reality that New Horizon Health fully recognizes. Consequently, New Horizon Health is gradually expanding its sales team to a scale of 1,000 personnel, with a particular focus on promoting the product in clinical settings. This initiative aims to educate more physicians about the advantages of Changweiqing, thereby providing a non-invasive alternative for patients who decline colonoscopy. Meanwhile, New Horizon Health is actively pursuing external collaborations, partnering with various end-channel stakeholders—including health examination centers, insurance providers, internet healthcare platforms, and retail pharmacies—to promote its products.

Current products represent the short-term value of New Horizon Health; to assess its long-term value, an analysis of its pipeline is required.

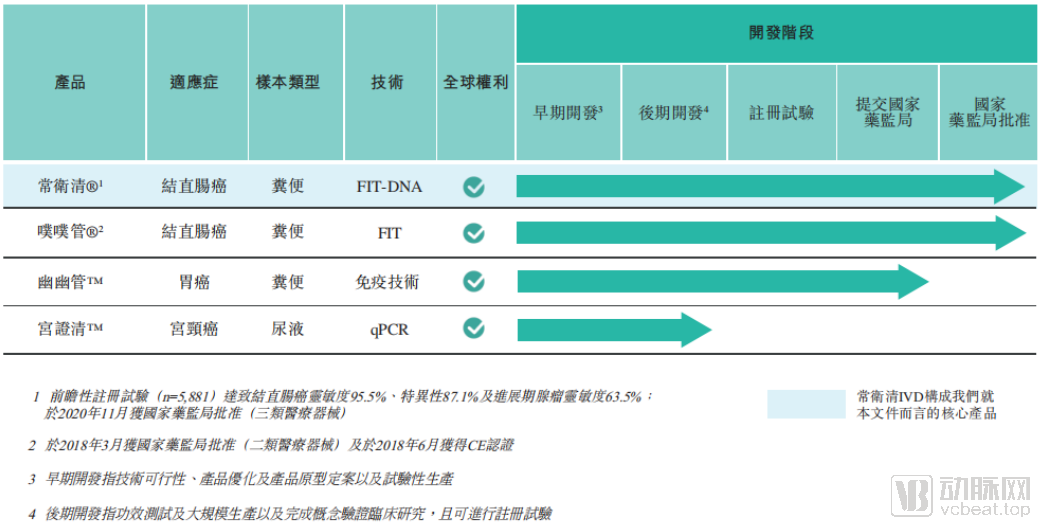

New Horizon Health Product Pipeline

New Horizon Health’s pipeline appears deceptively simple, yet its four product lines actually cover the three major high-risk cancers detectable via stool and urine samples. Two products that have already completed regulatory submission—ColoClear and PP Tube—target colorectal cancer; YouYou Tube, which has just completed clinical trials and submitted for registration, targets gastric cancer; and CerviClear, currently preparing to initiate registration-enabling clinical trials, targets cervical cancer.

We have heard too much about the stories of Colotect and Pupu Tube. Therefore, we now shift our focus to two other products: Youyou Tube and Gongzhengqing. After completing registration and certification in the future, these two products will, together with Colotect, form New Horizon Health’s comprehensive early screening product portfolio.

Youyou Tube: A Non-Invasive Option for Gastric Cancer Screening

According to the updates in New Horizon Health’s post-hearing information package, its stool-based self-test product for gastric cancer screening, Youyou Tube, completed registration clinical trials in November 2020 and submitted a registration application to the National Medical Products Administration (NMPA) in the same month.

Gastric cancer has now become the second most common cancer in China, with 455,800 newly diagnosed cases reported in 2019. It is also the third leading cause of cancer-related mortality in the country, accounting for 327,800 deaths in 2019. According to a report by Frost & Sullivan, the gastric cancer screening market in China grew from RMB 1 billion in 2015 to RMB 2.1 billion in 2019, and is projected to reach RMB 15.7 billion by 2030, at a compound annual growth rate (CAGR) of 20.3%.

In gastric cancer screening, the currently predominant methods include endoscopy-based imaging techniques, while Helicobacter pylori (H. pylori) infection status serves as a crucial tool for early detection. H. pylori is a major pathogen implicated in gastric cancer. Infection with this bacterium induces chronic inflammation and significantly elevates the risk of developing duodenal and gastric ulcers, as well as gastric cancer.

Currently, there are two main clinical methods for detecting Helicobacter pylori. One involves obtaining gastric mucosal tissue via gastroscopy to perform a rapid urease test (RUT), which is an invasive procedure. While the accuracy of invasive testing is unquestionable, its drawbacks are also evident: it offers a poor patient experience and can easily compromise adherence among patients requiring long-term screening.

Another option is the non-invasive urea breath test (UBT), which utilizes C13/C14 isotopes for detection. Although UBT demonstrates high accuracy, the use of isotopes presents certain limitations: on one hand, it is not suitable for specific populations, such as pregnant women and children; on the other hand, the potential for radioactive contamination associated with C14 isotopes poses concerns that hinder its widespread application as a screening method.

Therefore, in recent years, with the maturation of antibody detection technologies, immunological fecal testing has emerged as a new non-invasive method for Helicobacter pylori detection.

The method used by Youyou Tube is to detect Helicobacter pylori in feces using the double-antibody sandwich technique.During testing, simply place the sample into the sample well. If Helicobacter pylori is present in the sample, a red line will appear in the test line region, indicating a positive result. Compared with the Rapid Urease Test (RUT) and Urea Breath Test (UBT), Youyou Guan offers advantages not only in safety and compliance but also enables users to perform the test at home and obtain results within minutes, providing convenience and speed.

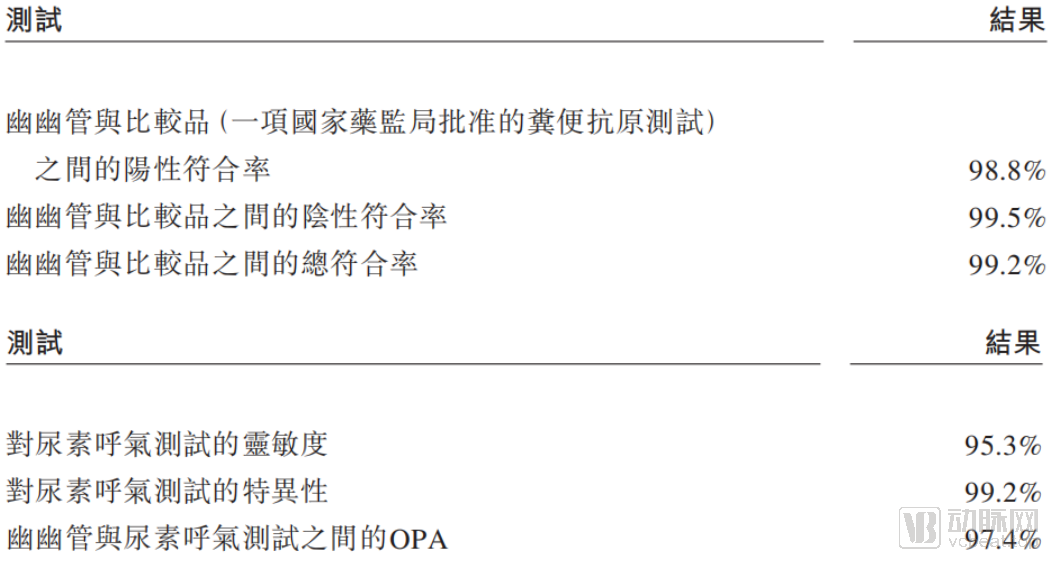

New Horizon Health disclosed partial clinical trial data for its Youyou Tube in the latest post-hearing information package. This registration clinical trial, with Beijing Shougang Hospital as the primary research institution, enrolled over 1,000 subjects who met the predefined recruitment criteria, comparing the Youyou Tube against previously approved fecal antigen tests and urea breath tests.

Partial Data Disclosure for Youyou Tube

Based on the clinical trial results, Youyouguan demonstrated a positive agreement rate of 98.8% and a negative agreement rate of 99.5% compared to the comparator product, indicating extremely high concordance. Furthermore, in comparison with the urea breath test, it achieved a sensitivity of 95.3% and a specificity of 99.2%. It should be noted that these data are preliminary; the final disclosed data may be subject to adjustment in accordance with further instructions from the National Medical Products Administration (NMPA).However, based solely on the current data disclosures, Youyou Tube demonstrates high concordance with both the comparator and the urea breath test, indicating highly promising prospects for its future application.

Gong Zheng Qing: Safe HPV Testing

Following the regulatory registration of Youyou Guan, New Horizon Health’s R&D team has already embarked on its third core project: Gongzhengqing, targeting cervical cancer.

The primary pathogen causing cervical cancer is HPV, a fact that has become widely known to the public amid the extensive HPV vaccine awareness campaigns of the past two years. Although HPV vaccines have been on the market for several years, universal vaccination coverage has not yet been achieved due to constraints such as age restrictions for eligibility, vaccine efficacy, pricing, and supply shortages. Currently, the main methods for cervical cancer screening are the Pap smear administered in hospitals and self-sampling kits used for at-home testing. In hospital settings, trained healthcare professionals perform the sampling, minimizing the risk of procedural errors. However, during self-sampling, improper technique by users may cause pain or even bleeding.

The greatest advantage of Gongzhengqing is the safety of its urine-based testing. Given that no urine-based HPV detection products have yet been approved in China, and there are currently no public disclosures regarding similar competing products, Gongzhengqing, currently offered under the Laboratory Developed Test (LDT) model, already holds a leading market position. Upon completion of future registration and certification, Gongzhengqing’s credibility is poised to increase significantly, providing a novel screening method for cervical cancer among women.

As disclosed in the prospectus of New Horizon Health, the registration clinical trial for GongZhengQing is expected to be launched before the fourth quarter of 2021. The plan is to recruit approximately 30,000 female subjects who meet the criteria for cervical cancer screening, and to accumulate sufficient data through a multi-year follow-up period to demonstrate the clinical safety and efficacy of GongZhengQing.

With significant short-term value and a robust long-term product pipeline, the third major factor influencing New Horizon Health’s valuation falls to its financial performance.

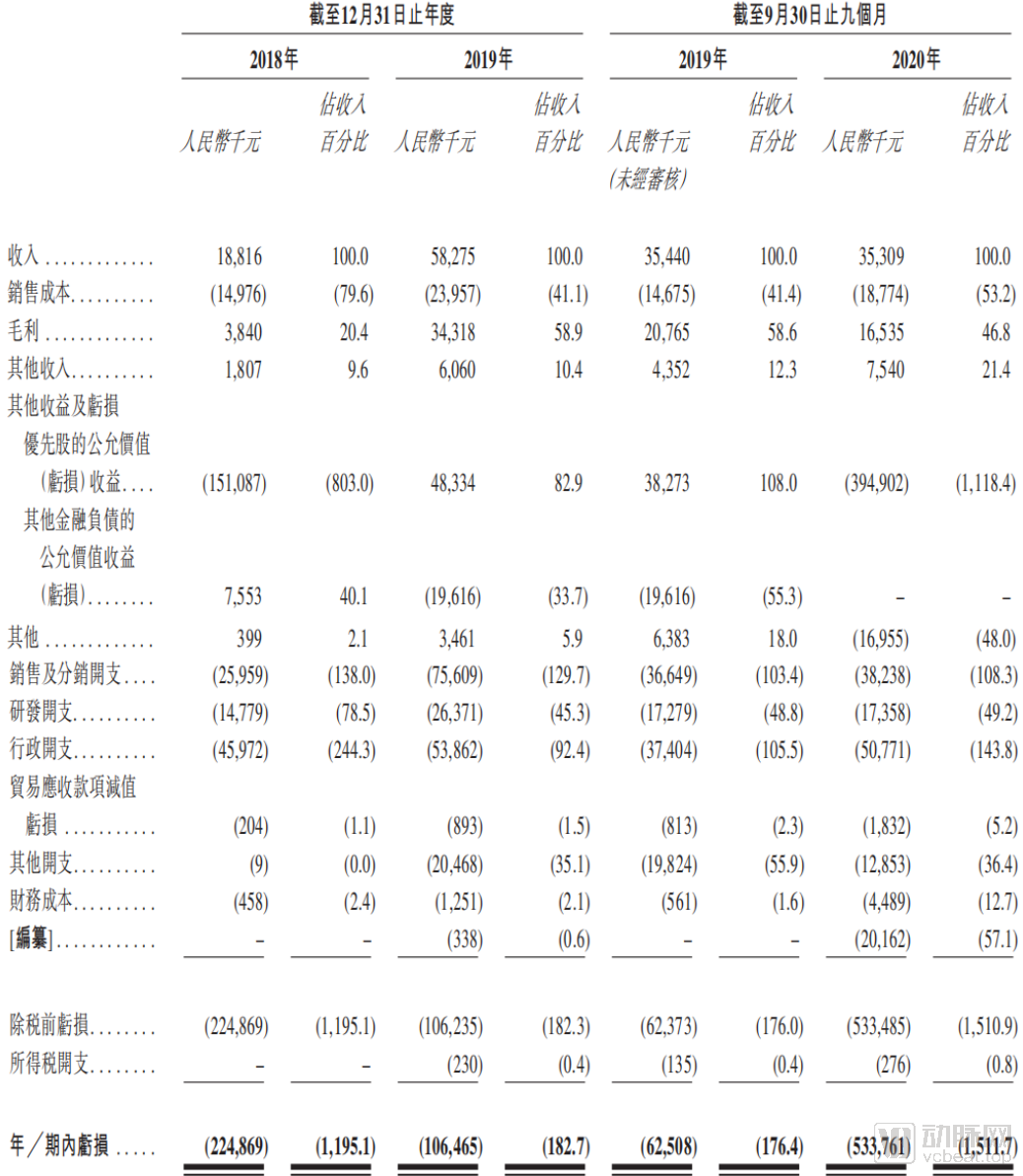

In the latest updated post-hearing information pack, the relevant financial data for the third quarter of 2020 has been incorporated into the summary tables, enabling New Horizon Health’s financial disclosures to more accurately reflect its actual operational performance.

Selected Financial Data of New Horizon Health

In terms of revenue, New Horizon Health experienced a significant surge in 2019, with the majority of its revenue derived from market sales of Changweiqing in the second half of the year. In the first half of 2020, the company, which relies primarily on offline channels such as hospitals and health examination centers, was severely impacted by the pandemic; however, it witnessed a notable recovery in the second half of 2020. A comparison between the initial application version and the post-hearing information package reveals that New Horizon Health’s revenue in the first half of 2020 had just exceeded RMB 10 million, while it surpassed RMB 35 million in the first nine months of 2020.

Given the higher sales revenue in the second half of 2020, New Horizon Health’s full-year revenue for 2020 may surpass that of 2019.

Considering further that the approval of its Class III medical device certificate has opened up channels for hospital entry and consumer-end promotion, New Horizon Health’s revenue expectations for 2021 remain highly promising.

The largest apparent loss actually stems primarily from RMB 482 million in “other gains and losses.” This loss is mainly attributable to changes in fair value arising from financing activities, rather than operational losses. Excluding this component, the actual operational loss is relatively modest.

Sales and R&D expenses are currently the primary sources of operating losses for New Horizon Health. The early cancer screening market is highly competitive; although New Horizon Health has received approval from the National Medical Products Administration (NMPA), it is now in a critical promotional phase following recent product approvals, making substantial investment in sales and distribution unavoidable. On the R&D front, New Horizon Health’s main expenditures are directed toward conducting several registration clinical trials, such as the Clear-C trial for Changweiqing and the registration trial for Youyouguan. With the initiation of the registration clinical trial application for Gongzhengqing in 2021, New Horizon Health’s R&D spending is likely to remain at an elevated level.

Pre-IPO Financing of New Horizon Health

Losses are difficult to avoid, but New Horizon Health has accumulated sufficient funds to address future risks. Since its inception in 2016, New Horizon Health has completed five rounds of financing, raising a total of approximately $150 million. Investors include several well-known domestic investment firms such as Legend Capital, Qiming Venture Partners, SoftBank China, DP Group, and Sherpa Investments.

Junlian Capital Managing Directors Wang Junfeng and Zhou QuanIn a statement to VCBeat, congratulations were extended to New Horizon Health: “As the company’s earliest and largest institutional investor, we are honored to have participated in and witnessed New Horizon Health’s journey from a startup with no finalized products to its current position as an industry leader. Chairman Chen Yiyou is a successful serial entrepreneur who embodies both scientific expertise and entrepreneurial acumen, while CEO Zhu Yeqing brings extensive experience in corporate management. Over years of investment collaboration, we have built a deep bond with the New Horizon team. Facts have validated the determination of Mr. Chen and Mr. Zhu in leading the team toward the company’s development goals. Their unwavering commitment to R&D, bold innovation, and ability to overcome significant challenges during the clinical phase of the Changweiqing product have shaped New Horizon into what it is today. We believe that following its IPO, New Horizon Health will further expand its early screening and diagnosis offerings for other cancer types, thereby further consolidating its leadership position in the industry.”

Cai Daqing, Founding Partner of Sherpa Capital“Congratulations to New Horizon Health! This also marks our first portfolio company to go public in the Year of the Ox. We have known New Horizon for many years, partnering with them since their Series A financing. We have always admired the determination and courage of Dr. Chen Yiyou and Dr. Zhu Yeqing in founding and scaling New Horizon. The successful acquisition of the ‘first approval for cancer early screening’ by Changweiqing is a testament to New Horizon Health’s years of dedicated efforts and represents a major milestone in China’s early screening market. We wish New Horizon Health continued growth and success as it remains deeply rooted in the early screening sector in its next phase of development!”

With strong support from numerous institutional investors, as of June 2020, New Horizon Health maintained total current assets of RMB 534 million, while its current liabilities amounted to only approximately RMB 92.73 million. Although the non-current liabilities of RMB 1.443 billion appear high, RMB 1.377 billion of this figure stems from preferred shares, with only about RMB 67 million arising from actual obligations such as bank borrowings and lease liabilities. Consequently, New Horizon Health’s actual asset-liability ratio is very low. Even excluding the funds raised from this IPO, its substantial cash reserves ensure that the company faces no short-term financial risks.

With favorable market conditions for its flagship products, continuous follow-up on subsequent products, and steady improvement in operational performance, New Horizon Health’s next strategic step is clear: by proceeding steadily and prudently, it has the capability to achieve success while maintaining stability. Indeed, New Horizon Health has chosen a prudent development path for its future plans.

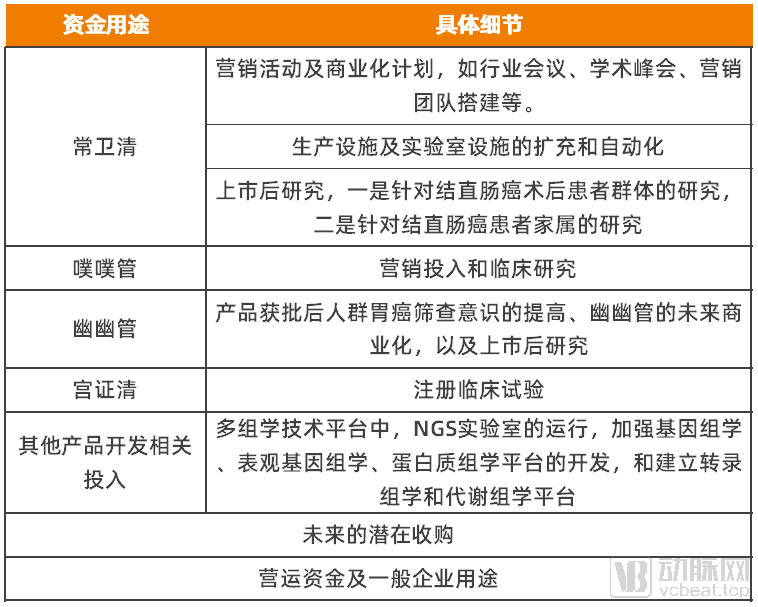

Primary Uses of Funds Raised in New Horizon Health's IPO

New Horizon Health will allocate the more than HK$2 billion raised from its listing to various purposes. The funds will be primarily used for product development and marketing promotion, with the remainder designated for potential future acquisitions and general corporate purposes.

Currently, New Horizon Health has not disclosed the allocation ratios of funds in the latest updated post-hearing information package. However, based on the company’s relevant descriptions, Changweiqing is undoubtedly the absolute core focus of New Horizon Health’s R&D and promotional efforts and will receive substantial funding. The other three products will have resources allocated appropriately according to their respective R&D progress to ensure steady advancement in their development and sales.

Following our analysis, New Horizon Health has fully demonstrated all the essential elements required to support its HK$35 billion market capitalization, at least in the disclosure of information post-hearing. This combination of factors was not achieved overnight but stems from New Horizon Health’s pragmatic and steady approach, as well as its unwavering commitment. The company’s listing marks a significant milestone for New Horizon Health and serves as the starting gun for the early screening market. As the frontrunner, New Horizon Health has already begun its charge, while the fierce competition for this trillion-dollar market is just beginning.